lcd panel demand brands

Well, I have a strong demand for a 32" 4K120+Hz OLED with VRR under 700$. Unfortunazely it does noz exist yet. Until then, I"m good with my 1440p144Hz VA... for 400$...

edit: since i replaced my CRT monitor where i had brightness knob and could turn black image into real invisible black I hated LCD so much because of this vomit gray shit glow black and i hate it so much to this day. i was thinking about LGs but burn in was way to common. if there was any availability of QD-OLEDs I would already had it. But in my country we have basically 2 sellers and they probably even don"t know QD-OLED exists and not even trying to get some inventory. other option is ebay but scalpers have it for 140% and shipping costs are 1/4 price of the product. i pray for the day i dont need to see vomit on my screen

LCD is basically dead unless they use the LCD Dual layering for monitors. I think there"s only been 1 TV by TCL that came out with the tech. I think its bad for TVs but could work for gaming monitors.

The global TFT-LCD display panel market attained a value of USD 148.3 billion in 2022. It is expected to grow further in the forecast period of 2023-2028 with a CAGR of 4.9% and is projected to reach a value of USD 197.6 billion by 2028.

The current global TFT-LCD display panel market is driven by the increasing demand for flat panel TVs, good quality smartphones, tablets, and vehicle monitoring systems along with the growing gaming industry. The global display market is dominated by the flat panel display with TFT-LCD display panel being the most popular flat panel type and is being driven by strong demand from emerging economies, especially those in Asia Pacific like India, China, Korea, and Taiwan, among others. The rising demand for consumer electronics like LCD TVs, PCs, laptops, SLR cameras, navigation equipment and others have been aiding the growth of the industry.

TFT-LCD display panel is a type of liquid crystal display where each pixel is attached to a thin film transistor. Since the early 2000s, all LCD computer screens are TFT as they have a better response time and improved colour quality. With favourable properties like being light weight, slim, high in resolution and low in power consumption, they are in high demand in almost all sectors where displays are needed. Even with their larger dimensions, TFT-LCD display panel are more feasible as they can be viewed from a wider angle, are not susceptible to reflection and are lighter weight than traditional CRT TVs.

The global TFT-LCD display panel market is being driven by the growing household demand for average and large-sized flat panel TVs as well as a growing demand for slim, high-resolution smart phones with large screens. The rising demand for portable and small-sized tablets in the educational and commercial sectors has also been aiding the TFT-LCD display panel market growth. Increasing demand for automotive displays, a growing gaming industry and the emerging popularity of 3D cinema, are all major drivers for the market. Despite the concerns about an over-supply in the market, the shipments of large TFT-LCD display panel again rose in 2020.

North America is the largest market for TFT-LCD display panel, with over one-third of the global share. It is followed closely by the Asia-Pacific region, where countries like India, China, Korea, and Taiwan are significant emerging market for TFT-LCD display panels. China and India are among the fastest growing markets in the region. The growth of the demand in these regions have been assisted by the growth in their economy, a rise in disposable incomes and an increasing demand for consumer electronics.

The report gives a detailed analysis of the following key players in the global TFT-LCD display panel Market, covering their competitive landscape, capacity, and latest developments like mergers, acquisitions, and investments, expansions of capacity, and plant turnarounds:

Prior to the Covid-19 pandemic outbreak in early 2020, the flat-panel display (FPD) market was gloomy. Oversupply, falling prices and losses were the common themes in the market.

It’s been a different story during the outbreak. In 2020, the FPD market rebounded. In the stay-at-home economy, consumers went on a buying spree for monitors, PCs, tablets and TVs. As a result, demand for displays exploded. And shortages soon surfaced for display driver ICs and other components.

Cars, industrial equipment, PCs, smartphones and other products all incorporate flat-panel displays in one form or another. The majority of TV screens are based on liquid-crystal displays (LCDs). TVs use other display types, such as organic light-emitting diodes (OLEDs) and quantum dots.

Smartphone displays are based on LCDs and OLEDs. Other display technologies, such as microLEDs and miniLEDs, are in the works. Flat-panel displays are made in giant fabs. Suppliers from China, Korea and Taiwan dominate the display market.

It’s been a roller coaster ride in the arena. “Before Covid, the FPD market in the second half of 2019 was not very pretty,” said Ross Young, CEO of Display Supply Chain Consultants (DSCC), in a presentation at Display Week 2021. “We had declining revenues, declining prices, declining margins, companies announcing their exit in the LCD market, CapEx was falling, and there was little interest from investors.”

Basically, demand for computers, TVs and other products were sluggish. Plus, there was too much display manufacturing capacity. So product prices fell and many suppliers were swimming in red ink. Driven by higher-margin OLEDs, the smartphone display market was slightly better.

The result? “From a demand standpoint, Covid-19 led to strong demand from the IT market. The education market saw very robust demand. Students and teachers needed more home computers, and schools accelerated their IT investments. Workers made home PCs a priority. There are also millions of workers that went from jobs not requiring a PC to jobs requiring a home PC,” he said.

Demand for PCs, TVs and other products fueled renewed growth for displays. In total, the flat-panel display market reached $118 billion in 2020, up 6% over 2019, according to DSCC. That’s above the previous 2% growth forecast.

The numbers include LCDs, OLEDs and other displays. Of those figures, the LCD market reached $84 billion, while OLEDs were $33 billion in 2020, according to DSCC.

Then, the market is projected to hit a record $152 billion in 2021, up 29% over 2020, according to the firm. Of those figures, the LCD market is expected to reach $113 billion, while OLEDs are $39 billion, they said.

Average selling prices are up, but the market is still beset with component shortages. “Panel prices have risen significantly, particularly since August of last year. They’ve more than doubled in some cases,” Young said. “Adding to the pricing pressure have been components shortages in driver ICs, touch controllers, glass substrates compensation film, polarizers and other materials. We do expect prices to peak in Q3 (of 2021) as a result of shortages easing and the impact of double booking, leaving some potential air pockets in demand. We expect panel pricing to fall in the fourth quarter, but we’re not expecting sharp downturns, as in the past, due to slower supply growth.”

Going forward, the market may come back down to earth. “After 29% growth in 2021, the FPD market is expected to fall by 5% in 2022, as shortage concerns ease, supply growth outpaces demand growth, and prices fall. We expect the IT markets to decline. TV revenues will fall significantly on lower prices, but still slower price declines than in previous downturns,” he said.

According to the latest report by IMARC Group, titled "TFT LCD Panel Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2021-2026,"the global TFT LCD panel marketreached a value of US$ 150.2 Billion in 2020. Looking forward, IMARC Group expects the market to reach a value of US$ 196.7 Billion by 2026. A thin-film-transistor liquid-crystal display (TFT LCD) panel is a liquid crystal display that is generally attached to a thin film transistor. It is an energy-efficient product variant that offers a superior quality viewing experience without straining the eye. Additionally, it is lightweight, less prone to reflection and provides a wider viewing angle and sharp images. Consequently, it is generally utilized in the manufacturing of numerous electronic and handheld devices. Some of the commonly available TFT LCD panels in the market include twisted nematic, in-plane switching, advanced fringe field switching, patterned vertical alignment and an advanced super view.

The global market is primarily driven by continual technological advancements in the display technology. This is supported by the introduction of plasma enhanced chemical vapor deposition (PECVD) technology to manufacture TFT panels that offers uniform thickness and cracking resistance to the product. Along with this, the widespread adoption of the TFT LCD panels in the production of automobiles dashboards that provide high resolution and reliability to the driver is gaining prominence across the globe. Furthermore, the increasing demand for compact-sized display panels and 4K television variants are contributing to the market growth. Moreover, the rising penetration of electronic devices, such as smartphones, tablets and laptops among the masses, is creating a positive outlook for the market. Other factors, including inflating disposable incomes of the masses, changing lifestyle patterns, and increasing investments in research and development (R&D) activities, are further projected to drive the market growth.

Key Market Segmentation:On the basis of the size, the market has been bifurcated into large size TFT-LCD display panel and medium and small size TFT-LCD display panel. The large size TFT-LCD display panel presently represents the leading market segment.

According to TrendForce research, terminal demand remains weak due to repercussions of the Russian-Ukrainian war, rising inflation, and China"s pandemic lockdowns as monitor brands began to reduce purchasing of LCD monitor panels in 2Q22. LCD monitors panel shipments in 2Q22 are estimated at 42.5 million units, down 11.3% QoQ.

According to TrendForce analysis, monitor brands set fairly high shipment targets in early 2022. Coupled with the impact of LCD monitor panel shortages in 2021, monitor brands gravitated towards overbuying panels in 1Q22 to prepare for ensuing shipments. Driven by strong demand from monitor brands, shipments of LCD monitor panels reached 47.9 million units in 1Q22, up 20% YoY, the highest level for the period since 2012.

However, due to changes in the international political and economic landscape in February this year, the market for consumer models has cooled and monitor brands have successively revised their LCD monitor shipment targets downward and simultaneously lowered their panel purchase volumes. In the face of interest rate hikes by the world"s major central banks and slowing economic growth, companies have also begun exercising caution in terms of capital expenditures, which has slowed demand for business-grade LCD monitors. In the past, inventory issues emerged and the overall market became oversupplied when monitor brands overstocked as consumer and business demand gradually cooled.

In addition, shipping and port congestion gradually eased in 1H22. The LCD monitors that were still in transit and accumulating in ports gradually arrived at distributors, resulting in a sharp rise in distribution inventory. Faced with the dual pressure of high whole LCD monitor and panel inventory, monitor brands were forced to reduce panel purchases in 2H22. Therefore, TrendForce forecasts that LCD monitor panel shipments will continue to decline to 37.8 million units in 3Q22, representing a QoQ decline of 11.2%. In 4Q22, there is a chance shipments will rebound marginally to 38.8 million units due to the sales surge initiated by monitor brands at the end of the year, representing a quarterly increase of 2.8%. Annual shipments are forecast to reach 167 million units, a drop of 3.6% YoY.

Moving into 2H22, terminal brands continue to adjust their inventory, not only weakening panel demand, but also inducing a sustained drop in panel quotations. The sharp increase in operating pressure affecting panel manufacturers has forced the display industry to restrain production. According to TrendForce"s "Monthly Panel Supplier Utilization Report," utilization rate (calculated by the volume of glass input) in 3Q22 is expected to fall to 70%, a substantial decrease of nearly 7.3 percentage points from 2Q22.

TrendForce indicates, border controls and lockdowns have led to a disruption of logistics and labor due to the impact of the pandemic in the past two years. In order to avoid production and shipment gridlock, branded manufacturers overstocked from distribution channels to components. However, as logistics and transportation conditions have improved, previously prepared materials have subsequently arrived in relevant warehouses or ports. As pandemic induced demand subsides, terminal sales have suffered due to rising global inflation and the Russian-Ukrainian war. As a result, the inventory problem continues to deteriorate and all aspects of the overall supply chain has entered red alert.

Since this type of situation applied not only to a single application, utilization rate is reduced whether it is Gen5, primarily used in producing laptops, or large-size LCD monitors and TVs. None of the large generational fabs were spared. TrendForce indicates that the utilization rate of Gen5 to Gen7.5 is expected to decrease by 7.7% percentage points to 63.7% and the utilization rate of Gen8 to Gen10.5 will decrease by 7 percentage points to 75% in 3Q22. More than 90% of the Gen10.5 utilization rate used to produce TVs is expected to drop by 17.8 percentage points QoQ, which also highlights the continuing pessimistic demand for TV panels in 3Q22.

As far as panel makers are concerned, depreciation and amortization pressure on Chinese panel makers is more severe than that of other panel makers due to the construction of new factories. In addition, looking at total shipments of larger-sized applications (TVs, monitor panels, and notebooks), Chinese panel makers account for more than half the market, so when the bottom drops out, impact on these companies will be greater than on competitors. Looking at the three leading Chinese panel manufacturers, although BOE’s capacity allocation is very flexible, a drop of 4 percentage points in overall utilization rate cannot be ruled out in 3Q22. At the same time, China Star Optoelectronics (CSOT) and Huike Optoelectronics (HKC) will not only readjust their older factories in 3Q22 but also slow the rate at which new factories ramp up. The overall operating watermark of these two panel manufacturers is estimated to decrease by 13.3 and 7.4 percentage points, respectively.

Although the pressure of depreciation and amortization on Taiwanese manufacturer AUO is small, in response to changes in market demand, the company had already started production adjustment in 2Q22. It is expected to continue implementing this strategy in 3Q22 with overall utilization rate falling to 50%. On the other hand, Innolux expects overall utilization to drop by 6.7 percentage points QoQ. Japanese panel manufacturer Sharp is at a relative disadvantage in terms of overhead, and its customer concentration is too high. Its major branded clients have canceled orders, allowing inventory to stack up quickly. Therefore, Sharp has only just announced that it will begin to aggressively scale-down in its Japanese production line in July. In turn, the company’s overall utilization rate decreased by 26.3 percentage points to 59.3% in 3Q22. LG Display, a Korean panel maker, is expected to maintain a similar operating level as in 2Q22 after a sustained contraction in LCD production capacity due to a strategic shift.

TrendForce indicates, if panel makers do not wish to face the risk of high inventories at the beginning of 2023, they should maintain reduced operations in 4Q22 in order to eliminate existing panel inventory. Therefore, it cannot be ruled out that the utilization rate of LCD Gen5 (including) and above large generational fabs will maintain the same level of operation as in 3Q22. In the past, production cuts were the main response whenever the market was oversupplied. However, with future production capacity still growing, the speed at which brands deplete their inventories and global political and economic trends will be key factors affecting the future display market. If market conditions continue to deteriorate, it cannot be ruled out that the industry will face another reshuffle, setting off a further wave of mergers and acquisitions.

Among the world famous brands, the screen of South Korea"s samsung and LG is known to be produced and sold by themselves.Display screens of other niche brands, and those brands capable of self-production and self-marketing, also have an unassailable position in their own segments, facing various brands.For buyers, how to find suitable suppliers from these LCD panel manufacturers?

The world-renowned LCD panel production line is mainly controlled by several enterprises: au optronics in Taiwan;Chi mei electronics in Taiwan, China;Sharp, Japan;South Korea samsung, South Korea LG;Philips;Boe, etc.These companies supply the world"s main demand for liquid crystal displays.

LG Display is currently the world"s first LCD panel manufacturer. It is affiliated to LG group and headquartered in Seoul, South Korea.Its subsidiaries are: LG electronics, LG display, GS caltex, LG chemistry, LG life and health, etc., covering the fields of chemical energy, electronics and appliances, communication and service.LG Display"s customers include Apple, HP, DELL, SONY, Toshiba, PHILIPS, Lenovo, Acer and other world-class consumer electronics manufacturers.LG"s manufacturing base in China is in nanjing, shenyang.

Samsung electronics is South Korea"s largest electronics company and the largest subsidiary of the samsung group.Its product development strategy emphasizes not only the matching principle of "leading technology, using the most advanced technology to develop new products in the leading-in stage to meet the high-end market demand", but also the matching principle of "leading technology, using the most advanced technology to develop new products, creating new demand and new high-end market".Samsung"s customers are mainly targeting samsung itself.Samsung"s manufacturing base in China is in suzhou, nanjing.

Innolux is a tft-lcd panel manufacturing company founded by foxconn technology group in 2003.The factory is located in longhua foxconn technology park in shenzhen.Innolux has a strong display technology research and development team, coupled with foxconn"s strong manufacturing capacity, to effectively play the vertical integration benefits, to improve the level of the world plane display industry will have a pointer contribution.In March 2010, it merged with chi mei electronics and tong bao optoelectronics.

Au optronics, formerly known as acer technology, was founded in August 1996. It was renamed au optronics after the merger of au optronics and united optronics in 2001.Au optronics is the world"s first tft-lcd design, manufacturing and development company to be publicly listed on the New York stock exchange (NYSE).

Boe, founded in April 1993, is the largest display panel manufacturer in China and a provider of Internet of things technology, products and services.At present, boe has reached the world"s first place in the field of notebook LCD, flat LCD and mobile LCD. With its success in joining the apple supply chain, boe will become the world"s top three LCD panel manufacturers in the near future.

Sharp is known as "the father of LCD panel".Since its founding in 1912, sharp corporation has been developing the world"s first calculator and liquid crystal display, represented by the live pencil, which is the name of the company. At the same time, sharp corporation has been actively expanding new fields, contributing to the improvement of human living standards and social progress.Sharp is already owned by foxconn.

The company has set up tft-lcd key materials and technology national engineering laboratory, national enterprise technology center, post-doctoral mobile workstation, and undertakes national development and reform commission, ministry of science and technology, ministry of industry and information technology and other major national special projects.The company"s strong technology and scientific research capabilities become the cornerstone of the company"s sustainable development.

Although flexible active-matrix organic light-emitting diode (AMOLED) panel shipments for smartphones are expected to continue growing in 2018, the pace will be much slower than expected, according to a latest report from business information provider IHS Markit(Nasdaq: INFO).

With the adoption by Apple’s iPhone X, shipments of film-based, flexible AMOLED panels for smartphones more than tripled in 2017 to 125 million units from 40 million units in 2016, and it was expected to see continued strong growth in 2018. However, sales of the iPhone X have not met market expectations, mainly because of the $1,000-plus price tag, which is partially attributed by a more pricey display panel.

“The weak demand for the iPhone X has made smartphone brands revisit their AMOLED panel purchasing plans,” said Hiroshi Hayase, senior director at IHS Markit. Now, flexible AMOLED panel shipments for smartphones are expected to reach 167 million units in 2018, up 34 percent from 2017, much slower than the expected almost double growth.

Apple seems to reexamine the percentage of its iPhone models using AMOLED panels and those using low-temperature-poly-silicon (LTPS) thin-film transistor liquid crystal display (TFT LCD) panels for 2018. Major Chinese smartphone brands, such as Huawei, Oppo, Vivo and Xiaomi, also appear to continue applying LTPS TFT LCD panels instead of switching to AMOLED for their 2018 models, while Samsung Electronics plans to keep using flexible AMOLED panels for the Galaxy S9 this year.

As a result, demand for AMOLED smartphone panels by switching from TFT LCD panels is expected to slow down. According to the latest Smartphone Display Intelligent Service report by IHS Markit, shipments of total AMOLED panel shipments for smartphones are forecast to grow 14 percent to 453 million units in 2018, from 397 million units in 2017. Glass-based, rigid AMOLED panel shipments are expected to grow at a single digit pace to 285 million units in 2018.

On the other hand, as demand for high-resolution smartphone displays is increasing in the mid-to-high-end smartphone market, demand for LTPS TFT LCD panels is forecast to keep growing in 2018 to 785 million units, up 19 percent from 656 million units in 2017. Shipments of LTPS TFT LCD panels are expected to grow stronger than AMOLED panels in the mid-high-end smartphone panel market in 2018.

Shipments of amorphous silicon (a-Si) TFT LCD panels used for low-end smartphones and feature phones are forecast to reach 807 million units in 2018, down 16 percent form 965 million units in 2017, offsetting the growth in AMOLED and LTPS TFT LCD panel demand.

Total shipments of mobile phone displays, including both TFT LCD and AMOLED panels, are forecast to increase by 1 percent to 2.02 billion units in 2018 compared to the previous year.

“As AMOLED panels allow more options in terms of form factors, demand for AMOLED for smartphones will continue to grow. However, it will start to outpace LTPS TFT LCD only after 2020,” Hayase said. “In order to compete with LTPS TFT LCD, production cost of both rigid and flexible AMOLED panels still need to be slashed, to close the price gap with LTPS TFT LCD.”

Screens that project information like pictures, movies, and messages are referred to as displays. Numerous technologies, including light-emitting diodes (LEDs), liquid crystal displays (LCDs), organic light emitting diodes (OLEDs), and others, are used in these display panels. Additionally, it plays a significant role in

The worldwide display market is expanding as a result of advancements in flexible displays, rising OLED display device demand, and the growing popularity of touch-based devices. However, barriers to market expansion include the expensive cost of cutting-edge display technologies like quantum dot and transparent displays, as well as the stalling growth of desktop, notebook, and tablet PCs. In addition, substantial development possibilities for the global display market are anticipated from new applications in flexible display technologies.

One of the key reasons fuelling the growth of the display market is the rise in demand for digital product and service promotion to get the attention of the target audience. The emergence of smart wearable gadgets, technical developments, and rising demand for OLED-based goods are all contributing to the market further.

Innovative items like leak detecting systems, home monitoring systems, and complex financial solutions are starting to appear, which has an additional impact on the industry. The industry is growing thanks to the use of organic light-emitting diode panels in televisions and smartphones. Additionally, the display market benefits from rising urbanisation, a shift in lifestyle, an increase in expenditures, and higher consumer spending.

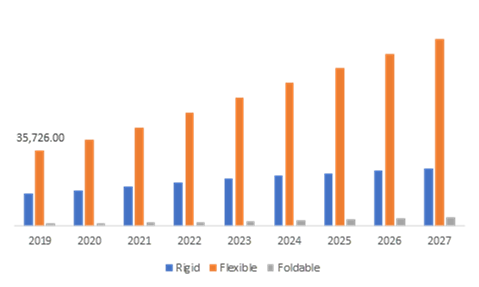

The flexible display technology has several benefits over rigid standard displays, which are often heavier. These benefits include light weight, flexibility, brightness, low power consumption, and shatter proofness. There are several consumer electronics products that employ these screens. The consumer electronics industry is expanding due to rising demand for products including smartphones, TVs, laptops, smart wearables, and other display devices.

Since touch-based gadgets are more accessible, the number of devices with touch sensors has grown tremendously in recent years. The proliferation of display devices is aided by the fact that touch-based gadgets need a display panel to function. As a result, a broad variety of home appliances, including the refrigerator, washing machine, microwave, etc., are enabled with the help of touch screens. The provision of cutting-edge display devices in automobiles, like the navigation system, heads-up display, digital rear-view mirrors, digital dashboard, and others, has also increased in the automotive sector. As a result, the market for displays is expanding due to the move toward touch-based technology.

Innovations in flexible displays, a growth in the demand for OLED display products, and a rise in the popularity of touch-based gadgets are what are driving the worldwide display market. However, the market is constrained by the expensive cost of cutting-edge display technologies like quantum dot and transparent displays, as well as the slow expansion of desktop, laptop, and tablet computers.Additionally, new applications for flexible display technologies, which are anticipated to produce profitable growth possibilities, are likely to boost the worldwide display market.

LCD technology has been widely utilised in display items during the preceding several decades. Currently, a number of settings, including retail, corporate offices, and banks, employ LCD-based gadgets. But it"s anticipated that LED technology will advance quickly throughout the course of the predicted period. The development of LED technology and its energy-efficiency are what are driving the demand for it. A disturbance in the supply-demand ratio, a decline in LCD display panel ASPs, and intense competition from emerging technologies are anticipated to push the LCD display sector into negative growth during the course of the projection period.

The smartphones will make up a large percentage of the market. This rise will be fueled by the growing use of OLED and flexible displays by smartphone manufacturers. Shipments of expensive flexible OLED displays are growing quickly, and the forecast year is expected to see this trend continue. The market"s new development path has been identified as the smart wearables category. The demand for these gadgets is expected to soar throughout the projected period due to the fast-growing market for these products and the widespread use of AR/VR technology.

Other factors contributing to the market"s growth in the area include the expansion of display panel production facilities and the quick uptake of OLED displays. APAC has low labour expenses, which lowers the overall cost of producing display panels. The market is also being supported by the increasing use of display devices across a variety of sectors, particularly in China, India, and South Korea.

Samsung Electronics launched the first 15.6-inch OLED panel in the notebook industry in January 2019. Additionally, compared to 4K LCD-based displays, the panel will produce richer colours and deeper blacks.

Display panel is a component that displays information in form of text, picture, video, and others. It acts as a direct interface in human and machine interaction. Display panels are used in variety of equipments, such as TV, smartphone, tablets, PCs, and others. Innovations in display technologies are focused on reducing harmful effects on health of end user. The technological advancements in display panel enhance viewing experience, consume less electricity, and dissipate less heat.

Growing demand for large-sized OLED panels for television and demand for public & commercial display panels drive growth of the world display panel market. However, decrease in ASP and revenues due to overcapacity obstruct growth of the market. On the other hand, demand for flexible displays for mobile phones and increasing focus on R&D activities open up new opportunities in the market.

The world display panel market is segmented based on technology, size, farm factor, resolution, applications, and geography. The technology segment is further classified into LED, OLED, and others. On the basis of size, the market is divided into small, medium, and large. Flat and flexible are farm factors discussed in the report. On the basis of resolution, the market is classified into 8K, 4K, WQHD, FHD, HD, and others. Applications covered in the report are TV, desktop monitor, notebook PC, tablet, mobile phone, automotive, digital signage, and others. Geographically, the market is divided into North America, Asia-Pacific, Europe, and Latin America, Middle East and Africa (LAMEA).

An extensive analysis of current research and clinical developments withinthe world display panel market is provided with key market dynamic factors that help in understanding the behavior of the market.

Westford,USA, Oct. 19, 2022 (GLOBE NEWSWIRE) -- The primary factors driving the growth of the Display Market are increasing demand from smartphone and tablet manufacturers, rising expenditure on smart Infra-Red (IR) sensors, and rapid expansion of digital media content. Smartphones are becoming more sophisticated and are using larger screens that require higher resolutions for better user experience. Tablets are also becoming increasingly popular as they offer a single device that can serve as both a computer and a mobile phone. This increase in demand for high-resolution displays is expected to drive the adoption of LED displays in the coming years.

The growth in demand for display market across various verticals such as healthcare, retail, automotive, appliance and others has led to an increasing demand for large sizes screens which can be cost effective owing to their mass production capabilities. Display manufacturers are also exploring new technologies such as flexible displays that can be rolled up like a traditional newspaper

One important technology that Samsung is investing in is AMOLED and QLED screens. QLEDs are generally considered to be more environmentally friendly than LCDs, since they use less power and create fewer byproducts.

Samsung has also been successful in pushing down prices for OLED displays over the past few years. This has made OLED panels more accessible to a wider range of customers, supporting growth at rival companies such as LG Electronics and Sony.

Quantum dots or QLED offer many advantages over traditional LCDs in the display market, such as better color reproduction, enhanced viewing angles, better response time, and lower power consumption. Their small size also makes them ideal for applications where sliding or tilting LCD panels are not possible or desirable. Quantum dot displays have already begun appearing in consumer electronics and will eventually replace traditional LCDs as the predominant type of display in devices like smartphones and tablets.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey