lcd panel demand made in china

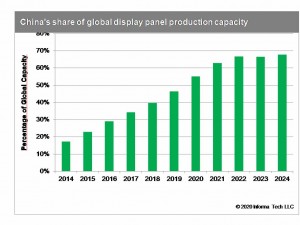

China is the leader in producing LCD display panels, with a forecast capacity share of 56 percent in 2020. China"s share is expected to increase in the coming years, stabilizing at 69 percent from 2023 onwards.Read moreLCD panel production capacity share from 2016 to 2025, by countryCharacteristicChinaJapanSouth KoreaTaiwan-----

DSCC. (June 8, 2020). LCD panel production capacity share from 2016 to 2025, by country [Graph]. In Statista. Retrieved January 19, 2023, from https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. "LCD panel production capacity share from 2016 to 2025, by country." Chart. June 8, 2020. Statista. Accessed January 19, 2023. https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. (2020). LCD panel production capacity share from 2016 to 2025, by country. Statista. Statista Inc.. Accessed: January 19, 2023. https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. "Lcd Panel Production Capacity Share from 2016 to 2025, by Country." Statista, Statista Inc., 8 Jun 2020, https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC, LCD panel production capacity share from 2016 to 2025, by country Statista, https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/ (last visited January 19, 2023)

LCD panel production capacity share from 2016 to 2025, by country [Graph], DSCC, June 8, 2020. [Online]. Available: https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

Panel makers are cutting production by 16 percent on average from this month, Rong Chaoping, senior researcher at market research firm AVC Revo, told Yicai Global. Television panel makers are expected to ship 3.6 million less panels than last month.

Panel makers will reduce capacity by between 15 and 20 percent this month, said Wu Rongbing, chief analyst at Chinese semiconductor intelligence service Omdia.

LCD TV display shipments from China’s five largest panel manufacturers accounted for 68.5 percent of the global market in April, a new high, and they were expected to exceed 70 percent this year, according to Omdia.

But there is much less demand for notebook computers, monitors and TVs now that fewer people are working from home as the Covid-19 pandemic wanes and amid pressure from global inflation. This is driving prices down, said Li Yaqin, general manager of market research firm Sigmaintell.

The global panel industry is expected to slash production by about 20 percent this year, according to Beijing-based Sigmaintell. It is the first time since 2013 that the worldwide sector has implemented such a large-scale and wide-ranging cut in manufacturing. But it should help to slow the fall in prices, Li said.

“Tumbling prices are squeezing profits,” Li said. “The price of a TV panel is now below cost price and that of some data panels is also below the manufacturing cost.”

“Panel makers are facing rising liquidity pressure and bigger losses as prices are now below cost price, so the display industry is likely to undergo another big reshuffle,” Rong said.

Excess supply will ease in the third quarter once output is cut, and prices will start to pick up and then flatten out, Li said. Demand for consumer electronic products is shrinking by far more than expected so it is too early to tell whether prices will rebound in the second half, she added.

Panel prices are likely to stop dropping this month or next as output falls, Wu said. Whether prices will start to pick up soon depends on when demand improves.

Chinese display panel makers accounted for nearly half of the share in the global liquid crystal display TV panel market in the first half of this year, dominating the industry.

Beijing-based market researcher Sigmaintell Consulting said shipments of LCD TV panels worldwide totaled 140 million pieces in the year"s first half, up 3.6 percent compared with the same period a year ago.

The supply of TV panels though has surpassed demand due to the slowdown in the global economy and weaker consumer purchasing power. Manufacturers are facing severe challenges from falling panel prices, the Sigmaintell report said.

The shipment of BOE"s LCD TV panels stood at 27.6 million in the Jan-June period while LG Display followed with 22.7 million, down 4.5 percent year-on-year. Innolux Display Group was in third place, having shipped 21.9 million units.

Shenzhen China Star Optoelectronics Technology Co Ltd, a subsidiary of consumer electronics giant TCL Corp, ranked fourth, shipping 19.3 million pieces of TV panels. Chinese panel makers accounted for a 45.8 percent share in the global LCD TV panel market.

Sigmaintell estimated that the gap between supply and demand would widen further, and the panel market may face a long-term risk of oversupply. The industry may have to undergo a reshuffle given fierce market competition, it said.

The panel makers must reduce costs, optimize their internal structures, promote technological innovation and explore more innovative applications, the report by the consultancy said.

Separately, BOE"s Gen 10.5 TFTLCD production line has entered operation in Hefei, Anhui province. The plant will produce high-definition LCD screens of 65 inches and above.

CSOT also announced in November last year that its Gen 11 TFT-LCD and active-matrix OLED production line had officially began operation. The project will produce 43-inch, 65-inch and 75-inch liquid crystal display screens.

China is expected to replace South Korea as the world"s largest flat-panel display producer in 2019, a report from the China Video Industry Association and the China Optics and Optoelectronics Manufacturers Association said.

"The average size of TV panels is likely to increase 1.4 inches in 2019. The 65-inch dimension will become the most popular size of TV," Li Yaqin, general manager of Sigmaintell, said while adding the 65-inch TV will become the mainstream screen in people"s living rooms in the future.

Compared with traditional LCD display panels, OLED has a fast response rate, wide viewing angles, high-contrast images and richer colors. It is thinner and can be made flexible.

Chinese manufacturers are expected to raise their market share from 39% this year to 52% next year in the monitor panel market, and 36% to 39% in the notebook panel market

Chinese manufacturers are expected to raise their market share from 39% this year to 52% next year in the monitor panel market, and 36% to 39% in the notebook panel market, according to TrendForce’s preliminary shipment forecast of panel makers for 2021. As such, these manufacturers are expected to maintain their plans of transitioning some production capacities from TV panel manufacturing to IT panel manufacturing in spite of the TV panel shortage in 2H20 caused by various factors such as the closedown of SDC’s LCD panel manufacturing operations, the rise of the stay-at-home economy, and the stimulus policies instituted by governments worldwide.

TrendForce indicates that, with regards to the standing of Chinese manufacturers in the IT panel industry, BOE has long established itself as the market leader, while CSOT and HKC are each also catching up fast. After acquiring SDC’s Suzhou-based Gen 8.5 fab, CSOT will possess even more production capacities for monitor panels. At the same time, HKC currently maintains three Gen 8.6 fabs, located in Chongqing, Chuzhou, and Mianyang, and plans to capture additional shares in the monitor panel and notebook panel markets.

Chinese panel makers have been gradually transitioning their current panel capacities to monitor panel production. Most significantly, as more Gen 10.5 production lines become available, TV panel production will most likely take place in Gen 10.5 fabs instead of Gen 8.5 fabs in the future, while the existing Gen 8.5 and Gen 8.6 production lines will be reallocated to monitor panel production in order to expend the excess capacity made available after TV panel production moves to Gen 10.5 fabs. In addition, after SDC’s forecasted closing of LCD panel manufacturing operations at the end of this year, CSOT and HKC will look to capture the resultant supply share of SDC’s absence in the market. On the other hand, since both TCL, which is CSOT’s parent company, and HKC possess monitor ODM operations, should the two companies decide to vertically integrate by making panels for their own monitor products, they will be able to effectively optimize their cost structures.

Although CSOT’s Wuhan-based T3 LTPS Gen 6 production line is primarily dedicated to smartphone and notebook panel manufacturing, the considerable reduction of LTPS smartphone panel demand from Huawei caused by U.S. sanctions means CSOT is expected to make plans for an increase in notebook panel shipment in order to make up for the shortfall. As well, thanks to high demand for TV panels this year, HKC’s production lines have been operating at maximum capacity utilization rates, in turn slowing down its notebook panel business. However, in light of the fact that the COVID-19 pandemic has brought about a rapid surge in TN notebook panel demand, HKC is therefore looking to TN panels as a new commercial opportunity in the notebook display market and subsequently prioritizing TN panel development over IPS panel development as its product strategy. Not only will this reprioritization allow HKC to align its strategy with the current market trend, but it will also quickly raise the yield rate of HKC’s Mianyang-based fab, which had never manufactured NB panels, by instead having the fab manufacture TN panels, which have a relatively simpler manufacturing process.

TrendForce analyst Jeff Yang indicates that, despite Chinese panel makers’ strong intention to enter the IT panel manufacturing business, success in the IT panel market is not solely decided by a company’s production capacity. For instance, with regards to monitor panels, CSOT’s technical competency is mostly focused on VA panels, meaning the company is constrained in its product mixes due to its lack of mainstream IPS offerings. Although HKC is equipped with both IPS and VA technologies, it lacks experience in manufacturing curved VA panels, leading its clients to take on a wait-and-see approach before placing additional orders. For notebook panels, although CSOT is primarily focusing on the mid-range and high-end LTPS notebook panel market, it faces intense competition from Samsung’s OLED notebook panels, which are gradually extending from the high-end segment to the mid-range segment as well. Likewise, HKC will have to take time in order to make headways in the notebook panel market, since it has not reached any production milestones, and it requires time to cultivate a significant client base.

China accounted for 40 percent of the global display market in terms of sales in the first quarter of this year, rising to the top by beating South Korea by a margin of seven percentage points. In 2019, South Korea was 11 percentage points ahead of China. Last year and this year, however, the global display demand surged with regard to COVID-19, LCD panel prices soared as a result, and Chinese companies boosted their share in the market they are dominating.

China’s global LCD panel market share for this year is estimated at 60.7 percent. In addition, its share in the smartphone OLED panel market is likely to rise from 15 percent to 27 percent this year and next year. In this market, Samsung Display’s current share is 80 percent and the share is forecast to fall to 60 percent or so next year.

According to market research firm DSCC, BOE, the largest display panel manufacturer in China, posted US$7.7 billion in sales and US$1.4 billion in operating profit in the first quarter to exceed the sales and profits of Samsung Display and LG Display for the first time ever.

Samsung Display will stop producing LCD panels by the end of the year. The display maker currently runs two LCD production lines in South Korea and two in China, according to Reuters. Samsung tells The Verge that the decision will accelerate the company’s move towards quantum dot displays, while ZDNetreports that its future quantum dot TVs will use OLED rather than LCD panels.

The decision comes as LCD panel prices are said to be falling worldwide. Last year, Nikkei reported that Chinese competitors are ramping up production of LCD screens, even as demand for TVs weakens globally. Samsung Display isn’t the only manufacturer to have closed down LCD production lines. LG Display announced it would be ending LCD production in South Korea by the end of the 2020 as well.

Last October Samsung Display announced a five-year 13.1 trillion won (around $10.7 billion) investment in quantum dot technology for its upcoming TVs, as it shifts production away from LCDs. However, Samsung’s existing quantum dot or QLED TVs still use LCD panels behind their quantum dot layer. Samsung is also working on developing self-emissive quantum-dot diodes, which would remove the need for a separate layer.

Samsung’s investment in OLED TVs has also been reported by The Elec. The company is no stranger to OLED technology for handhelds, but it exited the large OLED panel market half a decade ago, allowing rival LG Display to dominate ever since.

Although Samsung Display says that it will be able to continue supplying its existing LCD orders through the end of the year, there are questions about what Samsung Electronics, the largest TV manufacturer in the world, will use in its LCD TVs going forward. Samsung told The Vergethat it does not expect the shutdown to affect its LCD-based QLED TV lineup. So for the near-term, nothing changes.

One alternative is that Samsung buys its LCD panels from suppliers like TCL-owned CSOT and AUO, which already supply panels for Samsung TVs. Last year The Elec reported that Samsung could close all its South Korean LCD production lines, and make up the difference with panels bought from Chinese manufacturers like CSOT, which Samsung Display has invested in.

China-based OLED panel producers BOE Technology Group and TCL China Star Optoelectronics Technology have steadily boosted their output of high-end OLED panels. By next year they’ll control some 43 per cent of global demand for OLEDs.

DSCC adds that if China overtakes South Korea in its share of OLED production, China will dominate virtually the entire display industry. Most Chinese-made OLED panels are small to midsize ones for smartphones, so the focus will then be on whether Chinese companies acquire capabilities for manufacturing large OLED panels for TV manufacturing.

South Korean companies have already lost out to China in the race to invest in producing large LCD panels. In large OLED panels, South Korean companies are steadily going on the defensive, suggests DSCC.

LG Display and Samsung Display are struggling to find their ways out of the deterioration of their performance even after withdrawing from production of liquid crystal display (LCD) panels. The high-priced organic light emitting diode (OLED) panel sector regarded as a future growth engine is not growing fast due to the economic downturn. Even in the OLED panel sector, Chinese display makers are within striking distance of Korean display makers, experts say.

On Aug. 30, Display Supply Chain Consultants (DSCC), a market research company, predicted that LCD TV panel prices hit an all-time low in August and that an L-shaped recession will continue in the fourth quarter. According to DSCC, the average price of a 65-inch ultra-high-definition (UHD) panel in August was only US$109, a 62 percent drop from the highest price of US$288 recorded in July in 2021. The average price of a 75-inch UHD panel was only US$218, which was only about half of the highest price of US$410 in July last year. DSCC predicted that the average panel price in the third quarter will fall by 15.7 percent. As Chinese companies’ price war and the effect of stagnation in consumption overlapped, the more LCD panels display makers produce, the more loss they suffer.

As panel prices fell, manufacturers responded by lowering facility utilization rates. DSCC said that the LCD factory utilization rate descended from 87 percent in April to 83 percent in May, 73 percent in June, and 70 percent in July.

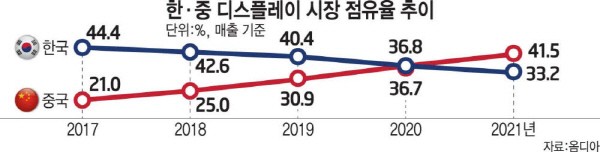

Now that the LCD panel business has become no longer lucrative, Korean display makers have shut down their LCD business or shrunk their sizes. In the LCD sector, China has outpaced Korea since 2018. China’s LCD market share reached 50.9 percent in 2021, while that of Korea dropped to 14.4 percent, lower than Taiwan’s 31.6 percent.

Samsung Display already announced its withdrawal from the LCD business in June. Only 10 years have passed since the company was spun off from Samsung Electronics in 2012. LG Display has decided to halt domestic LCD TV panel production until 2023 and reorganize its business structure centering on OLED panels. Its Chinese LCD production line will be gradually converted to produce LCD panels for IT or commercial products. TrendForce predicted that LG Display will stop operating its P7 Plant in the first quarter of next year.

Korean display makers’ waning LCD business led to a situation in which Korea even lost first place in the display industry. Korea with a display market share of 33.2 percent was already overtaken by China with 41.5 percent) in 2021 according to market researcher Omdia and the Korea Display Industry Association. Korea’s market share has never rebounded in for five years since 2017 amid the Korean government’s neglect. Seventeen years have passed since 2004 when Korea overtook Japan to rise to the top of the world in the LCD industry. Korea’s LCD exports amounted to more than US$30 billion in 2014, but fell to US$21.4 billion last year.

A bigger problem is that Korean display makers may lose its leadership in the OLED panel sector although it is still standing at the top spot. While Korea’s OLED market share fell from 98.1 percent in 2016 to 82.8 percent last year, that of China rose from 1.1 percent to 16.6 percent. Considering that the high-end TV market is highly likely to shrink for the time being due to a full-fledged global consumption contraction, some analysts say that the technology gap between Korea and China can be sharply narrowed through this looming TV market slump. According to industry sources, the Chinese government is now focusing on giving subsidies to the development of OLED panel technology rather LCD technology. On the other hand, in Korea, displays were also wiped out from national strategic technology industry items under the Restriction of Special Taxation Act which can receive tax benefits for R&D activities on displays.

As TrendForce points out, agencies within the US government are taking notice of China’s certain advantages in the development of display technologies and the build-up of panel production capacity. However, the US will unlikely attempt to directly impose control over panel supply with new trade restrictions in the short term. On the other hand, the upstream portion of the supply chain – especially the sections concerning driver ICs and other related semiconductor chips – are starting to react to the tightening of the US sanctions against Chinese semiconductor companies.

Furthermore, some electronics OEMs have recently been re-examining their panel supply chains to evaluate the sourcing of semiconductor components. While OEMs have yet to explicitly ban the use of panel-related chips from Chinese suppliers, they are actively developing backup plans that would seek alternative supply sources in case the US further broadens the scope its technology export rules on Chinese companies.

Again, looking at OEMs, they have not rejected panels from certain suppliers for now; but they might start to prefer or exclude particular IC design houses that offer driver chips. As for foundries and OSAT providers, decoupling has begun in accordance with the decisions of some downstream customers. In the future, there is a distinct possibility that Chinese IC design houses, foundries and OSAT providers could be barred from participating in the supply chains for the product models targeting the US market.

Presently, Chinese foundries have steadily raised their collective market share for large-sized driver ICs to around 25%. They still have much ground to catch up when compared with the 40% held by Taiwan-based foundries, but this share figure is still significant. If the US government imposes new restrictions seeking to prevent Chinese foundries from using mature semiconductor process technologies to manufacture chips such as driver ICs, then the supply chains for panels and related ICs will likely face another huge wave of capacity crunch and supply shortage.

Nevertheless, since there are no direct orders from the US government targeting panel supply and related components at this moment, TrendForce believes the decoupling process in the supply chain for driver ICs is going to be a slow and drawn-out process.

According to market research firm Omdia, China recorded $64.8 billion in sales including LCD and OLED in the global display market last year. China took over Korea’s No. 1 spot with a market share of 41.5%. Korea"s market share fell 8.3 points (p) to 33.2%. This is the first time since 2004, in 17 years, that Korea had to hand over the No. 1 spot. Korea had a 9.4 p advantage in market share over China up until 2019.

China overtook Korea and seized power in the LCD market by offering a low-priced products. BOE, China"s largest panel manufacturer, has become the world"s largest LCD manufacturer with help of the subsidy from the Chinese government. LCD sales was $28.6 billion last year, accounting for 26.3% of the total LCD market. The sales of Chinese companies such as BOE, CSOT, Tianma, and Visionox increased significantly as demand for TV and information technology (IT) devices increased with the prolonged COVID 19 and increased price of LCD panel.

After taken over in the LCD market, Korea is focusing on the highly-valued OLED market. Samsung Display and LG Display are transforming their LCD production lines to OLED. Korea is the No. 1 with 82.3% of the global OLED market shares according to Omdia, and China’s market share only accounts for16.6%.

China"s dominance is expected to continue for some time because the large display market such as TVs and laptops still depends on LCD. Only when Korea starts to reduce OLED panel prices by mass producing OLED, then Korea can replace the LCD market led by China.

China has also started to narrow the gap with Korea in OLED industry. BOE and other companies have commercialized OLED for small and medium-sized displays such as mobile, laptop, and tablet. Following LCD market, China is threatening Korea in OLED market as well as China expands OLED market share mainly in the Chinese smartphone market.

Critics are pointing out that Korea needs to expand in OLED market and develop new technologies in order to maintain the OLED gap with China. Korea must take control over the large TV panel market, which has a large technological gap with China, and create a new form factor with new technologies such as flexible, rollable, and bendable panels.

Chinese display manufacturers are chasing their South Korean rivals closely by planning to release a larger volume of liquid-crystal panels over 32 inches this year, said a market researcher Sunday.

According to a report on the 2017 shipment strategies of Chinese TV panel makers by IHS Markit, Chinese LCD panel suppliers are forecast to ship out a total of 320,000 large-size panels larger than 32 inches by the end of this year, a 33 percent surge from last year.

In the report, Wu mentioned the plans of major Chinese panel firms such as BOE, CSOT, CEC-Panda and HKC to focus on expanding production of 43, 55 and 58-inch panels, adding that demand for 32-inch panels will gradually decrease.

“By the end of 2018, China will be the largest region for TFT LCD capacity, and larger-sized products may make their factories more efficient and profitable than they have been when producing 32-inch panels,” he said.

“The strategies of Chinese panel makers will significantly influence global supply and demand,” Wu said. “In 2015 and 2016, the Chinese companies shipped 33.2 percent of worldwide LCD TV panel, trailing only Korean panel makers at 36.4 percent.”

The competition structure has been advantageous for the Korean players, since their Chinese rivals had been focusing on small LCD panels until last year. But now the Korean firms are facing fiercer competition in prices.

Although demand for organic-light emitting diode panels in the TV market is gradually rising, dominance of LCD panels is projected to continue for the foreseeable future.

“While OLEDs are expected to post sharp growth, they will not be able to usurp LCD as the panels of choice for upper-end TVs,” another report by IHS Markit said.

Recent observations by market intelligence firm TrendForce suggests that the ongoing expansion of the US semiconductor trade restrictions against China could eventually spread to the display panel industry. Agencies within the US government are taking notice of China’s certain advantages in the development of display technologies and build-up of panel production capacity.

However, the US will unlikely attempt to directly impose control over panel supply with new trade restrictions in the short term. On the other hand, the upstream portion of the supply chain, especially the sections concerning driver ICs and other related semiconductor chips, are starting to react to the tightening of the US sanctions against Chinese semiconductor companies. Furthermore, some electronics OEMs have recently been re-examining their panel supply chains to evaluate the sourcing of semiconductor components. While OEMs have yet to explicitly ban the use of panel-related chips from Chinese suppliers, they are actively developing backup plans that would seek alternative supply sources in case the US further broadens the scope its technology export rules on Chinese companies.

The continuation and strengthening of the restrictions on semiconductor trade is starting to have an effect on the supply chain related to driver ICs. TrendForce’s latest investigation finds signs of decoupling or bifurcation. Specifically, there is a divergence towards both extremes: a supply chain that totally excludes Chinese content versus a counterpart that is “de-Americanized”. Again, looking at OEMs, they have not rejected panels from certain suppliers for now, but they might start to prefer or exclude particular IC design houses that offer driver chips. As for foundries and OSAT providers, decoupling has begun in accordance with the decisions of some downstream customers. In the future, there is a distinct possibility that Chinese IC design houses, foundries and OSAT providers could be barred from participating in the supply chains for the product models targeting the US market.

Presently, Chinese foundries have steadily raised their collective market share for large-sized driver ICs to around 25%. They still have much ground to catch up when compared with the 40% held by Taiwan-based foundries, but this share figure is still significant. If the US government imposes new restrictions seeking to prevent Chinese foundries from using mature semiconductor process technologies to manufacture chips such as driver ICs, then the supply chains for panels and related ICs will likely face another huge wave of capacity crunch and supply shortage.

Nevertheless, since there are no direct orders from the US government targeting panel supply and related components at this moment, TrendForce believes the decoupling process in the supply chain for driver ICs is going to be a slow and drawn-out process. In the long run, decoupling as an overarching trend will make the supply chain more fragmented and inefficient. This development, in turn, will increase the overall cost for all parties involved. Furthermore, due to the need to mitigate the potential risks resulting from the decoupling process, the supply chain could even see an elevation of minimum inventory level and a prolonging of order lead time.

TrendForce holds the view that both risks and opportunities exist in the decoupling and rearrangement of the supply chain. Some IC design houses could gradually redirect wafer input to fabs outside China for some of their offerings in order to eliminate the possible risks associated with the US sanctions or satisfy some customers’ demand for non-Chinese components. Thus, IC design houses and foundries that operate in Taiwan could gain new orders as the supply chain undergoes an internal shakeup. On the other hand, their counterparts in Mainland China could have more opportunities to rise as major players thanks to their government’s strategy for localizing supply chains.

![]()

However, as China’s LCD industry continues to catch up and develop, China currently accounts for more than 50% of the global LCD production capacity and has become the largest production area for integrated LCD products.

As early as 2019, my country’s total LCD production capacity reached 11.34.81 billion square meters, ranking first in the world. In the past two years, not only the LCD industry still has an advantage, new display technologies such as OLED panels also account for 10% of the production capacity.

China has accounted for more than 50% of global LCD production capacity, and BOE’s share is close to 30%, making it the world’s largest LCD manufacturer.

With the gradual withdrawal of major manufacturers such as Samsung and LG from the LCD market, BOE is still increasing its production capacity, and its market share is expected to further increase in the future.

Over the years, products such as mobile phones, LCD TVs, and conference tablets have continued to develop, with larger sizes and lower prices, and consumers are willing to replace them with new ones.

Although the sales growth of mobile phones and TVs in the past two years has not been as good as expected, from a global perspective, the Chinese market is still an extremely important part of the demand for LCD panels.

Samsung Display is ending direct production of LCD panels in South Korea and China by the end of this year, according to a report by the global news agency Reuters.

Samsung’s gorgeous QLED displays (got one) are LCDs with a quantum dots layer, and there is lots of R&D work going on to add quantum dots to OLED displays, which would boost their brightness and color volume as well.

The investment for the next five years will be focused on converting one of its South Korean LCD lines into a facility to mass produce more advanced “quantum dot” screens.

Samsung Display’s cross-town rival LG Display Co Ltd said earlier this year that it will halt domestic production of LCD TV panels by the end of 2020.

This is happening, maybe not entirely but heavily, because Chinese government-backed manufacturers like BOE have greatly upped production capacity for LCD TVs, driving prices and margins down for consumer and professional display products.

Samsung Display reportedly plans to shut down ahead of schedule four of its LCD panel production lines as early as in the third quarter of 2020, as the vendor is looking to accelerate its exit from the LCD segment, according to industry sources.

The ongoing coronavirus pandemic is apparently an impetus pushing Samsung Display to phase out its LCD panel production, as the crisis has wrecked havoc on the global economy, slowing down business activities and halting sports events such as the Tokyo Olympics 2020, which is seriously undercutting demand for TVs and adding downward pressure on panel prices, said the sources.

Samsung Display also plans to keep production at its 8.5G LCD fab in Suzhou, China in the meantime, while overhauling its L7-2 fab for production of POLED panels and its L8 fab for QD-OLED panels, indicated the sources.

The Korean panel maker is also looking to halt the operations of the Suzhou 8.5G line by the third quarter of 2022 and is currently in talks to sell the LCD panel plant to Chinese panel makers, said the sources, adding that the completion of a deal will mark Samsung Display ‘s exit from the LCD TV panel market.

Meanwhile, TV panel prices, which have been trending upward recently along with reduced production caused by the pandemic, are expected to stay flat in April, as capacity resumption of most panel plants in China is expected to reach over 90% in the month, while TV brands are likely to slow down their panel purchases amid pandemic-induced uncertainty, commented the sources.

Presumably, while Samsung may not be directly manufacturing LCD, the industry will still be able to buy Samsung LCD displays – just manufactured, as some will be already, by other companies in China and Taiwan.

I really don’t see direct view LED taking the place of single LCD displays, but much of the future of signage is in LED that fills entire walls and other surfaces, inside and outside.

LCD supply and demand rapidly changed from Q2’21 to Q3’21. LCD TV demand in developed countries became weak by COVID-19’s bubble’s EOL (end of life) in emerging countries and the pandemic of COVID-19 made LCD TV demand weak in emerging regions. LCD panel production area seems to have increased by 3% from Q2’21 to Q3’21, while the panel shipment area seems to have declined by 3% from Q2’21 to Q3’21. Especially LCD TV panel shipment seems to have declined by 8% in units from Q2’21 to Q3’21. The gap between LCD TV panel shipment and production was a big in Q3’21. Chinese and Taiwanese LCD panel suppliers’ LCD fab utilization remain high even under huge price fall in October 2021. I would like to show the fab utilization forecast from 2021 to 2022 and how much panel inventories will be carried over to 2022.

Regarding OLED, the surplus of flexible OLED will continue for a while but it is expected to be getting better from now by the demand increase for China smartphone brands. Rigid OLED fab utilization has been high level in SDC A2 fab in 2021 by increasing the production for non-smartphone like notebook PC and game applications. The next remarkable point of rigid OLED supply demand is if how much the IT demands like notebook PC, table and monitor will catch up with the new fab, G8.5 Oxide RGB based OLED fab investment in 2023. Just in case that Samsung VD will really purchase WOLED in 2022, LGD will probably need to pull in the next investment of WOLED fab. Samsung VD may also increase the LCD purchasing from LGD. This Samsung VD’s activity will give an impact on China LCD suppliers. In this speech, OLED TV and Mobile OLED supply and demand will also be explained.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey