lcd panel supply chain made in china

Introduction: Global LCD industry shift and automotive intelligence together to promote the rapid development of China’s LCD panel industry, which will bring a continuous increase in demand for backlight modules, China’s backlight module industry has greater potential for development.

LCD panel backlight module consists of a backlight light source, light guide, optical film, and a plastic frame, which is an important component of LCD display panel. As the backlight module has technology-intensive and labor-intensive attributes, with abundant high-skilled labor advantage China is attracting the global LCD panel industry to the domestic rapid transfer.

From LCD application to the present, the global LCD panel industry capacity transfer has gone through three periods, 2000 Japan dominated the global LCD industry; 2000 – 2010, Japan’s production capacity to South Korea and Taiwan; 2010 to the present, Japanese manufacturers gradually withdraw from the LCD panel industry, production capacity began to transfer to mainland China, so far, mainland China LCD production capacity has occupied the global half of the world.

In recent years, South Korea’s Samsung and LG display will shift their business focus to OLED, and will gradually shut down their LCD production lines and withdraw from the LCD panel industry; at the time of South Korean manufacturers’ withdrawal, domestic enterprises are stepping up new construction to expand LCD production capacity.

BOE, Huaxing photoelectric, Huike, CEC in 2020 – 2021, a total of eight 7 generation LCD production lines completed and put into operation, and domestic panel manufacturers have further expansion plans, the next few years domestic LCD production capacity will continue to increase.

LCD panel manufacturers tend to choose the nearby supporting module suppliers for the safety of the key component supply chain and cost reduction considerations. LCD panel production capacity transfer to China will bring opportunities to domestic backlight module manufacturers and drive the development of the domestic backlight module industry.

The future of the car will pay more attention to the human driving experience, to the intelligent development, which will bring the increasing demand for car display. On the one hand, the number of car displays gradually increased, for example, the instrument panel, rearview mirror, central control platform more to display the way, the passenger and rear position with entertainment display. On the other hand, the car display is constantly to a large screen, multi-screen development, especially in high-end models, the large display has become standard, for example, Tesla Model S screen size of 17 inches, Mercedes-Benz A-class car configuration of two 10.5-inch display.

According to the terminal application size, backlight module can be divided into large, medium, and small size, of which small size backlight module is mainly used in smartphones, wearable devices, and other terminals, the medium size used in notebook computers, tablet PCs, car screens and other terminals, the large size is mainly used in LCD TV.

From the industry development trend, smartphone display is transitioning to OLED, LCD TV market is gradually saturated, the future of large size and small size backlight module market potential is relatively small; and the future of the car display market potential is huge, by the backlight module manufacturers are unanimously optimistic, are currently accelerating the layout ( see Table 2 ). Focusing on the traditional medium-sized backlight module field, Hanbo Hi-Tech and Weishi Electronics have significant advantages in core technology patents, downstream customer resources, process experience accumulation, production costs, etc., and have more development advantages in the future.

The current global LCD display panel industry is rapidly moving to China, which brings development opportunities to China’s backlight module industry. In addition, automotive intelligence will also bring a continuous increase in demand for medium-sized car displays, the first to enter the field of medium-sized backlight module manufacturers with its customer resources, core technology, scale efficiency, and other advantages will be more beneficial.

China has become the world"s largest LCD panel manufacturing base and is investing in a complete Mini/Micro-LED industry chain. Li Leiguang, JW Insights" chief analyst of the display industry, shared this information at a Mini/Micro-LED industry forum held in Shenzhen in late October.

With over 16 years of experience in the display industry, Li Leiguang has a deep understanding of China"s domestic display industry from materials and panel technologies to industrial policies. He has written industrial research and planning reports for various government departments in Shenzhen, Zhaoqing, Meishan, and Chengdu as well as customized reports for corporate clients in the display industry chain. This article is an excerpt from his speech.

China had long depended on imports of IC and display screens in the manufacturing of display products. IC and display screens are the two pillar sectors of the ICT Industry. The trend has been changing. With the continuous increase of high-generation production lines and capacity of domestic panel manufacturers and the gradual closure of LCD production lines by South Korean manufacturers, China"s LCD panel market share has increased year by year.

In 2020, China achieved a trade surplus in LCD panels for the first time. Meanwhile, the TFT-LCD has become a mainstream choice in the display panel industry after nearly 30 years of development.

JW Insights data shows that China has invested a total of RMB1.2 trillion($187.56 billion) in TFT-LCD and AMOLED panel production lines; Some 50 TFT-LCD and AMOLED panel production lines have been built, with 197 million m2/year TFT-LCD production capacity, 8.9 million m2/year AMOLED production capacity.

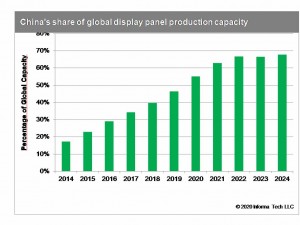

China"s LCD production capacity accounted for 50% of the global production capacity in 2020, becoming the world"s largest LCD panel production center; It will reach more than 75% of the world"s total by 2025.

China"s mainland is currently the only region that maintains continuous growth in LCD panel production capacity. With Japanese and South Korean manufacturers gradually withdrawing from the LCD panel, China is becoming the dominant player.

Chinese domestic display panel manufacturers are also embracing new display technologies such as Mini LED, Mirco LED, OLED and Micro OLED (silicon-based OLED), which are in an explosive market growth phase.

Unlike LCD technology that originated overseas, China has kept pace with the world in Mini/Micro-LED and has established a relatively complete industrial chain in it. Currently, the Mini LED is mainly used for LCD panel backlighting; It will be an inevitable trend for the direct LED display with Mini LED in large-screen in the future.

However, TFT-LCD technology will remain the mainstay for a long time in the future, because of its maturity and competitive prices. Multiple display technologies will coexist in the future; Micro-LED panels mass production will not be achieved in the short term.

Recent observations by market intelligence firm TrendForce suggests that the ongoing expansion of the US semiconductor trade restrictions against China could eventually spread to the display panel industry. Agencies within the US government are taking notice of China’s certain advantages in the development of display technologies and build-up of panel production capacity.

However, the US will unlikely attempt to directly impose control over panel supply with new trade restrictions in the short term. On the other hand, the upstream portion of the supply chain, especially the sections concerning driver ICs and other related semiconductor chips, are starting to react to the tightening of the US sanctions against Chinese semiconductor companies. Furthermore, some electronics OEMs have recently been re-examining their panel supply chains to evaluate the sourcing of semiconductor components. While OEMs have yet to explicitly ban the use of panel-related chips from Chinese suppliers, they are actively developing backup plans that would seek alternative supply sources in case the US further broadens the scope its technology export rules on Chinese companies.

The continuation and strengthening of the restrictions on semiconductor trade is starting to have an effect on the supply chain related to driver ICs. TrendForce’s latest investigation finds signs of decoupling or bifurcation. Specifically, there is a divergence towards both extremes: a supply chain that totally excludes Chinese content versus a counterpart that is “de-Americanized”. Again, looking at OEMs, they have not rejected panels from certain suppliers for now, but they might start to prefer or exclude particular IC design houses that offer driver chips. As for foundries and OSAT providers, decoupling has begun in accordance with the decisions of some downstream customers. In the future, there is a distinct possibility that Chinese IC design houses, foundries and OSAT providers could be barred from participating in the supply chains for the product models targeting the US market.

Conversely, the ban on Chinese suppliers will not apply to product models targeting the Chinese market. Instead, OEMs might actually increase Chinese suppliers’ participation in order to raise the chance of a successfully entry into this region. Component suppliers such as IC design houses, too, could adopt a similar strategy so as to insert themselves into the Chinese market. To comply with and support the localization policy of the Chinese government, component suppliers could increase the portion of partners or clients from China and establish a separate local supply chain.

Presently, Chinese foundries have steadily raised their collective market share for large-sized driver ICs to around 25%. They still have much ground to catch up when compared with the 40% held by Taiwan-based foundries, but this share figure is still significant. If the US government imposes new restrictions seeking to prevent Chinese foundries from using mature semiconductor process technologies to manufacture chips such as driver ICs, then the supply chains for panels and related ICs will likely face another huge wave of capacity crunch and supply shortage.

Nevertheless, since there are no direct orders from the US government targeting panel supply and related components at this moment, TrendForce believes the decoupling process in the supply chain for driver ICs is going to be a slow and drawn-out process. In the long run, decoupling as an overarching trend will make the supply chain more fragmented and inefficient. This development, in turn, will increase the overall cost for all parties involved. Furthermore, due to the need to mitigate the potential risks resulting from the decoupling process, the supply chain could even see an elevation of minimum inventory level and a prolonging of order lead time.

TrendForce holds the view that both risks and opportunities exist in the decoupling and rearrangement of the supply chain. Some IC design houses could gradually redirect wafer input to fabs outside China for some of their offerings in order to eliminate the possible risks associated with the US sanctions or satisfy some customers’ demand for non-Chinese components. Thus, IC design houses and foundries that operate in Taiwan could gain new orders as the supply chain undergoes an internal shakeup. On the other hand, their counterparts in Mainland China could have more opportunities to rise as major players thanks to their government’s strategy for localizing supply chains.

Faced with a reduced workforce caused by travel bans and quarantine conditions, LCD and OLED fabrication plants (fabs) across China struggled to resume normal operations in early‐ to mid‐February. Chinese LCD fabs were only expected to have a capacity utilization of 70 to 75 percent for the month compared to a normal rate of 90 to 95 percent, according to research from Omdia Display.

The biggest impact is in LCD displays for TVs and notebook computers. By late 2019, the prolonged issue of LCD panel over‐supply driven by Chinese fabs had begun to reverse course as Korean manufacturers restructured their capacity, shutting down some fabs and converting others to OLED production. According to Hsieh, concerns about an LCD panel supply going forward already had spurred some TV manufacturers to increase orders, and now that LCD production in China is slowing as a result of the COVID‐19 outbreak, LCD panel makers are seeking sharp price increases from their original equipment manufacturer (OEM) customers, with a month‐to‐month jump of as much as 10 percent in some cases.

Omdia had originally forecast that the price for an open‐cell LCD TV panel was going to rise by $1 or $2 per month in February, but the actual increase may wind up being $3 to $5 for the month. “The problem is the coronavirus is coming so fast [that] the panel maker has been given a very good reason to increase the price radically,” Hsieh says. He also expects prices to increase for notebook displays, for which he predicts a 30–40 percent decrease in production for 2020"s first financial quarter (Q1), because of shortages in LCD modules.

In Wuhan itself, there are five major fabs, with four making smartphone displays. China Star and Tianma each operate a low‐temperature polycrystalline silicon LCD fab and a flexible OLED fab in the city, while BOE has a new Gen 10.5 LCD plant aimed at TV panels. Hsieh says that the China Star and Tianma OLED fabs are both in the ramping‐up stages, and the new BOE fab also is moving slowly. The biggest impact of COVID‐19 in Wuhan may be on the China Star Gen 6 OLED plant. Along with BOE, it"s slated to be a key supplier of flexible OLED panels for Lenovo"s new Motorola Razr foldable phone. “It"s unfortunate timing,” Hsieh says. —Glen Dickson

Attendees visit the booth of TV panel maker Shenzhen China Star Optoelectronics Technology during an international exhibition in Shanghai on July 11, 2019. [Photo by Lyu Liang/For China Daily]

Chinese companies have gained a competitive edge in the large-screen display industry and the exit of South Korean counterparts such as Samsung Electronics and LG Display from the liquid crystal display market will bring opportunities for China"s panel makers despite the challenges posed by the COVID-19 pandemic.

Market research firm Sigmaintell said BOE Technology Group Co Ltd-a leading Chinese supplier of display products and solutions-became the world"s largest shipper of LCD TV panels for the first time in 2019.

The Beijing-based company shipped 53.3 million units of LCD panels in 2019, with production capacity increasing by more than 20 percent on a yearly basis.

The consultancy said the LCD TV panel production area of Chinese manufacturers will account for more than 50 percent of the global total this year, surpassing South Korean competitors who are accelerating the shutdown of large-sized LCD panel production capacity due to competition from Chinese manufacturers.

It estimated the production capacity of large-sized LCD panels will continue to increase in China over the next three years. In addition, global LCD TV panel shipments stood at 283 million pieces last year, a slight decrease of 0.2 percent year-on-year. Meanwhile, the shipment area was 160 million square meters, an increase of 6.3 percent year-on-year.

"Chinese companies have gained an upper hand in large-screen LCD displays. Samsung and LG"s decision to exit from the LCD sector means Chinese panel makers will take a dominant position in this field," said Li Dongsheng, founder and chairman of Chinese tech giant TCL Technology Group Corp.

Li said South Korean firms will focus on organic LED screens and quantum dot LED displays, while Chinese TV panel makers are catching up at a rapid pace.

The pandemic will accelerate reshuffling in the display industry as supply has surpassed demand in the past few years and competition has become very fierce, he added.

Data consultancy Digitimes Research said it comes as little surprise that Samsung has opted to withdraw from the LCD panel sector as its LCD business was losing money in every quarter of 2019 due to challenges from Chinese competitors.

BOE said its Gen 10.5 TFTLCD production line achieved mass production in Hefei, Anhui province, in March 2018. The plant mainly produces high-definition LCD screens of 65 inches and above. With a total investment of 46 billion yuan ($6.5 billion), the company"s second Gen 10.5 TFT-LCD production line launched operations in Wuhan, Hubei province, in December.

The Gen 11 TFT-LCD and active-matrix OLED production line of Shenzhen China Star Optoelectronics Technology, a subsidiary of TCL, officially entered operations in November 2018, producing 43-inch, 65-inch and 75-inch LCD screens.

Chen Lijuan, an analyst at Sigmaintell, said panel manufacturers should not just invest in production lines, but also pay more attention to the establishment of the whole supply chain, including raw materials, equipment and technology.

Bian Zheng, deputy director of research at AVC Revo, a unit of market consultancy firm AVC, said China will have a 51 percent market share in global TV shipments in 2020, while South Korea will have 25 percent, adding that large-screen TV panels will bolster healthy development of the industry.

Bian said the OLED and QLED will be the next-generation flat-panel display technologies to be in the spotlight. LG Display is currently the world"s only supplier of large-screen OLED TV panels.

OLED is a relatively new technology and part of recent display innovation. It has a fast response rate, wide viewing angles, super high-contrast images and richer colors. It is much thinner and can be made flexible, compared with traditional LCD display panels.

LCD supply and demand rapidly changed from Q2’21 to Q3’21. LCD TV demand in developed countries became weak by COVID-19’s bubble’s EOL (end of life) in emerging countries and the pandemic of COVID-19 made LCD TV demand weak in emerging regions. LCD panel production area seems to have increased by 3% from Q2’21 to Q3’21, while the panel shipment area seems to have declined by 3% from Q2’21 to Q3’21. Especially LCD TV panel shipment seems to have declined by 8% in units from Q2’21 to Q3’21. The gap between LCD TV panel shipment and production was a big in Q3’21. Chinese and Taiwanese LCD panel suppliers’ LCD fab utilization remain high even under huge price fall in October 2021. I would like to show the fab utilization forecast from 2021 to 2022 and how much panel inventories will be carried over to 2022.

Regarding OLED, the surplus of flexible OLED will continue for a while but it is expected to be getting better from now by the demand increase for China smartphone brands. Rigid OLED fab utilization has been high level in SDC A2 fab in 2021 by increasing the production for non-smartphone like notebook PC and game applications. The next remarkable point of rigid OLED supply demand is if how much the IT demands like notebook PC, table and monitor will catch up with the new fab, G8.5 Oxide RGB based OLED fab investment in 2023. Just in case that Samsung VD will really purchase WOLED in 2022, LGD will probably need to pull in the next investment of WOLED fab. Samsung VD may also increase the LCD purchasing from LGD. This Samsung VD’s activity will give an impact on China LCD suppliers. In this speech, OLED TV and Mobile OLED supply and demand will also be explained.

The escalating coronavirus crisis is impacting production at display panel factories located in the semi-quarantined city of Wuhan, China, spurring a significant near-term reduction in the global supply of panels used in liquid crystal display televisions (LCDs) and other products.

The five factories in the city producing liquid crystal displays (LCDs) and organic light-emitting diode (OLED) panels will experience near-term slowdowns in production compared to expected levels, according to IHS Markit technology research, now a part of Informa Tech.

With the situation evolving quickly, IHS Markit technology research is still assessing the magnitude of the supply shortfall on multiple display types and markets. However, leading Chinese panel makers stated they believe that total capacity utilization for all LCD fabs in the country could fall by at least 10 percent and perhaps by more than 20 percent during the month of February.

With China expected to own 55 percent of global display manufacturing capacity in 2020, the immediate impact of the production reduction has been a worldwide decrease in availability and an increase in pricing for LCD-TV panels. This has resulted in turmoil throughout the display supply chain as suppliers and purchasers alike scramble to adjust to swiftly changing market conditions.

The leading Chinese suppliers of LCD panels for TVs, notebook PCs and PC monitors now are planning to raise panel prices more aggressively. For example, the price for an open-cell LCD-TV panel was originally expected to rise by $1 or $2 per month in February. However, the actual increase may be $3 to $5 for the month.

Beyond the immediate production impact at these facilities, the coronavirus is also likely to trigger delays in the ramp-up of manufacturing at new display fabs during the first half of 2020. This will reduce overall panel availability during the next few months. It also could result in further panel supply tightness as TV display buyers hasten the pace of their panel purchases to build stockpiles for future shortfalls.

While major panel makers are rightly concerned about the coronavirus’s impact on consumer sales, demand for their products from TV makers has actually increased. TV makers are pulling in their panel demand and sometimes double-booking orders to shore up their inventories. The panel maker indicated that the demand surge for orders delivered in February is as large as 10 percent above the previous demand forecast.

LCD panel makers outsource much of the production of such modules. However, production at several key third-party module suppliers has now ceased, impacting panel production severely throughout the country. Key module supplier SkyTech is sharply reducing production until mid-February.

Panel makers maintain their own captive LCD module factories. However, these operations are also facing production bottlenecks amid the coronavirus crisis.

China-based OLED panel producers BOE Technology Group and TCL China Star Optoelectronics Technology have steadily boosted their output of high-end OLED panels. By next year they’ll control some 43 per cent of global demand for OLEDs.

Analysts at Display Supply Chain Consultants (DSCC) say that South Korea’s technology giants LG Display and Samsung currently have a 55 per cent market share (in 2022) and helped by what DSCC describe as ‘generous state subsidies”.

DSCC adds that if China overtakes South Korea in its share of OLED production, China will dominate virtually the entire display industry. Most Chinese-made OLED panels are small to midsize ones for smartphones, so the focus will then be on whether Chinese companies acquire capabilities for manufacturing large OLED panels for TV manufacturing.

South Korean companies have already lost out to China in the race to invest in producing large LCD panels. In large OLED panels, South Korean companies are steadily going on the defensive, suggests DSCC.

BOE Technology Group and TCL China Star Optoelectronics Technology (TCL CSOT) are among the Chinese panel makers to have ramped up output since around 2019 with generous state subsidies. China is gaining on South Korea, whose share of capacity is seen reaching 55% for 2022 in an October estimate by U.S. market intelligence firm Display Supply Chain Consultants (DSCC).

The effect on the supply chain has been dramatic and immediate. Many factories in China have seen spikes in Covid cases, reducing their workforce to a fraction of their full capacity. This happened during the peak production season right before the Chinese New Year.

The effect on the supply chain will be to increase lead times and cause shortages in the market. Many US companies have recently been trying to readjust orders to accommodate the temporary slowdown in the economy. With the tightening in the supply chain, a better strategy may be to increase orders so the limited factory resources are allocated to your company.

In 2021, the output value of China’s display industry reached about 586.8 billion yuan, a figure nearly eight times that of 10 years ago, data from the China Optics and Optoelectronics Manufactures Association LCB, or CODA, showed. The area of the country’s display panel shipments stood at about 160 million square meters, over seven times larger than 10 years ago. The size of China’s display industry and the area of its display panel shipments both ranked first in the world.

China has made breakthroughs in some core technologies in key fields. Chinese liquid crystal display (LCD) enterprises have broken technical barriers and taken 70 percent of the global market share. Chinese companies have also acquired key technologies in organic light emitting diode (OLED) and rapidly expanded their production scale. China is also catching up in new-generation display technologies.

China will make greater efforts to gain a foothold in the medium and high ends of the industrial chain of the new display industry, said an official with the MIIT.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey