lcd panel supply chain price

LCD TV panel prices have reached all-time lows but they continue to decline, and although the pace of decline is slowing in the third quarter, we now forecast that the industry will have an “L-shaped” recovery in the fourth quarter. In other words, no recovery at all until 2023. The ‘perfect storm’ of a continued oversupply, near-universally weak demand and excessive inventory throughout the supply chain has combined, and every screen size of TV panel has reached an all-time low price. Although fab utilization has slowed sharply in July, we do not see any signal to suggest that prices can increase any time soon.

After LCD TV panel prices hit bottom in September 2022 and prices for several sizes increased in Q4, the rally in prices proved to be short-lived and prices have been in a holding pattern, with no changes from December into February. While prices for most sizes increased in Q4, the increase was modest. The last phase of the downward spiral in panel prices was characterized by a massive inventory drawdown in the display supply chain and a corresponding massive reduction in fab utilization by panel makers.

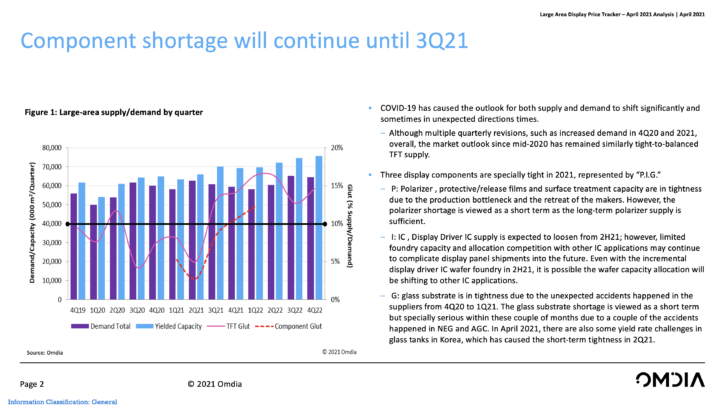

Based on Omdia’s Large Area Display Price Tracker, April 2021, Sanju Khatri, director of consulting for displays, ProAV and consumer devices at research and consultancy firm Omdia, provided some analysis on disruption in the display supply chain due to component shortage and high demand. Impact will be mostly felt on LCD technology, as strong demand and component shortage will lead to the following price cycles for LCD panels.

To read more about the broader supply situation, here’s our interview with manufacturers including Crestron, Valens, Barco, Legrand AV, MXL, and AVIXA .

EDITOR’S NOTE: Three distinct terms are used below. Components (display driver IC, glass, and polarizer); panel (raw LCD panels) and brands/finished sets/device vendors (TV, monitor/laptops/ProAV vendors).

Strong consumer demand for TVs/IT displays. The “at home” trends are including work at home, learn at home, entertain at home and shop at home. The LCD TV, Notebook, LCD monitor, and tablet PC products continue to have the strong demand thanks to the “at home” trends.

Display panel makers are increasing prices sharply to take the fast turnaround on profitability. The LCD TV open cell prices have been increasing by 40%-50% from June 2020 to December 2020. And it is expected there will be another 20% increase from January 2021 to May 2021.

Component shortage(Glass substrate, Display Driver IC, T-con, PMIC, Polarizer films) are frustrating the supply chain from time to time, making the set makers to be more nervous thus giving more orders. Three display components are especially tight in 2021, represented by “P.I.G.”

P: Polarizer, protective/release films and surface treatment capacity are in tightness due to the production bottleneck and the retreat of the makers. However, the polarizer shortage is viewed as a short term as the long-term polarizer supply is sufficient.

I: IC, Display Driver IC supply is expected to loosen from 2H21however, limited foundry capacity and allocation competition with other IC applications may continue to complicate display panel shipments into the future. Even with the incremental display driver IC wafer foundry in the second half of 2021 (2H21), it is possible the wafer capacity allocation will be shifting to other IC applications.

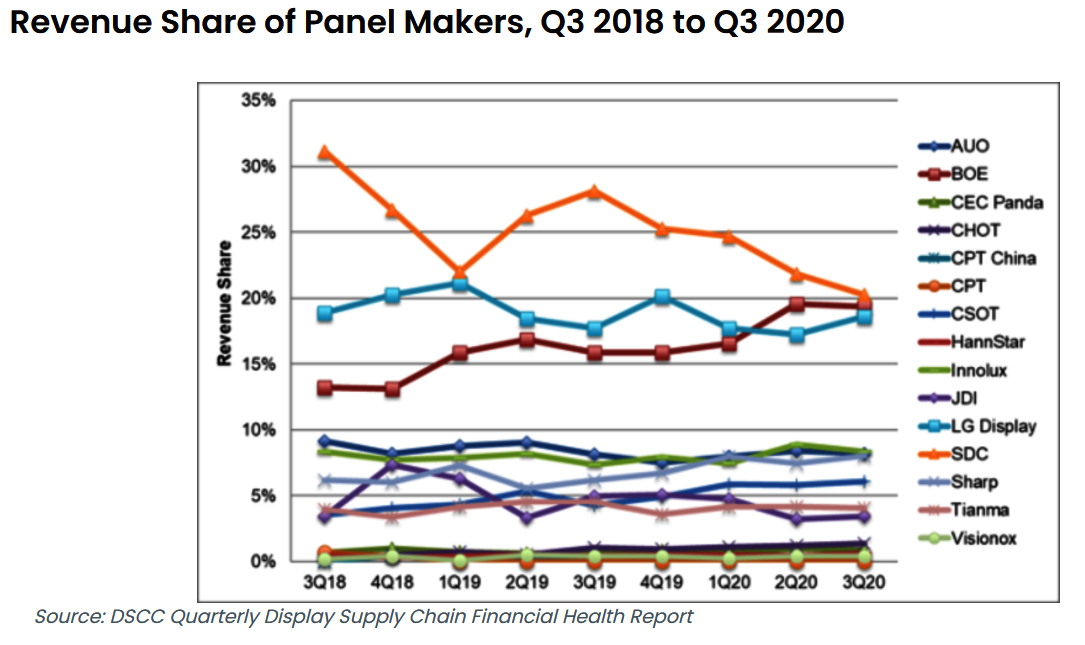

What They Say In its blog (registration required), DSCC highlighted the difference in financial results between LCD and OLED makers, with an increasing ‘chasm’ between OLED-focused makers and those making LCDs. Q3 was the …

After fifteen months of decreases, LCD TV panel prices finally hit bottom in September 2022 and prices for several sizes increased in October. We now expect to see a modest increase in prices through …

What They Say DSCC commented in its blog on the all time lows that are now being seen in LCD TV panels and forecast that the prices will continue to decline, with an expectation …

What They Say DSCC published a blog article with extracts from its latest OLED shipment report and said that OLED panel revenues increased 12% Y/Y on 3% Y/Y unit declines as a result of …

What They Say Earlier this week, DSCC published a blog article summarising the situation on LCD TV panel pricing, describing the situation as a ‘Perfect Storm’ with Continued oversupply Near-universally weak demand and excessive …

Yesterday, DSCC’s Bob O’Brien published a blog article that revealed that Samsung has told all its business groups to suspend purchases and control their inventory status. Samsung has informed flat panel display makers in …

What They Say Earlier this week, DSCC published a blog article characterising the inventory issues in the supply chain as acting like a “Gale-Force Headwind for Display Industry” and the Nikkey reinforced this idea …

What They Say In a blog article (registration required), Ross Young of DSCC picked out some highlights of his keynote talk at the SID/DSCC Business Conference of Display Week. (The Tragedy of the LCD …

LCD TV panel prices have been declining since July 2021 and the trend is expected to continue throughout Q2 2022. With an improvement in the Covid19 situation and a shift away from STH (Stay-at-home) …

Linda Lin covers large-sized TFT LCD panels and is in charge of survey reports involving the manufacturers and vendors of the notebook panel supply chain.

Linda worked previously at LCD market research firm WitsView, leading the research on panels as well as on downstream products that included monitors and TVs. At the Market Intelligence & Consulting Institute, Taiwan Chief Information and Communications Technology (ICT) market research group, she oversaw regional research for South and East Asia. It was during this time that she decided to make large-sized displays her main focus. Linda has a master’s degree in business administration from National Yunlin University of Science and Technology in Taiwan.

Kimi is a senior analyst for display (TFT LCD and OLED) touch and user interface at Omdia. He covers display price, supply chain, fingerprint, cover lens, shipment forecasts, and emerging technologies.

Prior to joining Omdia (formerly IHS Markit), Kimi was a research analyst at Tianma Group, where he spent over two years in LCD and AMOLED market research. He also oversaw the China FPD industry market at the Topology Research Institute for over five years. Kimi has a bachelor"s degree in telecommunications engineering and a master’s degree in microelectronics from Shanghai University, China.

Stacy is an experienced analyst in Omdia’s display research team, covering small and medium displays. She focuses on automotive displays, smartphone displays, and wearable displays. As a Principal Analyst, she covers small and medium display shipments, supply chain, pricing, and business strategy analysis. She is the lead analyst of the automotive display intelligent service.

As part of Omdia’s small/medium displays practice, Joy covers displays under 9 inches in size utilized in smartphones, tablets, wearables, and automotive displays. Her research touches areas such as the AMOLED ecosystem, new trends in smartphone panel displays, and the supply chain in China for smartphone displays.

Joy brings 17 years of experience to the subjects she covers. She worked previously at BOE, the giant Chinese display manufacturer, as a product manager for medical and industrial displays. She started her career at Tianma Group as an LCD module design engineer, then became manager of product design and development. She transferred to the marketing department as an analyst for mobile phone displays and then for automotive displays. Joy has a bachelor’s degree in automation from Beihang University, a major public research institution in China. She also holds a master’s degree in business management from Renmin University of China.

Mr. Hidetoshi Himuro is a Director at Omdia. He previously worked at DisplaySearch, a leader in primary research and forecasting on the global display market. At DisplaySearch, he served as director of IT & FPD market research. He was responsible for market research and analysis of large-area LCD applications, including monitor, notebook PCs and public display/digital signage. He also forecasted monthly large-area LCD panel pricing. With his background in engineering, he covered the LCD panel technology roadmap.

Prior to DisplaySearch, Mr. Himuro held a number of positions at NEC in both Japan and the US. At NEC, his diverse responsibilities included strategic planning, project management, LCD panel and monitor set procurement, design verification, vendor relationships and hardware development for notebook PCs and LCD monitors and their LCD panels. He has a bachelor"s degree in Electrical Engineering from Tokyo University of Science, Japan.

Peter Su conducts research on large-sized displays, tracking supply-and-demand dynamics, market trends, and product roadmaps on panels sized more than 9 inches measured diagonally and used in tablets, notebooks, monitors, and televisions.

Previously, Peter was at DisplaySearch, where he worked with large displays as well. At AU Optronics, he was in panel sales and strategic product marketing in the notebook PC and tablet business units. There, he was also involved in PC capacity planning, technology investment projects, and both upstream and downstream channels for panels and mobile PCs. Peter has a bachelor"s degree in economics from the University of Victoria in Canada, and a master’s degree in business administration from Concordia University Wisconsin in Mequon, Wisconsin.

Vicki Chen focuses on display materials and components, including new form factors, weight efficiencies, and technological advances in displays. She brings more than 10 years of experience in the flat-panel-display industry.

Vicki worked previously at Chinese firm Sigmaintell Consulting, where she was responsible for research on the mobile phone panel market and value chain. She also worked in new-project development at Taiwan Display, a part of Japan Display. She had her first taste of the flat-panel display industry and its workings as a product planning engineer in charge of the request-for-quote (RFQ) development for mobile phone products for China Brands at Innolux, a TFT LCD panel manufacturer in Taiwan.

Mr. Hiroshi Hayase is a Senior Director at Omdia. He previously worked at DisplaySearch and Solarbuzz, leading providers of display and solar market intelligence. With nearly 30 years of experience in the LCD industry, he brings an unparalleled focus to sales, marketing management, production, product engineering and market research and analysis.

At DisplaySearch, Mr. Hayase served as vice president of small and medium displays. Before that, he was responsible for sales and market research at a Taiwanese LCD panel/module manufacturer, Wintek Japan Corporation. Earlier, he served as sales manager with Applied Komatsu Technology (AKT), where he was responsible for sales of CVD systems to major Japanese panel producers. He also has 13 years of experience in sales management and production engineering across the full range of LCD production processes with Seiko Epson. Mr. Hayase holds a bachelor"s degree in Mechanical Engineering from Shizuoka University, Japan.

He previously worked at DisplaySearch and Solarbuzz, leading providers of display and solar market intelligence. Mr. Annis is a leading expert in flat panel display research and served in a dual role as vice president of manufacturing research at DisplaySearch as well as at its sister company of Solarbuzz. At DisplaySearch, he was responsible for analyzing emerging technologies, tracking and forecasting flat panel display investments, and researching equipment, materials and process trends. At Solarbuzz, he developed the company"s proprietary polysilicon, wafer and cell manufacturing databases and authored related reports.

Mr. Robin Wu is a Principal Analyst at Omdia. Previously he worked at DisplaySearch, a leader in primary research and forecasting on the global display market. At DisplaySearch, he served as a PC and TFT analyst, specializing in trend analysis of China"s PC, monitor, and panel markets. He also acted as vice chair of the VESA monitor task group in 2010 and has focused on monitor/panel standardization since early 2009.

Prior to DisplaySearch, Mr. Wu spent nearly seven years at the leading IT brand IBM/Lenovo. There, he focused on monitor/TFT business, delivering industry-leading green ThinkVision products and managing panel sourcing and qualifications. In addition to providing support to the desktop/AIO business, he acted as a liaison in the industry, building strong relationships with leading PC monitor OEMs in China. Mr. Wu has a bachelor"s degree in Mechanics & Electronics and a master"s degree in Micro-Electro-Mechanical Systems from Huazhong University of Science and Technology, China.

Jeff Lin is a longtime analyst and researcher in the field of displays, having previously worked at DisplaySearch, a leader in primary research and forecasting on the global display market. At DisplaySearch, he worked as an analyst covering Taiwan"s display market and was responsible for market research and analysis of the PC monitor value chain and large-area panel roadmap.

Before DisplaySearch, Jeff gained valuable experience handling panel sourcing and desktop monitor market analysis at BenQ Corporation. Prior to that, he served as a key monitor account sales manager at Samsung Electronics Taiwan, where he formed key relationships with leading PC monitor company and OEMs in the country. Before Samsung, he was an engineer at Chunghwa Picture Tubes (CPT), where he led TV panel development projects and planned TV panel roadmaps.

Jimmy joined the company in 2014 following the acquisition of DisplaySearch, where he served as a senior analyst covering display materials and LED analysis. Jimmy also worked at Samsung—first at Samsung LED, and then at Samsung Electronics. There, he led several R&D projects on new light sources for LCD backlighting and new BLU structures.

Jerry Kang is responsible for the OLED display market analysis at IHS. His main focus is the AMOLED panel and the next generation display market including flexible and transparent display with AMOLED.

Prior to joining IHS in 2011, Jerry worked as an OLED development engineer at Samsung SDI and Samsung Mobile Display, in charge of operational circuit designing for OLED and LCD.

David Hsieh is a noted expert in research and analysis of the TFT LCD, and LCD TV value chain for Mainland China and Taiwan. As head of the Displays team, he oversees the division’s end-to-end research on displays, covering the supply chain, materials and components, supply-and-demand dynamics, pricing and cost modeling, revenue and shipment forecasts, and emerging technologies.

In an earlier stint at DisplaySearch, he led the company’s primary research and forecasting on the global display market while concurrently serving as vice president of the greater China market. David also worked at HannStar Display, a leading manufacturer of TFT LCD panels, as a key account manager, production planner, and production engineer for the HannStar TFT LCD module line.

In his previous roles at the company, Jusy led the research team on TV technology and ecosystems, which included the panel display market for TVs and large-sized LCDs. He has also worked on the global monitor and public information markets.

The automotive industry has always been very conservative in the semiconductors it uses, often ten or 15-year-old technology. This approach makes sense in modern cars, which are complex systems with over 100 integrated circuits and voltages from 12 volts upwards that would not be kind to leading-edge semis. Therefore any chip in the vehicle that fails could cause a trip to the dealership. Add to that complexity the many years the industry has been refining "just-in-time" supply chain management.

The price of LCD display panels for TVs is still falling in November and is on the verge of falling back to the level at which it initially rose two years ago (in June 2020). Liu Yushi, a senior analyst at CINNO Research, told China State Grid reporters that the wave of “falling tide” may last until June this year. For related panel companies, after the performance surge in the past year, they will face pressure in 2022.

LCD display panel prices for TVs will remain at a high level throughout 2021 due to the high base of 13 consecutive months of increase, although the price of LCD display panels peaked in June last year and began to decline rapidly. Thanks to this, under the tight demand related to panel enterprises last year achieved substantial profit growth.

According to China State Grid, the annual revenue growth of major LCD display panel manufacturers in China (Shentianma A, TCL Technology, Peking Oriental A, Caihong Shares, Longteng Optoelectronics, AU, Inolux Optoelectronics, Hanyu Color Crystal) in 2021 is basically above double digits, and the net profit growth is also very obvious. Some small and medium-sized enterprises directly turn losses into profits. Leading enterprises such as BOE and TCL Technology more than doubled their net profit.

Take BOE as an example. According to the 2021 financial report released by BOE A, BOE achieved annual revenue of 219.31 billion yuan, with a year-on-year growth of 61.79%; Net profit attributable to shareholders of listed companies reached 25.831 billion yuan, up 412.96% year on year. “The growth is mainly due to the overall high economic performance of the panel industry throughout the year, and the acquisition of the CLP Panda Nanjing and Chengdu lines,” said Xu Tao, chief electronics analyst at Citic Securities.

In his opinion, as BOE dynamically optimizes its product structure, and its flexible OLED continues to enter the supply chain of major customers, BOE‘s market share as the panel leader is expected to increase further and extend to the Internet of Things, which is optimistic about the company’s development in the medium and long term.

“There are two main reasons for the ideal performance of domestic display panel enterprises.” A color TV industry analyst believes that, on the one hand, under the effect of the epidemic, the demand for color TV and other electronic products surges, and the upstream raw materials are in shortage, which leads to the short supply of the panel industry, the price rises, and the corporate profits increase accordingly. In addition, as Samsung and LG, the two-panel giants, gradually withdrew from the LCD panel field, they put most of their energy and funds into the OLED(organic light-emitting diode) display panel industry, resulting in a serious shortage of LCD display panels, which objectively benefited China’s local LCD display panel manufacturers such as BOE and TCL China Star Optoelectronics.

Liu Yushi analyzed to reporters that relevant TV panel enterprises made outstanding achievements in 2021, and panel price rise is a very important contributing factor. In addition, three enterprises, such as BOE(BOE), CSOT(TCL China Star Optoelectronics) and HKC(Huike), accounted for 55% of the total shipments of LCD TV panels in 2021. It will be further raised to 60% in the first quarter of 2022. In other words, “simultaneous release of production capacity, expand market share, rising volume and price” is also one of the main reasons for the growth of these enterprises. However, entering the low demand in 2022, LCD TV panel prices continue to fall, and there is some uncertainty about whether the relevant panel companies can continue to grow.

According to Media data, in February this year, the monthly revenue of global large LCD panels has been a double decline of 6.80% month-on-month and 6.18% year-on-year, reaching $6.089 billion. Among them, TCL China Star and AU large-size LCD panel revenue maintained year-on-year growth, while BOE, Innolux, and LG large-size LCD panel monthly revenue decreased by 16.83%, 14.10%, and 5.51% respectively.

Throughout Q1, according to WitsView data, the average LCD TV panel price has been close to or below the average cost, and cash cost level, among which 32-inch LCD TV panel prices are 4.03% and 5.06% below cash cost, respectively; The prices of 43 and 65 inch LCD TV panels are only 0.46% and 3.42% higher than the cash cost, respectively.

The market decline trend is continuing, the reporter queried Omdia, WitsView, Sigmaintel(group intelligence consulting), Oviriwo, CINNO Research, and other institutions regarding the latest forecast data, the analysis results show that the price of the TV LCD panels is expected to continue to decline in April. According to CINNO Research, for example, prices for 32 -, 43 – and 55-inch LCD TV panels in April are expected to fall $1- $3 per screen from March to $37, $65, and $100, respectively. Prices of 65 – and 75-inch LCD TV panels will drop by $8 per screen to $152 and $242, respectively.

“In the face of weak overall demand, major end brands requested panel factories to reduce purchase volumes in March due to high inventory pressure, which led to the continued decline in panel prices in April.” Beijing Di Xian Information Consulting Co., LTD. Vice general manager Yi Xianjing so analysis said.

“Since 2021, international logistics capacity continues to be tight, international customers have a long delivery cycle, some orders in the second half of the year were transferred to the first half of the year, pushing up the panel price in the first half of the year but also overdraft the demand in the second half of the year, resulting in the panel price began to decline from June last year,” Liu Yush told reporters, and the situation between Russia and Ukraine has suddenly escalated this year. It also further affected the recovery of demand in Europe, thus prolonging the downward trend in prices. Based on the current situation, Liu predicted that the bottom of TV panel prices will come in June 2022, but the inflection point will be delayed if further factors affect global demand and lead to additional cuts by brands.

With the price of TV panels falling to the cash cost line, in Liu’s opinion, some overseas production capacity with old equipment and poor profitability will gradually cut production. The corresponding profits of mainland panel manufacturers will inevitably be affected. However, due to the advantages in scale and cost, there is no urgent need for mainland panel manufacturers to reduce the dynamic rate. It is estimated that Q2’s dynamic level is only 3%-4% lower than Q1’s. “We don’t have much room to switch production because the prices of IT panels are dropping rapidly.”

Ovirivo analysts also pointed out that the current TV panel factory shipment pressure and inventory pressure may increase. “In the first quarter, the production line activity rate is at a high level, and the panel factory has entered the stage of loss. If the capacity is not adjusted, the panel factory will face the pressure of further decline in panel prices and increased losses.”

In the first quarter of this year, the retail volume of China’s color TV market was 9.03 million units, down 8.8% year on year. Retail sales totaled 28 billion yuan, down 10.1 percent year on year. Under the situation of volume drop, the industry expects this year color TV manufacturers will also set off a new round of LCD display panel prices war.

Display Logic has developed global sources of supply far beyond those of our competitors. Among those are selected manufacturers with which we have partnered with preferential pricing agreements.

It may seem odd in the face of stalled economies and stalled AV projects, but the costs of LCD display products are on the rise, according to a report from Digital Supply Chain Consulting, or DSCC.

Demand for LCD products remains strong , says DSCC, at the same time as shortages are deepening for glass substrates and driver integrated circuits. Announcements by the Korean panel makers that they will maintain production of LCDs and delay their planned shutdown of LCD lines has not prevented prices from continuing to rise.

I assume, but absolutely don’t know for sure, that panel pricing that affects the much larger consumer market must have a similar impact on commercial displays, or what researchers seem to term public information displays.

Panel prices increased more than 20% for selected TV sizes in Q3 2020 compared to Q2, and by 27% in Q4 2020 compared to Q3, we now expect that average LCD TV panel prices in Q1 2021 will increase by another 12%.

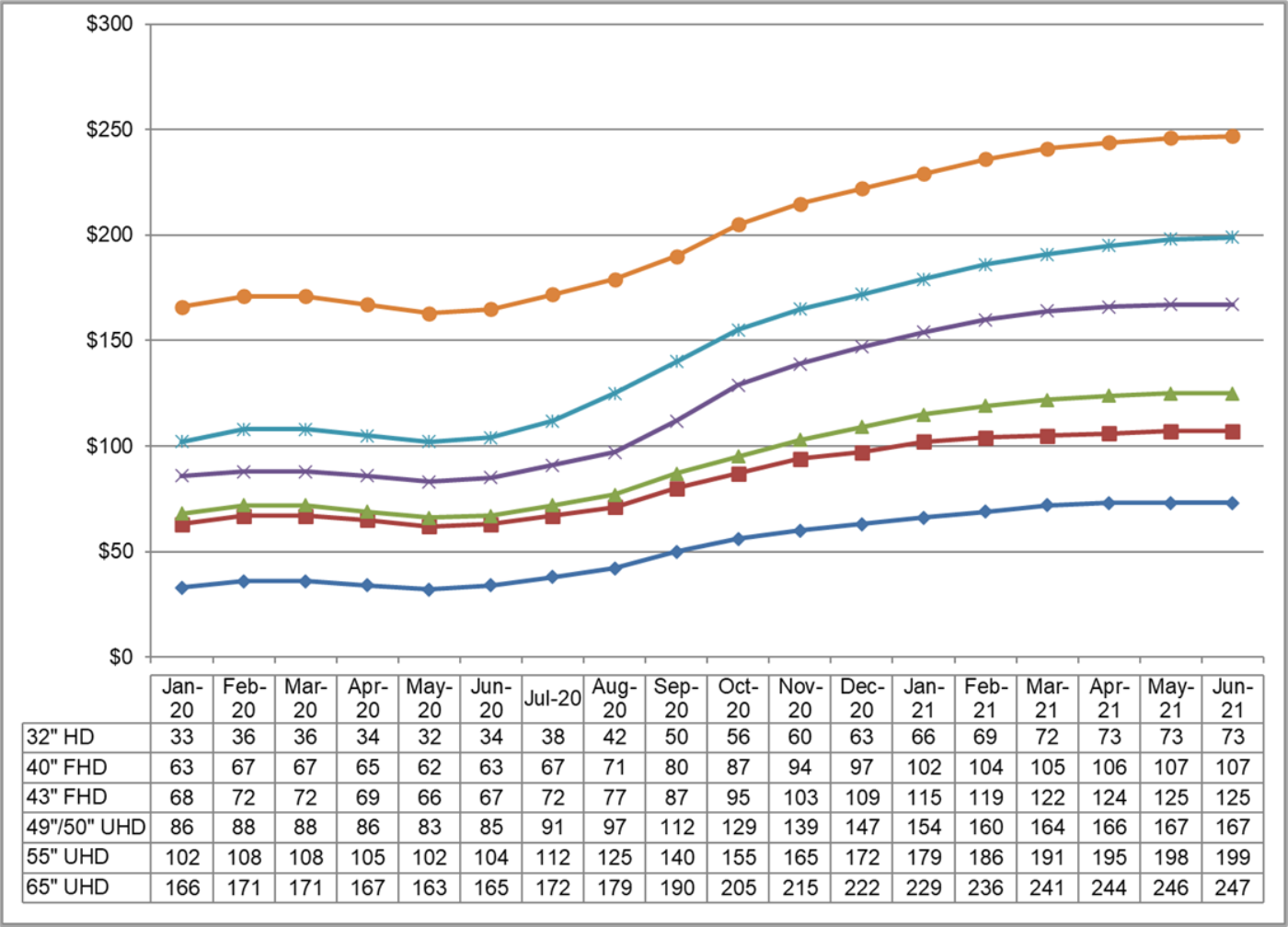

The first chart shows our latest TV panel price update, with prices increasing across the board from a low in May 2020 to an expected peak in May/June of this year. Last month’s update predicted a peak in February/March. However, our forecast for the peak has been increased and pushed out after AGC reported a major accident at a glass plant in Korea and amid continuing problems with driver IC shortages.

Prices increased in Q4 for all sizes of TV panels, with massive percentage increases in sizes from 32” to 55” ranging from 28% to 38%. Prices for 65” and 75” increased at a slower rate, by 19% and 8% respectively, as capacity has continued to increase on those sizes with Gen 10.5 expansions.

Prices for every size of TV panel will increase in Q1 at a slower rate, ranging from 5% for 75” to 16% for 43”, and we now expect that prices will continue to increase in Q2, with the increases ranging from 3% to 6% on a Q/Q basis. We now expect that prices will peak in Q2 and will start to decline in Q3, but the situation remains fluid.

All that said, LCD panels are way less costly, way lighter and slimmer, and generally look way better than the ones being used 10 years ago, so prices is a relative problem.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey