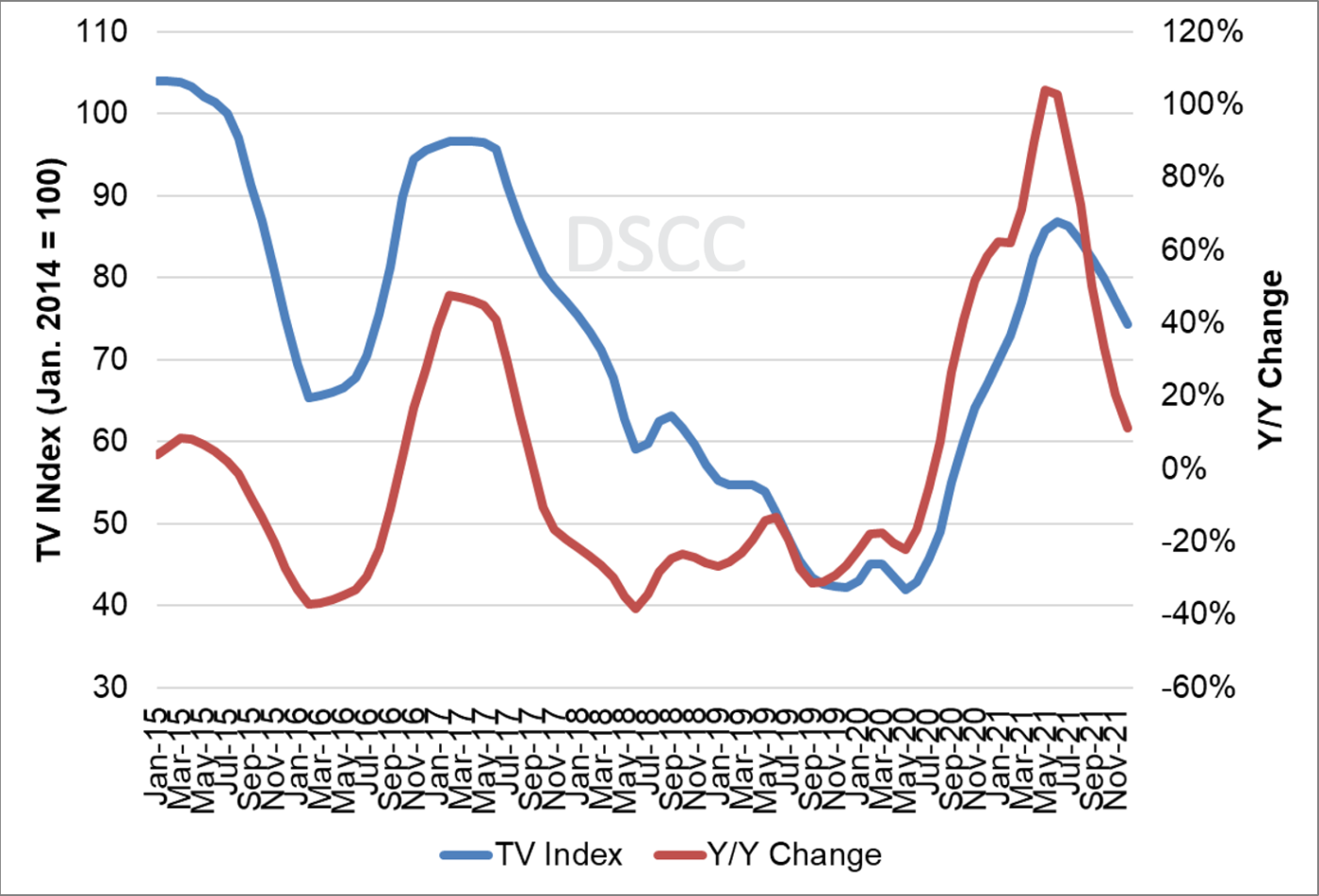

lcd panel price trend 2021 brands

Prices for all TV panel sizes fluctuated and are forecast to fluctuate between 2020 and 2022. The period from March 2020 to July 2021 saw the biggest price increases, when a 65" UHD panel cost between 171 and 288 U.S. dollars. In the fourth quarter of 2021, such prices fell and are expected to drop to an even lower amount by March 2022.Read moreLCD TV panel prices worldwide from January 2020 to March 2022, by size(in U.S. dollars)Characteristic32" HD43" FHD49"/50" UHD55" UHD65" UHD------

DSCC. (January 10, 2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) [Graph]. In Statista. Retrieved February 08, 2023, from https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars)." Chart. January 10, 2022. Statista. Accessed February 08, 2023. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. (2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars). Statista. Statista Inc.. Accessed: February 08, 2023. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "Lcd Tv Panel Prices Worldwide from January 2020 to March 2022, by Size (in U.S. Dollars)." Statista, Statista Inc., 10 Jan 2022, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC, LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) Statista, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/ (last visited February 08, 2023)

LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) [Graph], DSCC, January 10, 2022. [Online]. Available: https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

The price of LCD display panels for TVs is still falling in November and is on the verge of falling back to the level at which it initially rose two years ago (in June 2020). Liu Yushi, a senior analyst at CINNO Research, told China State Grid reporters that the wave of “falling tide” may last until June this year. For related panel companies, after the performance surge in the past year, they will face pressure in 2022.

LCD display panel prices for TVs will remain at a high level throughout 2021 due to the high base of 13 consecutive months of increase, although the price of LCD display panels peaked in June last year and began to decline rapidly. Thanks to this, under the tight demand related to panel enterprises last year achieved substantial profit growth.

According to China State Grid, the annual revenue growth of major LCD display panel manufacturers in China (Shentianma A, TCL Technology, Peking Oriental A, Caihong Shares, Longteng Optoelectronics, AU, Inolux Optoelectronics, Hanyu Color Crystal) in 2021 is basically above double digits, and the net profit growth is also very obvious. Some small and medium-sized enterprises directly turn losses into profits. Leading enterprises such as BOE and TCL Technology more than doubled their net profit.

Take BOE as an example. According to the 2021 financial report released by BOE A, BOE achieved annual revenue of 219.31 billion yuan, with a year-on-year growth of 61.79%; Net profit attributable to shareholders of listed companies reached 25.831 billion yuan, up 412.96% year on year. “The growth is mainly due to the overall high economic performance of the panel industry throughout the year, and the acquisition of the CLP Panda Nanjing and Chengdu lines,” said Xu Tao, chief electronics analyst at Citic Securities.

In his opinion, as BOE dynamically optimizes its product structure, and its flexible OLED continues to enter the supply chain of major customers, BOE‘s market share as the panel leader is expected to increase further and extend to the Internet of Things, which is optimistic about the company’s development in the medium and long term.

TCL explained that the major reasons for the significant year-on-year growth in revenue and profit were the significant year-on-year growth of the company’s semiconductor display business shipment area, the average price of major products and product profitability, and the optimization of the business mix and customer structure further enhanced the contribution of product revenue.

“There are two main reasons for the ideal performance of domestic display panel enterprises.” A color TV industry analyst believes that, on the one hand, under the effect of the epidemic, the demand for color TV and other electronic products surges, and the upstream raw materials are in shortage, which leads to the short supply of the panel industry, the price rises, and the corporate profits increase accordingly. In addition, as Samsung and LG, the two-panel giants, gradually withdrew from the LCD panel field, they put most of their energy and funds into the OLED(organic light-emitting diode) display panel industry, resulting in a serious shortage of LCD display panels, which objectively benefited China’s local LCD display panel manufacturers such as BOE and TCL China Star Optoelectronics.

Liu Yushi analyzed to reporters that relevant TV panel enterprises made outstanding achievements in 2021, and panel price rise is a very important contributing factor. In addition, three enterprises, such as BOE(BOE), CSOT(TCL China Star Optoelectronics) and HKC(Huike), accounted for 55% of the total shipments of LCD TV panels in 2021. It will be further raised to 60% in the first quarter of 2022. In other words, “simultaneous release of production capacity, expand market share, rising volume and price” is also one of the main reasons for the growth of these enterprises. However, entering the low demand in 2022, LCD TV panel prices continue to fall, and there is some uncertainty about whether the relevant panel companies can continue to grow.

According to Media data, in February this year, the monthly revenue of global large LCD panels has been a double decline of 6.80% month-on-month and 6.18% year-on-year, reaching $6.089 billion. Among them, TCL China Star and AU large-size LCD panel revenue maintained year-on-year growth, while BOE, Innolux, and LG large-size LCD panel monthly revenue decreased by 16.83%, 14.10%, and 5.51% respectively.

Throughout Q1, according to WitsView data, the average LCD TV panel price has been close to or below the average cost, and cash cost level, among which 32-inch LCD TV panel prices are 4.03% and 5.06% below cash cost, respectively; The prices of 43 and 65 inch LCD TV panels are only 0.46% and 3.42% higher than the cash cost, respectively.

The market decline trend is continuing, the reporter queried Omdia, WitsView, Sigmaintel(group intelligence consulting), Oviriwo, CINNO Research, and other institutions regarding the latest forecast data, the analysis results show that the price of the TV LCD panels is expected to continue to decline in April. According to CINNO Research, for example, prices for 32 -, 43 – and 55-inch LCD TV panels in April are expected to fall $1- $3 per screen from March to $37, $65, and $100, respectively. Prices of 65 – and 75-inch LCD TV panels will drop by $8 per screen to $152 and $242, respectively.

“In the face of weak overall demand, major end brands requested panel factories to reduce purchase volumes in March due to high inventory pressure, which led to the continued decline in panel prices in April.” Beijing Di Xian Information Consulting Co., LTD. Vice general manager Yi Xianjing so analysis said.

“Since 2021, international logistics capacity continues to be tight, international customers have a long delivery cycle, some orders in the second half of the year were transferred to the first half of the year, pushing up the panel price in the first half of the year but also overdraft the demand in the second half of the year, resulting in the panel price began to decline from June last year,” Liu Yush told reporters, and the situation between Russia and Ukraine has suddenly escalated this year. It also further affected the recovery of demand in Europe, thus prolonging the downward trend in prices. Based on the current situation, Liu predicted that the bottom of TV panel prices will come in June 2022, but the inflection point will be delayed if further factors affect global demand and lead to additional cuts by brands.

With the price of TV panels falling to the cash cost line, in Liu’s opinion, some overseas production capacity with old equipment and poor profitability will gradually cut production. The corresponding profits of mainland panel manufacturers will inevitably be affected. However, due to the advantages in scale and cost, there is no urgent need for mainland panel manufacturers to reduce the dynamic rate. It is estimated that Q2’s dynamic level is only 3%-4% lower than Q1’s. “We don’t have much room to switch production because the prices of IT panels are dropping rapidly.”

Ovirivo analysts also pointed out that the current TV panel factory shipment pressure and inventory pressure may increase. “In the first quarter, the production line activity rate is at a high level, and the panel factory has entered the stage of loss. If the capacity is not adjusted, the panel factory will face the pressure of further decline in panel prices and increased losses.”

In the first quarter of this year, the retail volume of China’s color TV market was 9.03 million units, down 8.8% year on year. Retail sales totaled 28 billion yuan, down 10.1 percent year on year. Under the situation of volume drop, the industry expects this year color TV manufacturers will also set off a new round of LCD display panel prices war.

THANK YOU FOR VISITING ENERGYTREND (HEREINAFTER REFERRED TO AS "THE WEBSITE"). THE WEBSITE, OWNED AND OPERATED BY TRENDFORCE CORP. (HEREINAFTER REFERRED TO AS "TRENDFORCE"), WILL COLLECT, HANDLE, AND USE PRIVATE USER DATA IN ACCORDANCE WITH THE PERSONAL INFORMATION PROTECTION LAW (HEREINAFTER "PERSONAL INFORMATION LAW") AND THE WEBSITE"S PRIVACY POLICY. THE WEBSITE AIMS TO RESPECT AND PROTECT ALL USERS" ONLINE PRIVACY RIGHTS. IN ORDER TO UNDERSTAND AS WELL AS PROTECT YOUR RIGHTS, PLEASE READ THE FOLLOWING TERMS CAREFULLY:

1.1. THE POLICY COVERS THE HANDLING OF THE PRIVATE INFORMATION EACH USER SHARES WITH TRENDFORCE WHILE VISITING OUR WEBSITES. IF A DIFFERENT PRIVATE POLICY HAS BEEN REFERED TO FOR SPECIFIC TRENDFORCE WEBSITES AND SERVICES, THAT POLICY WILL REPLACE OR SUPPLEMENT THE PRIVACY POLICY MENTIONED IN THIS DOCUMENT. THIS POLICY ALSO COVERS INDIVIDUALS LEGALLY RESIDING IN OR ORGANIZATIONS LEGALLY BASED IN MEMBER COUNTRIES OF THE EUROPEAN UNION (EU) AND ARE SUBJECTED TO EU GENERAL DATA PROTECTION REGULATION (GDPR) WITH REGARD TO PROVISION OF SERVICES AND PERSONAL DATA PROTECTION.

1.2. THIS POLICY IS NOT APPLICABLE TO EITHER COMPANIES OTHER THAN TRENDFORCE AND ITS SUBSIDIARIES OR PERSONNEL NOT EMPLOYED OR AUTHORIZED BY TRENDFORCE AND ITS SUBSIDIARIES.

2.4. THE WEBSITE COLLECTS TRANSACTION DATA BETWEEN YOU AND TRENDFORCE AND FROM RELEVANT BUSINESS PARTNERS. THESE INCLUDE SPECIFIC PRODUCTS AND SERVICES THAT ARE DIRECTLY OBTAINED FROM THE WEBSITE.

b. THIS WEBSITE WILL NOTIFY YOU ON MATTERS RELATED TO YOUR PERSONAL DATA BY EMAIL, OR TRENDFORCE CORP. WILL NOTIFY YOU BY OTHER MEANS (SUCH AS VIA TELEPHONE). CLIENTS ARE FULLY RESPONSIBLE FOR PROVIDING AN UPDATED, VALID, AND DELIVERABLE EMAIL ADDRESS THAT CAN RECEIVE NOTIFICATION EMAILS FROM TRENDFORCE CORP.

EXCEPT AS OTHERWISE EXPRESSEDLY PROVIDED BY GDPR OR ORDERED BY THE LAWS OF A COMPETENT JURISDICTION, CLIENTS CAN USE CUSTOMER EMAILServiceGDPR@energytrend.comTO CONTACT THIS WEBSITE TO EXERCISE THEIR RIGHTS PERTAINING TO THEIR ACCOUNT USER NAMES, ACCOUNT USER DATA, SESSION COOKIES, AND OTHER FORMS OF ACCOUNT DATA RECORDS. THESE RIGHTS INCLUDE RIGHT TO ACCESS, RIGHT TO RECTIFICATION, RIGHT TO BE FORGOTTEN/DATA ERASURE, RIGHT TO RESTRICTION OF PROCESSING, RIGHT OF DATA PORTABILITY, RIGHT TO OBJECT, AND ETC. TO EXERCISE THESE RIGHTS, A CLIENT MUST INCLUDE LEGALLY VALID AND VERIFICABLE PROOFS OF PERSONAL IDENITIFICATION ALONG WITH HIS/HER REQUEST. FURTHEMORE, THE CLIENT ISSUING THE REQUEST TO EXERCISE THESE RIGHTS MUST HAVE FUFILLED VARIOUS LEGAL OBLIGATIONS ON HIS/HER PART BEFOREHAND. AFTERWARDS, TRENDFORCE WILL FULFILL THE CLIENTS’ REQUEST/PROVIDE RESOLUTIONS WITHIN REASONABLE TIME AND EFFORT.

Browse Detailed TOC, Tables, and Figures with Charts which is spread across 111 Pages that provide exclusive data, information, vital statistics, trends, and competitive landscape details in this niche sector.

LCD TV Panel Market Size is projected to Reach Multimillion USD by 2027, In comparison to 2021, at unexpected CAGR during the Forecast Period 2022-2028.

Considering the economic change due to COVID-19 and Russia-Ukraine War Influence, LCD TV Panel accounted for % of the global market of LCD TV Panel in 2022.

This LCD TV Panel Market Report offers analysis and insights based on original consultations with important players such as CEOs, Managers, Department Heads of Suppliers, Manufacturers, Distributors, etc.

The Global LCD TV Panel Market is anticipated to rise at a considerable rate during the forecast period, between 2022 and 2027. In 2021, the market is growing at a steady rate and with the rising adoption of strategies by key players, the market is expected to rise over the projected horizon.

LCD displays utilize two sheets of polarizing material with a liquid crystal solution between them. An electric current passed through the liquid causes the crystals to align so that light cannot pass through them. Each crystal, therefore, is like a shutter, either allowing light to pass through or blocking the light. LCD panel is the key components of LCD display. And the price trends of LCD panel directly affect the price of liquid crystal displays. LCD panel consists of several components: Glass substrate, drive electronics, polarizers, color filters etc. Only LCD panel applied for TV will be counted in this report

Samsung Display, LG Display, Innolux Crop and AUO captured the top four revenue share spots in the LCD TV Panel market in 2015. Samsung Display dominated with 22.11 percent revenue share, followed by LG Display with 19.72 percent revenue share and Innolux Crop Display with 19.30 percent revenue share.

The global LCD TV Panel market is valued at USD 51130 million in 2019. The market size will reach USD 59640 million by the end of 2026, growing at a CAGR of 2.2% during 2021-2026.

LCD TV Panel market is segmented by Size, and by Application. Players, stakeholders, and other participants in the global LCD TV Panel market will be able to gain the upper hand as they use the report as a powerful resource. The segmental analysis focuses on production capacity, revenue and forecast by Size and by Application for the period 2016-2027.

The report focuses on the LCD TV Panel market size, segment size (mainly covering product type, application, and geography), competitor landscape, recent status, and development trends. The report considers key geographic segments and describes all the favorable conditions driving the market growth.

Geographically, the Major Regions Covered in LCD TV Panel Market Report Are:To comprehend LCD TV Panel market dynamics across major global regions. ● North America(United States, Canada)

According to IMARC Group’s latest report, titled “TFT LCD Panel Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2022-2027”, the global TFT LCD panel market size reached US$ 157 Billion in 2021. Looking forward, IMARC Group expects the market to reach US$ 207.6 Billion by 2027, exhibiting a growth rate (CAGR) of 4.7% during 2022-2027.

A thin-film-transistor liquid-crystal display (TFT LCD) panel is a liquid crystal display that is generally attached to a thin film transistor. It is an energy-efficient product variant that offers a superior quality viewing experience without straining the eye. Additionally, it is lightweight, less prone to reflection and provides a wider viewing angle and sharp images. Consequently, it is generally utilized in the manufacturing of numerous electronic and handheld devices. Some of the commonly available TFT LCD panels in the market include twisted nematic, in-plane switching, advanced fringe field switching, patterned vertical alignment and an advanced super view.

The global market is primarily driven by continual technological advancements in the display technology. This is supported by the introduction of plasma enhanced chemical vapor deposition (PECVD) technology to manufacture TFT panels that offers uniform thickness and cracking resistance to the product. Along with this, the widespread adoption of the TFT LCD panels in the production of automobiles dashboards that provide high resolution and reliability to the driver is gaining prominence across the globe. Furthermore, the increasing demand for compact-sized display panels and 4K television variants are contributing to the market growth. Moreover, the rising penetration of electronic devices, such as smartphones, tablets and laptops among the masses, is creating a positive outlook for the market. Other factors, including inflating disposable incomes of the masses, changing lifestyle patterns, and increasing investments in research and development (R&D) activities, are further projected to drive the market growth.

The competitive landscape of the TFT LCD panel market has been studied in the report with the detailed profiles of the key players operating in the market.

According to TrendForce, LCD TV panel quotations bore the brunt of continuous downgrades in the purchase volume of TV brands and pricing for most panel sizes have fallen to record lows. Recently, it was announced that the 32-inch and 43-inch panels fell by approximately US$5~US$6 in early June, 55-inch panels fell approximately US$7, and 65-inch and 75-inch panels are also facing overcapacity pressure, down US$12 to US$14. In order to alleviate pressure caused by price decline and inventory, panel makers are successively planning to initiate more significant production control in 3Q22. According to TrendForce’s latest research, overall LCD TV panel production capacity in 3Q22 will be reduced by 12% compared with original planning.

As Chinese panel makers account for nearly 66% of TV panel shipments, BOE, CSOT, and HKC are industry leaders. When there is an imbalance in supply and demand, a focus on strategic direction is prioritized. According to TrendForce, TV panel production capacity of the three aforementioned companies in 3Q22 is expected to decrease by 15.8% compared with their original planning, and 2% compared with 2Q22. Taiwanese manufacturers account for nearly 20% of TV panel shipments so, under pressure from falling prices, allocation of production capacity is subject to dynamic adjustment. On the other hand, Korean factories have gradually shifted their focus to high-end products such as OLED, QDOLED, and QLED, and are backed by their own brands. However, in the face of continuing price drops, they too must maintain operations amenable to flexible production capacity adjustments.

TrendForce indicates, in order to reflect real demand, Chinese panel makers have successively reduced production capacity. However, facing a situation in which terminal demand has not improved, it may be difficult to reverse the decline of panel pricing in June. However, as TV sizes below 55 inches (inclusive) have fallen below their cash cost in May (which is seen as the last line of defense for panel makers) and is even flirting with the cost of materials, coupled with production capacity reduction from panel makers, the price of TV panels has a chance to bottom out at the end of June and be flat in July. However, demand for large sizes above 65 inches (inclusive) originates primarily from Korean brands. Due to weak terminal demand, TV brands revising their shipment targets for this year downward, and purchase volume in 3Q22 being significantly cut down, it is difficult to see a bottom for large-size panel pricing. TrendForce expects that, optimistically, this price decline may begin to dissipate month by month starting in June but supply has yet to reach equilibrium, so the price of large sizes above 65 inches (inclusive) will continue to decline in 3Q22.

TrendForce states, as panel makers plan to reduce production significantly, the price of TV panels below 55 inches (inclusive) is expected to remain flat in 3Q22. However, panel manufacturers cutting production in the traditional peak season also means that a disappointing 2H22 peak season is a foregone conclusion and it will not be easy for panel prices to reverse. However, it cannot be ruled out, as operating pressure grows, the number and scale of manufacturers participating in production reduction will expand further and it timeframe extended, enacting more effective suppression on the supply side, so as to accumulate greater momentum for a rebound in TV panel quotations.

For more information on reports and market data from TrendForce’s Department of Display Research, please click here, or email Ms. Vivie Liu from the Sales Department at vivieliu@trendforce.com

For additional insights from TrendForce analysts on the latest tech industry news, trends, and forecasts, please visit our blog at https://insider.trendforce.com/

According to TrendForce research, terminal demand remains weak due to repercussions of the Russian-Ukrainian war, rising inflation, and China"s pandemic lockdowns as monitor brands began to reduce purchasing of LCD monitor panels in 2Q22. LCD monitors panel shipments in 2Q22 are estimated at 42.5 million units, down 11.3% QoQ.

According to TrendForce analysis, monitor brands set fairly high shipment targets in early 2022. Coupled with the impact of LCD monitor panel shortages in 2021, monitor brands gravitated towards overbuying panels in 1Q22 to prepare for ensuing shipments. Driven by strong demand from monitor brands, shipments of LCD monitor panels reached 47.9 million units in 1Q22, up 20% YoY, the highest level for the period since 2012.

However, due to changes in the international political and economic landscape in February this year, the market for consumer models has cooled and monitor brands have successively revised their LCD monitor shipment targets downward and simultaneously lowered their panel purchase volumes. In the face of interest rate hikes by the world"s major central banks and slowing economic growth, companies have also begun exercising caution in terms of capital expenditures, which has slowed demand for business-grade LCD monitors. In the past, inventory issues emerged and the overall market became oversupplied when monitor brands overstocked as consumer and business demand gradually cooled.

In addition, shipping and port congestion gradually eased in 1H22. The LCD monitors that were still in transit and accumulating in ports gradually arrived at distributors, resulting in a sharp rise in distribution inventory. Faced with the dual pressure of high whole LCD monitor and panel inventory, monitor brands were forced to reduce panel purchases in 2H22. Therefore, TrendForce forecasts that LCD monitor panel shipments will continue to decline to 37.8 million units in 3Q22, representing a QoQ decline of 11.2%. In 4Q22, there is a chance shipments will rebound marginally to 38.8 million units due to the sales surge initiated by monitor brands at the end of the year, representing a quarterly increase of 2.8%. Annual shipments are forecast to reach 167 million units, a drop of 3.6% YoY.

For more information on reports and market data from TrendForce’s Department of Display Research, please click here, or email Ms. Vivie Liu from the Sales Department at vivieliu@trendforce.com

For additional insights from TrendForce analysts on the latest tech industry news, trends, and forecasts, please visit our blog at https://insider.trendforce.com/

In a series of 2021 predictions in a report from Bob O’Brien of the Digital Supply Chain (DSCC) he suggests that LCD television panel prices will remain higher in 2021 than in 2020 at least until Q4 this year.

O’Brien says: “2020 started with panel prices rising after Samsung and LGD announced that they would shut down LCD capacity to shift to OLED. Then the pandemic hit and led to panicked price reductions as everyone feared a global recession, until it became clear that stay-at-home orders and lockdowns resulted in increased demand for TVs. Prices started to increase in June, slowly at first and then accelerating in Q4 to end the year up more than 50 per cent.”

“While Q1 would normally be the beginning of a seasonal slowdown for TV demand, we do not expect that panel prices will decline because of fears of a glass shortage resulting from a power outage at NEG coupled with Gen 10.5 glass problems at Corning. By the end of Q1, though, glass supply will be restored and the seasonal falloff in demand in the spring and summer months will lead panel prices to fall,” he added.

“The big increases in LCD TV panel prices have led Samsung and LG Display to change their plans and extend the life of LCD lines. These companies are making the sensible decision that they should continue to run lines that bring in cash, but the spectre of shutdown will remain hanging over the industry. Although prices will fall, they will remain above 2020 levels through the summer and panel prices are likely to stabilize in the 2nd half of 2021 at levels substantially higher than their all-time lows of Q2 2020.”

He also adds that this time last year saw most observers suggesting – and anticipating – that LCD displays were ‘old technology’ and investment in LCD output would slow. “The two Korean panel makers, who once dominated the LCD industry, announced that they were withdrawing from LCD to focus on OLED. Investment in China increasingly focused on OLED. During 2020, it became increasingly clear that this assessment was premature, and LCD has a lot of life left. Strong demand led to panel price increases, which greatly improved the profitability of LCD makers. Furthermore, LG’s struggles with manufacturing its White OLEDs in Guangzhou, and many panel makers’ struggles with increasing yields on OLED smartphone panels, reminded the industry that OLED is difficult to make and substantially higher cost than LCD. Finally, the emergence of MiniLED backlight technology provided the incumbent LCD technology with a performance champion to challenge OLED.”

O’Brien says that the South Korean’s have reversed their slowdown plans, or at least delayed closing LCD fabrications plants. “This will help to keep supply/demand in balance for 2021, after the Q1 glass shortage is alleviated. However, capacity additions for OLED fall short of the ~5 per cent per year area growth in demand that we expect, and LCD will be in increasingly tight supply unless new capacity is added.”

LCD TV Panel Market is 2022 Research Report on Global professional and comprehensive report on the LCD TV Panel Market. The report monitors the key trends and market drivers in the current scenario and offers on the ground insights. Top Key Players are – Samsung Display, LG Display, Innolux Crop., AUO, CSOT, BOE, Sharp, Panasonic, CEC-Panda.

Global “LCD TV Panel Market” (2022-2028) the report additionally centers around worldwide significant makers of the LCD TV Panel market with important data, such as, company profiles, segmentation information, challenges and limitations, driving factors, value, cost, income and contact data. Upstream primitive materials and hardware, coupled with downstream request examination is likewise completed. The Global LCD TV Panel market improvement patterns and marketing channels are breaking down. In conclusion, the attainability of new speculation ventures is surveyed and in general, the research ends advertised.

Global LCD TV Panel Market Report 2022 is spread across 117 pages and provides exclusive vital statistics, data, information, trends and competitive landscape details in this niche sector.

The information for each competitor includes – Company Profile, Main Business Information, SWOT Analysis, Sales, Revenue, Price and Gross Margin, Market Share.

LCD displays utilize two sheets of polarizing material with a liquid crystal solution between them. An electric current passed through the liquid causes the crystals to align so that light cannot pass through them. Each crystal, therefore, is like a shutter, either allowing light to pass through or blocking the light. LCD panel is the key components of LCD display. And the price trends of LCD panel directly affect the price of liquid crystal displays. LCD panel consists of several components: Glass substrate, drive electronics, polarizers, color filters etc. Only LCD panel applied for TV will be counted in this report.

Due to the COVID-19 pandemic, the global LCD TV Panel market size is estimated to be worth USD 53490 million in 2021 and is forecast to a readjusted size of USD 53490 million by 2028 with a CAGR of 2.2% during the review period. Fully considering the economic change by this health crisis, by Size accounting for (%) of the LCD TV Panel global market in 2021, is projected to value USD million by 2028, growing at a revised (%) CAGR in the post-COVID-19 period. While by Size segment is altered to an (%) CAGR throughout this forecast period.

Global LCD TV Panel key players include Samsung Display, LG Display, Innolux Crop, AUO, CSOT, etc. Global top five manufacturers hold a share over 80%.

The global LCD TV Panel market is segmented by company, region (country), by Size and by Application. Players, stakeholders, and other participants in the global LCD TV Panel market will be able to gain the upper hand as they use the report as a powerful resource. The segmental analysis focuses on sales, revenue and forecast by region (country), by Size and by Application for the period 2017-2028.

Global LCD TV Panel market analysis and market size information is provided by regions (countries). Segment by Application, the LCD TV Panel market is segmented into United States, Europe, China, Japan, Southeast Asia, India and Rest of World. The report includes region-wise LCD TV Panel market forecast period from history 2017-2028. It also includes market size and forecast by players, by Type, and by Application segment in terms of sales and revenue for the period 2017-2028.

The report introduced the LCD TV Panel basics: definitions, classifications, applications and market overview; product specifications; manufacturing processes; cost structures, raw materials and so on. Then it analyzed the world’s main region market conditions, including the product price, profit, capacity, production, supply, demand and market growth rate and forecast etc. In the end, the report introduced new project SWOT analysis, investment feasibility analysis, and investment return analysis.

LCD TV Panel market size competitive landscape provides details and data information by players. The report offers comprehensive analysis and accurate statistics on revenue by the player for the period 2017-2021. It also offers detailed analysis supported by reliable statistics on revenue (global and regional level) by players for the period 2017-2021. Details included are company description, major business, company total revenue and the sales, revenue generated in LCD TV Panel business, the date to enter into the LCD TV Panel market, LCD TV Panel product introduction, recent developments, etc.

The report offers detailed coverage of LCD TV Panel industry and main market trends with impact of coronavirus. The market research includes historical and forecast market data, demand, application details, price trends, and company shares of the leading LCD TV Panel by geography. The report splits the market size, by volume and value, on the basis of application type and geography. Report covers the present status and the future prospects of the global LCD TV Panel market for 2017-2028.

Global LCD TV Panel Market report forecast to 2028 is a professional and comprehensive research report on the world’s major regional market conditions, focusing on the main regions (North America, Europe and Asia-Pacific) and the main countries (United States, Germany, United Kingdom, Japan, South Korea and China).

To Know How COVID-19 Pandemic Will Impact LCD TV Panel Market/Industry- Request a sample copy of the report-https://www.researchreportsworld.com/enquiry/request-covid19/21019731

The report offers exhaustive assessment of different region-wise and country-wise LCD TV Panel market such as U.S., Canada, Germany, France, U.K., Italy, Russia, China, Japan, South Korea, India, Australia, Taiwan, Indonesia, Thailand, Malaysia, Philippines, Vietnam, Mexico, Brazil, Turkey, Saudi Arabia, U.A.E, etc. Key regions covered in the report are North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

For the period 2017-2028, the report provides country-wise revenue and volume sales analysis and region-wise revenue and volume analysis of the global LCD TV Panel market. For the period 2017-2021, it provides sales (consumption) analysis and forecast of different regional markets by Application as well as by Type in terms of volume.

What are the market opportunities and threats faced by the vendors in the global LCD TV Panel market? What industrial trends, drivers, and challenges are manipulating its growth?

With tables and figures helping analyze worldwide Global LCD TV Panel market trends, this research provides key statistics on the state of the industry and is a valuable source of guidance and direction for companies and individuals interested in the market.

Strong demand for LCD products combined with concerns about shortages in key components have driven LCD TV panel prices to their most significant increases ever on a percentage basis, and prices show no signs of slowing down in Q2. In our last update in early April, we anticipated that price increases would decelerate in Q2, but we now see price increases accelerating compared to Q1. Panel prices increased by 27% in Q4 2020 compared to Q3 and slowed down to 14.5% in Q1 2021 compared to Q4, but our current estimate is that average LCD TV panel prices in Q2 2021 will increase by another 17%. We now expect prices to peak sometime in Q3 2021.

In 2021, LCD panel prices are expected to climb in 1Q, remain flat in 2Q, and decline from 3Q. Backed by ongoing facility expansions, Chinese LCD panel makers should see a continuing rise in M/S. In addition, a recent blackout at the Japanese factory of NEG, a glass substrate maker, should also benefit Chinese firms.

LCD panel prices, which ended high in 2020, are expected to continue rising in 1Q21 on an anticipated decrease in glass substrate supply. On Dec 10, a power outage occurred at NEG’s Takatsuki plant in Japan. With normalization at the Takatsuki plant expected in 1Q21, domestic and Taiwanese panel makers’ sourcing of glass substrate is unlikely to proceed smoothly in the near future. In 2Q21, an acceleration in panel production alongside normalized supply of glass substrate should prevent LCD panel price growth. The rate of glass substrate supply excess is forecast to widen from 0.5% in 1Q21 to 3.6% in 2Q21.

LCD panel prices are forecast to decline from 3Q21, as supply should exceed demand. We expect supply excess for LCD panels to reach 3.2% in 3Q21 and 3.4% in 4Q21 on the back of ongoing production expansion at Chinese manufacturers.

Chinese LCD panel makers are to continue expanding their production capacity, centering on 8G-and-above facilities, in a bid to increase M/S. Given Korea’s withdrawal from the LCD arena, we expect the global number of LCD production facilities (8G or higher) to fall from 32 in 2020 to 31 in 2021 to 30 in 2022. On the other hand, with Chinese panel makers ramping up investment, the portion of Chinese manufacturers is to increase from 63% in 2020 to 68% in 2021 to 78% in 2022, with China coming to claim a market-leading position.

Of note, Chinese panel makers are highly likely to see M/S expansion in 1Q21, as they are insulated from the effects of NEG’s Takatsuki power outage. Chinese companies’ glass substrate supply chain has diversified to encompass Corning, AGC, and NEG (China, Xiamen plant).

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey