lcd panel price trend 2021 made in china

The price of LCD display panels for TVs is still falling in November and is on the verge of falling back to the level at which it initially rose two years ago (in June 2020). Liu Yushi, a senior analyst at CINNO Research, told China State Grid reporters that the wave of “falling tide” may last until June this year. For related panel companies, after the performance surge in the past year, they will face pressure in 2022.

LCD display panel prices for TVs will remain at a high level throughout 2021 due to the high base of 13 consecutive months of increase, although the price of LCD display panels peaked in June last year and began to decline rapidly. Thanks to this, under the tight demand related to panel enterprises last year achieved substantial profit growth.

According to China State Grid, the annual revenue growth of major LCD display panel manufacturers in China (Shentianma A, TCL Technology, Peking Oriental A, Caihong Shares, Longteng Optoelectronics, AU, Inolux Optoelectronics, Hanyu Color Crystal) in 2021 is basically above double digits, and the net profit growth is also very obvious. Some small and medium-sized enterprises directly turn losses into profits. Leading enterprises such as BOE and TCL Technology more than doubled their net profit.

Take BOE as an example. According to the 2021 financial report released by BOE A, BOE achieved annual revenue of 219.31 billion yuan, with a year-on-year growth of 61.79%; Net profit attributable to shareholders of listed companies reached 25.831 billion yuan, up 412.96% year on year. “The growth is mainly due to the overall high economic performance of the panel industry throughout the year, and the acquisition of the CLP Panda Nanjing and Chengdu lines,” said Xu Tao, chief electronics analyst at Citic Securities.

In his opinion, as BOE dynamically optimizes its product structure, and its flexible OLED continues to enter the supply chain of major customers, BOE‘s market share as the panel leader is expected to increase further and extend to the Internet of Things, which is optimistic about the company’s development in the medium and long term.

TCL explained that the major reasons for the significant year-on-year growth in revenue and profit were the significant year-on-year growth of the company’s semiconductor display business shipment area, the average price of major products and product profitability, and the optimization of the business mix and customer structure further enhanced the contribution of product revenue.

“There are two main reasons for the ideal performance of domestic display panel enterprises.” A color TV industry analyst believes that, on the one hand, under the effect of the epidemic, the demand for color TV and other electronic products surges, and the upstream raw materials are in shortage, which leads to the short supply of the panel industry, the price rises, and the corporate profits increase accordingly. In addition, as Samsung and LG, the two-panel giants, gradually withdrew from the LCD panel field, they put most of their energy and funds into the OLED(organic light-emitting diode) display panel industry, resulting in a serious shortage of LCD display panels, which objectively benefited China’s local LCD display panel manufacturers such as BOE and TCL China Star Optoelectronics.

Liu Yushi analyzed to reporters that relevant TV panel enterprises made outstanding achievements in 2021, and panel price rise is a very important contributing factor. In addition, three enterprises, such as BOE(BOE), CSOT(TCL China Star Optoelectronics) and HKC(Huike), accounted for 55% of the total shipments of LCD TV panels in 2021. It will be further raised to 60% in the first quarter of 2022. In other words, “simultaneous release of production capacity, expand market share, rising volume and price” is also one of the main reasons for the growth of these enterprises. However, entering the low demand in 2022, LCD TV panel prices continue to fall, and there is some uncertainty about whether the relevant panel companies can continue to grow.

According to Media data, in February this year, the monthly revenue of global large LCD panels has been a double decline of 6.80% month-on-month and 6.18% year-on-year, reaching $6.089 billion. Among them, TCL China Star and AU large-size LCD panel revenue maintained year-on-year growth, while BOE, Innolux, and LG large-size LCD panel monthly revenue decreased by 16.83%, 14.10%, and 5.51% respectively.

Throughout Q1, according to WitsView data, the average LCD TV panel price has been close to or below the average cost, and cash cost level, among which 32-inch LCD TV panel prices are 4.03% and 5.06% below cash cost, respectively; The prices of 43 and 65 inch LCD TV panels are only 0.46% and 3.42% higher than the cash cost, respectively.

The market decline trend is continuing, the reporter queried Omdia, WitsView, Sigmaintel(group intelligence consulting), Oviriwo, CINNO Research, and other institutions regarding the latest forecast data, the analysis results show that the price of the TV LCD panels is expected to continue to decline in April. According to CINNO Research, for example, prices for 32 -, 43 – and 55-inch LCD TV panels in April are expected to fall $1- $3 per screen from March to $37, $65, and $100, respectively. Prices of 65 – and 75-inch LCD TV panels will drop by $8 per screen to $152 and $242, respectively.

“In the face of weak overall demand, major end brands requested panel factories to reduce purchase volumes in March due to high inventory pressure, which led to the continued decline in panel prices in April.” Beijing Di Xian Information Consulting Co., LTD. Vice general manager Yi Xianjing so analysis said.

“Since 2021, international logistics capacity continues to be tight, international customers have a long delivery cycle, some orders in the second half of the year were transferred to the first half of the year, pushing up the panel price in the first half of the year but also overdraft the demand in the second half of the year, resulting in the panel price began to decline from June last year,” Liu Yush told reporters, and the situation between Russia and Ukraine has suddenly escalated this year. It also further affected the recovery of demand in Europe, thus prolonging the downward trend in prices. Based on the current situation, Liu predicted that the bottom of TV panel prices will come in June 2022, but the inflection point will be delayed if further factors affect global demand and lead to additional cuts by brands.

With the price of TV panels falling to the cash cost line, in Liu’s opinion, some overseas production capacity with old equipment and poor profitability will gradually cut production. The corresponding profits of mainland panel manufacturers will inevitably be affected. However, due to the advantages in scale and cost, there is no urgent need for mainland panel manufacturers to reduce the dynamic rate. It is estimated that Q2’s dynamic level is only 3%-4% lower than Q1’s. “We don’t have much room to switch production because the prices of IT panels are dropping rapidly.”

Ovirivo analysts also pointed out that the current TV panel factory shipment pressure and inventory pressure may increase. “In the first quarter, the production line activity rate is at a high level, and the panel factory has entered the stage of loss. If the capacity is not adjusted, the panel factory will face the pressure of further decline in panel prices and increased losses.”

In the first quarter of this year, the retail volume of China’s color TV market was 9.03 million units, down 8.8% year on year. Retail sales totaled 28 billion yuan, down 10.1 percent year on year. Under the situation of volume drop, the industry expects this year color TV manufacturers will also set off a new round of LCD display panel prices war.

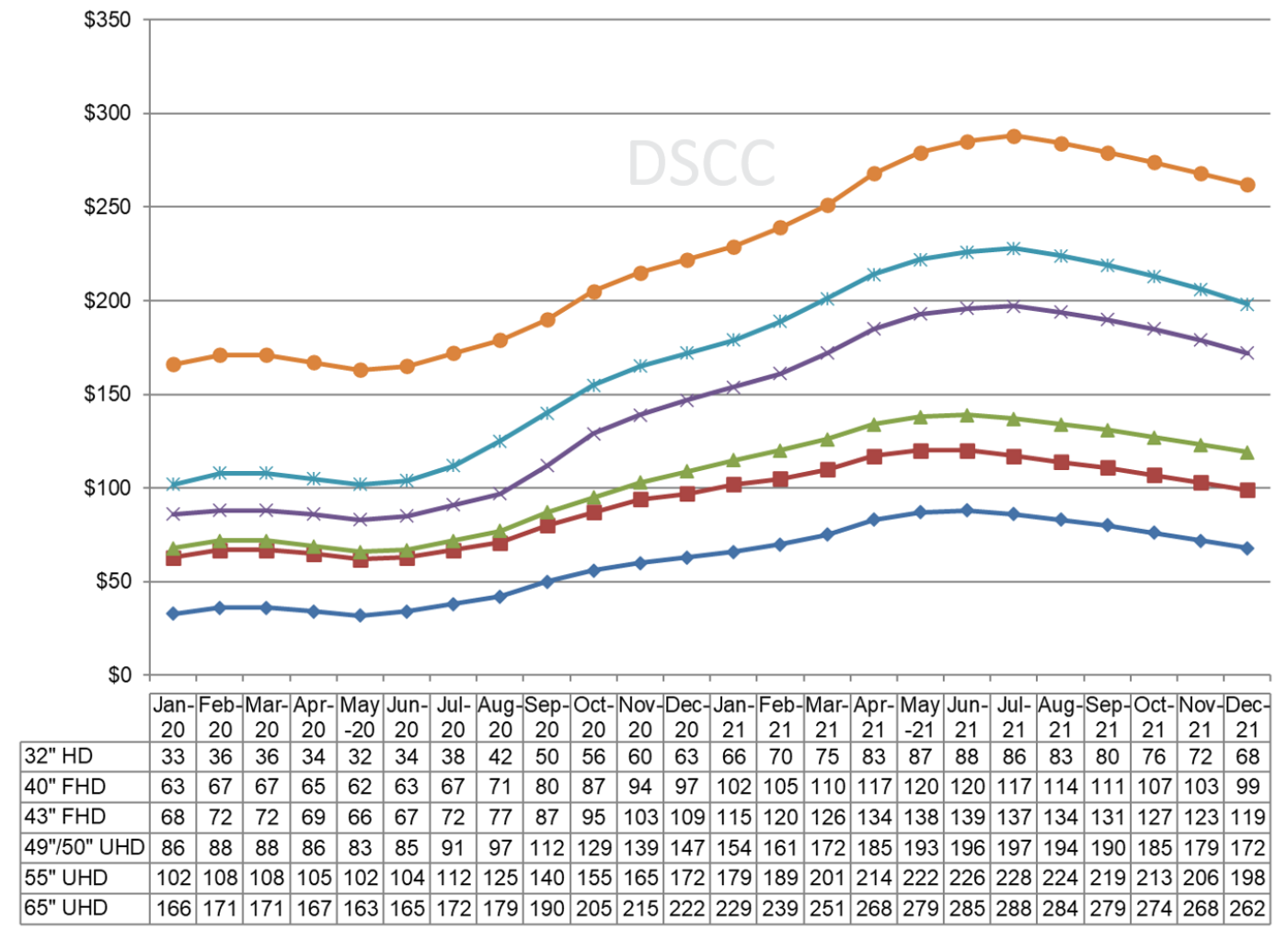

Prices for all TV panel sizes fluctuated and are forecast to fluctuate between 2020 and 2022. The period from March 2020 to July 2021 saw the biggest price increases, when a 65" UHD panel cost between 171 and 288 U.S. dollars. In the fourth quarter of 2021, such prices fell and are expected to drop to an even lower amount by March 2022.Read moreLCD TV panel prices worldwide from January 2020 to March 2022, by size(in U.S. dollars)Characteristic32" HD43" FHD49"/50" UHD55" UHD65" UHD------

DSCC. (January 10, 2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) [Graph]. In Statista. Retrieved February 08, 2023, from https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars)." Chart. January 10, 2022. Statista. Accessed February 08, 2023. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. (2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars). Statista. Statista Inc.. Accessed: February 08, 2023. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "Lcd Tv Panel Prices Worldwide from January 2020 to March 2022, by Size (in U.S. Dollars)." Statista, Statista Inc., 10 Jan 2022, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC, LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) Statista, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/ (last visited February 08, 2023)

LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) [Graph], DSCC, January 10, 2022. [Online]. Available: https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

In 2021, LCD panel prices are expected to climb in 1Q, remain flat in 2Q, and decline from 3Q. Backed by ongoing facility expansions, Chinese LCD panel makers should see a continuing rise in M/S. In addition, a recent blackout at the Japanese factory of NEG, a glass substrate maker, should also benefit Chinese firms.

LCD panel prices, which ended high in 2020, are expected to continue rising in 1Q21 on an anticipated decrease in glass substrate supply. On Dec 10, a power outage occurred at NEG’s Takatsuki plant in Japan. With normalization at the Takatsuki plant expected in 1Q21, domestic and Taiwanese panel makers’ sourcing of glass substrate is unlikely to proceed smoothly in the near future. In 2Q21, an acceleration in panel production alongside normalized supply of glass substrate should prevent LCD panel price growth. The rate of glass substrate supply excess is forecast to widen from 0.5% in 1Q21 to 3.6% in 2Q21.

LCD panel prices are forecast to decline from 3Q21, as supply should exceed demand. We expect supply excess for LCD panels to reach 3.2% in 3Q21 and 3.4% in 4Q21 on the back of ongoing production expansion at Chinese manufacturers.

Chinese LCD panel makers are to continue expanding their production capacity, centering on 8G-and-above facilities, in a bid to increase M/S. Given Korea’s withdrawal from the LCD arena, we expect the global number of LCD production facilities (8G or higher) to fall from 32 in 2020 to 31 in 2021 to 30 in 2022. On the other hand, with Chinese panel makers ramping up investment, the portion of Chinese manufacturers is to increase from 63% in 2020 to 68% in 2021 to 78% in 2022, with China coming to claim a market-leading position.

Of note, Chinese panel makers are highly likely to see M/S expansion in 1Q21, as they are insulated from the effects of NEG’s Takatsuki power outage. Chinese companies’ glass substrate supply chain has diversified to encompass Corning, AGC, and NEG (China, Xiamen plant).

Data from China Optics and Optoelectronics Manufactures Association Liquid Crystal Branch (CODA) shows that in 2021, the output value of China"s display industry was about 586.8 billion yuan (about $84.05 billion), nearly eight times higher than 10 years ago while delivered display panels totaled about 160 million square meters, more than seven times that of a decade ago.

According to CODA, China"s proportion of industry scale and display panel delivered area in the global market has increased to 36.9 percent and 63.3 percent respectively, ranking first in the world.

Statistics show that in the third quarter of 2022, the market share of OLED panels for domestic smart phones accounted for 30 percent of the global market, an increase of 10 percent over the same period last year.

Chinese manufacturers are expected to raise their market share from 39% this year to 52% next year in the monitor panel market, and 36% to 39% in the notebook panel market

Chinese manufacturers are expected to raise their market share from 39% this year to 52% next year in the monitor panel market, and 36% to 39% in the notebook panel market, according to TrendForce’s preliminary shipment forecast of panel makers for 2021. As such, these manufacturers are expected to maintain their plans of transitioning some production capacities from TV panel manufacturing to IT panel manufacturing in spite of the TV panel shortage in 2H20 caused by various factors such as the closedown of SDC’s LCD panel manufacturing operations, the rise of the stay-at-home economy, and the stimulus policies instituted by governments worldwide.

TrendForce indicates that, with regards to the standing of Chinese manufacturers in the IT panel industry, BOE has long established itself as the market leader, while CSOT and HKC are each also catching up fast. After acquiring SDC’s Suzhou-based Gen 8.5 fab, CSOT will possess even more production capacities for monitor panels. At the same time, HKC currently maintains three Gen 8.6 fabs, located in Chongqing, Chuzhou, and Mianyang, and plans to capture additional shares in the monitor panel and notebook panel markets.

Chinese panel makers have been gradually transitioning their current panel capacities to monitor panel production. Most significantly, as more Gen 10.5 production lines become available, TV panel production will most likely take place in Gen 10.5 fabs instead of Gen 8.5 fabs in the future, while the existing Gen 8.5 and Gen 8.6 production lines will be reallocated to monitor panel production in order to expend the excess capacity made available after TV panel production moves to Gen 10.5 fabs. In addition, after SDC’s forecasted closing of LCD panel manufacturing operations at the end of this year, CSOT and HKC will look to capture the resultant supply share of SDC’s absence in the market. On the other hand, since both TCL, which is CSOT’s parent company, and HKC possess monitor ODM operations, should the two companies decide to vertically integrate by making panels for their own monitor products, they will be able to effectively optimize their cost structures.

Although CSOT’s Wuhan-based T3 LTPS Gen 6 production line is primarily dedicated to smartphone and notebook panel manufacturing, the considerable reduction of LTPS smartphone panel demand from Huawei caused by U.S. sanctions means CSOT is expected to make plans for an increase in notebook panel shipment in order to make up for the shortfall. As well, thanks to high demand for TV panels this year, HKC’s production lines have been operating at maximum capacity utilization rates, in turn slowing down its notebook panel business. However, in light of the fact that the COVID-19 pandemic has brought about a rapid surge in TN notebook panel demand, HKC is therefore looking to TN panels as a new commercial opportunity in the notebook display market and subsequently prioritizing TN panel development over IPS panel development as its product strategy. Not only will this reprioritization allow HKC to align its strategy with the current market trend, but it will also quickly raise the yield rate of HKC’s Mianyang-based fab, which had never manufactured NB panels, by instead having the fab manufacture TN panels, which have a relatively simpler manufacturing process.

TrendForce analyst Jeff Yang indicates that, despite Chinese panel makers’ strong intention to enter the IT panel manufacturing business, success in the IT panel market is not solely decided by a company’s production capacity. For instance, with regards to monitor panels, CSOT’s technical competency is mostly focused on VA panels, meaning the company is constrained in its product mixes due to its lack of mainstream IPS offerings. Although HKC is equipped with both IPS and VA technologies, it lacks experience in manufacturing curved VA panels, leading its clients to take on a wait-and-see approach before placing additional orders. For notebook panels, although CSOT is primarily focusing on the mid-range and high-end LTPS notebook panel market, it faces intense competition from Samsung’s OLED notebook panels, which are gradually extending from the high-end segment to the mid-range segment as well. Likewise, HKC will have to take time in order to make headways in the notebook panel market, since it has not reached any production milestones, and it requires time to cultivate a significant client base.

Large LCD panel prices have been continuously increasing for last 10 months due to an increase in demand and tight supply. This has helped the LCD industry to recover from drastic panel price reductions, revenue and profit loss in 2019. It has also contributed to the growth of Quantum Dot and MiniLED LCD TV.

Strong LCD TV panel demand is expected to continue in 2021, but component shortages, supply constraints and very high panel price increase can still create uncertainties.

LCD TV panel capacity increased substantially in 2019 due to the expansion in the number of Gen 10.5 fabs. After growth in 2018, LCD TV demand weakened in 2019 caused by slower economic growth, trade war and tariff rate increases. Capacity expansion and higher production combined with weaker demand resulted in considerable oversupply of LCD TV panels in 2019 leading to drastic panel price reductions. Some panel prices went below cash cost, forcing suppliers to cut production and delay expansion plans to reduce losses.

Panel over-supply also brought down panel prices to way lower level than what was possible through cost improvement. Massive 10.5 Gen capacity that can produce 8-up 65" and 6-up 75" panels from a single mother glass substrate helped to reduce larger size LCD TV panel costs. Also extremely low panel price in 2019 helped TV brands to offer larger size LCD TV (>60-inch size) with better specs and technology (Quantum Dot & MiniLED) at more competitive prices, driving higher shipments and adoption rates in 2019 and 2020.

While WOLED TV had higher shipment share in 2018, Quantum Dot and MiniLED based LCD TV gained higher unit shares both in 2019 and 2020 according to Omdia published data. This trend is expected to continue in 2021 and in the next few years with more proliferation of Quantum Dot and MiniLED TVs.

Panel suppliers’ financial results suffered in 2019 as they lost money. Suppliers from China, Korea and Taiwan all lowered their utilization rates in the second half of 2019 to reduce over-supply. Very low prices combined with lower utilization rates made the revenue and profitability situation for panel suppliers difficult in 2019. BOE and China Star cut the utilization rates of their Gen 10.5 fabs. Sharp delayed the start of production at its 10.5 Gen fab in China. LGD and Samsung display decided to shift away from LCD more towards OLED and QDOLED respectively. Both companies cut utilization rates in their 7, 7.5 and 8.5 Gen fabs. Taiwanese suppliers also cut their 8.5 Gen fab utilization rates.

Some suppliers also shifted capacity away from TV to other applications. In summary, drastic price reduction resulted in a cut in utilization rates, delays in fab construction and ramp-ups and the closing down of older fabs, or conversion to OLED or QDOLED fabs. This helped to reduce oversupply.

An increase in demand for larger size TVs in the second half of 2020 combined with component shortages has pushed the market to supply constraint and caused continuous panel price increases from June 2020 to March 2021. Market demand for tablets, notebooks, monitors and TVs increased in 2020 especially in the second half of the year due to the impact of "stay at home" regulations, when work from home, education from home and more focus on home entertainment pushed the demand to higher level.

With stay at home continuing in the firts half of 2021 and expected UEFA Europe football tournaments and the Olympic in Japan (July 23), TV brands are expecting stronger demand in 2021. The panel price increase resulting in higher costs for TV brands. It has also made it difficult for lower priced brands (Tier2/3) to acquire enough panels to offer lower priced TVs. Further, panel suppliers are giving priority to top brands with larger orders during supply constraint. In recent quarters, the top five TV brands including Samsung, LG, and TCL have been gaining higher market share.

From June 2020 to January 2021, the 32" TV panel price has increased more than 100%, whereas 55" TV panel prices have increased more than 75% and the 65" TV panel price has increased more than 38% on average according to DSCC data. Panel prices continued to increase through Q1 and the trend is expected to continue in Q2 2021 due to component shortages.

In last few months top glass suppliers Corning, NEG and AGC have all experienced production problems. A tank failure at Corning, a power outage at NEG and an accident at an AGC glass plant all resulted in glass supply constraints when demand and production has been increasing. In March this year Corning announced its plan to increase glass prices in Q2 2021. Corning has also increased supply by starting glass tank in Korea to supply China’s 10.5 Gen fabs that are ramping up. Most of the growth in capacity is coming from Gen 8.6 and Gen 10.5 fabs in China.

Besides glass there have been other component shortages including driver ICs and polarizers. Component shortages are expected to continue in the first half of 2021.

Major increases in panel prices from June 2020, have increased costs and reduced profits for TV brand manufacturers. TV brands are starting to increase TV set prices slowly in certain segments. Notebook brands are also planning to raise prices for new products to reflect increasing costs. Monitor prices are starting to increase in some segments. Despite this, buyers are still unable to fullfill orders due to supply issues.

TV panel prices increased in Q4 2020 and are also expected to increase in the first half of 2021. This can create challenges for brand manufacturers as it reduces their ability to offer more attractive prices in coming months to drive demand. Still, set-price increases up to March have been very mild and only in certain segments. Some brands are still offering price incentives to consumers in spite of the cost increases. For example, in the US market retailers cut prices of big screen LCD and OLED TV to entice basketball fans in March.

Higher LCD price and tight supply helped LCD suppliers to improve their financial performance in the second half of 2020. This caused a number of LCD suppliers especially in China to decide to expand production and increase their investment in 2021.

New opportunities for MiniLED based products that reduce the performance gap with OLED, enabling higher specs and higher prices are also driving higher investment in LCD production. Suppliers from China already have achieved a majority share of TFT-LCD capacity.

BOE has acquired Gen 8.5/8.6 fabs from CEC Panda. ChinaStar has acquired a Gen 8.5 fab in Suzhou from Samsung Display. Recent panel price increases have also resulted in Samsung and LGD delaying their plans to shut down LCD production. These developments can all help to improve supply in the second half of 2021. Fab utilization rates in Taiwan and China stayed high in the second half of 2020 and are expected to stay high in the first half of 2021.

Price increases for TV sets are still not widespread yet and increases do not reflect the full cost increase. However, if set prices continue to increase to even higher levels, there is the potential for an impact on demand.

QLED and MiniLED gained share in the premium TV market in 2019, impacting OLED shares and aided by low panel prices. With the LCD panel price increases in 2020 the cost gap between OLED TV and LCD has gone down in recent quarters.

OLED TV also gained higher market share in the premium TV market especially sets from LG and Sony in the last quarter of 2020, according to industry data. LG Display is implimenting major capacity expansion of its OLED TV panels with its Gen 8.5 fab in China.Strong sales in Q4 2020 and new product sizes such as 48-inch and 88-inch have helped LG Display’s OLED TV fabs to have higher utilization rates.

Samsung is also planning to start production of QDOLED in 2021. Higher production and cost reductions for OLED TV may help OLED to gain shares in the premium TV market if the price gap continues to reduce with LCD.

Lower tier brands are not able to offer aggressive prices due to the supply constraint and panel price increases. If these conditions continue for too long, TV demand could be impacted.

Strong LCD TV demand especially for Quantum Dot and MiniLED TV is expected to continue in 2021. The economic recovery and sports events (UEFA Europe footbal and the Olympics in Japan) are expected to drive demand for TV, but component shortages, supply constraints and too big a price increase could create uncertainties. Panel suppliers have to navigate a delicate balance of capacity management and panel prices to capture the opportunity for higher TV demand. (SD)

TrendForce’s latest research finds that TV brands’ promotional activities related to China’s Singles’ Day were helped by the steep decline in display panel prices. With panel prices reaching a very low level, TV brands were able to cut their prices further so as to raise shipments of whole TV sets during the promotional period. On the other hand, the major international brands have come into the second half of this year with a high level of inventory as their sales performances were weaker than expected during the first half. In order to effectively consume the existing inventory, TV brands have significantly corrected down the panel procurement quantity for 2H22. As a result, TrendForce now estimates that global TV shipments in 2H22 will reach 109 million units, reflecting a YoY decline of 2.7%. Global TV shipments during the whole 2022 are currently projected to total 202 million units, showing YoY decline of 3.9%. This annual shipment figure represents a decade low.

This year, the TV market has seen a continuous decline in shipments. Fortunately, there has also been a sharp drop in prices of large-sized panels. Furthermore, freight transportation costs have fallen by more than 50%. Thus, TV brands have been able to vigorously promote large-sized products, and the average size of TVs has also risen by 1.4 inches to 56 inches.

TrendForce further points out that moving into 2023, supply will remain fairly plentiful for TV panels. With the chance of a substantial rally in panel prices being extremely low, brands should feel an easing of cost pressure and have more flexibility when it comes to large-scale promotional activities. However, the IMF has downgraded its global economic growth forecast for 2023 to 2.7%. Moreover, the US, the Eurozone, and China as the world’s three largest regional economies will continue to experience stagnation. Regarding the ongoing inflation, it has recently started to ease a bit in Europe and the US, but the major regional consumer markets on the whole will continue be under its pressure. Because of these factors, TrendForce believes the growth momentum of TV shipments will be severely constrained next year. Global TV shipments are currently forecasted to again register a YoY decline for 2023, falling by 1.4% to 199 million units.

TV sales in China during this year have been noticeably affected by government measures for controlling local COVID-19 outbreaks. During this second half of the year, TV panel prices have fallen to a new record low, and brands have also been aggressively cutting prices so as to meet their annual shipments targets. However, despite all these, TV sales in China for the Singles’ Day period still fell nearly 10% YoY. Turning to the North America, TV sales there shrank by 16.5% YoY for 1H22 as the rapidly mounting inflationary pressure squeezed consumers’ budgets. Around that same time, TV brands also reached their limit in terms of inventory accumulation. To reduce the glut, brands conducted inventory check across all sections of their supply chains and made significant revisions to their procurement plans. Now, in 2H22, brands have been aggressively spurring demand. Full-scale promotional activities commenced on Amazon’s Prime Day, and TV sales were then ramped up to a peak on Black Friday. Among brands, TCL made the largest price concession for this year, cutting the price of its 55-inch Mini LED backlit model by 70% to US$199. Other brands also energetically promoted their particular product models in the holiday sales competition. On account of brands’ efforts, TV sales in North America for the Black Friday period rose by 13% YoY. While China and North America have exhibited very contrasting performances for the busy season, it is also clear that TV brands on the whole have gradually lowered their inventories to a relatively optimal level after months of promotional activities across channels and corrections to panel procurements.

Another notable development that TrendForce has observed in the TV market is the tepid performance of high-end products. Due to the lack of supporting broadcasting content and high retail prices, most TV brands have not been particularly keen on pushing 8K models. And after years of advocacy, Samsung remains the single dominant brand for 8K TVs with a market share almost 70%. Additionally, high inflation has eaten into consumers’ budgets this year. TrendForce therefore projects that 8K TV shipments will register a YoY decline for the first time in 2022, dropping by 7.4% to just about 400,000 units. It is also worth noting that Europe as one of the main sales regions for 8K TVs could be affected by the updated EU energy consumption labelling scheme (i.e., Energy Efficiency Index). Specifically, energy consumption rules have been further tightened so that some older 8K models could be banned from the region starting in March 2023. However, Samsung is planning to launch new 8K models that meet the updated energy consumption standards. Moreover, display panel suppliers continue to promote 8K products so as to widen adoption among TV brands. TrendForce currently forecasts that shipments of 8K TVs will surpass the 500,000 unit mark for 2023, registering a YoY growth of 20%.

TrendForce’s latest research on panel prices finds that LCD panel prices have plummeted. In fact, the price of a 55-inch UHD LCD was 4.8 times lower than the price of a WOLED (white OLED) O/C panel at the end of 3Q22. With the price difference between the two panels returning to where it was at the start of 2020, selling WOLED TVs have been quite challenging for brands that do offer this kind of product. Therefore, TrendForce estimates that shipments of WOLED TVs will shrink by 6.2% YoY to 6.29 million units for 2022. Assuming that LG Display does not want to sacrifice profitability, it will maintain a conservative pricing strategy when quoting WOLED panels next year. Given this situation, TrendForce forecasts that WOLED TV shipments will dip again by 2.7% YoY for 2023.

For more information on reports and market data from TrendForce’s Department of Display Research, please click here, or email Ms. Vivie Liu from the Sales Department at vivieliu@trendforce.com

For additional insights from TrendForce analysts on the latest tech industry news, trends, and forecasts, please visit our blog at https://insider.trendforce.com/

It appears too soon to say that Samsung Display and LG Display, the nation’s top display makers, will exit from the less lucrative LCD market amid a cutthroat competition with Chinese rivals with cheaper pricing.

Until a few years ago, the two firms had hinted at retiring from the old-school LCD business to focus on more advanced technologies such as upgraded LCDs or OLEDs to widen the gap with Chinese runner-ups.

But experts here say there has been a sign of change in the attitudes more recently, pointing out that their full shutdown of LCD operations ultimately would hinge on elevating profitability of their high-end push.

In 2020 alone, Samsung Display posted a deficit of more than 1 trillion won ($841.5 million) in its LCD business. But it has no other option but to continue production to meet the demand from its parent Samsung Electronics, the world’s largest TV maker.

The firm last year sold its LCD production facility in China to its Chinese rival TCL China Star Optoelectronics Technology, a key supplier to Samsung TVs. But the LCD line in Suzhou, China recently cut its panel supply almost in half, with Samsung’s display unit highly likely to be tasked with filling the void.

“(Samsung Electronics) have few choices but to contract with Samsung Display to make up for its LCD TV set capacity,” said Yi Choong-hoon, chief analyst at UBI Research.

This put Samsung Display‘s full exit plan in disarray. After the sell-off of the Chinese facility, the firm is also scaling down its LCD plant in Asan, South Chungcheong Province, to convert part of the facilities to its quantum-dot OLED lines to supply to set makers including Japanese firm Sony.

LG Display’s LCD business -- with production lines in Paju, Gyeonggi Province and Guangzhou, China -- is poised to generate 2.5 trillion won in operating profit for 2021, up fourfold from the previous year, according to Kim Jung-hwan, an analyst at Korea Investment & Securities, on Thursday.

This comes in sharp contrast with OLED TV earnings estimate. According to Kim, LG Display‘s OLED TV operations will post 152 billion won in operating loss, as its fourth-quarter forecast to generate 62 billion won income was dwarfed by 214 billion won losses for the previous three quarters. Since inception, LG’s OLED panel business has been in the red due to heavy spending.

Now, the question is whether the company is ready to be fully dedicated to next-generational OLED panels for premium TVs featuring self-lit pixels. Yi of UBI Research says it is too premature.

“A bigger penetration of OLED TVs to consumers is a prerequisitie for a conversion of (LG Display’s) existing LCD TV lines to OLED TV lines,” he said.

Analysts also said LG Display has already streamlined its LCD TV lines under a series of restructuring of LCD TV lines, including a conversion to lines for IT devices including mobile phones.

“(LG Display‘s) LCD TV fabs with low profit margin have completed a retreat in the first half of 2021,” said Kim Sun-woo of Meritz Securities. “LG is now capable of maintaining LCD capacity with a decent profit margin.”

This comes against the backdrop of industry projections that LCD TV panel prices continue to fall steadily over the course of the first quarter, and Chinese rivals are forecast to ramp up dominance in LCD market,

According to US-based market intelligence firm Display Supply Chain Consultants, Chinese firms’ LCD market share on a capacity basis are forecast to rise to 71 percent by 2025, from 53 percent in 2020, far outpacing Korea, Japan and Taiwan, as of June 2020.

Another estimate, released earlier this week, showed the price for LCD TV panels regardless of size -- ranging from 32- to 65-inch -- is projected to fall until March, giving up almost entire gains from July 2020 to July 2021 that is partly attributable to announced exits of Korean LCD panel makers.

The quarter-on-quarter price declines in the first quarter of 2022 to range between 10 percent and 23 percent and average 15 percent, with mid-sized panels taking the largest dip.

“Although the declines are slowing down in the first quarter, they are still severe for panel makers,” noted Robert O‘Brien, co-founder and principal analyst at DSCC.

LCD manufacturers are mainly located in China, Taiwan, Korea, Japan. Almost all the lcd or TFT manufacturers have built or moved their lcd plants to China on the past decades. Top TFT lcd and oled display manufactuers including BOE, COST, Tianma, IVO from China mainland, and Innolux, AUO from Tianwan, but they have established factories in China mainland as well, and other small-middium sizes lcd manufacturers in China.

China flat display revenue has reached to Sixty billion US Dollars from 2020. there are 35 tft lcd lines (higher than 6 generation lines) in China,China is the best place for seeking the lcd manufacturers.

The first half of 2021, BOE revenue has been reached to twenty billion US dollars, increased more than 90% than thesame time of 2020, the main revenue is from TFT LCD, AMoled. BOE flexible amoled screens" output have been reach to 25KK pcs at the first half of 2021.the new display group Micro LED revenue has been increased to 0.25% of the total revenue as well.

Established in 1993 BOE Technology Group Co. Ltd. is the top1 tft lcd manufacturers in China, headquarter in Beijing, China, BOE has 4 lines of G6 AMOLED production lines that can make flexible OLED, BOE is the authorized screen supplier of Apple, Huawei, Xiaomi, etc,the first G10.5 TFT line is made in BOE.BOE main products is in large sizes of tft lcd panel,the maximum lcd sizes what BOE made is up to 110 inch tft panel, 8k resolution. BOE is the bigger supplier for flexible AM OLED in China.

As the market forecast of 2022, iPhone OLED purchasing quantity would reach 223 million pcs, more 40 million than 2021, the main suppliers of iPhone OLED screen are from Samsung display (61%), LG display (25%), BOE (14%). Samsung also plan to purchase 3.5 million pcs AMOLED screen from BOE for their Galaxy"s screen in 2022.

Technology Co., Ltd), established in 2009. CSOT is the company from TCL, CSOT has eight tft LCD panel plants, four tft lcd modules plants in Shenzhen, Wuhan, Huizhou, Suzhou, Guangzhou and in India. CSOTproviding panels and modules for TV and mobile

three decades.Tianma is the leader of small to medium size displays in technologyin China. Tianma have the tft panel factories in Shenzhen, Shanhai, Chendu, Xiamen city, Tianma"s Shenzhen factory could make the monochrome lcd panel and LCD module, TFT LCD module, TFT touch screen module. Tianma is top 1 manufactures in Automotive display screen and LTPS TFT panel.

Tianma and BOE are the top grade lcd manufacturers in China, because they are big lcd manufacturers, their minimum order quantity would be reached 30k pcs MOQ for small sizes lcd panel. price is also top grade, it might be more expensive 50%~80% than the market price.

Panda electronics is established in 1936, located in Nanjing, Jiangshu, China. Panda has a G6 and G8.6 TFT panel lines (bought from Sharp). The TFT panel technologies are mainly from Sharp, but its technology is not compliance to the other tft panels from other tft manufactures, it lead to the capacity efficiency is lower than other tft panel manufacturers. the latest news in 2022, Panda might be bougt to BOE in this year.

Established in 2005, IVO is located in Kunsan,Jiangshu province, China, IVO have more than 3000 employee, 400 R&D employee, IVO have a G-5 tft panel production line, IVO products are including tft panel for notebook, automotive display, smart phone screen. 60% of IVO tft panel is for notebook application (TOP 6 in the worldwide), 23% for smart phone, 11% for automotive.

Besides the lcd manufacturers from China mainland,inGreater China region,there are other lcd manufacturers in Taiwan,even they started from Taiwan, they all have built the lcd plants in China mainland as well,let"s see the lcd manufacturers in Taiwan:

Innolux"s 14 plants in Taiwan possess a complete range of 3.5G, 4G, 4.5G, 5G, 6G, 7.5G, and 8.5G-8.6G production line in Taiwan and China mainland, offering a full range of large/medium/small LCD panels and touch-control screens.including 4K2K ultra-high resolution, 3D naked eye, IGZO, LTPS, AMOLED, OLED, and touch-control solutions,full range of TFT LCD panel modules and touch panels, including TV panels, desktop monitors, notebook computer panels, small and medium-sized panels, and medical and automotive panels.

AUO is the tft lcd panel manufacturers in Taiwan,AUO has the lcd factories in Tianma and China mainland,AUOOffer the full range of display products with industry-leading display technology,such as 8K4K resolution TFT lcd panel, wide color gamut, high dynamic range, mini LED backlight, ultra high refresh rate, ultra high brightness and low power consumption. AUO is also actively developing curved, super slim, bezel-less, extreme narrow bezel and free-form technologies that boast aesthetic beauty in terms of design.Micro LED, flexible and foldable AMOLED, and fingerprint sensing technologies were also developed for people to enjoy a new smart living experience.

Hannstar was found in 1998 in Taiwan, Hannstar display hasG5.3 TFT-LCD factory in Tainan and the Nanjing LCM/Touch factories, providing various products and focus on the vertical integration of industrial resources, creating new products for future applications and business models.

driver, backlight etc ,then make it to tft lcd module. so its price is also more expensive than many other lcd module manufacturers in China mainland.

Maclight is a China based display company, located in Shenzhen, China. ISO9001 certified, as a company that more than 10 years working experiences in display, Maclight has the good relationship with top tft panel manufacturers, it guarantee that we could provide a long term stable supply in our products, we commit our products with reliable quality and competitive prices.

Maclight products included monochrome lcd, TFT lcd module and OLED display, touch screen module, Maclight is special in custom lcd display, Sunlight readable tft lcd module, tft lcd with capacitive touch screen. Maclight is the leader of round lcd display. Maclight is also the long term supplier for many lcd companies in USA and Europe.

If you want tobuy lcd moduleorbuy tft screenfrom China with good quality and competitive price, Maclight would be a best choice for your glowing business.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey