lcd panel market share 2016 price

BOE was the leading LCD TV panel vendor during the first half of 2020, having shipped approximately 23.26 million units worldwide. In that period, global shipments of LCD TV panels totaled over 115 million units.

BOE Technology, founded in 1993, has become China’s largest TV panel maker and it continues to make a name for itself in the global consumer electronics market. It was the first company to introduce a gen 10.5 LCD plant in late 2017. Since then, BOE’s LCD panel production capacity has grown annually, surpassing former leading manufacturer LG Display. In recent years, BOE accounted for over 20 percent of large-area TFT LCD display unit shipments worldwide.

Chinese panel makers accelerate worldwide LCD TV panel shipmentsChina became the leading LCD panel producer worldwide in 2017, overtaking powerhouses South Korea and Taiwan. Chinese shipments of LCD TV panels 60-inch and larger have also increased significantly in recent years, with roughly 2.24 million units sold in the first quarter of 2019 worldwide, in comparison to just 117,000 units a year before. This figure is forecast to increase in the future, paving the way for Chinese panel makers’ worldwide success. At the same time, the concurrent specialization on large LCD panels by Chinese and South Korean suppliers will likely push down panel prices.Read moreGlobal LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor(in millions)tablecolumn chartCharacteristicBOELGDInnoluxCSOTSDCAUOCEC GroupOthers1H 202023.2611.7920.3421.312.1310.14-16.17

TrendForce. (July 28, 2020). Global LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor (in millions) [Graph]. In Statista. Retrieved January 29, 2023, from https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/

TrendForce. "Global LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor (in millions)." Chart. July 28, 2020. Statista. Accessed January 29, 2023. https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/

TrendForce. (2020). Global LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor (in millions). Statista. Statista Inc.. Accessed: January 29, 2023. https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/

TrendForce. "Global Lcd Tv Panel Unit Shipments from H1 2016 to H1 2020, by Vendor (in Millions)." Statista, Statista Inc., 28 Jul 2020, https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/

TrendForce, Global LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor (in millions) Statista, https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/ (last visited January 29, 2023)

Global LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor (in millions) [Graph], TrendForce, July 28, 2020. [Online]. Available: https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/

This graph shows the market share of large-area displays by application worldwide in 2016. In 2016, large-area TV displays accounted for 39.2 percent of the global large-area display market.Read moreShare of the large-area display market worldwide in 2016, by applicationCharacteristicMarket share--

TechNavio. (January 17, 2017). Share of the large-area display market worldwide in 2016, by application [Graph]. In Statista. Retrieved January 29, 2023, from https://www.statista.com/statistics/786696/large-area-display-market-share-worldwide/

TechNavio. "Share of the large-area display market worldwide in 2016, by application." Chart. January 17, 2017. Statista. Accessed January 29, 2023. https://www.statista.com/statistics/786696/large-area-display-market-share-worldwide/

TechNavio. (2017). Share of the large-area display market worldwide in 2016, by application. Statista. Statista Inc.. Accessed: January 29, 2023. https://www.statista.com/statistics/786696/large-area-display-market-share-worldwide/

TechNavio. "Share of The Large-area Display Market Worldwide in 2016, by Application." Statista, Statista Inc., 17 Jan 2017, https://www.statista.com/statistics/786696/large-area-display-market-share-worldwide/

TechNavio, Share of the large-area display market worldwide in 2016, by application Statista, https://www.statista.com/statistics/786696/large-area-display-market-share-worldwide/ (last visited January 29, 2023)

Share of the large-area display market worldwide in 2016, by application [Graph], TechNavio, January 17, 2017. [Online]. Available: https://www.statista.com/statistics/786696/large-area-display-market-share-worldwide/

LCD TV Panel Market Size is projected to Reach Multimillion USD by 2027, In comparison to 2021, at unexpected CAGR during the Forecast Period 2022-2028.

Considering the economic change due to COVID-19 and Russia-Ukraine War Influence, LCD TV Panel accounted for % of the global market of LCD TV Panel in 2022.

This LCD TV Panel Market Report offers analysis and insights based on original consultations with important players such as CEOs, Managers, Department Heads of Suppliers, Manufacturers, Distributors, etc.

The Global LCD TV Panel Market is anticipated to rise at a considerable rate during the forecast period, between 2022 and 2027. In 2021, the market is growing at a steady rate and with the rising adoption of strategies by key players, the market is expected to rise over the projected horizon.

LCD displays utilize two sheets of polarizing material with a liquid crystal solution between them. An electric current passed through the liquid causes the crystals to align so that light cannot pass through them. Each crystal, therefore, is like a shutter, either allowing light to pass through or blocking the light. LCD panel is the key components of LCD display. And the price trends of LCD panel directly affect the price of liquid crystal displays. LCD panel consists of several components: Glass substrate, drive electronics, polarizers, color filters etc. Only LCD panel applied for TV will be counted in this report

Samsung Display, LG Display, Innolux Crop and AUO captured the top four revenue share spots in the LCD TV Panel market in 2015. Samsung Display dominated with 22.11 percent revenue share, followed by LG Display with 19.72 percent revenue share and Innolux Crop Display with 19.30 percent revenue share.

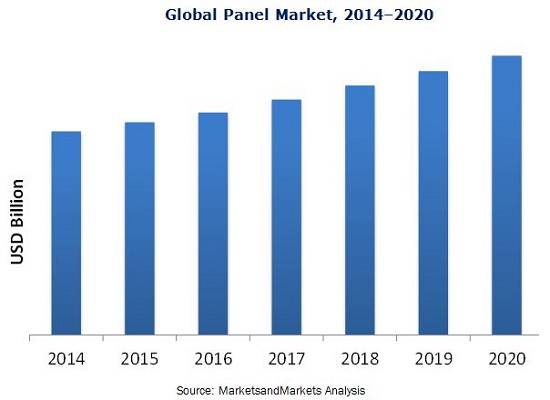

The global LCD TV Panel market is valued at USD 51130 million in 2019. The market size will reach USD 59640 million by the end of 2026, growing at a CAGR of 2.2% during 2021-2026.

LCD TV Panel market is segmented by Size, and by Application. Players, stakeholders, and other participants in the global LCD TV Panel market will be able to gain the upper hand as they use the report as a powerful resource. The segmental analysis focuses on production capacity, revenue and forecast by Size and by Application for the period 2016-2027.

The report focuses on the LCD TV Panel market size, segment size (mainly covering product type, application, and geography), competitor landscape, recent status, and development trends. The report considers key geographic segments and describes all the favorable conditions driving the market growth.

On the basis of the End Users/Applications, this report focuses on the status and outlook for major applications/end users, consumption (sales), market share, and growth rate for each application, including:

Geographically, the Major Regions Covered in LCD TV Panel Market Report Are:To comprehend LCD TV Panel market dynamics across major global regions. ● North America(United States, Canada)

Market is changing rapidly with the ongoing expansion of the industry. Advancement in technology has provided today’s businesses with multifaceted advantages resulting in daily economic shifts. Thus, it is very important for a company to comprehend the patterns of market movements in order to strategize better. An efficient strategy offers the companies a head start in planning and an edge over the competitors.Industry Researchis a credible source for gaining the market reports that will provide you with the lead your business needs.

Is there a problem with this press release? Contact the source provider Comtex at editorial@comtex.com. You can also contact MarketWatch Customer Service via our Customer Center.

This market research report includes a detailed segmentation of the global large area LCD display market by application (TVs, notebooks, monitors, tablets, and others). It outlines the market shares for key regions such as the Americas, APAC, and EMEA. The key vendors analyzed in this report are AU Optronics, BOE Technology, Innolux, LG Display, and Samsung Display.

Technavio’s research analyst predicts the global large area LCD display market to grow at a CAGR of 3% during the forecast period. The formation of UHD alliances is the primary growth driver for this market. During 2015, supply chain members of the global UHD TV market announced the formation of the UHD Alliance to support innovative technologies including 4K and higher resolution, high dynamic range, immersive 3D audio, and wider color gamut.

The decline in ASP of the LCD panel is expected to boost the market growth during the forecast period. During 2014, per meter square, ASP of LCD panel was $472, which declined to $416 during 2015. Vendors reduced the ASP to reduce excess inventory. The declining per square meter ASP of LCD panel drove the shipment of LCD display in terms of area.

During 2015, the TV segment dominated the large area LCD display market with a market share of 38%. The primary reason for the growth of this product segment was the strong demand for 4K TVs of 40 inches and larger screen size. During 2015, several manufacturers introduced 4K TVs ranging from 50 inches and above.

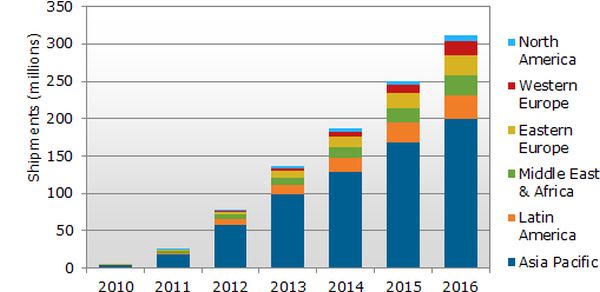

During 2015, APAC accounted for 81% of the market share and is expected to grow at a CAGR of 1% during the forecast period. The high concentration of display device manufacturers and LCD panel manufacturers in this region are the primary growth drivers. Technavio expects that the well-established supply chain for display devices in APAC would continue to support the dominance of this region in the market during the forecast period. China is emerging fast as a leading hub for large area TFT LCD display manufacturers because of the rise in the number of display device manufacturers in the country.

Manufacturing LCD display panels require economies of scale because the equipment used to manufacture displays are expensive. This presents high entry barriers for LCD display panel manufacturers. Currently, the global large area LCD display market is dominated by China, Japan, South Korea, and Taiwan in terms of production and revenue contribution. Chinese manufacturers have the advantage of manufacturing LCD panels at a lower cost. This has resulted in price wars among LCD manufacturers and has accelerated the declining ASP of LCD panels. Vendors such as LG and Samsung are under a lot of pressure as profit margins have come down because of increased competition.

Other prominent vendors in the market include Chi Mei Optoelectronics, Chunghwa Picture Tube (CPT), HannsTouch Solution, HannStar Display, InfoVision Optoelectronics, Japan Display, Kaohsiung Opto-Electronics, NEC Display Solutions, Panasonic, and Sharp.

According to IMARC Group’s latest report, titled “TFT LCD Panel Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2022-2027”, the global TFT LCD panel market size reached US$ 157 Billion in 2021. Looking forward, IMARC Group expects the market to reach US$ 207.6 Billion by 2027, exhibiting a growth rate (CAGR) of 4.7% during 2022-2027.

A thin-film-transistor liquid-crystal display (TFT LCD) panel is a liquid crystal display that is generally attached to a thin film transistor. It is an energy-efficient product variant that offers a superior quality viewing experience without straining the eye. Additionally, it is lightweight, less prone to reflection and provides a wider viewing angle and sharp images. Consequently, it is generally utilized in the manufacturing of numerous electronic and handheld devices. Some of the commonly available TFT LCD panels in the market include twisted nematic, in-plane switching, advanced fringe field switching, patterned vertical alignment and an advanced super view.

We are regularly tracking the direct effect of COVID-19 on the market, along with the indirect influence of associated industries. These observations will be integrated into the report.

The global market is primarily driven by continual technological advancements in the display technology. This is supported by the introduction of plasma enhanced chemical vapor deposition (PECVD) technology to manufacture TFT panels that offers uniform thickness and cracking resistance to the product. Along with this, the widespread adoption of the TFT LCD panels in the production of automobiles dashboards that provide high resolution and reliability to the driver is gaining prominence across the globe. Furthermore, the increasing demand for compact-sized display panels and 4K television variants are contributing to the market growth. Moreover, the rising penetration of electronic devices, such as smartphones, tablets and laptops among the masses, is creating a positive outlook for the market. Other factors, including inflating disposable incomes of the masses, changing lifestyle patterns, and increasing investments in research and development (R&D) activities, are further projected to drive the market growth.

The competitive landscape of the TFT LCD panel market has been studied in the report with the detailed profiles of the key players operating in the market.

IMARC Group is a leading market research company that offers management strategy and market research worldwide. We partner with clients in all sectors and regions to identify their highest-value opportunities, address their most critical challenges, and transform their businesses.

IMARC’s information products include major market, scientific, economic and technological developments for business leaders in pharmaceutical, industrial, and high technology organizations. Market forecasts and industry analysis for biotechnology, advanced materials, pharmaceuticals, food and beverage, travel and tourism, nanotechnology and novel processing methods are at the top of the company’s expertise.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

1.1. THE POLICY COVERS THE HANDLING OF THE PRIVATE INFORMATION EACH USER SHARES WITH TRENDFORCE WHILE VISITING OUR WEBSITES. IF A DIFFERENT PRIVATE POLICY HAS BEEN REFERED TO FOR SPECIFIC TRENDFORCE WEBSITES AND SERVICES, THAT POLICY WILL REPLACE OR SUPPLEMENT THE PRIVACY POLICY MENTIONED IN THIS DOCUMENT. THIS POLICY ALSO COVERS INDIVIDUALS LEGALLY RESIDING IN OR ORGANIZATIONS LEGALLY BASED IN MEMBER COUNTRIES OF THE EUROPEAN UNION (EU) AND ARE SUBJECTED TO EU GENERAL DATA PROTECTION REGULATION (GDPR) WITH REGARD TO PROVISION OF SERVICES AND PERSONAL DATA PROTECTION.

2.1 THE WEBSITE WILL COLLECT AND USE USER INFORMATION FOR PURPOSES SUCH AS MARKETING, CONSUMER PROTECTION, CONSUMER/CLIENT MANAGEMENT, E-COMMERCE SERVICES, FINANCIAL ACCOUNTING, CONTRACTUAL MATTERS, RESEARCH ANALYSIS, AND DATA PROCESSING. WHEN REQUIRED BY LAW, THE WEBSITE MAY ALSO PROVIDE PERSONAL INFORMATION TO NON-GOVERNMENT AGENCIES.

THE WEBSITE WILL NOT DISCLOSE OR SHARE ANY PERSONAL INFORMATION EXCPET PER SPECIAL REQUEST OR WHEN PERMISSION IS RECEIVED FROM THE USER. OTHER EXCEPTIONS INCLUDE:

IN ACCORDANCE WITH ARTICLE 3 OF THE PERSONAL INFORMATION PROTECTION LAW, YOU WILL HAVE THE OPTION TO EXERCISE THE FOLLOWING RIGHTS WITH REGARD TO THE PERSONAL INFORMATION SHARED WITH THE WEBSITE:

a. TO PREVENT UNAUTHORIZED PARTIES FROM ACCESSING, MODIFYING, OR LEAKING PERSONAL USER DATA, THE WEBSITE WILL TAKE STEPS TO IMPLEMENT PROPER SAFETY MEASURES. THE DATA SEARCHED AND RECORDED ON THE WEBSITE AND THE APPROPRIATE SAFETY MEASURES CHOSEN WILL ALL BE REVIEWED CAREFULLY. CONSIDERING HOW THE SAFETY OF TRANSMITTING DATA ON THE INTERNET CAN NEVER BE GUARANTEED COMPLETELY, USERS SHOULD KEEP IN MIND ALL POSSIBLE RISKS ASSOCIATED WITH ONLINE DATA TRANSFERS AND TAKE RESPONSIBILITY FOR ANY INFORMATION SHARED WITH OR OBTAINED FROM THE WEBSITE.

BE SURE TO PROTECT ALL PASSWORDS AND PERSONAL INFORMATION, REFRAIN FROM DISCLOSING PRIVATE USER INFORMATION TO ANY THIRD PARTY, AND REGISTER WITH THE WEBSITE UPON COMPLETING ALL NECESSARY MEMBERSHIP PROCEDURES. WHEN USING A SHARED OR PUBLIC COMPUTER, PLEASE MAKE SURE TO PROPERLY CLOSE ALL RELEVANT BROWSERS TO PREVENT OTHERS FROM READING YOUR PERSONAL E-MAILS OR INFORMATION.

TFT or thin-film transistor is combined with LCD to improve colour quality leading to a sharper image, as each pixel on a TFT-LCD is attached to a transistor. Due to the small sizes of each transistor, TFT-LCD display panels consume less power. They are widely used in computers, TVs, laptops, and mobile phones as it gives a more enhanced image than older technologies and prevents the distortion of image.

With the growing applications of TFT-LCD, there has been an increased competition among the manufacturers for the best cutting technology, i.e. ‘generations’, to produce TFT-LCD panels. In 2017, BOE, one of the major TFT-LCD manufacturers globally, put the world’s highest generation line, Generation 10.5 TFT-LCD production line, into production ahead of schedule in Hefei, China. With more Gen 10.5 facilities starting mass production, the market is primed for the production of 65 inches and larger TFT-LCD panels. More than 85.5% of the TFT-LCD display panels consumed in 2018 were large-sized panels sized over 10 inches.

Driven by the demand for TFT-LCD display panels in TV and monitor panels, the global shipment of large TFT-LCD panels grew again in 2018, despite over-supply concerns. The market is also driven by a rising demand for automotive displays. While automotive display systems were earlier reserved for luxury vehicles, cars for the mass-market are increasingly including high resolution display systems in their design due to a decline in prices along with the rising production and demand for automobiles. This growth in automotive displays has been supported by the rising investments in automotive display panels by big display panel manufacturers in Asia. The Asia Pacific countries like China and India are the fastest growing markets in the region due to rapid economic growth and a growing demand for consumer-based electronics. Currently, the global market for TFT-LCD display panel is dominated by North America.

Region-wise, the global market for TFT-LCD display panel can be divided into North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

The report also offers historical (2018-2022) and forecast (2023-2028) market information for the sizes, applications, and major regions of TFT-LCD display panel.

The report analyses the market dynamics, covering the key demand and price indicators in the market, along with providing an assessment of the SWOT and Porter’s Five Forces models.

The major players in the global TFT-LCD display panel market are Samsung Electronics Co., Ltd., LG Display Co., Ltd., Japan Disney Inc., Sharp Corporation, BOE Technology Group Co., Ltd., AUO Corporation, Raystar Optronics Inc., WINSTAR Display Co., Ltd., Kingtech Group Co., Ltd., and Tricomtek Co., Ltd., among others. The comprehensive report by EMR looks into the market share, capacity, and latest developments like mergers and acquisitions, plant turnarounds, and capacity expansions of the major players.

*At Expert Market Research, we strive to always give you current and accurate information. The numbers depicted in the description are indicative and may differ from the actual numbers in the final EMR report.

LG Display and Samsung Display are struggling to find their ways out of the deterioration of their performance even after withdrawing from production of liquid crystal display (LCD) panels. The high-priced organic light emitting diode (OLED) panel sector regarded as a future growth engine is not growing fast due to the economic downturn. Even in the OLED panel sector, Chinese display makers are within striking distance of Korean display makers, experts say.

On Aug. 30, Display Supply Chain Consultants (DSCC), a market research company, predicted that LCD TV panel prices hit an all-time low in August and that an L-shaped recession will continue in the fourth quarter. According to DSCC, the average price of a 65-inch ultra-high-definition (UHD) panel in August was only US$109, a 62 percent drop from the highest price of US$288 recorded in July in 2021. The average price of a 75-inch UHD panel was only US$218, which was only about half of the highest price of US$410 in July last year. DSCC predicted that the average panel price in the third quarter will fall by 15.7 percent. As Chinese companies’ price war and the effect of stagnation in consumption overlapped, the more LCD panels display makers produce, the more loss they suffer.

As panel prices fell, manufacturers responded by lowering facility utilization rates. DSCC said that the LCD factory utilization rate descended from 87 percent in April to 83 percent in May, 73 percent in June, and 70 percent in July.

Now that the LCD panel business has become no longer lucrative, Korean display makers have shut down their LCD business or shrunk their sizes. In the LCD sector, China has outpaced Korea since 2018. China’s LCD market share reached 50.9 percent in 2021, while that of Korea dropped to 14.4 percent, lower than Taiwan’s 31.6 percent.

Samsung Display already announced its withdrawal from the LCD business in June. Only 10 years have passed since the company was spun off from Samsung Electronics in 2012. LG Display has decided to halt domestic LCD TV panel production until 2023 and reorganize its business structure centering on OLED panels. Its Chinese LCD production line will be gradually converted to produce LCD panels for IT or commercial products. TrendForce predicted that LG Display will stop operating its P7 Plant in the first quarter of next year.

Korean display makers’ waning LCD business led to a situation in which Korea even lost first place in the display industry. Korea with a display market share of 33.2 percent was already overtaken by China with 41.5 percent) in 2021 according to market researcher Omdia and the Korea Display Industry Association. Korea’s market share has never rebounded in for five years since 2017 amid the Korean government’s neglect. Seventeen years have passed since 2004 when Korea overtook Japan to rise to the top of the world in the LCD industry. Korea’s LCD exports amounted to more than US$30 billion in 2014, but fell to US$21.4 billion last year.

A bigger problem is that Korean display makers may lose its leadership in the OLED panel sector although it is still standing at the top spot. While Korea’s OLED market share fell from 98.1 percent in 2016 to 82.8 percent last year, that of China rose from 1.1 percent to 16.6 percent. Considering that the high-end TV market is highly likely to shrink for the time being due to a full-fledged global consumption contraction, some analysts say that the technology gap between Korea and China can be sharply narrowed through this looming TV market slump. According to industry sources, the Chinese government is now focusing on giving subsidies to the development of OLED panel technology rather LCD technology. On the other hand, in Korea, displays were also wiped out from national strategic technology industry items under the Restriction of Special Taxation Act which can receive tax benefits for R&D activities on displays.

LCD panel prices have risen for 4 months in a row because of your home gaming? Since this year, the whole LCD panel market has smoked. Whether after the outbreak of the epidemic, LCD panel market prices rose for four months, or the panel giants in Japan and South Korea successively sold production lines, or the Chinese mainland listed companies frequently integrated acquisition, investment, and plant construction, all make the industry full of interesting.

LCD panel prices are already a fact. Since May this year, LCD panel prices have risen for four months in a row, making the whole industry chain dynamic. Why are LCD panels going up in price in a volatile 2020? The key factor lies in the imbalance between supply and demand.

The price of LCDS for large-size TVs of 70 inches or more hasn’t budged much. In addition, LTPS screens and AMOLED screens used in high-end phones have seen little or no increase in price.

As for October, LCD panel price increases are expected to moderate. The data shows that in October 32 inches or 2 dollars; Gains of 39.5 to 43 inches will shrink to $3;55 inches will fall back below $10; The 65-inch gain will narrow to $5.

During the epidemic, people stayed at home and had no way to go out for entertainment. They relied on TV sets, PCS, and game consoles for entertainment. After the resumption of economic work and production, the market of traditional home appliances picked up rapidly, and LCD production capacity was quickly digested.

However, due to the shutdown of most factories lasting 1-2 months during the epidemic period, LCD panel production capacity was limited, leading to insufficient production capacity in the face of the market outbreak, which eventually led to the market shortage and price increase for 4 consecutive months.

In fact, the last round of price rise of LCD panels was from 2016 to 2017, and its overall market price has continued to fall since 2018. Even in 2019, individual types have fallen below the material cost, and the whole industry has experienced a general operating loss. As a result, LCD makers have been looking for ways to improve margins since last year.

A return to a reasonable price range is the most talked about topic among panel makers in 2019, according to one practitioner. Some manufacturers for the serious loss of the product made the decision to reduce production or even stop production; Some manufacturers planned to raise the price, but due to the epidemic in 2020, the downstream demand was temporarily suppressed and the price increase was postponed. After the outbreak was contained in April, LCD prices began to rise in mid-to-late May.

In fact, the market price of LCD panels continued to decline in 2018-2019 because of the accelerated rise of China’s LCD industry and the influx of a large number of local manufacturers, which doubled the global LCD panel production capacity within a few years, but there was no suitable application market to absorb it. The result of excess capacity is oversupply, ultimately making LCD panel prices remain depressed.

Against this background, combined with the impact of the epidemic in 2020, the operating burden of LCD companies in Japan and South Korea has been further aggravated, and it is difficult to make profits in the production of LCD panels, so they have to announce the withdrawal of LCD business.

business in June 2022. In August, Sharp bought JDI Baishan, a plant in Ishikawa prefecture that makes liquid crystal display panels for smartphones. In early September, Samsung Display sold a majority stake in its SUZHOU LCD production plant to Starlight Electronics Technology, a unit of TCL Technology Group. LGD has not only pulled out of some of its production capacity but has announced that it will close its local production line in 2020. According to DSCC, a consultancy, the share of LCD production capacity in South Korea alone will fall from 19% to 7% between 2020 and 2021.

It is worth mentioning that in industry analysis, in view of the fact that Korean companies are good at using “dig through old bonus – selling high price – the development of new technology” the cycle of development mode, another 2020 out of the LCD production capacity, the main reason may be: taking the advantage of China’s expanding aggressively LCD manufacturers, Korean companies will own LCD panel production line hot sell, eliminating capacity liquid to extract its final value, and turning to the more profitable advantage of a new generation of display technologies, such as thinner, color display better OLED, etc. Samsung, for example, has captured more than 80% of the OLED market with its first-mover advantage.

From the perspective of production capacity, the launch of LCD tracks by major manufacturers in Japan and South Korea must reduce some production capacity in the short term, which to some extent induces market price fluctuations. In the long run, some of the Japanese and Korean LCD production capacity has been bought by Chinese manufacturers, coupled with frequent investment in recent years, the overall capacity is sure to recover as before, or even more than before. But now it will take time to expand the production layout, which more or less will cause supply imbalance, the industry needs to be cautious.

The LCD panel industry started in the United States and then gradually moved to Japan, South Korea, China, and Taiwan. At present, the proportion of production capacity in The Chinese mainland has reached 52% in 2020, and there are leading LCD panel products in China represented by BOE, Huxing Optoelectronics. Meanwhile, the production capacity layout of BOE, Huike, Huxing Optoelectronics, and other manufacturers has been basically completed, making industrial integration a necessity.

On the one hand, South Korean enterprises out of the LCD track, the domestic factory horse enclosure, plant expansion action. While LCDs may not sell as well as “upstart” flexible screens, respondents believe they are still strong enough in the traditional home appliance market to warrant continued investment. Zhao Bin, general manager of TCL Huaxing Development Center, has said publicly that the next-generation display technology will be mature in four to five years, but the commercialization of products may not take place until a decade later. “LCD will still be the mainstream in this decade,” he said.

On the other hand, there is no risk of neck jam in China’s LCD panel industry, which is generally controllable. In mainland China, there will be 21 production lines capable of producing 32-inch or larger LCD panels by 2021, accounting for about two-thirds of the global total. In terms of the proportion of production capacity, the Chinese mainland accounted for 42% of the global LCD panel in 2019, 51% this year, and will continue to climb to 63% next year.

Of course, building factories and expanding production cannot be accomplished overnight. In the process of production capacity recovery, it is predicted that there will be several price fluctuations, and the cost may be passed on to the downstream LCD panel manufacturers or consumers when the price rises greatly, which requires continuous attention.

WASHINGTON, July 28, 2022 (GLOBE NEWSWIRE) -- Vantage Market Research"s latest research on the Global Curved Display Devices Market finds that the introductions of new products related to Curved Display Devices Market based on the technology are likely to strengthen the growth of the Curved Display Devices Market over the analysis period. The Global Market revenue was valued at USD 5.4 Billion in 2021.

The Global Curved Display Devices Market size is forecasted to reach USD 13.2 Billion by 2028 and is forecast and grow exhibiting a Compound Annual Growth Rate (CAGR) of 16.2% during the forecast period; states Vantage Market Research, in a report, titled "Curved Display Devices Market Size, Share & Trends Analysis Report by Display Type (LCD, EPD, LED, OLED), by Application (Smartphones & Tablets, Televisions, Smart Wearable, Laptops & Computers), by End-User (Consumer Electronics, Transportation, Retail, Advertising), by Region (North America, Europe, Asia Pacific, Latin America) - Global Industry Assessment (2016 - 2021) & Forecast (2022 - 2028)".

Using industry data and interview with experts, you can learn about topics such as regional impact analysis, global forecast, competitive landscape analysis, size & share of regional markets.

Free sample includes, Industry Operating Conditions, Industry Market Size, Profitability Analysis, SWOT Analysis, Industry Major Players, Historical and Forecast, Growth Porter"s 5 Forces Analysis, Revenue Forecasts, Industry Trends, Industry Financial Ratios.

The report also presents the country-wise and region-wise analysis of the Vantage Market Research and includes a detailed analysis of the key factors affecting the growth of the market.

Sample Report further sheds light on the Major Market Players with their Sales Volume, Business Strategy and Revenue Analysis, to offer the readers an advantage over others.

Key Insights & Findings from the Report: According to our primary respondents’ research, the Curved Display Devices market is predicted to grow at a CAGR of roughly 16.2% during the forecast period.

The Curved Display Devices market was estimated to be worth roughly USD 5.4 Billion in 2021 and is expected to reach USD 13.2 Billion by 2028; based on primary research.

There is an increase in the automotive and industrial use of curved display technology in various applications such as Smartphones, TVs, and Computer Monitors, to name a few., where the benefits are present. For example, the Human Machine Interface (HMI) used in the automotive industry demonstrates technological breakthroughs and analyzes consumer electronics market demand. The most acceptable way to remove analog components such as buttons, and knots, to note a few, on HMI is to use curved displays. As the emphasis on curved display technology in consumer electronics and automotive applications is adapted to users, their demand in these fields will likely grow again.

These days, with rapidly paced changing surroundings, the curved show era is relatively new within the digital display market and is gaining sturdy interest amongst users. Moreover, curved monitors are now making their debut inside the market on a far smaller scale than televisions and mobile phones. In televisions and mobiles, a curved display tasks the photo at the screen and affords a mile"s more expansive field of view than a general flat display screen. And so, the rise in advanced and digital technology fuels the market growth.

Benefits of Purchasing Curved Display Devices Market Reports: Customer Satisfaction: Our team of experts assists you with all your research needs and optimizes your reports.

North America is expected to dominate the growth of Curved Display Devices Market in 2021 and is expected to continue to dominate the forecast period owing to rising revenue losses and increased consumer spending, and the presence of prominent emerging economists in the region. In addition, improving government programs to facilitate investment and build better quality production infrastructure in the country is another factor expected to support market growth to some extent in the region.

This market titled “Curved Display Devices Market” will cover exclusive information in terms of Regional Analysis, Forecast, and Quantitative Data – Units, Key Market Trends, and various others as mentioned below: ParameterDetails

The report can be customized as per client needs or requirements. For any queries, you can contact us on sales@vantagemarketresearch.com or +1 (202) 380-9727. Our sales executives will be happy to understand your needs and provide you with the most suitable reports.

Browse More Related Report: Embedded Hypervisor Market Size, Share & Trends Analysis Report by Component (Software, Services), by Type (Bare Metal , Hosted ), by Technology (Desktop Virtualization, Server Virtualization, Data Centre Virtualization), by Enterprise Size (Small & Medium Sized Enterprise, Large Enterprise), by Application (Android & iOS Device, Laptop, 5G, SCADA), by End-use (Aerospace, Defense, Automotive, Industrial), by Region (North America, Europe, Asia Pacific, Latin America, Middle East & Africa) - Global Industry Assessment (2016 - 2021) & Forecast (2022 - 2028).

Wearable AI Market Size, Share & Trends Analysis Report by Application (Consumer electronics, Healthcare, Automotive, Military and Defense), by Type (Smart Watch, Smart Glasses, Smart Earwear, Smart Glove), by Region (North America, Europe, Asia Pacific, Latin America and Middle East & Africa) - Global Industry Assessment (2016 - 2021) & Forecast (2022 - 2028).

Optical Brighteners Market Size, Share & Trends Analysis Report by Application (Paper, Detergents & Soaps, Fabrics, Synthetics & Plastics ), by End-Use (Consumer Product, Security & Safety, Textiles & Apparel, Packaging), by Region (North America, Asia Pacific, Europe, Latin America) - Global Industry Assessment (2016 - 2021) & Forecast (2022 - 2028).

Low Power Next Generation Display Market by Type (Quantum Dot Display (QD-LED), Field Emission Display (FED), Laser Phosphor Display (LPD), Organic Light-Emitting Diode (OLED), by Application (Consumer Electronics, Home Appliance, Advertising and Public Display, Automotive), by Region (North America, Europe, Asia Pacific, Middle East & Africa) - Global Industry Assessment (2016 - 2021) & Forecast (2022 - 2028).

E-KYC Market Size, Share & Trends Analysis Report by Product (Identity Authentication & Matching, Video Verification, Digital ID Schemes, Enhanced vs Simplified Due Diligence), by Deployment Mode (Cloud-Based, On-Premise), by End-Use (Banks, Financial Institutions, E-Payment Service Providers, Telecom Companies, Government Entities¸ Insurance Companies), by Region (North America, Europe, Asia Pacific, Latin America, Middle East & Africa) - Global Industry Assessment (2016 - 2021) & Forecast (2022 - 2028).

We, at Vantage Market Research, provide quantified B2B high quality research on more than 20,000 emerging markets, in turn, helping our clients map out constellation of opportunities for their businesses. We, as a competitive intelligence market research and consulting firm provide end to end solutions to our client enterprises to meet their crucial business objectives. Our clientele base spans across 70% of Global Fortune 500 companies. The company provides high quality data and market research reports. The company serves various enterprises and clients in a wide variety of industries. The company offers detailed reports on multiple industries including Chemical Materials and Energy, Food and Beverages, Healthcare Technology, etc. The company’s experienced team of Analysts, Researchers, and Consultants use proprietary data sources and numerous statistical tools and techniques to gather and analyse information.

This report provides strategists, marketers and senior management with the critical information they need to assess the global flexible display market.

The global flexible display market is expected to grow from $10.58 billion in 2021 to $14.34 billion in 2022 at a compound annual growth rate (CAGR) of 35.6%. The flexible display market is expected to grow to $44.72 billion in 2026 at a CAGR of 32.9%.

Major players in the flexible display market are BOE Technology Group Co., LG Display Co.Ltd, Royole Corporation, Samsung Electronics Co. Ltd, Japan Display Inc., AU Optronics Corp., Innolux Corporation, Corning Incorporated, Sharp Corporation, Visionox Company, E Ink Holdings Inc., and Koninklijke Philips N.V.

The flexible display market consists of sales of flexible displays by entities (organizations, sole traders, and partnerships) that are used in virtual reality (VR) headsets, digital cameras, laptops, and televisions. A flexible display refers to an electronic display printed on a foldable plastic membrane that can easily be twisted. These displays can withstand being folded, bent, and twisted, and they are more flexible as compared to a flat display. These have better durability and are lightweight in nature.

The main types of flexible display are OLED (organic light-emitting diodes), LCD (liquid-crystal display), EPD (electronic paper display), and others.

North America was the largest region in the flexible display market in 2021. The regions covered in the flexible display market report are Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East and Africa.

The rising demand for OLED-based devices is expected to propel the growth of the flexible display market going forward. An OLED refers to an organic electroluminescent (organic EL) diode, which is a light-emitting diode, that contains an emissive electroluminescent layer that gives good quality to the picture. Most flexible displays are made of OLED displays because they give better picture quality even when the screen is bent and twisted.

For instance, according to Displaydaily, a US-based technology news publisher, in 2019, there were 3.4 million OLED display TV units sold, and this number is expected to grow by 19% to $6.4 billion units by 2024. Also in 2019, 466 million units of OLED display phones were sold. Therefore, the rising use of OLED displays in devices such as smartphones and TV is driving the growth of the flexible display market.

Technological advancements have emerged as a key trend gaining popularity in the flexible display market. Major companies operating in the flexible display market are focused on technological advancements to strengthen their position in the market.

The countries covered in the flexible display market report are Australia, Brazil, China, France, Germany, India, Indonesia, Japan, Russia, South Korea, UK, USA.

6.1. Global Flexible Display Market, Segmentation By Display Type, Historic and Forecast, 2016-2021, 2021-2026F, 2031F, $ BillionOLED (Organic Light-Emitting Diodes)

A plasma display panel (PDP) is a type of flat panel display that uses small cells containing plasma: ionized gas that responds to electric fields. Plasma televisions were the first large (over 32 inches diagonal) flat panel displays to be released to the public.

Until about 2007, plasma displays were commonly used in large televisions (30 inches (76 cm) and larger). By 2013, they had lost nearly all market share due to competition from low-cost LCDs and more expensive but high-contrast OLED flat-panel displays. Manufacturing of plasma displays for the United States retail market ended in 2014,

Plasma displays are bright (1,000 lux or higher for the display module), have a wide color gamut, and can be produced in fairly large sizes—up to 3.8 metres (150 in) diagonally. They had a very low luminance "dark-room" black level compared with the lighter grey of the unilluminated parts of an LCD screen. (As plasma panels are locally lit and do not require a back light, blacks are blacker on plasma and grayer on LCD"s.)LED-backlit LCD televisions have been developed to reduce this distinction. The display panel itself is about 6 cm (2.4 in) thick, generally allowing the device"s total thickness (including electronics) to be less than 10 cm (3.9 in). Power consumption varies greatly with picture content, with bright scenes drawing significantly more power than darker ones – this is also true for CRTs as well as modern LCDs where LED backlight brightness is adjusted dynamically. The plasma that illuminates the screen can reach a temperature of at least 1,200 °C (2,190 °F). Typical power consumption is 400 watts for a 127 cm (50 in) screen. Most screens are set to "vivid" mode by default in the factory (which maximizes the brightness and raises the contrast so the image on the screen looks good under the extremely bright lights that are common in big box stores), which draws at least twice the power (around 500–700 watts) of a "home" setting of less extreme brightness.

Plasma screens are made out of glass, which may result in glare on the screen from nearby light sources. Plasma display panels cannot be economically manufactured in screen sizes smaller than 82 centimetres (32 in).enhanced-definition televisions (EDTV) this small, even fewer have made 32 inch plasma HDTVs. With the trend toward large-screen television technology, the 32 inch screen size is rapidly disappearing. Though considered bulky and thick compared with their LCD counterparts, some sets such as Panasonic"s Z1 and Samsung"s B860 series are as slim as 2.5 cm (1 in) thick making them comparable to LCDs in this respect.

Wider viewing angles than those of LCD; images do not suffer from degradation at less than straight ahead angles like LCDs. LCDs using IPS technology have the widest angles, but they do not equal the range of plasma primarily due to "IPS glow", a generally whitish haze that appears due to the nature of the IPS pixel design.

Superior uniformity. LCD panel backlights nearly always produce uneven brightness levels, although this is not always noticeable. High-end computer monitors have technologies to try to compensate for the uniformity problem.

Uses more electrical power, on average, than an LCD TV using a LED backlight. Older CCFL backlights for LCD panels used quite a bit more power, and older plasma TVs used quite a bit more power than recent models.

Fixed-pixel displays such as plasma TVs scale the video image of each incoming signal to the native resolution of the display panel. The most common native resolutions for plasma display panels are 852×480 (EDTV), 1,366×768 and 1920×1080 (HDTV). As a result, picture quality varies depending on the performance of the video scaling processor and the upscaling and downscaling algorithms used by each display manufacturer.

Early high-definition (HD) plasma displays had a resolution of 1024x1024 and were alternate lighting of surfaces (ALiS) panels made by Fujitsu and Hitachi.

A panel of a plasma display typically comprises millions of tiny compartments in between two panels of glass. These compartments, or "bulbs" or "cells", hold a mixture of noble gases and a minuscule amount of another gas (e.g., mercury vapor). Just as in the fluorescent lamps over an office desk, when a high voltage is applied across the cell, the gas in the cells forms a plasma. With flow of electricity (electrons), some of the electrons strike mercury particles as the electrons move through the plasma, momentarily increasing the energy level of the atom until the excess energy is shed. Mercury sheds the energy as ultraviolet (UV) photons. The UV photons then strike phosphor that is painted on the inside of the cell. When the UV photon strikes a phosphor molecule, it momentarily raises the energy level of an outer orbit electron in the phosphor molecule, moving the electron from a stable to an unstable state; the electron then sheds the excess energy as a photon at a lower energy level than UV light; the lower energy photons are mostly in the infrared range but about 40% are in the visible light range. Thus the input energy is converted to mostly infrared but also as visible light. The screen heats up to between 30 and 41 °C (86 and 106 °F) during operation. Depending on the phosphors used, different colors of visible light can be achieved. Each pixel in a plasma display is made up of three cells comprising the primary colors of visible light. Varying the voltage of the signals to the cells thus allows different perceived colors.

In a monochrome plasma panel, the gas is mostly neon, and the color is the characteristic orange of a neon-filled lamp (or sign). Once a glow discharge has been initiated in a cell, it can be maintained by applying a low-level voltage between all the horizontal and vertical electrodes–even after the ionizing voltage is removed. To erase a cell all voltage is removed from a pair of electrodes. This type of panel has inherent memory. A small amount of nitrogen is added to the neon to increase hysteresis.phosphor. The ultraviolet photons emitted by the plasma excite these phosphors, which give off visible light with colors determined by the phosphor materials. This aspect is comparable to fluorescent lamps and to the neon signs that use colored phosphors.

Every pixel is made up of three separate subpixel cells, each with different colored phosphors. One subpixel has a red light phosphor, one subpixel has a green light phosphor and one subpixel has a blue light phosphor. These colors blend together to create the overall color of the pixel, the same as a triad of a shadow mask CRT or color LCD. Plasma panels use pulse-width modulation (PWM) to control brightness: by varying the pulses of current flowing through the different cells thousands of times per second, the control system can increase or decrease the intensity of each subpixel color to create billions of different combinations of red, green and blue. In this way, the control system can produce most of the visible colors. Plasma displays use the same phosphors as CRTs, which accounts for the extremely accurate color reproduction when viewing television or computer video images (which use an RGB color system designed for CRT displays).

Plasma displays are different from liquid crystal displays (LCDs), another lightweight flat-screen display using very different technology. LCDs may use one or two large fluorescent lamps as a backlight source, but the different colors are controlled by LCD units, which in effect behave as gates that allow or block light through red, green, or blue filters on the front of the LCD panel.

Each cell on a plasma display must be precharged before it is lit, otherwise the cell would not respond quickly enough. Precharging normally increases power consumption, so energy recovery mechanisms may be in place to avoid an increase in power consumption.LED illumination can automatically reduce the backlighting on darker scenes, though this method cannot be used in high-contrast scenes, leaving some light showing from black parts of an image with bright parts, such as (at the extreme) a solid black screen with one fine intense bright line. This is called a "halo" effect which has been minimized on newer LED-backlit LCDs with local dimming. Edgelit models cannot compete with this as the light is reflected via a light guide to distribute the light behind the panel.

Image burn-in occurs on CRTs and plasma panels when the same picture is displayed for long periods. This causes the phosphors to overheat, losing some of their luminosity and producing a "shadow" image that is visible with the power off. Burn-in is especially a problem on plasma panels because they run hotter than CRTs. Early plasma televisions were plagued by burn-in, making it impossible to use video games or anything else that displayed static images.

In 1983, IBM introduced a 19-inch (48 cm) orange-on-black monochrome display (Model 3290 Information Panel) which was able to show up to four simultaneous IBM 3270 terminal sessions. By the end of the decade, orange monochrome plasma displays were used in a number of high-end AC-powered portable computers, such as the Compaq Portable 386 (1987) and the IBM P75 (1990). Plasma displays had a better contrast ratio, viewability angle, and less motion blur than the LCDs that were available at the time, and were used until the introduction of active-matrix color LCD displays in 1992.

Due to heavy competition from monochrome LCDs used in laptops and the high costs of plasma display technology, in 1987 IBM planned to shut down its factory in Kingston, New York, the largest plasma plant in the world, in favor of manufacturing mainframe computers, which would have left development to Japanese companies.Larry F. Weber, a University of Illinois ECE PhD (in plasma display research) and staff scientist working at CERL (home of the PLATO System), co-founded Plasmaco with Stephen Globus and IBM plant manager James Kehoe, and bought the plant from IBM for US$50,000. Weber stayed in Urbana as CTO until 1990, then moved to upstate New York to work at Plasmaco.

In 1995, Fujitsu introduced the first 42-inch (107 cm) plasma display panel;Philips introduced the first large commercially available flat-panel TV, using the Fujitsu panels. It was available at four Sears locations in the US for $14,999, including in-home installation. Pioneer also began selling plasma televisions that year, and other manufacturers followed. By the year 2000 prices had dropped to $10,000.

In late 2006, analysts noted that LCDs had overtaken plasmas, particularly in the 40-inch (100 cm) and above segment where plasma had previously gained market share.

Until the early 2000s, plasma displays were the most popular choice for HDTV flat panel display as they had many benefits over LCDs. Beyond plasma"s deeper blacks, increased contrast, faster response time, greater color spectrum, and wider viewing angle; they were also much bigger than LCDs, and it was believed that LCDs were suited only to smaller sized televisions. However, improvements in VLSI fabrication narrowed the technological gap. The increased size, lower weight, falling prices, and often lower electrical power consumption of LCDs made them competitive with plasma television sets.

At the 2010 Consumer Electronics Show in Las Vegas, Panasonic introduced their 152" 2160p 3D plasma. In 2010, Panasonic shipped 19.1 million plasma TV panels.

Panasonic was the biggest plasma display manufacturer until 2013, when it decided to discontinue plasma production. In the following months, Samsung and LG also ceased production of plasma sets. Panasonic, Samsung and LG were the last plasma manufacturers for the U.S. retail market.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey