lcd panel market share 2016 pricelist

BOE was the leading LCD TV panel vendor during the first half of 2020, having shipped approximately 23.26 million units worldwide. In that period, global shipments of LCD TV panels totaled over 115 million units.

BOE Technology, founded in 1993, has become China’s largest TV panel maker and it continues to make a name for itself in the global consumer electronics market. It was the first company to introduce a gen 10.5 LCD plant in late 2017. Since then, BOE’s LCD panel production capacity has grown annually, surpassing former leading manufacturer LG Display. In recent years, BOE accounted for over 20 percent of large-area TFT LCD display unit shipments worldwide.

Chinese panel makers accelerate worldwide LCD TV panel shipmentsChina became the leading LCD panel producer worldwide in 2017, overtaking powerhouses South Korea and Taiwan. Chinese shipments of LCD TV panels 60-inch and larger have also increased significantly in recent years, with roughly 2.24 million units sold in the first quarter of 2019 worldwide, in comparison to just 117,000 units a year before. This figure is forecast to increase in the future, paving the way for Chinese panel makers’ worldwide success. At the same time, the concurrent specialization on large LCD panels by Chinese and South Korean suppliers will likely push down panel prices.Read moreGlobal LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor(in millions)tablecolumn chartCharacteristicBOELGDInnoluxCSOTSDCAUOCEC GroupOthers1H 202023.2611.7920.3421.312.1310.14-16.17

TrendForce. (July 28, 2020). Global LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor (in millions) [Graph]. In Statista. Retrieved January 29, 2023, from https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/

TrendForce. "Global LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor (in millions)." Chart. July 28, 2020. Statista. Accessed January 29, 2023. https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/

TrendForce. (2020). Global LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor (in millions). Statista. Statista Inc.. Accessed: January 29, 2023. https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/

TrendForce. "Global Lcd Tv Panel Unit Shipments from H1 2016 to H1 2020, by Vendor (in Millions)." Statista, Statista Inc., 28 Jul 2020, https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/

TrendForce, Global LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor (in millions) Statista, https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/ (last visited January 29, 2023)

Global LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor (in millions) [Graph], TrendForce, July 28, 2020. [Online]. Available: https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/

Prices for all TV panel sizes fluctuated and are forecast to fluctuate between 2020 and 2022. The period from March 2020 to July 2021 saw the biggest price increases, when a 65" UHD panel cost between 171 and 288 U.S. dollars. In the fourth quarter of 2021, such prices fell and are expected to drop to an even lower amount by March 2022.Read moreLCD TV panel prices worldwide from January 2020 to March 2022, by size(in U.S. dollars)Characteristic32" HD43" FHD49"/50" UHD55" UHD65" UHD------

DSCC. (January 10, 2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) [Graph]. In Statista. Retrieved January 29, 2023, from https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars)." Chart. January 10, 2022. Statista. Accessed January 29, 2023. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. (2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars). Statista. Statista Inc.. Accessed: January 29, 2023. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "Lcd Tv Panel Prices Worldwide from January 2020 to March 2022, by Size (in U.S. Dollars)." Statista, Statista Inc., 10 Jan 2022, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC, LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) Statista, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/ (last visited January 29, 2023)

LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) [Graph], DSCC, January 10, 2022. [Online]. Available: https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

1.1. THE POLICY COVERS THE HANDLING OF THE PRIVATE INFORMATION EACH USER SHARES WITH TRENDFORCE WHILE VISITING OUR WEBSITES. IF A DIFFERENT PRIVATE POLICY HAS BEEN REFERED TO FOR SPECIFIC TRENDFORCE WEBSITES AND SERVICES, THAT POLICY WILL REPLACE OR SUPPLEMENT THE PRIVACY POLICY MENTIONED IN THIS DOCUMENT. THIS POLICY ALSO COVERS INDIVIDUALS LEGALLY RESIDING IN OR ORGANIZATIONS LEGALLY BASED IN MEMBER COUNTRIES OF THE EUROPEAN UNION (EU) AND ARE SUBJECTED TO EU GENERAL DATA PROTECTION REGULATION (GDPR) WITH REGARD TO PROVISION OF SERVICES AND PERSONAL DATA PROTECTION.

2.1 THE WEBSITE WILL COLLECT AND USE USER INFORMATION FOR PURPOSES SUCH AS MARKETING, CONSUMER PROTECTION, CONSUMER/CLIENT MANAGEMENT, E-COMMERCE SERVICES, FINANCIAL ACCOUNTING, CONTRACTUAL MATTERS, RESEARCH ANALYSIS, AND DATA PROCESSING. WHEN REQUIRED BY LAW, THE WEBSITE MAY ALSO PROVIDE PERSONAL INFORMATION TO NON-GOVERNMENT AGENCIES.

THE WEBSITE WILL NOT DISCLOSE OR SHARE ANY PERSONAL INFORMATION EXCPET PER SPECIAL REQUEST OR WHEN PERMISSION IS RECEIVED FROM THE USER. OTHER EXCEPTIONS INCLUDE:

IN ACCORDANCE WITH ARTICLE 3 OF THE PERSONAL INFORMATION PROTECTION LAW, YOU WILL HAVE THE OPTION TO EXERCISE THE FOLLOWING RIGHTS WITH REGARD TO THE PERSONAL INFORMATION SHARED WITH THE WEBSITE:

a. TO PREVENT UNAUTHORIZED PARTIES FROM ACCESSING, MODIFYING, OR LEAKING PERSONAL USER DATA, THE WEBSITE WILL TAKE STEPS TO IMPLEMENT PROPER SAFETY MEASURES. THE DATA SEARCHED AND RECORDED ON THE WEBSITE AND THE APPROPRIATE SAFETY MEASURES CHOSEN WILL ALL BE REVIEWED CAREFULLY. CONSIDERING HOW THE SAFETY OF TRANSMITTING DATA ON THE INTERNET CAN NEVER BE GUARANTEED COMPLETELY, USERS SHOULD KEEP IN MIND ALL POSSIBLE RISKS ASSOCIATED WITH ONLINE DATA TRANSFERS AND TAKE RESPONSIBILITY FOR ANY INFORMATION SHARED WITH OR OBTAINED FROM THE WEBSITE.

BE SURE TO PROTECT ALL PASSWORDS AND PERSONAL INFORMATION, REFRAIN FROM DISCLOSING PRIVATE USER INFORMATION TO ANY THIRD PARTY, AND REGISTER WITH THE WEBSITE UPON COMPLETING ALL NECESSARY MEMBERSHIP PROCEDURES. WHEN USING A SHARED OR PUBLIC COMPUTER, PLEASE MAKE SURE TO PROPERLY CLOSE ALL RELEVANT BROWSERS TO PREVENT OTHERS FROM READING YOUR PERSONAL E-MAILS OR INFORMATION.

The upstream materials or components of the LCD panel industry mainly include liquid crystal materials, glass substrates, polarizing lenses, and backlight LEDs (or CCFL, which accounts for less than 5% of the market).

The middle reaches is the main panel factory processing and manufacturing, through the glass substrate TFT arrays and CF substrate, CF as upper and TFT self-built perfusion liquid crystal and the lower joint, and then put a polaroid, connection driver IC and control circuit board, and a backlight module assembling, eventually forming the whole piece of LCD module. The downstream is a variety of fields of application terminal-based brand, assembly manufacturers. At present, the United States, Japan, and Germany mainly focus on upstream raw materials, while South Korea, Taiwan, and the mainland mainly seek development in mid-stream panel manufacturing.

With the successive production of the high generation line in mainland China, the panel production capacity and technology level have been steadily improved, and the industrial competitiveness has been gradually enhanced. Nowadays, the panel industry is divided into three parts: South Korea, mainland China, and Taiwan, and mainland China is expected to become the no.1 in the world in 2019.

In the past decade, China’s panel display industryhas achieved leapfrog development, and the overall size of the industry has ranked among the top three in the world. Chinese mainland panel production capacity is expanding rapidly, although Japanese panel manufacturers master a large number of key technologies, gradually lose the price competitive advantage, compression panel production capacity. Panel production is concentrated in South Korea, Taiwan, and China, which is poised to become the world’s largest producer of LCD panels.

Up to 2016, BOE‘s global market share continued to increase: smartphone LCD, tablet PC display, and laptop display accounted for the world’s first market share, and display screen increased to the world’s second, while TV LCD remained the world’s third. In LCD TV panels, Chinese panel makers have accounted for 30 percent of global shipments to 77 million units, surpassing Taiwan’s 25.5 percent market share for the first time and ranking second only to South Korea.

In terms of the area of shipment, the area of board shipment of JD accounted for only 8.3% in 2015, which has been greatly increased to 13.6% in the first half of 2016, while the area of shipment of hu xing optoelectronics in the first half of 2015 was only 5.1%, which has reached 7.8% in the first half of 2016. The panel factories in mainland China are expanding their capacity at an average rate of double-digit growth and transforming it into actual shipments and areas of shipment. On the other hand, although the market share of South Korea, Japan, and Taiwan is gradually decreasing, some South Korean and Japanese manufacturers have been inclined to the large-size HD panel and AMOLED market, and the production capacity of the high-end LCD panel is further concentrated in mainland China.

Domestic LCD panel production line capacity gradually released, overlay the decline in global economic growth, lead to panel makers from 15 in the second half began, in a low profit or loss, especially small and medium-sized production line, the South Korean manufacturers take the lead in transformation strategy, closed in medium and small size panel production line, South Korea’s 19-panel production line has shut down nine, and part of the production line is to research and development purposes. Some production lines are converted to LTPS production lines through process conversion. Korean manufacturers are turning to OLED panels in a comprehensive way, while Japanese manufacturers are basically giving up the LCD panel manufacturing business and turning to the core equipment and materials side. In addition to the technical direction of the research and judgment, more is the LCD panel business orders and profits have been severely compressed, Korean and Japanese manufacturers have no desire to fight. Since many OLED technologies are still in their infancy in mainland China, it is a priority to move to high-end panels such as OLED as soon as possible. Taiwanese manufacturers have not shut down factories on a large scale, but their advantages in LCD technology and OLED technology have been slowly eroded by the mainland.

STONE provides a full range of 3.5 inches to 15.1 inches of small and medium-size standard quasi TFT LCD module, LCD display, TFT display module, display industry, industrial LCD screen, under the sunlight visually highlight TFT LCD display, industrial custom TFT screen, TFT LCD screen-wide temperature, industrial TFT LCD screen, touch screen industry. The TFT LCD module is very suitable for industrial control equipment, medical instruments, POS system, electronic consumer products, vehicles, and other products.STONE provides a full range of 3.5 inches to 15.1 inches of small and medium-size standard quasi TFT LCD module, LCD display, TFT display module, display industry, industrial LCD screen, under the sunlight visually highlight TFT LCD display, industrial custom TFT screen, TFT LCD screen-wide temperature, industrial TFT LCD screen, touch screen industry. The TFT LCD module is very suitable for industrial control equipment, medical instruments, POS system, electronic consumer products, vehicles, and other products.

LCD panel prices have risen for 4 months in a row because of your home gaming? Since this year, the whole LCD panel market has smoked. Whether after the outbreak of the epidemic, LCD panel market prices rose for four months, or the panel giants in Japan and South Korea successively sold production lines, or the Chinese mainland listed companies frequently integrated acquisition, investment, and plant construction, all make the industry full of interesting.

LCD panel prices are already a fact. Since May this year, LCD panel prices have risen for four months in a row, making the whole industry chain dynamic. Why are LCD panels going up in price in a volatile 2020? The key factor lies in the imbalance between supply and demand.

The price of LCDS for large-size TVs of 70 inches or more hasn’t budged much. In addition, LTPS screens and AMOLED screens used in high-end phones have seen little or no increase in price.

As for October, LCD panel price increases are expected to moderate. The data shows that in October 32 inches or 2 dollars; Gains of 39.5 to 43 inches will shrink to $3;55 inches will fall back below $10; The 65-inch gain will narrow to $5.

During the epidemic, people stayed at home and had no way to go out for entertainment. They relied on TV sets, PCS, and game consoles for entertainment. After the resumption of economic work and production, the market of traditional home appliances picked up rapidly, and LCD production capacity was quickly digested.

However, due to the shutdown of most factories lasting 1-2 months during the epidemic period, LCD panel production capacity was limited, leading to insufficient production capacity in the face of the market outbreak, which eventually led to the market shortage and price increase for 4 consecutive months.

In fact, the last round of price rise of LCD panels was from 2016 to 2017, and its overall market price has continued to fall since 2018. Even in 2019, individual types have fallen below the material cost, and the whole industry has experienced a general operating loss. As a result, LCD makers have been looking for ways to improve margins since last year.

A return to a reasonable price range is the most talked about topic among panel makers in 2019, according to one practitioner. Some manufacturers for the serious loss of the product made the decision to reduce production or even stop production; Some manufacturers planned to raise the price, but due to the epidemic in 2020, the downstream demand was temporarily suppressed and the price increase was postponed. After the outbreak was contained in April, LCD prices began to rise in mid-to-late May.

In fact, the market price of LCD panels continued to decline in 2018-2019 because of the accelerated rise of China’s LCD industry and the influx of a large number of local manufacturers, which doubled the global LCD panel production capacity within a few years, but there was no suitable application market to absorb it. The result of excess capacity is oversupply, ultimately making LCD panel prices remain depressed.

Against this background, combined with the impact of the epidemic in 2020, the operating burden of LCD companies in Japan and South Korea has been further aggravated, and it is difficult to make profits in the production of LCD panels, so they have to announce the withdrawal of LCD business.

business in June 2022. In August, Sharp bought JDI Baishan, a plant in Ishikawa prefecture that makes liquid crystal display panels for smartphones. In early September, Samsung Display sold a majority stake in its SUZHOU LCD production plant to Starlight Electronics Technology, a unit of TCL Technology Group. LGD has not only pulled out of some of its production capacity but has announced that it will close its local production line in 2020. According to DSCC, a consultancy, the share of LCD production capacity in South Korea alone will fall from 19% to 7% between 2020 and 2021.

It is worth mentioning that in industry analysis, in view of the fact that Korean companies are good at using “dig through old bonus – selling high price – the development of new technology” the cycle of development mode, another 2020 out of the LCD production capacity, the main reason may be: taking the advantage of China’s expanding aggressively LCD manufacturers, Korean companies will own LCD panel production line hot sell, eliminating capacity liquid to extract its final value, and turning to the more profitable advantage of a new generation of display technologies, such as thinner, color display better OLED, etc. Samsung, for example, has captured more than 80% of the OLED market with its first-mover advantage.

From the perspective of production capacity, the launch of LCD tracks by major manufacturers in Japan and South Korea must reduce some production capacity in the short term, which to some extent induces market price fluctuations. In the long run, some of the Japanese and Korean LCD production capacity has been bought by Chinese manufacturers, coupled with frequent investment in recent years, the overall capacity is sure to recover as before, or even more than before. But now it will take time to expand the production layout, which more or less will cause supply imbalance, the industry needs to be cautious.

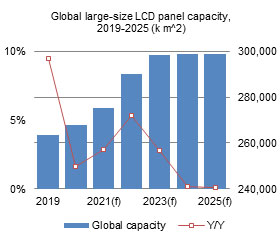

The LCD panel industry started in the United States and then gradually moved to Japan, South Korea, China, and Taiwan. At present, the proportion of production capacity in The Chinese mainland has reached 52% in 2020, and there are leading LCD panel products in China represented by BOE, Huxing Optoelectronics. Meanwhile, the production capacity layout of BOE, Huike, Huxing Optoelectronics, and other manufacturers has been basically completed, making industrial integration a necessity.

On the one hand, South Korean enterprises out of the LCD track, the domestic factory horse enclosure, plant expansion action. While LCDs may not sell as well as “upstart” flexible screens, respondents believe they are still strong enough in the traditional home appliance market to warrant continued investment. Zhao Bin, general manager of TCL Huaxing Development Center, has said publicly that the next-generation display technology will be mature in four to five years, but the commercialization of products may not take place until a decade later. “LCD will still be the mainstream in this decade,” he said.

On the other hand, there is no risk of neck jam in China’s LCD panel industry, which is generally controllable. In mainland China, there will be 21 production lines capable of producing 32-inch or larger LCD panels by 2021, accounting for about two-thirds of the global total. In terms of the proportion of production capacity, the Chinese mainland accounted for 42% of the global LCD panel in 2019, 51% this year, and will continue to climb to 63% next year.

Of course, building factories and expanding production cannot be accomplished overnight. In the process of production capacity recovery, it is predicted that there will be several price fluctuations, and the cost may be passed on to the downstream LCD panel manufacturers or consumers when the price rises greatly, which requires continuous attention.

Large LCD panel prices have been continuously increasing for last 10 months due to an increase in demand and tight supply. This has helped the LCD industry to recover from drastic panel price reductions, revenue and profit loss in 2019. It has also contributed to the growth of Quantum Dot and MiniLED LCD TV.

Strong LCD TV panel demand is expected to continue in 2021, but component shortages, supply constraints and very high panel price increase can still create uncertainties.

LCD TV panel capacity increased substantially in 2019 due to the expansion in the number of Gen 10.5 fabs. After growth in 2018, LCD TV demand weakened in 2019 caused by slower economic growth, trade war and tariff rate increases. Capacity expansion and higher production combined with weaker demand resulted in considerable oversupply of LCD TV panels in 2019 leading to drastic panel price reductions. Some panel prices went below cash cost, forcing suppliers to cut production and delay expansion plans to reduce losses.

Panel over-supply also brought down panel prices to way lower level than what was possible through cost improvement. Massive 10.5 Gen capacity that can produce 8-up 65" and 6-up 75" panels from a single mother glass substrate helped to reduce larger size LCD TV panel costs. Also extremely low panel price in 2019 helped TV brands to offer larger size LCD TV (>60-inch size) with better specs and technology (Quantum Dot & MiniLED) at more competitive prices, driving higher shipments and adoption rates in 2019 and 2020.

While WOLED TV had higher shipment share in 2018, Quantum Dot and MiniLED based LCD TV gained higher unit shares both in 2019 and 2020 according to Omdia published data. This trend is expected to continue in 2021 and in the next few years with more proliferation of Quantum Dot and MiniLED TVs.

Panel suppliers’ financial results suffered in 2019 as they lost money. Suppliers from China, Korea and Taiwan all lowered their utilization rates in the second half of 2019 to reduce over-supply. Very low prices combined with lower utilization rates made the revenue and profitability situation for panel suppliers difficult in 2019. BOE and China Star cut the utilization rates of their Gen 10.5 fabs. Sharp delayed the start of production at its 10.5 Gen fab in China. LGD and Samsung display decided to shift away from LCD more towards OLED and QDOLED respectively. Both companies cut utilization rates in their 7, 7.5 and 8.5 Gen fabs. Taiwanese suppliers also cut their 8.5 Gen fab utilization rates.

An increase in demand for larger size TVs in the second half of 2020 combined with component shortages has pushed the market to supply constraint and caused continuous panel price increases from June 2020 to March 2021. Market demand for tablets, notebooks, monitors and TVs increased in 2020 especially in the second half of the year due to the impact of "stay at home" regulations, when work from home, education from home and more focus on home entertainment pushed the demand to higher level.

With stay at home continuing in the firts half of 2021 and expected UEFA Europe football tournaments and the Olympic in Japan (July 23), TV brands are expecting stronger demand in 2021. The panel price increase resulting in higher costs for TV brands. It has also made it difficult for lower priced brands (Tier2/3) to acquire enough panels to offer lower priced TVs. Further, panel suppliers are giving priority to top brands with larger orders during supply constraint. In recent quarters, the top five TV brands including Samsung, LG, and TCL have been gaining higher market share.

From June 2020 to January 2021, the 32" TV panel price has increased more than 100%, whereas 55" TV panel prices have increased more than 75% and the 65" TV panel price has increased more than 38% on average according to DSCC data. Panel prices continued to increase through Q1 and the trend is expected to continue in Q2 2021 due to component shortages.

Major increases in panel prices from June 2020, have increased costs and reduced profits for TV brand manufacturers. TV brands are starting to increase TV set prices slowly in certain segments. Notebook brands are also planning to raise prices for new products to reflect increasing costs. Monitor prices are starting to increase in some segments. Despite this, buyers are still unable to fullfill orders due to supply issues.

TV panel prices increased in Q4 2020 and are also expected to increase in the first half of 2021. This can create challenges for brand manufacturers as it reduces their ability to offer more attractive prices in coming months to drive demand. Still, set-price increases up to March have been very mild and only in certain segments. Some brands are still offering price incentives to consumers in spite of the cost increases. For example, in the US market retailers cut prices of big screen LCD and OLED TV to entice basketball fans in March.

Higher LCD price and tight supply helped LCD suppliers to improve their financial performance in the second half of 2020. This caused a number of LCD suppliers especially in China to decide to expand production and increase their investment in 2021.

New opportunities for MiniLED based products that reduce the performance gap with OLED, enabling higher specs and higher prices are also driving higher investment in LCD production. Suppliers from China already have achieved a majority share of TFT-LCD capacity.

BOE has acquired Gen 8.5/8.6 fabs from CEC Panda. ChinaStar has acquired a Gen 8.5 fab in Suzhou from Samsung Display. Recent panel price increases have also resulted in Samsung and LGD delaying their plans to shut down LCD production. These developments can all help to improve supply in the second half of 2021. Fab utilization rates in Taiwan and China stayed high in the second half of 2020 and are expected to stay high in the first half of 2021.

QLED and MiniLED gained share in the premium TV market in 2019, impacting OLED shares and aided by low panel prices. With the LCD panel price increases in 2020 the cost gap between OLED TV and LCD has gone down in recent quarters.

OLED TV also gained higher market share in the premium TV market especially sets from LG and Sony in the last quarter of 2020, according to industry data. LG Display is implimenting major capacity expansion of its OLED TV panels with its Gen 8.5 fab in China.Strong sales in Q4 2020 and new product sizes such as 48-inch and 88-inch have helped LG Display’s OLED TV fabs to have higher utilization rates.

Samsung is also planning to start production of QDOLED in 2021. Higher production and cost reductions for OLED TV may help OLED to gain shares in the premium TV market if the price gap continues to reduce with LCD.

Lower tier brands are not able to offer aggressive prices due to the supply constraint and panel price increases. If these conditions continue for too long, TV demand could be impacted.

Strong LCD TV demand especially for Quantum Dot and MiniLED TV is expected to continue in 2021. The economic recovery and sports events (UEFA Europe footbal and the Olympics in Japan) are expected to drive demand for TV, but component shortages, supply constraints and too big a price increase could create uncertainties. Panel suppliers have to navigate a delicate balance of capacity management and panel prices to capture the opportunity for higher TV demand. (SD)

Sweta Dash, President, Dash-InsightsSweta Dash is the founding president of Dash-Insights, a market research and consulting company specializing in the display industry. For more information, contact

TFT or thin-film transistor is combined with LCD to improve colour quality leading to a sharper image, as each pixel on a TFT-LCD is attached to a transistor. Due to the small sizes of each transistor, TFT-LCD display panels consume less power. They are widely used in computers, TVs, laptops, and mobile phones as it gives a more enhanced image than older technologies and prevents the distortion of image.

With the growing applications of TFT-LCD, there has been an increased competition among the manufacturers for the best cutting technology, i.e. ‘generations’, to produce TFT-LCD panels. In 2017, BOE, one of the major TFT-LCD manufacturers globally, put the world’s highest generation line, Generation 10.5 TFT-LCD production line, into production ahead of schedule in Hefei, China. With more Gen 10.5 facilities starting mass production, the market is primed for the production of 65 inches and larger TFT-LCD panels. More than 85.5% of the TFT-LCD display panels consumed in 2018 were large-sized panels sized over 10 inches.

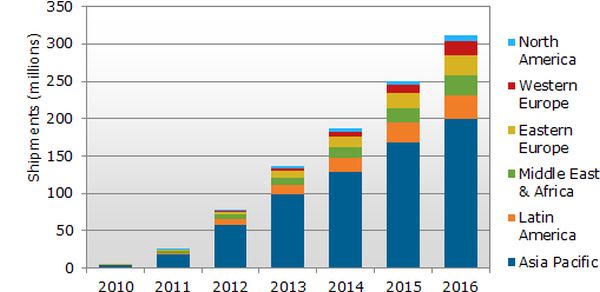

Driven by the demand for TFT-LCD display panels in TV and monitor panels, the global shipment of large TFT-LCD panels grew again in 2018, despite over-supply concerns. The market is also driven by a rising demand for automotive displays. While automotive display systems were earlier reserved for luxury vehicles, cars for the mass-market are increasingly including high resolution display systems in their design due to a decline in prices along with the rising production and demand for automobiles. This growth in automotive displays has been supported by the rising investments in automotive display panels by big display panel manufacturers in Asia. The Asia Pacific countries like China and India are the fastest growing markets in the region due to rapid economic growth and a growing demand for consumer-based electronics. Currently, the global market for TFT-LCD display panel is dominated by North America.

Region-wise, the global market for TFT-LCD display panel can be divided into North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

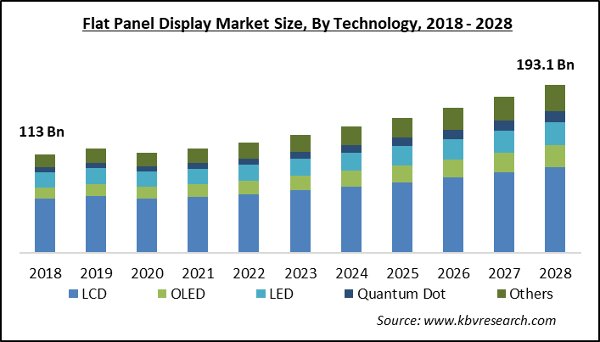

The report also offers historical (2018-2022) and forecast (2023-2028) market information for the sizes, applications, and major regions of TFT-LCD display panel.

The report analyses the market dynamics, covering the key demand and price indicators in the market, along with providing an assessment of the SWOT and Porter’s Five Forces models.

The major players in the global TFT-LCD display panel market are Samsung Electronics Co., Ltd., LG Display Co., Ltd., Japan Disney Inc., Sharp Corporation, BOE Technology Group Co., Ltd., AUO Corporation, Raystar Optronics Inc., WINSTAR Display Co., Ltd., Kingtech Group Co., Ltd., and Tricomtek Co., Ltd., among others. The comprehensive report by EMR looks into the market share, capacity, and latest developments like mergers and acquisitions, plant turnarounds, and capacity expansions of the major players.

*At Expert Market Research, we strive to always give you current and accurate information. The numbers depicted in the description are indicative and may differ from the actual numbers in the final EMR report.

Strong demand for LCD products combined with concerns about shortages in key components have driven LCD TV panel prices to their most significant increases ever on a percentage basis, and prices show no signs of slowing down in Q2. In our last update in early April, we anticipated that price increases would decelerate in Q2, but we now see price increases accelerating compared to Q1. Panel prices increased by 27% in Q4 2020 compared to Q3 and slowed down to 14.5% in Q1 2021 compared to Q4, but our current estimate is that average LCD TV panel prices in Q2 2021 will increase by another 17%. We now expect prices to peak sometime in Q3 2021.

LG Display’ shipments of 65" and 75" TV panels increased significantly by 38.5% and 132.7% respectively, indicating its preparation for further competition with BOE in large-size TV panel sector.

WitsView, a division of TrendForce, reports that global LCD TV panel shipments increased quarter by quarter in 2017. 1H17 showed less momentum for holiday sales due to the high prices, but shipments rebounded in 2H17 as the prices declined and TV makers prepared for the year-end sales. Moreover, the new production capacities of BOE’s Gen 8.5 fab in Fuqing and HKC’s Gen 8.6 fab in Chongqing have been focusing on middle-size TV panels (43" and 32" respectively), bringing the annual shipments beyond expectation to 263.83 million pieces, an increase of 1.3% compared with 2016.

As for 2018, Iris Hu, research manager of WitsView, points out that panel makers will continue to increase the production shares of large-size panels and UHD panels to boost the revenue and profit. “The penetration rate of UHD panels is expected to reach 42% this year, an increase of 7.4 percentage points compared with 2017”, says Hu. Regarding the new production capacity, BOE’s Gen 10.5 fab produces mainly large-size TV panels (65" and 75"), but CEC’s two fabs still put their priorities at middle-size ones (32" and 50"). Meanwhile, replacement of CRT TV sets with 32" and 23.6" LCD ones is still ongoing in emerging markets, making the average panel size grow slower to 45.8 inches, only 1.3 inches up from 2017. Overall speaking, global TV panel shipments this year will have chance to hit a second-highest number in history, reaching 269.49 million pieces, an annual increase of 2.2%.

In the global TV panel shipment ranking for 2017, LG Display (LGD) came first place with a shipment of around 50.85 million pieces last year, a decrease of 3.9%. LGD expanded its production capacity in Guangzhou fab for 50K sheet, but in terms of panel size, increasing the production capacity share of 65" and greater panels has been the trend. Particularly, LGD shipments of 65" and 75" panels have increased significantly by 38.5% and 132.7% respectively, indicating that LGD has been making efforts to retain its market share in large-size TV panel sector before BOE’s Gen 10.5 fab enter mass production.

BOE deliberately slowed down its 32" TV panel production growth in 2017, so the shipments of this size increased by only 0.4%, totaling 43.81 million pieces. But its total shipments climbed to second place for the first time as Samsung Display (SDC)’s closure of L7-1 fab influenced its production. As BOE’s Gen 8.5 fab in Fuqing entered mass production in 2Q17, BOE’s shipments of 43" TV panels grew remarkably by 247.6% last year.

Innolux’s Gen 8.6 fab entered mass production in early 2017, but the yield rate and output were less than expectation in the first half of 2017. In the second half, high pricing of panels led to shrinking demand, resulting in Innolux’s slow-moving and excess stocks. In addition, Innolux announced to enter the TV assembly market, which made its clients more conservative in making orders. Fortunately Innolux figured out the solutions of pricing and stock problems, and ended up with shipments of 41.8 million pieces, an increase of 0.2%, ranking the third.

SDC’s shipments saw a substantial decline of 15.4% last year since the closure of its L7-1 fab. Its overall TV panel shipments turned out to be 39.6 million pieces, the highest decline among the six major panel makers. Although its shipments have dropped out of top 3, SDC has improved capacity utilization by simplifying its product mix, and has invested in production equipment of UHD and large-size panels to increase the value of its products. As for product portfolio, SDC took initiatives to develop UHD panels, whose proportion came to 54.6% among all of SDC’s products, and also remained a major supplier of large-size panels (55", 65" and 75"). Particularly, its market share of 65" sector was as high as 36.3%, showing definite advantages over its competitors.

China Star Optoelectronics Technology (CSOT) kept increasing the shipments after the capacity of the second phase of its second Gen 8.5 fab was expanded to 140K sheet. CSOT’s final shipments recorded 38.64 million pieces, an increase of 16.8% compared with the previous year. Particularly, 55" panels recorded a 19.4% shipment growth, as CSOT’s capacity expansion came mainly from this size. As for the growth by shipment area, CSOT recorded a 19.6% YoY increase, the highest among the six major panel makers.

TV panel shipments for AU Optronics (AUO) in 2017 came to around 27.21 million pieces, 0.1% down from the previous year. AUO continued to optimize its product portfolio and increased the proportion of large-size panels, so it finally recorded a 5.1% growth of shipment area. In addition, AUO also put focus on increasing the proportion of UHD products, reaching 44% of all its products, the third highest number following LGD and SDC.

This market research report includes a detailed segmentation of the global large area LCD display market by application (TVs, notebooks, monitors, tablets, and others). It outlines the market shares for key regions such as the Americas, APAC, and EMEA. The key vendors analyzed in this report are AU Optronics, BOE Technology, Innolux, LG Display, and Samsung Display.

Technavio’s research analyst predicts the global large area LCD display market to grow at a CAGR of 3% during the forecast period. The formation of UHD alliances is the primary growth driver for this market. During 2015, supply chain members of the global UHD TV market announced the formation of the UHD Alliance to support innovative technologies including 4K and higher resolution, high dynamic range, immersive 3D audio, and wider color gamut.

The decline in ASP of the LCD panel is expected to boost the market growth during the forecast period. During 2014, per meter square, ASP of LCD panel was $472, which declined to $416 during 2015. Vendors reduced the ASP to reduce excess inventory. The declining per square meter ASP of LCD panel drove the shipment of LCD display in terms of area.

During 2015, the TV segment dominated the large area LCD display market with a market share of 38%. The primary reason for the growth of this product segment was the strong demand for 4K TVs of 40 inches and larger screen size. During 2015, several manufacturers introduced 4K TVs ranging from 50 inches and above.

During 2015, APAC accounted for 81% of the market share and is expected to grow at a CAGR of 1% during the forecast period. The high concentration of display device manufacturers and LCD panel manufacturers in this region are the primary growth drivers. Technavio expects that the well-established supply chain for display devices in APAC would continue to support the dominance of this region in the market during the forecast period. China is emerging fast as a leading hub for large area TFT LCD display manufacturers because of the rise in the number of display device manufacturers in the country.

Manufacturing LCD display panels require economies of scale because the equipment used to manufacture displays are expensive. This presents high entry barriers for LCD display panel manufacturers. Currently, the global large area LCD display market is dominated by China, Japan, South Korea, and Taiwan in terms of production and revenue contribution. Chinese manufacturers have the advantage of manufacturing LCD panels at a lower cost. This has resulted in price wars among LCD manufacturers and has accelerated the declining ASP of LCD panels. Vendors such as LG and Samsung are under a lot of pressure as profit margins have come down because of increased competition.

Other prominent vendors in the market include Chi Mei Optoelectronics, Chunghwa Picture Tube (CPT), HannsTouch Solution, HannStar Display, InfoVision Optoelectronics, Japan Display, Kaohsiung Opto-Electronics, NEC Display Solutions, Panasonic, and Sharp.

LG Display and Samsung Display are struggling to find their ways out of the deterioration of their performance even after withdrawing from production of liquid crystal display (LCD) panels. The high-priced organic light emitting diode (OLED) panel sector regarded as a future growth engine is not growing fast due to the economic downturn. Even in the OLED panel sector, Chinese display makers are within striking distance of Korean display makers, experts say.

On Aug. 30, Display Supply Chain Consultants (DSCC), a market research company, predicted that LCD TV panel prices hit an all-time low in August and that an L-shaped recession will continue in the fourth quarter. According to DSCC, the average price of a 65-inch ultra-high-definition (UHD) panel in August was only US$109, a 62 percent drop from the highest price of US$288 recorded in July in 2021. The average price of a 75-inch UHD panel was only US$218, which was only about half of the highest price of US$410 in July last year. DSCC predicted that the average panel price in the third quarter will fall by 15.7 percent. As Chinese companies’ price war and the effect of stagnation in consumption overlapped, the more LCD panels display makers produce, the more loss they suffer.

As panel prices fell, manufacturers responded by lowering facility utilization rates. DSCC said that the LCD factory utilization rate descended from 87 percent in April to 83 percent in May, 73 percent in June, and 70 percent in July.

Now that the LCD panel business has become no longer lucrative, Korean display makers have shut down their LCD business or shrunk their sizes. In the LCD sector, China has outpaced Korea since 2018. China’s LCD market share reached 50.9 percent in 2021, while that of Korea dropped to 14.4 percent, lower than Taiwan’s 31.6 percent.

Samsung Display already announced its withdrawal from the LCD business in June. Only 10 years have passed since the company was spun off from Samsung Electronics in 2012. LG Display has decided to halt domestic LCD TV panel production until 2023 and reorganize its business structure centering on OLED panels. Its Chinese LCD production line will be gradually converted to produce LCD panels for IT or commercial products. TrendForce predicted that LG Display will stop operating its P7 Plant in the first quarter of next year.

Korean display makers’ waning LCD business led to a situation in which Korea even lost first place in the display industry. Korea with a display market share of 33.2 percent was already overtaken by China with 41.5 percent) in 2021 according to market researcher Omdia and the Korea Display Industry Association. Korea’s market share has never rebounded in for five years since 2017 amid the Korean government’s neglect. Seventeen years have passed since 2004 when Korea overtook Japan to rise to the top of the world in the LCD industry. Korea’s LCD exports amounted to more than US$30 billion in 2014, but fell to US$21.4 billion last year.

A bigger problem is that Korean display makers may lose its leadership in the OLED panel sector although it is still standing at the top spot. While Korea’s OLED market share fell from 98.1 percent in 2016 to 82.8 percent last year, that of China rose from 1.1 percent to 16.6 percent. Considering that the high-end TV market is highly likely to shrink for the time being due to a full-fledged global consumption contraction, some analysts say that the technology gap between Korea and China can be sharply narrowed through this looming TV market slump. According to industry sources, the Chinese government is now focusing on giving subsidies to the development of OLED panel technology rather LCD technology. On the other hand, in Korea, displays were also wiped out from national strategic technology industry items under the Restriction of Special Taxation Act which can receive tax benefits for R&D activities on displays.

According to CINNO Research"s monthly LCD TV LCD panel shipment report, in February 2020, global LCD TV panel shipments were 19.64 million, a 5.1% month-on-month decrease from January 2020 and a 5.6% year-on-year decrease from February 2019. Problems such as tight logistics resources and poor supply chain operation caused by the COVID-19 epidemic were one of the main reasons for the decline in LCD TV shipments in February.

Starting from the end of 2019, LCD TV panel prices gradually stopped falling and began to rebound. Due to the impact of the COVID-19 epidemic on the supply chains of China and South Korea, the tension in panel supply has been further exacerbated in the short term, which has contributed to the rebound in panel prices. On the other hand, as the spread of the international epidemic continues to deteriorate, sports events that were originally considered to be crucial to TV sales such as the Champions League, European Cup, NBA, E3 2020, etc. have been cancelled or postponed, and the Tokyo Olympics also faced serious delays. Risks have added many variables to 2020, and the reduction in demand is expected to be difficult to support the continued increase in panel prices.

As Korean companies gradually withdrew from the LCD TV market, and the new capacity of mainland Chinese manufacturers has gradually achieved success, according to CINNO Research"s monthly LCD TV LCD panel shipment report, in terms of shipments, mainland China panel manufacturers in February 2020, it has accounted for 59.4% of total shipments, close to 60%. TCL CSOT became the world"s largest LCD TV panel supplier for the first time with 18.8% share, BOE ranked second with 17.4% market share, and HKC shipments also grew rapidly, ranking third with 13.4% share, Innolux and Samsung Display SDC ranked 4-5 with 12.3% and 10.5%.

According to CINNO Research"s monthly LCD TV LCD panel shipment report, in terms of shipment area, panel manufacturers in mainland China accounted for 56.6% of the total shipment area. CSOT also won the first place with a share of 19.6%, BOE, Samsung Display SDC, CEC (including Panda, Rainbow), LG Display LGD ranked 18.7%, 12.6%, 10.8% and 10.2% respectively. 2nd to 5th.

Large-area TFT LCD panel shipments decreased by 10% Month on Month (MoM) and 5% Year on Year (YoY) in April, to 74.1million units, representing historically low shipment performance since May 2020. Omdia defines large-area TFT LCD displays as larger than 9 inches.

"With continued ramifications from the pandemic, demand for IT panels for monitors and notebook PCs remained strong in 4Q21. But as the market became saturated starting in 2022, IT panel shipments started slowing in 1Q22 and early 2Q22," said Robin Wu, Principal Analyst for Large Area Display & Production, Omdia.

Wu said that notebook panel shipments decreased 21% MoM in April, to 18.2 million units, or a 33% decrease from a peak of 27.3 million units in November 2021.

While TV panel prices have decreased noticeably since 3Q21, TV LCD panel shipments increased to a peak of 23.4 million in December 2021, driven by low prices. But rising inflation, the Ukraine crisis and continued lockdowns in China have slowed demand. As a result, TV panel shipments posted a 9% MoM decline in April, to 21.7million units.

Many TV panel prices have fallen below manufacturing cost, and panel makers began to lose money in their TV panel business starting in 4Q21. But Chinese panel makers, the biggest capacity owners, still haven"t reduced their fab utilization. With no sign of demand recovery in 2Q22 or even 3Q22, the supply/demand situation is unlikely to see improvement, Wu said.

"IT LCD panels could still deliver positive cash flow for panel makers. But with prices dropping dramatically, panel makers will soon start to lose money in their IT panel business," Wu said. "Maybe only then will panel makers reduce their glass input and the overall supply/demand situation will return to balance."

About OmdiaOmdia is a leading research and advisory group focused on the technology industry. With clients operating in over 120 countries, Omdia provides market-critical data, analysis, advice, and custom consulting.

LG takes pride as the leading provider of innovative, flexible and feature-packed Commercial Display Products in the market. Boasting the cutting-edge features and modern design, LG Commercial Displays redefines a whole new way of delivering an ultimate viewing experience to enhance engagement with the audience. From Ultra UD OLED monitors for a digital signage network to hospitality TVs for in-room entertainment solutions, LG Commercial Displays offer a variety of display products to meet the demands of every business environment including:

Global TFT LCD Panel Market Report (97 Pages) provides exclusive vital statistics, data, information, trends and competitive landscape details in this niche sector.

This report aims to provide a comprehensive presentation of the global market for TFT LCD Panel, with both quantitative and qualitative analysis, to help readers develop business/growth strategies, assess the market competitive situation, analyze their position in the current marketplace, and make informed business decisions regarding TFT LCD Panel.

The TFT LCD Panel market size, estimations, and forecasts are provided in terms of output/shipments (K Units) and revenue (USD millions), considering 2021 as the base year, with history and forecast data for the period from 2017 to 2027. This report segments the global TFT LCD Panel market comprehensively. Regional market sizes, concerning products by types, by application, and by players, are also provided. The influence of COVID-19 and the Russia-Ukraine War were considered while estimating market sizes.

The TFT LCD Panel market report provides answers to the following key questions: ● What is the global (North America, Europe, Asia-Pacific, South America, Middle East and Africa) sales value, production value, consumption value, import and export of TFT LCD Panel?

● Who are the global key manufacturers of the TFT LCD Panel Industry? How is their operating situation (capacity, production, sales, price, cost, gross, and revenue)?

Key inclusions of the TFT LCD Panel market report: ● To provide the leading TFT LCD Panel companies, their company profiles, product portfolios, market shares, and revenue analyses.

The research report has incorporated the analysis of different factors that augment the market’s growth. It constitutes trends, restraints, and drivers that transform the market in either a positive or negative manner. This section also provides the scope of different segments and applications that can potentially influence the market in the future. The detailed information is based on current trends and historic milestones. This section also provides an analysis of the volume of production about the global market and about each type. This section mentions the volume of production by region. Pricing analysis is included in the report according to each type, manufacturer, region and global price from 2016 to 2027.

A thorough evaluation of the restrains included in the report portrays the contrast to drivers and gives room for strategic planning. Factors that overshadow the market growth are pivotal as they can be understood to devise different bends for getting hold of the lucrative opportunities that are present in the ever-growing market. Additionally, insights into market expert’s opinions have been taken to understand the market better.

● To provide detailed information about the crucial factors that are influencing the growth of the market (drivers, restraints, opportunities, and challenges)

● To historical and forecast the data of the market segments with respect to United States, EU, CIS, China, India, Japan, SEA, South America, Middle East, Oceania and the Rest of the World

Is there a problem with this press release? Contact the source provider Comtex at editorial@comtex.com. You can also contact MarketWatch Customer Service via our Customer Center.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey