lcd panel price ihs pricelist

(August 29, 2018) – Large thin-film transistor liquid crystal display (TFT LCD) panel shipments hit a record monthly high in July 2018 in terms of unit and area shipment. Unit shipments increased by 10 percent in July compared to a year ago to reach 64.3 million units, while area shipments jumped 19 percent during the same period to 17 million square meters, according to IHS Markit (Nasdaq: INFO), a world leader in critical information, analytics and solutions.

. “Despite the growing production, panel makers have maintained the utilization rate and instead tried to push out panel shipments by lowering panel prices in the first half of 2018. That’s one of the reasons that panel shipments are continuously growing.”

The LCD TV panel contributed to the record high shipments of larger-than-9-inch LCD panels in July. Unit shipments of LCD TV panels increased by 15 percent in July year on year to 24.6 million units and area shipments jumped 21 percent to 13.3 million square meters, according to the

Panel makers suffered from high TV panel inventories in the first half of 2018 due to growing production capacities. Panel prices have been weak for a year and panel makers’ profit margins have plunged. “Therefore, panel makers wanted to clear up the inventory before the third quarter, high-demand season, when they aim to raise the panel price back again,” Wu said. “That has led to the fast growth in TV panel shipments lately, which as a result pulled the total large panel shipments to a historical high in July.” As the panel makers hoped, LCD TV panel prices rebounded in July 2018.

Chinese panel maker BOE led the large TFT LCD market in July 2018 in terms of unit shipments with a stake of 24 percent, followed by LG Display with 19 percent. However, in terms of area shipments, South Korea’s LG Display continued to lead with a 20 percent share, followed by BOE with 18 percent.

IHS Markit provides information about the entire range of large display panels shipped worldwide and regionally, including monthly and quarterly revenues and shipments by display area, application, size and aspect ratio for each supplier.

IHS Markit (Nasdaq: INFO) is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers next-generation information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 business and government customers, including 80 percent of the Fortune Global 500 and the world’s leading financial institutions.

IHS Markit is a registered trademark of IHS Markit Ltd. and/or its affiliates. All other company and product names may be trademarks of their respective owners © 2018 IHS Markit Ltd. All rights reserved.

Korean TV panel makers have been reducing output of 32-inch to boost production of larger-sized panels and generate higher profitability while Chinese panel makers initially intending to increase TV panel production by annual double-digit rates are now shifting strategies, expanding instead the production of IT displays in 2017 to diversify portfolios away from focusing on TV screens alone toward more panels for notebook PCs and monitors, moves could further tighten TV panel supply next year.

However, Samsung Display’s decision to shut down its L7-1 line, which is responsible for a majority of the global supply of 40-inch thin-film transistor (TFT) LCDs remains the major cause of tight supply. The L7-1 is a Gen 7 TFT LCD fab turning out glass substrates measuring 1870 x 2200 millimeters for 40-inch TV panels. The shut down of the L7-1 fab was a surprise and their latest decision may seem hard to understand in the wake of higher demand. But the company’s decision comes as the L-1 has proven to be unprofitable and the use of the facility for the growing OLED demand was calculated to throw off greater free cash. So Samsung decided to repurpose the older and non-profitable TFT LCD fabs, which accounted for 3-4% of global capacity to OLED production. Now there are possible shutdowns involving other larger-sized panel-making fabs, including Samsung Display’s L7-2 line. New panel fabs in China slated to start MP in the latter half of 2017, allayed jitters and indicating that an imbalance in the supply and demand of 40-inch TFT-LCD panels could be easing.. But if Samsung Display decides to also shutter its L7-2 line, the resulting misalignment in supply and demand would then last much longer, extending until 2018. Together the L7-1 and L7-2 fabs can be considered as twin fabs in South Korea, so speculation is understandable that Samsung Display might restructure L7-2 after shutting down the L7-1 line.

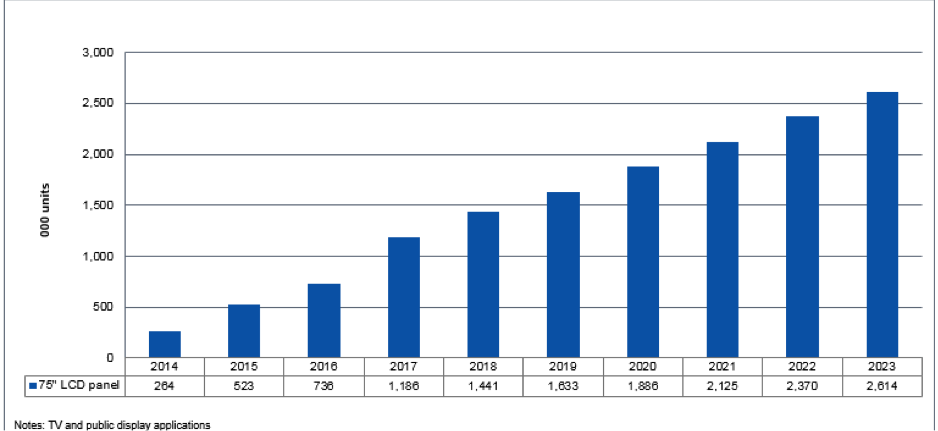

IHS cites three reasons why Samsung Display will not close the L7-2 fab:First, burgeoning demand for 75-inch or larger-sized TFT-LCD panels requires the operation of the L7-2 line, which primarily produces these super-large panels. As shown in the following graph, the 75-inch TFT LCD panel market is expected to grow at double-digit rates every year. For 2017, annual demand for the 75-inch TFT LCD is forecast to exceed 1 million units—a volume large enough so as to not be ignored by Samsung. For a company that supplies large and high-end panels to many premium electronics brands across the world, it will not be easy to give up the lucrative opportunities presented by 75-inch panel production. On this point then, the company is more than likely to maintain its L7-2 line, which is optimized for Gen 7 panels, in a bid to keep its lead in the 75-inch or larger-sized panel market.

Second, the L7-2 line is capable of producing not only amorphous silicon (a-Si) TFT panels used for TVs but also of panels featuring PLS—plane to line switching—TFT technology used by high-end monitors. In order to enable the supply of high-end monitors utilizing PLS TFT panels, the L7-2 fab should remain open.

Finally, steady demand for 40-inch TFT-LCD panels will also prevent closure of the L7-2 line at any time soon. Even after the L7-1 shutdown, Samsung Display is expected to continue to supply 40-inch panels to key customers. The L7-2 will be Samsung’s only fab capable of manufacturing 40-inch panels after the L7-1 closure, with the L7-2 projected to produce about 5 million 40-inch TFT LCD panels annually. Considering the 20 million 40-inch panels that Samsung produces annually, 5 million is a relatively small amount—but large enough to make a huge difference if the company continues to provide the panels. In particular, the continued supply of 40-inch panels should help Samsung Display keep its customers who still need the panels, and for Samsung to maintain leverage during negotiations with panel buyers.

Global corporate investment into LCD displays is expected to become obscure beginning in 2022, triggering forecasts that suppliers producing LCD-related equipment will quickly have to switch their main area of business.

According to market research firm IHS Markit, the final investment into the sector will be next year when BOE expands its B17 line producing Gen-10.5 panels and CSOT makes investment into its T7 plant for Gen-10.5 displays.

Investment into OLED, on the other hand, will surge. IHS Markit said over the next five years, up to $8billion is to be poured into the sector. Chinese panel companies are likely to spend extensively on Gen-6 flexible OLEDs, Y-OCTA and TFE technology. Expenses on ink-jet equipment are also to rise.

Beginning next year, Chinese display makers will start the full-fledged operation of large-sized tenth-generation or later liquid crystal display (LCD) panel factories. As a result, some experts say that an increase in global flat panel display production capacity may extend the current LCD oversupply period.

According to market researcher IHS Markit on December 7, China"s large display makers such as BOE which is the largest display manufacturer of China, China Star (CSOT) and Foxconn, will put seven 10-generation LCD factories to work one by one from next year to 2020.

As a result, IHS Markit predicts that global LCD panel supply growth will reach 59% per annum on average over the next five years to 2022. The proportion of 10G or later LCD panel production will also climb from 4% this year to 26% in 2020, according to IHS Markit. Purchases of flat panel display production equipment are also expected to exceed US$ 20 billion next year.

It is forecast that the LCD oversupply which began at the end of 2015 is expected to continue for at least five years. The price of a 55-inch LCD panel which rose above US$ 228 in 2015 dropped to US$ 200 in 2016 and then sank to US$ 180 in December of this year, according to market research firm WitsView.

As LCD panel prices have tumbled due to increased supply, the premium TV market is also moving rapidly towards large-screen models. Display panel manufacturers are competing to build a 10.5th-generation plant optimized for 65-inch and 75-inch displays. As 8th-generation and 8.6th-generation plants which account for the majority of large-area LCD production lines are optimized to produce 55-inch and 58-inch panels, respectively, they are less efficient at producing larger LCD panels.

BOE started the full-scale operation of its 8.5th-generation production line this year, and will start running its 10th-generation plant in the first half of next year. China Star (CSOT) and CEC-Panda are also in the process of building large LCD production lines. In the third quarter, BOE of China dethroned LG Display which has been at the top spot for 31 consecutive quarters while ranking first with a market share of 21.7% (based on shipment) in the 9-inch or larger display panel market.

Currently, LG Display is enjoying 90% of its total sales in the LCD sector and making its profit structure centered on the large organic light emitting diode (OLED) business. However, the company already missed investment timing for nearly half a year such as a delay in investment in the establishment of an 8G OLED factory in Guangzhou in China. Thus, a lot of attention is being paid to how LG Display will tackle this matter.

“As 10.5th-generation plants will be put into full operation, prices of 65-inch or larger panels will slide more than 5% each year, while demand will increase 2.5-fold to 40 million units per year,” an industry observer said. “65-inch or larger TVs will become the mainstream in the future.”

OPIS has been a news and price reporting leader in the downstream refined products marketplace since 1977. We have served customers throughout the many industry segments – traders, suppliers, commercial end-users, wholesalers and retailers – with up-to-the minute, news, analysis and pricing that appears in our many published reports and on-line services.

OPIS editors always search for the most complete picture of market activity in their assessments. We believe transaction data should form the bedrock of any price assessment. However, with some products and in some markets the amount of transactional data is much less comprehensive. In such case, OPIS price reporters use bid/ask ranges to set highs and lows in accordance with established methodologies. Highest bid and lowest offer may set the parameters of these ranges. In some cases, historically demonstrated mathematical formulae may be applied to calculate the differential value of an illiquid product relative to a more liquid product.

OPIS has a complaints policy inline with the IOSCO Oil PRA Principles. This policy describes the procedures and mechanisms for receiving, investigating and retaining records concerning complaints about it price assessments.

A methodology change is likely to be material if it impacts the index calculation process or formula, the quality of the input data, the index selection rules, the underlying market or reality measured, the panel of Contributors to the benchmark, or the benchmark level. Where a methodology change is beneficial and material, and where it is judged to be appropriate and proportionate, the OPIS Editorial team will start a wider consultation which is addressed to all relevant stakeholders.

OPIS’ overarching strategic goal continues to be that it is recognized as a widely accepted fuel price benchmark for supply contracts and competitive positioning. OPIS is relied on as a trusted benchmark because, based on its published methodology and internal policies and practices, OPIS can provide assurance it remains completely unbiased and independent. OPIS has no stake in fuel transactions, is not funded by oil industry initiatives, and strictly adheres to antitrust guidelines determined by independent legal counsel.

OPIS does not discriminate between reporting parties that are in good standing and have demonstrated a commitment and reputation for truthful and accurate price discovery when calculating its market assessments.

OPIS market editors give all due priority to concluded transactions when making market assessments with the exception of market trading days in which an exceptional event or anomaly occurs just prior to OPIS’ deadline for publishing market assessments. However, all price assessments that deviate from OPIS’ prioritization policy for transactional data require the consultation and prior approval of a supervisory editor.

OPIS market assessors sample on a daily basis a broad cross-section of refiners, traders, marketers, brokers and end users active in buying, selling or trading physical barrels. OPIS policies and practices require market assessors to cast a wide net to capture as many transactions as possible in arriving at OPIS day-to-day price assessments of spot market values. OPIS market assessors take an “arm’s length” approach to covering the market.

OPIS daily spot market assessments include information obtained from “back office deal logs” sent to OPIS as part of its daily market price discovery. The information highlights actual transactions during the day, including price, volume, product, timing and counter party. OPIS market assessors compare the end-of-the-day deal logs with our confirmed deals through the day to ensure OPIS does not duplicate information. OPIS confirms deals via constant communication with traders and brokers in the marketplace.

OPIS takes into account in its daily full-day price assessments market data from a variety of approved reporting entities. The volume of data coming from any single entity on any given day can vary, depending on that entities activity (buying or selling needs) in the marketplace.

For over 30 years clients have trusted OPIS to adhere to strict anti-trust guidelines in collecting and distributing sensitive oil pricing data. With oil prices under increasing scrutiny, OPIS recognizes that suppliers cannot afford even the slightest perception of price sharing or price signaling. That’s why OPIS does not provide price notification and messaging services for suppliers and embargoes release of all rack pricing data until after the changes become effective to customers.

Every day, including Saturdays, OPIS updates its wholesale terminal prices from hundreds of sources. Some suppliers confirm prices directly using the same pricing messages their customers receive. For many other suppliers, prices are collected from their customers who OPIS deems are reliable sources.

Verification of prices is done using documents provided by either the supplier or customers. Multiple sources are required for prices received via customer channels. In order for a supplier’s price to be added to OPIS rack coverage, their price and the consistent supply of barrels at that location must be verified with multiple customers. It must also be a wholesale terminal rack price and not a commercial or consumer end-user price; this avoids mixing classes of trade and misrepresenting true wholesale postings and averages.

OPIS uses several levels of automation to make sure prices that have not changed at usual intervals are fresh. If a price has not changed in 48 hours, it is electronically flagged and a pricing specialist is alerted so as to track down whether the number still represents an active and meaningful listing. OPIS specialists pinpoint prices that are outside specified reasonable parameters to avoid displaying inactive prices where product may not be available or where special circumstances may dictate that the number is not representative of where most wholesale commerce is taking place. Products tagged as “out-of-product” or “out-of-average” will not be part of the OPIS lows, highs or averages. When an entire terminal is shut down due to weather or other catastrophic events, supplier prices are left intact, until suppliers stop sending prices for the terminal.

Time Stamp (all times are ET)9:00 a.m. – OPIS wholesale terminal prices for gasoline, distillate, and other products are updated and ready for release.

10:00 a.m. – OPIS contract summary data used for benchmarking is available. The contract data includes the Contract Average which is a gross price that OPIS has had since 1995. As of April 1, 2004, we added a Contract Low and Contract High as well as Contract Net Average, Contract Net Low and Contract Net High pricing. Branded and Unbranded numbers are also available as Contract prices. The contract data is frozen for 24 hours to allow customers to reconcile exchanges, sales or other benchmark deals. The contract summary data is also archived. The reason OPIS created the Contract summary data is because OPIS updates price moves throughout the day and publishes them on demand for clients.

by 4:59 p.m. – OPIS archives the closing rack price database for that business day (except for on major holidays, when the closing rack prices are archived at 2:00 p.m.). The current day’s history is available the next business day. The OPIS rack history database is the largest of its kind and dates back to December 15, 1980.

11:59 p.m. – OPIS Calendar-Day Average rack prices are a snapshot of the average of all supplier postings in each OPIS rack market at 11:59 p.m. eastern time. The snapshot includes all price moves from 12:00 a.m. (midnight) until the file is frozen at 11:59 p.m. (Example: The Jan. 3 Calendar-Day Average encompasses all price moves that were made at 12:00 a.m. on Jan. 3 up through 11:59 p.m. on Jan. 3. Hence, it is an average of all prices on that calendar day.)

This “Original OPIS Rack Benchmark” started in 1980 when the market moved only once a week. Since major fuel purchases are still referenced to this published price, it is one of many benchmarks available from OPIS today. OPIS Newsletter pricing is frozen each Thursday evening (except on holidays) and is based on that day’s closing gross average of all supplier postings in each OPIS Rack market. Each OPIS Newsletter Rack Benchmark report also contains the OPIS 5-Day Average Benchmark which is the rack average of the gross closing prices from the prior Friday, Monday, Tuesday, Wednesday, and Thursday (except on certain holiday weeks). If a holiday falls on a Thursday, like Thanksgiving, the Newsletter Rack Benchmark is frozen on Wednesday at close and the 5-Day Average Benchmark becomes a 4-Day average from the previous Friday, Monday, Tuesday, and Wednesday.

OPIS Newsletter Rack Benchmark pricing is available as full PADD reports in the OPIS Newsletter which is delivered every Monday. OPIS Newsletter Rack Benchmark pricing is also delivered immediately after the prices are frozen on an individual rack basis.

Rack FormatsOPIS Standard Display – Provides one price per product, per supplier in each market, even when suppliers post at multiple terminals. We select the primary terminal for each supplier, so the OPIS averages that are so critical for benchmarking and market analysis are not skewed.

OPIS Terminal Display – Shows product prices posted for every supplier at all terminals in a given location for total price transparency and includes the location and owner.

In addition to providing daily, up-to-the-minute wholesale rack prices, OPIS maintains the largest and most extensive wholesale terminal price historical database of any company in the world. OPIS’s historical rack prices date back to 1981, when oil prices were decontrolled. Prices are available on a daily, weekly or monthly basis by market, by company, and by product.

The OPIS Low 2 and Low 3 Premium Benchmark averages are calculated by averaging the lowest two (or lowest three, for the low 3 average) supplier prices per rack city, product, grade, RVP (if applicable) and octane (if it is an OPIS octane specific rack report).

The OPIS 2nd Low Premium Benchmark represents the second lowest price per rack city, product, grade and RVP (if applicable) and octane (if it is an OPIS octane specific rack report). In the event that two suppliers have the same price, the 2nd Low Premium Benchmark may be the same value as the OPIS Low Benchmark.

Definitions of Inclusion for Standard and Terminal Rack ReportsIn a standard rack report, if a single supplier represents the lowest two prices with their branded and unbranded postings, both of the supplier’s postings will be averaged together for the low 2 average.

In a terminal rack report, if a single supplier has the same lowest price listed at three different terminal locations in a rack city, OPIS will average that supplier’s prices together to get the low 3 average.

Each day OPIS uncovers wholesale fuel purchases transacted at values below the lowest rack price that appears in the OPIS daily wholesale rack display. We verify these transactions and publish these discovered ‘Bottom Line’ values by market and product to give buyers and sellers visibility into the lowest transacted wholesale purchase prices on any given day.

Bottom Line prices are contrasted against the OPIS benchmark low posted price to identify how much lower these Bottom Line prices are. Only markets where Bottom Line wholesale values below the OPIS benchmark low will appear. Bottom Line prices include TVAs and other discounts and are often contract prices between suppliers and purchasers reflecting volume discounts, although specific volumes are not reported.

OPIS Temperature Correction Assessment (TCA) = Volume Correction Factor * Contract Average Price of Product in cents/gal * (60° F – Average Temperature)

Every day OPIS captures nearly 5 million retail gasoline and diesel prices for up to 150,000 unique fuel stations throughout North America. Through relationships with fleet card companies, direct feeds from leading retailers, and crowdsourced data from popular mobile applications, OPIS is able to provide the most comprehensive and accurate pump prices in the industry.

The OPIS retail data is relied on by many of the top fuel retailers in the country to replace store manager surveys. Additionally, many websites and mobile applications source fuel prices from OPIS, and most of the largest automobile manufacturers display our real-time fuel prices in their connected car onboard platforms.

To ensure accuracy of the retail prices and station information, OPIS scrubs the incoming data from our suppliers using many quality control processes. Automated queries such as station brand changes, product mapping, and price flipping among many others alert our team of more than a dozen data quality analysts of changes in real time, who validate and update station and pricing information to ensure the highest standard of accuracy.

OPIS surveys the current retail prices of No. 2 low sulfur and Ultra Low Sulfur diesel fuel from more than 8,000 active truckstops and travel plazas in the U.S. and Canada. Retail prices are gathered by major fuel card companies including Comdata and EFS as well as through direct feeds from major truckstop chains.

OPIS reports wholesale fuel prices by products as defined by EPA standards more so than by any type of product use. For example, the EPA defines low-sulfur fuels as having a sulfur content of less than 500ppm and Ultra Low Sulfur diesel as less than 15 ppm.

OPIS marries this retail price data with current rack and tax rate information to calculate the estimated laid-in costs and profit margins of fuel at each of the fueling sites included in the OPIS survey. The OPIS estimated cost figures are recognized as the industry standard for benchmarking “Cost Plus” fuel purchases by large trucking fleets.

Diesel fuel is dyed red to denote it is being used for tax-exempt purposes. Entities that are tax-exempt (school boards, etc.) use red-dyed fuel because it is tax exempt. There is no difference in red-dyed product specifications. Red-dyed prices typically are 0.25 to 0.35cts higher than clear prices to recoup the charge for the dye and dying process.

The Retail Diesel prices and the OPIS Gross Contract Average are used to create these numbers. The data is delivered Monday through Friday by email, the Internet, FTP and many third-party vendors.

Many of the daily prices we report provide key benchmarks for some of the largest buyers and sellers of NGLs in the world. Large utilities, petrochemical companies, industrial and manufacturing companies, rail companies, fleets, natural gas producers, gas processing companies, refiners, pipeline companies, and state and local governments buy and sell NGLs based on OPIS spot market assessments.

For North American markets, editors confirm and record deals done for NGLs between 9am and 4pm Eastern time (8am-3pm Central time) on a fixed price basis or in a relationship to another product or location or timing (example: E-P mix at a differential to purity ethane, TET propane at a differential to non-TET propane, prompt a penny over any current month). Transaction data is due to OPIS no later than 4:15 pm ET.

OPIS tracks any current month, prompt, and out month trading for NGLs. OPIS NGL prices labeled as “any current month” represent transactions for product that buyer and seller agree will be delivered at any time during the current calendar month. OPIS NGL prices labeled as “prompt current month” represent transactions for product that buyer and seller agree will be delivered within the next 48 hours. OPIS NGL prices labeled as “out month” represent transactions for product that buyer and seller agree will be delivered any time in the next calendar month.

For Hattiesburg Spot Gas Liquids Prices, prices for a volume of 5,000 barrel (bbl) will be the minimum considered for use both for in-line and storage propane price ranges. The 5,000-bbl volume reflects the most commonly reported trade done for this market. Deals done at those volumes are not automatically included by virtue of the volume. Price ranges will reflect either fixed-price trades, buy/sell trades or spreads to Mont Belvieu markets. Unless a specific spread or buy/sell value is reported, editors will have discretion with regard to assessing the timing and relation between Hattiesburg fixed-price trades and Mont Belvieu prices. In the absence of reported trades, editors will assess Hattiesburg prices based on the most recent spread assessments to Mont Belvieu propane markets.

Minimum volumes are not necessarily a consideration for Louisiana, Canada and West Coast price ranges due to illiquidity and infrequent trading in those regions. Those markets will continue to be assessed based on most recent transactions reported to OPIS, market surveys of most recent spread assessments to more liquid markets and the best bid-ask spread available through brokers and electronic exchanges.

Editors have the ability to review and reflect transactions reached on electronic platforms, such as ICE, within published ranges, but posted “bid/asked” numbers or even confirmed deals on such networks are viewed subjectively by OPIS staff. It is up to individual OPIS editors to determine whether prices quoted on electronic platforms fall within the reasonable realm of where business is being done — OPIS will not include a price within its daily ranges simply because it appeared on an electronic platform. Finally, a note about errors and disputes. We recognize that ascertaining a spot product range is highly subjective, and realize that there will be parties that dispute our “call.” Ranges are only changed in the case of clerical errors such as typos or transpositional mistakes. We never alter ranges simply because of oil firm complaints.

In the northwest European propane market, OPIS assesses cargoes basis CIF Flushing for 10-25 days forward delivery. The grade and quality, delivery and nomination terms are based on the prevailing, industry-accepted forward contract, such as the TOT contract. Positions referencing alternative forward delivery contracts will be considered if the dates fall into the 10-25 day forward delivery range. Assessments consider physical spot deals and swaps transacted between 4:00-4:30pm London time. Butane prices are for field grade mixed butane cargoes above 4,000mt delivered 5-20 days forward basis cif ARA.

In general, editors may disregard the prices for two-party calendar spreads. However, editors do consider the differential implied by such transactions. For instance, if two firms agreed to exchange Mt. Belvieu ethane for the current month versus the out month, at a differential of 1cts/gal, the editor would consider that differential in the day’s assessment of the market.

In the case of a three-party spread – one in which firm A completes a calendar spread by selling to Firm B and buying from Firm C in different months – editors may consider the prices as well as the monthly differential when computing the day’s ranges.

Editors may consider both the prices and differentials achieved in a product spread (such as ethane for EP mix) or geographical spread (such as Conway propane for Mt. Belvieu Non-TET propane).

OPIS NGL spot market products offer twice-a-day market assessments – at midday and following the futures’ market’s close at the end of a business day for Mont Belvieu and Conway markets, with once daily assessments offered for all other markets. In addition to in-depth market analysis that explains what factors are influencing price direction, OPIS provides a range of actual spot prices, reporting a daily market “low,” “high,” “average” for each of the products in each of these markets: Mont Belvieu, Texas; Conway and Bushton, Kan.; Napoleonville and Geismar/Sorrento, La.; Hattiesburg, Miss.; Los Angeles, Bakersfield, and San Francisco, Calif. and Sarnia and Edmonton, Canada. Averages are simple averages of the daily low and high, as opposed to weighted averages.

In Mont Belvieu markets, TET prices apply to product traded in the original TET facility currently owned by the Energy Transfer LP and Regency Energy Partners LP joint venture, (LST). Non-TET prices only apply to product traded in the Mont Belvieu Caverns facility that is a subsidiary of Enterprise Products Partners, LP. Other Non-TET prices apply to product traded in Targa Resources storage. EP Mix and Purity Ethane apply to those products traded in the Mont Belvieu Caverns facility that is a subsidiary of Enterprise Products Partners, LP.

The aggregate prices are automated prices based on and derived from the daily assessed lows and highs of each product from the OPIS Mont Belvieu Spot Gas Liquids Prices. The aggregate low and high prices will both be rounded to the nearest thousandth, while the aggregate average price and aggregate month to date price will be rounded to the nearest ten thousandth for “Any Current Month”, “Prompt Current Month” and “Out Month” for each product and will be calculated and reported as follows:

For the daily aggregate propane, isobutane and natural gasoline prices, OPIS will calculate the average of the daily assessed spot lows for TET, Non-TET and Other Non-TET for their respective product, to provide the aggregate low, and the average of the daily assessed spot highs for TET, Non-TET and Other Non-TET for their respective product, to provide the aggregate high.

For the daily aggregate normal butane prices, OPIS will calculate the average of the daily assessed spot lows for TET, TET Isomerization Grade (Isom), Non-TET and Other Non-TET normal butane to provide the aggregate low, and the average of the daily assessed spot highs for TET, TET Isomerization Grade (Isom), Non-TET and Other Non-TET normal butane to provide the aggregate high.

For the daily aggregate EP mix prices, OPIS will calculate the average of the daily assessed spot lows for EP mix and Other Non-TET EP mix to provide the aggregate low, and the average of the daily assessed spot highs for EP mix and Other Non-TET EP mix to provide the aggregate high.

For the daily aggregate purity ethane prices, OPIS will calculate the average of the daily assessed spot lows for purity ethane and Other Non-TET purity ethane to provide the aggregate low, and the average of the daily assessed spot highs for purity ethane and Other Non-TET purity ethane to provide the aggregate high.

For all products, the daily aggregate average price will be calculated by averaging the daily aggregate low price with the daily aggregate high price for each product. The daily month to date aggregate price will be calculated by averaging the daily aggregate averages for that month for each product.

This index is an automated composite price representing the components of y-grade, or raw make, based on the percentage content of the stream as such: 42% NGL-MONT BELVIEU Purity Ethane-OPIS; 28% NGL-MONT BELVIEU Propane (NON-TET)-OPIS; 11% NGL-MONT BELVIEU Normal Butane (NON-TET)-OPIS; 6% NGL MONT BELVIEU Isobutane (NON-TET)-OPIS; 13% MONT BELVIEU Natural Gasoline (NON-TET)-OPIS. The price is based on the daily averages of Non-TET any current month product prices which are traded in the Mont Belvieu Caverns facility that is a subsidiary of Enterprise Products Partners, LP and published daily in the OPIS North America LPG Report. It is priced in US cents/gal and $/bbl.

Note: In Mt. Belvieu TET (LST) normal butane references refinery grade butane regardless of location. Non-TET and Other non-TET normal butane refer to isomerization grade normal butane. Conway prices reflect the market for isomerization grade normal butane.

OPIS FOB Southeast Louisiana Spot Gas Liquids Aggregate Prices (cts/gal)The aggregate prices are automated prices based on and derived from the daily assessed lows and highs of each product from the OPIS FOB Napoleonville and Geismar/Sorrento Area Spot Gas Liquids Prices. The aggregate low and high prices will both be rounded to the nearest thousandth, while the aggregate average price and aggregate month to date price will be rounded to the nearest ten thousandth for “Any Current Month”, “Prompt Current Month” and “Out Month” for each product and will be calculated and reported as follows:

The daily OPIS FOB Southeast Louisiana Spot Gas Liquids Aggregate Prices for “Any Current Month” would be calculated by averaging the FOB Napoleonville and FOB Geismar/Sorrento Area spot lows assessed for that day, averaging the FOB Napoleonville and FOB Geismar/Sorrento Area spot highs assessed for that day, and the aggregate average would be based on the aggregate low and aggregate high. The aggregate month to date average would be the average of the daily aggregate averages for that month. These same calculations would be used for “Prompt Current Month” and “Out Month” using the associated prices from OPIS FOB Napoleonville and FOB Geismar/Sorrento Area Spot Gas Liquids Prices.

Editors track any, prompt and out month prices for Edmonton propane, field grade butane and natural gasoline; and for Sarnia propane, normal butane and isobutane.

Assessments reflect spot prices in each location. Local posted prices are, however, taken into consideration to determine market value in the absence of spot liquidity.

All prices are assessed in cents per gallon in the daily OPIS North America LPG report, though price reporting on the part of market participants often follows different formats. Data received is converted to cents per gallon.

All prices are assessed in cents per gallon in the daily report, though price reporting on the part of market participants often follows different formats. Data received is converted to cents per gallon.

As of Oct. 1, 2014, OPIS began assessing West Coast LPG markets on a daily basis. Editors track any month prices for Bakersfield propane, normal butane, butane mix and natural gasoline; San Francisco and Los Angeles propane, normal butane, butane mix and isobutane. Assessments reflect spot prices in each location. Local posted prices are, however, taken into consideration to determine market value in the absence of spot liquidity. Propane is quoted at fixed prices, FOB terminals in U.S. cents/gallon, excluding taxes and discounts. Normal butane and isobutane are quoted at differentials to Mont Belvieu non-TET grades, delivered basis to refineries in U.S. cents/gallon. Natural gasoline is quoted at a differential to WTI averages, delivered basis to refineries in U.S. cents/gallon.

Starting Jan. 1, 2015 West Coast NGL spot market assessments based on postings will exclude OPIS posted LPG CAR costs. Some suppliers have indicated they will not include CAR values in their posted prices. Others have indicated that they will. In the latter case, we will adjust (normalize) to “prices without CAR cost” by removing the OPIS Assessed CAR value for suppliers who embed the value into the posted price. If a supplier offers transparency into the actual cost they include for CAR, we will adjust the posted price according to that value and not the OPIS Assessed CAR Value.

In the event that all suppliers include a CAR value in their postings at a particular market, OPIS will adjust those prices to create a normalized rack price from which to base a spot market assessment.

Bakersfield natural gasoline is priced as a differential to WTI crude oil averages. In addition to the cents per gallon assessment in its report, OPIS tracks the dollars per barrel premium or discount to WTI crude oil for Bakersfield natural gasoline.

Frac spreads in the North American LPG Report are calculated using the following formula: [NGL product average price/NGL product heating value] /100 – referenced month NYMEX natural gas futures settle price x 100 x NGL product heating value. As raw mix/y-grade stream compositions vary widely, the frac spreads published by OPIS are intended only as a general guide, and are not specific to any particular stream or site.

OPIS U.S. Gulf Coast FOB LNG Price Assessments ($/MMBtu)OPIS U.S. Gulf Coast FOB LNG Price Assessments represent the prices of liquefied natural gas traded and/or stored in the operational LNG terminals of the U.S. Gulf Coast with the intent of exporting and only includes U.S. Gulf Coast LNG projects that have reached substantial completion.

The OPIS U.S Gulf Coast FOB LNG Price Assessments will provide four 15-day forward periods of assessments, which include 1-15 days, 16-30 days, 31-45 days and 46-60 days. OPIS will publish two prices for these four period – an outright price for LNG and a differential value for LNG above four base prices.

The first 15-day period (1st – 15th days), is based on the OPIS Spot Henry Hub Natural Gas spot price published on the concurrent business day by OPIS Point Logic, that reflects the natural gas price calculated from actual reported transactions. The second 15-day period (16-30 days) is based on the 1st month of Henry Hub Futures. The third (31-45 days) and fourth (46-60 days) 15-day periods are based on the 2nd month of Henry Hub Futures. Futures will roll forward to the next month on the day before expiry.

The assessments include volumes of 1,000-1,150 Btu/scf calorific value and cargoes of 130,000-180,000 cubic meters. OPIS, at its discretion may consider including volumes out of this range. All prices are shown in US dollar per millions of British Thermal units ($/MMBtu).

In addition, the OPIS NGL Forwards Report features ethylene forward cash cost price tables and charts for Mont Belvieu ethane, TET propane, and non-TET normal butane and natural gasoline. These prices combine OPIS NGL pricing (as the raw material for Mont Belvieu ethylene) with OPIS PCW benchmark petrochemical prices. The ethylene forward cash costs are indicators of the price to produce ethylene using the various NGL feedstocks’ values in the forward markets.

Methodology for NGL Forward price assessments. . .At times, liquidity may be low in gas liquids forward markets and price reporting can be subjective. Therefore, editors gather data from a cross-section of market participants, and any information received pertaining to forward transactions is kept strictly confidential.

OPIS editors have the discretion to exclude forward values that represent extraordinary circumstances or are far outside the range of other values reported on a given day. Prices generally represent volumes of 10,000 bbl or greater at Mont Belvieu and 2,500 bbl or greater at Conway. Editors have the ability to reflect transactions reached on electronic platforms, but will not include a price in daily ranges simply because it appeared on an electronic platform. Prices are only corrected in the case of clerical mistakes and typographical errors.

Fractionation SpreadsMonthly fractionation spreads in the NGL Forwards Report are calculated using the following formula: [NGL product average price/NGL product heating value] /100 – referenced month NYMEX natural gas futures settle price x 100 x NGL product heating value. As raw mix/y-grade stream compositions vary widely, the fractionation spreads published by OPIS are intended only as a general guide, and are not specific to any particular stream or site.

Product Ratios to Crude OilThe formula for calculating monthly NGLs as a percentage of crude oil is as follows: (PRICE * 42) / ( 2/3rd Cycle WTI + 1/3rd Cycle+1 WTI)

Millions of gallons of gasoline, diesel fuel, heating oil, jet fuel, ethanol and other oil products are bought and sold each day in cash bulk markets. Commonly known in the trade as “spot” market prices, these transactions typically occur at the leading oil refining, barge and pipeline centers in the United States. These include the U.S. Gulf Coast, Group 3, Chicago, Atlantic Coast, Los Angeles, San Francisco Bay and Pacific Northwest. (View a complete at-a-glance listing of products and locations).

OPIS Last: The OPIS “Last” is a price indicator of where cash or spot market prices end for each full-day spot market trading session. It provides a numerical approximation of a refined products end-of-the day value.

While the OPIS Spot “Mean” is calculated using actual deal transactions from “low” to “high” during the day, editors do take into account in full-day price assessment end-of-the-day market shifts that potentially indicate new pricing levels.

OPIS editors sample on a daily basis a broad cross-section of refiners, traders, marketers, brokers and end users active in buying, selling or trading physical barrels. We cast a wide net to capture as many transactions as possible in arriving at our day-to-day price assessments of spot market values. Editors take an “arm’s length” approach to covering the market.

Editors confirm and record deals done for gasoline and distillate products that meet minimum pipeline/barge volumes specific to each geographic market. As the majority of the market is done on an EFP basis, we follow deals as basis discounts or premiums to the New York Mercantile Exchange. We consider fixed-price deals only if they fall within the full-day differential range based off the NYMEX at settlement, or to assess cash-for-cash “regrade” transactions.

OPIS daily spot market assessments include information obtained from “back office deal logs” sent to us as part of our daily market price discovery. The information highlights actual transactions during the day, including price, volume, product, timing and counter party.

OPIS has signed confidentiality agreements with some providers not to make this information public, except to use the transactions in our daily range of prices and weighted averages providing it meets our volume and timing criteria. OPIS editors compare the end-of-the-day deal logs with our confirmed deals through the day to insure we do not duplicate information.

Ranges in these reports apply the highest and lowest done deal differentials versus the NYMEX at settlement, resulting in an absolute full-day trading range in cents per gallon. We do not round prices up or down.

Midday market direction for implied cash prices is important for OPIS customers using this information to make rack pricing decisions. That range is simply an estimate of where the market has been trading or talked in the morning session and is published solely to provide a gauge of where implied absolute prices would be if a snapshot was taken at midday. Due to the incredible volatility in the futures and physical markets, alike, the midday indications are not included in the end-of-day, full-day assessments unless the midday numbers fall into a range covered by the full-day numbers.

OPIS spot methodology for gasoline Reid Vapor Pressure has always designated RVP levels during the spring/summer months when federal and state mandates require lower RVP gasoline. During the fall/winter months, OPIS spot prices have always defaulted to the seasonal RVP requirements. Starting September 2, 2009, OPIS now designates gasoline RVP levels year-round, with designations specific to trading cycles by product by market.

The OPIS Spot Ticker is your full-day, real-time window into what U.S. spot prices are doing. OPIS editors throughout the day update the OPIS Spot Ticker with done deals and buy-sell levels tracked in the market. It’s a web-based tool that offers real-time updates of OPIS spot prices and cash market trading differentials in major regions, along with news and events affecting prices.

The OPIS Spot Ticker also offers customers overnight implied spot price discovery by linking final-day cash basis trading differentials to the Globex overnight NYMEX ticks. These implied numbers are for directional purposes only to give subscribers an idea of what direction prices are moving after hours. They are not included as a part of any OPIS daily spot range of prices.

Gulf Coast waterborne assessments are calculated by adding to spot prices the cost of getting material to port, typically 1.25cts/gal for gasoline and high-sulfur diesel and 1.00cts/gal for ultra-low-sulfur diesel (both 61-gr and 62-gr), low-sulfur on-road, low-sulfur off-road and ultra-low-sulfur heating oil. These premiums are reviewed annually.

Pipeline GasolineConventional unleaded: 87, 89 and 93 octane. 89-octane unleaded is not a fungible spot product. OPIS assesses an implied price, using a blend ratio of premium gasoline and its regular-grade counterpart

Reformulated unleaded: 87, 89, 93 octane. RFG blended with ethanol is not a fungible spot product. Each day OPIS creates an “implied” value for this product by taking 90% of the RBOB price and 10% of the price of spot ethanol

Waterborne GasolineConventional unleaded: 87, 89 and 93 octane. 89-octane unleaded is not a fungible spot product. OPIS assesses an implied price, using a blend ratio of premium gasoline and its regular-grade counterpart

Because up-line allocations can sometimes affect the price of unrestricted line space, OPIS editors reserve the right to exclude any deals or positions that are not representative of the market or cannot be confirmed by counter-parties or independent market observers.

Reformulated unleaded: 87, 89, 93octane. RFG blended with ethanol is not a fungible spot product. Each day OPIS creates an “implied” value for this product by taking 90% of the RBOB price and 10% of the price of spot ethanol

GasolineConventional unleaded: 87, 89 and 93 octane, conforms to Colonial Pipeline. 89-octane unleaded is not a fungible spot product. OPIS assesses an implied price, using a blend ratio of premium gasoline and its regular-grade counterpart

Laurel PipelineRanges reflect non-Pennsylvania-origin barrels loading FOB Philadelphia. Prompt timing includes barrels loading into Laurel Pipeline up to nine full business days out. When no cycles are scheduled up to nine days out for a given product, the next cycle to schedule for that product will be included in the prompt spot price assessment.

GasolineConventional unleaded: 84, 89 and 91 octane. 89-octane unleaded is not a fungible spot product. OPIS assesses an implied price, using a blend ratio of premium gasoline and sub-octane regular

Conventional unleaded: 89 and 91-93 octane. 89-octane unleaded is not a fungible spot product. OPIS assesses an implied price, using a blend ratio of premium unleaded gasoline and CBOB

Editors confirm and record trades for gasoline and distillate products with a minimum pipeline size of 10,000 bbl in Los Angeles; 5,000 bbl in San Francisco and 5,000 bbl in the Pacific Northwest. As the majority of the market is traded on an EFP basis, OPIS assesses the spot market as basis discounts or premiums to the New York Mercantile Exchange (NYMEX). Fixed-price deals are considered only if they fall within the full-day differential range based off the NYMEX at settlement. Fixed price deals are converted to an exchange for physical (EFP) basis when reported and confirmed and then reapplied to the NYMEX settlement price. Trading activity for California markets on a North-South basis will require a volume match between the San Francisco and Los Angeles origins to be considered in the assessment process.

Gasoline, diesel fuel, and jet fuel physical assessments reflect barrels shipping on Kinder Morgan’s West Line pipeline system with a minimum volume size of 10,000 barrels. The L.A. CARB diesel fuel assessment reflects pipeline trades with a GATX storage facility option. The L.A. jet fuel assessment reflects pipeline trades that include a pump-over option to the Los Angeles International Airport storage facility (LAX). Physical spot market assessments are published as both a differential and an outright price.

RVP:OPIS’ Los Angeles gasoline assessments follow the RVP schedule for Kinder Morgan’s West Line pipeline system. During L.A. CARBOB’s transition from high-RVP to low-RVP, OPIS prompt prices will represent a cycle-specific, high-RVP gasoline blend through the end of the first cycle of February on Kinder Morgan’s West Line pipeline system. After the first pipeline cycle in February freezes, OPIS prompt CARBOB assessments will revert back to “any-month” pricing.

When prompt L.A. CARBOB assessments reflect the February first cycle only, high-RVP gasoline specification, the first forward physical price assessment will be reflective of a February “any-timing” low-RVP L.A. CARBOB until the prompt market transitions to the low-RVP gasoline specification at the beginning of February’s second pipeline cycle.

CARB-RFG (regular and premium): Not a fungible spot product. Each day OPIS creates an “implied” value for this product by taking 90% of the spot L.A. CARBOB price and 10% of spot L.A. ethanol.

Gasoline and distillates physical assessments reflect barrels shipping on Kinder Morgan’s North Line pipeline system with a minimum volume size of 5,000 barrels. Physical spot market assessments are published as both a differential and an outright price.

RVP: OPIS’ San Francisco gasoline assessments follow the RVP schedule for Kinder Morgan’s North Line-Zero Line pipeline system. During S.F. CARBOB’s transition from high-RVP to low-RVP, OPIS prompt prices will represent a cycle-specific, high-RVP gasoline blend through the end of the first cycle of March on Kinder Morgan’s North Line pipeline system. After the first pipeline cycle in March freezes, OPIS prompt S.F. CARBOB assessments will revert back to “any month” pricing.

When prompt S.F. CARBOB assessments reflect the March first cycle only, high-RVP gasoline specification, the first forward physical price assessment will be reflective of a March “any-timing” low-RVP CARBOB until the prompt market transitions to the low-RVP gasoline specification at the beginning of February’s second pipeline cycle.

CARB-RFG (regular and premium): Not a fungible spot product. Each day OPIS creates an “implied” value for this product by taking 90% of the spot S.F. CARBOB price and 10% of spot S.F. ethanol.

OPIS Pacific Northwest gasoline and diesel spot prices reflect an FOB Portland assessment and include trading activity, with a minimum requirement of 5,000 bbl, for products shipping on the Olympic Pipeline as well as trading activity for barrels at the Kinder Morgan Willbridge and Nustar Portland terminals. The Seattle gasoline spot prices reflect an FOB Seattle assessment, with a minimum volume requirement of 5,000 bbl and include trading activity for barrels shipping on the Olympic Pipeline. The Pacific Northwest jet fuel assessment reflects an FOB Seattle barge assessment, with a minimum volume of 5,000 bbl. Physical spot market assessments are published as both a differential and an outright price.

Timing: CARBOB paper price discovery includes two forward months, as well as two forward quarters. For CARB diesel and Jet Fuel, paper price discovery includes two forward months and one forward quarter.

In the OPIS U.S. West Coast Spot market report, a rack-to-retail trend snapshot is provided as a tool that can be used through downstream channels to help forecast the trend line for gasoline and diesel fuel rack to retail markets in Southern California. The L.A. CARBOB and L.A. CARB No. 2 oil prices are the daily prompt spot price assessments in those markets. The Basket of Racks price for gasoline combines OPIS Gross Contract Average prices for the Los Angeles and Colton racks for regular CARBRFG Ethanol 10% and includes CAR normalization, valuing the cost of compliance with both CAR and LCFS program. The Basket of Racks price for diesel fuel combines OPIS Gross Contract Average prices for the Los Angeles and Colton racks for CARB ultra-low diesel fuel and includes CAR normalization, valuing the cost of compliance with both CAR and the LCFS program. The retail gasoline and diesel averages represent the most recent price across of Los Angeles, Orange, San Bernardino and Riverside counties.

Prices: OPIS publishes ANS outright prices in $/bbl considering bids, offers and trades as differentials to NYMEX WTI Calendar Month Average (CMA), NYMEX WTI prompt, ICE Brent CMA and ICE Brent prompt.

Timing: OPIS ANS crude oil prices reflect deliveries within two calendar months from the first publishing day on or after the 10th of each month. For example, on Jan. 10, OPIS ANS prices reflect delivery in March, and on Feb. 10, ANS prices reflect delivery in April.

OPIS provides daily price discovery for California Carbon Allowances (CCA) created for the state’s cap-and-trade regulations that are being traded in the marketplace.

OPIS provides a daily price for the estimated impact of cap-and-trade regulations on gasoline and diesel fuel delivered at each California rack. California’s cap-and-trade regulations officially impact the California rack market beginning January 1, 2015; OPIS began publishing the CAR price August 1, 2014, ahead of the regulation compliance start date.

Timing: Current day pricing based on the OPIS CCA Current Year Vintage prompt timing assessment. OPIS will also provide a week average and a 30-day average for CAR assessment prices.

Since biomass derived fuels have a compliance obligation under the California cap-and-trade program, OPIS considers the CO2e/gal values for those products when calculating the CAR price for blended gasoline and biodiesel delivered at the rack.

The assessment for CAR gasoline prices (CARB RFG) = 90% gasoline grade’s CO2e/gal x the prompt CCA assessment + 10% ethanol CO2e/gal x the prompt CCA assessment.

The assessment for CAR biodiesel prices (B5) = 95% CARB diesel CO2e/gal x the prompt CCA assessment + 5% biodiesel CO2e/gal x the prompt CCA assessment.

CAR Gasoline RVP schedule: The schedule for determining winter or summer blend gasoline CAR calculations at each rack terminal will be determined by the following RVP cap limits and dates set for each air basin in California’s Reformulated Gasoline Regulations. OPIS reserves the right to publish seasonal CAR gasoline prices at each terminal, reflecting vapor pressure specifications based on actual supply availability, which can fluctuate during transition months, apart from the air district’s mandated RVP date.Air BasinSummerWinter*Mojave DesertMarch 1November 1

Twice a year during the RVP transition periods, OPIS will publish a CAR price assessment for both winter and summer gasoline grades in the West Coast Spot market reports. Both gasoline seasonal CAR price assessments will be published September 28, 29 or 30-October 31 and February 27, 28 or 29-April 30.

The OPIS Mexico Fuels Report provides a daily price index that assesses the value of Mexico delivered fuels, based on the daily OPIS assessments for U.S. benchmark refined product spot markets. The report also provides Mexico RVP and octane blend value differential assessments, prices for Mexico wholesale markets, spot-to-wholesale arbitrage heat maps, and price assessments for Americas freight rates. The daily OPIS Mexico Fuels Report features news, analysis, and pricing transparency into the buildup cost of importing fuel from the U.S. into Mexico.

OPIS Mexico Waterborne Landed Spot Gasoline PricesWaterborne landed spot gasoline prices combine OPIS U.S. benchmark pipeline gasoline spot price assessments, OPIS assessed RVP and Octane differentials, OPIS Americas Clean Freight assessments, logistical costs, and removes the OPIS assessed U.S. Renewable Volume Obligation to provide a fuel price index for Mexico ports and CRE RVP regions.

Renewable Volume Obligation (RVO): OPIS Mexico Waterborne Landed Spot Gasoline prices remove 100% of the OPIS current year, prompt RVO assessment (see methodology OPIS Renewable Fuels / RIN Credits).

Mexico RVP Differential: OPIS calculates the RVP price difference between Mexico CRE regulated seasonal RVP gasoline per region and the OPIS benchmark tradable spec RVP gasoline pipeline assessments for source spot markets based on the IHS Markit blend value equation. The OPIS RVP Differential calculation utilizes assessments and specifications for OPIS benchmark regular and premium gasoline in the source spot markets as well as the OPIS benchmark spot price assessment for Mt. Belvieu Non-TET butane. The Mexico RVP Differential is added to the OPIS price assessment for regular unleaded and regular sub-octane in the U.S. source spot market.

Mexico Octane Differential: OPIS calculates the octane price difference between Mexico CRE regulated regular and premium gasoline and OPIS benchmark tradable spec pipeline gasoline assessments for source spot markets using the IHS Markit blend value equation. The Octane Differential is added to the OPIS price assessments for regular unleaded and regular sub-octane in the U.S. source spot market, where applicable.

OPIS Mexico Waterborne Landed Spot Distillates PricesWaterborne landed spot diesel fuel prices and landed spot jet fuel prices combine OPIS U.S. benchmark spot price assessments, OPIS Americas Clean Freight assessments, logistical costs, and removes the OPIS assessed U.S. Renewable Volume Obligation (diesel fuel only) to provide a fuel price index for Mexico marine ports.

Renewable Volume Obligation (RVO)%: OPIS Mexico waterborne landed spot diesel Fuel prices remove 100% of the OPIS current year, prompt RVO assessment (see methodology OPIS Renewable Fuels / RIN Credits). OPIS Mexico waterborne landed spot jet fuel prices do not remove RVO.

Oxygenates landed spot prices combine OPIS U.S. Gulf Coast benchmark MTBE spot price assessments, OPIS assessed Mexico Rail Rates or OPIS Americas Clean Freight Rates.

OPIS Mexico Rail Landed Spot Refined Products PricesRail landed spot gasoline prices combine OPIS U.S. benchmark pipeline gasoline spot price assessments, OPIS assessed RVP and Octane differentials, OPIS assessed Mexico Rail Rates, and removes a percentage of the OPIS assessed U.S. Renewable Volume Obligation to provide a fuel price index for Mexico rail markets and CRE RVP regions. Rail landed spot diesel fuel prices combine OPIS U.S. benchmark spot price assessments, OPIS average rates for Mexico rail routes, and removes a percentage of the OPIS assessed U.S. Renewable Volume Obligation to provide a fuel price index for Mexico rail markets.

Renewable Volume Obligation (RVO)%: OPIS Mexico rail landed spot gasoline and diesel fuel prices remove 60% of the OPIS current year, prompt RVO assessment (see methodology OPIS Renewable Fuels / RIN Credits).

OPIS Mexico Rail RatesOPIS publishes rates for rail transport of gasoline, diesel and MTBE from Texas to several locations on the Mexico-US border and within Mexico. The rates are updated at the beginning of each month and applied to the daily OPIS Rail Landed Spot price calculations.

The route rates are sourced from rail tariffs as well as counterparties or stakeholders involved in or close to the market. The rates assume a tank car on a manifest train with no term contract pricing. If sourcing is unavailable for a route at the time of assessment, OPIS will consider the price changes along other routes as well as the per-mile cost along nearby routes with similar carriers to determine the rate.

Pemex Wholesale Prices vs. OPIS U.S. Gulf Coast Spot Price SpreadOPIS provides a daily price spread between Pemex posted wholesale prices and the OPIS U.S. Gulf Coast spot market refined products prices for 75 Mexico terminals. The price spread reveals the arbitrage between the Gulf Coast pipeline spot market and the Pemex posted wholesale markets for regular and premium gasoline as well as ultra-low-sulfur diesel. OPIS also provides a heat map for regular gasoline and ultra-low-sulfur diesel so that fuel suppliers can identify spot-to-wholesale arbitrages at a glance.

East Coast Mexico: Tuxpan, Tampico, Pajaritos, Progreso, Veracruz and Ciudad MaderoProductOriginOPIS Price BasisCRE RVPRVP IndexOctane IndexFreight Routeex-RVO %WB LogisticDistributionReg Unl 87USGCReg Unl 87NorthYesNoUSGC-EC Mex100%YesNuevo León, Chihuahua, Durango, Coahuila, Tamaulipas, San Luis Potosí.

Lazaro CardenasProductOriginOPIS Price BasisCRE RVPRVP IndexOctane IndexFreight Routeex-RVO %WB LogisticDistributionReg Unl 87USGCReg UnlCenterYesNoUSGC-Lazaro Cardenas100%YesAguascalientes, Jalisco, Guanajuato, Michoacán, Zacatecas, Morelos, Tlaxcala, State of Mexico, Hidalgo, Querétaro.

RosaritoProductOriginOPIS Price BasisCRE RVPRVP IndexOctane IndexFreight Routeex-RVO %WB LogisticDistributionReg Unl 87USGCReg UnlPacificYesNoUSGC-Rosarito100%YesBaja California, Baja California Sur, Sonora, Sinaloa, Nayarit, Colima, Guerrero, Oaxaca, Chiapas

GuaymasProductOriginOPIS Price BasisCRE RVPRVP IndexOctane IndexFreight Routeex-RVO %WB LogisticDistributionReg Unl 87USGCReg UnlPacificYesNoUSGC-Guaymas100%YesBaja California, Baja California Sur, Sonora, Sinaloa, Nayarit, Colima, Guerrero, Oaxaca, Chiapas

Topo

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey