lcd panel price ihs quotation

(June 21, 2018) – Despite better-than-expected first-quarter demand for thin-film transistor liquid-crystal display (TFT-LCD) TV sets and TV panels, market players would be well advised to adopt a more conservative outlook in demand growth for the coming quarters, according to

Earlier market expectations assumed that demand would slow in the first quarter prompted by the observation that TV set makers would put a hold on panel purchases based on hopes that panel prices would drop further. Such a view was largely attributed by the development of Chinese panel makers planning aggressive investments over the next two to three years.

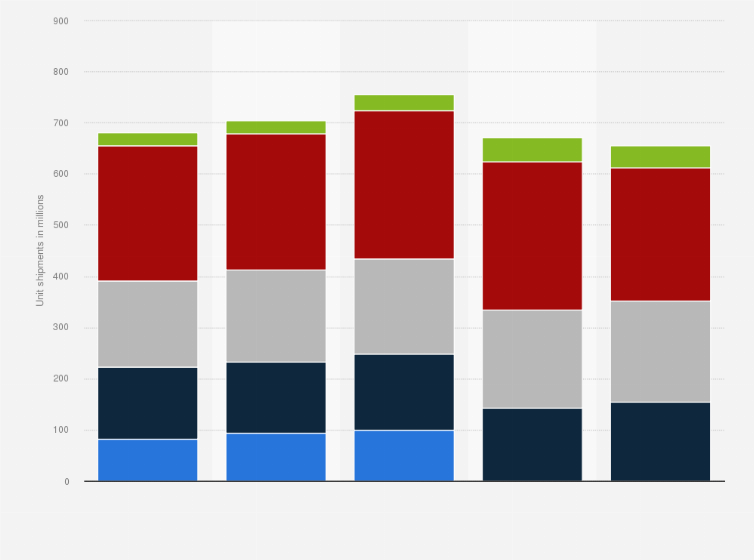

As it turned out, panel makers managed to sell more panels than originally forecasted in the first quarter because panel prices declined much faster than expected. According to IHS Markit, TV panel unit shipments increased by 13.3 percent in the first quarter compared to a year ago, while TV set shipments rose 7.9 percent during the same period.

by IHS Markit, the accumulated gap between LCD TV panel and set shipments in the second and third quarters of 2018 is expected to be higher than past 10 years, reaching 8.3 percent and 8.4 percent, respectively, from 7.9 percent in the first quarter. Furthermore, the gap is expected to remain high until 2019.

“The main reason for the higher gap is the aggressive investment in 10.5 generation fabs. TFT LCD capacity, in terms of area, will soar in the next four years,” Park said. “As capacity is expected to increase more than demand, panel suppliers will likely push to sell panels at lower prices while set makers are to hesitate buying panels expecting the price to drop even further.”

However, when the accumulated gap in panel-set shipments is high, an inventory correction should always follow. “TV makers should narrow the gap for healthy inventory control and reducing panel orders is a step in that direction,” Park said. “If TV set makers’ panel purchasing drops, it will likely cause a cash flow issue to panel suppliers, and they would need to reduce the utilization rate to control the supply.”

IHS Markit (Nasdaq: INFO) is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers next-generation information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 business and government customers, including 80 percent of the Fortune Global 500 and the world’s leading financial institutions.

IHS Markit is a registered trademark of IHS Markit Ltd. and/or its affiliates. All other company and product names may be trademarks of their respective owners © 2018 IHS Markit Ltd. All rights reserved.

(2 November, 2017) – A major decrease in manufacturing cost gap between organic light-emitting diode (OLED) display and liquid crystal display (LCD) panel is expected to support the expansion of OLED TVs, according to new analysis from

analysis estimates that the total manufacturing cost of a 55-inch OLED ultra-high definition (UHD) TV panel -- at the larger end for OLED TVs -- stood at $582 per unit in the second quarter of 2017, a 55 percent drop from when it was first introduced in the first quarter of 2015. The cost is expected to decline further to $242 by the first quarter of 2021, IHS Markit said.

The manufacturing cost of a 55-inch OLED UHD TV panel has narrowed to 2.5 times that of an LCD TV panel with the same specifications, compared to 4.3 times back in the first quarter of 2015.

“Historically, a new technology takes off when the cost gap between a dominant technology and a new technology gets narrower,” said Jimmy Kim, principal analyst for display materials at IHS Markit. “The narrower gap in the manufacturing cost between the OLED and LCD panel will help the expansion of OLED TVs.”

However, it is not just the material that determines the cost gap. In fact, when the 55-inch UHD OLED TV panel costs were 2.5 times more than LCD TV panel, the gap in the material costs was just 1.7 times. Factors other than direct material costs, such as production yield, utilization rate, depreciation expenses and substrate size, do actually matter, IHS Markit said.

The total manufacturing cost difference will be reduced to 1.8 times from the current 2.5 times, when the yield is increased to a level similar to that of LCD panels. “However, due to the depreciation cost of OLED, there are limitations in cost reduction from just improving yield,” Kim said. “When the depreciation is completed, a 31 percent reduction in cost can be expected from now.”

by IHS Markit provides more detailed cost analysis of OLED panels, including details of boards, arrays, luminescent materials, encapsulants and direct materials such as driver ICs. The report also covers overheads such as occupancy rate, selling, general and depreciation costs. In addition, this report analyzes OLED panels in a wide range of sizes and applications.

IHS Markit (Nasdaq: INFO) is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers next-generation information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 key business and government customers, including 85 percent of the Fortune Global 500 and the world’s leading financial institutions. Headquartered in London, IHS Markit is committed to sustainable, profitable growth.

IHS Markit is a registered trademark of IHS Markit Ltd and/or its affiliates. All other company and product names may be trademarks of their respective owners © 2017 IHS Markit Ltd. All rights reserved.

As part of Omdia’s displays research practice, Ricky Park examines all the major flat panel display (FPD) applications. He analyzes historical shipments and forecast projections, including details from global FPD producers, and provides insights on the many different segments, technologies, features, sizes, resolutions, and prices within the FPD industry.

Ricky joined Omdia (formerly IHS Markit) in 2012 when it acquired Displaybank, where he had worked for 11 years. He has published syndicated reports covering display technologies and has served as project manager of industry feasibility studies for Fortune 500 companies. One of the main developers of Omdia’s displays practice, Ricky applied his unique methodologies, processes, and network capabilities to expand the business into its current form. He has also conducted analytical studies of key markets, specializing in various technologies and applications of the electronics value chain industry. Ricky received his bachelor’s degree in engineering from Hanyang University in Seoul, South Korea.

Queenie Jiang is a research analyst in the Displays team at Omdia and based in Shanghai, China. She covers display components research with a specific focus on China; she analyzes the market, prices, supply chains, and technologies.

Queenie joined the company in 2013. Before becoming an analyst, Queenie was a marketing manager at Omdia, where she spent seven years in the Components and Devices pillar. Prior to joining Omdia (formerly IHS Markit), Queenie worked in the project development team at Trina Solar. She holds a bachelor’s degree in Korean from Yangzhou University, China, and Yeungnam University, South Korea.

Linda Lin covers large-sized thin-film-transistor LCD panels and is in charge of survey reports covering manufacturers and vendors in the notebook panel supply chain. With her many years of experience, Linda has developed first-rate relationships throughout her extensive network of contacts and connections in the display industry.

Linda previously worked at LCD market research firm WitsView, leading research on panels and downstream products, including monitors and TVs. At the Market Intelligence & Consulting Institute, Taiwan’s chief information and communications technology market research group, she oversaw regional research for South and East Asia. It was during this time that Linda decided to make large-sized displays her main focus. Linda has a master’s degree in business administration from National Yunlin University of Science and Technology in Taiwan.

Deborah Yang is a noted expert with over 14 years of experience in research and analysis of the flat panel display supply chain across the world. She works in the display team, responsible for the display and OEM supply chain research, including covering the display industry dynamics, pricing trends, and business relations and strategy in the Omdia technology group.

Deborah Yang previously worked at IHS Markit, following its acquisition of DisplaySearch, as director of Taiwan and China display market research. Prior to DisplaySearch, Deborah spent more than 10 years at Royal Phillips Electronics. There, she held the position of business intelligence manager in the flat panel purchasing department of the Philips CE Business Group. Deborah received an award for her role as senior market analyst at Philips and was a nominee for the Royal Philips Electronics PD PBE Best Practice Award. She holds a Master of Business Administration from Preston University, Wyoming, US, and a bachelor"s degree in economics from SooChow University, Taiwan.

As part of Omdia’s displays practice, Jay focuses on researching AMOLED panel display technology and the associated markets. He covers the emerging technologies, process development, and product trends related to AMOLED displays.

Peter is an expert in research and analysis of large area displays (TVs, monitors, notebooks, and tablets), covering TFT, LCD, and OLED marketing, technology, and panel strategy. His analysis of supply capacity, product specifications, pricing, and short-term and long-term forecasts bring value to both panel makers and brand customers.

Robin Wu covers large-sized displays, including the production strategies of display manufacturers and investment flows in the industry. He joined the Omdia (previously IHS Markit) in 2014, where he served as an analyst for PCs and TFT LCDs, specializing in trend analysis of China"s PC, monitor, and display panel markets.

He was also the vice chairman of the VESA monitor task group in 2010, and he has been tracking monitor and panel standardization concerns since early 2009. Robin worked previously at IBM/Lenovo, spending nearly seven years on its monitor and LCD business, delivering the company’s industry leading green ThinkVision products while also managing panel sourcing and qualifications. He was also the industry liaison, building strong relationships with leading PC monitor OEMs in China. Robin has a bachelor"s degree in mechanics and electronics, as well as a master"s degree in microelectromechanical systems from Huazhong University of Science and Technology, a key national university in China.

Prior to joining Omdia, formerly IHS Markit including DisplaySearch acquired by IHS, in 2008, Ken was in marketing and sales, starting with software engineer in the visual display division at Samsung Electronics. He has a bachelor"s degree in computer science from Kookmin University in Seoul, Korea.

Prior to joining to Informa Tech (now Omdia), he served as a director in IHS Markit’s large-area displays and display chemical materials analysis team. He also led the display material/components research team at NPD DisplaySearch Korea, where he was the office’s general manager. Before that, he worked in the R&D and marketing teams of Samsung SDI’s CRT and PDP division, managing PDP product planning and technology marketing and leading the flat panel display (FPD) benchmarking team.

Jimmy is a Senior Principal Analyst in charge of display materials and cost analysis within the Omdia group. He joined Omdia (formerly IHS Markit) in November 2014, when IHS Markit acquired DisplaySearch, where he served as a senior analyst in charge of display materials and LED analysis.

Before DisplaySearch, he spent three years on the marketing team at Samsung LED (currently Samsung Electronics), leading the display-related LED market team and creating marketing strategies for the company. Prior to Samsung LED, Jimmy spent five years at Samsung Electronics working on the R&D team for the LCD business. There, he led several R&D projects on new light sources for LCD backlights and new BLU structures. He earned his Ph.D. from the School of Materials Science and Engineering at Seoul National University, Korea.

Prior to joining Omdia, Tay developed market insights at Hewlett Packard. He also worked as a B2B specialist in the printing division at Samsung Electronics where he managed overseas customers. Before that, he was with a B2B division at Samsung Fine Chemicals for electronic materials including LCD.

Before joining Omdia, formerly IHS Markit, in 2011, Jerry was an OLED development engineer at Samsung SDI and Samsung Mobile Display, where he led the company’s research of the OLED technology and the global OLED display market. With more than 18 years of industry experience, Jerry is known for his professional analysis and strategic insights on the technology and the OLED, quantum dot, and micro LED displays markets. He is frequently quoted in the media and is a frequent guest speaker at major conferences worldwide. Jerry holds a bachelor’s degree in electronics engineering from Pusan National University in South Korea.

Alex joined Omdia in 2005 and has carried out multiple projects for players in the display industry as well as government entities. He has led numerous projects, including feasibility studies of investment, marketability forecasts of emerging technologies, establishment of business cluster development strategy, and long-term LCD and OLED market volume and pricing forecasts. This experience has provided him with extensive network capability in the display panel market and in-depth knowledge of the supply chain. Alex received a bachelor’s degree in sociology from Hanyang University in Seoul, Korea.

Brian Huh is responsible for the market research of small and medium displays (below 9 inches), including smartphone, automotive, wearable, and other emerging applications. His primary research is on the TFT LCD/AMOLED display market outlook and the supply chain of small and medium displays.

Brian joined Informa Tech (now Omdia) in 2019 when it acquired IHS Markit. At IHS Markit, he researched on the small and medium displays market for six years. Brian’s previous work experience also includes working at Hydis in South Korea as a TFT LCD module process engineer, product planner, and strategic marketing manager for 11 years. He holds a bachelor"s degree in electronics from Dongguk University in South Korea.

David Hsieh is an expert in the TFT LCD, OLED, LCD TV, and smartphone display value chain for mainland China, Taiwan, Japan, and Korea. David is head of the Displays team and oversees the division’s end-to-end research on displays, covering the supply chain, materials, components, supply and demand dynamics, pricing, cost modeling, revenue and shipment forecasts, and emerging technologies.

In 2019, David and his leading display research analysts team joined Omdia from IHS Markit. Prior to Omdia, David was named as one of just 11 technology fellows by IHS Markit an honor that recognizes his deep expertise and exceptional standing within the analyst community. He is a graduate of Chung-Yuan Christian University in Taiwan and has a bachelor’s degree in industrial engineering. David also holds a master’s degree in business administration from Preston University, Wyoming, US. David is a fluent speaker of Chinese, Taiwanese, Japanese, and English.

Jusy joined IHS Markit (now Omdia) in 2004 and became a leading TV research analyst. His work has concentrated on demand forecasting and competitive, pricing, and technology trend analysis. He has also served as project manager for consultancy projects related to display technology, market and consumer trends, and feasibility study and cost analysis for manufacturers, government institutions, and investment companies. He frequently speaks at major industry events around the world, including display conferences like SID and IMID. Based in South Korea, Jusy speaks fluent Korean, English, and Japanese and has a broad network of key contacts in South Korea and Japan.

Irene is Omdia’s Senior Principal Analyst for display materials and components research, focusing on optical films for displays and touch panels. She provides insights by covering various optical film industries and delivering market forecasts based on the panel and set markets, supply/demand and technology dynamics, pricing and cost modeling, and makers’ strategies.

Jimmy joined the company in 2014 following the acquisition of DisplaySearch, where he served as a senior analyst covering display materials and LED analysis. Jimmy also worked at Samsung—first at Samsung LED, and then at Samsung Electronics. There, he led several R&D projects on new light sources for LCD backlighting and new BLU structures.

As part of Omdia’s displays practice, Jay focuses on researching AMOLED panel display technology and the associated markets. He covers the emerging technologies, process development, and product trends related to AMOLED displays.

Prior to working at Omdia, Jeff was an engineer at Chunghwa Picture Tubes, where he led TV panel development projects and promoted products. He worked at Samsung Electronics Taiwan, winning the annual best sales award while handling HP’s monitor business account, and was a procurement manager at Benq for monitor panel and TV set purchasing and panel price trend analysis. Jeff joined DisplaySearch in 2010 as a value chain analyst for the tablet, notebook PC, monitor, and public display supply chain. Jeff graduated from Taiwan’s National Cheng Kung University with a degree in environmental engineering and holds an MBA from National Chengchi University in Taiwan.

Deborah Yang is a noted expert with over 14 years of experience in research and analysis of the flat panel display supply chain across the world. She works in the display team, responsible for the display and OEM supply chain research, including covering the display industry dynamics, pricing trends, and business relations and strategy in the Omdia technology group.

Deborah Yang previously worked at IHS Markit, following its acquisition of DisplaySearch, as director of Taiwan and China display market research. Prior to DisplaySearch, Deborah spent more than 10 years at Royal Phillips Electronics. There, she held the position of business intelligence manager in the flat panel purchasing department of the Philips CE Business Group. Deborah received an award for her role as senior market analyst at Philips and was a nominee for the Royal Philips Electronics PD PBE Best Practice Award. She holds a Master of Business Administration from Preston University, Wyoming, US, and a bachelor"s degree in economics from SooChow University, Taiwan.

Peter is an expert in research and analysis of large area displays (TVs, monitors, notebooks, and tablets), covering TFT, LCD, and OLED marketing, technology, and panel strategy. His analysis of supply capacity, product specifications, pricing, and short-term and long-term forecasts bring value to both panel makers and brand customers.

Vicki Chen focuses on display materials and components, including new form factors, weight efficiencies, and technological advances in displays. She joined the company in 2018, bringing more than 10 years of experience in the flat panel display (FPD) industry.

Vicki worked previously at Chinese firm Sigmaintell Consulting, where she was responsible for research on the mobile phone panel market and value chain. She also worked in new-project development at Taiwan Display, a part of Japan Display. She had her first taste of the FPD industry and worked as a product planning engineer in charge of the request-for-quote (RFQ) development for mobile phone products for Chinese brands at Innolux, a TFT LCD panel manufacturer in Taiwan. Vicki has an undergraduate degree from Nanchang Hangkong University, also known as Nanchang Aviation University, in China.

Robin Wu covers large-sized displays, including the production strategies of display manufacturers and investment flows in the industry. He joined the Omdia (previously IHS Markit) in 2014, where he served as an analyst for PCs and TFT LCDs, specializing in trend analysis of China"s PC, monitor, and display panel markets.

He was also the vice chairman of the VESA monitor task group in 2010, and he has been tracking monitor and panel standardization concerns since early 2009. Robin worked previously at IBM/Lenovo, spending nearly seven years on its monitor and LCD business, delivering the company’s industry leading green ThinkVision products while also managing panel sourcing and qualifications. He was also the industry liaison, building strong relationships with leading PC monitor OEMs in China. Robin has a bachelor"s degree in mechanics and electronics, as well as a master"s degree in microelectromechanical systems from Huazhong University of Science and Technology, a key national university in China.

Ricky Park currently leads the LCD research team, which has published more than 15 syndicated reports covering the large-area TFT-LCD panel market and all other applications utilizing larger-sized panels. He also serves as project manager for dozens of high-value industry feasibility studies carried out for Fortune 500 companies.

Ricky was one of the main developers of the LCD research practice, where he applied his unique methodologies, processes, and network capabilities to expand the TFT-LCD research business into its current form. He has conducted numerous analytical studies of key markets, specializing in various technologies and applications of the electronics value chain industry.

He joined IHS in November 2014, when IHS acquired DisplaySearch, a leader in primary research and forecasting on the global display market. At DisplaySearch, he served as director of large-area displays & FPD materials analysis in the company"s Korea office. He is a recognized display expert and has been invited to speak on large-area displays, especially on PDP technology, at many Korean FPD forums.

Prior to joining the company, he developed market insights from analysis experiences in the OPS Planning & Analytics team at Hewlett Packard. He also worked as a B2B specialist in the printing division at Samsung Electronics for managing overseas customers in China, Middle East, and Africa. Before that, he was also in a B2B division at Samsung Fine Chemicals for electronic materials including LCD and PDP Prism film. Tay has a Bachelor’s of Science in chemical engineering from Yonsei University in Seoul, Korea.

Jerry Kang is responsible for the OLED display market analysis at IHS. His main focus is the AMOLED panel and the next generation display market including flexible and transparent display with AMOLED.

Prior to joining IHS in 2011, Jerry worked as an OLED development engineer at Samsung SDI and Samsung Mobile Display, in charge of operational circuit designing for OLED and LCD.

Alex Kang is responsible for large-area TFT-LCD panel market research at Omdia, including manufacturing fab and supply chain management. He is one of the key contacts for the LCD research.

Alex joined the team in 2005 and has carried out multiple projects for the players in the display industry and government entities. He led numerous projects, including feasibility studies of investment, marketability forecast of emerging technologies, establishment of business cluster development strategy, and long-term LCD market volume and pricing forecast.

Brian Huh is a principal analyst within the Omdia (previously IHS) technology group. He joined in November 2014, when the company acquired DisplaySearch, a leader in primary research and forecasting on the global display market. At DisplaySearch, he served as a senior analyst for small and medium displays, including emerging displays, touch screen panels and mobile PC displays.

Prior to DisplaySearch, Brian worked at Hydis in South Korea as a TFT LCD module process engineer for five years and as a strategic marketing manager for six years. He is an expert in planning new products and promotions, formulating product and business strategy, and forecasting for mobile PC panels and smartphone displays. Brian has a bachelor"s degree in electronics from Dongguk University in Seoul, South Korea. He speaks both Korean and English.

David Hsieh is a noted expert in research and analysis of the TFT LCD, and LCD TV value chain for Mainland China and Taiwan. As head of the Displays team, he oversees the division’s end-to-end research on displays, covering the supply chain, materials and components, supply-and-demand dynamics, pricing and cost modeling, revenue and shipment forecasts, and emerging technologies.

In an earlier stint at DisplaySearch, he led the company’s primary research and forecasting on the global display market while concurrently serving as vice president of the greater China market. David also worked at HannStar Display, a leading manufacturer of TFT LCD panels, as a key account manager, production planner, and production engineer for the HannStar TFT LCD module line.

David belongs to a distinguished circle of only 11 Technology Fellows named by IHS Markit during his time at the company, an honor that recognizes his deep expertise and exceptional standing within the analyst community.

In his previous roles at the company, Jusy led the research team on TV technology and ecosystems, which included the panel display market for TVs and large-sized LCDs. He has also worked on the global monitor and public information markets.

As part of Omdia’s small/medium displays practice, Joy covers displays under 9 inches in size utilized in smartphones, tablets, wearables, and automotive displays. Her research touches areas such as the AMOLED ecosystem, new trends in smartphone panel displays, and the supply chain in China for smartphone displays.

Joy brings 17 years of experience to the subjects she covers. She worked previously at BOE, the giant Chinese display manufacturer, as a product manager for medical and industrial displays. She started her career at Tianma Group as an LCD module design engineer, then became manager of product design and development. She transferred to the marketing department as an analyst for mobile phone displays and then for automotive displays. Joy has a bachelor’s degree in automation from Beihang University, a major public research institution in China. She also holds a master’s degree in business management from Renmin University of China.

PC brands continued to seek lower prices, even on bundle deals, in March. These deals have already been completed to secure volumes, or receive volumes at short notice.

Most panel makers have lowered production of HD TN eDP panels, due to significant losses made on these units. 15.6″ HD TN LVDS models, for example, reached end-of-life in 2015, although a few were available in the end market. Chinese second- and third-tier makers asked for $27 – $30+ prices for this model.

IHS expects prices for mainstream panels to remain flat through May and June, due to the reduction in HD TN panel supply. Capacity will instead be shifted to monitor, mobile or automotive applications, or 7″ cell glass.

The Taiwan earthquake (Earthquake Rocks Taiwan Production Base), and a lower supply of 7″ cells, led to a 5% QoQ price hike for Chinese white-box makers. However, IHS expects demand to be weaker in Q2, due to fewer projects and a seasonal slow-down. Apple’s 9.7″ iPad Pro will be the only tablet to stimulate demand.

Most tablet makers are considering hybrid (2-in-1) projects; both premium and entry-level models are being produced for the back-to-school season in Q3. Therefore, IHS believes that tablet panel prices will remain flat in the Chinese white-box segment, as prices are already low and there is less supply. On the branded side, prices are heading slightly downwards.

Smartphone demand has not been strong recently. Brands are cautious about over-ordering. There is a ‘delicate’ balance between cell makers, model makers and brands that has kept module prices stable in April.

Demand for panels with 1920 x 1080 and higher resolutions is still good, even for future models. Panel makers have released new lower quotes for clients, which have lowered the ASPs of Full HD displays by 1-2%.

The partnership will see IHS Markit’s thinkFolio clients gain click-to-view, consolidated, and pre-trade institutional bond quote data from 34 dealers, as well as post-trade and normalised TRACE data.

“Our client base, regardless of domicile, continue to participate heavily in the US investment grade and high yield marketplace. Having direct, actionable, BondCliQ aggregated dealer quote information and historical TRACE intelligence embedded within thinkFolio screens will facilitate corporate bond price discovery, streamline communication between portfolio managers and traders, and offer deeper best execution insights.”

“By collaborating with IHS Markit, BondCliQ dealers can distribute their markets directly to the global thinkFolio client network which instantly improves the link between market-maker quotes and customer engagement,” BondCliQ chief executive, Chris White, commented. “This simple and efficient approach reduces disintermediation by bringing the buy-side and the sell-side closer together.”

Until about a year ago, active-matrix organic light-emitting diode (AMOLED)–based smartphones remained Samsung’s niche. Almost all the AMOLEDs Samsung was making went into Galaxy products. AMOLED prices were relatively high compared to equivalent liquid crystal displays (LCDs). Samsung’s AMOLED fab utilization was low, and it was struggling to ramp up its A3 flexible AMOLED dedicated fab. Its AMOLED business was challenged to raise profits.

What a difference a year makes! Now in June 2016, the outlook for AMOLED smartphones has dramatically shifted in a positive direction. Samsung’s AMOLED fab utilization is high, prices for external customers are on par with LCDs, and the company’s AMOLED business is profitable. Over the same period, it has become evident that Apple plans to transition the iPhone display from rigid LCDs to flexible AMOLEDs in the next couple of years. Meanwhile, more and more people are talking about the coming flexible or foldable OLED displays that will bring revolutionary change to the form factor of handheld devices.

These shifts in market outlook have created an unprecedented wave of new flexible AMOLED fab investment plans for makers in Korea, China, and Japan. Competitors are trying to replicate Samsung’s success, hoping to escape the commoditization and low profitability of LCDs—and chasing after potential Apple business. A large number of new fabs are now being built, and they are the most expensive ever made relative to glass size and input capacity.

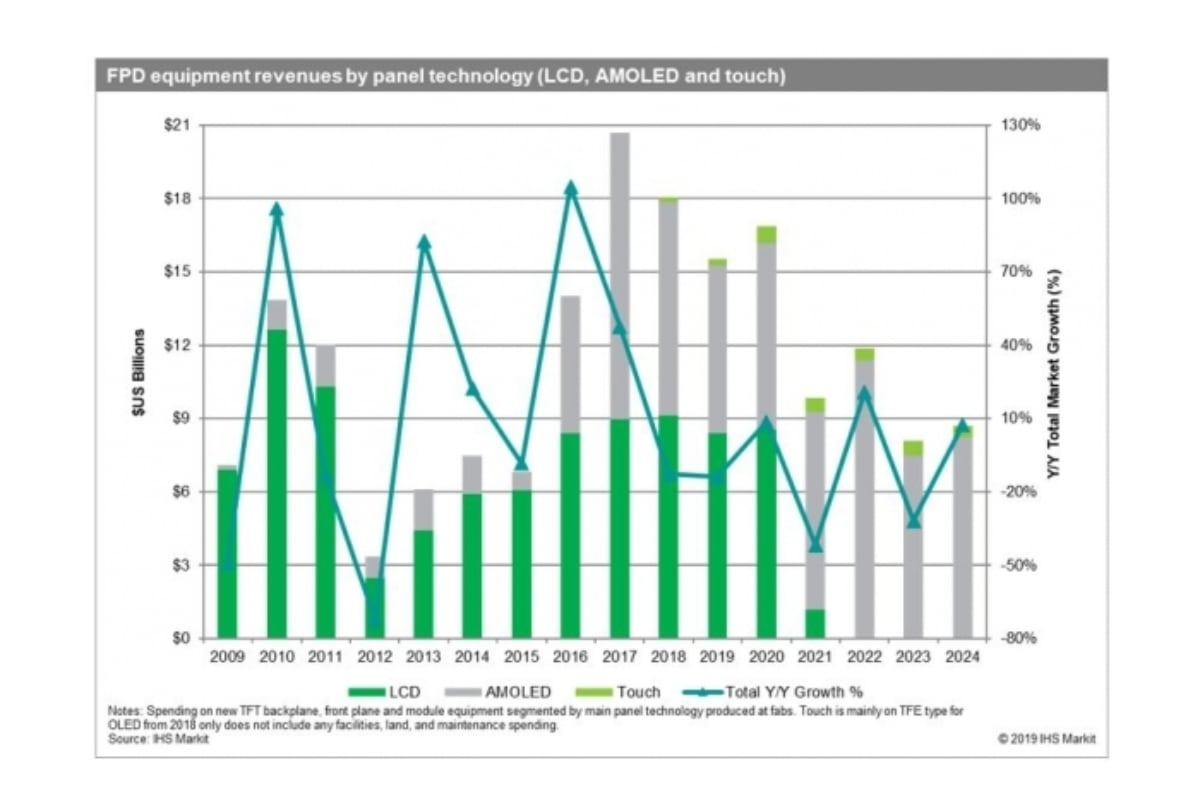

Although Samsung’s AMOLED process to date has used a simplified p-channel metal-oxide-semiconductor (PMOS) thin-film transistor (TFT) for the back plane, other makers and new lines targeting Apple demand appear to be preparing for processes that use up to 50% more mask steps. Low temperature polysilicon and oxide (LTPO) is one of the candidates. This drives significantly more TFT equipment, automation, and other spending. Furthermore, all the new AMOLED fabs will be designed to produce flexible AMOLEDs or will be hybrid rigid/flexible lines. Flexible capability adds costs to the TFT backplane process by requiring flexible substrate coating, curing, and encapsulation steps. Flexible capability adds cost to the front plane process by requiring thin-film encapsulation (TFE), laser lift-off (LLO), and a variety of other steps necessary to handle flexible panels. As shown below, the new flexible AMOLED fabs for mobile display production have a total costs that is almost 1.4x higher than previous rigid AMOLED lines, according to the IHS Technology Display Supply Demand & Equipment Tracker report.

In other words, pushed by a complex TFT process and flexible display requirements, the new AMOLED fabs are the most expensive flat-panel display (FPD) factories ever built, nearly 1.4x that of previously constructed rigid AMOLED lines.

Capital equipment markets tend to be highly cyclical, but the high cost of flexible AMOLED fabs is pushing the equipment market in 2016 and 2017 to near-historic two-year highs. Some concerns have been raised that equipment supply bottlenecks will restrict panel makers’ ability to build fabs according to schedule. Most of these concerns have focused on high-resolution photolithography machines, RGB evaporators, and some high-performance vacuum tools.

However, presented with the best business opportunity since 2010 and 2011, equipment makers are rapidly adding capacity as well as actively managing their suppliers and scheduling in order to meet customer requests. Although any unexpected supply chain disruption could delay some fab plans, it now appears that most of the new fabs will be built out in line with panel makers’ target schedules.

According to the IHS Technology Display Supply Demand & Equipment Tracker report, the large number of new flexible AMOLED investments, along with the high costs of these lines, is pushing the FPD equipment market to near-record two-year highs of $12.6 billion in 2016 and $12.3 billion in 2017.

Forecasting the supply and demand of flexible AMOLEDs in 2018 is a challenging task, not only due to the assumptions that must be made about both capacity and demand, but also the questions about yield rates, how long it will take fabs to ramp and begin commercial production, and the price competitiveness of these new fabs. Building rational forecasts of capacity is possible based on panel maker plans because new factories have lead times of up to two years.

In order to test supply and demand under the more optimistic scenario of faster adoption by Apple, the IHS forecast for total AMOLED smartphones was increased to 503 million units in 2017 and 653 million in 2018. This includes Samsung Galaxy phones, other brands such as Chinese cell phone makers, and a reasonable adoption forecast for Apple. Other mobile applications are also counted in demand. Relatively long ramp-up times and low yield rates for all makers, except Samsung, were assumed. Prices were presumed to be competitive and not directly tested in this analysis.

Analyzing all panel makers’ capacity plans and the comparatively aggressive demand forecast, the glut level is projected to increase from 2016 through 2018, suggesting a trend of growing oversupply.

Samsung’s strategy likely involves adding enough capacity to enable it to continue—for as long as possible and almost exclusively—to dominate the AMOLED market for mobile applications. Samsung Display has a substantial technology and cost lead over even its closest competitors. It controls much of its own process know-how, and it will be a difficult path for followers to catch up in the near- or even mid-term. According to our analysis, Samsung could potentially maintain its AMOLED monopoly through 2018 or longer, even when taking into consideration the large increase in demand as the iPhone transitions from LCD to AMOLED.

The shift from rigid LCD to flexible AMOLED is the most significant change in FPD process technology since the start of the LCD era almost 20 years ago. All panel makers are now scrambling to avoid being left behind during this technology revolution.

However, as supply/demand analysis suggests, all the capacity being added by new AMOLED players may well get ahead of how much the market can absorb. Demand could grow faster than the accelerated forecast; however, it is not clear by how much. In 2018 and 2019 the market for both rigid and flexible AMOLED may be restricted by prices. It is unlikely that many makers will be able to compete on price and performance with Samsung or even with low-cost, high-end LCDs without incurring financial losses.

In the long run, all the investment in AMOLED capacity will help reduce material prices, strengthen the equipment supply chain, and allow the market to trend towards balance. However, it would also not be surprising for new AMOLED entrants to struggle to ramp up new fabs in 2018 and 2019, and suffer from low utilization and profitability as the industry works through the currently forecast flexible AMOLED supply glut.

Commodities & Futures: Futures prices are delayed at least 10 minutes as per exchange requirements. Change value during the period between open outcry settle and the commencement of the next day"s trading is calculated as the difference between the last trade and the prior day"s settle. Change value during other periods is calculated as the difference between the last trade and the most recent settle. Source: FactSet

Mutual Funds & ETFs: All of the mutual fund and ETF information contained in this display, with the exception of the current price and price history, was supplied by Lipper, A Refinitiv Company, subject to the following: Copyright © Refinitiv. All rights reserved. Any copying, republication or redistribution of Lipper content, including by caching, framing or similar means, is expressly prohibited without the prior written consent of Lipper. Lipper shall not be liable for any errors or delays in the content, or for any actions taken in reliance thereon.

IHS Markit has partnered with BondCliQ to embed US corporate bond pricing content and interactive functionality withinthinkFolio, our leading multi-asset investment management platform. The collaboration will provide click-to-view, consolidated, pre-trade, institutional quote data from 34 dealers, and post-trade, normalized, analytics-enriched TRACE data directly within thinkFolio"s modular screens.

"Given the fragmented and dynamic liquidity profile of fixed income markets, we are focused on continually enhancing thinkFolio to provide richer pre-trade insights and analytics to our users," said Brett Schechterman, Global Head of thinkFolio at IHS Markit. "Our client base, regardless of domicile, continue to participate heavily in the US investment grade and high yield marketplace. Having direct, actionable, BondCliQ aggregated dealer quote information and historical TRACE intelligence embedded within thinkFolio screens will facilitate corporate bond price discovery, streamline communication between portfolio managers and traders, and offer deeper best execution insights."

"By collaborating with IHS Markit, BondCliQ dealers can distribute their markets directly to the global thinkFolio client network which instantly improves the link between market-maker quotes and customer engagement," said Chris White, CEO, BondCliQ. "This simple and efficient approach reduces disintermediation by bringing the buy-side and the sell-side closer together."

The statistic illustrates the worldwide notebook PC display average panel price from 2016 to 2018. In 2017, the average price for individual notebook displays was projected to reach 46.68 U.S. dollars worldwide.Read moreGlobal notebook PC display average panel price from 2016 to 2018(in U.S. dollars)CharacteristicAverage panel price in U.S. dollars--

IHS. (October 26, 2017). Global notebook PC display average panel price from 2016 to 2018 (in U.S. dollars) [Graph]. In Statista. Retrieved January 28, 2023, from https://www.statista.com/statistics/779169/global-notebook-pc-display-average-panel-price/

IHS. "Global notebook PC display average panel price from 2016 to 2018 (in U.S. dollars)." Chart. October 26, 2017. Statista. Accessed January 28, 2023. https://www.statista.com/statistics/779169/global-notebook-pc-display-average-panel-price/

IHS. (2017). Global notebook PC display average panel price from 2016 to 2018 (in U.S. dollars). Statista. Statista Inc.. Accessed: January 28, 2023. https://www.statista.com/statistics/779169/global-notebook-pc-display-average-panel-price/

IHS. "Global Notebook Pc Display Average Panel Price from 2016 to 2018 (in U.S. Dollars)." Statista, Statista Inc., 26 Oct 2017, https://www.statista.com/statistics/779169/global-notebook-pc-display-average-panel-price/

IHS, Global notebook PC display average panel price from 2016 to 2018 (in U.S. dollars) Statista, https://www.statista.com/statistics/779169/global-notebook-pc-display-average-panel-price/ (last visited January 28, 2023)

Global notebook PC display average panel price from 2016 to 2018 (in U.S. dollars) [Graph], IHS, October 26, 2017. [Online]. Available: https://www.statista.com/statistics/779169/global-notebook-pc-display-average-panel-price/

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey