lcd panel price ihs for sale

(2 November, 2017) – A major decrease in manufacturing cost gap between organic light-emitting diode (OLED) display and liquid crystal display (LCD) panel is expected to support the expansion of OLED TVs, according to new analysis from

analysis estimates that the total manufacturing cost of a 55-inch OLED ultra-high definition (UHD) TV panel -- at the larger end for OLED TVs -- stood at $582 per unit in the second quarter of 2017, a 55 percent drop from when it was first introduced in the first quarter of 2015. The cost is expected to decline further to $242 by the first quarter of 2021, IHS Markit said.

The manufacturing cost of a 55-inch OLED UHD TV panel has narrowed to 2.5 times that of an LCD TV panel with the same specifications, compared to 4.3 times back in the first quarter of 2015.

“Historically, a new technology takes off when the cost gap between a dominant technology and a new technology gets narrower,” said Jimmy Kim, principal analyst for display materials at IHS Markit. “The narrower gap in the manufacturing cost between the OLED and LCD panel will help the expansion of OLED TVs.”

However, it is not just the material that determines the cost gap. In fact, when the 55-inch UHD OLED TV panel costs were 2.5 times more than LCD TV panel, the gap in the material costs was just 1.7 times. Factors other than direct material costs, such as production yield, utilization rate, depreciation expenses and substrate size, do actually matter, IHS Markit said.

The total manufacturing cost difference will be reduced to 1.8 times from the current 2.5 times, when the yield is increased to a level similar to that of LCD panels. “However, due to the depreciation cost of OLED, there are limitations in cost reduction from just improving yield,” Kim said. “When the depreciation is completed, a 31 percent reduction in cost can be expected from now.”

by IHS Markit provides more detailed cost analysis of OLED panels, including details of boards, arrays, luminescent materials, encapsulants and direct materials such as driver ICs. The report also covers overheads such as occupancy rate, selling, general and depreciation costs. In addition, this report analyzes OLED panels in a wide range of sizes and applications.

IHS Markit (Nasdaq: INFO) is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers next-generation information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 key business and government customers, including 85 percent of the Fortune Global 500 and the world’s leading financial institutions. Headquartered in London, IHS Markit is committed to sustainable, profitable growth.

IHS Markit is a registered trademark of IHS Markit Ltd and/or its affiliates. All other company and product names may be trademarks of their respective owners © 2017 IHS Markit Ltd. All rights reserved.

At least five LCD display factories at the epicenter of the coronavirus outbreak are suffering production slowdowns, which is turn is expected to have an effect on the supply and pricing of displays used in PCs and LCD TVs.

Five LCD fabs reside in Wuhan, China, which has basically been shut down to prevent the coronavirus from spreading. Informa Tech’s IHS Markit service said Friday that they expect that the capacity utilization for all LCD fabs in China could fall by at least 10 percent and by as much as 20 percent during February.

As a result, LCD panel prices are expected to rise. IHS said that preliminary estimates say that per-panel prices could rise $1 to $2, but could go as high as $3 to $5. That might not sound like much, but manufacturers typically tack on extra profit margins at each stage of production, potentially raising sale prices somewhat higher.

IHS estimates that about 55 percent of all LCD panels in the world will ship from China in 2020, meaning that the Chinese outbreak will have worldwide effects on the supply chain. Five fabs are in Wuhan itself, including two fabs owned by China Star Optoelectronics Technology, two owned by Tianma, and one BOE fab.

“Display facilities in Wuhan currently are dealing with the very real impacts of the coronavirus outbreak,” said David Hsieh, senior director of displays, at IHS Markit technology research, in a statement. “These factories are facing shortages of both labor and key components as a result of mandates designed to limit the contagion’s spread. In the face of these challenges, top display suppliers in China have informed our experts that a near-term production decline is unavoidable.”

IHS reported seeing panic buying, including doublebooking, where a buyer will buy as much as they need from two suppliers just to ensure that they’ll be able to get the supplies they require. Even if the supplies are there, IHS also said that production at several key third-party LCD module suppliers has now ceased, severely impacting panel production throughout the country.Besides the slowdown in production at fabs that are already operating, IHS said that it expects new fabs to not come on line as quickly as expected.

All this is expected to have a direct effect on LCD panel pricing, and possibly ripple effects through laptop manufacturing as well. It’s worth noting that while Intel and AMD did not cite coronavirus effects among their forecasts, Microsoft did, with a broader than usual forecast for the second half of the year.

Prices on LCD TVs in certain screen sizes could come down more noticeably this year as open cell panel suppliers, primarily in China and South Korea, continue to adjust down production volumes amidst building inventory rather than give in to pressure from TV makers to drop prices too close to cost.

David Hsieh, senior director of display research for IHS, said major LCD open cell panel producers from China, and to a lesser degree South Korea, are seeing pressure to reduce prices, and will need to reduce capacity utilization through the second quarter of 2018.

For perspective, global television sales were soft through much of 2017 due to panel shortages in certain screen sizes, which kept prices on finished TVs stable much of the year, presenting less opportunity for aggressive price promotion.

Hsieh said Korean panel makers expect more panel price pressure in the fourth quarter of 2018 due to new capacity coming online from BOE’s 10.5 Gen fab (producing mainly 65-inch 4K panels), the end of the traditional sports season in most parts of the world, and TV makers adjusting inventories and capacity utilization after comparatively stable panel prices in the second and third quarters.

Hsieh warned that continuous oversupply conditions are likely in those periods, where panel makers did not reduce capacity utilization. As a result, high inventory is present in open cell panel screen sizes of 40, 50, 60, 70, and 65 inches. This is intensifying pressure from TV makers to reduce open cell prices, particularly during the spring.

An open cell panel, is the part of an LCD minus the backlight. Due to the price of finished LCD TVs declining as at a faster rate than the of the panels alone, the industry in recent years has turned more and more to producing open cell panels to reduce the cost to TV makers, and to enable thinner panel depths.

“Some TV makers still expect panel prices to fall below last cycle’s low,” Hsieh wrote. “Panel makers cannot agree to these prices now or in the near-term.”

Meanwhile, TV makers, particularly in China, are feeling pressure to lower prices as a result of slower demand for TVs contributing to larger inventories in the first quarter of 2018.

“TV makers are holding enough inventory to get better bargains from panel suppliers, but some are bluffing to get price concessions,” Hsieh revealed. “Some TV makers may resume panel purchasing or inventory additions when they sense panel prices are at a low.”

Hsieh said TV panel demand is not bad for Korean panel makers. “LG Display expects TV panel demand to continue at 4.2 4.3 million per month in Q2, and Samsung Display expects it to be over 2.0 million per month in that quarter. The issue for Korean panel makers is not demand; it is that panel prices will inevitably fall due to market trends and special promotions from some Chinese and Taiwanese panel makers.”

The LCD, or liquid-crystal display, is the king of the display industry-dominating all major product segments from televisions, to computers, to smartphones and tablets. But having reached maturity after decades of development, and continuing to face challenges from rival technologies, is LCD in danger of losing its market hegemony?

LCD primarily dominated the small-sized markets up until the late 1990s when massive investment in large-scale production using larger-sized factories, or fabs as they are commonly referred to, made it possible to produce big sizes at dramatically lower costs. This initiated a massive change in many market segments, such as TVs and desktop monitors, as well as enabling new product segments to emerge, grow and mature, like notebook PCs, smartphones and tablets. With LCD dominating the display landscape today, new challengers have emerged in recent years with the potential to disrupt the comfortable position that LCD enjoys today.

Early in the history of the flat-panel TV market, plasma TVs became synonymous with a flat-panel TV since it was the only flat display technology available in the larger sizes traditionally associated with TVs. This was especially true at the higher price points the TVs commanded. Can anyone remember the sub-HD 42" plasma TV from Philips for sale at $10,000 around the year 2000? As investment levels rose for new and more advanced production capacity in LCDs, far outpacing that for competing display technologies like plasma, LCD TVs started to capture market share at ever-larger screen sizes while enjoying faster cost reduction.

By 2014, LCD accounted for more than 95 percent share among TV shipments worldwide, leaving just a handful of plasma TV sets and bulky cathode-ray-tube (CRT) televisions still being shipped today. IHS expects both CRT and plasma shipments to end as soon as their production base shuts down. Meanwhile, new display technologies like organic light-emitting diode (OLED) have yet to make a significant impact on the TV market. Similarly, in the desktop monitor space, LCD rapidly replaced CRT as the display technology of choice, although there was never another flat-panel display technology to compete with.

The interesting thing about LCD is that it has succeeded so well despite being a deficient technology in many ways compared to the alternatives. Plasma, a self-emissive technology like CRT, produces more accurate colors, better contrast and greater motion performance than LCD. However, when asked what matters most when choosing a good TV, a majority of consumers claim picture quality trumps all other attributes. So why has LCD come to dominate the TV market?

To be sure, LCD has employed more technological innovation than competing display technologies in order to compensate for its performance deficiencies. In fact, most of the major new feature introductions in the display industry center on advancing LCD performance. Such innovations include higher frame rates to overcome motion blurring, LED backlights with local dimming to enhance contrast and reduce energy consumption, and quantum dots to improve color. Furthermore, because LCD is not a self-emissive technology, it can achieve greater pixel density and higher resolutions than both plasma and OLED in some cases. Each of these incremental improvements has eroded the performance advantages plasma makers had been touting for years.

Even so, many enthusiasts in both the professional industry and consumer marketplace still prefer the picture quality of plasma to LCD. Two reasons why all major suppliers and manufacturers in the plasma industry ended production and threw their support behind LCD were scale and economics.

During much of the 2000s, there were more than two dozen LCD panel manufacturers. In contrast, the number of plasma makers never exceeded half a dozen. Moreover, the level of manufacturing investment in plasma panel production couldn"t come close to the outlays made by LCD panel makers. Why?

The success of any core technology, including displays, depends on the success of the end-market customers, in this case the brands that sell these products to consumers. In 2005, shipments from the top 10 plasma TV brands accounted for just 2.7 percent of total TV market shipment volume. By comparison, the top 10 brands within the LCD TV category during the same year accounted for over 8.4 percent of total TV market shipment volume. At that time, CRT was still the No. 1 display technology, even though LCD was growing much faster than plasma and enjoyed a broader group of successful brands promoting the technology.

Fast forward to 2010, the pivotal year that plasma TV share peaked and began to decline, and the LCD bandwagon momentum became impossible to overcome. Plasma brands began to exit the category, consolidate, or retreat into large-sized niches where LCD couldn"t yet compete on price as effectively. However, investment continued in larger-sized fabs for LCDs, and IHS forecasts that 2015 will see the final shipments of plasma TVs worldwide. In most cases, the plasma TV suppliers also had significant LCD production bases or were working on new OLED display technology, and the suppliers chose to reallocate their resources away from plasma in the wake of the inevitable outcome.

Not only can the support of brands within a category lead a display technology to succeed or fail, but the support of application category can also contribute to economies of scale. In particular, the PC and information technology (IT) categories have been instrumental in the success of LCD. And unlike plasma, the growth of these other IT-related categories occurred earlier and with broader applications beyond TV.

Since 2005, aggressive capacity expansions in LCD factories have reconfigured the competition in flat-panel displays, according to David Hsieh, senior director of displays at IHS. The assertive supply-side expansion comes from panel makers, with the display supply chain gaining good resources from the well-established PC/IT market, especially for desktop monitors and notebook PCs, and then subsequently for tablet PCs. As a result, panel makers have gained great growth and financial reward from the PC market since the start of the new millennium, Hsieh noted, at the same time that process technology improvement and supply-chain growth have improved the capability of panel makers to build bigger glass-substrate fabs for enhanced LCD production efficiency.

Investment continues today in expanding LCD production and competitiveness. While TVs account for most of the revenue from LCD panel production, newer applications like smartphones are playing a greater role in industry profit and revenue growth.

For LCD panel manufacturers, investments in LCD are ongoing to grow both LCD supply capacity and factory size as manufacturers strive to compete and expand incrementally into larger screen-size categories. The investment in capacity and production technology has flowed in waves from Japan to South Korea to Taiwan and now to China, lowering the cost of production at each stage. This progressive East-to-West migration of the supply chain for LCD has allowed all end markets to benefit from lower costs, further spurring the replacement by LCD of the older CRT installed base.

Investment in LCD is substantial, and despite the market"s ups and downs fueled by a phenomenon known as the Crystal Cycle, average annual investment is in the $5 billion range. The Crystal Cycle describes the cyclicality driving the LCD industry. Starting from the initial investment, a glut in supply results that creates a drop in panel prices, which fuels end-market growth as retail prices fall. The end-market growth then uses up industry capacity, creating a shortage of panels that drives commoditized panel prices higher, boosting panel-maker profits. This, in turn, creates capital used to fund the next wave of investment. And although global events can have a major impact, IHS has seen the LCD industry"s resiliency in bouncing back by breaking into new categories or defeating other display technologies.

In tracking the investment made in equipment used to produce displays, the results show that LCD dominates, even if a considerable investment in OLED-a newcomer display technology hoping to take a larger part of the display market-has been growing as well.

Although LCD is the dominant display technology today, new technologies are constantly being introduced with an eye to possibly dislodging it from its lofty perch. One relatively recent newcomer is OLED, a self-emissive display technology like plasma in that it produces light directly from each cell. This is in contrast to LCD, which uses a backlight to produce light, then shutters that light through a color filter. Producing the light directly within the cell has many benefits, especially in contrast and efficiency, as well as making the display thinner and lighter. And although judgments are subjective, OLED is regarded by many as trumping all other display technologies-even plasma-in terms of pure picture performance.

Potentially, OLED could be less expensive to manufacture than LCD because of the simpler bill of materials and less complicated production process. While LCD is a very mature technology and enjoys production yields of more than 90 percent, OLED has had to overcome challenges with both manufacturing processes and materials that lead to a much lower effective yield. Yield is measured by looking at total glass input area minus unusable waste, either in the form of discarded materials from the process or in flawed panels. In the case of OLED, this has been a huge challenge.

A simpler structure enables OLED to be thinner, lighter and more efficient than LCD, but the process cost is still three to four times higher than for LCD because less equipment is being developed, with the OLED process also still not as mature as LCD. Nonetheless, the yield rate-which is the biggest challenge for OLED--could also be the biggest threat to LCD. If OLED can be produced with yield rates similar to LCD, then the gap in cost between OLED and LCD will narrow, with OLED a much better form factor and possessing higher color performance than LCD.

The problem with making OLED displays is much greater at higher resolutions, such as 4K-also called UHD-because the flaw rate is compounded by the greater pixel density. Thus far, OLED manufacturers have been doing a good job of improving the yield on smaller displays. Samsung has introduced OLEDs in a range of smartphones and tablets, and likely extending to other small or medium applications, including smartwatches. But even though Samsung did introduce a large OLED TV, it has since withdrawn from TV applications, leaving LG as the primary manufacturer participating in the OLED marketplace. Samsung, not one to cede a category to LG, and still dominating global TV sales, has led with more LCD innovations aimed at narrowing the performance gap with OLED. This includes curved LCD TVs-OLED was originally thought to be the only display that could be curved-and wide-color-gamut LCD TVs through a new technology called quantum dots. Quantum dots enable the LED backlight to produce a wider range of colors that compares very favorably against OLED, at a fraction of the cost of OLED.

There are other new technologies poised to impact the LCD category. At this year"s CES event, Sharp introduced displays based on microelectromechanical systems (MEMS) that use a shutter technology and alternating colors of LED lights that were rapidly refreshed. Such displays have very fast motion response, a greater range of operating temperatures and very high optical efficiency, which reduces power consumption. These attributes could be especially beneficial when battery power is a concern, such as on mobile displays. Given the growth trajectory of smartphones, it"s fair to say that MEMS displays are worth keeping an eye on, as they could well herald the next challenge to LCD"s dominion. For now, however, LCD remains nearly invincible.

A major decrease in manufacturing cost gap between organic light-emitting diode (OLED) display and liquid crystal display (LCD) panel is expected to support the expansion of OLED TVs, according to new analysis from IHS Markit (Nasdaq: INFO), a world leader in critical information, analytics and solutions.

The he OLED Display Cost Modelanalysis estimates that the total manufacturing cost of a 55-inch OLED ultra-high definition (UHD) TV panel — at the larger end for OLED TVs — stood at $582 per unit in the second quarter of 2017, a 55 percent drop from when it was first introduced in the first quarter of 2015. The cost is expected to decline further to $242 by the first quarter of 2021, IHS Markit said.

The manufacturing cost of a 55-inch OLED UHD TV panel has narrowed to 2.5 times that of an LCD TV panel with the same specifications, compared to 4.3 times back in the first quarter of 2015.

“Historically, a new technology takes off when the cost gap between a dominant technology and a new technology gets narrower,” said Jimmy Kim, principal analyst for display materials at IHS Markit. “The narrower gap in the manufacturing cost between the OLED and LCD panel will help the expansion of OLED TVs.”

However, it is not just the material that determines the cost gap. In fact, when the 55-inch UHD OLED TV panel costs were 2.5 times more than LCD TV panel, the gap in the material costs was just 1.7 times. Factors other than direct material costs, such as production yield, utilization rate, depreciation expenses and substrate size, do actually matter, IHS Markit said.

The total manufacturing cost difference will be reduced to 1.8 times from the current 2.5 times, when the yield is increased to a level similar to that of LCD panels. “However, due to the depreciation cost of OLED, there are limitations in cost reduction from just improving yield,” Kim said. “When the depreciation is completed, a 31 percent reduction in cost can be expected from now.”

The OLED Display Cost Model by IHS Markit provides more detailed cost analysis of OLED panels, including details of boards, arrays, luminescent materials, encapsulants and direct materials such as driver ICs. The report also covers overheads such as occupancy rate, selling, general and depreciation costs. In addition, ths report analyzes OLED panels in a wide range of sizes and applications.

For information about purchasing this report, contact the sales department at IHS in Americas at +1 (844) 301-7334 or [email protected]; in Europe, Middle East and Africa (EMEA) at +44 1344 328 300 or [email protected]; or Asia-Pacific (APAC) at +60 4 291 3600 or [email protected].

[Introduction]: This paper analyzes the competitive pattern of the panel display industry from both supply and demand sides. On the supply side, the optimization of the industry competition pattern by accelerating the withdrawal of Samsung’s production capacity is deeply discussed. Demand-side focuses on tracking global sales data and industry inventory changes.

Since April 2020, the display device sector rose 4.81%, ranking 11th in the electronic subsectors, 3.39 percentage points behind the SW electronic sector, 0.65 percentage points ahead of the Shanghai and Shenzhen 300 Index. Of the top two domestic panel display companies, TCL Technology is up 11.35 percent in April and BOE is up 4.85 percent.

Specific to the panel display plate, we still do the analysis from both ends of supply and demand: supply-side: February operating rate is insufficient, especially panel display module segment grain rate is not good, limited capacity to boost the panel display price. Since March, effective progress has been made in the prevention and control of the epidemic in China. Except for some production lines in Wuhan that have been delayed, other domestic panels show that the production lines have returned to normal. In South Korea, Samsung announced recently that it would accelerate its withdrawal from all LCD production lines. This round of output withdrawal exceeded market expectations both in terms of pace and amplitude. We will make a detailed analysis of it in Chapter 2.

Demand-side: We believe that people spend more time at home under the epidemic situation, and TV, as an important facility for family entertainment, has strong demand resilience. In our preliminary report, we have interpreted the pick-up trend of domestic TV market demand in February, which also showed a good performance in March. At present, the online market in China maintains a year-on-year growth of about 30% every week, while the offline market is still weak, but its proportion has been greatly reduced. At present, people are more concerned about the impact of the epidemic overseas. According to the research of Cinda Electronics Industry Chain, in the first week, after Italy was closed down, local TV sales dropped by about 45% from the previous week. In addition, Media Markt, Europe’s largest offline consumer electronics chain, also closed in mid-March, which will affect terminal sales to some extent, and panel display prices will continue to be under pressure in April and May. However, we believe that as the epidemic is brought under control, overseas market demand is expected to return to the pace of China’s recovery.

From a price perspective, the panel shows that prices have risen every month through March since the bottom of December 19 reversed. However, according to AVC’s price bulletin of TV panel display in early April, the price of TV panel display in April will decrease slightly, and the price of 32 “, 39.5 “, 43 “, 50 “and 55” panels will all decrease by 1 USD.65 “panel shows price down $2; The 75 “panel shows the price down by $3.The specific reasons have been described above, along with the domestic panel display production line stalling rate recovery, supply-side capacity release; The epidemic spread rapidly in Europe and the United States, sports events were postponed, local blockades were gradually rolled out, and the demand side declined to a certain extent.

Looking ahead to Q2, we think prices will remain under pressure in May, but prices are expected to pick up in June as Samsung’s capacity is being taken out and the outbreak is under control overseas. At the same time, from the perspective of channel inventory, the current all-channel inventory, including the inventory of all panel display factories, has fallen to a historical low. The industry as a whole has more flexibility to cope with market uncertainties. At the same time, low inventory is also the next epidemic warming panel show price foreshadowing.

In terms of valuation level, due to the low concentration and fierce competition in the panel display industry in the past ten years, the performance of sector companies is cyclical to a certain extent. Therefore, PE, PB, and other methods should be comprehensively adopted for valuation. On the other hand, the domestic panel shows that the leading companies in the past years have sustained large-scale capital investment, high depreciation, and a long period of poor profitability, leading to the inflated TTM PE in the first half of 2014 to 2017. Therefore, we will display the valuation level of the sector mainly through the PB-band analysis panel in this paper.

In 2017, due to the combined impact of panel display price rise and OLED production, the valuation of the plate continued to expand, with the highest PB reaching 2.8 times. Then, with the price falling, the panel shows that PB bottomed out at the end of January 2019 at only 1.11 times. From the end of 2019 to February, the panel shows that rising prices have driven PB all the way up, the peak PB reached 2.23 times. Since entering March, affected by the epidemic, in the short term panel prices under pressure, the valuation of the plate once again fell back to 1.62 times. In April, the epidemic situation in the epidemic country was gradually under control, and the valuation of the sector rebounded to 1.68 times.

We believe the sector is still at the bottom of the stage as Samsung accelerates its exit from LCD capacity and industry inventories remain low. Therefore, once the overseas epidemic is under control and the domestic demand picks up, the panel shows that prices will rise sharply. In addition, the plate will also benefit from Ultra HD drive in the long term. Panel display plate medium – and long-term growth logic is still clear. Coupled with the optimization of the competitive pattern, industry volatility will be greatly weakened. The current plate PB compared to the historical high has sufficient space, optimistic about the plate leading company’s investment value.

Revenue at Innolux and AU Optronics has been sluggish for several months and improved in March. Since the third quarter of 2017, Innolux’s monthly revenue growth has been negative, while AU Optronics has only experienced revenue growth in a very few months.AU Optronics recorded a record low revenue in January and increased in February and March. Innolux’s revenue returned to growth in March after falling to its lowest in recent years in February. However, because the panel display manufacturers in Taiwan have not put in new production capacity for many years, the production process of the existing production line is relatively backward, and the competitiveness is not strong.

On March 31, Samsung Display China officially sent a notice to customers, deciding to terminate the supply of all LCD products by the end of 2020.LGD had earlier announced that it would close its local LCDTV panel display production by the end of this year. In the following, we will analyze the impact of the accelerated introduction of the Korean factory on the supply pattern of the panel display industry from the perspective of the supply side.

The early market on the panel display plate is controversial, mainly worried about the exit of Korean manufacturers, such as LCD display panel price rise, or will slow down the pace of capacity exit as in 17 years. And we believe that this round of LCD panel prices and 2017 prices are essentially different, the LCD production capacity of South Korean manufacturers exit is an established strategy, will not be transferred because of price warming. Investigating the reasons, we believe that there are mainly the following three factors driving:

(1) Under the localization, scale effect, and aggregation effect, the Chinese panel leader has lower cost and stronger profitability than the Japanese and Korean manufacturers. In terms of cost structure, according to IHS data, material cost accounts for 70% of the cost displayed by the LCD panel, while depreciation accounts for 17%, so the material cost has a significant impact on it. At present, the upstream LCD, polarizer, PCB, mold, and key target material line of the mainland panel display manufacturers are fully imported into the domestic, effectively reducing the material cost. In addition, at the beginning of the factory, manufacturers not only consider the upstream glass and polarizer factory but also consider the synergy between the downstream complete machine factory, so as to reduce the labor cost, transportation cost, etc., forming a certain industrial clustering effect. The growing volume of shipments also makes the economies of scale increasingly obvious. In the long run, the profit gap between the South Korean plant and the mainland plant will become even wider.

(2) The 7 and 8 generation production lines of the Korean plant cannot adapt to the increasing demand for TV in average size. Traditionally, the 8 generation line can only cut the 32 “, 46 “, and 60” panel displays. In order to cut the other size panel displays economically and effectively, the panel display factory has made small adjustments to the 8 generation line size, so there are the 8.5, 8.6, 8.6+, and 8.7 generation lines. But from the cutting scheme, 55 inches and above the size of the panel display only part of the generation can support, and the production efficiency is low, hindering the development of large size TV. Driven by the strong demand for large-size TV, the panel display generation line is also constantly breaking through. In 2018, BOE put into operation the world’s first 10.5 generation line, the Hefei B9 plant, with a designed capacity of 120K/ month. The birth of the 10.5 generation line is epoch-making. It solves the cutting problem of large-size panel displays and lays the foundation for the outbreak of large-size TV. From the cutting method, one 10.5 generation line panel display can effectively cut 18 43 inches, 8 65 inches, 6 75 inches panel display, and can be more efficient in hybrid mode cutting, with half of the panel display 65 inches, the other half of the panel display 75 inches, the yield is also guaranteed. Currently, there are a total of five 10.5 generation lines in the world, including two for domestic panel display companies BOE and Huaxing Optoelectronics. Sharp has a 10.5 generation line in Guangzhou, which is mainly used to produce its own TV. Korean manufacturers do not have the 10.5 generation line. In the context of the increasing size of the TV, Korean manufacturers are obviously at a disadvantage in competitiveness.

(3) As the large-size OLED panel display technology has become increasingly mature, Samsung and LGD hope to transfer production to large-size OLED with better profit prospects as soon as possible. Apart from the price factor, the reason why South Korean manufacturers are exiting LCD production is more because the large-size OLED panel display technology is becoming mature, and Samsung and LGD hope to switch to large-size OLED production as soon as possible, which has better profit prospects. At present, there are three major large-scale OLED solutions including WOLED, QD OLED, and printed OLED, while there is only WOLED with a mass production line at present.

According to statistics, shipments of OLED TVs totaled 2.8 million in 2018 and increased to 3.5 million in 2019, up 25 percent year on year. But it accounted for only 1.58% of global shipments. The capacity gap has greatly limited the volume of OLED TV.LG alone consumes about 47% of the world’s OLED TV panel display capacity, thanks to its own capacity. Other manufacturers can only purchase at a high price. According to the industry chain survey, the current price of a 65-inch OLED panel is around $800-900, while the price of the same size LCD panel is currently only $171.There is a significant price difference between the two.

To sum up, we believe that Samsung, LGD, and other South Korean factories are resolute in their capacity to withdrawal from this round and will not be delayed or change their plans due to the impact of subsequent price recovery.

Samsung and LGD began to shut down LCD production lines in Q3 last year, leading to the recovery of the panel display sector. Entering 2020, the two major South Korean plants have announced further capacity withdrawal planning. In the following section, we will focus on its capacity exit plan and compare it with the original plan. It can be seen that the pace and magnitude of Samsung’s exit this round is much higher than the market expectation:

(1) LGD: LGD currently has three large LCD production lines of P7, P8, and P9 in China, with a designed capacity of 230K, 240K, and 90K respectively. At the CES exhibition at the beginning of this year, the company announced that IT would shut down all TV panel display production capacity in South Korea in 2020, mainly P7 and P8 lines, while P9 is not included in the exit plan because IT supplies IT panel display for Apple.

(2) Samsung: At present, Samsung has L8-1, L8-2, and L7-2 large-size LCD production lines in South Korea, with designed production capacities of 200K, 150K, and 160K respectively. At the same time in Suzhou has a 70K capacity of 8 generation line.

Global shipments of TV panel displays totaled 281 million in 2019, down 1.06 percent year on year, according to Insight. In fact, TV panel display shipments have been stable since 2015 at between 250 and 300 million units. At the same time, from the perspective of the structure of sales volume, the period from 2005 to 2010 was the period when the size of China’s TV market grew substantially. Third-world sales also leveled off in 2014. We believe that the sales volume of the TV market has stabilized and there is no big fluctuation. The impact of the epidemic on the overall demand may be more optimistic than the market expectation.

In contrast to the change in volume, we believe that the core driver of the growth in TV panel display demand is actually the increase in TV size. According to the data statistics of Group Intelligence Consulting, the average size of TV panel display in 2014 was 0.47 square meters, equivalent to the size of 41 inches screen. In 2019, the average TV panel size is 0.58 square meters, which is about the size of a 46-inch screen. From 2014 to 2019, the average CAGR of TV panel display size is 4.18%. Meanwhile, the shipment of TV in 2019 also increased compared with that in 2014. Therefore, from 2014 to 2019, the compound growth rate of the total area demand for TV panel displays is 6.37%.

It is assumed that 4K screen and 8K screen will accelerate the penetration and gradually become mainstream products in the next 2-3 years. The pace of screen size increase will accelerate. We have learned through industry chain research that the average size growth rate of TV will increase to 6-8% in 2020. Driven by the growth of the average size, the demand area of global TV panel displays is expected to grow even if TV sales decline, and the upward trend of industry demand remains unchanged.

Meanwhile, the global LCDTV panel display demand will increase significantly in 2021, driven by the recovery of terminal demand and the continued growth of the average TV size. In 2021, the whole year panel display will be in a short supply situation, the mainland panel shows that both males will enjoy the price elasticity.

This paper analyzes the competition pattern of the panel display industry from both supply and demand sides. On the supply side, the optimization of the industry competition pattern by accelerating the withdrawal of Samsung’s production capacity is deeply discussed. Demand-side focuses on tracking global sales data and industry inventory changes. Overall, we believe that the current epidemic has a certain impact on demand, and the panel shows that prices may be under short-term pressure in April or May. But as Samsung’s exit from LCD capacity accelerates, industry inventories remain low. So once the overseas epidemic is contained and domestic demand picks up, the panel suggests prices will surge. We are firmly optimistic about the A-share panel display plate investment value, maintain the industry “optimistic” rating. Suggested attention: BOE A, TCL Technology.

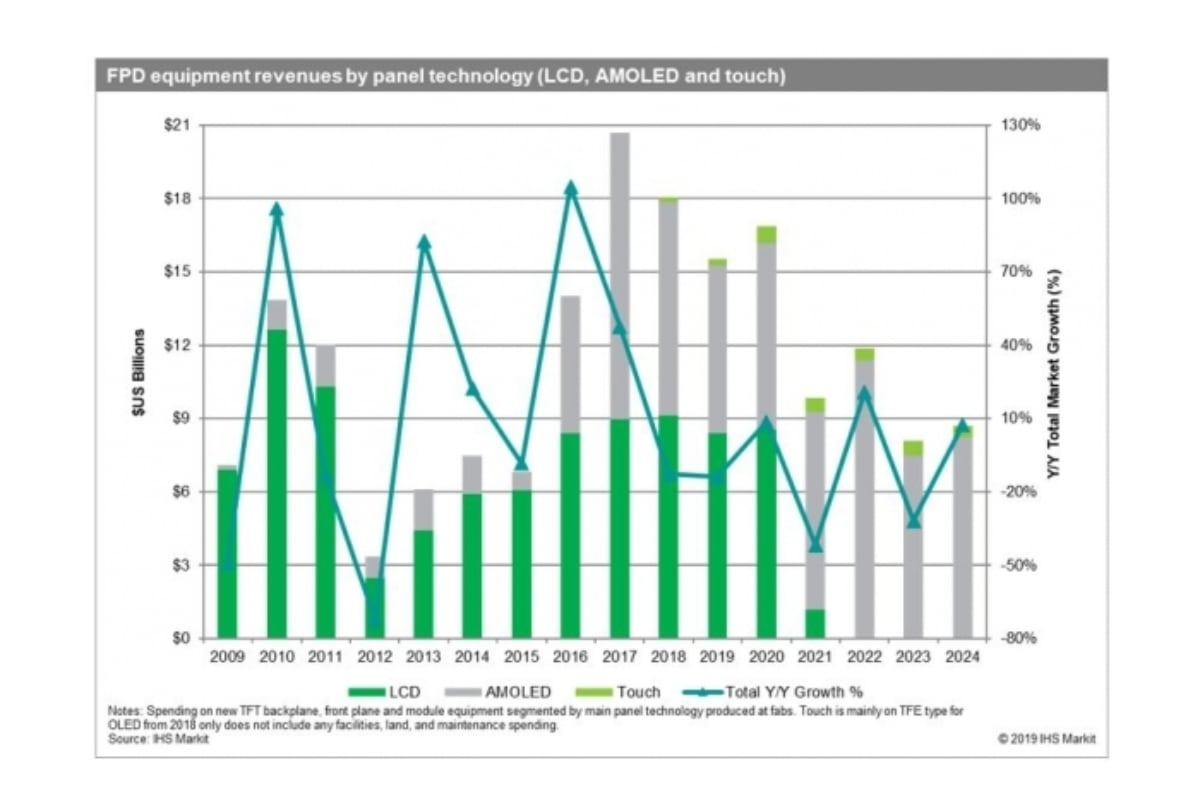

Market research firm IHS Markit says flat panel display sales are expectedto fall from $20.2 billion in 2017 to $14.0 billion in 2020, declining at a compound annual rate of 11.6 percent.

“The expansion of the FPD equipment market that started in 2016 has been driven by the high equipment intensity of new flexible active-matrix organic light-emitting diode (AMOLED) display factories and the scale of Gen 10.5/11 LCD factories,” says Chase Li, senior analyst at IHS Markit. “This expansion has been further fueled by Chinese local governments, which have supported panel makers with various mechanisms such as financing, land grants, reduced taxes, infrastructure and direct subsidies.”

Such broad government support of Chinese FPD fabs for all types of display technologies and factory sizes is starting to distort the supply/demand balance as the new capacity begins to ramp. In the case of flexible AMOLED factories targeting smartphones, many multiple billion-dollar investments and even expansion phases have been moving forward before panel makers have proven their ability to produce high quality panels at high yields and competitive costs.

The glut level of thin-film transistor (TFT) AMOLED panels for mobile applications is forecast to exceed 40 percent of the demand in terms of area in 2019. This implies that, on average, factories for mobile applications are likely to be under-utilized.

This situation has caused both panel makers and China’s local governments to evaluate more critically new flexible AMOLED factory plans. Even South Korean panel makers have pulled back from their previous plans to expand Gen 6 flexible AMOLED capacity continuously due to slower-than-expected panel demand growth. Reduced spending on AMOLED fabs for mobile applications accounts for most of the decline in equipment spending in 2018 and 2019.

Even so, Chinese local governments continue to fund selected projects despite the tightening of credit, particularly for Gen 10.5/11 LCD factories. These projects are predicted to keep equipment spending relatively firm through 2020. However, it threatens to push the large display supply/demand glut level to a record annual high of 18 percent in 2020, unless panel makers reduce excessive LCD TV panel capacity by converting some of it to OLED TV panel production and shutter less productive legacy factories.

High-end OLED TVs are one segment that is still expected to face tight panel supply for the next few years. Although, demand is low compared to standard LCD TVs, OLED TVs are a growing niche, whose panel demand is forecast to rise from 2.9 million units in 2018 to 6.7 million units in 2020. Being the only panel maker to have commercialized OLED TV panels to-date, LG Display is shipping all the panels it fabricates and running its current factories at full utilization.

According to the AMOLED and LCD Supply Demand & Equipment Tracker by IHS Markit, equipment spending in 2019 will be significantly supported by the conversion of legacy LCD fabs to advanced AMOLED factories. JOLED, Samsung Display and others are utilizing previously purchased TFT tools, while adding OLED frontplane, color conversion, cell and module equipment, hoping that they will keep them ahead of rivals and enable them to ride the growth of the AMOLED TV market.

“The FPD equipment market has always been highly volatile depending on market and technology changes. Some slow-down is not surprising following years of record high equipment spending,” Li said. “How all the equipment being installed will affect the future opportunity is a question that equipment makers are now struggling to answer. Based on IHS Markit analysis, the correction will continue beyond 2020. Even so, hope for expanding the new technology investments in AMOLED and quantum-dot (QD) OLED TVs as well as foldable displays, combined with industry restructuring and increased demand as prices fall offers the hope of another positive cycle coming.”

The lowest-priced item that has been used or worn previously.The item may have some signs of cosmetic wear, but is fully operational and functions as intended. This item may be a floor model or store return that has been used.See details for description of any imperfections.

LONDON (June 21, 2018) – Despite better-than-expected first-quarter demand for thin-film transistor liquid-crystal display (TFT-LCD) TV sets and TV panels, market players would be well advised to adopt a more conservative outlook in demand growth for the coming quarters, according to IHS Markit (Nasdaq: INFO), a world leader in critical information, analytics and solutions.

Earlier market expectations assumed that demand would slow in the first quarter prompted by the observation that TV set makers would put a hold on panel purchases based on hopes that panel prices would drop further. Such a view was largely attributed by the development of Chinese panel makers planning aggressive investments over the next two to three years.

As it turned out, panel makers managed to sell more panels than originally forecasted in the first quarter because panel prices declined much faster than expected. According to IHS Markit, TV panel unit shipments increased by 13.3 percent in the first quarter compared to a year ago, while TV set shipments rose 7.9 percent during the same period.

“LCD TV panel shipments are expected to grow faster than the LCD TV set shipments, expanding the accumulated gap between the two even further,” said Ricky Park, director of display research at IHS Markit.

According to the latest Displaylong term demand forecast tracker by IHS Markit, the accumulated gap between LCD TV panel and set shipments in the second and third quarters of 2018 is expected to be higher than past 10 years, reaching 8.3 percent and 8.4 percent, respectively, from 7.9 percent in the first quarter. Furthermore, the gap is expected to remain high until 2019.

“The main reason for the higher gap is the aggressive investment in 10.5 generation fabs. TFT LCD capacity, in terms of area, will soar in the next four years,” Park said. “As capacity is expected to increase more than demand, panel suppliers will likely push to sell panels at lower prices while set makers are to hesitate buying panels expecting the price to drop even further.”

However, when the accumulated gap in panel-set shipments is high, an inventory correction should always follow. “TV makers should narrow the gap for healthy inventory control and reducing panel orders is a step in that direction,” Park said. “If TV set makers’ panel purchasing drops, it will likely cause a cash flow issue to panel suppliers, and they would need to reduce the utilization rate to control the supply.”

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey