lcd panel price ihs made in china

(April 30, 2019) – With Chinese panel makers accelerating the mass production of large thin-film transistor (TFT) liquid crystal display (LCD) TV panels faster than expected, they accounted for 33.9 percent of the 60-inch and larger LCD TV panel shipments in the first quarter of 2019. Their market share has expanded nearly 10 times from 3.6 percent in just over a year, according to business information provider

South Korean panel makers still accounted for the largest share in the 60-inch and larger LCD TV panel shipments, with a 45.1 percent share in the first quarter. However, Chinese panel makers’ share in the large LCD TV panel market is expected to continue to grow.

BOE accounted for 29 percent of the total 60-inch and larger LCD TV panel shipments in the first quarter of 2019. It is estimated that the B9 10.5G fab has reached its maximum capacity of 120,000 sheets in the first quarter of 2019.

ChinaStar also started to mass produce large LCD panels at its T6 10.5G fab in the first quarter. CEC-Panda and CHOT ramped up mass production at their 8.6G fabs to the maximum design capacity in the first quarter. Foxconn/Sharp is forecast to begin mass production at their Guangzhou 10.5G fab in the second half of 2019.

“As both Chinese and South Korean panel suppliers are focusing on large LCD TV panels, competition between them will become more intense, pressuring the price of large LCD TV panels even further throughout 2019,” Wu said.

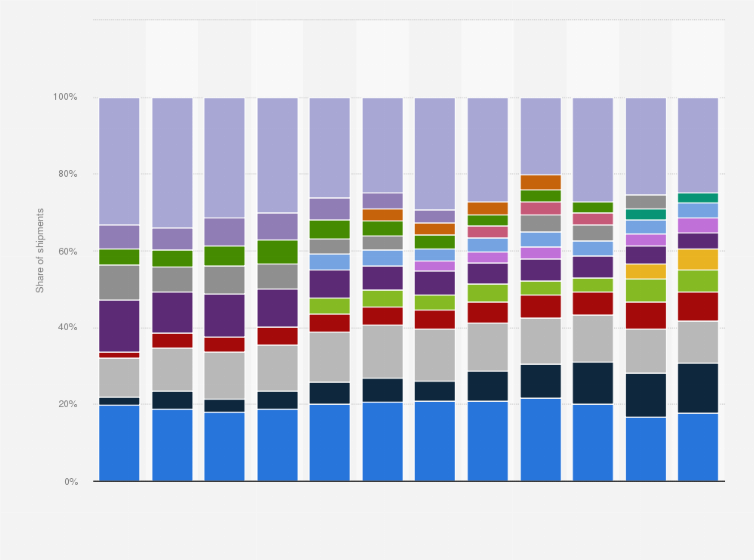

by IHS Markit, shipments of larger than 9-inch TFT-LCD panels reached 178.3 million units in the first quarter of 2019, down 1 percent from a year ago. By area, the shipment increased by 6.7 percent to 49.1 million square meters during the same period.

BOE led the unit shipments of large TFT-LCD panels with a 24.6 percent share in the first quarter of 2019, followed by LG Display (18.8 percent) and Innolux (16 percent). By area shipments, LG Display accounted for the largest share of 20 percent, followed by BOE (19.9 percent) and Samsung Display (14.1 percent).

IHS Markit provides information on the entire range of large display panels shipped worldwide and regionally, including monthly and quarterly revenues and shipments by display area, application, size and aspect ratio of each supplier.

IHS Markit (Nasdaq: INFO) is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers next-generation information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 business and government customers, including 80 percent of the Fortune Global 500 and the world’s leading financial institutions.

IHS Markit is a registered trademark of IHS Markit Ltd. and/or its affiliates. All other company and product names may be trademarks of their respective owners © 2019 IHS Markit Ltd. All rights reserved.

LCD panel makers are at risk of incurring deep losses this year as the rise of Chinese manufacturers aggravates already severe oversupply, IHS Technology said yesterday.

The global supply of LCD panels is expected to increase 6 percent annually this year, outpacing the 3 percent growth in demand, mostly on the back of Chinese panel manufacturers BOE Technology Group (京東方) and China Star Optoelectronics Technology Co (華星光電), the market researcher projected.

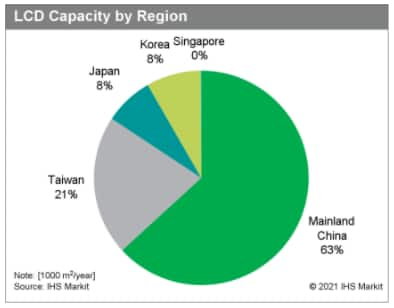

China’s global market share is expected to expand to 23.7 percent this year by capacity from last year’s 19.5 percent, stealing share from Taiwan, IHS Technology said.

“We only see a brief rebound in panel prices in the second quarter and third quarter, primarily due to stock-building demand from major TV brands including Samsung Electronics Co and Chinese TV vendors,” IHS Technology senior director David Hsieh (謝勤益) said at an annual display forum.

Chinese display manufacturers are chasing their South Korean rivals closely by planning to release a larger volume of liquid-crystal panels over 32 inches this year, said a market researcher Sunday.

According to a report on the 2017 shipment strategies of Chinese TV panel makers by IHS Markit, Chinese LCD panel suppliers are forecast to ship out a total of 320,000 large-size panels larger than 32 inches by the end of this year, a 33 percent surge from last year.

In the report, Wu mentioned the plans of major Chinese panel firms such as BOE, CSOT, CEC-Panda and HKC to focus on expanding production of 43, 55 and 58-inch panels, adding that demand for 32-inch panels will gradually decrease.

“By the end of 2018, China will be the largest region for TFT LCD capacity, and larger-sized products may make their factories more efficient and profitable than they have been when producing 32-inch panels,” he said.

“The strategies of Chinese panel makers will significantly influence global supply and demand,” Wu said. “In 2015 and 2016, the Chinese companies shipped 33.2 percent of worldwide LCD TV panel, trailing only Korean panel makers at 36.4 percent.”

The competition structure has been advantageous for the Korean players, since their Chinese rivals had been focusing on small LCD panels until last year. But now the Korean firms are facing fiercer competition in prices.

Although demand for organic-light emitting diode panels in the TV market is gradually rising, dominance of LCD panels is projected to continue for the foreseeable future.

“While OLEDs are expected to post sharp growth, they will not be able to usurp LCD as the panels of choice for upper-end TVs,” another report by IHS Markit said.

At least five LCD display factories at the epicenter of the coronavirus outbreak are suffering production slowdowns, which is turn is expected to have an effect on the supply and pricing of displays used in PCs and LCD TVs.

Five LCD fabs reside in Wuhan, China, which has basically been shut down to prevent the coronavirus from spreading. Informa Tech’s IHS Markit service said Friday that they expect that the capacity utilization for all LCD fabs in China could fall by at least 10 percent and by as much as 20 percent during February.

As a result, LCD panel prices are expected to rise. IHS said that preliminary estimates say that per-panel prices could rise $1 to $2, but could go as high as $3 to $5. That might not sound like much, but manufacturers typically tack on extra profit margins at each stage of production, potentially raising sale prices somewhat higher.

IHS estimates that about 55 percent of all LCD panels in the world will ship from China in 2020, meaning that the Chinese outbreak will have worldwide effects on the supply chain. Five fabs are in Wuhan itself, including two fabs owned by China Star Optoelectronics Technology, two owned by Tianma, and one BOE fab.

“Display facilities in Wuhan currently are dealing with the very real impacts of the coronavirus outbreak,” said David Hsieh, senior director of displays, at IHS Markit technology research, in a statement. “These factories are facing shortages of both labor and key components as a result of mandates designed to limit the contagion’s spread. In the face of these challenges, top display suppliers in China have informed our experts that a near-term production decline is unavoidable.”

IHS reported seeing panic buying, including doublebooking, where a buyer will buy as much as they need from two suppliers just to ensure that they’ll be able to get the supplies they require. Even if the supplies are there, IHS also said that production at several key third-party LCD module suppliers has now ceased, severely impacting panel production throughout the country.Besides the slowdown in production at fabs that are already operating, IHS said that it expects new fabs to not come on line as quickly as expected.

All this is expected to have a direct effect on LCD panel pricing, and possibly ripple effects through laptop manufacturing as well. It’s worth noting that while Intel and AMD did not cite coronavirus effects among their forecasts, Microsoft did, with a broader than usual forecast for the second half of the year.

Beginning next year, Chinese display makers will start the full-fledged operation of large-sized tenth-generation or later liquid crystal display (LCD) panel factories. As a result, some experts say that an increase in global flat panel display production capacity may extend the current LCD oversupply period.

According to market researcher IHS Markit on December 7, China"s large display makers such as BOE which is the largest display manufacturer of China, China Star (CSOT) and Foxconn, will put seven 10-generation LCD factories to work one by one from next year to 2020.

As a result, IHS Markit predicts that global LCD panel supply growth will reach 59% per annum on average over the next five years to 2022. The proportion of 10G or later LCD panel production will also climb from 4% this year to 26% in 2020, according to IHS Markit. Purchases of flat panel display production equipment are also expected to exceed US$ 20 billion next year.

It is forecast that the LCD oversupply which began at the end of 2015 is expected to continue for at least five years. The price of a 55-inch LCD panel which rose above US$ 228 in 2015 dropped to US$ 200 in 2016 and then sank to US$ 180 in December of this year, according to market research firm WitsView.

As LCD panel prices have tumbled due to increased supply, the premium TV market is also moving rapidly towards large-screen models. Display panel manufacturers are competing to build a 10.5th-generation plant optimized for 65-inch and 75-inch displays. As 8th-generation and 8.6th-generation plants which account for the majority of large-area LCD production lines are optimized to produce 55-inch and 58-inch panels, respectively, they are less efficient at producing larger LCD panels.

BOE started the full-scale operation of its 8.5th-generation production line this year, and will start running its 10th-generation plant in the first half of next year. China Star (CSOT) and CEC-Panda are also in the process of building large LCD production lines. In the third quarter, BOE of China dethroned LG Display which has been at the top spot for 31 consecutive quarters while ranking first with a market share of 21.7% (based on shipment) in the 9-inch or larger display panel market.

Currently, LG Display is enjoying 90% of its total sales in the LCD sector and making its profit structure centered on the large organic light emitting diode (OLED) business. However, the company already missed investment timing for nearly half a year such as a delay in investment in the establishment of an 8G OLED factory in Guangzhou in China. Thus, a lot of attention is being paid to how LG Display will tackle this matter.

“As 10.5th-generation plants will be put into full operation, prices of 65-inch or larger panels will slide more than 5% each year, while demand will increase 2.5-fold to 40 million units per year,” an industry observer said. “65-inch or larger TVs will become the mainstream in the future.”

According to media reports out of Asia, buyers of large lots of 32-inch open-cell LCD panels – mostly destined for television production – are paying around $54-$59 per panel. In some cases, even lower prices are available. This price is about 40% lower than the price of that panel one year ago.

One report noted that in just the first quarter of 2016, the price of a 42-inch LCD panel is now $115, fully 8% lower than at the end of December. The same situation exists in the PC market as well. One report noted that the price of a 15.6-inch LCD display, destined for a notebook PC, is now only $25.50 down 10% since the end of December.

While dropping panel prices can be good news for consumers, who are finding great deals on televisions and computers around the world – it is terrible news for the industry, as profits get pressured…or eliminated altogether. Most markets are reporting dramatic drops in television pricing – even on the step-up 4K Ultra HD televisions – on which many brands hoped to realize more profit on this latest video technology.

Although the LCD panel industry had expected an increase in 2016, it now appears that the best they can hope for us flat shipments. And even that dismal estimate may be optimistic. Industry insiders are now forecasting sales of 224 million panels globally – about the same level as 2015.

The global economic slowdown has caused a dramatic drop-off in television sales. Most manufacturers had targeted increased panel sales in developing markets. But as it has turned out, sales declines globally have offset whatever gains they’ve been able to make in these newer markets.

A report by the Nikkei points out that China’s BOE Technology Group, as well as other Chinese LCD panel makers, are ramping up production in this environment and are guilty of fueling a price war. IHS, a U.S. market research company, estimates that production capacity for panels 9.1-inches or larger will exceed demand by 14% this year. This amount is well beyond a more normal rate of 10% or less.

The global display market is fluctuating due to side-effects from the novel coronavirus. As Chinese Government has been controlling traffics and extended Chinese New Year holiday in order to prevent the spread of the virus and cross-contamination, it is expected that operation rates and productivities of major display panel makers that have set up their production lines in China will start to decline sharply.

South Korea’s display industry is paying close attention to the LCD panel market’s situation. As Chinese companies that had aggressively gone after South Korean companies while having subsidies from Chinese Government on their back have slowed down a bit, this will give time to South Korean companies to restructure their strategies on management. Fact that the LCD panel prices are going up due to the reduction of outputs of LCD panels stemming from decreased operation rates of fabs is an unexpected favorable factor for South Korea’s display industry.

A market research company called IHS Market predicted through its recent report that there would be a lack of supplies of display panels and increased selling prices as the recent novel coronavirus situation affects the production of display panels within China. It predicted that operation rates of LCD fabs of major Chinese panel makers would be reduced by anywhere between 10% and 20% in February.

“It is expected that China will be responsible for 55% of global production of LCD panels this year.” said IHS Market. “However, reduced production by Chinese makers will lead to a rise in the LCD TV panel prices.”

“Based on active policies on the LCD panel prices by LCD panel suppliers, there is a chance that the increase in the LCD panel price can be anywhere between $3 and $5 when it was expected to be between $1 and $2.” said IHS Market. “There is a chance that laptop and monitor makers face a lack of inventories of panels.”

Another market research company called WitsView put out a result that said the LCD panel price in February is 1% higher than the LCD panel price in last February. Unlike 2019 where the LCD panel prices had continued to go down, they have been on an upward trend in the first two months of 2020. Considering the fact that an adjustment of the selling price of LCD panel due to the novel coronavirus was not applied to WitsView’s prediction, there is a chance that increase rates are much higher.

South Korea is also expecting an increase in the selling price of LCD panel. KB Securities expects that the selling price will rebound as the supply amount of LCD panels will be reduced by 20% globally in the first half of this year due to side-effects from the novel coronavirus. KB Securities made its prediction based on a possibility that BOE, which is the world’s biggest LCD maker, can face a setback to its production of Gen 10.5 LCD panels.

KB Securities believes that it will be inevitable that BOE’s fabs will be shut down due to a setback in supplies of raw materials stemming from Chinese Government’s containment of Wuhan. As a result, it expects that LCD panel makers will actively increase their prices in the near future.

Also, South Korea’s display industry expects that it will soon enjoy unexpected benefits resulting from a global increase in the LCD prices. It also expects that profitability in OLED panels will be improved as the difference in the OLED TV panel prices and the LCD panel price becomes narrower.

“Setback to supplies of small to medium OLED panels by CSOT and Tianma that have their plants set up in Wuhan will prepare an opportunity for LG Display’s performance in its small to medium OLED panels that are all produced domestically.” said Kim Dong-won who is a researcher from KB Securities.

The industry believes that side-effects from the coronavirus situation will continue for few months as some employees have yet to report to their workplaces after Chinese New Year holiday just like previous years and as it is unclear when operation rates of plants will start to recover. It is expected that these factors will lead to an upward trend in the selling price of LCD for a while.

Display fabs that are located in Wuhan have taken the most blows to their businesses. Some of these fabs are owned by CSOT (LTPS LCD fab, Gen 6 OLED fab), Tianma (Gen 4.5 LTPS fab, Gen 6 OLED fab), and BOE (Gen 10.5 LCD fab).

It is likely that fabs operated by South Korean companies that are located in China will also take a hit to their businesses. LG Display currently operates a LCD panel fab in Guangzhou and it has started operating its fab in Nanjing, which had been stopped for a short period of time due to a recommendation from Nanjing Government, since the 10th. On the same day, Samsung Electronics and LG Electronics restarted their fabs in Suzhou and Hangzhou respectively.

The LCD, or liquid-crystal display, is the king of the display industry-dominating all major product segments from televisions, to computers, to smartphones and tablets. But having reached maturity after decades of development, and continuing to face challenges from rival technologies, is LCD in danger of losing its market hegemony?

LCD primarily dominated the small-sized markets up until the late 1990s when massive investment in large-scale production using larger-sized factories, or fabs as they are commonly referred to, made it possible to produce big sizes at dramatically lower costs. This initiated a massive change in many market segments, such as TVs and desktop monitors, as well as enabling new product segments to emerge, grow and mature, like notebook PCs, smartphones and tablets. With LCD dominating the display landscape today, new challengers have emerged in recent years with the potential to disrupt the comfortable position that LCD enjoys today.

Early in the history of the flat-panel TV market, plasma TVs became synonymous with a flat-panel TV since it was the only flat display technology available in the larger sizes traditionally associated with TVs. This was especially true at the higher price points the TVs commanded. Can anyone remember the sub-HD 42" plasma TV from Philips for sale at $10,000 around the year 2000? As investment levels rose for new and more advanced production capacity in LCDs, far outpacing that for competing display technologies like plasma, LCD TVs started to capture market share at ever-larger screen sizes while enjoying faster cost reduction.

By 2014, LCD accounted for more than 95 percent share among TV shipments worldwide, leaving just a handful of plasma TV sets and bulky cathode-ray-tube (CRT) televisions still being shipped today. IHS expects both CRT and plasma shipments to end as soon as their production base shuts down. Meanwhile, new display technologies like organic light-emitting diode (OLED) have yet to make a significant impact on the TV market. Similarly, in the desktop monitor space, LCD rapidly replaced CRT as the display technology of choice, although there was never another flat-panel display technology to compete with.

The interesting thing about LCD is that it has succeeded so well despite being a deficient technology in many ways compared to the alternatives. Plasma, a self-emissive technology like CRT, produces more accurate colors, better contrast and greater motion performance than LCD. However, when asked what matters most when choosing a good TV, a majority of consumers claim picture quality trumps all other attributes. So why has LCD come to dominate the TV market?

To be sure, LCD has employed more technological innovation than competing display technologies in order to compensate for its performance deficiencies. In fact, most of the major new feature introductions in the display industry center on advancing LCD performance. Such innovations include higher frame rates to overcome motion blurring, LED backlights with local dimming to enhance contrast and reduce energy consumption, and quantum dots to improve color. Furthermore, because LCD is not a self-emissive technology, it can achieve greater pixel density and higher resolutions than both plasma and OLED in some cases. Each of these incremental improvements has eroded the performance advantages plasma makers had been touting for years.

Even so, many enthusiasts in both the professional industry and consumer marketplace still prefer the picture quality of plasma to LCD. Two reasons why all major suppliers and manufacturers in the plasma industry ended production and threw their support behind LCD were scale and economics.

During much of the 2000s, there were more than two dozen LCD panel manufacturers. In contrast, the number of plasma makers never exceeded half a dozen. Moreover, the level of manufacturing investment in plasma panel production couldn"t come close to the outlays made by LCD panel makers. Why?

The success of any core technology, including displays, depends on the success of the end-market customers, in this case the brands that sell these products to consumers. In 2005, shipments from the top 10 plasma TV brands accounted for just 2.7 percent of total TV market shipment volume. By comparison, the top 10 brands within the LCD TV category during the same year accounted for over 8.4 percent of total TV market shipment volume. At that time, CRT was still the No. 1 display technology, even though LCD was growing much faster than plasma and enjoyed a broader group of successful brands promoting the technology.

Fast forward to 2010, the pivotal year that plasma TV share peaked and began to decline, and the LCD bandwagon momentum became impossible to overcome. Plasma brands began to exit the category, consolidate, or retreat into large-sized niches where LCD couldn"t yet compete on price as effectively. However, investment continued in larger-sized fabs for LCDs, and IHS forecasts that 2015 will see the final shipments of plasma TVs worldwide. In most cases, the plasma TV suppliers also had significant LCD production bases or were working on new OLED display technology, and the suppliers chose to reallocate their resources away from plasma in the wake of the inevitable outcome.

Not only can the support of brands within a category lead a display technology to succeed or fail, but the support of application category can also contribute to economies of scale. In particular, the PC and information technology (IT) categories have been instrumental in the success of LCD. And unlike plasma, the growth of these other IT-related categories occurred earlier and with broader applications beyond TV.

Since 2005, aggressive capacity expansions in LCD factories have reconfigured the competition in flat-panel displays, according to David Hsieh, senior director of displays at IHS. The assertive supply-side expansion comes from panel makers, with the display supply chain gaining good resources from the well-established PC/IT market, especially for desktop monitors and notebook PCs, and then subsequently for tablet PCs. As a result, panel makers have gained great growth and financial reward from the PC market since the start of the new millennium, Hsieh noted, at the same time that process technology improvement and supply-chain growth have improved the capability of panel makers to build bigger glass-substrate fabs for enhanced LCD production efficiency.

Investment continues today in expanding LCD production and competitiveness. While TVs account for most of the revenue from LCD panel production, newer applications like smartphones are playing a greater role in industry profit and revenue growth.

For LCD panel manufacturers, investments in LCD are ongoing to grow both LCD supply capacity and factory size as manufacturers strive to compete and expand incrementally into larger screen-size categories. The investment in capacity and production technology has flowed in waves from Japan to South Korea to Taiwan and now to China, lowering the cost of production at each stage. This progressive East-to-West migration of the supply chain for LCD has allowed all end markets to benefit from lower costs, further spurring the replacement by LCD of the older CRT installed base.

Investment in LCD is substantial, and despite the market"s ups and downs fueled by a phenomenon known as the Crystal Cycle, average annual investment is in the $5 billion range. The Crystal Cycle describes the cyclicality driving the LCD industry. Starting from the initial investment, a glut in supply results that creates a drop in panel prices, which fuels end-market growth as retail prices fall. The end-market growth then uses up industry capacity, creating a shortage of panels that drives commoditized panel prices higher, boosting panel-maker profits. This, in turn, creates capital used to fund the next wave of investment. And although global events can have a major impact, IHS has seen the LCD industry"s resiliency in bouncing back by breaking into new categories or defeating other display technologies.

In tracking the investment made in equipment used to produce displays, the results show that LCD dominates, even if a considerable investment in OLED-a newcomer display technology hoping to take a larger part of the display market-has been growing as well.

Although LCD is the dominant display technology today, new technologies are constantly being introduced with an eye to possibly dislodging it from its lofty perch. One relatively recent newcomer is OLED, a self-emissive display technology like plasma in that it produces light directly from each cell. This is in contrast to LCD, which uses a backlight to produce light, then shutters that light through a color filter. Producing the light directly within the cell has many benefits, especially in contrast and efficiency, as well as making the display thinner and lighter. And although judgments are subjective, OLED is regarded by many as trumping all other display technologies-even plasma-in terms of pure picture performance.

Potentially, OLED could be less expensive to manufacture than LCD because of the simpler bill of materials and less complicated production process. While LCD is a very mature technology and enjoys production yields of more than 90 percent, OLED has had to overcome challenges with both manufacturing processes and materials that lead to a much lower effective yield. Yield is measured by looking at total glass input area minus unusable waste, either in the form of discarded materials from the process or in flawed panels. In the case of OLED, this has been a huge challenge.

A simpler structure enables OLED to be thinner, lighter and more efficient than LCD, but the process cost is still three to four times higher than for LCD because less equipment is being developed, with the OLED process also still not as mature as LCD. Nonetheless, the yield rate-which is the biggest challenge for OLED--could also be the biggest threat to LCD. If OLED can be produced with yield rates similar to LCD, then the gap in cost between OLED and LCD will narrow, with OLED a much better form factor and possessing higher color performance than LCD.

The problem with making OLED displays is much greater at higher resolutions, such as 4K-also called UHD-because the flaw rate is compounded by the greater pixel density. Thus far, OLED manufacturers have been doing a good job of improving the yield on smaller displays. Samsung has introduced OLEDs in a range of smartphones and tablets, and likely extending to other small or medium applications, including smartwatches. But even though Samsung did introduce a large OLED TV, it has since withdrawn from TV applications, leaving LG as the primary manufacturer participating in the OLED marketplace. Samsung, not one to cede a category to LG, and still dominating global TV sales, has led with more LCD innovations aimed at narrowing the performance gap with OLED. This includes curved LCD TVs-OLED was originally thought to be the only display that could be curved-and wide-color-gamut LCD TVs through a new technology called quantum dots. Quantum dots enable the LED backlight to produce a wider range of colors that compares very favorably against OLED, at a fraction of the cost of OLED.

There are other new technologies poised to impact the LCD category. At this year"s CES event, Sharp introduced displays based on microelectromechanical systems (MEMS) that use a shutter technology and alternating colors of LED lights that were rapidly refreshed. Such displays have very fast motion response, a greater range of operating temperatures and very high optical efficiency, which reduces power consumption. These attributes could be especially beneficial when battery power is a concern, such as on mobile displays. Given the growth trajectory of smartphones, it"s fair to say that MEMS displays are worth keeping an eye on, as they could well herald the next challenge to LCD"s dominion. For now, however, LCD remains nearly invincible.

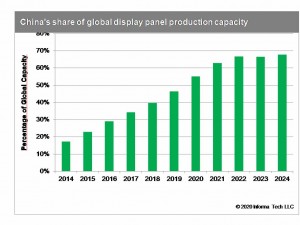

KYOTO, Japan (November 5, 2015) - While conventional thin film transistor liquid crystal (TFT LCD) displays are rapidly trending towards commoditization and currently suffering from declining prices and margins, China is quickly adding capacity in all flat-panel display (FPD) manufacturing segments. Supported by financial incentives from local governments, Chinese TFT capacity is projected to grow 40 percent per year between 2010 and 2018. In 2010 China accounted for just 4 percent of total TFT capacity. However by 2018, China is forecast to become the largest FPD-producing region in the world, accounting for 35 percent of the global market, according to IHS Inc. (NYSE: IHS), the leading global source of critical information and insight.

While Chinese capacity expands, Japan, South Korea and Taiwan have restricted investments to focus mainly on advanced technologies. TFT capacity for flat panel display (FPD) production in these countries is forecast to grow on average at less than 2 percent per year between 2010 and 2018.

Based on the latest IHS Display Supply Demand & Equipment Tracker, BOE Technology Group stands out as the leading producer of FPDs in China. With a capacity growth rate of 44 percent per year between 2010 and 2018, BOE will become the main driver for Chinese share gains. By 2018, the company will have ramped up more FPD capacity than any other producers, except for LG Display and Samsung Display.

In China the central government has generally encouraged investment in FPDs, in order to shift the economy to higher technology manufacturing, to increase domestic supply and to support gross domestic product (GDP) growth. Provincial governments have become the main enabler of capacity expansion through product and technology subsidies, joint ventures and other direct investments, by providing land and facilities and through tax incentives. In return, new FPD fabs increase tax revenue, support land value appreciation, increase employment and spur the local economy. The economic benefits generated from the feedback loop between local governments, panel makers and new FPD factories are still considered sufficiently positive in China to warrant application of significant public resources.

"China currently produces only about a third of the FPD panels it consumes. However, by rapidly expanding capacity, panel makers and government officials are expecting to double domestic production rates in the next few years and are also looking to export markets," Annis said. "How excessive global supply, falling prices and lower profitability will affect these plans over time is not yet exactly clear. Even so, there is now so much new capacity in the pipeline that China will almost certainly become the top producer of FPDs by 2018."

Until about a year ago, active-matrix organic light-emitting diode (AMOLED)–based smartphones remained Samsung’s niche. Almost all the AMOLEDs Samsung was making went into Galaxy products. AMOLED prices were relatively high compared to equivalent liquid crystal displays (LCDs). Samsung’s AMOLED fab utilization was low, and it was struggling to ramp up its A3 flexible AMOLED dedicated fab. Its AMOLED business was challenged to raise profits.

What a difference a year makes! Now in June 2016, the outlook for AMOLED smartphones has dramatically shifted in a positive direction. Samsung’s AMOLED fab utilization is high, prices for external customers are on par with LCDs, and the company’s AMOLED business is profitable. Over the same period, it has become evident that Apple plans to transition the iPhone display from rigid LCDs to flexible AMOLEDs in the next couple of years. Meanwhile, more and more people are talking about the coming flexible or foldable OLED displays that will bring revolutionary change to the form factor of handheld devices.

These shifts in market outlook have created an unprecedented wave of new flexible AMOLED fab investment plans for makers in Korea, China, and Japan. Competitors are trying to replicate Samsung’s success, hoping to escape the commoditization and low profitability of LCDs—and chasing after potential Apple business. A large number of new fabs are now being built, and they are the most expensive ever made relative to glass size and input capacity.

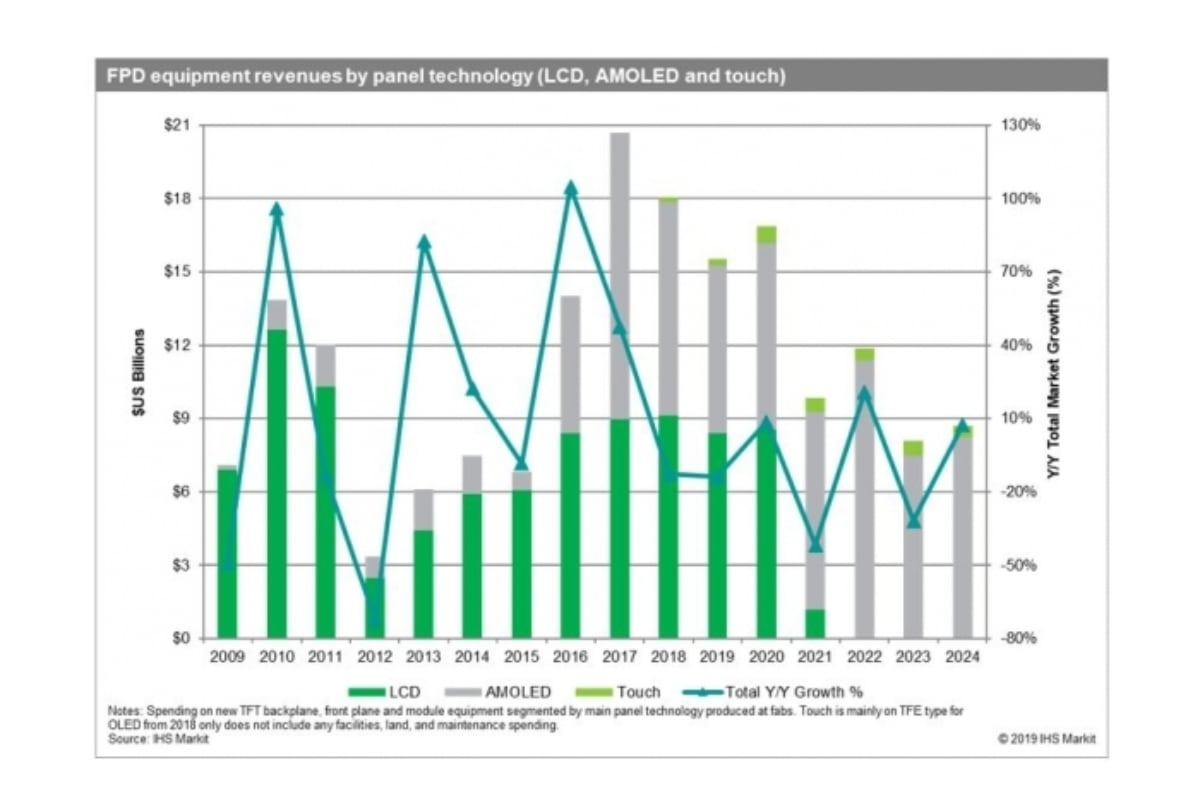

Although Samsung’s AMOLED process to date has used a simplified p-channel metal-oxide-semiconductor (PMOS) thin-film transistor (TFT) for the back plane, other makers and new lines targeting Apple demand appear to be preparing for processes that use up to 50% more mask steps. Low temperature polysilicon and oxide (LTPO) is one of the candidates. This drives significantly more TFT equipment, automation, and other spending. Furthermore, all the new AMOLED fabs will be designed to produce flexible AMOLEDs or will be hybrid rigid/flexible lines. Flexible capability adds costs to the TFT backplane process by requiring flexible substrate coating, curing, and encapsulation steps. Flexible capability adds cost to the front plane process by requiring thin-film encapsulation (TFE), laser lift-off (LLO), and a variety of other steps necessary to handle flexible panels. As shown below, the new flexible AMOLED fabs for mobile display production have a total costs that is almost 1.4x higher than previous rigid AMOLED lines, according to the IHS Technology Display Supply Demand & Equipment Tracker report.

In other words, pushed by a complex TFT process and flexible display requirements, the new AMOLED fabs are the most expensive flat-panel display (FPD) factories ever built, nearly 1.4x that of previously constructed rigid AMOLED lines.

Capital equipment markets tend to be highly cyclical, but the high cost of flexible AMOLED fabs is pushing the equipment market in 2016 and 2017 to near-historic two-year highs. Some concerns have been raised that equipment supply bottlenecks will restrict panel makers’ ability to build fabs according to schedule. Most of these concerns have focused on high-resolution photolithography machines, RGB evaporators, and some high-performance vacuum tools.

However, presented with the best business opportunity since 2010 and 2011, equipment makers are rapidly adding capacity as well as actively managing their suppliers and scheduling in order to meet customer requests. Although any unexpected supply chain disruption could delay some fab plans, it now appears that most of the new fabs will be built out in line with panel makers’ target schedules.

According to the IHS Technology Display Supply Demand & Equipment Tracker report, the large number of new flexible AMOLED investments, along with the high costs of these lines, is pushing the FPD equipment market to near-record two-year highs of $12.6 billion in 2016 and $12.3 billion in 2017.

Forecasting the supply and demand of flexible AMOLEDs in 2018 is a challenging task, not only due to the assumptions that must be made about both capacity and demand, but also the questions about yield rates, how long it will take fabs to ramp and begin commercial production, and the price competitiveness of these new fabs. Building rational forecasts of capacity is possible based on panel maker plans because new factories have lead times of up to two years.

In order to test supply and demand under the more optimistic scenario of faster adoption by Apple, the IHS forecast for total AMOLED smartphones was increased to 503 million units in 2017 and 653 million in 2018. This includes Samsung Galaxy phones, other brands such as Chinese cell phone makers, and a reasonable adoption forecast for Apple. Other mobile applications are also counted in demand. Relatively long ramp-up times and low yield rates for all makers, except Samsung, were assumed. Prices were presumed to be competitive and not directly tested in this analysis.

Analyzing all panel makers’ capacity plans and the comparatively aggressive demand forecast, the glut level is projected to increase from 2016 through 2018, suggesting a trend of growing oversupply.

Samsung’s strategy likely involves adding enough capacity to enable it to continue—for as long as possible and almost exclusively—to dominate the AMOLED market for mobile applications. Samsung Display has a substantial technology and cost lead over even its closest competitors. It controls much of its own process know-how, and it will be a difficult path for followers to catch up in the near- or even mid-term. According to our analysis, Samsung could potentially maintain its AMOLED monopoly through 2018 or longer, even when taking into consideration the large increase in demand as the iPhone transitions from LCD to AMOLED.

The shift from rigid LCD to flexible AMOLED is the most significant change in FPD process technology since the start of the LCD era almost 20 years ago. All panel makers are now scrambling to avoid being left behind during this technology revolution.

However, as supply/demand analysis suggests, all the capacity being added by new AMOLED players may well get ahead of how much the market can absorb. Demand could grow faster than the accelerated forecast; however, it is not clear by how much. In 2018 and 2019 the market for both rigid and flexible AMOLED may be restricted by prices. It is unlikely that many makers will be able to compete on price and performance with Samsung or even with low-cost, high-end LCDs without incurring financial losses.

In the long run, all the investment in AMOLED capacity will help reduce material prices, strengthen the equipment supply chain, and allow the market to trend towards balance. However, it would also not be surprising for new AMOLED entrants to struggle to ramp up new fabs in 2018 and 2019, and suffer from low utilization and profitability as the industry works through the currently forecast flexible AMOLED supply glut.

Prices on LCD TVs in certain screen sizes could come down more noticeably this year as open cell panel suppliers, primarily in China and South Korea, continue to adjust down production volumes amidst building inventory rather than give in to pressure from TV makers to drop prices too close to cost.

David Hsieh, senior director of display research for IHS, said major LCD open cell panel producers from China, and to a lesser degree South Korea, are seeing pressure to reduce prices, and will need to reduce capacity utilization through the second quarter of 2018.

For perspective, global television sales were soft through much of 2017 due to panel shortages in certain screen sizes, which kept prices on finished TVs stable much of the year, presenting less opportunity for aggressive price promotion.

Hsieh said Korean panel makers expect more panel price pressure in the fourth quarter of 2018 due to new capacity coming online from BOE’s 10.5 Gen fab (producing mainly 65-inch 4K panels), the end of the traditional sports season in most parts of the world, and TV makers adjusting inventories and capacity utilization after comparatively stable panel prices in the second and third quarters.

Hsieh warned that continuous oversupply conditions are likely in those periods, where panel makers did not reduce capacity utilization. As a result, high inventory is present in open cell panel screen sizes of 40, 50, 60, 70, and 65 inches. This is intensifying pressure from TV makers to reduce open cell prices, particularly during the spring.

An open cell panel, is the part of an LCD minus the backlight. Due to the price of finished LCD TVs declining as at a faster rate than the of the panels alone, the industry in recent years has turned more and more to producing open cell panels to reduce the cost to TV makers, and to enable thinner panel depths.

“Some TV makers still expect panel prices to fall below last cycle’s low,” Hsieh wrote. “Panel makers cannot agree to these prices now or in the near-term.”

Meanwhile, TV makers, particularly in China, are feeling pressure to lower prices as a result of slower demand for TVs contributing to larger inventories in the first quarter of 2018.

“TV makers are holding enough inventory to get better bargains from panel suppliers, but some are bluffing to get price concessions,” Hsieh revealed. “Some TV makers may resume panel purchasing or inventory additions when they sense panel prices are at a low.”

Hsieh said TV panel demand is not bad for Korean panel makers. “LG Display expects TV panel demand to continue at 4.2 4.3 million per month in Q2, and Samsung Display expects it to be over 2.0 million per month in that quarter. The issue for Korean panel makers is not demand; it is that panel prices will inevitably fall due to market trends and special promotions from some Chinese and Taiwanese panel makers.”

The supply of driver IC is forecast to tighten throughout 2018, estimated to exceed demand by 4 percent, according to the new Display Driver IC Market Tracker by IHS Markit. Foundries have cut their production capacity of cheap driver ICs while increasing production of high-profit ICs and large-scale integrations (LSIs), mainly to satisfy orders from industries producing Internet of Things (IoT) and automotive technologies.

In addition, large panel driver ICs are mainly produced using 8-inch wafers but no foundries are making further investments into these wafer sizes as a generational transition is making its way into 12-inch wafers. “It seems that panel makers can secure driver IC supplies only by offering higher prices,” said Tadashi Uno, senior analyst at IHS Markit.

The average driver IC price increased by about 10 percent during the first half of 2018. Tight supply of driver ICs has impacted the prices of IT panels, such as desktop monitors, notebook PC and tablet PC panels, and has also extended into TV and smartphone panel prices since the third quarter of 2018.

Glass substrates are also in a tight supply situation since the beginning of third quarter2018, according to the Display Glass Market Tracker by IHS Markit. The supply-demand glut in the third quarter has been below 5 percent, which is considered a tight supply threshold, while taking into account later delivery times.

“Major glass makers are investing in glass-melting tanks in China, but the higher glass consumption of Chinese panel makers’ means it exceeds more than double the glass production capacity of the country,” Uno said. “Chinese panel makers also import products from Japan, South Korea and Taiwan but they are stymied by glass production delays and delivery.”

According to the Display Optical Film Market Tracker by IHS Markit, polarizers have been in a tight supply situation since the third quarter. In July, film makers, such as Dai Nippon Printing and Nitto Denko, stopped operations for more than a week due to heavy rain in Japan. The production facilities are not damaged directly, but damaged infrastructures, such as roads, waterworks and electric facilities, have caused delivery delays.

Logistics issues remain even though operations have resumed. “Non-TAC polarizers, especially acryl polarizers, were already in tight supply but the recent floods have made the situation worse,” said Irene Heo, senior principal analyst at IHS Markit. Polarizer supply-demand glut is expected to be 4 percent in the third quarter, below the 5 percent balance bar.

“The main reason for the slow cost reduction is the increasing price of driver ICs,” Uno said. “However, glass substrate and polarizer price reductions have been relatively stable.”

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey