credit card with lcd display quotation

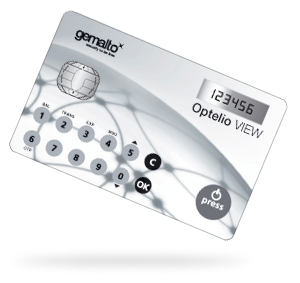

Nov. 6, 2012: The MasterCard Display Card, manufactured by NagraID Security, looks and functions almost exactly like a regular credit card but features an embedded LCD screen and touch-sensitive buttons. (MasterCard)

MasterCard has introduced a new high-tech credit card -- -- one that looks and functions almost exactly like an ordinary card, save for the integrated display and numerical keypad. The screen looks and acts like the display on a calculator; it should boost security by allowing the cardholder to generate single use numerical passwords for authentication.

“Instead of sending customers another bulky token, could we replace something which already exists in the customer’s wallet?” asked V. Subba, regional head of retail banking products for Standard Chartered Bank. “That was when credit, debit and ATM cards, immediately came to mind.”

Banks looking to boost security for online banking use a separate authentication token or device, the company noted. A Display Card could do both -- and in the future it could incorporate additional functionalities and be able to indicate other real time information such as available credit balance, loyalty or reward points, recent transactions and so on.

“With the continued growth in online and now mobile initiated remote payments, consumers are naturally demanding increased security,” explained Matthew Driver, a regional president for MasterCard.

Pity the poor credit card. In these days of smartphones, tablets, and sharks with frickin" laser beams attached to their heads, they just seem so retro.

But they"re getting a makeover. In Singapore, MasterCard has unveiled a credit card to be released in January 2013 that includes "an embedded LCD display and touch-sensitive buttons," the company said this week. Eventually, this card might use its display to show "real time information such as available credit balance, loyalty or reward points, recent transactions, and other interactive information." But for now, the technology will be used to generate one-time passwords as an extra security measure.

"The MasterCard Display Card, manufactured by NagraID Security, looks and functions almost exactly like a regular credit, debit or ATM card, but features an embedded LCD display and touch-sensitive buttons which allow a cardholder to generate a One-Time Password (OTP) as an authentication security measure," MasterCard said. "From January 2013 onwards, all Standard Chartered Online Banking or Breeze Mobile Banking users will use the Standard Chartered security token card as a new personal security device for higher-risk transactions such as payments or transfers above a certain amount, adding third party payees, or changing personal details." Advertisement

The idea isn"t a new one. It"s not even MasterCard"s first attempt. The company actually unveiled very similar cards in June 2010 for use in Turkey, and they have been rolled out to other countries such as Romania. Visa launched almost identical cards in Europe last year, and a company called Dynamics showed off some newfangled credit cards with displays at this year"s Consumer Electronics Show. MasterCard touts the cards as a way to demand extra tokens from customers without making credit cards a hassle to use.

Stealing and using credit card data is far too easy, so adding two-factor authentication technology into the cards themselves strikes us as a good idea. But even without newfangled cards, the process of how we pay for stuff is getting an overhaul, albeit a slow one. NFC chips, Apple"s Passbook, and Google Wallet are among the options for higher-tech ways to pay. The ubiquity of smartphones may make it more likely that phone-based systems will outpace the adoption of new types of credit cards, especially as these display cards have been around a couple of years without spreading worldwide. But most of us are still using regular old credit cards—and if our next credit cards embed some modern technology to make them more secure, so much the better.

Aside from the increased functionality, the card operates like a standard credit, debit or ATM card. The idea is to provide a two-in-one device for users who have to carry a second authentication device for sensitive transactions.

Despite the narrow targeting of the Display Card, MasterCard adds that in the future, "this card could incorporate additional functionalities and be able to indicate other real-time information such as available credit balance, loyalty or reward points, recent transactions, and other interactive information."

One takeaway from the announcement is that, even in Asia, smartphone-based commerce still hasn"t taken off. Hence Google"s apparent interest in a Google Wallet plastic credit card which would be a stopgap solution until mobile payments become mainstream.

To accept card payments at your business’s premises, you’ll need a card machine. But with so many available on the market, which device is best for your small business?

Based on our in-depth research that analyses the best card readers out there based on price, features, and customer support, we’ve selected the very best options for small businesses, so you can compare these top machines and find out which is best-suited to help you take payments.

According to our research (which you can find out more about by jumping further down the page to our methodology), the SumUp Air card reader is the best overall credit card machine for small businesses. It’s light, limber, and as easy to use as it is to transport, while also managing to boast some of the cheapest rates in the industry.

Our other top mobile credit card machines for small businesses come from Zettle, Square, and PayPal, while Ingenico dominates the countertop and portable varieties. Models such as the VEGA3000 from Castles Technology, and the Verifone V200c and V400m, also figure prominently among our expert selections.

Why not grab quotes right here, right now? Simply answer a few questions about your small business’ requirements, and we’ll match you with one or more leading credit card machine providers. They’ll then be in touch to provide free, no-obligation quotes, all tailored entirely to your business.

On this page, we’ll review the best mobile credit card machines, the best countertop credit card machines, and the best portable credit card machines. Before we dive in, here’s a quick rundown of what each of these terms mean.Mobile credit card machines can function without a wifi connection or power source, so they’re ideal for taking payments in a variety of different locations, including outdoors.

Countertop credit card machines are designed to sit in a fixed spot at your premises, as they need power and internet connections. You usually see these card machines on shop and cafe tills.

Portable credit card machinesare battery-powered and can connect wirelessly to your wifi, so can be carried around your premises. Think restaurants and bars that take payments at customers’ tables.

Mobile card machines are for anyone who needs to be able to accept card payments on the go, but without necessarily having access to an internet connection, or a stable power source.

For one, they’re super simple. You’ll pay just a single fee to purchase your card reader, rather than renting it on a monthly basis (as is the case with most countertop and portable card machines).

These types of card machines also come with slick, intuitive apps that help you process and reconcile payments, send digital receipts, and take stock of your inventory. Interested? Let’s take a look at our top four mobile credit machines for small businesses:

According to our research, the sleek and minimalistic SumUp is the very best mobile card reader that the market has to offer. Not only does it flaunt some of the cheapest transaction rates going, we found that its card reader – which measures up at just 84 x 84 x 23mm in size – is also one of the most user-friendly around. Read more + Read less -

“SumUp is one of the easiest methods of collecting payments. Everything seems to be accessible; whether that’s requesting payments from customers, to setting up web sales and accepting direct card payments. I have absolutely no problem recommending SumUp’s services!”

Zettle (formerly iZettle) emerged out of Sweden just under a decade ago, and its pint-sized, payment-taking (and new and improved) card reader has gone from strength to strength since, including an acquisition by PayPal in 2018. Costing the same amount as SumUp’s card reader – but with a slightly larger transaction fee of 1.75% – Zettle doesn’t quite make the top spot here. Read more + Read less -

“A superb service from start to finish. [Zettle’s] technical support team was really good, particularly when I had an issue adding a bank account – they diagnosed and fixed the issue while I was on the phone. The card reader and app work perfectly for our business, and the online tools mean that we have the complete sales and stocking system we wanted.

So, SumUp or Zettle? We’ve summarised all the key arguments in SumUp vs Zettle – our guide to picking between two of the most clever, capable, and cost-effective card machines that money can buy. Check it out!

With a range of versatile, mobile card machines for small businesses (and a sumptuous set of POS equipment to boot) Square is well-suited to forward-thinking merchants – particularly those with an eye for aesthetics. This reader connects wirelessly to Android and iOS devices, and can accept Google Pay, Apple Pay, and Samsung Pay, as well as the usual card providers. And If you upgrade to Square’s instant deposits, you’ll see payments in your account within 20 minutes. Read more + Read less -

Card readerTransaction fee (in-person)Online transaction feeVirtual terminal fee £16 (excl. VAT) 1.75% 1.9% for European cards, 2.9% for non-European cards 2.5%

If you do business exclusively from a bricks and mortar establishment, you won’t necessarily needa mobile payments solution. In fact, you can save money in the long-term by opting for a countertop card machine.

Countertop card machines allow you to take payments from a fixed place (usually your countertop). They plug directly into your mains for power, and straight into your internet via an Ethernet cable. Handily, that means that these devices aren’t reliant on battery power – or a patchy wifi connection – to function.

Countertop credit card machines are ideal for small retail businesses. Unlike the mobile card readers discussed above, you won’t buy your countertop device up front. Instead, you’ll rent the terminal on a monthly basis, but pay less in transaction fees.

The Desk 5000 from Ingenico belongs to a new era of credit card machines, for a new generation of small businesses. Capable of handling just about any payment method you can conceive of – including Apple and Android Pay, as well as all major card types – it’s not only fast; it’s flexible, too. Ingenico’s operating system integrates with a host of smart business apps, so you won’t just be taking payments; you’ll be getting a range of insights into sales and employee performance, too. Read more + Read less -

Rental fee (per month)Transaction fees £15 With Santander merchant services 1% or 1.5% minimum Depending on the plan and merchant account provider you choose

It takes just 30 seconds to complete, and by telling us more about your small business’s specific requirements, we can help ensure that you receive the best, most personalised rates on credit card machines.

With a trendy, robust design, a powerful processor, and best in class security features, the Verifone V200c is ideal for small businesses looking to get started accepting credit and debit card payments – without breaking the bank! The V200c’s huge memory means it can support a wide range of business apps, which will help you foster greater customer loyalty, and create a more engaging experience at the point of sale. Read more + Read less -

Castles Technology’s VEGA3000 credit card machine for small business is one of the most widely-used countertop devices in the industry; which is reassuring when you’re looking for your very first reader. Boasting wifi, GPRS, Bluetooth and USB connectivity (the full house!), this reliable card machine is simple to use: an imperative for newbies. It also comes equipped with the latest high-tech software to safeguard transactions, assuaging the security concerns you might have when you’re just starting up. Its lightning-quick transaction speeds also make for a positive experience for your customers, which can only serve to help build a good reputation. Read more + Read less -

Portable card machines afford you the flexibility to move around, taking payments and printing receipts on the go at your bricks and mortar premises – without relying on mobile network coverage. They’re the perfect choice for a restaurant or bar setting, where you’ll need to take the credit card machine directly to wherever your customer is sitting.

Typically, portable credit card machines for small businesses usually connect via your premises’ wifi connection. Most function at a range of up to 60 metres.

Like their countertop counterparts, most portable credit card machines for small businesses aren’t bought outright, but rented on a monthly basis by the merchant account provider you end up choosing.

For this reason, prices aren’t always freely available, and you’ll have to either get in touch with the supplier for more pricing info, or utilise our free quote-finding form to request tailored, no-obligation quotes instead.

Ingenico’s iWL card machine series constitutes a range of lightweight, feature-heavy handheld devices that are ideal for small businesses. You can connect using GPRS, 3G, wifi, or Bluetooth technology, and charge them easily via a set of portable, professional-looking charging ports. What’s more, the iWL card terminals are water and shock resistant, making them an ideal choice if your bar or restaurant operates in an outdoor space (which, given the COVID-19 restrictions of 2020, we’re guessing it might’ve had to!). Read more + Read less -

The V400m is Verifone’s most compact payment terminal yet, but that doesn’t mean it compromises on features. It boasts Bluetooth, 4G, USB, and wifi connectivity, as well as an almost IMAX-sized colour touchscreen display (despite being, according to Verifone, the world’s smallest full-function payment device). Oh, and when you add in its Herculean battery life and quick processing speeds? Well, then the V400m weighs in as one of the most versatile mobile PDQ machines on the market – not to mention being ideal for small businesses! Read more + Read less -

With a slick touchscreen, sleek design, and highly pushable buttons, the Ingenico Tetra Move 5000 is about as easy on the eyes as they come. But that doesn’t mean there isn’t more to it than meets the eye, because the Move 5000’s capabilities go well beyond the tabletop. You’ll also get access to Ingenico’s cloud-based reporting and analytical capabilities, and be able to manage your online receipts and transaction history with ease. Read more + Read less -

Rental fee (per month)Transaction fees £15 – £25 per month With Santander merchant services Minimum 1% or 1.5% Depending on your plan and merchant account provider

With a competitive transaction fee rate of 1.69% and pocket-friendly ease of use, the mobile SumUp Air is our top credit card machine for small businesses. But there are plenty more we’d also recommend. The mobile Zettle card reader 2 stands out for its excellent EPOS integrations, while Square’s mobile card reader is a good option for merchants looking to spend as little as possible.

If you’re in the market for a countertop machine, the Ingenico Tetra Desk 5000 offers fast, flexible payment processing, while Verifone’s V200c can help you provide your customers with a personalised buying experience. But the easy-to-use Castles VEGA3000 is our top pick for merchants who are new to credit card processing.

Finally, if you’re after a portable credit card machine, the shock-proof, waterproof Ingenico iWL series is an excellent choice for outdoor businesses. The compact Verifone V400m is a great all-rounder with very reliable battery life, while the Ingenico Tetra Move 5000’s reporting features are great for businesses that plan to make the most of analytics.

Ultimately, it’s best to remember that the best card machine for you depends on the unique needs and qualities of your small business. You’ll need to consider key factors including upfront costs, transaction fees and other charges, and user-friendliness.

And, if you’re still stuck on which card reader is right for you, our free quote-finding tool can help. We’ll match your small business with the credit card machine suppliers that meet your requirements, and they’ll be in touch to offer free, personalised quotes and advice, with zero obligation.

At Expert Market, it’s our aim to provide you with the most accurate, up-to-date, and transparent product and service reviews possible. So, to help you better understand the best merchant account options out there, we’ve conducted in-depth, extensive research into the payments industry and its top companies.

We worked with two independent researchers over 60+ hours to rate 13 different merchant services providers – eight traditional (dedicated) merchant account suppliers, and five payment facilitators.

Customer approval: we assigned each provider a ‘customer score’, which involved seeking opinions from within the community, as well as feeding data aggregated from online sources into a unique algorithm. This allowed us to calculate overall customer approval scores for each merchant account supplier, in real time.

We take the integrity of our research seriously. If you’ve got any questions at all about our research process, feel free to get in touch with Rob, our financial services specialist, at rob.binns@expertmarket.co.uk.

The latest data tells us that in 2020, debit cards were the UK’s most-used payment method, with card payments accounting for more than 50% of all payments. What’s more, one in four payments were contactless.

If you’re opting for a mobile card reader, you’ll pay just a single, one-off fee to purchase the device outright – typically anywhere between £16 and £45 (excl. VAT) – plus a transaction fee of around 1.69% to 2.5% per sale.

This contrasts with the monthly rental fees you’ll usually have to pay to secure the services of a portable or countertop card machine for your small business. Costs here normally come in at between £7 and £30 per month, with transaction fees ringing up at around 1% to 1.5% per sale.

How much you pay for your credit card machine will also depend on the merchant account provider you pick to supply your payment processing, as well as the plan you select. Some companies offer pay-as-you-go pricing structures, while others work on a subscription basis. It’s up to you to pick the right company and plan for you – so be sure to utilise our free quote-finding form to get the best results!

To explore the full range of fees associated with accepting card payments, and learn more how much your small business can expect to pay, we recommend getting acquainted with our guide to comparing merchant account fees.

Sure, some providers – such as Square, and occasionally SumUp and Zettle – have been known to run promotions in which they offer their card readers for free. But by free, we mean “free”, because you’ll still, of course, be eligible for transaction fees. So, while you may be scoring a £20 to £30 saving on the card reader, you’ll still be paying a cut of every sale you go on to make with said device.

So rather than choosing a credit card machine based on how much you could save initially, you’ll benefit more from choosing the machine that best reflects the size, style, and unique needs of your small business.

You can purchase a credit card machine for your small business either directly through the supplier (as is the case with models from SumUp, Zettle, Square, and PayPal), or rent one as part of an agreement with a merchant services provider.

The reason you can’t just walk into a shop and pluck a card machine off the shelf is that – before you can start taking anykind of credit or debit card payments – you’ll first need a merchant account. This is where funds go after they’ve left the customer’s pocket, but before they’ve reached your bank account.

You can acquire a merchant account through a third-party company (such as Fiserv, Handepay, or Retail Merchant Services), or with some high street banks, such as Barclays and HSBC.

You’ll usually only have to connect a few cables, and get your terminal ready to go by following a few on-screen prompts. You’ll also want to make sure your card machine (and its charging port) is located in the most optimal location for serving the customer; whether that’s on your countertop, or – in the case of a bar or restaurant – somewhere your servers can easily access it.

Yes! Contract-free plans are usually more common among mobile card readers than any other kinds. Square won’t ask you to sign a contract to use its card reader, and the SumUp Air doesn’t come with fixed-term contracts, so you’ll have the flexibility to opt out when you want to.

Using a credit card over debit cards and cash can often be advantageous. With responsible credit habits, you can work toward building your credit score and even earn credit card rewards, such as points, miles or cash back.

However, some stores may charge you extra fees when using your credit card. There are three types of fees worth noting: surcharges, convenience fees and minimum purchase requirements. This guide will discuss the difference between each and if stores are legally allowed to implement them.

Credit card surcharges are optional fees added by a merchant when customers use a credit card to pay at checkout. Surcharges are legal unless restricted by state law. Businesses that choose to add surcharges are required to follow protocols to ensure full transparency. The surcharge regulations outlined below only apply within the U.S.

Under Visa and Mastercard, retailers are required to register the surcharge with the payment network. Then, they must display a notice of the surcharge at the point of sale — both in-store and online. The consumer"s receipt must also indicate a surcharge was added to the bill.

If merchants add a surcharge, they must decide to add them at the brand or product level — but not both. A brand level surcharge adds the same fee to all credit card transactions from the same payment network, such as Visa or Mastercard. A product level surcharge applies to a particular type of Visa or Mastercard, such as Visa Signature or World Elite Mastercard. The maximum surcharge is 4% of the credit card transaction.

Credit card convenience fees can be charged in some instances and will vary by issuer. On Visa, these fees can be charged when a merchant offers an alternative payment method — one that"s different from how it usually conducts business. Other issuers have varying rules that only allow official government agencies and select companies to charge convenience fees.

For example, a museum may not impose a convenience fee at the register if that"s how most people buy their tickets. However, if the museum adds on an option to purchase tickets online with a Visa card, a convenience fee may be charged.

American ExpressOnly government agencies, educational institutions, utility companies and rental establishments can charge credit card convenience fees

Ten states prohibit credit card surcharges and convenience fees: California, Colorado, Connecticut, Florida, Kansas, Maine, Massachusetts, New York, Oklahoma and Texas. It is illegal for merchants to add any surcharges to credit card transactions or charge convenience fees to nontraditional payment methods in these states.

Minimum purchase amounts are thresholds merchants can impose on credit card transactions. This amount must be under $10. While not technically required, merchants who decide to add a minimum purchase requirement are encouraged to disclose this through proper signage and verbal communication to the cardholder.

Credit card surcharges, convenience fees and minimum purchase requirements are all fees that merchants can add to offset the cost of pricey processing fees. Keep in mind that surcharges and convenience fees are illegal in some states and can only be applied to credit card transactions.

Yes. Merchants can apply varying surcharges by card brand or card product, but not both. For example, a retailer may impose surcharges only on American Express cards or only on certain products, such as Visa Signature cards.

Tip: After you start your trade-in process, you’ll get a confirmation email. To send your old phone to us, we’ll send you a kit with a prepaid envelope.

If the trade-in device"s value matches the estimate: If you purchase a Pixel, we’ll credit the Post-Inspection Value (PIV) to the form of payment used for your phone purchase.

If you get the confirmation email within the last 10–14 business days and a refund didn’t show up in your account, contact our support team. Refunds may take up to 14 business days to be applied to your card.

Rates, discount points and terms are based on an evaluation of each member"s credit history, loan-to-value (LTV), occupancy, payment type, loan amount and loan purpose, so your rate and terms may differ. All loans are subject to credit approval. Questions? Please contact Navy Federal at 1-888-842-NFCU (6328).

Navy Federal also offers home loans for investment properties. When reviewing quotes from other lenders, make certain you obtain the discount points and any origination fees for comparison with Navy Federal"s rates. APRs reflect down payment/equity, unless otherwise noted.

Any refinance mortgage where the proceeds will be used to pay any debt other than debt used in the purchase of the home is considered a cash-out refinance. Additional discount points will apply to cash-out loans, which are based on credit history and loan-to-value. Cash-Out Refinance is not allowed on Choice products.

Loans with subordinate financing and loans secured by condominium properties may require additional discount points. Conforming loans secured by two-unit properties are subject to an additional 1.00% discount point. Manufactured homes are subject to an additional 0.50% discount point.

If you select the Float to Lock Commitment, it means that you want to allow the interest rate and/or discount points to float with the market. You must lock in your interest rate and/or discount points at least seven (7) calendar days prior to settlement/closing.

The Freedom Lock Option is available on refinance and purchase loans for a non-refundable 0.250% fee added to the origination. You will have the opportunity to relock one time if rates improve, with no maximum interest rate reduction. The fee must be collected up-front. VA Loans are not eligible for the Freedom Lock Option.

The Special Freedom Lock Promotion is a limited-time offer and subject to change at any time. Offer is available for new loan applications at no additional fee, with a maximum interest rate reduction of up to 0.500%. You will have the opportunity to relock twice if rates improve, and your loan must close within your initial lock commitment period. The Special Freedom Lock option is available for:

The differences between these cards are straightforward. A debit card makes payment with its holder’s current account balance. A prepaid card can make payments with pre-loaded funds for retail and online purchases and ATM withdrawals. A credit card, however, pays with funds borrowed from a financial institution. If you want to know more about card types, visit the Openbank website or Finanzas para mortales (Finance for mortals).

There are also many types of credit card. Classic cards let cardholders borrow money for payments on the condition that they repay the bank in one month (usually from the payment date). Gold and platinum credit cards have a higher credit limit. Revolving cards automatically defer payments. Lastly, points cards accumulate benefits and deals for cardholders.

Have you ever wondered why your credit card is shaped the way it is? Or how the size of a credit card was chosen? There are standards that determine your card’s look, feel, and thickness. Without them, no one would be able to transact business.

As a business owner, you may be wondering about plastic card thicknesses so that you can implement a rewards program or gift card campaign.So get out your wallet and take a gander at the array of cards you have in there. Are some thicker than others? Are they all the same size? Think about your driver’s license, debit card, credit cards, gift cards, anddiscount fundraising cardsas you read this article.

There are actually international standards for the size of credit cards. If we didn’t have any, can you imagine how difficult it would be to manage all those cards in your wallet? You’d have ID cards fitting in sideways and credit cards getting lost in their slots. In addition, credit card machines would be proprietary to certain cards and not others. No, that just wouldn’t do.

Instead, theInternational Organization for Standardizationhas developed four different standard sizes for identification cards. They each have names: ID-000, ID-1, ID-2, and ID-3. The standard credit card size is ID-1, a size that is also commonly referred to as CR80. A standard CR80 credit card has the following dimensions:

This means that any card you obtain for standard business transactions—anything from credit or debit purchases to gift card use—is about 3.5 inches by 2 inches.

Now that you know what size your wallet slots are, does it have you wondering how thick they need to be? The standard thickness for an ID-1 or CR80 credit card is 0.03 inches, or 0.76 millimeters. Mil, often confused with the millimeter, is actually equal to one thousandth of an inch. This makes a credit card 30 mil thick.

Plastic card printing companies will even make cards thinner than this;30 milis actually a durable thickness for plastic cards. Which makes sense because credit cards take a lot of abuse with all those credit card machines they slide through.

In fact, did you know that the magnetic strip, or mag strip, on the back of a card partly determines this standardsize? If your card needs to be run through a machine, it needs to match thesizethat machine is made for. This means that most money-based cards need the standard CR80size(gift cardsand credit/debit cards).

For example, a card that feels more flexible is most likely set at a thickness of 20-24 mil. There are even thinner cards on the market, around 10-15 mil, and they can feel almost as thin as paper. And don’t forget cards that are thicker than .76 mm—cards used for parking garages and getting into buildings are made to be more inflexible than credit cards.

If you’re a small business owner developing a gift card program, you definitely should have these considerations in mind. At 4ColorPrint, we can help you through the process of getting these cards made.

Credits cards and debit cards have chips in them to ward off fraud. But Dynamics is introducing a new Wallet Card today that can run circles around that technology.

The Wallet Card has the support of a consortium of financial companies, including MasterCard, which led the last financing round for Pittsburgh, Pennsylvania-based Dynamics. The Wallet Card has a cell phone chip and most of the working parts of a computer, including a display — all inside a piece of plastic that looks like any other credit card.

Dynamics is showing the Wallet Card at CES 2018, the big tech trade show in Las Vegas this week. Jeff Mullen, founder and CEO of Dynamics, said in an interview that the new card will provide an “unprecedented level of security.”

For instance, if you learn from the display on the card that the last purchase made on your card was fraudulent, you can request a new card from the bank and it will be issued on the spot, with proper authentication. You no longer have to call the bank to get a card reissued. Your new number account and card number are simply downloaded onto the card.

If you lose the card or report it stolen or forget your pin code, the bank can disable the card through the cell connection and send you a new card. Cards can be couriered to the consumer in a matter of hours, and the consumer can restore the wallet by downloading cards. The speed could reduce fraud losses and prevent purchase delays, Mullen said.

Another is that you can now have multiple cards on one Wallet Card. Consumers can access their debit, credit, prepaid, multicurrency, one-time use, or loyalty cards on a single card with the tap of a button. When you get to a checkout stand, you could choose to pay with points or credit simply by pressing a button on the card.

It is also easily distributed. Banks can distribute Wallet Card anytime and anywhere — such as in their retail branches, during events, or even in-flight, and consumers can activate it immediately. Card information can then be downloaded through a secure, over-the-air cellular connection. At the same time, Mullen said the cards have built-in security in hardware elements.

And the technology could lead to tighter connections between consumers, issuers, and retailers. Messages can be sent to the Wallet Card at any time. For example, after every purchase, a message may be sent to notify the consumer of the purchase and of their remaining balance if they used a debit or loyalty card.

Consumers can be notified of a suspicious purchase and click on “Not me” to have a fraud alert set and a new card number issued. They can also receive coupons directly on their cards.

The Wallet Card has more than 200 internal components, and it’s the latest rendition of electronic credit and debit cards that Mullen and his team dreamed up at Carnegie Mellon University. He started the company in 2007, beginning a long journey to replace the mag stripe credit card, which has been in use since the 1970s and is fraught with all kinds of security risks.

This new card has “organic harvesting,” which means it can use renewable energy sources to keep its battery charged. It has a card-programmable magnetic stripe, card-programmable EMV chip (the chip cards that have become so popular), and a card-programmable contactless chip. That means it could be used in just about any territory.

Dynamics has the support of the Wallet Card Consortium, which includes a number of big banks, payment networks, and carriers. Members include Visa, MasterCard, Sprint, and JCB (a Tokyo-based credit card company).

Dynamics has raised $110 million to date from investors that include MasterCard, CIBC, Adams Capital Management, and Bain Capital Ventures. The company’s earlier intelligent account cards are currently used by more than 10 million consumers. Customers include the big Canadian coffee chain Tim Horton’s, the Upper Deck Company, and CIBC.

Get the wholesale e ink display card at Alibaba.com. The EAS system at Alibaba.com features high sensitivity to help protect the safety of your staff and shop.

We use selected materials for the various components of the e ink display card. The alarm volume is quite loud so users can hear the alarm at the checkout counter or even when they are away from the door.

Most decoders of the e ink display card are non-contact devices with a certain decoding height. The electronic tag can be decoded without touching the degaussing area when the cashier registers or packs the item. The decoder and laser bar code scanner works well with the equipment, so that payment and decoding are completed simultaneously. This makes it convenient for the cashier and the customer. Our system enables integration with the laser bar code. This eliminates mutual interference between the two devices and improves the decoding sensitivity. In case someone leaves the shop with undecoded goods, it will trigger an alarm in the EAS as they pass through the detector device. This enables the cashier, customers, and security personnel to deal with the issue in time.

Options are potentially one of the most profitable investment instruments available in today?s intensely volatile financial markets. Just a few years ago, the information needed to exploit the vast earnings potential of options was beyond the reach of all but a handful of analysts. Now, anyone with a PC and a few basic software tools has direct access to all the up-to-the-minute market information needed to compete successfully with the "big boys." But, having information and knowing how to wield it are two very different things. In this groundbreaking book, online options trading innovator George Fontanills arms you with the knowledge and skills youneed to unleash the phenomenal power of your computer to become a successful online options trader.

Following a concise review of the basics of online trading--including hardware andsoftware requirements and essential online resources--Fontanills cuts to the chase with step-by-step coverage of 15 proven managed risk option trading strategies. Specifically designed for online traders, these tested off-floor techniques provide you with a sure-fire method for consistently building up your trading account. Drawing upon his years as a leading international options educator, Fontanills makes it easy for you to master online options trading by walking you through a series of hypothetical trades that demonstrate how to compute the maximum risk, maximum profit, breakevens, and exit alternatives for each strategy.

"George Fontanills, the dean of options trading, has put together an online options trading approach that is down-to-earth and insightful. Armed with this book, investors should feel well equipped to play on the battlefield, having been forewarned of the risks, dangers, and opportunities. Fontanills cares about everyone?s money as much as he cares about his own--a rare find in the world of finance." - Peter D. Henig Senior Editor, The Red Herring

"Options trading expert George Fontanills has written the definitive guide to trading options online. Filled with everything from a comprehensive list of insightful website reviews to innovative options strategies, Trade Options Online is a ?must read? for all investors who want to compete successfully in the computerized markets of the twenty-first century!" - Brown President and CEO

Now in its ninth edition, Human Resource Management in the Hospitality Industry: An Introductory Guide, is fully updated with new legal information, data, statistics and examples. Taking a "process" approach, it provides the reader with an essential understanding of the purpose, policies and processes concerned with managing an enterprise¿s workforce within the current business and social environment.

Since the eighth edition of this book there have been many important developments in this field and this ninth edition has been completely revised and updated in the following ways: Extensively updated content to reflect recent issues and trends including: labour markets and industry structure, impacts of IT and social media, growth of international multi ¿ unit brands, role of employer branding, talent management, equal opportunities and managing diversity. All explored specifically within the Hospitality Industry

An extended case study drawing from the authors¿ experience working with Forte and Co., Centre hotels, Choice Hotels and Bass, Price Waterhouse and Grant Thornton explores key issues and shows real life applications of HRM in the Hospitality Industry

Written in a user friendly style and with strong support from the Institute of Hospitality, each chapter includes international examples, bulleted lists, guides to further reading and exercises to test knowledge.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey