credit card with lcd display for sale

OK, this one gets a WOW. I have to admit I dont exactly get how it works, but Im loving that one of the FUTURE intended uses is to be able to check your balance right from the card… ok that freaked me out a little.

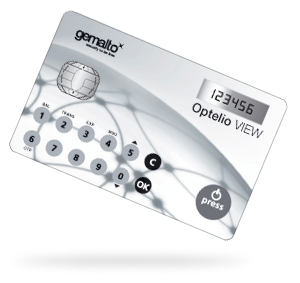

MasterCard has introduced a new high-tech credit card — — one that looks and functions almost exactly like an ordinary card, save for the integrated display and numerical keypad. The screen looks and acts like the display on a calculator; it should boost security by allowing the cardholder to generate single use numerical passwords for authentication.

“Instead of sending customers another bulky token, could we replace something which already exists in the customer’s wallet?” asked V. Subba, regional head of retail banking products for Standard Chartered Bank. “That was when credit, debit and ATM cards, immediately came to mind.”

Banks looking to boost security for online banking use a separate authentication token or device, the company noted. A Display Card could do both — and in the future it could incorporate additional functionalities and be able to indicate other real time information such as available credit balance, loyalty or reward points, recent transactions and so on.

“With the continued growth in online and now mobile initiated remote payments, consumers are naturally demanding increased security,” explained Matthew Driver, a regional president for MasterCard.

Since then the Indiegogo crowdfunding campaign has been issued success and has already raised over $1.2 million with still 16 days remaining...Read more

The display smart card combines all your customers" needs for typical daily banking and payment activities -- from ATM and EMV payment, loyalty, and bank account access to generating one-time passwords for online authentication.

The display payment card integrates a magnetic stripe and an EMV contact or contactless chip for payment, with a keypad option that protects the card.

It offers anatural step up in banking and authentication solutions, making it easy for banks and their customers to migrate from traditional EMV payment cards to more multifunctional Smart Mobile devices (SMDs).

The display payment card is fully integrated with our services -- card personalization, customized card printing, engraving, and packaging, to end-user mailing and fulfillment.

NOTE: This is an NRS PAYlocked modeland will ONLY work with NRS PAY Credit Card Processing.BEFORE YOU BUY:IF YOU ARE NOT AN NRS PAY CREDIT CARD PROCESSING CUSTOMER, THIS UNIT WILL NOT WORK FOR YOU. If you"re not interested in using NRS PAY processing, YOU SHOULD PURCHASE OUR UNLOCKED MODELS - (PLEASE SEE OUR OTHER LISTINGS)

The NRS PAY locked POS will include instructions for self-installation & setup , plus you can receive FREE, live, setup training.What’s included ?15-Inch Touch Screen Monitor with Customer-Facing Display

Receipt Printer – 1 paper roll includedSHIPPED SEPARATELY AFTER CONTACTING NRS SUPPORTPAX S300 credit card reader will be calibrated specifically for your processing account and will be shipped separately.

Alibaba.com features an exciting range of lcd display smart card that are suitable for all types of residential and commercial requirements. These fascinating lcd display smart card are of superior quality delivering unmatched viewing experience and are vibrant when it comes to both, picture quality and aesthetic appearances. These products are made with advanced technologies offering clear patterns with long serviceable lives. Buy these incredible lcd display smart card from leading suppliers and wholesalers on the site for unbelievable prices and massive discounts.

The optimal quality lcd display smart card on the site are made of sturdy materials that offer higher durability and consistent performance over the years. These top-quality displays are not only durable but are sustainable against all kinds of usages and are eco-friendly products. The lcd display smart card accessible here are made with customized LED modules for distinct home appliances and commercial appliances, instruments, and have elegant appearances. These wonderful lcd display smart card are offered in distinct variations and screen-ratio for optimum picture quality.

Alibaba.com has a massive stock of durable and proficient lcd display smart card at your disposal that are worth every penny. These spectacular lcd display smart card are available in varied sizes, colors, shapes, screen patterns and models equipped with extraordinary features such as being waterproof, heatproof and much more. These are energy-efficient devices and do not consume loads of electricity. The lcd display smart card you can procure here are equipped with advanced LED chips, dazzling HD quality, and are fully customizable.

Save money by browsing through the distinct lcd display smart card ranges at Alibaba.com and get the best quality products delivered. These products are available with after-sales maintenance and are also available as OEM orders. The products are ISO, CE, ROHS, REACH certified.

Credits cards and debit cards have chips in them to ward off fraud. But Dynamics is introducing a new Wallet Card today that can run circles around that technology.

The Wallet Card has the support of a consortium of financial companies, including MasterCard, which led the last financing round for Pittsburgh, Pennsylvania-based Dynamics. The Wallet Card has a cell phone chip and most of the working parts of a computer, including a display — all inside a piece of plastic that looks like any other credit card.

Dynamics is showing the Wallet Card at CES 2018, the big tech trade show in Las Vegas this week. Jeff Mullen, founder and CEO of Dynamics, said in an interview that the new card will provide an “unprecedented level of security.”

For instance, if you learn from the display on the card that the last purchase made on your card was fraudulent, you can request a new card from the bank and it will be issued on the spot, with proper authentication. You no longer have to call the bank to get a card reissued. Your new number account and card number are simply downloaded onto the card.

If you lose the card or report it stolen or forget your pin code, the bank can disable the card through the cell connection and send you a new card. Cards can be couriered to the consumer in a matter of hours, and the consumer can restore the wallet by downloading cards. The speed could reduce fraud losses and prevent purchase delays, Mullen said.

Another is that you can now have multiple cards on one Wallet Card. Consumers can access their debit, credit, prepaid, multicurrency, one-time use, or loyalty cards on a single card with the tap of a button. When you get to a checkout stand, you could choose to pay with points or credit simply by pressing a button on the card.

It is also easily distributed. Banks can distribute Wallet Card anytime and anywhere — such as in their retail branches, during events, or even in-flight, and consumers can activate it immediately. Card information can then be downloaded through a secure, over-the-air cellular connection. At the same time, Mullen said the cards have built-in security in hardware elements.

And the technology could lead to tighter connections between consumers, issuers, and retailers. Messages can be sent to the Wallet Card at any time. For example, after every purchase, a message may be sent to notify the consumer of the purchase and of their remaining balance if they used a debit or loyalty card.

Consumers can be notified of a suspicious purchase and click on “Not me” to have a fraud alert set and a new card number issued. They can also receive coupons directly on their cards.

The Wallet Card has more than 200 internal components, and it’s the latest rendition of electronic credit and debit cards that Mullen and his team dreamed up at Carnegie Mellon University. He started the company in 2007, beginning a long journey to replace the mag stripe credit card, which has been in use since the 1970s and is fraught with all kinds of security risks.

This new card has “organic harvesting,” which means it can use renewable energy sources to keep its battery charged. It has a card-programmable magnetic stripe, card-programmable EMV chip (the chip cards that have become so popular), and a card-programmable contactless chip. That means it could be used in just about any territory.

Dynamics has the support of the Wallet Card Consortium, which includes a number of big banks, payment networks, and carriers. Members include Visa, MasterCard, Sprint, and JCB (a Tokyo-based credit card company).

Dynamics has raised $110 million to date from investors that include MasterCard, CIBC, Adams Capital Management, and Bain Capital Ventures. The company’s earlier intelligent account cards are currently used by more than 10 million consumers. Customers include the big Canadian coffee chain Tim Horton’s, the Upper Deck Company, and CIBC.

PCI PTS 5.x certified, the Ingenico Lane/8000 is designed to ensure long-term compliance. II Pt uses the latest cryptographic schemes with future-proof encryption and additional anti-theft systems, such as Kensington locks.

An intuitive, interactive device, the Ingenico Lane/8000 transforms the point of sale into a point of engagement. It offers the same user experience, touchscreen capabilities, and user-friendly interface as a tablet. Multimedia support is also available along with Bluetooth LE.

New: Manage bookings, payments, and staff on a powerful handheld device with Square Appointments on Square TerminalTake payments. Get paid. No surprises.

Chip cards (or EMV) are the new standard in payment cards. Insert chip cards into Terminal and complete the sale in just two seconds—one of the fastest you’ll find.

Get up and running in fewer than five minutes—no need to go through a bank. Square Terminal is an intuitively designed credit card machine so you, your team, and your customers can use it right away.Software solutions customized for your business

Square Terminal can integrate with your custom or third-party POS to automatically sync in-person payments with your software.It won’t let you down. And neither will we.

“With Square Terminal, everything is very simple and transparent. All things considered, we save money with Square.”Kerrie Volau, Practice Manager, Eye CarumbaThere’s so much more waiting for you.

If your business does more than $250,000 in credit card sales, talk to us about a custom processing rate and other ways we can save you money.Frequently asked questionsSquare Terminal is an all-in-one device for taking card payments and printing receipts. It comes with free Square Point-of-Sale software that’s easy to set up and easy to use, and a built-in battery that lasts all day, so you never miss a sale.

Square Terminal is a credit card terminal that makes it easy for any business to take card payments and run a point of sale. Customers simply tap, insert, or swipe their credit or debit cards for fast, efficient, and seamless payments.

Square Terminal costs $299 before taxes and fees, with hardware financing options available at checkout. To connect Square Terminal to the internet via ethernet, or to connect accessories such as a cash drawer, barcode scanner, or additional printers, you can add an optional Hub for $39.

Square Terminal requires an internet connection. Connect Square Terminal to the internet via Wi-Fi, or via Ethernet with an optional Hub. When you don’t have an internet connection, you can use Offline Mode to take payments.Available at local retailers*All credit sale plans are issued by Block, Inc. Not available to merchants in AL, DE, MS, MO, NH, and TN. Purchase amounts must be from $49 to $10,000. APR is 15%. Available plan lengths vary from 3, 6, 12, and/or 24 months installments depending on purchase amount. Sales tax, where applicable, will be due at checkout. All plans subject to credit approval and other factors.

Meet MasterCard"s new "Display Card," which basically combines the usual credit/debit or ATM card with an authentication token. The authentication portion features a touch-sensitive keypad and LCD display -- hence the name "Display Card" -- for reflecting a one-time password (OTP).

Currently, many banks issue a separate authentication token for online banking services, particularly high-risk transactions, such as payments or transfers above a certain amount, adding payees, or changing personal details. The new 2-in-1 cards would therefore eliminate the hassle of carrying a separate authentication device -- good news for people who carry their whole lives in their pockets.

Besides generating OTPs, the Display Card may in the future be able to show your available credit balance, reward points, or even recent transactions.

The Verifone 820 Duet has a large, bright-color touch screen display, and the attached handheld unit fits in the palm of their hand for secure debit PIN entry. The user-friendly backlit keypad makes for easy data entry with an ultra-sleek PIN pad.

The VX 820 DUET has the muscle for fast transactions and the brains to deliver great customer interactions. With increased processing speed due to a 400 MHz ARM11 processor and memory that can exceed 500MB, the Verifone VX 820 DUET can support a range of applications.

The Verifone VX520 can be set up to handle transactions over Ethernet or traditional analog dial up, and with the optional battery, can be made into a mobile terminal using GPRS. Connections are located on the bottom of the terminal to secure and hide unsightly wires.

It can handle encryption, decryption and processing at lightning fast speeds thanks to its powerful ARM11 processor. With its large memory space, the Verifone VX520 can handle applications such as loyalty cards, gift cards and NFC payments. The backlit screen and keypad allow for easy data entry. The Verifone VX520 Color is EMV-ready with standard PCI PTS 3.0 and also supports end-to-end encryption with VeriShield Total Protect.

Even though the Verifone MagIC3 C-Series is designed to be cost-effective at low volume, it is still fully compliant with the latest security and communications standards such as EMV and PCI.

The Verifone H5000’s color LCD display features adjustable backlighting and touch screen entry. Powered by a 32 bit processor, transactions are performed quickly and accurately.

Connectivity is via a v.34 modem with a fallback method of processing over IP. The T4210’s peripheral port can be used to connect devices such as external PIN pads, check readers and contactless readers along with the previously mentioned EMV card readers.

The Verifone Optimum T4230’s thermal printer can be used for receipt and value-added coupon printing. The backlit display supports a sharper image for maximum visibility. Color coded ports allow for easy terminal deployment.

A credit card reader is essential to many small businesses, and choosing the right card reader can help your company operate more smoothly. The best choice depends on your budget, the features you need and whether you"re accepting payments at a counter or on the go.

Square’s contactless and chip card reader enables you to accept credit cards with chips and digital wallets, such as tap-and-pay credit cards and smartphone apps, including Apple Pay and Google Pay. It uses Bluetooth technology instead of connecting directly to a device, which lets you keep your cell phone or tablet nearby — but not out all the time.

The reader must be charged, but the charging dock can double as a support for the reader for a counter or table. You can also charge it with a USB charger.

Square also offers Tap to Pay on iPhone, which lets merchants accept card payments using only a regular iPhone with the Square POS app. Customers hold their cards or their own iPhone wallets near the merchant"s phone to pay.

This credit card reader by Clover works with phones and tablets via Bluetooth. It also processes every type of credit card payment your customers could want: magstripe-only cards, chip cards and contactless payments.

You can choose between the starter plan or the standard package. Both provide basic payment processing with 24/7 live support. However, the standard plan includes added features such as sales tracking, detailed reporting, inventory management and itemized orders.

PayPal’s Zettle accepts chip and contactless payments, but it doesn’t read magstripes. It does, however, let customers pay with QR codes on PayPal and Venmo platforms. Its POS software offers sales reports, inventory management, tracking sales performance and more.

Transaction fees generally fall in line with competitors, with lower rates available for transactions made by QR code. All funds go into your PayPal account rather than a bank account. You’ll need to request a transfer to move the funds to your business bank account before you can use them outside of PayPal.

Powerful and compact, the SumUp Plus credit card reader works through Bluetooth with Apple and Android devices and promises more than 500 transactions on one charge. In addition to having a screen to show transaction details, the reader comes with a few helpful POS software features that allow you to manage products in your catalog, track sales, send digital receipts and manage employee accounts. However, you might find that the overall POS is lacking when compared with the more robust options on the market.

The Clover Flex is a small but powerful handheld credit card reader. It can process all three credit card payment types, scan bar codes and even print receipts. It"s one of the few options in this category that has its own screen, removing your personal device from the equation and allowing customers a bit more of a professional experience when checking out on the spot.

Helcim’s card reader accepts chip and contactless payments, but it can’t read magstripe cards. Because it connects through Bluetooth, it needs to be charged. It also provides POS software through the Helcim app with features that include customer management and inventory tracking plus analytics and reporting.. A standout feature is its self-service portal, which allows customers to log in to see their payment information and purchase history.

Helcim bases its fees on the type of card and interchange fees, which are set by card networks. It also offers volume-based discounts. The processor doesn’t require you to sign a contract, choose a monthly fee or pay to cancel your service.

The Toast Go 2 allows you to submit orders at tables and accept all three styles of payment. It"s also spill proof, will hold a charge for 24 hours and has a 6.4-inch touchscreen for quick checkout. The free version of Toast’s POS software comes with basic features, including point-of-sale and payment processing, but advanced features are available with paid plans. One downside: The company requires contracts.

Square Terminal allows you to accept all three methods of credit card payments: chip, contactless and magstripe. It comes in on the lower end of the all-inclusive card readers.

The company"s standard flat-rate processing fees apply and depend on whether you run the card in person or enter it manually. There"s no monthly contract.

The Square Stand is designed specifically for a single smart device: the iPad — although it works only with certain iPad models. Snap an iPad into the Square Stand, and use it as a desktop point-of-sale. The configuration allows you to provide a larger screen for transaction details, and the swivel feature allows customers to sign on the iPad without having to pass the device around. It can process chip and contactless payments but not magstripe unless you buy a Square Reader.

The Clover Mini is a countertop setup that doesn"t require a tablet. It allows your business to accept all types of payments and print receipts. You also get some nifty POS features, including inventory, customer and employee management functions with paid monthly plans.

The Clover Station Solo is a register-style system that offers merchants a 14-inch high-definition screen and a receipt printer for the full checkout experience. The system works with Clover’s POS for retail, offering payment processing, inventory and staff management, reporting and more. For restaurants, the Station Solo fits nicely with customizing and tracking orders, managing table mapping and much more for streamlined service.

The Square Register is the first fully integrated credit card scanner system from Square and is a complete countertop POS system that can accept magstripe, chip card and contactless forms of payment. It boasts two screens — one for the employee and one for the customer to show transaction details — for a seamless experience. It also offers an extra-long cable that allows businesses to separate the Register and customer"s screen to encourage social distancing. Its software provides merchants inventory, employee and customer relationship management functions, plus a reporting suite where you can view sales data.

The Clover Station Duo ups the game with a combination of a 14-inch screen for you and a 7-inch screen for your customers. This makes it easier for customers to confirm orders and pay however they want — credit card, debit card, and contactless payment methods. Designed for retail stores, restaurant environments and service businesses, the Station Duo offers the same features of the Station Solo with more power.

While this option tops the list for the most expensive system, the Station Duo is currently sold with a cash drawer and a receipt printer, giving you the gamut of checkout features.

A card reader is a device merchants use to detect and transmit information on credit cards, debit cards or other payment cards, such as account number, authorization code or account name.

How much do you want to spend? A card reader without a screen is the cheapest option, and sometimes free. But depending on brand, type and features you want, you could pay more than $1,000. Remember to keep processing costs in mind: If a free reader charges more per transaction, you may not actually save money.

How will you accept payments?Some card readers — such asthose that work with iPhones — are portable and can turn a mobile device into a card reader, if you want to accept payments on-to-go. Other options are fixed attachments to a register, making them a better fit for counter-based businesses.

What features do you need?If you want to simply accept magstripe, chip and contactless payments, a basic card reader can likely do the job. But if you"re looking for more sophisticated features, like inventory management or advanced sales analytics, consider a comprehensive POS system instead.

Accepting credit cards doesn’t have to be complicated for your small business. The most common place to start is with a credit card machine. You’ll also have to consider swipe rates, merchant accounts, hardware and security standards, but we’ve got you covered. Here are the answers to frequently asked questions about credit card machines for your small business.

Credit card machines are used to collect payments from customers who wish to pay by credit or debit card. They are typically connected to the internet or a phone line, to send data to the processor. For most credit card processors, funds are transferred from the customer’s bank to the business’s merchant account. In some cases, the credit card processor uses a merchant account and holds funds on your behalf, and then directly deposits them into your checking account at your discretion.

There are various types of credit card machines, and each offers unique benefits. Some of the most common types of credit card terminals are countertop, mobile, virtual and integrated point-of-sale (POS) systems.

These credit card machines are the most common, and require a wired connection to your phone line or internet network. The device usually sits on a counter or tabletop. Countertop terminals can process both credit and debit cards, and some have a keypad for PIN entry. Many of them support card-not-present transactions, in which a merchant types in the customer’s credit card number. Here are some benefits of using this type of terminal:Secure transactions: Because they are hardwired, countertop credit card machines are not very vulnerable to data theft.

Card-not-present transactions: Card-not-present transactions are mostly used for phone or internet orders, but can also be used when a credit card’s chip or magnetic strip is defective.

These are some disadvantages to using countertop terminals:Hardwire connection: Since they require a hardwired phone or internet connection, they are not suitable for mobile selling either within or outside your company.

Mobile terminals rely on a wireless connection through Wi-Fi, a phone or a tablet to process card payments on the go. This means they can be moved from the checkout counter to other places in the store – or even taken out to events. Here are some advantages of using mobile terminals:Portability: Your business can better serve your customers’ peak demand by sending cashiers in line to process orders. Perhaps your company is portable by nature, and the mobile terminal gives it more profitability.

Mobile terminals are best for businesses that are mobile and/or participate in events such as food trucks and farmers or flea market vendors. They are also useful for high-demand businesses, such as ticket vendors and Chick-fil-A locations. Finally, businesses that do house calls, like plumbers and tow truck drivers, can benefit from mobile credit card terminals.

These terminals allow your e-commerce business to process credit and debit cards by entering the payment information into a secure website. A client’s card does not need to be present to process this type of transaction.

These are some benefits to using virtual terminals:Cards optional: You can run your business virtually and still process credit card transactions with this type of system.

These are some drawbacks of virtual terminals:High costs: Because card-not-present transactions are more prone to fraud, credit card processors tend to charge higher fees for them.

High mishaps:With this type of system, you’d have to type in the credit card number, expiration date and security code each time a customer makes a purchase. This is time-consuming and more likely to result in errors.

Credit cards only:Virtual terminals only process credit cards – not cash, checks or debit cards – so you’d need a backup system in place to process those kinds of transactions.

Some virtual terminals charge a subscription fee, in addition to your transaction fees on purchases. The transaction fees tend to be higher than when customers insert, tap or swipe their cards in person because of fraud.

These are some disadvantages of integrated POS terminals:Limited processors:Each POS system usually only has a few payment processors that integrate with their system. You will need to choose from among that limited group. It will also be more difficult to switch to another payment processor that has low rates.

Editor’s note: Looking for the right credit card machine for your business? Fill out the below questionnaire to have our vendor partners contact you about your needs.

A credit card machine is simply a credit card reader and PIN pad. A POS system is a complete checkout terminal that comes with a credit card machine, monitor or tablet, a cash register and printer. POS systems can also include additional software or apps that track inventory, monitor sales, generate discounts, create financial reports and help with marketing.

When choosing a POS system or credit card processor for your business, you have many choices. To make it easier, we have evaluated the top providers in the industry and chosen the best picks for different needs.

Many vendors offer free credit card machines; others allow you to buy or lease your equipment. Pricing depends on the model and features, such as Europay, Mastercard and Visa (EMV) and near-field communication (NFC) capabilities. Costs are also based on whether you rent or purchase the machine, and if you receive it from the vendor or a third party. Generally, the most basic credit card machines cost less than $100, and more expensive models can cost several hundred.

Other costs to consider include credit card processing fees, monthly service fees, setup fees, gateway fees and compliance fees. These costs vary by vendor, and many waive some fees for new customers.

By contrast, tiered pricing depends on the type of credit card being used. This pricing structure is less favorable because it works by bundling different types of credit cards into tiers – with increasing swipe rates. These tiers are classified as qualified, midqualified and nonqualified cards. These include regular cards, debit cards, rewards cards, business cards and other types of credit and debit cards. Generally, credit card processors decide which types of cards are qualified, midqualified and nonqualified for their particular service, so tiers and pricing vary.

Flagship Merchant Services is our choice for the best high-volume credit card processor, because it uses both interchange-plus pricing and tiered pricing. (Note that tiered pricing is the advertised cost, so you’ll have to ask for interchange pricing.) Flagship’s interchange-plus rate is 0.3% plus 10 cents per transaction, and is negotiable for your company’s high sales volumes. Its tiered pricing starts at 0.38% for qualified debit cards and 1.58% for credit cards, plus 19 to 21 cents per transaction – the price increases for midqualified and nonqualified cards.

Some credit card processors also charge a flat percentage per transaction. This is typically the case with mobile credit card processors, such as Square and PayPal, which charge 2.75% and 2.7% respectively per swipe.

A merchant account allows your business to accept credit cards. It transmits payment data from a customer’s bank to your company’s bank, and authorizes credit card transactions. Merchant accounts are offered either by the credit card processor or directly from a financial institution – typically a bank. You will normally need to apply for a merchant account. However, not all credit card processors require a merchant account.

Some credit card machines are compatible with tablets, but the most common way to accept credit cards with an iPhone, iPad, Android or other mobile device is by using a credit card swiper. This small dongle attaches to the headphone or auxiliary plug on a mobile phone or tablet, and processes credit cards using a mobile app. Another way to accept credit cards using a mobile device is by using a virtual terminal: A feature that lets you manually input credit cards into the app.

NFC technology allows businesses to accept credit cards without swiping them. To accept mobile payments with EMV technology, you’ll need an NFC-enabled credit card machine – such as Apple Pay, Android Pay or Samsung Pay.

EMV technology aims to defend both the consumers and your business from credit card fraud and cyberattacks. It also protects your company from liability in the event of a credit-card-related security breach. Traditional credit card swipers read the magnetic stripe on the back of credit cards. For better security, EMV reads a chip embedded in new credit cards. Most new credit card machines are equipped with both an EMV chip reader and a traditional credit card swiper.

The two main security features to look for in a credit card machine and credit card processor are data security standard – also known as the Payment Card Industry Data Security Standard (PCI DSS) – and EMV capabilities. PCI DSS consists of several security measures, including point-to-point data encryption. Although credit card processors have PCI DSS as a part of their service, it is your responsibility to make sure they are compliant to protect sensitive information and avoid hefty fees. [Read related article:Accepting Credit Cards? PCI Compliance a Concern for Small Businesses]

As with most banking transactions, credit card funds go through an automated clearinghouse (ACH), and transactions are typically completed within two business days. There may be delays in some cases, usually because of holds by banks or chargebacks. Each credit card processor and bank has its own policies, so be sure to read the fine print regarding holds on funds.

Generally, yes, you can still get a credit card machine if you have bad credit. However, many credit card processors consider your personal credit when processing merchant account applications. If you want to obtain a credit card machine and you have low or bad credit, look for a credit card processor that either doesn’t require a merchant account or specializes in high-risk applicants.

There’s certainly no shortage of options for consumers looking to open an account with a major credit agency, a preferred brand or a favorite store. Here are just a few of the card types your customers may use to make purchases:Consumer credit cards: These are the most common credit cards issued. Consumers can obtain these credit cards from a number of preferred brands and services, such as an airline or online shopping platform. Oftentimes, these cards offer special deals on select products and services.

Business credit cards: These credit cards cater to the needs of your growing business, offering high lines of credit and the ability to authorize employees. They often include special offers tailored to the industry.

Student credit cards:Student credit cards typically come with offers specific to young people, have lower credit limits, and are generally unsecured, which means they don’t require a deposit to be opened.

If you are looking for window decals or decals for your check-out counter, POS Supply Solutions has several options for you. Show the public that you accept Visa, MasterCard, American Express, Discover and Diners Club. Even if you only accept Visa and MasterCard, the decals are laid out in such a way that you can easily remove Discover and Diners Club without losing the borders.

We stay up to date on POS and Credit Card trends so YOU can focus on being the best at YOUR business. POS systems and Credit Card processing are highly technical. There’s never enough time for you to become an expert in everything. Let us be your trusted advisor in these complex areas of your business. We’ve been successfully serving the Carolinas since 1997.

Credit Card Pin Pads go hand-in-hand with your POS system. Connect EMV payments with your point-of-sale system. These units must be plugged in to work with your system. You can find contactless payment options in each of our new models.

A compact, secure and ruggedized credit card terminal capable of processing payments with a variety of connectivity options. Equipped with a 32-Bit ARM9 CPU, large memory, and a high-speed thermal printer, the S-80 is an ideal payment device for use in banking, large retail, hospitality, food service, and convenience stores.

The A920 combines the full features of an Android tablet with a powerful payment terminal, all in a sleek and compact design. The A920 delivers an integrated camera, high-speed thermal printer, and high-capacity battery to meet the daily demands across all dynamic Retail or Hospitality environments.

This credit card pin pad fits comfortably into the palm of your hand, offering everything merchants could want in a sleek, stylish payment device. Providing unsurpassed security and reliability and redefining the classic PIN pad, the SP30 offers the smallest footprint in two configurations: as a terminal connected to a Point-of-Sale (POS) or as an accessory PIN pad device that connects to a PAX payment terminal such as the A80. Its high-speed processor and large memory support a broad range of payment and value-added applications. The SP30 offers a built-in contactless card reader, a magnetic card reader, and an IC card reader.

Robust and optimized for fast checkout, the iPP 320 is designed to meet the needs of intense retail environments. It is compact, requires minimum counter space and provides easy handling. A large 15-key backlit keypad, LCD display and function keys allow comfortable, convenient interactions. In addition to accepting EMV chip & PIN, magstripe, and NFC/contactless payments, the iPP 320 also supports new NFC technologies, such as loyalty, and wallets.

features a sleek and ergonomic design, with intuitive ATM-style interface and large keypad to make it look as good as it feels. Includes PCI 3.X approval, EMV compliance, and VeriShield Total Protect, which delivers end-to-end encryption and tokenization.With its blazing-fast processor, the VX 805 PIN pad can handle even the most complex and demanding transactions.

Just under 4 inches, Dynamag saves space on the countertop or in your custom build and still provides a long swipe path. Dynamag card reader supports USB HID or USB Keyboard emulation interfaces and is powered and connected via USB.

Incorporate cutting-edge payment systems into your restaurant or retail business with the chip credit card readers and pin pads for sale from Total Merchant Supply. Visit us today and let our expert team set you up with the POS pin pad and contactless card reader system to enhance your business.

Apple Pay allows you to make easy, secure, and private transactions in stores, in apps, and on the web. You can also send and receive money with friends and family using Apple Pay in Messages (U.S. only). And with contactless rewards cards in Wallet, you can receive and redeem rewards when paying with Apple Pay. Apple Pay is designed with your security and privacy in mind, making it a simpler and more secure way to pay than using your physical credit, debit, and prepaid cards.

Apple Pay is also designed to protect your personal information. Apple doesn’t store or have access to the original credit, debit, or prepaid card numbers that you use with Apple Pay. And when you use Apple Pay with credit, debit, or prepaid cards, Apple doesn"t retain any transaction information that can be tied back to you—your transactions stay between you, the merchant or developer, and your bank or card issuer.

When you add a credit, debit, prepaid, or transit card (where available) to Apple Pay, information that you enter on your device is encrypted and sent to Apple servers. If you use the camera to enter the card information, the information is never saved on your device or photo library.

Apple decrypts the data, determines your card’s payment network, and re-encrypts the data with a key that only your payment network (or any providers authorized by your card issuer for provisioning and token services) can unlock.

Information that you provide about your card, whether certain device settings are enabled, and device use patterns—such as the percent of time the device is in motion and the approximate number of calls you make per week—may be sent to Apple to determine your eligibility to enable Apple Pay. Information may also be provided by Apple to your card issuer, payment network, or any providers authorized by your card issuer to enable Apple Pay, to determine the eligibility of your card, to set up your card with Apple Pay, and to prevent fraud.

After your card is approved, your bank, your bank’s authorized service provider, or your card issuer creates a device-specific Device Account Number, encrypts it, and sends it along with other data (such as the key used to generate dynamic security codes that are unique to each transaction) to Apple. The Device Account Number can’t be decrypted by Apple but is stored in the Secure Element—an industry-standard, certified chip designed to store your payment information safely—on your device. Unlike with usual credit or debit card numbers, the card issuer can prevent its use on a magnetic stripe card, over the phone, or on websites. The Device Account Number in the Secure Element is isolated from iOS, watchOS, and macOS, is never stored on Apple servers, and is never backed up to iCloud.

Apple doesn’t store or have access to the original card numbers of credit, debit, or prepaid cards that you add to Apple Pay. Apple Pay stores only a portion of your actual card numbers and a portion of your Device Account Numbers, along with a card description. Your cards are associated with your Apple ID to help you add and manage your cards across your devices.

When you use Apple Pay in stores that accept contactless payments, Apple Pay uses Near Field Communication (NFC) technology between your device and the payment terminal. NFC is an industry-standard, contactless technology that’s designed to work only across short distances. If your iPhone is on and detects an NFC field, it will present you with your default card. To send your payment information, you must authenticate using Face ID, Touch ID, or your passcode (except in Japan if you designate a Suica card for Express Transit). With Face ID or with Apple Watch, you must double-click the side button when the device is unlocked to activate your default card for payment.

After you authenticate your transaction, the Secure Element provides your Device Account Number and a transaction-specific dynamic security code to the store’s point of sale terminal along with additional information needed to complete the transaction. Again, neither Apple nor your device sends your actual payment card number. Before they approve the payment, your bank, card issuer, or payment network can verify your payment information by checking the dynamic security code to make sure that it’s unique and tied to your device.

To securely transmit your payment information when you pay in apps or on the web, Apple Pay receives your encrypted transaction and re-encrypts it with a developer-specific key before the transaction information is sent to the developer or payment processor. This key helps ensure that only the app or the website that you’re purchasing from can access your encrypted payment information. Websites must verify their domain every time they offer Apple Pay as a payment option. Like with in-store payments, Apple sends your Device Account Number to the app or website along with the transaction-specific dynamic security code. Neither Apple nor your device sends your actual payment card number to the app.

When you add contactless rewards cards to Wallet, all the information is stored on your device and encrypted with your passcode. You can choose to have a rewards card automatically presented for use in the merchant’s stores when you make an Apple Pay purchase (or you can turn off this setting in Wallet). Apple requires all information sent to the payment terminal to be encrypted. Rewards card information is sent only with your authorization. And Apple doesn’t receive any information about the rewards transaction other than what"s displayed on the pass. iCloud backs up your cards and keeps your rewards cards up-to-date on multiple devices.

If you sign up for a rewards card and provide information to the merchant, such as your name, postal code, email address, and phone number, Apple will receive notification of the signup, but the information that you share will be sent directly from your device to the merchant and is treated in accordance with the merchant’s privacy policy.

If you turned on Find My iPhone on your device, you can suspend Apple Pay by placing your device in Lost Mode instead of immediately canceling your cards. If you find your device, you can reenable Apple Pay.

You can go to your Apple ID account page to remove the ability to make payments with the credit, debit, and prepaid cards that you were using with Apple Pay on the device.

Erasing your device remotely using Find My iPhone also removes the ability to pay with the cards that you were using with Apple Pay. Your credit, debit, and prepaid cards will be suspended from Apple Pay by your bank, your bank’s authorized service provider, your card issuer, or your issuer"s authorized service provider, even if your device is offline and not connected to a cellular or Wi-Fi network. If you find your device, you can add the cards again using Wallet.

In addition, you can call your bank or issuer to suspend your credit, debit, or prepaid cards from Apple Pay. Suica cards can"t be suspended if your device is offline (more information below). The ability to use rewards cards stored on your device is removed only if or when your device is online.

Apple Pay allows you to send and receive money with other people in Messages. When you receive money, it’s added to your Apple Pay Cash card that can be used to make purchases using Apple Pay in stores, in apps, and on the web. Person to person payments and the Apple Pay Cash card are services provided by Apple’s partner bank, Green Dot Bank, member FDIC. You can learn how Green Dot Bank protects your information by reviewing their privacy policy at applepaycash.greendot.com/privacy/.

When you set up Apple Pay Cash, the same information as when you add a credit or debit card may be shared with Green Dot Bank and with Apple Payments Inc. Apple created Apple Payments Inc., a wholly-owned subsidiary, to protect your privacy by storing and processing information about your Apple Pay Cash transactions separately from the rest of Apple, in a way that the rest of Apple doesn’t know. This information is used only for troubleshooting, regulatory purposes, and to prevent fraud for Apple Pay Cash.

To verify your identity, you may be asked to provide information including your name and address to the bank and their identity verification service provider. This information is used only for fraud prevention and to comply with U.S. financial regulations. Your name and address is securely stored by the partner bank and Apple Payments Inc., but any additional information that you’re asked to provide—such as social security number, date of birth, answers to questions (e.g., confirm street name you have previously lived on), or a copy of your government ID—can’t be read by Apple.

When you use Apple Pay Cash—including when you add money or transfer money to a bank account—our partner bank, Apple, and Apple Payments Inc. may use and store information about you, your device, and your account to process the transaction, for troubleshooting, to help prevent fraud, and to comply with financial regulations. Apple may provide Apple Payments Inc. with approximate use patterns from your device about how frequently you communicate with that person by phone, email, or in Messages. The content of your communication isn’t collected. This information is stored for a limited time, and in such a way that it is not linked to you unless the associated transaction is determined to require further analysis due to suspicious activity. You can view transactions that required further analysis in the list of your Apple Pay Cash card transactions.

If you designate a transit card that you added to Apple Pay as an Express Transit card, you can pay and ride without having to use Face ID, Touch ID, or a passcode first. You can manage Express Transit on your iPhone in Settings > Wallet & Apple Pay, and on your Apple Watch via the Apple Watch app.

You can temporarily suspend transit cards by using Find My iPhone to place your device into Lost Mode. Or you can remove transit cards by erasing your device remotely using Find My iPhone or by removing all cards from your Apple ID account page. Transit cards can"t be removed or suspended if your device is offline.

We have a wide variety of credit card terminals and POS systems designed to fit your needs and boost your bottom line. The revolutionary Clover™ Station Solo, for example, can transform the way you work by helping you track inventory, manage employees, drive customer loyalty, and accept payments all on a single, dynamic system.

Experience easy Internet set-up for all POS systems using your existing broadband connection. Most of these card terminals can also connect wirelessly

Because more and more consumers depend on payment options other than cash, it is critical for businesses of all sizes to have convenient and reliable POS terminals that can handle today’s increasingly diverse payment needs. Fiserv’s credit card machines can support all of the most popular payment options out there – including chip, magstripe, and contactless payments made via mobile or NFC-enabled devices.

With no upfront investment, you can pay for any of these powerful point-of-sale terminals out of your cash flow, and preserve your working capital and available credit.

Our Clover Station Solo can help lighten your workload. It is an all-in-one POS and payments system that can simplify your operations – allowing you to focus more on doing what you love. The Clover Station Solo can transform the way you work by accepting payments, tracking inventory, managing employees, and driving customer loyalty all within your POS system.

The Clover Mini is a small, yet powerful POS system. As your business grows, your Clover Mini can grow with it. You"ll be able to accept all types of payments, including EMV® chip and contactless payments. You can also set up a customer loyalty program and run your business on cloud-based software so you can access your information from any device. This pint-sized POS system can help turn business insights into actionable data.

The Clover Flex is all about making your payment solutions flexible enough to meet the demands of your ever-growing business. You’ll be able to take payments such as magnetic stripe, EMV chip, standard credit and debit cards, and contactless payments.

Because all of our wireless POS systems come with Wi-Fi and LTE connectivity, Clover Flex lets you do business from any location. Better still, you can protect your customers and your business from fraud with built-in Clover Security.Learn More >>

Clover Go is an all-in-one credit card reader that can handle contactless, chip, and swipe payments – including Apple PayTM, Samsung Pay, and Android PayTM – right from your smartphone or tablet. These super portable card machines are ready to go right out of the box. Just charge, pair with your iOS or Android device, download the Clover Go app, and you’re ready to go!

All your transactions are backed with Clover Security data protection. The web dashboard from Clover will allow you to manage your business from anywhere you have an Internet connection.

Your single source for end-to-end, secure and scalable point-of-sale (POS) systems and credit card machines. We offer equipment, key injection, programming, repairs and financing. Our consultative and customized approach helps your business grow by leveraging the most innovative and cost-effective payment and POS solutions available in North America.

The FD150 gives you a full range of solutions for payment processing including EMV, contactless, debit cards, gift cards and EBT secured with PCI compliance level 5 protection.

The RP10 companion device to the FD150 accepts PIN and signature debit cards, credit cards, EMV cards, gift cards, EBT, STAR® Network, and contactless transactions.

Give your customers peace of mind by allowing them to stay in control of their cards, reduce physical touchpoints with employees, and take advantage of level 5 PCI compliance.

This powerful all-in-one advanced countertop device is part of the Verifone® Engage portfolio. The V400cPlus combines the latest features, functionality, and performance into an efficient, high-end solution. It has built-in PIN, chip and NFC/contactless functionality that simplifies and centralizes payment acceptance into one device. It meets the demand for smart, easy-to-use, credit card machines.

The V200c’s ergonomic design with tactile keyboard and hard cap keys for added durability makes it ideal for both customer and merchant use. As part of the Verifone® Engage portfolio, it combines the latest features, functionality, and performance into an efficient, affordable, all-in-one countertop POS terminal.

The P200’s sleek design and vibrant user interface enhance the shopping experience while pairing with the V400c or V200c for a unified consumer-facing solution. It’s a fast, cost-effective, lightweight, multipayment acceptance PIN pad.

The V400m is an all-in-one PIN, chip, and contactless device that simplifies and centralizes payments. With wireless connectivity, the V400m enables absolute portability, making it ideal for pay at the table, curbside transactions, kiosks, and line busting.

With Fiserv, there are no upfront investments for any of our credit card machines – and you can pay for your equipment out of your existing cash flow. This allows you to preserve your working capital and available credit so you can continue to focus on growing your business. Fiserv also offers fixed, affordable monthly payments and flexible term options whenever you lease any of our point-of-sale terminals.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey