lcd panel production cost made in china

China is the leader in producing LCD display panels, with a forecast capacity share of 56 percent in 2020. China"s share is expected to increase in the coming years, stabilizing at 69 percent from 2023 onwards.Read moreLCD panel production capacity share from 2016 to 2025, by countryCharacteristicChinaJapanSouth KoreaTaiwan-----

DSCC. (June 8, 2020). LCD panel production capacity share from 2016 to 2025, by country [Graph]. In Statista. Retrieved January 07, 2023, from https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. "LCD panel production capacity share from 2016 to 2025, by country." Chart. June 8, 2020. Statista. Accessed January 07, 2023. https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. (2020). LCD panel production capacity share from 2016 to 2025, by country. Statista. Statista Inc.. Accessed: January 07, 2023. https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. "Lcd Panel Production Capacity Share from 2016 to 2025, by Country." Statista, Statista Inc., 8 Jun 2020, https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC, LCD panel production capacity share from 2016 to 2025, by country Statista, https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/ (last visited January 07, 2023)

Panel makers are cutting production by 16 percent on average from this month, Rong Chaoping, senior researcher at market research firm AVC Revo, told Yicai Global. Television panel makers are expected to ship 3.6 million less panels than last month.

Panel makers will reduce capacity by between 15 and 20 percent this month, said Wu Rongbing, chief analyst at Chinese semiconductor intelligence service Omdia.

TCL China Star intends to continue with its production cuts until September, while Beijing-based BOE and HKC Optoelectronics Technology have not yet decided how long they will reduce output, Rong said. None of the three companies responded when contacted by Yicai Global.

LCD TV display shipments from China’s five largest panel manufacturers accounted for 68.5 percent of the global market in April, a new high, and they were expected to exceed 70 percent this year, according to Omdia.

The global panel industry is expected to slash production by about 20 percent this year, according to Beijing-based Sigmaintell. It is the first time since 2013 that the worldwide sector has implemented such a large-scale and wide-ranging cut in manufacturing. But it should help to slow the fall in prices, Li said.

“Tumbling prices are squeezing profits,” Li said. “The price of a TV panel is now below cost price and that of some data panels is also below the manufacturing cost.”

“Panel makers are facing rising liquidity pressure and bigger losses as prices are now below cost price, so the display industry is likely to undergo another big reshuffle,” Rong said.

Panel prices are likely to stop dropping this month or next as output falls, Wu said. Whether prices will start to pick up soon depends on when demand improves.

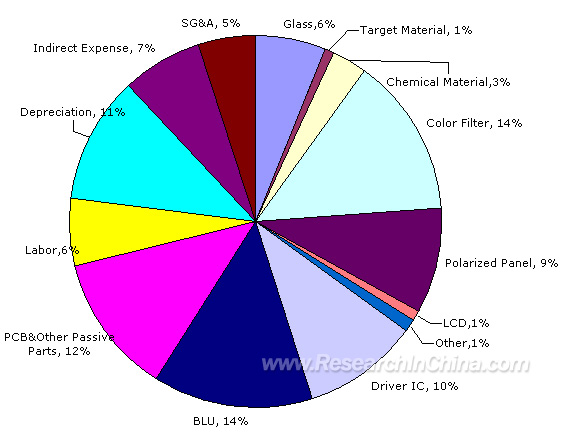

Introduction: Global LCD industry shift and automotive intelligence together to promote the rapid development of China’s LCD panel industry, which will bring a continuous increase in demand for backlight modules, China’s backlight module industry has greater potential for development.

LCD panel backlight module consists of a backlight light source, light guide, optical film, and a plastic frame, which is an important component of LCD display panel. As the backlight module has technology-intensive and labor-intensive attributes, with abundant high-skilled labor advantage China is attracting the global LCD panel industry to the domestic rapid transfer.

From LCD application to the present, the global LCD panel industry capacity transfer has gone through three periods, 2000 Japan dominated the global LCD industry; 2000 – 2010, Japan’s production capacity to South Korea and Taiwan; 2010 to the present, Japanese manufacturers gradually withdraw from the LCD panel industry, production capacity began to transfer to mainland China, so far, mainland China LCD production capacity has occupied the global half of the world.

In recent years, South Korea’s Samsung and LG display will shift their business focus to OLED, and will gradually shut down their LCD production lines and withdraw from the LCD panel industry; at the time of South Korean manufacturers’ withdrawal, domestic enterprises are stepping up new construction to expand LCD production capacity.

BOE, Huaxing photoelectric, Huike, CEC in 2020 – 2021, a total of eight 7 generation LCD production lines completed and put into operation, and domestic panel manufacturers have further expansion plans, the next few years domestic LCD production capacity will continue to increase.

LCD panel manufacturers tend to choose the nearby supporting module suppliers for the safety of the key component supply chain and cost reduction considerations. LCD panel production capacity transfer to China will bring opportunities to domestic backlight module manufacturers and drive the development of the domestic backlight module industry.

The future of the car will pay more attention to the human driving experience, to the intelligent development, which will bring the increasing demand for car display. On the one hand, the number of car displays gradually increased, for example, the instrument panel, rearview mirror, central control platform more to display the way, the passenger and rear position with entertainment display. On the other hand, the car display is constantly to a large screen, multi-screen development, especially in high-end models, the large display has become standard, for example, Tesla Model S screen size of 17 inches, Mercedes-Benz A-class car configuration of two 10.5-inch display.

According to the terminal application size, backlight module can be divided into large, medium, and small size, of which small size backlight module is mainly used in smartphones, wearable devices, and other terminals, the medium size used in notebook computers, tablet PCs, car screens and other terminals, the large size is mainly used in LCD TV.

From the industry development trend, smartphone display is transitioning to OLED, LCD TV market is gradually saturated, the future of large size and small size backlight module market potential is relatively small; and the future of the car display market potential is huge, by the backlight module manufacturers are unanimously optimistic, are currently accelerating the layout ( see Table 2 ). Focusing on the traditional medium-sized backlight module field, Hanbo Hi-Tech and Weishi Electronics have significant advantages in core technology patents, downstream customer resources, process experience accumulation, production costs, etc., and have more development advantages in the future.

The current global LCD display panel industry is rapidly moving to China, which brings development opportunities to China’s backlight module industry. In addition, automotive intelligence will also bring a continuous increase in demand for medium-sized car displays, the first to enter the field of medium-sized backlight module manufacturers with its customer resources, core technology, scale efficiency, and other advantages will be more beneficial.

LCD manufacturers are mainly located in China, Taiwan, Korea, Japan. Almost all the lcd or TFT manufacturers have built or moved their lcd plants to China on the past decades. Top TFT lcd and oled display manufactuers including BOE, COST, Tianma, IVO from China mainland, and Innolux, AUO from Tianwan, but they have established factories in China mainland as well, and other small-middium sizes lcd manufacturers in China.

China flat display revenue has reached to Sixty billion US Dollars from 2020. there are 35 tft lcd lines (higher than 6 generation lines) in China,China is the best place for seeking the lcd manufacturers.

The first half of 2021, BOE revenue has been reached to twenty billion US dollars, increased more than 90% than thesame time of 2020, the main revenue is from TFT LCD, AMoled. BOE flexible amoled screens" output have been reach to 25KK pcs at the first half of 2021.the new display group Micro LED revenue has been increased to 0.25% of the total revenue as well.

Established in 1993 BOE Technology Group Co. Ltd. is the top1 tft lcd manufacturers in China, headquarter in Beijing, China, BOE has 4 lines of G6 AMOLED production lines that can make flexible OLED, BOE is the authorized screen supplier of Apple, Huawei, Xiaomi, etc,the first G10.5 TFT line is made in BOE.BOE main products is in large sizes of tft lcd panel,the maximum lcd sizes what BOE made is up to 110 inch tft panel, 8k resolution. BOE is the bigger supplier for flexible AM OLED in China.

Technology Co., Ltd), established in 2009. CSOT is the company from TCL, CSOT has eight tft LCD panel plants, four tft lcd modules plants in Shenzhen, Wuhan, Huizhou, Suzhou, Guangzhou and in India. CSOTproviding panels and modules for TV and mobile

three decades.Tianma is the leader of small to medium size displays in technologyin China. Tianma have the tft panel factories in Shenzhen, Shanhai, Chendu, Xiamen city, Tianma"s Shenzhen factory could make the monochrome lcd panel and LCD module, TFT LCD module, TFT touch screen module. Tianma is top 1 manufactures in Automotive display screen and LTPS TFT panel.

Tianma and BOE are the top grade lcd manufacturers in China, because they are big lcd manufacturers, their minimum order quantity would be reached 30k pcs MOQ for small sizes lcd panel. price is also top grade, it might be more expensive 50%~80% than the market price.

Panda electronics is established in 1936, located in Nanjing, Jiangshu, China. Panda has a G6 and G8.6 TFT panel lines (bought from Sharp). The TFT panel technologies are mainly from Sharp, but its technology is not compliance to the other tft panels from other tft manufactures, it lead to the capacity efficiency is lower than other tft panel manufacturers. the latest news in 2022, Panda might be bougt to BOE in this year.

Established in 2005, IVO is located in Kunsan,Jiangshu province, China, IVO have more than 3000 employee, 400 R&D employee, IVO have a G-5 tft panel production line, IVO products are including tft panel for notebook, automotive display, smart phone screen. 60% of IVO tft panel is for notebook application (TOP 6 in the worldwide), 23% for smart phone, 11% for automotive.

Besides the lcd manufacturers from China mainland,inGreater China region,there are other lcd manufacturers in Taiwan,even they started from Taiwan, they all have built the lcd plants in China mainland as well,let"s see the lcd manufacturers in Taiwan:

Innolux"s 14 plants in Taiwan possess a complete range of 3.5G, 4G, 4.5G, 5G, 6G, 7.5G, and 8.5G-8.6G production line in Taiwan and China mainland, offering a full range of large/medium/small LCD panels and touch-control screens.including 4K2K ultra-high resolution, 3D naked eye, IGZO, LTPS, AMOLED, OLED, and touch-control solutions,full range of TFT LCD panel modules and touch panels, including TV panels, desktop monitors, notebook computer panels, small and medium-sized panels, and medical and automotive panels.

AUO is the tft lcd panel manufacturers in Taiwan,AUO has the lcd factories in Tianma and China mainland,AUOOffer the full range of display products with industry-leading display technology,such as 8K4K resolution TFT lcd panel, wide color gamut, high dynamic range, mini LED backlight, ultra high refresh rate, ultra high brightness and low power consumption. AUO is also actively developing curved, super slim, bezel-less, extreme narrow bezel and free-form technologies that boast aesthetic beauty in terms of design.Micro LED, flexible and foldable AMOLED, and fingerprint sensing technologies were also developed for people to enjoy a new smart living experience.

Hannstar was found in 1998 in Taiwan, Hannstar display hasG5.3 TFT-LCD factory in Tainan and the Nanjing LCM/Touch factories, providing various products and focus on the vertical integration of industrial resources, creating new products for future applications and business models.

driver, backlight etc ,then make it to tft lcd module. so its price is also more expensive than many other lcd module manufacturers in China mainland.

Maclight is a China based display company, located in Shenzhen, China. ISO9001 certified, as a company that more than 10 years working experiences in display, Maclight has the good relationship with top tft panel manufacturers, it guarantee that we could provide a long term stable supply in our products, we commit our products with reliable quality and competitive prices.

Maclight products included monochrome lcd, TFT lcd module and OLED display, touch screen module, Maclight is special in custom lcd display, Sunlight readable tft lcd module, tft lcd with capacitive touch screen. Maclight is the leader of round lcd display. Maclight is also the long term supplier for many lcd companies in USA and Europe.

If you want tobuy lcd moduleorbuy tft screenfrom China with good quality and competitive price, Maclight would be a best choice for your glowing business.

LCD panel prices have risen for 4 months in a row because of your home gaming? Since this year, the whole LCD panel market smoke. Whether after the outbreak of the epidemic, LCD panel market prices rose for four months, or the panel giants in Japan and South Korea successively sold production lines, or the Chinese mainland listed companies frequently integrated acquisition, investment, and plant construction, all make the industry full of interesting.

LCD panel pricesare already a fact. Since May this year, LCD panel prices have risen for four months in a row, making the whole industry chain dynamic. Why are LCD panels going up in price in a volatile 2020? The key factor lies in the imbalance between supply and demand.

The price of LCDS for large-size TVs of 70 inches or more hasn"t budged much. In addition, LTPS screens and AMOLED screens used in high-end phones have seen little or no increase in price.

As for October, LCD panel price increases are expected to moderate. The data shows that in October 32 inches or 2 dollars; Gains of 39.5 to 43 inches will shrink to $3;55 inches will fall back below $10; The 65-inch gain will narrow to $5.

During the epidemic, people stayed at home and had no way to go out for entertainment. They relied on TV sets, PCS, and game consoles for entertainment. After the resumption of economic work and production, the market of traditional home appliances picked up rapidly, and LCD production capacity was quickly digested.

However, due to the shutdown of most factories lasting 1-2 months during the epidemic period, LCD panel production capacity was limited, leading to insufficient production capacity in the face of the market outbreak, which eventually led to the market shortage and price increase for 4 consecutive months.

In fact, the last round of price rise of LCD panel was from 2016 to 2017, and its overall market price has continued to fall since 2018. Even in 2019, individual types have fallen below the material cost, and the whole industry has experienced a general operating loss. As a result, LCD makers have been looking for ways to improve margins since last year.

A return to a reasonable price range is the most talked about topic among panel makers in 2019, according to one practitioner. Some manufacturers for the serious loss of the product made the decision to reduce production or even stop production; Some manufacturers planned to raise the price, but due to the epidemic in 2020, the downstream demand was temporarily suppressed and the price increase was postponed. After the outbreak was contained in April, LCD prices began to rise in mid-to-late May.

In fact, the market price of LCD panels continued to decline in 2018-2019 because of the accelerated rise of China"s LCD industry and the influx of a large number of local manufacturers, which doubled the global LCD panel production capacity within a few years, but there was no suitable application market to absorb it. The result of excess capacity is oversupply, ultimately making LCD panel prices remain depressed.

Against this background, combined with the impact of the epidemic in 2020, the operating burden of LCD companies in Japan and South Korea has been further aggravated, and it is difficult to make profits in the production of LCD panels, so they have to announce the withdrawal of LCD business.

business in June 2022. In August, Sharp bought JDI Baishan, a plant in Ishikawa prefecture that makes liquid crystal display panels for smartphones. In early September, Samsung Display sold a majority stake in its SUZHOU LCD production plant to Starlight Electronics Technology, a unit of TCL Technology Group. LGD has not only pulled out of some of its production capacity but has announced that it will close its local production line in 2020. According to DSCC, a consultancy, the share of LCD production capacity in South Korea alone will fall from 19% to 7% between 2020 and 2021.

It is worth mentioning that in industry analysis, in view of the fact that Korean companies are good at using "dig through old bonus - selling high price - the development of new technology" the cycle of development mode, another 2020 out of the LCD production capacity, the main reason may be: taking the advantage of China"s expanding aggressively LCD manufacturers, Korean companies will own LCD panel production line hot sell, eliminating capacity liquid to extract its final value, and turning to the more profitable advantage of a new generation of display technologies, such as thinner, color display better OLED, etc. Samsung, for example, has captured more than 80% of the OLED market with its first-mover advantage.

From the perspective of production capacity, the launch of LCD tracks by major manufacturers in Japan and South Korea must reduce some production capacity in the short term, which to some extent induces market price fluctuations. In the long run, some of the Japanese and Korean LCD production capacity has been bought by Chinese manufacturers, coupled with frequent investment in recent years, the overall capacity is sure to recover as before, or even more than before. But now it will take time to expand the production layout, more or less will cause supply imbalance, the industry needs to be cautious.

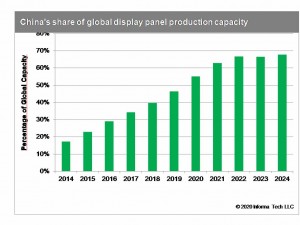

The LCD panel industry started in the United States and then gradually moved to Japan, South Korea, China, and Taiwan. At present, the proportion of production capacity in The Chinese mainland has reached 52% in 2020, and there are leading LCD panel products in China represented by BOE, Huxing Optoelectronics. Meanwhile, the production capacity layout of BOE, Huike, Huxing Optoelectronics, and other manufacturers has been basically completed, making industrial integration a necessity.

On the one hand, South Korean enterprises out of the LCD track, the domestic factory horse enclosure, plant expansion action. While LCDs may not sell as well as "upstart" flexible screens, respondents believe they are still strong enough in the traditional home appliance market to warrant continued investment. Zhao Bin, general manager of TCL Huaxing Development Center, has said publicly that the next-generation display technology will be mature in four to five years, but the commercialization of products may not take place until a decade later. "LCD will still be the mainstream in this decade," he said.

On the other hand, there is no risk of neck jam in China"s LCD panel industry, which is generally controllable. In mainland China, there will be 21 production lines capable of producing 32-inch or larger LCD panels by 2021, accounting for about two-thirds of the global total. In terms of the proportion of production capacity, the Chinese mainland accounted for 42% of the global LCD panel in 2019, 51% this year, and will continue to climb to 63% next year.

Of course, building factories and expanding production cannot be accomplished overnight. In the process of production capacity recovery, it is predicted that there will be several price fluctuations, and the cost may be passed on to the downstream LCD panel manufacturers or consumers when the price rises greatly, which requires continuous attention.

Chinese display manufacturers are chasing their South Korean rivals closely by planning to release a larger volume of liquid-crystal panels over 32 inches this year, said a market researcher Sunday.

According to a report on the 2017 shipment strategies of Chinese TV panel makers by IHS Markit, Chinese LCD panel suppliers are forecast to ship out a total of 320,000 large-size panels larger than 32 inches by the end of this year, a 33 percent surge from last year.

In the report, Wu mentioned the plans of major Chinese panel firms such as BOE, CSOT, CEC-Panda and HKC to focus on expanding production of 43, 55 and 58-inch panels, adding that demand for 32-inch panels will gradually decrease.

“By the end of 2018, China will be the largest region for TFT LCD capacity, and larger-sized products may make their factories more efficient and profitable than they have been when producing 32-inch panels,” he said.

“The strategies of Chinese panel makers will significantly influence global supply and demand,” Wu said. “In 2015 and 2016, the Chinese companies shipped 33.2 percent of worldwide LCD TV panel, trailing only Korean panel makers at 36.4 percent.”

The competition structure has been advantageous for the Korean players, since their Chinese rivals had been focusing on small LCD panels until last year. But now the Korean firms are facing fiercer competition in prices.

Although demand for organic-light emitting diode panels in the TV market is gradually rising, dominance of LCD panels is projected to continue for the foreseeable future.

“While OLEDs are expected to post sharp growth, they will not be able to usurp LCD as the panels of choice for upper-end TVs,” another report by IHS Markit said.

Chinese display panel makers accounted for nearly half of the share in the global liquid crystal display TV panel market in the first half of this year, dominating the industry.

Beijing-based market researcher Sigmaintell Consulting said shipments of LCD TV panels worldwide totaled 140 million pieces in the year"s first half, up 3.6 percent compared with the same period a year ago.

The supply of TV panels though has surpassed demand due to the slowdown in the global economy and weaker consumer purchasing power. Manufacturers are facing severe challenges from falling panel prices, the Sigmaintell report said.

The shipment of BOE"s LCD TV panels stood at 27.6 million in the Jan-June period while LG Display followed with 22.7 million, down 4.5 percent year-on-year. Innolux Display Group was in third place, having shipped 21.9 million units.

Shenzhen China Star Optoelectronics Technology Co Ltd, a subsidiary of consumer electronics giant TCL Corp, ranked fourth, shipping 19.3 million pieces of TV panels. Chinese panel makers accounted for a 45.8 percent share in the global LCD TV panel market.

Sigmaintell estimated that the gap between supply and demand would widen further, and the panel market may face a long-term risk of oversupply. The industry may have to undergo a reshuffle given fierce market competition, it said.

The panel makers must reduce costs, optimize their internal structures, promote technological innovation and explore more innovative applications, the report by the consultancy said.

Separately, BOE"s Gen 10.5 TFTLCD production line has entered operation in Hefei, Anhui province. The plant will produce high-definition LCD screens of 65 inches and above.

CSOT also announced in November last year that its Gen 11 TFT-LCD and active-matrix OLED production line had officially began operation. The project will produce 43-inch, 65-inch and 75-inch liquid crystal display screens.

China is expected to replace South Korea as the world"s largest flat-panel display producer in 2019, a report from the China Video Industry Association and the China Optics and Optoelectronics Manufacturers Association said.

"The average size of TV panels is likely to increase 1.4 inches in 2019. The 65-inch dimension will become the most popular size of TV," Li Yaqin, general manager of Sigmaintell, said while adding the 65-inch TV will become the mainstream screen in people"s living rooms in the future.

Compared with traditional LCD display panels, OLED has a fast response rate, wide viewing angles, high-contrast images and richer colors. It is thinner and can be made flexible.

BOE Technology Group and TCL China Star Optoelectronics Technology (TCL CSOT) are among the Chinese panel makers to have ramped up output since around 2019 with generous state subsidies. China is gaining on South Korea, whose share of capacity is seen reaching 55% for 2022 in an October estimate by U.S. market intelligence firm Display Supply Chain Consultants (DSCC).

TOKYO -- China is expanding its presence in the field of key components for the electronics industry, such as liquid crystal display panels and semiconductors. In China, seven state-of-the-art LCD panel factories will come onstream over the next three years, and there has emerged a plan to construct one of the world"s largest memory chip plants.

LG Display and Samsung Display are struggling to find their ways out of the deterioration of their performance even after withdrawing from production of liquid crystal display (LCD) panels. The high-priced organic light emitting diode (OLED) panel sector regarded as a future growth engine is not growing fast due to the economic downturn. Even in the OLED panel sector, Chinese display makers are within striking distance of Korean display makers, experts say.

On Aug. 30, Display Supply Chain Consultants (DSCC), a market research company, predicted that LCD TV panel prices hit an all-time low in August and that an L-shaped recession will continue in the fourth quarter. According to DSCC, the average price of a 65-inch ultra-high-definition (UHD) panel in August was only US$109, a 62 percent drop from the highest price of US$288 recorded in July in 2021. The average price of a 75-inch UHD panel was only US$218, which was only about half of the highest price of US$410 in July last year. DSCC predicted that the average panel price in the third quarter will fall by 15.7 percent. As Chinese companies’ price war and the effect of stagnation in consumption overlapped, the more LCD panels display makers produce, the more loss they suffer.

As panel prices fell, manufacturers responded by lowering facility utilization rates. DSCC said that the LCD factory utilization rate descended from 87 percent in April to 83 percent in May, 73 percent in June, and 70 percent in July.

Now that the LCD panel business has become no longer lucrative, Korean display makers have shut down their LCD business or shrunk their sizes. In the LCD sector, China has outpaced Korea since 2018. China’s LCD market share reached 50.9 percent in 2021, while that of Korea dropped to 14.4 percent, lower than Taiwan’s 31.6 percent.

Samsung Display already announced its withdrawal from the LCD business in June. Only 10 years have passed since the company was spun off from Samsung Electronics in 2012. LG Display has decided to halt domestic LCD TV panel production until 2023 and reorganize its business structure centering on OLED panels. Its Chinese LCD production line will be gradually converted to produce LCD panels for IT or commercial products. TrendForce predicted that LG Display will stop operating its P7 Plant in the first quarter of next year.

Korean display makers’ waning LCD business led to a situation in which Korea even lost first place in the display industry. Korea with a display market share of 33.2 percent was already overtaken by China with 41.5 percent) in 2021 according to market researcher Omdia and the Korea Display Industry Association. Korea’s market share has never rebounded in for five years since 2017 amid the Korean government’s neglect. Seventeen years have passed since 2004 when Korea overtook Japan to rise to the top of the world in the LCD industry. Korea’s LCD exports amounted to more than US$30 billion in 2014, but fell to US$21.4 billion last year.

A bigger problem is that Korean display makers may lose its leadership in the OLED panel sector although it is still standing at the top spot. While Korea’s OLED market share fell from 98.1 percent in 2016 to 82.8 percent last year, that of China rose from 1.1 percent to 16.6 percent. Considering that the high-end TV market is highly likely to shrink for the time being due to a full-fledged global consumption contraction, some analysts say that the technology gap between Korea and China can be sharply narrowed through this looming TV market slump. According to industry sources, the Chinese government is now focusing on giving subsidies to the development of OLED panel technology rather LCD technology. On the other hand, in Korea, displays were also wiped out from national strategic technology industry items under the Restriction of Special Taxation Act which can receive tax benefits for R&D activities on displays.

AfghanistanAlbaniaAlgeriaAmerican SamoaAndorraAngolaAnguillaAntigua and BarbudaArgentinaArmeniaArubaAscensionAustraliaAustriaAzerbaijanBahamasBahrainBangladeshBarbadosBelarusBelgiumBelizeBeninBermudaBhutanBoliviaBosnia-HercegovinaBotswanaBrazilBritish Indian Ocean TerritoryBruneiBulgariaBurkina FasoBurundiCambodiaCameroonCanadaCape VerdeCayman IslandsCentral African RepublicChadChileChinaChristmas IslandCocos (Keeling) IslandsColombiaComorosCongoCongo, Dem Rep ofCook IslandsCosta RicaCroatiaCubaCyprusCzech RepublicDenmarkDjiboutiDominicaDominican RepublicEast TimorEcuadorEgyptEl SalvadorEquatorial GuineaEritreaEstoniaEthiopiaFalkland IslandsFaroe IslandsFijiFinlandFranceFrench GuianaFrench PolynesiaFrench Southern TerritoriesGabonGambiaGeorgiaGermanyGhanaGibraltarGreeceGreenlandGrenadaGuadeloupeGuamGuatemalaGuineaGuinea-BissauGuyanaHaitiHeard Island and McDonald IsHondurasHungaryIcelandIndiaIndonesiaIranIraqIrelandIsraelItalyIvory CoastJamaicaJapan 曰本JordanKazakhstanKenyaKirgizstanKiribatiKosovoKuwaitLaosLatviaLebanonLeeward IslesLesothoLiberiaLibyaLiechtensteinLithuaniaLuxembourgMacauMacedonia, FYRMadagascarMalawiMalaysiaMaldivesMaliMaltaMarshall IslandsMartiniqueMauritaniaMauritiusMayotteMexicoMicronesia, Fed States ofMoldovaMonacoMongoliaMontenegroMontserratMoroccoMozambiqueMyanmarNamibiaNauruNepalNetherlandsNetherlands AntillesNew CaledoniaNew ZealandNicaraguaNigerNigeriaNorfolk IslandNorth KoreaNorthern Mariana IslandsNorwayOmanPakistanPalauPalestinePanamaPapua New GuineaParaguayPeruPhilippinesPitcairn IslandPolandPortugalPuerto RicoQatarReunionRomaniaRussiaRwandaST MartinSaint HelenaSaint Kitts and NevisSaint LuciaSaint Vincent and GrenadinesSamoaSao Tome and PrincipeSaudi ArabiaSenegalSerbiaSeychellesSierra LeoneSlovakiaSloveniaSolomon IslandsSomaliaSouth AfricaSouth GeorgiaSpainSri LankaSudanSurinameSwazilandSwedenSwitzerlandSyriaTaiwanTajikistanTanzaniaThailandTogoTokelauTongaTrinidad and TobagoTunisiaTurkeyTurkmenistanTurks and Caicos IslandsTuvaluUS Minor Outlying IsUgandaUkraineUnited Arab EmiratesUnited KingdomUruguayUzbekistanVanuatuVenezuelaVietnamVirgin Islands, BritishVirgin Islands, USWallis and FutunaYemenZambiaZimbabwe

China has become the world"s largest LCD panel manufacturing base and is investing in a complete Mini/Micro-LED industry chain. Li Leiguang, JW Insights" chief analyst of the display industry, shared this information at a Mini/Micro-LED industry forum held in Shenzhen in late October.

With over 16 years of experience in the display industry, Li Leiguang has a deep understanding of China"s domestic display industry from materials and panel technologies to industrial policies. He has written industrial research and planning reports for various government departments in Shenzhen, Zhaoqing, Meishan, and Chengdu as well as customized reports for corporate clients in the display industry chain. This article is an excerpt from his speech.

China had long depended on imports of IC and display screens in the manufacturing of display products. IC and display screens are the two pillar sectors of the ICT Industry. The trend has been changing. With the continuous increase of high-generation production lines and capacity of domestic panel manufacturers and the gradual closure of LCD production lines by South Korean manufacturers, China"s LCD panel market share has increased year by year.

In 2020, China achieved a trade surplus in LCD panels for the first time. Meanwhile, the TFT-LCD has become a mainstream choice in the display panel industry after nearly 30 years of development.

JW Insights data shows that China has invested a total of RMB1.2 trillion($187.56 billion) in TFT-LCD and AMOLED panel production lines; Some 50 TFT-LCD and AMOLED panel production lines have been built, with 197 million m2/year TFT-LCD production capacity, 8.9 million m2/year AMOLED production capacity.

China"s LCD production capacity accounted for 50% of the global production capacity in 2020, becoming the world"s largest LCD panel production center; It will reach more than 75% of the world"s total by 2025.

China"s mainland is currently the only region that maintains continuous growth in LCD panel production capacity. With Japanese and South Korean manufacturers gradually withdrawing from the LCD panel, China is becoming the dominant player.

Chinese domestic display panel manufacturers are also embracing new display technologies such as Mini LED, Mirco LED, OLED and Micro OLED (silicon-based OLED), which are in an explosive market growth phase.

Chinese screen manufacturers plan to invest nearly RMB 30 billion($4.7 billion) in silicon-based OLED products lines, with more than 15 planned production lines and the total production capacity equivalent to 95 million units 1-inch screen, according to JW Insights statistics.

Unlike LCD technology that originated overseas, China has kept pace with the world in Mini/Micro-LED and has established a relatively complete industrial chain in it. Currently, the Mini LED is mainly used for LCD panel backlighting; It will be an inevitable trend for the direct LED display with Mini LED in large-screen in the future.

However, TFT-LCD technology will remain the mainstay for a long time in the future, because of its maturity and competitive prices. Multiple display technologies will coexist in the future; Micro-LED panels mass production will not be achieved in the short term.

Faced with a reduced workforce caused by travel bans and quarantine conditions, LCD and OLED fabrication plants (fabs) across China struggled to resume normal operations in early‐ to mid‐February. Chinese LCD fabs were only expected to have a capacity utilization of 70 to 75 percent for the month compared to a normal rate of 90 to 95 percent, according to research from Omdia Display.

That labor challenge was exacerbated further in mid‐to‐late February by bottlenecks in chemical materials and key components such as polarizers and printed circuit boards. “Those materials and component companies are facing the same situation—a shortage of labor, a shortage of logistics support, and the quarantine procedures,” says Omdia Display"s Senior Director David Hsieh. The net result could be as much as a 40 to 50 percent drop in overall display production in China for February, he notes.

The biggest impact is in LCD displays for TVs and notebook computers. By late 2019, the prolonged issue of LCD panel over‐supply driven by Chinese fabs had begun to reverse course as Korean manufacturers restructured their capacity, shutting down some fabs and converting others to OLED production. According to Hsieh, concerns about an LCD panel supply going forward already had spurred some TV manufacturers to increase orders, and now that LCD production in China is slowing as a result of the COVID‐19 outbreak, LCD panel makers are seeking sharp price increases from their original equipment manufacturer (OEM) customers, with a month‐to‐month jump of as much as 10 percent in some cases.

Omdia had originally forecast that the price for an open‐cell LCD TV panel was going to rise by $1 or $2 per month in February, but the actual increase may wind up being $3 to $5 for the month. “The problem is the coronavirus is coming so fast [that] the panel maker has been given a very good reason to increase the price radically,” Hsieh says. He also expects prices to increase for notebook displays, for which he predicts a 30–40 percent decrease in production for 2020"s first financial quarter (Q1), because of shortages in LCD modules.

While concerns over COVID‐19 caused the cancellation of the Mobile World Congress (MWC) tradeshow in Barcelona, Spain, the near‐term impact of the epidemic on smartphone display production appears to be minimal. Q1 production of smartphone displays is generally slow, notes Hsieh, with OEMs traditionally announcing new smartphone models at MWC, but not placing orders for displays until Q2 or Q3. And the bulk of OLED displays, which dominate the market for new high‐end phones, also are made by Korean manufacturers such as Samsung Display. Last year, Korean fabs shipped 433 million smartphone displays, while China was at 54 million. Hsieh said initial targets for 2020 were 476 million smartphone OLEDs shipped from Korea and 128 million from China, which would more than double China"s total from last year. Although the coronavirus will cause a “short‐term setback” for Chinese smartphone OLED makers, he still has a target of more than 100 million Chinese OLEDs.

In Wuhan itself, there are five major fabs, with four making smartphone displays. China Star and Tianma each operate a low‐temperature polycrystalline silicon LCD fab and a flexible OLED fab in the city, while BOE has a new Gen 10.5 LCD plant aimed at TV panels. Hsieh says that the China Star and Tianma OLED fabs are both in the ramping‐up stages, and the new BOE fab also is moving slowly. The biggest impact of COVID‐19 in Wuhan may be on the China Star Gen 6 OLED plant. Along with BOE, it"s slated to be a key supplier of flexible OLED panels for Lenovo"s new Motorola Razr foldable phone. “It"s unfortunate timing,” Hsieh says. —Glen Dickson

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey