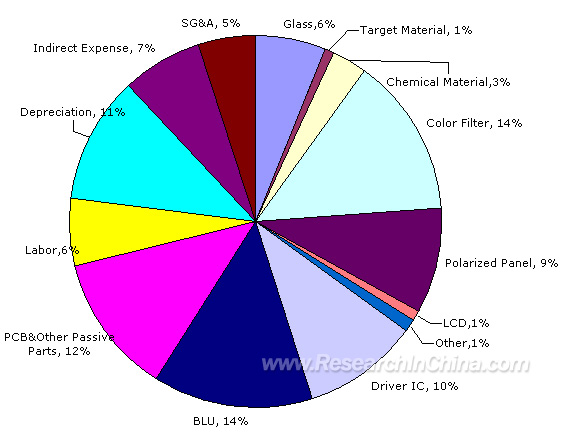

lcd panel production cost brands

LCD panel prices have risen for 4 months in a row because of your home gaming? Since this year, the whole LCD panel market has smoked. Whether after the outbreak of the epidemic, LCD panel market prices rose for four months, or the panel giants in Japan and South Korea successively sold production lines, or the Chinese mainland listed companies frequently integrated acquisition, investment, and plant construction, all make the industry full of interesting.

LCD panel prices are already a fact. Since May this year, LCD panel prices have risen for four months in a row, making the whole industry chain dynamic. Why are LCD panels going up in price in a volatile 2020? The key factor lies in the imbalance between supply and demand.

The price of LCDS for large-size TVs of 70 inches or more hasn’t budged much. In addition, LTPS screens and AMOLED screens used in high-end phones have seen little or no increase in price.

As for October, LCD panel price increases are expected to moderate. The data shows that in October 32 inches or 2 dollars; Gains of 39.5 to 43 inches will shrink to $3;55 inches will fall back below $10; The 65-inch gain will narrow to $5.

During the epidemic, people stayed at home and had no way to go out for entertainment. They relied on TV sets, PCS, and game consoles for entertainment. After the resumption of economic work and production, the market of traditional home appliances picked up rapidly, and LCD production capacity was quickly digested.

However, due to the shutdown of most factories lasting 1-2 months during the epidemic period, LCD panel production capacity was limited, leading to insufficient production capacity in the face of the market outbreak, which eventually led to the market shortage and price increase for 4 consecutive months.

In fact, the last round of price rise of LCD panels was from 2016 to 2017, and its overall market price has continued to fall since 2018. Even in 2019, individual types have fallen below the material cost, and the whole industry has experienced a general operating loss. As a result, LCD makers have been looking for ways to improve margins since last year.

A return to a reasonable price range is the most talked about topic among panel makers in 2019, according to one practitioner. Some manufacturers for the serious loss of the product made the decision to reduce production or even stop production; Some manufacturers planned to raise the price, but due to the epidemic in 2020, the downstream demand was temporarily suppressed and the price increase was postponed. After the outbreak was contained in April, LCD prices began to rise in mid-to-late May.

In fact, the market price of LCD panels continued to decline in 2018-2019 because of the accelerated rise of China’s LCD industry and the influx of a large number of local manufacturers, which doubled the global LCD panel production capacity within a few years, but there was no suitable application market to absorb it. The result of excess capacity is oversupply, ultimately making LCD panel prices remain depressed.

Against this background, combined with the impact of the epidemic in 2020, the operating burden of LCD companies in Japan and South Korea has been further aggravated, and it is difficult to make profits in the production of LCD panels, so they have to announce the withdrawal of LCD business.

business in June 2022. In August, Sharp bought JDI Baishan, a plant in Ishikawa prefecture that makes liquid crystal display panels for smartphones. In early September, Samsung Display sold a majority stake in its SUZHOU LCD production plant to Starlight Electronics Technology, a unit of TCL Technology Group. LGD has not only pulled out of some of its production capacity but has announced that it will close its local production line in 2020. According to DSCC, a consultancy, the share of LCD production capacity in South Korea alone will fall from 19% to 7% between 2020 and 2021.

It is worth mentioning that in industry analysis, in view of the fact that Korean companies are good at using “dig through old bonus – selling high price – the development of new technology” the cycle of development mode, another 2020 out of the LCD production capacity, the main reason may be: taking the advantage of China’s expanding aggressively LCD manufacturers, Korean companies will own LCD panel production line hot sell, eliminating capacity liquid to extract its final value, and turning to the more profitable advantage of a new generation of display technologies, such as thinner, color display better OLED, etc. Samsung, for example, has captured more than 80% of the OLED market with its first-mover advantage.

From the perspective of production capacity, the launch of LCD tracks by major manufacturers in Japan and South Korea must reduce some production capacity in the short term, which to some extent induces market price fluctuations. In the long run, some of the Japanese and Korean LCD production capacity has been bought by Chinese manufacturers, coupled with frequent investment in recent years, the overall capacity is sure to recover as before, or even more than before. But now it will take time to expand the production layout, which more or less will cause supply imbalance, the industry needs to be cautious.

The LCD panel industry started in the United States and then gradually moved to Japan, South Korea, China, and Taiwan. At present, the proportion of production capacity in The Chinese mainland has reached 52% in 2020, and there are leading LCD panel products in China represented by BOE, Huxing Optoelectronics. Meanwhile, the production capacity layout of BOE, Huike, Huxing Optoelectronics, and other manufacturers has been basically completed, making industrial integration a necessity.

On the one hand, South Korean enterprises out of the LCD track, the domestic factory horse enclosure, plant expansion action. While LCDs may not sell as well as “upstart” flexible screens, respondents believe they are still strong enough in the traditional home appliance market to warrant continued investment. Zhao Bin, general manager of TCL Huaxing Development Center, has said publicly that the next-generation display technology will be mature in four to five years, but the commercialization of products may not take place until a decade later. “LCD will still be the mainstream in this decade,” he said.

On the other hand, there is no risk of neck jam in China’s LCD panel industry, which is generally controllable. In mainland China, there will be 21 production lines capable of producing 32-inch or larger LCD panels by 2021, accounting for about two-thirds of the global total. In terms of the proportion of production capacity, the Chinese mainland accounted for 42% of the global LCD panel in 2019, 51% this year, and will continue to climb to 63% next year.

Of course, building factories and expanding production cannot be accomplished overnight. In the process of production capacity recovery, it is predicted that there will be several price fluctuations, and the cost may be passed on to the downstream LCD panel manufacturers or consumers when the price rises greatly, which requires continuous attention.

BOE Technology Group, the Chinese electronic components producer, is expected to be the leader in producing LCD display panels in the coming years, with a forecast capacity share of 24 percent by 2022. China is the country that has the largest LCD capacity, with a 56 percent share in 2020.Read moreLCD panel production capacity share from 2016 to 2022, by manufacturerCharacteristicBOEChina StarInnoluxAUOLGDHKCCEC PandaSharpSDCOther-----------

DSCC. (June 8, 2020). LCD panel production capacity share from 2016 to 2022, by manufacturer [Graph]. In Statista. Retrieved January 07, 2023, from https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. "LCD panel production capacity share from 2016 to 2022, by manufacturer." Chart. June 8, 2020. Statista. Accessed January 07, 2023. https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. (2020). LCD panel production capacity share from 2016 to 2022, by manufacturer. Statista. Statista Inc.. Accessed: January 07, 2023. https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. "Lcd Panel Production Capacity Share from 2016 to 2022, by Manufacturer." Statista, Statista Inc., 8 Jun 2020, https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC, LCD panel production capacity share from 2016 to 2022, by manufacturer Statista, https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/ (last visited January 07, 2023)

China is the leader in producing LCD display panels, with a forecast capacity share of 56 percent in 2020. China"s share is expected to increase in the coming years, stabilizing at 69 percent from 2023 onwards.Read moreLCD panel production capacity share from 2016 to 2025, by countryCharacteristicChinaJapanSouth KoreaTaiwan-----

DSCC. (June 8, 2020). LCD panel production capacity share from 2016 to 2025, by country [Graph]. In Statista. Retrieved January 07, 2023, from https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. "LCD panel production capacity share from 2016 to 2025, by country." Chart. June 8, 2020. Statista. Accessed January 07, 2023. https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. (2020). LCD panel production capacity share from 2016 to 2025, by country. Statista. Statista Inc.. Accessed: January 07, 2023. https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. "Lcd Panel Production Capacity Share from 2016 to 2025, by Country." Statista, Statista Inc., 8 Jun 2020, https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC, LCD panel production capacity share from 2016 to 2025, by country Statista, https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/ (last visited January 07, 2023)

Flat-panel displays are thin panels of glass or plastic used for electronically displaying text, images, or video. Liquid crystal displays (LCD), OLED (organic light emitting diode) and microLED displays are not quite the same; since LCD uses a liquid crystal that reacts to an electric current blocking light or allowing it to pass through the panel, whereas OLED/microLED displays consist of electroluminescent organic/inorganic materials that generate light when a current is passed through the material. LCD, OLED and microLED displays are driven using LTPS, IGZO, LTPO, and A-Si TFT transistor technologies as their backplane using ITO to supply current to the transistors and in turn to the liquid crystal or electroluminescent material. Segment and passive OLED and LCD displays do not use a backplane but use indium tin oxide (ITO), a transparent conductive material, to pass current to the electroluminescent material or liquid crystal. In LCDs, there is an even layer of liquid crystal throughout the panel whereas an OLED display has the electroluminescent material only where it is meant to light up. OLEDs, LCDs and microLEDs can be made flexible and transparent, but LCDs require a backlight because they cannot emit light on their own like OLEDs and microLEDs.

Liquid-crystal display (or LCD) is a thin, flat panel used for electronically displaying information such as text, images, and moving pictures. They are usually made of glass but they can also be made out of plastic. Some manufacturers make transparent LCD panels and special sequential color segment LCDs that have higher than usual refresh rates and an RGB backlight. The backlight is synchronized with the display so that the colors will show up as needed. The list of LCD manufacturers:

Organic light emitting diode (or OLED displays) is a thin, flat panel made of glass or plastic used for electronically displaying information such as text, images, and moving pictures. OLED panels can also take the shape of a light panel, where red, green and blue light emitting materials are stacked to create a white light panel. OLED displays can also be made transparent and/or flexible and these transparent panels are available on the market and are widely used in smartphones with under-display optical fingerprint sensors. LCD and OLED displays are available in different shapes, the most prominent of which is a circular display, which is used in smartwatches. The list of OLED display manufacturers:

MicroLED displays is an emerging flat-panel display technology consisting of arrays of microscopic LEDs forming the individual pixel elements. Like OLED, microLED offers infinite contrast ratio, but unlike OLED, microLED is immune to screen burn-in, and consumes less power while having higher light output, as it uses LEDs instead of organic electroluminescent materials, The list of MicroLED display manufacturers:

LCDs are made in a glass substrate. For OLED, the substrate can also be plastic. The size of the substrates are specified in generations, with each generation using a larger substrate. For example, a 4th generation substrate is larger in size than a 3rd generation substrate. A larger substrate allows for more panels to be cut from a single substrate, or for larger panels to be made, akin to increasing wafer sizes in the semiconductor industry.

"Samsung Display has halted local Gen-8 LCD lines: sources". THE ELEC, Korea Electronics Industry Media. August 16, 2019. Archived from the original on April 3, 2020. Retrieved December 18, 2019.

"TCL to Build World"s Largest Gen 11 LCD Panel Factory". www.businesswire.com. May 19, 2016. Archived from the original on April 2, 2018. Retrieved April 1, 2018.

"Panel Manufacturers Start to Operate Their New 8th Generation LCD Lines". 대한민국 IT포털의 중심! 이티뉴스. June 19, 2017. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"TCL"s Panel Manufacturer CSOT Commences Production of High Generation Panel Modules". www.businesswire.com. June 14, 2018. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"Samsung Display Considering Halting Some LCD Production Lines". 비즈니스코리아 - BusinessKorea. August 16, 2019. Archived from the original on April 5, 2020. Retrieved December 19, 2019.

Herald, The Korea (July 6, 2016). "Samsung Display accelerates transition from LCD to OLED". www.koreaherald.com. Archived from the original on April 1, 2018. Retrieved April 1, 2018.

"China"s BOE to have world"s largest TFT-LCD+AMOLED capacity in 2019". ihsmarkit.com. 2017-03-22. Archived from the original on 2019-08-16. Retrieved 2019-08-17.

According to TrendForce, LCD TV panel quotations bore the brunt of continuous downgrades in the purchase volume of TV brands and pricing for most panel sizes have fallen to record lows. Recently, it was announced that the 32-inch and 43-inch panels fell by approximately US$5~US$6 in early June, 55-inch panels fell approximately US$7, and 65-inch and 75-inch panels are also facing overcapacity pressure, down US$12 to US$14. In order to alleviate pressure caused by price decline and inventory, panel makers are successively planning to initiate more significant production control in 3Q22. According to TrendForce’s latest research, overall LCD TV panel production capacity in 3Q22 will be reduced by 12% compared with original planning.

As Chinese panel makers account for nearly 66% of TV panel shipments, BOE, CSOT, and HKC are industry leaders. When there is an imbalance in supply and demand, a focus on strategic direction is prioritized. According to TrendForce, TV panel production capacity of the three aforementioned companies in 3Q22 is expected to decrease by 15.8% compared with their original planning, and 2% compared with 2Q22. Taiwanese manufacturers account for nearly 20% of TV panel shipments so, under pressure from falling prices, allocation of production capacity is subject to dynamic adjustment. On the other hand, Korean factories have gradually shifted their focus to high-end products such as OLED, QDOLED, and QLED, and are backed by their own brands. However, in the face of continuing price drops, they too must maintain operations amenable to flexible production capacity adjustments.

TrendForce indicates, in order to reflect real demand, Chinese panel makers have successively reduced production capacity. However, facing a situation in which terminal demand has not improved, it may be difficult to reverse the decline of panel pricing in June. However, as TV sizes below 55 inches (inclusive) have fallen below their cash cost in May (which is seen as the last line of defense for panel makers) and is even flirting with the cost of materials, coupled with production capacity reduction from panel makers, the price of TV panels has a chance to bottom out at the end of June and be flat in July. However, demand for large sizes above 65 inches (inclusive) originates primarily from Korean brands. Due to weak terminal demand, TV brands revising their shipment targets for this year downward, and purchase volume in 3Q22 being significantly cut down, it is difficult to see a bottom for large-size panel pricing. TrendForce expects that, optimistically, this price decline may begin to dissipate month by month starting in June but supply has yet to reach equilibrium, so the price of large sizes above 65 inches (inclusive) will continue to decline in 3Q22.

TrendForce states, as panel makers plan to reduce production significantly, the price of TV panels below 55 inches (inclusive) is expected to remain flat in 3Q22. However, panel manufacturers cutting production in the traditional peak season also means that a disappointing 2H22 peak season is a foregone conclusion and it will not be easy for panel prices to reverse. However, it cannot be ruled out, as operating pressure grows, the number and scale of manufacturers participating in production reduction will expand further and it timeframe extended, enacting more effective suppression on the supply side, so as to accumulate greater momentum for a rebound in TV panel quotations.

According to TrendForce"s latest panel price report, TV panel pricing is expected to arrest its fall in October after five consecutive quarters of decline and the prices of certain panel sizes may even be poised to move up. The price decline of IT panels, whether notebook panels or LCD monitor panels, has also begun showing signs of easing and overall pricing of large-size panels is developing towards bottoming out.

TrendForce indicates, with panel makers actively implementing production reduction plans, TV inventories have also experienced a period of adjustment, with pressure gradually being alleviated. At the same time, the arrival of peak sales season at year’s end has also boosted demand marginally. In particular, Chinese brands are still holding out hope for Double Eleven (Singles’ Day) Shopping Festival promotions and have begun to increase their stocking momentum in turn. Under the influence of strictly controlled utilization rate and marginally stronger demand, TV panel pricing, which are approaching the limit of material costs, is expected to halt its decline in October. Prices of panels below 75 inches (inclusive) are expected to cease their declines. The strength of demand for 32-inch products is the most obvious and prices are expected to increase by US$1. As for other sizes, it is currently understood that PO (Purchase Order) quotations given by panel manufacturers in October have are all increased by US$3~5. Currently China"s Golden Week holiday is ongoing but, after the holiday, panel manufacturers and brands are expected to wrestle with pricing. Based on prices stabilizing, whether pricing can actually be increased still depends on the intensity of demand generated by branded manufacturers for different sized products.

TrendForce observes that current demand for monitor panels is weak, and brands are poorly motivated to stock goods. At the same time, the implementation of production cuts by panel manufacturers has played a role and room for price negotiation has gradually narrowed. At present, the decline in panel pricing has slowed. Prices of small-size TN panels below 21.5 inches (inclusive) are expected to cease declining in October due to reduced supply and flat demand. As for mainstream sizes such as 23.8 and 27-inch, price declines are expected to be within US$1.5. The current demand for notebook panels is also weak and customers must still face high inventory issues and are relatively unwilling to buy panels. Panel makers are also trying to slow the decline in panel prices through their implementation of production reduction plans. Declining panel prices are currently expected to continue abating in October. Pricing for 14-inch and 15.6-inch HD TN panels are expected to drop by US$0.2~0.3, falling from a 1.8% drop in September to 0.7%, while pricing for 14-inch and 15.6-inch FHD IPS panels are expected to fall by US$1~1.2, falling from a 3.4% drop in September to 2.4%.

Compared with past instances when TV panels drove a supply/demand reversal through a sharp increase in demand and spiking prices, this current period of lagging TV panel pricing has been halted and reversed through active control of utilization rates by panel manufacturers and a slight increase in demand momentum. The basis for this break in decline and subsequent price increase is relatively weak. Therefore, in order to maintain the strength of this price backstop and eventual escalation and move towards a healthier supply/demand situation, panel manufacturers must continue to strictly and prudently control the utilization rate of TV production lines, in addition to observing whether sales performance from the forthcoming Chinese festivals beat expectations, allowing stocking momentum to continue, and laying a solid foundation for TV panels to completely escape sluggish market conditions.

The price of IT panels has also adhered to the effect of production reduction and the magnitude of its price drops has gradually eased. TrendForce believes, since the capacity for supplying IT panels is still expanding into the future, it is difficult to see declines in mainstream panel prices halt completely when demand remains weak. Even if new production capacity from Chinese panel factories is gradually completed starting from 2023, price competition in the IT panel market will intensify once products are verified by branded clients, so potential downward pressure in pricing still exists.

Panel makers are cutting production by 16 percent on average from this month, Rong Chaoping, senior researcher at market research firm AVC Revo, told Yicai Global. Television panel makers are expected to ship 3.6 million less panels than last month.

Panel makers will reduce capacity by between 15 and 20 percent this month, said Wu Rongbing, chief analyst at Chinese semiconductor intelligence service Omdia.

TCL China Star intends to continue with its production cuts until September, while Beijing-based BOE and HKC Optoelectronics Technology have not yet decided how long they will reduce output, Rong said. None of the three companies responded when contacted by Yicai Global.

LCD TV display shipments from China’s five largest panel manufacturers accounted for 68.5 percent of the global market in April, a new high, and they were expected to exceed 70 percent this year, according to Omdia.

The global panel industry is expected to slash production by about 20 percent this year, according to Beijing-based Sigmaintell. It is the first time since 2013 that the worldwide sector has implemented such a large-scale and wide-ranging cut in manufacturing. But it should help to slow the fall in prices, Li said.

“Tumbling prices are squeezing profits,” Li said. “The price of a TV panel is now below cost price and that of some data panels is also below the manufacturing cost.”

“Panel makers are facing rising liquidity pressure and bigger losses as prices are now below cost price, so the display industry is likely to undergo another big reshuffle,” Rong said.

Panel prices are likely to stop dropping this month or next as output falls, Wu said. Whether prices will start to pick up soon depends on when demand improves.

In 1991, a business unit called Samsung Display was formed to produce the panels used in products made by its parent company, Samsung Electronics. Afterward, it was a leading supplier of LCD panels not just for Samsung Electronics but for other companies in the industry as well.

The business received a stay of execution when the pandemic led to a global surge in demand for consumer electronics, but that demand is now declining, and projections aren"t good for LCD panel revenue.

Add to that the fact that emerging technologies like QD-OLED are the future for TV and monitors, and the case for keeping Samsung Display"s LCD business going becomes a hard one to make.

Samsung Display will now focus heavily on OLED and quantum dot. Most of the employees working in the LCD business will move to quantum dot, the publication claims.

Even if there isn"t a statement about a change in direction, the writing has been on the wall for Samsung"s LCD business. Unless something radical changes, it"s more a question of when than if at this point.

Back in 2016, to determine if the TV panel lottery makes a significant difference, we bought three different sizes of the Samsung J6300 with panels from different manufacturers: a 50" (version DH02), a 55" (version TH01), and a 60" (version MS01). We then tested them with the same series of tests we use in all of our reviews to see if the differences were notable.

Our Samsung 50" J6300 is a DH02 version, which means the panel is made by AU Optronics. Our 55" has an original TH01 Samsung panel. The panel in our 60" was made by Sharp, and its version is MS01.

Upon testing, we found that each panel has a different contrast ratio. The 50" AUO (DH02) has the best contrast, at 4452:1, followed by the 60" Sharp (MS01) at 4015:1. The Samsung 55" panel had the lowest contrast of the three: 3707:1.

These results aren"t really surprising. All these LCD panels are VA panels, which usually means a contrast between 3000:1 and 5000:1. The Samsung panel was quite low in that range, leaving room for other panels to beat it.

The motion blur results are really interesting. The response time of the 55" TH01 Samsung panel is around double that of the Sharp and AUO panels. This is even consistent across all 12 transitions that we measured.

For our measurements, a difference in response time of 10 ms starts to be noticeable. All three are within this range, so the difference isn"t very noticeable to the naked eye, and the Samsung panel still performs better than most other TVs released around the same time.

We also got different input lag measurements on each panel. This has less to do with software, which is the same across each panel, and more to do with the different response times of the panels (as illustrated in the motion blur section). To measure input lag, we use the Leo Bodnar tool, which flashes a white square on the screen and measures the delay between the signal sent and the light sensor detecting white. Therefore, the tool"s input lag measurement includes the 0% to 100% response time of the pixel transition. If you look at the 0% to 100% transitions that we measured, you will see that the 55" takes about 10 ms longer to transition from black to white.

All three have bad viewing angles, as expected for VA panels. If you watch TV at an angle, most likely none of these TVs will satisfy you. The picture quality degrades at about 20 degrees from the side. The 60" Sharp panel is worse than the other ones though. In the video, you can see the right side degrading sooner than the other panels.

It"s unfortunate that manufacturers sometimes vary the source of their panels and that consumers don"t have a way of knowing which one they"re buying. Overall though, at least in the units we tested, the panel lottery isn"t something to worry about. While there are differences, the differences aren"t big and an original Samsung panel isn"t necessarily better than an outsourced one. It"s also fairly safe to say that the same can be said of other brands. All panels have minute variations, but most should perform within the margin of error for each model.

New Vision Display is a custom LCD display manufacturer serving OEMs across diverse markets. One of the things that sets us apart from other LCD screen manufacturers is the diversity of products and customizations we offer. Our LCD portfolio ranges from low-cost monochrome LCDs to high-resolution, high-brightness color TFT LCDs – and pretty much everything in between. We also have extensive experience integrating LCD screen displays into complete assemblies with touch and cover lens.

Sunlight readable, ultra-low power, bistable (“paper-like”) LCDs. Automotive grade, wide operating/storage temperatures, and wide viewing angles. Low tooling costs.

Among the many advantages of working with NVD as your LCD screen manufacturer is the extensive technical expertise of our engineering team. From concept to product, our sales and technical staff provide expert recommendations and attentive support to ensure the right solution for your project.

As a leading LCD panel manufacturer, NVD manufactures custom LCD display solutions for a variety of end-user applications: Medical devices, industrial equipment, household appliances, consumer electronics, and many others. Our state-of-the-art LCD factories are equipped to build custom LCDs for optimal performance in even the most challenging environments. Whether your product will be used in the great outdoors or a hospital operating room, we can build the right custom LCD solution for your needs. Learn more about the markets we serve below.

(2 November, 2017) – A major decrease in manufacturing cost gap between organic light-emitting diode (OLED) display and liquid crystal display (LCD) panel is expected to support the expansion of OLED TVs, according to new analysis from

analysis estimates that the total manufacturing cost of a 55-inch OLED ultra-high definition (UHD) TV panel -- at the larger end for OLED TVs -- stood at $582 per unit in the second quarter of 2017, a 55 percent drop from when it was first introduced in the first quarter of 2015. The cost is expected to decline further to $242 by the first quarter of 2021, IHS Markit said.

The manufacturing cost of a 55-inch OLED UHD TV panel has narrowed to 2.5 times that of an LCD TV panel with the same specifications, compared to 4.3 times back in the first quarter of 2015.

“Historically, a new technology takes off when the cost gap between a dominant technology and a new technology gets narrower,” said Jimmy Kim, principal analyst for display materials at IHS Markit. “The narrower gap in the manufacturing cost between the OLED and LCD panel will help the expansion of OLED TVs.”

However, it is not just the material that determines the cost gap. In fact, when the 55-inch UHD OLED TV panel costs were 2.5 times more than LCD TV panel, the gap in the material costs was just 1.7 times. Factors other than direct material costs, such as production yield, utilization rate, depreciation expenses and substrate size, do actually matter, IHS Markit said.

The total manufacturing cost difference will be reduced to 1.8 times from the current 2.5 times, when the yield is increased to a level similar to that of LCD panels. “However, due to the depreciation cost of OLED, there are limitations in cost reduction from just improving yield,” Kim said. “When the depreciation is completed, a 31 percent reduction in cost can be expected from now.”

by IHS Markit provides more detailed cost analysis of OLED panels, including details of boards, arrays, luminescent materials, encapsulants and direct materials such as driver ICs. The report also covers overheads such as occupancy rate, selling, general and depreciation costs. In addition, this report analyzes OLED panels in a wide range of sizes and applications.

Carbon fiber-framed indoor LED video wall and floor displays with exceptional on-camera visual properties and deployment versatility for various installations including virtual production and extended reality.

a line of extreme and ultra-narrow bezel LCD displays that provides a video wall solution for demanding requirements of 24x7 mission-critical applications and high ambient light environments

LCD manufacturers are mainly located in China, Taiwan, Korea, Japan. Almost all the lcd or TFT manufacturers have built or moved their lcd plants to China on the past decades. Top TFT lcd and oled display manufactuers including BOE, COST, Tianma, IVO from China mainland, and Innolux, AUO from Tianwan, but they have established factories in China mainland as well, and other small-middium sizes lcd manufacturers in China.

China flat display revenue has reached to Sixty billion US Dollars from 2020. there are 35 tft lcd lines (higher than 6 generation lines) in China,China is the best place for seeking the lcd manufacturers.

The first half of 2021, BOE revenue has been reached to twenty billion US dollars, increased more than 90% than thesame time of 2020, the main revenue is from TFT LCD, AMoled. BOE flexible amoled screens" output have been reach to 25KK pcs at the first half of 2021.the new display group Micro LED revenue has been increased to 0.25% of the total revenue as well.

Established in 1993 BOE Technology Group Co. Ltd. is the top1 tft lcd manufacturers in China, headquarter in Beijing, China, BOE has 4 lines of G6 AMOLED production lines that can make flexible OLED, BOE is the authorized screen supplier of Apple, Huawei, Xiaomi, etc,the first G10.5 TFT line is made in BOE.BOE main products is in large sizes of tft lcd panel,the maximum lcd sizes what BOE made is up to 110 inch tft panel, 8k resolution. BOE is the bigger supplier for flexible AM OLED in China.

Technology Co., Ltd), established in 2009. CSOT is the company from TCL, CSOT has eight tft LCD panel plants, four tft lcd modules plants in Shenzhen, Wuhan, Huizhou, Suzhou, Guangzhou and in India. CSOTproviding panels and modules for TV and mobile

three decades.Tianma is the leader of small to medium size displays in technologyin China. Tianma have the tft panel factories in Shenzhen, Shanhai, Chendu, Xiamen city, Tianma"s Shenzhen factory could make the monochrome lcd panel and LCD module, TFT LCD module, TFT touch screen module. Tianma is top 1 manufactures in Automotive display screen and LTPS TFT panel.

Tianma and BOE are the top grade lcd manufacturers in China, because they are big lcd manufacturers, their minimum order quantity would be reached 30k pcs MOQ for small sizes lcd panel. price is also top grade, it might be more expensive 50%~80% than the market price.

Panda electronics is established in 1936, located in Nanjing, Jiangshu, China. Panda has a G6 and G8.6 TFT panel lines (bought from Sharp). The TFT panel technologies are mainly from Sharp, but its technology is not compliance to the other tft panels from other tft manufactures, it lead to the capacity efficiency is lower than other tft panel manufacturers. the latest news in 2022, Panda might be bougt to BOE in this year.

Established in 2005, IVO is located in Kunsan,Jiangshu province, China, IVO have more than 3000 employee, 400 R&D employee, IVO have a G-5 tft panel production line, IVO products are including tft panel for notebook, automotive display, smart phone screen. 60% of IVO tft panel is for notebook application (TOP 6 in the worldwide), 23% for smart phone, 11% for automotive.

Besides the lcd manufacturers from China mainland,inGreater China region,there are other lcd manufacturers in Taiwan,even they started from Taiwan, they all have built the lcd plants in China mainland as well,let"s see the lcd manufacturers in Taiwan:

Innolux"s 14 plants in Taiwan possess a complete range of 3.5G, 4G, 4.5G, 5G, 6G, 7.5G, and 8.5G-8.6G production line in Taiwan and China mainland, offering a full range of large/medium/small LCD panels and touch-control screens.including 4K2K ultra-high resolution, 3D naked eye, IGZO, LTPS, AMOLED, OLED, and touch-control solutions,full range of TFT LCD panel modules and touch panels, including TV panels, desktop monitors, notebook computer panels, small and medium-sized panels, and medical and automotive panels.

AUO is the tft lcd panel manufacturers in Taiwan,AUO has the lcd factories in Tianma and China mainland,AUOOffer the full range of display products with industry-leading display technology,such as 8K4K resolution TFT lcd panel, wide color gamut, high dynamic range, mini LED backlight, ultra high refresh rate, ultra high brightness and low power consumption. AUO is also actively developing curved, super slim, bezel-less, extreme narrow bezel and free-form technologies that boast aesthetic beauty in terms of design.Micro LED, flexible and foldable AMOLED, and fingerprint sensing technologies were also developed for people to enjoy a new smart living experience.

Hannstar was found in 1998 in Taiwan, Hannstar display hasG5.3 TFT-LCD factory in Tainan and the Nanjing LCM/Touch factories, providing various products and focus on the vertical integration of industrial resources, creating new products for future applications and business models.

driver, backlight etc ,then make it to tft lcd module. so its price is also more expensive than many other lcd module manufacturers in China mainland.

Maclight is a China based display company, located in Shenzhen, China. ISO9001 certified, as a company that more than 10 years working experiences in display, Maclight has the good relationship with top tft panel manufacturers, it guarantee that we could provide a long term stable supply in our products, we commit our products with reliable quality and competitive prices.

Maclight products included monochrome lcd, TFT lcd module and OLED display, touch screen module, Maclight is special in custom lcd display, Sunlight readable tft lcd module, tft lcd with capacitive touch screen. Maclight is the leader of round lcd display. Maclight is also the long term supplier for many lcd companies in USA and Europe.

If you want tobuy lcd moduleorbuy tft screenfrom China with good quality and competitive price, Maclight would be a best choice for your glowing business.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey