lcd panel shortage quotation

COVID-19 has had a dramatic effect on the electronics industry. The worldwide drive for people to work and educate from home and the increase in demand for medical products have taken the supply of electronics components from overcapacity to shortage and extended lead times. This was multiplied by the shutdown of manufacturing and the attempt to catch up with previous demand. The industrial market has also gotten hit by the loss of small gen fab capacity due to the shutting down of older, less competitive fabs.

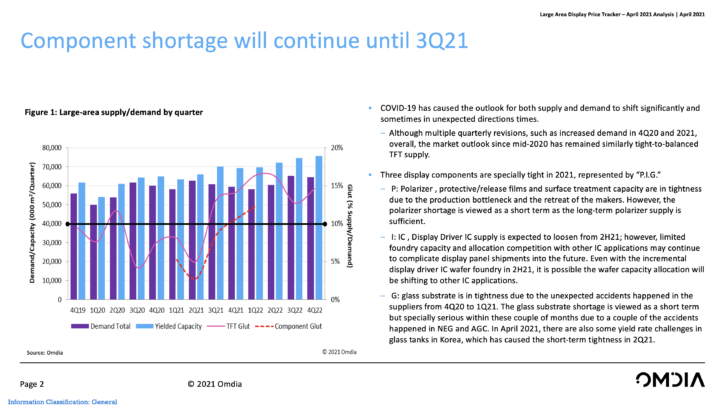

Before COVID-19, the display market had been in an oversupply with the slowdown in cell phone demand. With the increased demand for laptops, monitors, and even TVs has backfilled this capacity and driven us into a shortage situation. This shortage of electronic components is not only in the display market but extends to basic components like resistors and capacitors.

The key components of TFT LCD panel are frequently transmitted, which not only drives the IC supply still tight, including accidents such as equipment failures in furnaces of large glass substrate manufacturers such as AGC , NEG and Corning, but also increases the inventory due to the expected price increase of downstream channel customers, resulting in the continuous bullish price of LCD panel in the near future. Following the continuous increase in the quotation in January and February, it is expected that the quotation in March and April after the lunar new year will still be supported.

Originally, the outside world was worried that the large Korean panel manufacturers have delayed the reduction / shutdown plan of LCD panels one after another. In addition, China"s new production capacity of generation 8.6 and generation 10.5 has resumed production one after another, and the production rate of new production lines has gradually increased, which may increase the supply of LCD panels in the second half of the year, and then affect the trend of panel quotation after the lunar year.

However, the recent frequent situation of key components of the panel has led to a strong continuation of the price rise of the panel. On the one hand, the supply of driving IC such as TCON and PMIC is still tight. It is estimated that the shortage may take more than 3 months to ease.

On the other hand, since the end of last year, the major glass substrate manufacturers Corning , NEG and AGC have successively reported accidents such as equipment failure, power failure and even explosion. Although the single impact of each glass furnace is limited, it has more or less impact on the overall panel industry. Especially during the period when the overall panel supply is limited and the price is bullish, even if individual panel factories can obtain the same amount of glass substrate supply during this period, the overall panel price will still rise in the first quarter under the consideration of avoiding capacity shift at the purchasing end and taking into account the maximum profit margin.

The short-term shortage of panels is difficult to solve, especially after the Spring Festival holiday, the factory is afraid to reproduce the "shortage of workers". At that time, the overall production situation will be more tight, and the shortage of panels will continue to burn.

According to the survey, the quotation of the three application large-size panels continued to rise in February after the overall increase in January. It is expected that the quotation in March and April will still be supported after the lunar new year. On the whole, the panel quotation in the first quarter has a double-digit range. The first quarter profit performance of Auo and Innolux, a large panel manufacturer, has the opportunity to be better than that of the previous quarter.

The report pointed out that in the second half of 2021, the supply of large-size display driver chips is expected to ease compared with the first half. There is still a risk of tension or shortage in 2022. For 12-inch wafers, LCD driver chip supply tends to be balanced or loose. However, the supply of AMOLED driver chips will be more challenging.

The demand for IT applications continues to be strong, and the penetration rate of high-resolution TV panels continues to increase. Therefore, large-size display driver chips will maintain relatively strong demand throughout 2021. But with the increase in vaccination rates and the opening of more cities, we can observe that market demand in the fourth quarter may begin to decline. And after nearly two years of strong growth, the total demand for large-size display driver chips is expected to drop by 1% year-on-year in 2022.

The demand for large-size display driver chips may begin to decrease in the fourth quarter. At the same time, Nexchip has some new capacity contributions from the third quarter. Therefore, the supply of large-size display driver chips in the second half of 2021 is expected to be relieved to a certain extent. There is still a gap, but it is not as good as The first half of the year was severe. However, since there is no new 8-inch wafer capacity increase, the supply of large-size display driver chips that mainly rely on 8-inch wafer capacity will remain tight until 2022, especially during the peak demand seasons in the third and fourth quarters. The risk of shortage is expected to remain.

In the small and medium-sized display driver chip market segment, the demand for smart phone display driver chips accounts for more than 60%. Unlike large-size applications, the mobile terminal market has not grown significantly. However, the tightness and shortage of wafers have made brands cautious about reducing demand, so they will continue to actively purchase in the first quarter of 2021, and there is a phenomenon that the off-season is not short. In the second quarter, everyone’s concerns about inventory and overbooking were increasing, and the price of display driver chips continued to rise, making everyone begin to review demand corrections. Therefore, some brands revised their demand downward. Even so, the demand overdraft may still seriously affect the fourth quarter demand, especially LCD demand. With the continuous increase of Nexchip and SMIC"s production capacity, LCD driver chips are expected to exceed demand in the fourth quarter. However, the demand for LCD driver chips is expected to increase slightly in 2022. When demand recovers, the supply of LCD driver chips will tend to be balanced.

On the contrary, AMOLED driver chips will face more challenges. Although the fab has expanded new production capacity to supply AMOLED driver chips, the SAMSUNG Austin factory affected by the snowstorm in the first quarter of 2021 will also resume in the second half of the year, but the demand for AMOLED driver chips has grown faster than the capacity growth rate. Therefore, the shortage of AMOLED driver chips will continue to exist in the second half of 2021. In 2022, due to the off-season in the first and second quarters, demand is expected to fall, and AMOLED driver chip supply may be able to maintain a balance in the first half of 2022. But with the arrival of the peak seasons in the third and fourth quarters, AMOLED driver chip supply will face a shortage. Although many fabs are currently expanding new 12-inch wafer capacity to supply AMOLED driver chips, such as UMC P6 capacity expansion, it takes about two years to build a fab, and the new capacity is expected to be in the second half of 2023. In order to start contributing production capacity. Therefore, prior to this, the supply of AMOLED driver chips with rapid growth in demand will continue to face challenges.

Recently, a data display panel related components or serious shortage tight supply , adequate capacity to bear the brunt of the printed circuit board , not only blocked the force pushing up revenues , but also face the dual pressures of declining prices .

Market spread, the panel related components , such as polarizers , color filter (CF), the rectifier diodes and passive components appear tight supply or shortage, fear of impact associated thin-film transistor liquid crystal display (TFT-LCD) panel makers AUO , new Chi Mei production carve out .

A panel pcb large domestic plant sources, related components out of stock or tight , the impact on the assembly , components most is the lack of PCB, is also bound by the delayed revenue , while other products out of tight favorable prices, but the PCB still have to face downward pressure on prices .

TSMT noted that February consolidated revenue due to lack of work , lack of material leading to decline in March but quickly returned to the level of January 30 billion . Manufacturers are still worried , worried about the lack of previous work downstream panel plant , shut excessive single case, the temperature increase in the fear of the camp to recover as expected .

Published: shortage of $1 component called display driver IC is causing serious production problems for any products with LCD display: monitors, PCs, game consoles and cars. With

Apple is an example of how demand for consumer products is impacting component supplies. The company is one of the pandemic winners in terms of sales revenue and has experienced a boom in demand for its Mac, iPad and 5G iPhone, which launched in late 2020. The company’s Q1 2021 revenue increased 54% to $89.6bn and its iPhone sales increased 66% to $47.9bn – effectively 54% of all revenues in Q1 2021. Part of this success has been achieved through its ability to avoid shortages by stockpiling critical components.

Up until now, many sectors including telecoms have been able to shelter themselves from shortages by advance ordering and stockpiling. Susquehanna Financial Group’s ongoing trend research on the lead time between ordering a chip and taking delivery illustrates the extent of the supply situation, where in July 2021 the lead time increased to 20.2 weeks up from 17 weeks in April.

Both Susquehanna and Bloomberg analysis suggest the increasing lead time gap is an indicator of buyers committing to future supply orders in order to avoid shortages down the line, but also evidence of stockpiling and over ordering which further exacerbates the situation.

The situation has the potential to impact the telecommunications industry where there are shortages of semiconductors in areas such as power management, memory, and screen display for telecommunications equipment. In April 2021, Bloomberg reported broadband providers (ISPs) were facing delays more than a year on internet router orders with carriers been quoted twice the normal order lead time of up to 60 weeks. The potential lack of supply of broadband routers could for example impact ISP broadband subscription sales/upgrades.

Advanced vision sensing will be increasingly required for facial recognition, computational photography, long range scanning, augmented reality and robotics. In July 2021, Semiconductor Engineering highlighted a shortage in CMOS image sensors, which enable camera functions for cars, smartphones, security cameras, and industrial/medical systems, assisting also in computational photography and augmented reality applications.

2. Analog/radio frequency (RF) / mixed signal (SoC) – Semiconductor Engineering highlighted shortages in areas such power management integrated chips (PMIC) and display driver integrated chips (DDIC) in July 2021. PMICs manage flow and direction of power in products such as smartphones as well as wearables and hearables. PMIC are also critical for PCs and servers.

Susquehanna’s May 2021 research highlighted power management lead times of 23.7 weeks in April, an increase of four weeks on the previous month, however in August research indicated a reduction in lead times for power management chips. DDIC manage power to flat-panel displays such as liquid-crystal displays (LCDs) and organic light-emitting diodes (OLEDs). The shortages are impacting automotive, PCs, smartphones, TVs and industrial equipment. Flat-panel displays are also in increasing demand in the automotive sector.

Cloud computing (server) requirements have increased further as people have shifted to fully or partially working from home. Hyperscalers such as Amazon, Microsoft and Google continue to make considerable investments in cloud infrastructure and platforms that also aim to support network operators. Semiconductor Engineering (July 2021) and Susquehanna Financial Group research highlighted shortages in microcontroller MCUs which integrate CPU and memory on the same chip and are used across cars, communications equipment, appliances and industrial equipment. Semiconductor Engineering also noted comments from the CEO of Tokyo Electron that DRAM (flash short term memory) supply was also “tight due to higher 5G mobile, PC, and data center demand”. Smartphones such as the 5G iPhone 12 for example come with 4GB DRAM.

Commenting on the shortage situation in its Q2 2021 analyst call, TSMC acknowledged the challenges caused by a structural increase long-term market demand as well as the short-term imbalances in the supply chain caused by COVID and geopolitical tensions. While the foundry does rule out an inventory correction in future, the CEO confirmed that he expected capacity to remain tight throughout this year and extend at least into 2022. TSMC believes even if an inventory correction were to occur the strength in demand for 5G and HPC applications means the downturn will be less volatile.

However, the combination of the current shortage with geopolitical tensions has resulted in governments stepping up efforts to ensure security of supply such as CHIPS for America Act and actions in Europe, China, India, Japan and South Korea.

Global shipping continues to be an issue across many sectors of the economy as shortage fears lead to over ordering of supplies across many sectors, which in turn contributes to container shortages (as containers are used for temporary storage). This combined with staff furloughing has created bottlenecks across global supply chains.

The fear of shortages itself became a self-fulfilling prophecy as companies fearing shortages (due to high demand, Brexit, upcoming US trade embargos) over ordered and stockpiled inventory to ensure supplies.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey