future of lcd displays made in china

Since no backlight is used, the display requires very little energy in order to operate. This means: a lot of money can be saved over time. Think about the costs of a drive thru menu that stays running all year for sixteen whole hours a day. Those costs add up. Can you imagine spending $20k a year – just to power your display? That would cut your profits in a very noticeable way. So, I bet you’d be pretty pleased to find such a low-energy alternative.

Reflective displays really are a unique thing. You don’t have to hide them from the sun. You don’t have to shield your screen with your hand in order to eliminate glare. You don’t have to tilt it at funny angles that cause your neck to throb in pain, just so that you can read what’s on the screen. Funny, because those are our natural reactions whenever LCD and sunlight combine. Not with a reflective display though.

You could almost compare a reflective display to a piece of paper in the way that it becomes more visible when light is shining directly on it. It’s really bizarre to see, and you almost have to witness it in order to wrap your head around it, because it’s totally unlike what you’re used to.

LG Display and Samsung Display are struggling to find their ways out of the deterioration of their performance even after withdrawing from production of liquid crystal display (LCD) panels. The high-priced organic light emitting diode (OLED) panel sector regarded as a future growth engine is not growing fast due to the economic downturn. Even in the OLED panel sector, Chinese display makers are within striking distance of Korean display makers, experts say.

On Aug. 30, Display Supply Chain Consultants (DSCC), a market research company, predicted that LCD TV panel prices hit an all-time low in August and that an L-shaped recession will continue in the fourth quarter. According to DSCC, the average price of a 65-inch ultra-high-definition (UHD) panel in August was only US$109, a 62 percent drop from the highest price of US$288 recorded in July in 2021. The average price of a 75-inch UHD panel was only US$218, which was only about half of the highest price of US$410 in July last year. DSCC predicted that the average panel price in the third quarter will fall by 15.7 percent. As Chinese companies’ price war and the effect of stagnation in consumption overlapped, the more LCD panels display makers produce, the more loss they suffer.

As panel prices fell, manufacturers responded by lowering facility utilization rates. DSCC said that the LCD factory utilization rate descended from 87 percent in April to 83 percent in May, 73 percent in June, and 70 percent in July.

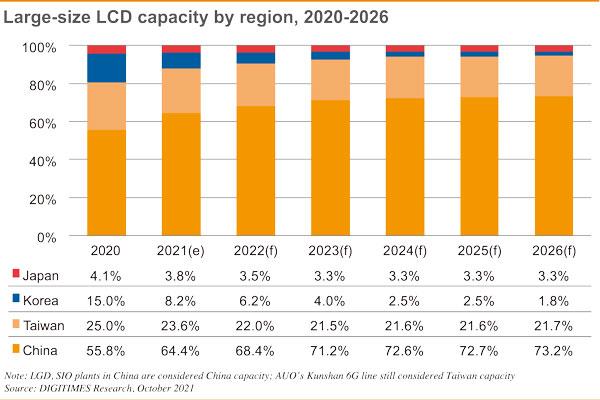

Now that the LCD panel business has become no longer lucrative, Korean display makers have shut down their LCD business or shrunk their sizes. In the LCD sector, China has outpaced Korea since 2018. China’s LCD market share reached 50.9 percent in 2021, while that of Korea dropped to 14.4 percent, lower than Taiwan’s 31.6 percent.

Samsung Display already announced its withdrawal from the LCD business in June. Only 10 years have passed since the company was spun off from Samsung Electronics in 2012. LG Display has decided to halt domestic LCD TV panel production until 2023 and reorganize its business structure centering on OLED panels. Its Chinese LCD production line will be gradually converted to produce LCD panels for IT or commercial products. TrendForce predicted that LG Display will stop operating its P7 Plant in the first quarter of next year.

Korean display makers’ waning LCD business led to a situation in which Korea even lost first place in the display industry. Korea with a display market share of 33.2 percent was already overtaken by China with 41.5 percent) in 2021 according to market researcher Omdia and the Korea Display Industry Association. Korea’s market share has never rebounded in for five years since 2017 amid the Korean government’s neglect. Seventeen years have passed since 2004 when Korea overtook Japan to rise to the top of the world in the LCD industry. Korea’s LCD exports amounted to more than US$30 billion in 2014, but fell to US$21.4 billion last year.

A bigger problem is that Korean display makers may lose its leadership in the OLED panel sector although it is still standing at the top spot. While Korea’s OLED market share fell from 98.1 percent in 2016 to 82.8 percent last year, that of China rose from 1.1 percent to 16.6 percent. Considering that the high-end TV market is highly likely to shrink for the time being due to a full-fledged global consumption contraction, some analysts say that the technology gap between Korea and China can be sharply narrowed through this looming TV market slump. According to industry sources, the Chinese government is now focusing on giving subsidies to the development of OLED panel technology rather LCD technology. On the other hand, in Korea, displays were also wiped out from national strategic technology industry items under the Restriction of Special Taxation Act which can receive tax benefits for R&D activities on displays.

Introduction: Global LCD industry shift and automotive intelligence together to promote the rapid development of China’s LCD panel industry, which will bring a continuous increase in demand for backlight modules, China’s backlight module industry has greater potential for development.

LCD panel backlight module consists of a backlight light source, light guide, optical film, and a plastic frame, which is an important component of LCD display panel. As the backlight module has technology-intensive and labor-intensive attributes, with abundant high-skilled labor advantage China is attracting the global LCD panel industry to the domestic rapid transfer.

From LCD application to the present, the global LCD panel industry capacity transfer has gone through three periods, 2000 Japan dominated the global LCD industry; 2000 – 2010, Japan’s production capacity to South Korea and Taiwan; 2010 to the present, Japanese manufacturers gradually withdraw from the LCD panel industry, production capacity began to transfer to mainland China, so far, mainland China LCD production capacity has occupied the global half of the world.

In recent years, South Korea’s Samsung and LG display will shift their business focus to OLED, and will gradually shut down their LCD production lines and withdraw from the LCD panel industry; at the time of South Korean manufacturers’ withdrawal, domestic enterprises are stepping up new construction to expand LCD production capacity.

BOE, Huaxing photoelectric, Huike, CEC in 2020 – 2021, a total of eight 7 generation LCD production lines completed and put into operation, and domestic panel manufacturers have further expansion plans, the next few years domestic LCD production capacity will continue to increase.

LCD panel manufacturers tend to choose the nearby supporting module suppliers for the safety of the key component supply chain and cost reduction considerations. LCD panel production capacity transfer to China will bring opportunities to domestic backlight module manufacturers and drive the development of the domestic backlight module industry.

The future of the car will pay more attention to the human driving experience, to the intelligent development, which will bring the increasing demand for car display. On the one hand, the number of car displays gradually increased, for example, the instrument panel, rearview mirror, central control platform more to display the way, the passenger and rear position with entertainment display. On the other hand, the car display is constantly to a large screen, multi-screen development, especially in high-end models, the large display has become standard, for example, Tesla Model S screen size of 17 inches, Mercedes-Benz A-class car configuration of two 10.5-inch display.

At the same time, there is also a huge demand for new cars in China. Although China’s car sales have reached 25 million, the current per capita car ownership in China is only a quarter of the developed countries, the future potential for new car demand is still very large. Therefore, China’s car display market growth potential is large, which will directly drive the domestic backlight module demand continues to increase.

According to the terminal application size, backlight module can be divided into large, medium, and small size, of which small size backlight module is mainly used in smartphones, wearable devices, and other terminals, the medium size used in notebook computers, tablet PCs, car screens and other terminals, the large size is mainly used in LCD TV.

From the market competition pattern, the domestic backlight module enterprises are deeply plowed in their respective competitive advantage in the field of segmentation, including Baoming technology, Longli technology mainly layout small size cell phone display field, Hanbo high-tech, Weishi electronics mainly layout in the size of car display and notebook computer field, Rui Yi photoelectric and photoelectric in each field have layout.

From the industry development trend, smartphone display is transitioning to OLED, LCD TV market is gradually saturated, the future of large size and small size backlight module market potential is relatively small; and the future of the car display market potential is huge, by the backlight module manufacturers are unanimously optimistic, are currently accelerating the layout ( see Table 2 ). Focusing on the traditional medium-sized backlight module field, Hanbo Hi-Tech and Weishi Electronics have significant advantages in core technology patents, downstream customer resources, process experience accumulation, production costs, etc., and have more development advantages in the future.

The current global LCD display panel industry is rapidly moving to China, which brings development opportunities to China’s backlight module industry. In addition, automotive intelligence will also bring a continuous increase in demand for medium-sized car displays, the first to enter the field of medium-sized backlight module manufacturers with its customer resources, core technology, scale efficiency, and other advantages will be more beneficial.

Attendees visit the booth of TV panel maker Shenzhen China Star Optoelectronics Technology during an international exhibition in Shanghai on July 11, 2019. [Photo by Lyu Liang/For China Daily]

Chinese companies have gained a competitive edge in the large-screen display industry and the exit of South Korean counterparts such as Samsung Electronics and LG Display from the liquid crystal display market will bring opportunities for China"s panel makers despite the challenges posed by the COVID-19 pandemic.

Market research firm Sigmaintell said BOE Technology Group Co Ltd-a leading Chinese supplier of display products and solutions-became the world"s largest shipper of LCD TV panels for the first time in 2019.

The Beijing-based company shipped 53.3 million units of LCD panels in 2019, with production capacity increasing by more than 20 percent on a yearly basis.

The consultancy said the LCD TV panel production area of Chinese manufacturers will account for more than 50 percent of the global total this year, surpassing South Korean competitors who are accelerating the shutdown of large-sized LCD panel production capacity due to competition from Chinese manufacturers.

It estimated the production capacity of large-sized LCD panels will continue to increase in China over the next three years. In addition, global LCD TV panel shipments stood at 283 million pieces last year, a slight decrease of 0.2 percent year-on-year. Meanwhile, the shipment area was 160 million square meters, an increase of 6.3 percent year-on-year.

"Chinese companies have gained an upper hand in large-screen LCD displays. Samsung and LG"s decision to exit from the LCD sector means Chinese panel makers will take a dominant position in this field," said Li Dongsheng, founder and chairman of Chinese tech giant TCL Technology Group Corp.

Li said South Korean firms will focus on organic LED screens and quantum dot LED displays, while Chinese TV panel makers are catching up at a rapid pace.

"The outbreak has caused a periodic drop in demand in the global display market and sped up the restructuring of the entire industry. Chinese enterprises are in a favorable position, and I believe that they will further enhance their competitiveness," Li said.

Data consultancy Digitimes Research said it comes as little surprise that Samsung has opted to withdraw from the LCD panel sector as its LCD business was losing money in every quarter of 2019 due to challenges from Chinese competitors.

BOE said its Gen 10.5 TFTLCD production line achieved mass production in Hefei, Anhui province, in March 2018. The plant mainly produces high-definition LCD screens of 65 inches and above. With a total investment of 46 billion yuan ($6.5 billion), the company"s second Gen 10.5 TFT-LCD production line launched operations in Wuhan, Hubei province, in December.

The Gen 11 TFT-LCD and active-matrix OLED production line of Shenzhen China Star Optoelectronics Technology, a subsidiary of TCL, officially entered operations in November 2018, producing 43-inch, 65-inch and 75-inch LCD screens.

Chen Lijuan, an analyst at Sigmaintell, said panel manufacturers should not just invest in production lines, but also pay more attention to the establishment of the whole supply chain, including raw materials, equipment and technology.

Bian Zheng, deputy director of research at AVC Revo, a unit of market consultancy firm AVC, said China will have a 51 percent market share in global TV shipments in 2020, while South Korea will have 25 percent, adding that large-screen TV panels will bolster healthy development of the industry.

Bian said the OLED and QLED will be the next-generation flat-panel display technologies to be in the spotlight. LG Display is currently the world"s only supplier of large-screen OLED TV panels.

OLED is a relatively new technology and part of recent display innovation. It has a fast response rate, wide viewing angles, super high-contrast images and richer colors. It is much thinner and can be made flexible, compared with traditional LCD display panels.

Li Yaqin, general manager of Sigmaintell, said 65-inch TVs will become the mainstream in people"s living rooms in the future, but OLED TVs will not be able to immediately spur customer purchases at this time though the future trend is for higher-tech options.

AfghanistanAlbaniaAlgeriaAmerican SamoaAndorraAngolaAnguillaAntigua and BarbudaArgentinaArmeniaArubaAscensionAustraliaAustriaAzerbaijanBahamasBahrainBangladeshBarbadosBelarusBelgiumBelizeBeninBermudaBhutanBoliviaBosnia-HercegovinaBotswanaBrazilBritish Indian Ocean TerritoryBruneiBulgariaBurkina FasoBurundiCambodiaCameroonCanadaCape VerdeCayman IslandsCentral African RepublicChadChileChinaChristmas IslandCocos (Keeling) IslandsColombiaComorosCongoCongo, Dem Rep ofCook IslandsCosta RicaCroatiaCubaCyprusCzech RepublicDenmarkDjiboutiDominicaDominican RepublicEast TimorEcuadorEgyptEl SalvadorEquatorial GuineaEritreaEstoniaEthiopiaFalkland IslandsFaroe IslandsFijiFinlandFranceFrench GuianaFrench PolynesiaFrench Southern TerritoriesGabonGambiaGeorgiaGermanyGhanaGibraltarGreeceGreenlandGrenadaGuadeloupeGuamGuatemalaGuineaGuinea-BissauGuyanaHaitiHeard Island and McDonald IsHondurasHungaryIcelandIndiaIndonesiaIranIraqIrelandIsraelItalyIvory CoastJamaicaJapan 曰本JordanKazakhstanKenyaKirgizstanKiribatiKosovoKuwaitLaosLatviaLebanonLeeward IslesLesothoLiberiaLibyaLiechtensteinLithuaniaLuxembourgMacauMacedonia, FYRMadagascarMalawiMalaysiaMaldivesMaliMaltaMarshall IslandsMartiniqueMauritaniaMauritiusMayotteMexicoMicronesia, Fed States ofMoldovaMonacoMongoliaMontenegroMontserratMoroccoMozambiqueMyanmarNamibiaNauruNepalNetherlandsNetherlands AntillesNew CaledoniaNew ZealandNicaraguaNigerNigeriaNorfolk IslandNorth KoreaNorthern Mariana IslandsNorwayOmanPakistanPalauPalestinePanamaPapua New GuineaParaguayPeruPhilippinesPitcairn IslandPolandPortugalPuerto RicoQatarReunionRomaniaRussiaRwandaST MartinSaint HelenaSaint Kitts and NevisSaint LuciaSaint Vincent and GrenadinesSamoaSao Tome and PrincipeSaudi ArabiaSenegalSerbiaSeychellesSierra LeoneSlovakiaSloveniaSolomon IslandsSomaliaSouth AfricaSouth GeorgiaSpainSri LankaSudanSurinameSwazilandSwedenSwitzerlandSyriaTaiwanTajikistanTanzaniaThailandTogoTokelauTongaTrinidad and TobagoTunisiaTurkeyTurkmenistanTurks and Caicos IslandsTuvaluUS Minor Outlying IsUgandaUkraineUnited Arab EmiratesUnited KingdomUruguayUzbekistanVanuatuVenezuelaVietnamVirgin Islands, BritishVirgin Islands, USWallis and FutunaYemenZambiaZimbabwe

► When the leading Korean players Samsung Display and LG Display exit LCD production, BOE will be the most significant player in the LCD market. Though OLED can replace the LCD, it will take years for it to be fully replaced.

When mainstream consumer electronics brands choose their device panels, the top three choices are Samsung Display, LG Display (LGD) and BOE (000725:SZ) – the first two from Korea and the third from China. From liquid-crystal displays (LCD) to active-matrix organic light-emitting diode (AMOLED), display panel technology has been upgrading with bigger screen products.

From the early 1990s, LCDs appeared and replaced cathode-ray tube (CRT) screens, which enabled lighter and thinner display devices. Japanese electronics companies like JDI pioneered the panel technology upgrade while Samsung Display and LGD were nobodies in the field. Every technology upgrade or revolution is a chance for new players to disrupt the old paradigm.

The landscape was changed in 2001 when Korean players firstly made a breakthrough in the Gen 5 panel technology – the later the generation, the bigger the panel size. A large panel size allows display manufacturers to cut more display screens from one panel and create bigger-screen products. "The bigger the better" is a motto for panel makers as the cost can be controlled better and they can offer bigger-size products to satisfy the burgeoning middle-class" needs.

LCD panel makers have been striving to realize bigger-size products in the past four decades. The technology breakthrough of Gen 5 in 2002 made big-screen LCD TV available and it sent Samsung Display and LGD to the front row, squeezing the market share of Japanese panel makers.

The throne chair of LCD passed from Japanese companies to Korean enterprises – and now Chinese players are clinching it, replacing the Koreans. After twenty years of development, Chinese panel makers have mastered LCD panel technology and actively engage in large panel R&D projects. Mass production created a supply surplus that led to drops in LCD price. In May 2020, Samsung Display announced that it would shut down all LCD fabs in China and Korea but concentrate on quantum dot LCD (Samsung calls it QLED) production; LGD stated that it would close LCD TV panel fabs in Korea and focus on organic LED (OLED). Their retreats left BOE and China Stars to digest the LCD market share.

Consumer preference has been changing during the Korean fab"s recession: Bigger-or-not is fine but better image quality ranks first. While LCD needs the backlight to show colors and substrates for the liquid crystal layer, OLED enables lighter and flexible screens (curvy or foldable), higher resolution and improved color display. It itself can emit lights – no backlight or liquid layer is needed. With the above advantages, OLED has been replacing the less-profitable LCD screens.

Samsung Display has been the major screen supplier for high-end consumer electronics, like its own flagship cell phone products and Apple"s iPhone series. LGD dominated the large OLED TV market as it is the one that handles large-size OLED mass production. To further understand Korean panel makers" monopolizing position, it is worth mentioning fine metal mask (FMM), a critical part of the OLED RGB evaporation process – a process in OLED mass production that significantly affects the yield rate.

Prior to 2018, Samsung Display and DNP"s monopolistic supply contract prevented other panel fabs from acquiring quality FMM products as DNP bonded with Hitachi Metal, the "only" FMM material provider choice for OLED makers. After the contract expired, panel makers like BOE could purchase FFM from DNP for their OLED R&D and mass production. Except for FFM materials, vacuum evaporation equipment is dominated by Canon Tokki, a Japanese company. Its role in the OLED industry resembles that of ASML in the integrated circuit space. Canon Tokki"s annual production of vacuum evaporation equipment is fewer than ten and thereby limits the total production of OLED panels that rely on evaporation technology.

The shortage of equipment and scarcity of materials inspired panel fabs to explore substitute technology; they discovered that inkjet printing has the potential to be the thing to replace evaporation. Plus, evaporation could be applied to QLED panels as quantum dots are difficult to be vaporized. Inkjet printing prints materials (liquefied organic gas or quantum dots) to substrates, saving materials and breaking free from FMM"s size restriction. With the new tech, large-size OLED panels can theoretically be recognized with improved yield rate and cost-efficiency. However, the tech is at an early stage when inkjet printing precision could not meet panel manufacturers" requirements.

Presently, Chinese panel fabs are investing heavily in OLED production while betting on QLED. BOE has four Gen 6 OLED product lines, four Gen 8.5 and one Gen 10.5 LCD lines; China Star, controlled by the major appliance titan TCL, has invested two Gen 6 OLED fabs and four large-size LCD product lines.

Remembering the last "regime change" that occurred in 2005 when Korean fabs overtook Japanese" place in the LCD market, the new phase of panel technology changed the outlook of the industry. Now, OLED or QLED could mark the perfect time for us to expect landscape change.

After Samsung Display and LGD ceding from LCD TV productions, the vacant market share will be digested by BOE, China Star and other LCD makers. Indeed, OLED and QLED have the potential to take over the LCD market in the future, but the process may take more than a decade. Korean companies took ten years from panel fab"s research on OLED to mass production of small- and medium-size OLED electronics. Yet, LCD screen cell phones are still available in the market.

LCD will not disappear until OLED/QLED"s cost control can compete with it. The low- to middle-end panel market still prefers cheap LCD devices and consumers are satisfied with LCD products – thicker but cheaper. BOE has been the largest TV panel maker since 2019. As estimated by Informa, BOE and China Star will hold a duopoly on the flat panel display market.

BOE"s performance seems to have ridden on a roller coaster ride in the past several years. Large-size panel mass production like Gen 8.5 and Gen 10.5 fabs helped BOE recognize the first place in production volume. On the other side, expanded large-size panel factories and expenses of OLED product lines are costly: BOE planned to spend CNY 176.24 billion (USD 25.92 billion) – more than Tibet"s 2019 GDP CNY 169.78 billion – on Chengdu and Mianyang"s Gen 6 AMOLED lines and Hefei and Wuhan"s Gen 10.5 LCD lines.

Except for making large-size TVs, bigger panels can cut out more display screens for smaller devices like laptops and cell phones, which are more profitable than TV products. On its first-half earnings concall, BOE said that it is shifting its production focus to cell phone and laptop products as they are more profitable than TV products. TV, IT and cell phone products counted for 30%, 44% and 33% of its productions respectively and the recent rising TV price may lead to an increased portion of TV products in the short term.

Except for outdoor large screens, TV is another driver that pushes panel makers to research on how to make bigger and bigger screens. A research done by CHEARI showed that Chinese TV sales dropped by 10.6% to CNY 128.2 billion from 2018 to 2019. Large-size TV sales increased as a total but the unit price decreased; high-end products like laser TV and OLED TV saw a strong growth of 131.2% and 34.1%, respectively.

Millions of young white-collars support the co-leasing business in China and breed the six-billion-dollar Ziroom, a unicorn company that provides rental and real estate management services. As apartments can be leased by single rooms instead of the whole apartment, living rooms become a public area while tenants prefer to stay in their private zones – it hints that the bedroom is too small to fit in a TV.

Besides the tier-1 cities" "disappearing living rooms," the mobile Internet gives another reason to explain the declining TV sale in China. Various streaming services and high-speed networks allow people to watch programs wherever and whenever they would like to. However, the change in life does not imply TV will disappear. For families, the living room is still a place for family members to gather and have fun. The growth of high-end TV sales also tells the "living room" economy.

Samsung Display is ending direct production of LCD panels in South Korea and China by the end of this year, according to a report by the global news agency Reuters.

The report suggests the electronics giant will instead focus production efforts on displays that use quantum dots technology – which in simple terms is the basis for a filter on displays that increases brightness and color volume.

Samsung’s gorgeous QLED displays (got one) are LCDs with a quantum dots layer, and there is lots of R&D work going on to add quantum dots to OLED displays, which would boost their brightness and color volume as well.

The investment for the next five years will be focused on converting one of its South Korean LCD lines into a facility to mass produce more advanced “quantum dot” screens.

Samsung Display’s cross-town rival LG Display Co Ltd said earlier this year that it will halt domestic production of LCD TV panels by the end of 2020.

This is happening, maybe not entirely but heavily, because Chinese government-backed manufacturers like BOE have greatly upped production capacity for LCD TVs, driving prices and margins down for consumer and professional display products.

Samsung is also putting more focus on direct view LED – with well-respected indoor and outdoor products, and forays into premium displays like The Wall series.

Samsung Display reportedly plans to shut down ahead of schedule four of its LCD panel production lines as early as in the third quarter of 2020, as the vendor is looking to accelerate its exit from the LCD segment, according to industry sources.

The ongoing coronavirus pandemic is apparently an impetus pushing Samsung Display to phase out its LCD panel production, as the crisis has wrecked havoc on the global economy, slowing down business activities and halting sports events such as the Tokyo Olympics 2020, which is seriously undercutting demand for TVs and adding downward pressure on panel prices, said the sources.

Samsung Display also plans to keep production at its 8.5G LCD fab in Suzhou, China in the meantime, while overhauling its L7-2 fab for production of POLED panels and its L8 fab for QD-OLED panels, indicated the sources.

The Korean panel maker is also looking to halt the operations of the Suzhou 8.5G line by the third quarter of 2022 and is currently in talks to sell the LCD panel plant to Chinese panel makers, said the sources, adding that the completion of a deal will mark Samsung Display ‘s exit from the LCD TV panel market.

Meanwhile, TV panel prices, which have been trending upward recently along with reduced production caused by the pandemic, are expected to stay flat in April, as capacity resumption of most panel plants in China is expected to reach over 90% in the month, while TV brands are likely to slow down their panel purchases amid pandemic-induced uncertainty, commented the sources.

Presumably, while Samsung may not be directly manufacturing LCD, the industry will still be able to buy Samsung LCD displays – just manufactured, as some will be already, by other companies in China and Taiwan.

I only observe and have no direct involvement in how the display giants operate, but from my perch in the bleachers, it seems to make sense to get out of producing a commodity product, when you are up against Chinese manufacturers who can make and sell them for less because of government subsidies and lower labor costs.

I really don’t see direct view LED taking the place of single LCD displays, but much of the future of signage is in LED that fills entire walls and other surfaces, inside and outside.

Most of their commercial displays are manufactured in Mexico. I am assuming this is referring only to their consumer displays as nothing is even mentioned about their Mexico facilities here.

The escalating coronavirus crisis is impacting production at display panel factories located in the semi-quarantined city of Wuhan, China, spurring a significant near-term reduction in the global supply of panels used in liquid crystal display televisions (LCDs) and other products.

The five factories in the city producing liquid crystal displays (LCDs) and organic light-emitting diode (OLED) panels will experience near-term slowdowns in production compared to expected levels, according to IHS Markit technology research, now a part of Informa Tech.

With the situation evolving quickly, IHS Markit technology research is still assessing the magnitude of the supply shortfall on multiple display types and markets. However, leading Chinese panel makers stated they believe that total capacity utilization for all LCD fabs in the country could fall by at least 10 percent and perhaps by more than 20 percent during the month of February.

With China expected to own 55 percent of global display manufacturing capacity in 2020, the immediate impact of the production reduction has been a worldwide decrease in availability and an increase in pricing for LCD-TV panels. This has resulted in turmoil throughout the display supply chain as suppliers and purchasers alike scramble to adjust to swiftly changing market conditions.

“Display facilities in Wuhan currently are dealing with the very real impacts of the coronavirus outbreak,” said David Hsieh, senior director, displays, at IHS Markit technology research. “These factories are facing shortages of both labor and key components as a result of mandates designed to limit the contagion’s spread. In the face of these challenges, top display suppliers in China have informed our experts that a near-term production decline is unavoidable.”

The leading Chinese suppliers of LCD panels for TVs, notebook PCs and PC monitors now are planning to raise panel prices more aggressively. For example, the price for an open-cell LCD-TV panel was originally expected to rise by $1 or $2 per month in February. However, the actual increase may be $3 to $5 for the month.

Beyond the immediate production impact at these facilities, the coronavirus is also likely to trigger delays in the ramp-up of manufacturing at new display fabs during the first half of 2020. This will reduce overall panel availability during the next few months. It also could result in further panel supply tightness as TV display buyers hasten the pace of their panel purchases to build stockpiles for future shortfalls.

The labor shortage encountered by fabs in Wuhan is partly the result of the Chinese government’s move to extend the Lunar New Year holiday by three days, with the last day now scheduled for Sunday, February 2. The extension is designed to reduce travel and cut down on public gatherings to contain the spread of the disease.

LCD panel makers outsource much of the production of such modules. However, production at several key third-party module suppliers has now ceased, impacting panel production severely throughout the country. Key module supplier SkyTech is sharply reducing production until mid-February.

Panel makers maintain their own captive LCD module factories. However, these operations are also facing production bottlenecks amid the coronavirus crisis.

The module shortage potentially could expand the impact of the contagion beyond China—with a knock-on effect on production at display manufacturers worldwide.

According to recent reports, LCD display manufacturing has now been taken over by Chinese manufacturers. Display makers like LG, Samsung, and others are now leaving the LCD display market for Chinese brands. These companies are now focusing on the OLED market. However, cheap smartphones will still make use of LCD displays. This means that more companies will now rely on these Chinese brands. According to a recent report, BOE may develop panels for Samsung’s entry-level models. These models will include the Samsung Galaxy A13, Galaxy A23, and other models.

Both Samsung and BOE are world-renowned screen R&D and product manufacturers. Their products are widely used by smartphone manufacturers. However, there are still some differences between the two. In addition to the related business of screen production, Samsung’s smartphones also occupy a considerable share of the market. However, BOE does not have its own smartphone products for the time being. The company focuses on supplying its displays to several mobile phone manufacturers.

As one of the most important screen manufacturers in China, BOE has close ties with various mobile phone manufacturers. This time, it was reported that among the iPhones made by Apple, the screens produced by BOE account for about 20% of the share. Apple is a world-renowned technology company, and it has always been strict with its products. Being able to enter Apple’s supply chain shows that BOE Screen is already very good in quality. Several other major Chinese manufacturers, such as Huawei and Xiaomi, also have many models that use BOE screens.

There is news that BOE is only developing panels for Samsung’s entry-level models. However, according to relevant industry sources, at the end of March, Samsung had proposed to BOE to supply the next-generation flagship smartphone panel. According to reports, both companies are currently discussing technical verification and contract signing. If this is true and goes well, perhaps we will see the appearance of Chinese screens on future Samsung flagship phones.

Samsung originally planned to stop the production of LCD panels by the end of 2020. However, the LCD panel market started to increase prices in the past year or so. This made Samsung’s LCD factory continue to operate for another two years. However, the company originally plans to exit the market at the end of 2022. Nevertheless, the LCD panel market has changed since the end of last year. The price has been falling significantly and it is now on a free fall. By January this year, the average price of a 32 -inch panel was only $ 38, a 64% drop relative to January last year.

As China witnesses the phenomenal growth of its display industry, its global counterparts also face new challenges. Large-scale production of traditional LCD panels has fallen into a “dilemma of abundance”, where the current focus of display enterprises has shifted to how to best develop the potential of new technologies.

In recent years, panel makers such as JDI, Innolux, AUO, LGD and BOE have made significant efforts on the layout of the vehicle display industry, which shows immense market potential.

Previously, vehicle display pursued an integrated design with a relatively long life cycle. However, an increasing number of separation screen designs is emerging with a shorter life cycle, which demonstrates five major visible development trends in consumer electronics display.

Large screen – a major trend in vehicle display. With the nonstop development of intelligent driving technology, cars will become more interactive and intelligent. Akin to mobile phone screens, vehicle display size will also continue to expand. Moreover, vehicle screens can now be expanded horizontally and vertically so as to provide a wider display space. In fact, a multitude of vehicles has begun to carry large screens. For example, all Byton vehicles come equipped with a 48-inch LCD screen.

High-definition – as mobile phone screens continue on a path of development, consumers will continue to propose higher requirements for vehicle display resolution. Low-resolution display has lost the ability to meet market demand, leading vehicle display closer towards higher resolution. LTPS LCD has better electron mobility than a-Si LCD, which is capable of meeting higher-resolution requirements. Due to its advantages of narrow bezel, high brightness and In-cell, LTPS is now widely adopted by manufacturers. JDI and Innolux were the first to move into mass production of LTPS, according to Sigmaintell, while TIANMA, LGD and AUO are currently in the game. In addition, panel makers, led by JDI, have been recommending LTPS technology to vehicle manufacturers since 2017. In the same year, LTPS took up 2% of the market share in the vehicle display industry. In effect, in addition to resolution, high-definition vehicle display has also led to higher requirements in contrast, field of view, optical index and response speed.

Interaction - Like smartphones, touchscreens might very well become a must-have for vehicle display. Vehicle display has higher requirements for touchscreen, which should be lighter and more sensitive. At present, vehicle display has introduced a large number of capacitive touch applications. In 2017, the TP loading rate reached 22%, and by 2020 it is projected to reach 58%. If OLED were widely introduced into the vehicle display market, its touch technology would also be worthy of attention. OLEDs are classified into rigid OLEDs and flexible OLEDs. The former will be dominated by On-Cell, while in-Cell may prove prevalent in the latter. By 2020, In-Cell is expected to be the mainstream in the OLED market.

Multi-screen - In addition to dashboard and central-control displays, much more is coming in the vehicle display arena. TIANMA believes that multi-screen can be viewed from two angles. The first is “from 0 to 1”, which means vehicles, where no screen existed before, can now be equipped with one, such as a rear seat control display or vehicle key display. The second is “from 1 to an”". HUD and Mirror were previously only installed in high-end vehicles. Due to security demands and the introduction of AR technology, HUD and Mirror have since seen significant development.

Polymorphism- Unlike flat display, flexible display will bring even more possibilities to interior design. More and more anomalous screens, flexible screens and transparent screens are coming into play. These new possibilities leave much space to think about layout and design of interior space, which would provide users with a higher sense of technology. It’s worth mentioning that Samsung was the first to introduce OLED to the vehicle industry, and despite the fact that they had once give up , they restart to promote the technology at present.

CODA and Reed Exhibitions Kuozhan will be holding DISPLAY CHINA 2019 on June 26-28, 2019. Its show floor will feature a 180-square-meter area, namely the New Vehicle Display Innovation Display Area. Invitees will include professional visitors of all levels from the automotive electronics industry, together with touchscreen and display panel factories. The concurrently held Smart Cabin & Vehicle Display and Intelligent Interactive Technology Conference 2019 will be held in cooperation with New Energy Times on June 28. This conference will discuss hot topics such as next-generation, vehicle image display control technology and flexible OLED applications, the latest solutions in multi-screen integration, DLP projection technology, holographic technology, vehicle display full-fit processes (OCA, OCR full-fit technology, full-fit process and problem analysis, In cell/On-cell technology application in vehicle), as well as exploring and predicting the development and future trends of the smart cabin market.

The plethora of drivers in modern times has the ability to ramp up industry development. There is also immense demand for product innovation. Development potential in the panel industry is not only huge in vehicle display. Intelligence interaction and commercial display are also uncharted lands just waiting to be explored. At present, about 39.9% of all digital signage panels are used in the retail market. The commercial retail industry is experiencing rapid growth. Consequently, last year saw its sharpest growth in commercial display panel shipments, at a year-on-year increase of nearly 27%. It is expected that the entire commercial display panel market will reach an annual revenue of $2.88 billion by 2020.

The organizers of DISPLAY CHINA long foresaw these trends, along with the struggle to promote industry development. To that end, they have striven to create an exclusive commercial platform dedicated to intelligent and interactive display, where buyers and industry leaders from commercial display, digital sign factories, vending machine manufacturers and interactive machine manufacturers can experience and purchase the latest touch display technology. The concurrently held Intelligent Interactive Development Summit will discuss the future development model of digital cities with, among others, industry experts, panel exhibitors and logo production buyers, who’ll be sharing their experiences and insights with a focus on the aspects of new framework materials, environmental protection and sustainable development to new display technologies, new software integration solutions and current commercial space solutions.

Looking back at DISPLAY CHINA 2018, the three-day event boasted an exhibition area that stretched across 12,000 square meters and attracted nearly 200 industry brands and a total of 12,710 visitors, including 1,160 professional visitors from 31 industry companies.

DISPLAY CHINA 2019 is projected to attract nearly 20 thousand professional visitors, 1,000 invited buyers, 2,000 visitor groups and 3,500 overseas buyers. Well-known enterprises such as BOE, JNC, TIANMA, ELC, Jingkun, LTMS, Edwards, KOSAN, Yangpu Industrial, Sunlonge, Youji Guangxian, Jspacktech, Huiguang, Naibo, Hangzhou Guangli, Maolian will be taking part in this year’s event.

Samsung Display will stop producing LCD panels by the end of the year. The display maker currently runs two LCD production lines in South Korea and two in China, according to Reuters. Samsung tells The Verge that the decision will accelerate the company’s move towards quantum dot displays, while ZDNetreports that its future quantum dot TVs will use OLED rather than LCD panels.

The decision comes as LCD panel prices are said to be falling worldwide. Last year, Nikkei reported that Chinese competitors are ramping up production of LCD screens, even as demand for TVs weakens globally. Samsung Display isn’t the only manufacturer to have closed down LCD production lines. LG Display announced it would be ending LCD production in South Korea by the end of the 2020 as well.

Last October Samsung Display announced a five-year 13.1 trillion won (around $10.7 billion) investment in quantum dot technology for its upcoming TVs, as it shifts production away from LCDs. However, Samsung’s existing quantum dot or QLED TVs still use LCD panels behind their quantum dot layer. Samsung is also working on developing self-emissive quantum-dot diodes, which would remove the need for a separate layer.

Although Samsung Display says that it will be able to continue supplying its existing LCD orders through the end of the year, there are questions about what Samsung Electronics, the largest TV manufacturer in the world, will use in its LCD TVs going forward. Samsung told The Vergethat it does not expect the shutdown to affect its LCD-based QLED TV lineup. So for the near-term, nothing changes.

One alternative is that Samsung buys its LCD panels from suppliers like TCL-owned CSOT and AUO, which already supply panels for Samsung TVs. Last year The Elec reported that Samsung could close all its South Korean LCD production lines, and make up the difference with panels bought from Chinese manufacturers like CSOT, which Samsung Display has invested in.

Samsung has also been showing off its MicroLED display technology at recent trade shows, which uses self-emissive LED diodes to produce its pixels. However, in 2019 Samsung predicted that the technology was two or three years away from being viable for use in a consumer product.

LCD manufacturers are mainly located in China, Taiwan, Korea, Japan. Almost all the lcd or TFT manufacturers have built or moved their lcd plants to China on the past decades. Top TFT lcd and oled display manufactuers including BOE, COST, Tianma, IVO from China mainland, and Innolux, AUO from Tianwan, but they have established factories in China mainland as well, and other small-middium sizes lcd manufacturers in China.

China flat display revenue has reached to Sixty billion US Dollars from 2020. there are 35 tft lcd lines (higher than 6 generation lines) in China,China is the best place for seeking the lcd manufacturers.

The first half of 2021, BOE revenue has been reached to twenty billion US dollars, increased more than 90% than thesame time of 2020, the main revenue is from TFT LCD, AMoled. BOE flexible amoled screens" output have been reach to 25KK pcs at the first half of 2021.the new display group Micro LED revenue has been increased to 0.25% of the total revenue as well.

Established in 1993 BOE Technology Group Co. Ltd. is the top1 tft lcd manufacturers in China, headquarter in Beijing, China, BOE has 4 lines of G6 AMOLED production lines that can make flexible OLED, BOE is the authorized screen supplier of Apple, Huawei, Xiaomi, etc,the first G10.5 TFT line is made in BOE.BOE main products is in large sizes of tft lcd panel,the maximum lcd sizes what BOE made is up to 110 inch tft panel, 8k resolution. BOE is the bigger supplier for flexible AM OLED in China.

As the market forecast of 2022, iPhone OLED purchasing quantity would reach 223 million pcs, more 40 million than 2021, the main suppliers of iPhone OLED screen are from Samsung display (61%), LG display (25%), BOE (14%). Samsung also plan to purchase 3.5 million pcs AMOLED screen from BOE for their Galaxy"s screen in 2022.

Technology Co., Ltd), established in 2009. CSOT is the company from TCL, CSOT has eight tft LCD panel plants, four tft lcd modules plants in Shenzhen, Wuhan, Huizhou, Suzhou, Guangzhou and in India. CSOTproviding panels and modules for TV and mobile

three decades.Tianma is the leader of small to medium size displays in technologyin China. Tianma have the tft panel factories in Shenzhen, Shanhai, Chendu, Xiamen city, Tianma"s Shenzhen factory could make the monochrome lcd panel and LCD module, TFT LCD module, TFT touch screen module. Tianma is top 1 manufactures in Automotive display screen and LTPS TFT panel.

Tianma and BOE are the top grade lcd manufacturers in China, because they are big lcd manufacturers, their minimum order quantity would be reached 30k pcs MOQ for small sizes lcd panel. price is also top grade, it might be more expensive 50%~80% than the market price.

Established in 2005, IVO is located in Kunsan,Jiangshu province, China, IVO have more than 3000 employee, 400 R&D employee, IVO have a G-5 tft panel production line, IVO products are including tft panel for notebook, automotive display, smart phone screen. 60% of IVO tft panel is for notebook application (TOP 6 in the worldwide), 23% for smart phone, 11% for automotive.

Besides the lcd manufacturers from China mainland,inGreater China region,there are other lcd manufacturers in Taiwan,even they started from Taiwan, they all have built the lcd plants in China mainland as well,let"s see the lcd manufacturers in Taiwan:

Innolux"s 14 plants in Taiwan possess a complete range of 3.5G, 4G, 4.5G, 5G, 6G, 7.5G, and 8.5G-8.6G production line in Taiwan and China mainland, offering a full range of large/medium/small LCD panels and touch-control screens.including 4K2K ultra-high resolution, 3D naked eye, IGZO, LTPS, AMOLED, OLED, and touch-control solutions,full range of TFT LCD panel modules and touch panels, including TV panels, desktop monitors, notebook computer panels, small and medium-sized panels, and medical and automotive panels.

AUO is the tft lcd panel manufacturers in Taiwan,AUO has the lcd factories in Tianma and China mainland,AUOOffer the full range of display products with industry-leading display technology,such as 8K4K resolution TFT lcd panel, wide color gamut, high dynamic range, mini LED backlight, ultra high refresh rate, ultra high brightness and low power consumption. AUO is also actively developing curved, super slim, bezel-less, extreme narrow bezel and free-form technologies that boast aesthetic beauty in terms of design.Micro LED, flexible and foldable AMOLED, and fingerprint sensing technologies were also developed for people to enjoy a new smart living experience.

Hannstar was found in 1998 in Taiwan, Hannstar display hasG5.3 TFT-LCD factory in Tainan and the Nanjing LCM/Touch factories, providing various products and focus on the vertical integration of industrial resources, creating new products for future applications and business models.

driver, backlight etc ,then make it to tft lcd module. so its price is also more expensive than many other lcd module manufacturers in China mainland.

Maclight products included monochrome lcd, TFT lcd module and OLED display, touch screen module, Maclight is special in custom lcd display, Sunlight readable tft lcd module, tft lcd with capacitive touch screen. Maclight is the leader of round lcd display. Maclight is also the long term supplier for many lcd companies in USA and Europe.

If you want tobuy lcd moduleorbuy tft screenfrom China with good quality and competitive price, Maclight would be a best choice for your glowing business.

Long-time display manufacturer Samsung Display will likely stop the production of LCD displays this year. A recent report says several factors have influenced the South Korean firm’s decision.

Samsung has been a reputed LCD display manufacturer since 1991. It manufactures panels for its own devices and also works as a supplier for several other Big Tech firms, such as Apple. Its displays are used in virtually all products, ranging from foldable smartphones to televisions and tablets.

Despite the company’s successful business, a recent report from The Korea Times suggests Apple is exiting the LCD production business for good. One of the biggest reasons cited for the decision is the increased competition from Chinese and Taiwanese display manufacturers in the recent past.

Samsung wanted to shut its LCD production late in 2020 and its move was on the cards for a while now. Samsung probably kept its LCD manufacturing facilities operational during the pandemic due to the sudden and unprecedented spike in demand. However, LCD technology has been eclipsed by OLED and QD-OLED technologies on most mainstream devices in the last few years. This is another reason why Samsung will probably shutter the business later this year.

Moreover, research firm Display Supply Chain Consultants (DSCC) believes the average price index of LCD panels measured as 100 in January 2014 will drop down to just 36.6 in September 2022. The figure is indicative of the demand for LCD panels and it plummeted to a record low of 41.5 in April this year. The April figure is a whopping 58 percent lower than the record-high index value of 87 in June 2021 when the pandemic was raging. This reduction in demand and price could also be detrimental to the company’s plans to soldier on producing LCDs.

The report says that in the future, Samsung will remain focused on manufacturing OLED panels and more advanced quantum dot OLED displays. LCD division staffers will likely be transferred to the QD-OLED division. Meanwhile, Samsung Display did not respond to the Korea Times’ request for comment.

In recent years, China and other countries have invested heavily in the research and manufacturing capacity of display technology. Meanwhile, different display technology scenarios, ranging from traditional LCD (liquid crystal display) to rapidly expanding OLED (organic light-emitting diode) and emerging QLED (quantum-dot light-emitting diode), are competing for market dominance. Amidst the trivium strife, OLED, backed by technology leader Apple"s decision to use OLED for its iPhone X, seems to have a better position, yet QLED, despite still having technological obstacles to overcome, has displayed potential advantage in color quality, lower production costs and longer life.

Zhao: We all know display technologies are very important. Currently, there are OLED, QLED and traditional LCD technologies competing with each other. What are their differences and specific advantages? Shall we start from OLED?

Huang: OLED has developed very quickly in recent years. It is better to compare it with traditional LCD if we want to have a clear understanding of its characteristics. In terms of structure, LCD largely consists of three parts: backlight, TFT backplane and cell, or liquid section for display. Different from LCD, OLED lights directly with electricity. Thus, it does not need backlight, but it still needs the TFT backplane to control where to light. Because it is free from backlight, OLED has a thinner body, higher response time, higher color contrast and lower power consumption. Potentially, it may even have a cost advantage over LCD. The biggest breakthrough is its flexible display, which seems very hard to achieve for LCD.

Liao: Actually, there were/are many different types of display technologies, such as CRT (cathode ray tube), PDP (plasma display panel), LCD, LCOS (liquid crystals on silicon), laser display, LED (light-emitting diodes), SED (surface-conduction electron-emitter display), FED (filed emission display), OLED, QLED and Micro LED. From display technology lifespan point of view, Micro LED and QLED may be considered as in the introduction phase, OLED is in the growth phase, LCD for both computer and TV is in the maturity phase, but LCD for cellphone is in the decline phase, PDP and CRT are in the elimination phase. Now, LCD products are still dominating the display market while OLED is penetrating the market. As just mentioned by Dr Huang, OLED indeed has some advantages over LCD.

Huang: Despite the apparent technological advantages of OLED over LCD, it is not straightforward for OLED to replace LCD. For example, although both OLED and LCD use the TFT backplane, the OLED’s TFT is much more difficult to be made than that of the voltage-driven LCD because OLED is current-driven. Generally speaking, problems for mass production of display technology can be divided into three categories, namely scientific problems, engineering problems and production problems. The ways and cycles to solve these three kinds of problems are different.

At present, LCD has been relatively mature, while OLED is still in the early stage of industrial explosion. For OLED, there are still many urgent problems to be solved, especially production problems that need to be solved step by step in the process of mass production line. In addition, the capital threshold for both LCD and OLED are very high. Compared with the early development of LCD many years ago, the advancing pace of OLED has been quicker.While in the short term, OLED can hardly compete with LCD in large size screen, how about that people may change their use habit to give up large screen?

Liao: I want to supplement some data. According to the consulting firm HIS Markit, in 2018, the global market value for OLED products will be US$38.5 billion. But in 2020, it will reach US$67 billion, with an average compound annual growth rate of 46%. Another prediction estimates that OLED accounts for 33% of the display market sales, with the remaining 67% by LCD in 2018. But OLED’s market share could reach to 54% in 2020.

Huang: While different sources may have different prediction, the advantage of OLED over LCD in small and medium-sized display screen is clear. In small-sized screen, such as smart watch and smart phone, the penetration rate of OLED is roughly 20% to 30%, which represents certain competitiveness. For large size screen, such as TV, the advancement of OLED [against LCD] may need more time.

Xu: LCD was first proposed in 1968. During its development process, the technology has gradually overcome its own shortcomings and defeated other technologies. What are its remaining flaws? It is widely recognized that LCD is very hard to be made flexible. In addition, LCD does not emit light, so a back light is needed. The trend for display technologies is of course towards lighter and thinner (screen).

But currently, LCD is very mature and economic. It far surpasses OLED, and its picture quality and display contrast do not lag behind. Currently, LCD technology"s main target is head-mounted display (HMD), which means we must work on display resolution. In addition, OLED currently is only appropriate for medium and small-sized screens, but large screen has to rely on LCD. This is why the industry remains investing in the 10.5th generation production line (of LCD).

Xu: While deeply impacted by OLED’s super thin and flexible display, we also need to analyse the insufficiency of OLED. With lighting material being organic, its display life might be shorter. LCD can easily be used for 100 000 hours. The other defense effort by LCD is to develop flexible screen to counterattack the flexible display of OLED. But it is true that big worries exist in LCD industry.

LCD industry can also try other (counterattacking) strategies. We are advantageous in large-sized screen, but how about six or seven years later? While in the short term, OLED can hardly compete with LCD in large size screen, how about that people may change their use habit to give up large screen? People may not watch TV and only takes portable screens.

Some experts working at a market survey institute CCID (China Center for Information Industry Development) predicted that in five to six years, OLED will be very influential in small and medium-sized screen. Similarly, a top executive of BOE Technology said that after five to six years, OLED will counterweigh or even surpass LCD in smaller sizes, but to catch up with LCD, it may need 10 to 15 years.

Xu: Besides LCD, Micro LED (Micro Light-Emitting Diode Display) has evolved for many years, though people"s real attention to the display option was not aroused until May 2014 when Apple acquired US-based Micro LED developer LuxVue Technology. It is expected that Micro LED will be used on wearable digital devices to improve battery"s life and screen brightness.

Micro LED, also called mLED or μLED, is a new display technology. Using a so-called mass transfer technology, Micro LED displays consist of arrays of microscopic LEDs forming the individual pixel elements. It can offer better contrast, response times, very high resolution and energy efficiency. Compared with OLED, it has higher lightening efficiency and longer life span, but its flexible display is inferior to OLED. Compared with LCD, Micro LED has better contrast, response times and energy efficiency. It is widely considered appropriate for wearables, AR/VR, auto display and mini-projector.

However, Micro LED still has some technological bottlenecks in epitaxy, mass transfer, driving circuit, full colorization, and monitoring and repairing. It also has a very high manufacturing cost. In short term, it cannot compete traditional LCD. But as a new generation of display technology after LCD and OLED, Micro LED has received wide attentions and it should enjoy fast commercialization in the coming three to five years.

Peng: It comes to quantum dot. First, QLED TV on market today is a misleading concept. Quantum dots are a class of semiconductor nanocrystals, whose emission wavelength can be continuously tuned because of the so-called quantum confinement effect. Because they are inorganic crystals, quantum dots in display devices are very stable. Also, due to their single crystalline nature, emission color of quantum dots can be extremely pure, which dictates the color quality of display devices.

Interestingly, quantum dots as light-emitting materials are related to both OLED and LCD. The so-called QLED TVs on market are actually quantum-dot enhanced LCD TVs, which use quantum dots to replace the green and red phosphors in LCD’s backlight unit. By doing so, LCD displays greatly improve their color purity, picture quality and potentially energy consumption. The working mechanisms of quantum dots in these enhanced LCD displays is their photoluminescence.

For its relationship with OLED, quantum-dot light-emitting diode (QLED) can in certain sense be considered as electroluminescence devices by replacing the organic light-emitting materials in OLED. Though QLED and OLED have nearly identical structure, they also have noticeable differences. Similar to LCD with quantum-dot backlighting unit, color gamut of QLED is much wider than that of OLED and it is more stable than OLED.

Another big difference between OLED and QLED is their production technology. OLED relies on a high-precision technique called vacuum evaporation with high-resolution mask. QLED cannot be produced in this way because quantum dots as inorganic nanocrystals are very difficul

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey