lcd panel supply chain supplier

DSCC’s mission is provide worldwide end-to-end supply chain expertise for all display-based products. To accomplish this, we have established close relationships with the display supply chain from component and equipment suppliers to flat panel suppliers, OEMs, brands and even retailers. This has been achieved by the extensive experience of its founders and employees which have decades of experience covering every layer of the display supply chain. Meet the DSCC team here and read what clients have to say about DSCC here.

On panel shipments, we survey panel suppliers, brands as well as component suppliers to ensure there is enough supply to meet demand. By knowing glass input as well as panel shipments, this also allows us to quantify yields.

For every display application, in addition to tracking supply and demand, we also quantify costs, prices and margins and factor into account regional differences.

VISLCD has been engaged in LCD production and sales for 9 years, and we have met many customers who shared with us that they had encountered unreliable LCD suppliers.

For example, the answer is not what you asked for, the LCD product cannot be delivered on time, the price of the LCD suddenly increases, the LCD module suddenly breaks down during the use of the product, or even the LCD is discontinued after less than 1 year of delivery…etc. In addition, there are many customers who are not sure what type of LCD supplier they are looking for.

In view of all the above, VISLCD has written this article to share knowledge about LCD suppliers and other issues related to LCD. We believe it will be helpful to LCD customers.

To understand LCD suppliers, we first need to know what kinds of LCD suppliers are available. Then LCD customers can find the right supplier based on information such as their product applications, LCD requirements and forecast volume.

LCD original manufacturer refers to the original manufacturer of LCD panel. Originated from the USA in the 1960’s, after more than 50 years of development, the manufacturers are now mainly located in China mainland, Korea and Taiwan. Among them, the Chinese manufacturers in recent years rely on the rapid scale, technology development and price advantage, has gradually occupied the main market share.

The video below is an official video presentation of the BOE display factory and Century Display (CTC), which will give you a more visual understanding of the original LCD manufacturer.

The 5.1 generation TFT-LCD line of Century Display in Shenzhen, China, for example, has been put into operation since 2008 with a cumulative fixed investment of more than $4 billion, and the cost of water, electricity, employee wages and equipment depreciation is as high as $0.5~100 million/month. The monthly production capacity is about 100,000 sheets ( 1300*1200mm/sheet). If all of them are used to produce 7-inch LCD panels, then the monthly shipment volume is up to 9,000,000 pcs. Therefore, a very large monthly shipment volume is required to meet the normal operation of the factory.

This is only the 5.1 generation TFT-LCD line, if it is 8.5 generation line or even 10 generation line or more, then the cost and shipment volume may be several times or even ten times more. It should be noted that the number of generations of LCD lines does not mean that the technology is high or low. The higher the generation, then the larger the size of the LCD can be put into production, of course, the greater the volume of shipments and investment amount.

LCD original manufacturers generally provide mainly LCD panels, but also provide COG (LCD + IC), FOG (LCD + IC + FPCA cable) and other kinds of LCD semi-finished products. Also includes a small amount of the original LCD module. But the original LCD factory will only deal with the famous brand companies directly (such as Apple, Dell, Xiaomi, etc.), or through agents to ship. And the MOQ quantity requirement is very high (generally 1,000,000 pcs/month or more), the unit price of original LCD module is also high and the degree of customization is low.

LCD original manufacturers usually have an order MOQ requirement for their agents, which translates into an LCD unit quantity of no less than 100,000pcs/month. When the LCD demand is high, this will not be a problem; but when the market is low, the agent must buy the agreed MOQ quantity of LCD from the original LCD manufacturer even if there is no customer demand for the time being. So when the low season, if your order quantity is large enough, then you may get a very good LCD panel price from the LCD agent, which may even be lower than the agent’s purchase price.

LCD module manufacturers is to purchase LCD semi-finished products (such as LCD panel, COG or FOG) from LCD agents, then purchase ICs from IC agents, produce or purchase backlight, FPCA cable and touch screen components, and then integrate all the above components into LCD module or touch LCD module. LCD module factories vary in size from tens of millions of pcs to hundreds of thousands of pcs shipped per month.

Medium and large size module factory generally get the semi-finished products are FOG LCD (also known as open cell LCD) from the original LCD manufacturers or LCD agents, and then add the backlight assembly into the finished LCD module. The advantage of doing so is that the quality is relatively stable, but the degree of customization will be much lower. Because FOG LCD already includes FPCA cable, generally speaking, the only thing that can be customized is the brightness of the backlight and the touch panel and cover glass (if needed). The rest are difficult to change, unless the customer’s LCD demand is very large.

The small and medium size module factory after years of mature development of the industry, the degree of customization will be much more flexible. The semi-finished products are mainly LCD panels, which means that the backlight size, backlight brightness, FPCA cable design, shape and PIN number, as well as the touch panel and cover glass can all be customized according to the customer’s requirements. But the MOQ requirement is higher for the backlight size. Other parts of the customization generally require LCD MOQ of at least 2,000~5,000 pcs, which varies depending on the LCD size.

Since LCD module manufactures vary in size and quality control(especially small and medium size LCD module factories), and most of the components are sourced, the selection of module factories is particularly important if customers want to buy LCDs with good quality and competitive prices.

For example, if the factory’s customers are mostly low-cost products or repaired product manufacturers, then it can be assumed that the quality of his products is not too good, LCD panels and some other components may be B-grade products, not A, can only meet short-term use.

This is essential to ensure supply. In case of supply shortage, many module factories with insufficient upstream channels sometimes cannot even start production. Because they can not buy raw materials such as LCD panels and ICs.

As the name implies, trading companies do not have their own factories, but directly sell finished LCD products from LCD resellers or LCD modules from module manufacturers. Generally speaking, the LCD prices of trading companies are relatively high and the quality and reliability are a little weaker. However, there is no shortage of good trading companies with good quality management teams and good upstream channel resources. The biggest advantage of trading companies is their flexibility, which can meet the diversified needs of customers.

2) Shenzhen has 3 types of buildings related to lcd (including other electronic products): office buildings, factories and markets. Almost all LCD panel and IC agents are located in various office buildings in Shenzhen, while component factories such as FPCA, Touch panel and backlight are located in various industrial parks in the suburbs. It is possible to find the right components and develop new products in the shortest time. Of course, there is also the famous Huaqiang bei(north) Electronic Market, a very complex place.

VISLCD was a trading company in the early days. But after nearly 9 years of development, it has developed into a combination of LCD module factory and LCD agent. The company is located in LCD base Shenzhen, China and operates in both Hong Kong and Shenzhen. We have our own module factory and have direct relationship with Century Display, LG, HKC and other LCD original manufacturers. Our main employees are also from these LCD manufacturers. We also accept all kinds of customized LCD business. Therefore, VISLCD is one of the best choices for medium-sized customers in terms of quality stability, semi-finished parts supply and customization.

In both LCD and OLED displays, producing these cells – which are highly complex – is by far the most difficult element of the production process. Indeed, the complexity of these cells, combined with the levels of investment needed to achieve expertise in their production, explains why there are less than 30 companies in the whole world that can produce them. China, for instance, has invested more than 300 billion yuan (approximately $45 billion USD) in just one of these companies – BOE – over the past 14 years.

Panox Display has been involved in the display industry for many years and has built strong and long-term partner relationships with many of the biggest OLED and LCD panel manufacturers. As a result, we are able to offer our clients guaranteed access to display products from the biggest manufacturers.

LG Display was, until 2021, the No. 1 display panel manufacturer in the world. Owned by LG Group and headquartered in Seoul, South Korea, it has R&D, production, and trade institutions in China, Japan, South Korea, the United States, and Europe.

Founded in 2001, AUO – or AU Optronics – is the world’s leading TFT-LCD panel manufacturer (with a 16% market share) that designs, develops, and manufactures the world’s top three liquid crystal displays. With panels ranging from as small as 1.5 inches to 46 inches, it boasts one of the world"s few large-, medium -and small-sized product lines.

AUO offers advanced display integration solutions with innovative technologies, including 4K2K ultra-high resolution, 3D, ultra-thin, narrow bezel, transparent display, LTPS, OLED, and touch solutions. AOU has the most complete generation production line, ranging from 3.5G to 8.5G, offering panel products for a variety of LCD applications in a range of sizes, from as small as 1.2 inches to 71 inches.

Now Sharp is still top 10 TV brands all over the world. Just like BOE, Sharp produce LCDs in all kinds of size. Including small LCD (3.5 inch~9.1 inch), medium LCD (10.1 ~27 inch), large LCD (31.5~110 inch). Sharp LCD has been used on Iphone series for a long time.

Beside those current LCDs, the industrial LCD of Sharp is also excellent and widely used in public facilities, factories, and vehicles. The Sharp industrial LCD, just means solid, high brightness, super long working time, highest stability.

Since its establishment, Truly Semiconductors has focused on researching, developing, and manufacturing liquid crystal flat panel displays. Now, after twenty years of development, it is the biggest small- and medium-sized flat panel display manufacturer in China.

Truly’s factory in Shanwei City is enormous, covering an area of 1 million square meters, with a net housing area of more than 100,000 square meters. It includes five LCD production lines, one OLED production line, three touch screen production lines, and several COG, LCM, MDS, CCM, TAB, and SMT production lines.

Its world-class production lines produce LCD displays, liquid crystal display modules (LCMs), OLED displays, resistive and capacitive touch screens (touch panels), micro camera modules (CCMs), and GPS receiving modules, with such products widely used in the smartphone, automobile, and medical industries. The LCD products it offers include TFT, TN, Color TN with Black Mark (TN type LCD display for onboard machines), STN, FSTN, 65K color, and 262K color or above CSTN, COG, COF, and TAB modules.

In its early days, Innolux attached great importance to researching and developing new products. Mobile phones, portable and mounted DVD players, digital cameras, games consoles, PDA LCDs, and other star products were put into mass production and quickly captured the market, winning the company considerable market share.

Looking forward to the future, the group of photoelectric will continue to deep LCD display field, is committed to the development of plane display core technology, make good use of global operations mechanism and depth of division of labor, promise customers high-quality products and services, become the world"s top display system suppliers, in 2006 in the global mobile phone color display market leader, become "Foxconn technology" future sustained rapid growth of the engine.

Founded in June 1998, Hannstar specializes in producing thin-film transistor liquid crystal display panels, mainly for use in monitors, notebook displays and televisions. It was the first company in Taiwan to adopt the world’s top ultra-wide perspective technology (AS-IPS).

The company has three LCD factories and one LCM factory. It has acquired state-of-the-art TFT-LCD manufacturing technology, which enables it to achieve the highest efficiency in the mass production of thin-film transistor liquid crystal display production technology. Its customers include many of the biggest and most well-known electronics companies and computer manufacturers in Taiwan and overseas.

TCL CSOT – short for TCL China Star Optoelectronics Technology (TCL CSOT) – was founded in 2009 and is an innovative technology enterprise that focuses on the production of semiconductor displays. As one of the global leaders in semiconductor display market, it has bases in Shenzhen, Wuhan, Huizhou, Suzhou, Guangzhou, and India, with nine panel production lines and five large modules bases.

TCL CSOT actively produces Mini LED, Micro LED, flexible OLED, printing OLED, and other new display technologies. Its product range is vast – including large, medium, and small panels and touch modules, electronic whiteboards, splicing walls, automotive displays, gaming monitors, and other high-end display application fields – which has enabled it to become a leading player in the global panel industry.

In the first quarter of 2022, TCL CSOT’s TV panels ranked second in the market, 55 inches, 65 " and 75 inches second, 8K, 120Hz first, the first, interactive whiteboard and digital sign plate; LTPS flat panel, the second, LTPS and flexible OLED fourth.

EDO (also known as EverDisplay Optonics) was founded in October 2012 and focuses on the production of small- and medium-sized high-resolution AMOLED semiconductor display panels.

Tianma Microelectronics was founded in 1983 and listed on the Shenzhen Stock Exchange in 1995. It is a high-tech enterprise specializing in the production of liquid crystal displays (LCD) and liquid crystal display modules (LCM).

After more than 30 years of development, it has grown into a large publicly listed company integrating LCD research and development, design, production, sales, and servicing. Over the years, it has expanded by investing in the construction of STN-LCD, CSTN-LCD, TFT-LCD and CF production lines and module factories across China (with locations in Shenzhen, Shanghai, Chengdu, Wuhan and Xiamen), as well R&D centers and offices in Europe, Japan, South Korea and the United States.

JDI (Japan Display Inc.) was established on November 15, 2011, as a joint venture between the Industrial Innovation Corporation, Sony, Hitachi, and Toshiba. It is dedicated to the production and development of small-sized displays. It mainly produces small- and medium-sized LCD display panels for use in the automotive, medical, and industrial fields, as well as personal devices including smartphones, tablets, and wearables.

Although Sony’s TVs use display panels from TCL CSOT (VA panel), Samsung. Sony still produces the world’s best micro-OLED display panels. Sony has many micro OLED model such as 0.23 inch, 0.39 inch, 0.5 inch, 0.64 inch, 0.68 inch, 0.71 inch. Panox Display used to test and sell many of them, compare to other micro OLED manufacuturers, Sony`s micro OLEDs are with the best image quality and highest brightness (3000 nits max).

That’s probably why you need to reevaluate today. Asking the right questions during this process clarifies the conditions you need to work successfully with the LCD display supplier.

Most of the review process is about asking the right questions about your needs to the supplier. Knowing exactly what display requirements the new LCD manufacturer should meet will inform you that they should what are the functions?

The reasons for this can be as varied as mechanical or motion-based constraints or temperature/environmental problems. There are also optical considerations such as contrast, brightness, response time, and perspective, as well as durability and interface requirements. You may also have custom features, such as a button or custom icon on a glass or touch panel.

There is a significant difference between the demand for 2,000 and 200,000 screens per year, not only in large quantities but also in determining whether LCD vendors can effectively meet the demand for mass-produced displays.

Depending on the impact of display changes, suppliers will need to have appropriate configuration controls and obsolescence mitigation in place to ensure that your supply chain is uninterrupted throughout the life cycle of the final product.

Whether you need a JIT order, late inventory, or less than the lead time order, you will determine what LCD display manufacturers need to use to ensure seamless integration.

STONE provides a full range of 3.5 inches to 15.1 inches of small and medium-size Standard Quasi Norris Norris LCD Module, LCD Display, TFT Display Module, Display industry, Industrial LCD Screen, Norris Norris, Norris Norris, Norris Norris. under the sunlight visually highlight TFT LCD display, industrial custom TFT screen, TFT LCD screen-wide temperature, industrial TFT LCD screen, touch screen industry. The TFT LCD module is very suitable for industrial control equipment, medical instruments, POS system, electronic consumer products, vehicles, and other products.

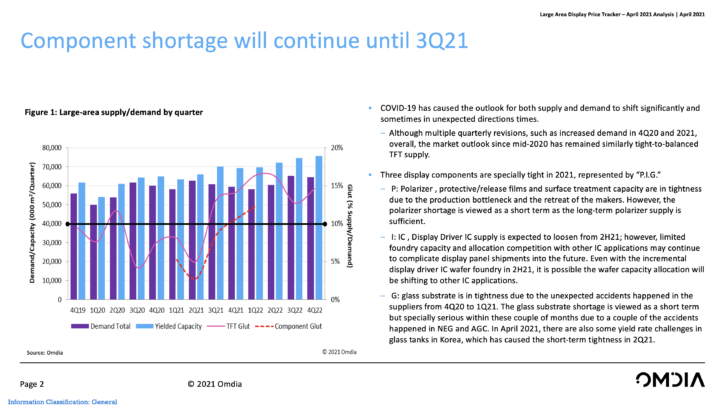

Based on Omdia’s Large Area Display Price Tracker, April 2021, Sanju Khatri, director of consulting for displays, ProAV and consumer devices at research and consultancy firm Omdia, provided some analysis on disruption in the display supply chain due to component shortage and high demand. Impact will be mostly felt on LCD technology, as strong demand and component shortage will lead to the following price cycles for LCD panels.

To read more about the broader supply situation, here’s our interview with manufacturers including Crestron, Valens, Barco, Legrand AV, MXL, and AVIXA .

EDITOR’S NOTE: Three distinct terms are used below. Components (display driver IC, glass, and polarizer); panel (raw LCD panels) and brands/finished sets/device vendors (TV, monitor/laptops/ProAV vendors).

Strong consumer demand for TVs/IT displays. The “at home” trends are including work at home, learn at home, entertain at home and shop at home. The LCD TV, Notebook, LCD monitor, and tablet PC products continue to have the strong demand thanks to the “at home” trends.

Display panel makers are increasing prices sharply to take the fast turnaround on profitability. The LCD TV open cell prices have been increasing by 40%-50% from June 2020 to December 2020. And it is expected there will be another 20% increase from January 2021 to May 2021.

Component shortage(Glass substrate, Display Driver IC, T-con, PMIC, Polarizer films) are frustrating the supply chain from time to time, making the set makers to be more nervous thus giving more orders. Three display components are especially tight in 2021, represented by “P.I.G.”

P: Polarizer, protective/release films and surface treatment capacity are in tightness due to the production bottleneck and the retreat of the makers. However, the polarizer shortage is viewed as a short term as the long-term polarizer supply is sufficient.

I: IC, Display Driver IC supply is expected to loosen from 2H21however, limited foundry capacity and allocation competition with other IC applications may continue to complicate display panel shipments into the future. Even with the incremental display driver IC wafer foundry in the second half of 2021 (2H21), it is possible the wafer capacity allocation will be shifting to other IC applications.

Fluorinated greenhouse gases (F-GHGs) are among the most potent and persistent greenhouse gases (GHGs) contributing to global climate change. These gases play a vital role in the manufacture of flat panel displays--most commonly liquid crystal display (LCD) panels--that go into televisions, computer monitors, and many other display products. The overall climate impact of the millions of display products used can be greatly reduced if suppliers of these components take steps to mitigate release of these F-GHGs to the atmosphere. While progress is underway, your awareness and support as a brand, retailer, or institutional buyer can expedite this effort. This webinar explained the manufacturing processes which release F-GHGs into the environment, how LCD suppliers are working to reduce their emissions, and the steps participants can take to support further improvements.

Apple is always looking to diversify its suppliers; this helps to improve existing technologies and make them less expensive. This time, TCL’s subsidiary CSOT wants to enter Apple’s LCD supply chain for upcoming Macs and iPads.

The publication says that CSOT is a “fierce competitor” to BOE in the global LCD market, but the company is ahead of CSOT in LCD panels for notebooks, tablets, and monitors as well as with the OLED technology for smartphones.

BOE, as you probably know, has for years been a third supplier of displays for Apple’s older LCD iPhones, but only started making OLED panels for Apple as of the iPhone 12. It was on track to pick up orders for 30-40M iPhones this year. It will also be responsible for around five million units of iPhone 14 OLED panels.

Not only that, but BOE is also supplying LCD panels to Apple for MacBooks and iPads. Analyst firm Omdia says the Chinese company will be the largest supplier of LCD panels for iPad this year.

CSOT also formed a team during the first half of the year to review building an OLED production line aimed at iPhones. CSOT’s expansion plan will, besides BOE, also threaten South Korean display maker LG Display, which leads the supply of LCD panels to Apple for high-end devices.

LG Display is expected to supply 14.8 million LCD panels to Apple for MacBooks this year, according to Omdia, making its share in this specific supply chain 55%. Having another competitor in the supply chain like CSOT could add pressure on LG Display to cut unit prices.

Display Logic has developed global sources of supply far beyond those of our competitors. Among those are selected manufacturers with which we have partnered with preferential pricing agreements.

Universal Display Corporation (UDC, or the Company)aims to develop, manufacture and distribute itsenergy-efficientPHOLED products in a safe,and anenvironmentally- andsocially-responsiblemanner.In furtherance of this belief, the Company is committed to responsible sourcing and ethical business practicesthroughout our supply chain.

We expect PPG,our exclusive manufacturer of UniversalPHOLED products, and their supply chain as well asUDC’s othersuppliersand subcontractors to fully comply with all applicable laws and to adhere to internationally recognized environmental, social and governance standards.The Company’sGlobal Supplier Code of Ethicsclearly states our expectations for every supplier and is referenced in our corporate purchase orders to all vendors.

PPG manages the supply chain for UDC’s PHOLED emitters. Many of these suppliers are ISO 9001 or cGMP certified, have a strong commitment to EHS principles and conduct their operations in compliance with the Company’s and PPG’s respective Global Supplier Code of Conduct. As of 2021, PPG included key suppliers into its EcoVadis program, for which PPG was awarded a Gold rating.

Recent observations by market intelligence firm TrendForce suggests that the ongoing expansion of the US semiconductor trade restrictions against China could eventually spread to the display panel industry. Agencies within the US government are taking notice of China’s certain advantages in the development of display technologies and build-up of panel production capacity.

However, the US will unlikely attempt to directly impose control over panel supply with new trade restrictions in the short term. On the other hand, the upstream portion of the supply chain, especially the sections concerning driver ICs and other related semiconductor chips, are starting to react to the tightening of the US sanctions against Chinese semiconductor companies. Furthermore, some electronics OEMs have recently been re-examining their panel supply chains to evaluate the sourcing of semiconductor components. While OEMs have yet to explicitly ban the use of panel-related chips from Chinese suppliers, they are actively developing backup plans that would seek alternative supply sources in case the US further broadens the scope its technology export rules on Chinese companies.

The continuation and strengthening of the restrictions on semiconductor trade is starting to have an effect on the supply chain related to driver ICs. TrendForce’s latest investigation finds signs of decoupling or bifurcation. Specifically, there is a divergence towards both extremes: a supply chain that totally excludes Chinese content versus a counterpart that is “de-Americanized”. Again, looking at OEMs, they have not rejected panels from certain suppliers for now, but they might start to prefer or exclude particular IC design houses that offer driver chips. As for foundries and OSAT providers, decoupling has begun in accordance with the decisions of some downstream customers. In the future, there is a distinct possibility that Chinese IC design houses, foundries and OSAT providers could be barred from participating in the supply chains for the product models targeting the US market.

Conversely, the ban on Chinese suppliers will not apply to product models targeting the Chinese market. Instead, OEMs might actually increase Chinese suppliers’ participation in order to raise the chance of a successfully entry into this region. Component suppliers such as IC design houses, too, could adopt a similar strategy so as to insert themselves into the Chinese market. To comply with and support the localization policy of the Chinese government, component suppliers could increase the portion of partners or clients from China and establish a separate local supply chain.

Presently, Chinese foundries have steadily raised their collective market share for large-sized driver ICs to around 25%. They still have much ground to catch up when compared with the 40% held by Taiwan-based foundries, but this share figure is still significant. If the US government imposes new restrictions seeking to prevent Chinese foundries from using mature semiconductor process technologies to manufacture chips such as driver ICs, then the supply chains for panels and related ICs will likely face another huge wave of capacity crunch and supply shortage.

Nevertheless, since there are no direct orders from the US government targeting panel supply and related components at this moment, TrendForce believes the decoupling process in the supply chain for driver ICs is going to be a slow and drawn-out process. In the long run, decoupling as an overarching trend will make the supply chain more fragmented and inefficient. This development, in turn, will increase the overall cost for all parties involved. Furthermore, due to the need to mitigate the potential risks resulting from the decoupling process, the supply chain could even see an elevation of minimum inventory level and a prolonging of order lead time.

TrendForce holds the view that both risks and opportunities exist in the decoupling and rearrangement of the supply chain. Some IC design houses could gradually redirect wafer input to fabs outside China for some of their offerings in order to eliminate the possible risks associated with the US sanctions or satisfy some customers’ demand for non-Chinese components. Thus, IC design houses and foundries that operate in Taiwan could gain new orders as the supply chain undergoes an internal shakeup. On the other hand, their counterparts in Mainland China could have more opportunities to rise as major players thanks to their government’s strategy for localizing supply chains.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey