lcd panel new pricelist

Prices for all TV panel sizes fluctuated and are forecast to fluctuate between 2020 and 2022. The period from March 2020 to July 2021 saw the biggest price increases, when a 65" UHD panel cost between 171 and 288 U.S. dollars. In the fourth quarter of 2021, such prices fell and are expected to drop to an even lower amount by March 2022.Read moreLCD TV panel prices worldwide from January 2020 to March 2022, by size(in U.S. dollars)Characteristic32" HD43" FHD49"/50" UHD55" UHD65" UHD------

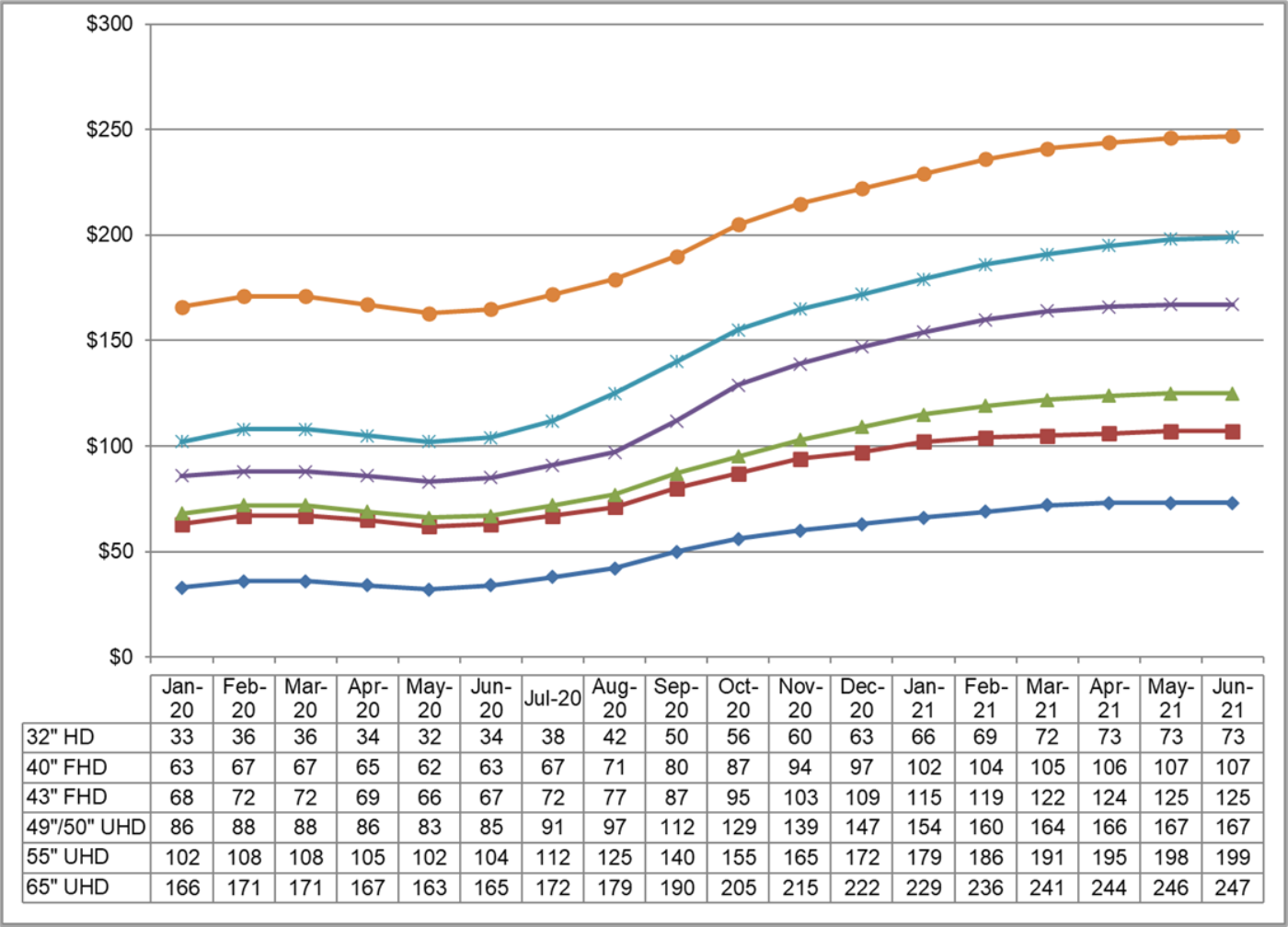

DSCC. (January 10, 2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) [Graph]. In Statista. Retrieved February 20, 2023, from https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars)." Chart. January 10, 2022. Statista. Accessed February 20, 2023. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. (2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars). Statista. Statista Inc.. Accessed: February 20, 2023. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "Lcd Tv Panel Prices Worldwide from January 2020 to March 2022, by Size (in U.S. Dollars)." Statista, Statista Inc., 10 Jan 2022, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC, LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) Statista, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/ (last visited February 20, 2023)

LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) [Graph], DSCC, January 10, 2022. [Online]. Available: https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

LCD TV panel prices reached all-time lows in August but they continue to decline in September, and we continue to forecast that the industry will have an “L-shaped” recovery in the fourth quarter. In other words, no recovery at all until 2023; the only question is how low prices will go before they flatten out. The ‘perfect storm’ of a continued oversupply, near-universally weak demand and excessive inventory throughout the supply chain has combined, and every screen size of TV panel has reached an all-time low price. Although fab utilization slowed sharply starting in July, we do not see any signal to suggest that prices can increase any time soon.

The price of LCD display panels for TVs is still falling in November and is on the verge of falling back to the level at which it initially rose two years ago (in June 2020). Liu Yushi, a senior analyst at CINNO Research, told China State Grid reporters that the wave of “falling tide” may last until June this year. For related panel companies, after the performance surge in the past year, they will face pressure in 2022.

LCD display panel prices for TVs will remain at a high level throughout 2021 due to the high base of 13 consecutive months of increase, although the price of LCD display panels peaked in June last year and began to decline rapidly. Thanks to this, under the tight demand related to panel enterprises last year achieved substantial profit growth.

According to China State Grid, the annual revenue growth of major LCD display panel manufacturers in China (Shentianma A, TCL Technology, Peking Oriental A, Caihong Shares, Longteng Optoelectronics, AU, Inolux Optoelectronics, Hanyu Color Crystal) in 2021 is basically above double digits, and the net profit growth is also very obvious. Some small and medium-sized enterprises directly turn losses into profits. Leading enterprises such as BOE and TCL Technology more than doubled their net profit.

Take BOE as an example. According to the 2021 financial report released by BOE A, BOE achieved annual revenue of 219.31 billion yuan, with a year-on-year growth of 61.79%; Net profit attributable to shareholders of listed companies reached 25.831 billion yuan, up 412.96% year on year. “The growth is mainly due to the overall high economic performance of the panel industry throughout the year, and the acquisition of the CLP Panda Nanjing and Chengdu lines,” said Xu Tao, chief electronics analyst at Citic Securities.

In his opinion, as BOE dynamically optimizes its product structure, and its flexible OLED continues to enter the supply chain of major customers, BOE‘s market share as the panel leader is expected to increase further and extend to the Internet of Things, which is optimistic about the company’s development in the medium and long term.

“There are two main reasons for the ideal performance of domestic display panel enterprises.” A color TV industry analyst believes that, on the one hand, under the effect of the epidemic, the demand for color TV and other electronic products surges, and the upstream raw materials are in shortage, which leads to the short supply of the panel industry, the price rises, and the corporate profits increase accordingly. In addition, as Samsung and LG, the two-panel giants, gradually withdrew from the LCD panel field, they put most of their energy and funds into the OLED(organic light-emitting diode) display panel industry, resulting in a serious shortage of LCD display panels, which objectively benefited China’s local LCD display panel manufacturers such as BOE and TCL China Star Optoelectronics.

Liu Yushi analyzed to reporters that relevant TV panel enterprises made outstanding achievements in 2021, and panel price rise is a very important contributing factor. In addition, three enterprises, such as BOE(BOE), CSOT(TCL China Star Optoelectronics) and HKC(Huike), accounted for 55% of the total shipments of LCD TV panels in 2021. It will be further raised to 60% in the first quarter of 2022. In other words, “simultaneous release of production capacity, expand market share, rising volume and price” is also one of the main reasons for the growth of these enterprises. However, entering the low demand in 2022, LCD TV panel prices continue to fall, and there is some uncertainty about whether the relevant panel companies can continue to grow.

According to Media data, in February this year, the monthly revenue of global large LCD panels has been a double decline of 6.80% month-on-month and 6.18% year-on-year, reaching $6.089 billion. Among them, TCL China Star and AU large-size LCD panel revenue maintained year-on-year growth, while BOE, Innolux, and LG large-size LCD panel monthly revenue decreased by 16.83%, 14.10%, and 5.51% respectively.

Throughout Q1, according to WitsView data, the average LCD TV panel price has been close to or below the average cost, and cash cost level, among which 32-inch LCD TV panel prices are 4.03% and 5.06% below cash cost, respectively; The prices of 43 and 65 inch LCD TV panels are only 0.46% and 3.42% higher than the cash cost, respectively.

The market decline trend is continuing, the reporter queried Omdia, WitsView, Sigmaintel(group intelligence consulting), Oviriwo, CINNO Research, and other institutions regarding the latest forecast data, the analysis results show that the price of the TV LCD panels is expected to continue to decline in April. According to CINNO Research, for example, prices for 32 -, 43 – and 55-inch LCD TV panels in April are expected to fall $1- $3 per screen from March to $37, $65, and $100, respectively. Prices of 65 – and 75-inch LCD TV panels will drop by $8 per screen to $152 and $242, respectively.

“In the face of weak overall demand, major end brands requested panel factories to reduce purchase volumes in March due to high inventory pressure, which led to the continued decline in panel prices in April.” Beijing Di Xian Information Consulting Co., LTD. Vice general manager Yi Xianjing so analysis said.

“Since 2021, international logistics capacity continues to be tight, international customers have a long delivery cycle, some orders in the second half of the year were transferred to the first half of the year, pushing up the panel price in the first half of the year but also overdraft the demand in the second half of the year, resulting in the panel price began to decline from June last year,” Liu Yush told reporters, and the situation between Russia and Ukraine has suddenly escalated this year. It also further affected the recovery of demand in Europe, thus prolonging the downward trend in prices. Based on the current situation, Liu predicted that the bottom of TV panel prices will come in June 2022, but the inflection point will be delayed if further factors affect global demand and lead to additional cuts by brands.

With the price of TV panels falling to the cash cost line, in Liu’s opinion, some overseas production capacity with old equipment and poor profitability will gradually cut production. The corresponding profits of mainland panel manufacturers will inevitably be affected. However, due to the advantages in scale and cost, there is no urgent need for mainland panel manufacturers to reduce the dynamic rate. It is estimated that Q2’s dynamic level is only 3%-4% lower than Q1’s. “We don’t have much room to switch production because the prices of IT panels are dropping rapidly.”

Ovirivo analysts also pointed out that the current TV panel factory shipment pressure and inventory pressure may increase. “In the first quarter, the production line activity rate is at a high level, and the panel factory has entered the stage of loss. If the capacity is not adjusted, the panel factory will face the pressure of further decline in panel prices and increased losses.”

In the first quarter of this year, the retail volume of China’s color TV market was 9.03 million units, down 8.8% year on year. Retail sales totaled 28 billion yuan, down 10.1 percent year on year. Under the situation of volume drop, the industry expects this year color TV manufacturers will also set off a new round of LCD display panel prices war.

Recently, it was announced that the 32-inch and 43-inch panels fell by approximately USD 5 ~ USD 6 in early June, 55-inch panels fell by approximately USD 7, and 65-inch and 75-inch panels are also facing overcapacity pressure, down from USD 12 to USD 14. In order to alleviate pressure caused by price decline and inventory, panel makers are successively planning to initiate more significant production control in 3Q22. According to TrendForce’s latest research, overall LCD TV panel production capacity in 3Q22 will be reduced by 12% compared with the original planning.

As Chinese panel makers account for nearly 66% of TV panel shipments, BOE, CSOT, and HKC are industry leaders. When there is an imbalance in supply and demand, a focus on strategic direction is prioritised. According to TrendForce, TV panel production capacity of the three aforementioned companies in 3Q22 is expected to decrease by 15.8% compared with their original planning, and 2% compared with 2Q22. Taiwanese manufacturers account for nearly 20% of TV panel shipments so, under pressure from falling prices, allocation of production capacity is subject to dynamic adjustment. On the other hand, Korean factories have gradually shifted their focus to high-end products such as OLED, QDOLED, and QLED, and are backed by their own brands. However, in the face of continuing price drops, they too must maintain operations amenable to flexible production capacity adjustments.

TrendForce indicates, that in order to reflect real demand, Chinese panel makers have successively reduced production capacity. However, facing a situation in which terminal demand has not improved, it may be difficult to reverse the decline of panel pricing in June. However, as TV sizes below 55 inches (inclusive) have fallen below their cash cost in May (which is seen as the last line of defense for panel makers) and are even flirting with the cost of materials, coupled with production capacity reduction from panel makers, the price of TV panels has a chance to bottom out at the end of June and be flat in July. However, demand for large sizes above 65 inches (inclusive) originates primarily from Korean brands. Due to weak terminal demand, TV brands revising their shipment targets for this year downward, and purchase volume in 3Q22 being significantly cut down, it is difficult to see a bottom for large-size panel pricing. TrendForce expects that, optimistically, this price decline may begin to dissipate month by month starting in June but supply has yet to reach equilibrium, so the price of large sizes above 65 inches (inclusive) will continue to decline in 3Q22.

TrendForce states, as panel makers plan to reduce production significantly, the price of TV panels below 55 inches (inclusive) is expected to remain flat in 3Q22. However, panel manufacturers cutting production in the traditional peak season also means that a disappointing 2H22 peak season is a foregone conclusion and it will not be easy for panel prices to reverse. However, it cannot be ruled out, as operating pressure grows, the number and scale of manufacturers participating in production reduction will expand further and its timeframe extended, enacting more effective suppression on the supply side, so as to accumulate greater momentum for a rebound in TV panel quotations.

In September, area prices for all screen sizes up to 65” fell in a range from $92 to $106 per square meter, with the 65” area price tied with 32” for the lowest in the industry at $92 per square meter. The largest screen size in our survey, 75” panels, continues to have a premium but that premium has eroded steadily. In June 2022, a 75” panel was priced at $144 per square meter, a $41 or 40% premium over the 32” area price. By September, the 75” premium over 32” had dropped to $27 and 29%. While prices for 65” and smaller panels increased in October, 75” prices stayed flat, and we expect that pattern to continue through Q4 and Q1.

The next chart shows our estimates of cash costs vs. panel prices for large TV panels. While 55” panels have been below cash costs for most of the year, 65” prices reached cash costs in Q2 and for the first time 75” panel prices fell below cash costs in Q3. We expect that 55” and 65” panel prices will increase in Q4 and Q1 2023 but will remain slightly below cash costs.

The drip follows year-on-year increases in 2021 and 2020, which were 26% and 14%, respectively, due to increased demand for liquid crystal display (LCD) panels from the Covid-19 pandemic.

We offer an extensive range of LCD Panels, Moving Display Kit & LED Video Wall. Our never-ending list of LCD panels allows the customers, OEMs & ODMs to enjoy highest level to flexibility when choosing a suitable display for an existing or a new project. However, if you can"t find a appropriate display that is matchingread more...

The price of LCD TV panels continues to fall, and that could be welcome news for anyone who’s in the market to buy a new living room portal in time for the World Cup and the Christmas holidays.

A report this week from the analyst firm Sigmaintell Consulting revealed that LCD panel prices fell again last month, with the cost of 32-inch displays slipping by $2 per panel, and 55-inch units falling by $4 each. Meanwhile, 65-inch panels now cost $8 less, while 65-inch ones are $10 cheaper than they were a month ago.

The price of LCD TV panels has been sliding for months now, since the end of last year. That’s great for consumers of course, with the price of upper-end TVs that use LCD panels falling quite noticeably, including some of the newest models out this year.

Typically, LCD panels that are shipped out from the factory go straight into production once they reach their customer, and then end up in stores as finished TVs within just a few of months. As such, analysts believe the latest price drops will result in some steep discounts on LCD TV prices just before Christmas and Black Friday come around.

LCD display prices are falling because the market is becoming increasingly clogged with panels made by Chinese manufacturers, who’re able to make them more cheaply. Indeed, their competitiveness is so extreme that they have forced traditional South Korean display making giants such as Samsung Display and LG Display to withdraw from the market. Last month it was reported that Samsung will exit completely by the end of this month, while LG has drastically reduced its own production and is likely to quit altogether in the coming months.

There were fears that recent COVID-19 related lockdowns in China might push LCD prices back up again, however that didn"t happen, and with cities like Beijing and Shanghai now reopening, it’s expected that the downward price pressure will continue unabated, Sigmaintell Consulting said.

For anyone who’s struggling with the increased living costs that have resulted from higher inflation this year, the TV price drop will come as a welcome surprise. Many households have no doubt tried to avoid making big purchases such as a new TV, but if you need one then it becomes an almost essential buy. With any luck, people in that situation will soon be able to get their hands on a decent new box without breaking the bank.

Large LCD panel prices have been continuously increasing for last 10 months due to an increase in demand and tight supply. This has helped the LCD industry to recover from drastic panel price reductions, revenue and profit loss in 2019. It has also contributed to the growth of QD and miniLED LCD TV. Strong LCD TV panel demand is expected to continue in 2021, but component shortages, supply constraints, and very high panel price increase can still create uncertainties.

It was earlier anticipated that price increases would decelerate in 2Q, but now the price increase is accelerating compared to 1Q, according to a research by DSCC. Panel prices increased by 27 percent in 4Q20 compared to 3Q and slowed down to 14.5 percent in 1Q21 compared to 4Q, but the current estimate is that average LCD TV panel prices in 2Q21 will increase by another 17 percent. The prices are expected to peak sometime in 3Q21.

Prices increased in 1Q21 for all sizes of TV panels, with double-digit percentage increases in sizes from 32- to 65-inch ranging from 12-18 percent. Prices for 75-inch increased by 8 percent as capacity has continued to increase on Gen 10.5 lines, where 75-inch is an efficient six-cut. Prices for every size of TV panel will continue to increase in 2Q at an even faster rate, ranging from 12 percent for 75-inch to 24 percent for 32-inch. The prices are expected to continue to increase in 3Q.

The current upturn in the crystal cycle has seen the biggest trough-to-peak price increases for LCD TV panels, and the recent acceleration of prices has further extended this record. Comparing the forecast for June 2021 panel prices with the prices in May 2020, there is a trough-to-peak increases from 34 percent for 75-inch to 181 percent for 32-inch, with an average of 111 percent. In comparison, the average trough-to-peak increase of the 2016 to 2017 cycle was 48 percent, and prior cycles saw smaller increases.

Before the current upswing, the largest panels sold with an area premium, but the current cycle has flipped that upside down. Whereas in May 2020, 75-inch panels sold at an area premium of USD 77 per square meter higher than the 32-inch panel price, as of May 2021, they are selling at a USD 65 discount on an area basis. This means that those Gen 10.5 fabs could earn higher revenues from making 32-inch panels than from 75-inch panels. The pattern for 65-inch is even more severe, and 65-inch is now selling at a USD 69 per square meter discount (alternately, a 22% area discount) compared to 32-inch.

The improved pricing for LCD TV panels has already improved the profitability of panel makers. It will continue to drive their profits even higher, especially the two prominent Taiwanese players, who have Gen 7.5 and Gen 8.5 fabs but no Gen 10.5 fabs. Chinese panel makers HKC and CHOT have a similar industrial profile and stand to benefit greatly as well. The leading companies with Gen 10.5 fabs (BOE, CSOT and Foxconn/Sharp) stand to benefit less because the price increases on the largest sizes are more modest, but every LCD panel maker is doing well.

TV makers continued to make strong profits in 1Q21 despite increasing panel prices. The TV market typically slows down in 1Q and 2Q. TV maker revenues declined seasonally in 1Q but less than usual, and the operating margins for both Samsung and LGE increased sequentially. Samsung’s CE division operating profits exceeded USD 1 billion for the quarter for only the second time ever. With demand remaining strong, TV makers have weathered the increase in panel prices and remained very profitable.

There is a surge in LCD equipment spending to respond to dramatically improved market conditions in the LCD market. DSCC sees LCD revenues rising 32 percent in 2021 to USD 112 billion on strong unit and area growth with prices and profitability rebounding to or even exceeding the 2017 levels. With LCD suppliers able to sell everything they can make at attractive margins; it should be no surprise that most LCD manufacturers are looking to expand capacity.

However, unlike previous upturns when many new fabs were built, in this upturn panel suppliers are looking to stretch their capacity through smaller investments, simplifying their processes and debottlenecking. Having said that, there will be two new Gen 8.6 mega fabs being built. The result versus last quarter is a 10 percent or a USD 2.2 billion increase in 2020-2024 LCD spending from USD 21.8 billion to USD 24 billion. The 2021 LCD equipment spending forecast is up 15 percent versus last quarter’s forecast to USD 10 billion, with 2021 LCD equipment spending up 125 percent versus 2021. In addition, 2022 was upgraded by 28 percent to USD 3.5 billion.

Although there is a healthy upgrade in LCD equipment spending in 2021 and 2022, the outlook for 2022-2024 spending is still significantly lower than in previous years, resulting in tighter capacity and slower price reductions in the next downturn. In addition, with Korean LCD suppliers expected to reduce their LCD capacity and convert to potentially higher margin OLEDs, the outlook for LCD pricing and profitability looks quite healthy, which may result in even more equipment spending, especially as miniLEDs gain acceptance.

Widespread component supply shortages could impact availability on LCD TV panels from CSOT and Innolux. The display panel manufacturers have warned that supplies of panels are expected to be tight throughout the year.

According to Li Dongsheng, chairman, TCL, panel shortages will continue in 1H21, following conditions already hampered last year during the start of the COVID-19 pandemic. The situation for 2H21 remains to be seen but for 2021 overall panel supply will be tight.

James Yang, president, Innolux, has warned of a shortage in LCD panels caused by strong demand for LCD coming out of the global crisis and the conditions are expected to continue through 2021. Innolux has seen shortages in LCD components including power semiconductors, driver ICs and glass substrates that have kept production below capacity. Shortages of ICs and semiconductors could continue right up to the 1H22.

Ironically, prior to the run-on LCD panel supplies, manufacturers were faced with the dilemma of overproduction causing a glut in inventory, which was driving prices artificially lower. This was the result of giant new LCD fabs coming online in China and other areas of Asia.

Panel makers, being cognizant of that threat, are expected to produce panels at a more tempered pace to keep margins healthy. LCD panel prices continued to rise in March after moving up in February.

Almost all Chinese panel makers are doing everything they can to incrementally increase their current factories’ capacities through productivity enhancements and new equipment purchases for debottlenecking or capacity expansions. For the same reasons, South Korean panel makers continue to delay shutting down their domestic LCD TV factories.

TV manufacturers have been moving aggressively to replenish inventories of LCD panels to meet strong sales of TVs and other devices to meeting escalating demand, particularly in the United States and Europe.

An increase in demand for larger size TVs in 2H20 combined with component shortages has pushed the market to supply constraint and caused continuous panel price increases from June 2020 to March 2021. The panel price increase resulting in higher costs for TV brands. It has also made it difficult for lower priced brands to acquire enough panels to offer lower priced TVs. Further, panel suppliers are giving priority to top brands with larger orders during supply constraint.

For 3 years, from 2017 to 2020, LCD panel makers suffered through a continuous pattern of price declines interrupted only with brief respites. With the COVID-19 demand surge assisted by shortages in glass and DDICs, panel prices are spiking. Korean, Taiwanese, and Chinese panel makers are reporting robust margins in 1Q 2021 and the good news is anticipated for panel makers to get even better in 2Q.

SEOUL, April 27 (Reuters) - LG Display Co Ltd (034220.KS) saw first-quarter profit plummet far below forecasts and warned of a further drop in panel prices as pandemic-driven demand for TVs, smartphones and laptops fades and competition heats up.

The South Korean Apple Inc (AAPL.O) supplier said it would shift its focus to higher-end products and gradually lower production of more commoditised LCD TV panels where it lacked a competitive advantage over cheaper Chinese rivals.

The LCD TV market shrank by more than 10% in the first quarter and Chinese competitors are pricing their products lower than LG Display"s expectations, Lee Tai-jong, head of the company"s large display marketing division, said on a call with analysts.

"Margins have been squeezed chiefly due to panel price declines and weaker demand, as consumers have already bought many screens during COVID-19 in the past two years," said Kim Yang-jae, an analyst at DAOL Investment & Securities.

In the first quarter, prices of 55-inch liquid crystal display (LCD) panels for TV sets fell 16% from the previous quarter while prices of LCD panels for notebooks and monitors dropped by around 7% to 11%, according to data from TrendForce"s WitsView.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey