world's largest lcd panel manufacturer price

Flat-panel displays are thin panels of glass or plastic used for electronically displaying text, images, or video. Liquid crystal displays (LCD), OLED (organic light emitting diode) and microLED displays are not quite the same; since LCD uses a liquid crystal that reacts to an electric current blocking light or allowing it to pass through the panel, whereas OLED/microLED displays consist of electroluminescent organic/inorganic materials that generate light when a current is passed through the material. LCD, OLED and microLED displays are driven using LTPS, IGZO, LTPO, and A-Si TFT transistor technologies as their backplane using ITO to supply current to the transistors and in turn to the liquid crystal or electroluminescent material. Segment and passive OLED and LCD displays do not use a backplane but use indium tin oxide (ITO), a transparent conductive material, to pass current to the electroluminescent material or liquid crystal. In LCDs, there is an even layer of liquid crystal throughout the panel whereas an OLED display has the electroluminescent material only where it is meant to light up. OLEDs, LCDs and microLEDs can be made flexible and transparent, but LCDs require a backlight because they cannot emit light on their own like OLEDs and microLEDs.

Liquid-crystal display (or LCD) is a thin, flat panel used for electronically displaying information such as text, images, and moving pictures. They are usually made of glass but they can also be made out of plastic. Some manufacturers make transparent LCD panels and special sequential color segment LCDs that have higher than usual refresh rates and an RGB backlight. The backlight is synchronized with the display so that the colors will show up as needed. The list of LCD manufacturers:

Organic light emitting diode (or OLED displays) is a thin, flat panel made of glass or plastic used for electronically displaying information such as text, images, and moving pictures. OLED panels can also take the shape of a light panel, where red, green and blue light emitting materials are stacked to create a white light panel. OLED displays can also be made transparent and/or flexible and these transparent panels are available on the market and are widely used in smartphones with under-display optical fingerprint sensors. LCD and OLED displays are available in different shapes, the most prominent of which is a circular display, which is used in smartwatches. The list of OLED display manufacturers:

MicroLED displays is an emerging flat-panel display technology consisting of arrays of microscopic LEDs forming the individual pixel elements. Like OLED, microLED offers infinite contrast ratio, but unlike OLED, microLED is immune to screen burn-in, and consumes less power while having higher light output, as it uses LEDs instead of organic electroluminescent materials, The list of MicroLED display manufacturers:

LCDs are made in a glass substrate. For OLED, the substrate can also be plastic. The size of the substrates are specified in generations, with each generation using a larger substrate. For example, a 4th generation substrate is larger in size than a 3rd generation substrate. A larger substrate allows for more panels to be cut from a single substrate, or for larger panels to be made, akin to increasing wafer sizes in the semiconductor industry.

"Samsung Display has halted local Gen-8 LCD lines: sources". THE ELEC, Korea Electronics Industry Media. August 16, 2019. Archived from the original on April 3, 2020. Retrieved December 18, 2019.

"TCL to Build World"s Largest Gen 11 LCD Panel Factory". www.businesswire.com. May 19, 2016. Archived from the original on April 2, 2018. Retrieved April 1, 2018.

"Panel Manufacturers Start to Operate Their New 8th Generation LCD Lines". 대한민국 IT포털의 중심! 이티뉴스. June 19, 2017. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"TCL"s Panel Manufacturer CSOT Commences Production of High Generation Panel Modules". www.businesswire.com. June 14, 2018. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"Samsung Display Considering Halting Some LCD Production Lines". 비즈니스코리아 - BusinessKorea. August 16, 2019. Archived from the original on April 5, 2020. Retrieved December 19, 2019.

Herald, The Korea (July 6, 2016). "Samsung Display accelerates transition from LCD to OLED". www.koreaherald.com. Archived from the original on April 1, 2018. Retrieved April 1, 2018.

www.etnews.com (30 June 2017). "Samsung Display to Construct World"s Biggest OLED Plant". Archived from the original on 2019-06-09. Retrieved 2019-06-09.

"China"s BOE to have world"s largest TFT-LCD+AMOLED capacity in 2019". ihsmarkit.com. 2017-03-22. Archived from the original on 2019-08-16. Retrieved 2019-08-17.

BOE Technology Group, the Chinese electronic components producer, is expected to be the leader in producing LCD display panels in the coming years, with a forecast capacity share of 24 percent by 2022. China is the country that has the largest LCD capacity, with a 56 percent share in 2020.Read moreLCD panel production capacity share from 2016 to 2022, by manufacturerCharacteristicBOEChina StarInnoluxAUOLGDHKCCEC PandaSharpSDCOther-----------

DSCC. (June 8, 2020). LCD panel production capacity share from 2016 to 2022, by manufacturer [Graph]. In Statista. Retrieved January 31, 2023, from https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. "LCD panel production capacity share from 2016 to 2022, by manufacturer." Chart. June 8, 2020. Statista. Accessed January 31, 2023. https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. (2020). LCD panel production capacity share from 2016 to 2022, by manufacturer. Statista. Statista Inc.. Accessed: January 31, 2023. https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. "Lcd Panel Production Capacity Share from 2016 to 2022, by Manufacturer." Statista, Statista Inc., 8 Jun 2020, https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC, LCD panel production capacity share from 2016 to 2022, by manufacturer Statista, https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/ (last visited January 31, 2023)

LCD panel production capacity share from 2016 to 2022, by manufacturer [Graph], DSCC, June 8, 2020. [Online]. Available: https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

China’s BOE has initiated a price war in the global LCD market. The world"s largest LCD maker said it would sell 65-inch LCD TV panels nearly at cost. Analysts say that BOE has set off an LCD chicken game in 10 years to take the premium market away from Korean companies.

The news put the Korean display industry on alert. "BOE informed TV companies that it would lower prices of its 65-inch panels by 20%," said a senior executive of a Korean display producer on June 26. “BOE started mass production of 10.5th-generation panels in the first quarter of this year. It seems to be determined to drive out Samsung Display and LG Display from the panel market.”

Currently, the prices of 65-inch LCD panels range from US$240 to US$250. Lowering prices by 20% means that BOE will sell products nearly at cost. This woud resume a chicken game in 10 years since 2008.

"Global TV makers are asking for further price cuts, citing the prices offered by BOE," said an official of a major LCD maker. “If this situation holds, BOE may sweep orders from minor TV companies, including Haier and TCL of China, in negotiations on tentative contracts for next year, which will be signed at the end of this year.”

Samsung Display led the market for 50-inch or larger panels with a market share of 21.7% in the first quarter, followed by LG Display with 18.8%. BOE came in sixth with a 7.6% market share.

After BOE stole LG"s thunder as the main OLED panel supplier for Huawei"s Mate 20 Pro, it has now displaced the Korean company as the world"s largest LCD TV and monitor panel supplier.

According to Sigmaintell Consulting, BOE shipped 54.3 million TV panels and 37.3 million monitor panels. In comparison, LG"s numbers stood at 48.6 million and 34.5 million, respectively.

But analysts think the competition will heat up in 2019 - CEC-Panda LCD Technology and China Star Optoelectronics Technology (CSOT) are about to ramp up production and adopt aggressive pricing strategies. CEC-Panda is expected to compete in the 21.5, 23.8 and 32.5-inch segment while CSOT will focus on the 21.5, 23.6, 31.5-inch markets.

TOKYO -- Prices of liquid crystal display panels are soaring like never before after pandemic stay-at-home demand for personal computers and televisions rapidly brought scarcity around the world.

LCD panels are key components of PCs and TVs. Increases in work from home and online education resulting from the global health crisis have created strong demand for PCs. TVs also are selling strongly.

SEOUL -- LG Display"s operating profit tumbled 96% last year to 92.9 billion won ($83.2 million), the South Korean company said on Jan. 30, drained by competition in a saturated liquid crystal display panel market.

STONE Technologies is a proud manufacturer of superior quality TFT LCD modules and LCD screens. The company also provides intelligent HMI solutions that perfectly fit in with its excellent hardware offerings.

STONE TFT LCD modules come with a microcontroller unit that has a 1GHz Cortex-A8 CPU. Such a module can easily be transformed into an HMI screen. Simple hexadecimal instructions can be used to control the module through the UART port. Furthermore, you can seamlessly develop STONE TFT LCD color user interface modules and add touch control, features to them.

Becoming a reputable TFT LCD manufacturer is no piece of cake. It requires a company to pay attention to detail, have excellent manufacturing processes, the right TFT display technology, and have a consumer mindset.

Now, we list down 10 of the best famous LCD manufacturers globally. We’ll also explore why they became among the top 10 LCD display Manufacturers in the world.

Interface Devises Business includes Display and Senor, Sensor, and Application Solutions. As a leading company in the global semiconductor display industry, BOE has made the Chinese display industry develop from scratch to maturity and prosperity. Now, more than one-quarter of the global display panels are made by BOE, with its UHD, flexible display, microdisplay, and other solutions broadly applied to well-known worldwide brands.

LG Display is a leading manufacturer of thin-film transistor liquid crystal displays (TFT-LCD) panels, OLED, and flexible displays.LG Display began developing TFT-LCD in 1987 and currently offers Display panels in a variety of sizes and specifications using different cutting-edge technologies (IPS, OLED, and flexible technology).

Samsung Electronics is South Korea’s largest electronics industry and the largest subsidiary of the Samsung Group. In the late 1990s, Samsung Electronics’ independent technology development and independent product innovation capabilities were further enhanced. Its product development strategy not only emphasizes “leading the technology but also using the most advanced technology to develop new products to meet the high-end market demand at the introduction stage”.In addition to the matching principle, it also emphasizes the principle of “leading technology, developing new products with the most advanced technology, creating new demand and new high-end market”.

Founded in 2003, Innolink listed its shares in Taiwan in 2006. In March 2010, it merged with Chi Mei Optoelectronics and Tong Bao Optoelectronics, the largest merger in the panel industry. Qunchuang is the surviving company and Chi Mei Electronics is the company name. In December 2012, it was renamed As Qunchuang Optoelectronics.

With innovative and differentiated technologies, QINNOOptoelectronics provides advanced display integration solutions, including 4K2K ultra-high resolution, 3D naked eye, IGZO, LTPS, AMOLED, OLED, and touch solutions. Qinnooptoelectronics sets specifications and leads the market. A wide range of product line is across all kinds of TFT LCD panel modules, touch modules, for example, TV panel, desktop and laptop computer monitor with panels, small and medium scale “panels, medical, automotive, etc., the supply of cutting-edge information and consumer electronics customers around the world, for the world TFT – LCD (thin-film transistor liquid crystal display) leading manufacturers.

AU Optronics Co., LTD., formerly AU Optronics Corporation, was founded in August 1996. It changed its name to AU Optronics after its merger with UNIOPtronics in 2001. Through two mergers, AU has been able to have a full range of generations of production lines for panels of all sizes.Au Optronics is a TFT-LCD design, manufacturing, and r&d company. Since 2008, au Optronics has entered the green energy industry, providing customers with high-efficiency solar energy solutions.

Sharp has been called the “father of LCD panels”.Since its founding in 1912, Sharp developed the world’s first calculator and LIQUID crystal display, represented by the living pencil, which was invented as the company name. At the same time, Sharp is actively expanding into new areas to improve people’s living standards and social progress. Made a contribution.

BYD IT products and businesses mainly include rechargeable batteries, plastic mechanism parts, metal parts, hardware electronic products, cell phone keys, microelectronics products, LCD modules, optoelectronics products, flexible circuit boards, chargers, connectors, uninterruptible power supplies, DC power supplies, solar products, cell phone decoration, cell phone ODM, cell phone testing, cell phone assembly business, notebook computer ODM, testing and manufacturing and assembly business, etc.

Toshiba is a famous multinational company with a history of 130 years. It covers a wide range of businesses, including social infrastructure construction, home appliances, digital products, and electronic components. It covers almost every aspect of production and life. Toshiba has the largest research and development institution in Japan. Through unremitting innovation and development, Toshiba has been at the forefront of science and technology in the world.

Kyocera was founded in 1959 as a manufacturer of technical ceramics. Industrial ceramics is a series of advanced materials with unique physical, chemical, and electronic properties. Today, most of Kyocera’s products are related to telecommunications, including semiconductor components, RF and microwave packaging, passive electronic components, wireless mobile phones and network equipment, crystal oscillators and connectors, and optoelectronic products for optoelectronic communication networks.

Tianma microelectronics co., LTD., founded in 1983, the company focus on smartphones, tablets, represented by high order laptop display market of consumer goods and automotive, medical, POS, HMI, etc., represented by professional display market, and actively layout smart home, intelligent wear, AR/VR, unmanned aerial vehicles (UAVs) and other emerging markets, to provide customers with the best product experience.IN terms of technology, the company has independently mastered leading technologies such as LTPS-TFT, AMOLED, flexible display, Oxide-TFT, 3D display, transparent display, and in-cell/on-cell integrated touch control. TFT-LCD key Materials and Technologies National Engineering Laboratory, national enterprise Technology Center, post-doctoral mobile workstation, and undertake national Development and Reform Commission, The Ministry of Science and Technology, the Ministry of Industry and Information Technology, and other major national thematic projects. The company’s long-term accumulation and continuous investment in advanced technology lay the foundation for innovation and development in the field of application.

LCD panel prices have risen for 4 months in a row because of your home gaming? Since this year, the whole LCD panel market has smoked. Whether after the outbreak of the epidemic, LCD panel market prices rose for four months, or the panel giants in Japan and South Korea successively sold production lines, or the Chinese mainland listed companies frequently integrated acquisition, investment, and plant construction, all make the industry full of interesting.

LCD panel prices are already a fact. Since May this year, LCD panel prices have risen for four months in a row, making the whole industry chain dynamic. Why are LCD panels going up in price in a volatile 2020? The key factor lies in the imbalance between supply and demand.

The price of LCDS for large-size TVs of 70 inches or more hasn’t budged much. In addition, LTPS screens and AMOLED screens used in high-end phones have seen little or no increase in price.

As for October, LCD panel price increases are expected to moderate. The data shows that in October 32 inches or 2 dollars; Gains of 39.5 to 43 inches will shrink to $3;55 inches will fall back below $10; The 65-inch gain will narrow to $5.

During the epidemic, people stayed at home and had no way to go out for entertainment. They relied on TV sets, PCS, and game consoles for entertainment. After the resumption of economic work and production, the market of traditional home appliances picked up rapidly, and LCD production capacity was quickly digested.

However, due to the shutdown of most factories lasting 1-2 months during the epidemic period, LCD panel production capacity was limited, leading to insufficient production capacity in the face of the market outbreak, which eventually led to the market shortage and price increase for 4 consecutive months.

In fact, the last round of price rise of LCD panels was from 2016 to 2017, and its overall market price has continued to fall since 2018. Even in 2019, individual types have fallen below the material cost, and the whole industry has experienced a general operating loss. As a result, LCD makers have been looking for ways to improve margins since last year.

A return to a reasonable price range is the most talked about topic among panel makers in 2019, according to one practitioner. Some manufacturers for the serious loss of the product made the decision to reduce production or even stop production; Some manufacturers planned to raise the price, but due to the epidemic in 2020, the downstream demand was temporarily suppressed and the price increase was postponed. After the outbreak was contained in April, LCD prices began to rise in mid-to-late May.

In fact, the market price of LCD panels continued to decline in 2018-2019 because of the accelerated rise of China’s LCD industry and the influx of a large number of local manufacturers, which doubled the global LCD panel production capacity within a few years, but there was no suitable application market to absorb it. The result of excess capacity is oversupply, ultimately making LCD panel prices remain depressed.

Against this background, combined with the impact of the epidemic in 2020, the operating burden of LCD companies in Japan and South Korea has been further aggravated, and it is difficult to make profits in the production of LCD panels, so they have to announce the withdrawal of LCD business.

business in June 2022. In August, Sharp bought JDI Baishan, a plant in Ishikawa prefecture that makes liquid crystal display panels for smartphones. In early September, Samsung Display sold a majority stake in its SUZHOU LCD production plant to Starlight Electronics Technology, a unit of TCL Technology Group. LGD has not only pulled out of some of its production capacity but has announced that it will close its local production line in 2020. According to DSCC, a consultancy, the share of LCD production capacity in South Korea alone will fall from 19% to 7% between 2020 and 2021.

It is worth mentioning that in industry analysis, in view of the fact that Korean companies are good at using “dig through old bonus – selling high price – the development of new technology” the cycle of development mode, another 2020 out of the LCD production capacity, the main reason may be: taking the advantage of China’s expanding aggressively LCD manufacturers, Korean companies will own LCD panel production line hot sell, eliminating capacity liquid to extract its final value, and turning to the more profitable advantage of a new generation of display technologies, such as thinner, color display better OLED, etc. Samsung, for example, has captured more than 80% of the OLED market with its first-mover advantage.

From the perspective of production capacity, the launch of LCD tracks by major manufacturers in Japan and South Korea must reduce some production capacity in the short term, which to some extent induces market price fluctuations. In the long run, some of the Japanese and Korean LCD production capacity has been bought by Chinese manufacturers, coupled with frequent investment in recent years, the overall capacity is sure to recover as before, or even more than before. But now it will take time to expand the production layout, which more or less will cause supply imbalance, the industry needs to be cautious.

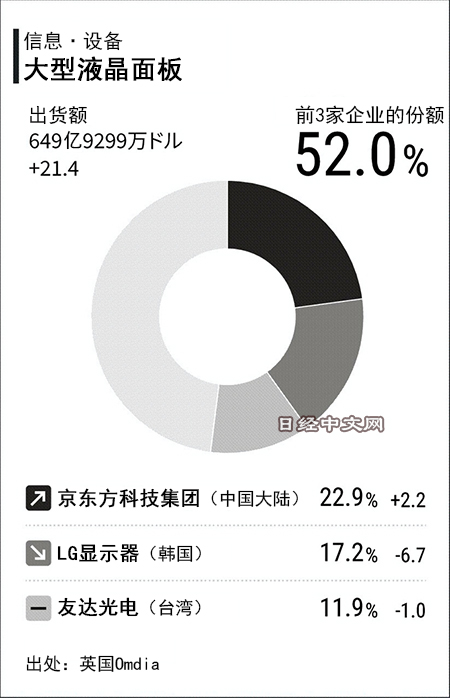

The LCD panel industry started in the United States and then gradually moved to Japan, South Korea, China, and Taiwan. At present, the proportion of production capacity in The Chinese mainland has reached 52% in 2020, and there are leading LCD panel products in China represented by BOE, Huxing Optoelectronics. Meanwhile, the production capacity layout of BOE, Huike, Huxing Optoelectronics, and other manufacturers has been basically completed, making industrial integration a necessity.

On the one hand, South Korean enterprises out of the LCD track, the domestic factory horse enclosure, plant expansion action. While LCDs may not sell as well as “upstart” flexible screens, respondents believe they are still strong enough in the traditional home appliance market to warrant continued investment. Zhao Bin, general manager of TCL Huaxing Development Center, has said publicly that the next-generation display technology will be mature in four to five years, but the commercialization of products may not take place until a decade later. “LCD will still be the mainstream in this decade,” he said.

On the other hand, there is no risk of neck jam in China’s LCD panel industry, which is generally controllable. In mainland China, there will be 21 production lines capable of producing 32-inch or larger LCD panels by 2021, accounting for about two-thirds of the global total. In terms of the proportion of production capacity, the Chinese mainland accounted for 42% of the global LCD panel in 2019, 51% this year, and will continue to climb to 63% next year.

Of course, building factories and expanding production cannot be accomplished overnight. In the process of production capacity recovery, it is predicted that there will be several price fluctuations, and the cost may be passed on to the downstream LCD panel manufacturers or consumers when the price rises greatly, which requires continuous attention.

LCD manufacturers are mainly located in China, Taiwan, Korea, Japan. Almost all the lcd or TFT manufacturers have built or moved their lcd plants to China on the past decades. Top TFT lcd and oled display manufactuers including BOE, COST, Tianma, IVO from China mainland, and Innolux, AUO from Tianwan, but they have established factories in China mainland as well, and other small-middium sizes lcd manufacturers in China.

China flat display revenue has reached to Sixty billion US Dollars from 2020. there are 35 tft lcd lines (higher than 6 generation lines) in China,China is the best place for seeking the lcd manufacturers.

The first half of 2021, BOE revenue has been reached to twenty billion US dollars, increased more than 90% than thesame time of 2020, the main revenue is from TFT LCD, AMoled. BOE flexible amoled screens" output have been reach to 25KK pcs at the first half of 2021.the new display group Micro LED revenue has been increased to 0.25% of the total revenue as well.

Established in 1993 BOE Technology Group Co. Ltd. is the top1 tft lcd manufacturers in China, headquarter in Beijing, China, BOE has 4 lines of G6 AMOLED production lines that can make flexible OLED, BOE is the authorized screen supplier of Apple, Huawei, Xiaomi, etc,the first G10.5 TFT line is made in BOE.BOE main products is in large sizes of tft lcd panel,the maximum lcd sizes what BOE made is up to 110 inch tft panel, 8k resolution. BOE is the bigger supplier for flexible AM OLED in China.

Technology Co., Ltd), established in 2009. CSOT is the company from TCL, CSOT has eight tft LCD panel plants, four tft lcd modules plants in Shenzhen, Wuhan, Huizhou, Suzhou, Guangzhou and in India. CSOTproviding panels and modules for TV and mobile

three decades.Tianma is the leader of small to medium size displays in technologyin China. Tianma have the tft panel factories in Shenzhen, Shanhai, Chendu, Xiamen city, Tianma"s Shenzhen factory could make the monochrome lcd panel and LCD module, TFT LCD module, TFT touch screen module. Tianma is top 1 manufactures in Automotive display screen and LTPS TFT panel.

Tianma and BOE are the top grade lcd manufacturers in China, because they are big lcd manufacturers, their minimum order quantity would be reached 30k pcs MOQ for small sizes lcd panel. price is also top grade, it might be more expensive 50%~80% than the market price.

Panda electronics is established in 1936, located in Nanjing, Jiangshu, China. Panda has a G6 and G8.6 TFT panel lines (bought from Sharp). The TFT panel technologies are mainly from Sharp, but its technology is not compliance to the other tft panels from other tft manufactures, it lead to the capacity efficiency is lower than other tft panel manufacturers. the latest news in 2022, Panda might be bougt to BOE in this year.

Established in 2005, IVO is located in Kunsan,Jiangshu province, China, IVO have more than 3000 employee, 400 R&D employee, IVO have a G-5 tft panel production line, IVO products are including tft panel for notebook, automotive display, smart phone screen. 60% of IVO tft panel is for notebook application (TOP 6 in the worldwide), 23% for smart phone, 11% for automotive.

Besides the lcd manufacturers from China mainland,inGreater China region,there are other lcd manufacturers in Taiwan,even they started from Taiwan, they all have built the lcd plants in China mainland as well,let"s see the lcd manufacturers in Taiwan:

Innolux"s 14 plants in Taiwan possess a complete range of 3.5G, 4G, 4.5G, 5G, 6G, 7.5G, and 8.5G-8.6G production line in Taiwan and China mainland, offering a full range of large/medium/small LCD panels and touch-control screens.including 4K2K ultra-high resolution, 3D naked eye, IGZO, LTPS, AMOLED, OLED, and touch-control solutions,full range of TFT LCD panel modules and touch panels, including TV panels, desktop monitors, notebook computer panels, small and medium-sized panels, and medical and automotive panels.

AUO is the tft lcd panel manufacturers in Taiwan,AUO has the lcd factories in Tianma and China mainland,AUOOffer the full range of display products with industry-leading display technology,such as 8K4K resolution TFT lcd panel, wide color gamut, high dynamic range, mini LED backlight, ultra high refresh rate, ultra high brightness and low power consumption. AUO is also actively developing curved, super slim, bezel-less, extreme narrow bezel and free-form technologies that boast aesthetic beauty in terms of design.Micro LED, flexible and foldable AMOLED, and fingerprint sensing technologies were also developed for people to enjoy a new smart living experience.

Hannstar was found in 1998 in Taiwan, Hannstar display hasG5.3 TFT-LCD factory in Tainan and the Nanjing LCM/Touch factories, providing various products and focus on the vertical integration of industrial resources, creating new products for future applications and business models.

driver, backlight etc ,then make it to tft lcd module. so its price is also more expensive than many other lcd module manufacturers in China mainland.

Maclight is a China based display company, located in Shenzhen, China. ISO9001 certified, as a company that more than 10 years working experiences in display, Maclight has the good relationship with top tft panel manufacturers, it guarantee that we could provide a long term stable supply in our products, we commit our products with reliable quality and competitive prices.

Maclight products included monochrome lcd, TFT lcd module and OLED display, touch screen module, Maclight is special in custom lcd display, Sunlight readable tft lcd module, tft lcd with capacitive touch screen. Maclight is the leader of round lcd display. Maclight is also the long term supplier for many lcd companies in USA and Europe.

If you want tobuy lcd moduleorbuy tft screenfrom China with good quality and competitive price, Maclight would be a best choice for your glowing business.

(Yicai Global) June 13 -- BOE Technology Group, TCL China Star Optoelectronics Technology and other big Chinese liquid crystal display manufacturers are reducing output starting from this month to try and stop a freefall in prices caused by a global glut.

Panel makers are cutting production by 16 percent on average from this month, Rong Chaoping, senior researcher at market research firm AVC Revo, told Yicai Global. Television panel makers are expected to ship 3.6 million less panels than last month.

Panel makers will reduce capacity by between 15 and 20 percent this month, said Wu Rongbing, chief analyst at Chinese semiconductor intelligence service Omdia.

LCD TV display shipments from China’s five largest panel manufacturers accounted for 68.5 percent of the global market in April, a new high, and they were expected to exceed 70 percent this year, according to Omdia.

The global panel industry is expected to slash production by about 20 percent this year, according to Beijing-based Sigmaintell. It is the first time since 2013 that the worldwide sector has implemented such a large-scale and wide-ranging cut in manufacturing. But it should help to slow the fall in prices, Li said.

“Tumbling prices are squeezing profits,” Li said. “The price of a TV panel is now below cost price and that of some data panels is also below the manufacturing cost.”

“Panel makers are facing rising liquidity pressure and bigger losses as prices are now below cost price, so the display industry is likely to undergo another big reshuffle,” Rong said.

Panel prices are likely to stop dropping this month or next as output falls, Wu said. Whether prices will start to pick up soon depends on when demand improves.

LG Display, the world"s largest LCD panel maker, clinched the title of world"s largest UHD TV panel vendor last month for the first time in 22 months, a research report released Thursday showed.

Taiwan-based Innolux -- LG"s main competitor -- came in second with 24 percent market share. Perennial rival Samsung Display followed in third with 20.2 percent. Innolux dominated the market previously by launching low-cost UHD TV panels to TV makers located within mainland China and the US, chipping away at LG and Samsung"s market share.

The rising popularity of high-priced UHD TVs in the world"s second largest market fueled growth for LG Display, which recently started operation at its factory in Guangzhou. The factory mainly supplies goods to Chinese TV makers, which also have factories nearby.

"We finally beat competitors by launching UHD TV panels made by our own M+ technology, which combines our innovative pixel arrangement structure and rendering technology using our own algorithm," a spokesman of LG Display said.

Meanwhile, the overall shipment of UHD TV panels was approximately 2.05 million worldwide for October, making LCD TVs still very much the standard in the market.

Workers manufacture display panels on an assembly line in Huainan High-Tech Industrial Development Zone in East China"s Anhui Province, on April 24, 2022. Photo: VCG

The year 2021 was a milestone for China"s display panel industry. Chinese display panel makers, led by companies such as BOE Technology Group Co, Shenzhen China Star Optoelectronics Technology Co, Tianma, and Visionox, accounted a combined 40.4 percent of global market share in turnover, outstripping South Korea"s 36.3 percent, data from Beijing-based market research provider Sigmaintell revealed.

A different set of data published by market research firm Omdia showed the same pattern. China recorded $64.8 billion in sales including liquid crystal display (LCD) and OLED in the global display market in 2021. China overtook South Korea"s No. 1 spot with a market share of 41.5 percent while South Korea"s market share fell to 33.2 percent.

On March 30, BOE, the world"s largest flat-panel display manufacturer, said its total revenue stood at 219.31 billion yuan ($33.57 billion) in 2021, up 61.79 percent from a yearly basis, while its net profit surged 412.96 percent year-on-year to hit 25.83 billion yuan.

Market competition in display panel, an indispensable part for consumer electronics, is fierce. And the competing relations between Chinese and South Korean companies exist in display panels for smartphones, televisions, monitors, among other product segments.

Display panel are comparable to today"s high-end semiconductors, for years the production of display panels had been monopolized by foreign companies. But after a decade of strenuous work to catchup, experts said that Chinese players now dominate today"s display panel manufacturing and the proliferation of display panel technology benefited global consumers by reducing the cost of a wide range of downstream electronic components and has in recent years caused domestic upstream business such as material-supplying company to flourish.

In terms of LCD, Chinese companies have long surpassed their South Korean counterparts in shipments, and in recent years Chinese companies also invested heavily in advanced production lines for small-size OLED screens that is used in smartphones.

Etnews suggested South Koran companies reduce OLED panel prices by mass producing OLED, which requires substantial investment in production capacity, only then can South Korea replace the LCD market led by China. The battlefield of choice for South Korean firms would be in large TV panel market, in which they still enjoy large technological gap with China.

Even as South Korean companies seek to entrench their lead position in large-size OLED, their efforts may not turn out to be as effective as imagined, Lee said, as large OLED may not prove to be a worthy barrier behind which South Korean companies could fall back upon as it does not have unique functions that could not be fulfilled by LCD.

In 2021, shipments of large-size OLED display panels were just 6.7 million units while in the same period the shipments of LCD reached 210 million units.

"Back in the days of LCD phasing out cathode ray tube and plasma display panel, LCD could fulfill unique functions the other two types could not. That is something we don"t see in OLED. The things OLED can do, LCD can also do and are being constantly perfected," Lee said. "That means fall back behind the OLED castles may not be enough to fend off challenges lurched out by Chinese players."

Lee said as the display panel industry moves forward, Chinese companies are betting big on research & development in new emerging display technologies such as mini-LED and micro-LED.

After more than 20 years of catching up, Chinese companies are now the number one manufacturers of LCD displays. In fact, the presence of Chinese brands is pushing the likes of Samsung out of the market. BOE is the world’s largest LCD panel factory. In the OLED field, BOE is still very much behind South Korean manufacturer, Samsung. However, a recent report claims that this year, BOE’s OLED shipments will soar by 70%.

According to reports, BOE plans to increase OLED panel deliveries by nearly 70% this year. Its two production lines in Chengdu and Mianyang will run at full capacity this fiscal year. The third production line in Chongqing is in full production. This will increase BOE’s OLED production from 60 million units in 2021 to 100 million units this year.

BOE’s Chongqing production line is testing panel quality from top smartphone and tablet makers, the report said. The Sichuan factory is already supplying Apple, and BOE apparently hopes that the Chongqing factory will also supply Apple with panels. Furthermore, the company is also considering building a new OLED factory in Chengdu, saying it is based on “assessing the strategy, market, technology and financial situation”, The new plant is scheduled to start production by the end of 2024, but production capacity has not been announced.

The report also points out that although BOE currently occupies the world’s largest share in the LCD panel field, surpassing its Korean competitors, in the field of OLED panels, South Korea’s Samsung Electronics and LG Display are still in a leading position.

Several Chinese panel manufacturers have surpassed Samsung and LG to become the main LCD panel manufacturers in recent years. Korean companies are no longer able to compete. Samsung will stop the production of LCD panels half a year ahead of schedule. Samsung originally planned to stop the production of LCD panels by the end of 2020. However, the LCD panel market started to increase prices in the past year or so. This made Samsung’s LCD factory continue to operate for another two years. However, the company originally plans to exit the market at the end of 2022. Nevertheless, the LCD panel market has changed since the end of last year. The price has been falling significantly and it is now on a free fall. By January this year, the average price of a 32 -inch panel was only $ 38, a 64% drop relative to January last year.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey