lcd panel market share 2016 supplier

BOE was the leading LCD TV panel vendor during the first half of 2020, having shipped approximately 23.26 million units worldwide. In that period, global shipments of LCD TV panels totaled over 115 million units.

BOE Technology, founded in 1993, has become China’s largest TV panel maker and it continues to make a name for itself in the global consumer electronics market. It was the first company to introduce a gen 10.5 LCD plant in late 2017. Since then, BOE’s LCD panel production capacity has grown annually, surpassing former leading manufacturer LG Display. In recent years, BOE accounted for over 20 percent of large-area TFT LCD display unit shipments worldwide.

Chinese panel makers accelerate worldwide LCD TV panel shipmentsChina became the leading LCD panel producer worldwide in 2017, overtaking powerhouses South Korea and Taiwan. Chinese shipments of LCD TV panels 60-inch and larger have also increased significantly in recent years, with roughly 2.24 million units sold in the first quarter of 2019 worldwide, in comparison to just 117,000 units a year before. This figure is forecast to increase in the future, paving the way for Chinese panel makers’ worldwide success. At the same time, the concurrent specialization on large LCD panels by Chinese and South Korean suppliers will likely push down panel prices.Read moreGlobal LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor(in millions)tablecolumn chartCharacteristicBOELGDInnoluxCSOTSDCAUOCEC GroupOthers1H 202023.2611.7920.3421.312.1310.14-16.17

TrendForce. (July 28, 2020). Global LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor (in millions) [Graph]. In Statista. Retrieved January 29, 2023, from https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/

TrendForce. "Global LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor (in millions)." Chart. July 28, 2020. Statista. Accessed January 29, 2023. https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/

TrendForce. (2020). Global LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor (in millions). Statista. Statista Inc.. Accessed: January 29, 2023. https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/

TrendForce. "Global Lcd Tv Panel Unit Shipments from H1 2016 to H1 2020, by Vendor (in Millions)." Statista, Statista Inc., 28 Jul 2020, https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/

TrendForce, Global LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor (in millions) Statista, https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/ (last visited January 29, 2023)

Global LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor (in millions) [Graph], TrendForce, July 28, 2020. [Online]. Available: https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/

BOE Technology Group, the Chinese electronic components producer, is expected to be the leader in producing LCD display panels in the coming years, with a forecast capacity share of 24 percent by 2022. China is the country that has the largest LCD capacity, with a 56 percent share in 2020.Read moreLCD panel production capacity share from 2016 to 2022, by manufacturerCharacteristicBOEChina StarInnoluxAUOLGDHKCCEC PandaSharpSDCOther-----------

DSCC. (June 8, 2020). LCD panel production capacity share from 2016 to 2022, by manufacturer [Graph]. In Statista. Retrieved January 29, 2023, from https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. "LCD panel production capacity share from 2016 to 2022, by manufacturer." Chart. June 8, 2020. Statista. Accessed January 29, 2023. https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. (2020). LCD panel production capacity share from 2016 to 2022, by manufacturer. Statista. Statista Inc.. Accessed: January 29, 2023. https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. "Lcd Panel Production Capacity Share from 2016 to 2022, by Manufacturer." Statista, Statista Inc., 8 Jun 2020, https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC, LCD panel production capacity share from 2016 to 2022, by manufacturer Statista, https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/ (last visited January 29, 2023)

LCD panel production capacity share from 2016 to 2022, by manufacturer [Graph], DSCC, June 8, 2020. [Online]. Available: https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

The upstream materials or components of the LCD panel industry mainly include liquid crystal materials, glass substrates, polarizing lenses, and backlight LEDs (or CCFL, which accounts for less than 5% of the market).

The middle reaches is the main panel factory processing and manufacturing, through the glass substrate TFT arrays and CF substrate, CF as upper and TFT self-built perfusion liquid crystal and the lower joint, and then put a polaroid, connection driver IC and control circuit board, and a backlight module assembling, eventually forming the whole piece of LCD module. The downstream is a variety of fields of application terminal-based brand, assembly manufacturers. At present, the United States, Japan, and Germany mainly focus on upstream raw materials, while South Korea, Taiwan, and the mainland mainly seek development in mid-stream panel manufacturing.

With the successive production of the high generation line in mainland China, the panel production capacity and technology level have been steadily improved, and the industrial competitiveness has been gradually enhanced. Nowadays, the panel industry is divided into three parts: South Korea, mainland China, and Taiwan, and mainland China is expected to become the no.1 in the world in 2019.

In the past decade, China’s panel display industryhas achieved leapfrog development, and the overall size of the industry has ranked among the top three in the world. Chinese mainland panel production capacity is expanding rapidly, although Japanese panel manufacturers master a large number of key technologies, gradually lose the price competitive advantage, compression panel production capacity. Panel production is concentrated in South Korea, Taiwan, and China, which is poised to become the world’s largest producer of LCD panels.

Up to 2016, BOE‘s global market share continued to increase: smartphone LCD, tablet PC display, and laptop display accounted for the world’s first market share, and display screen increased to the world’s second, while TV LCD remained the world’s third. In LCD TV panels, Chinese panel makers have accounted for 30 percent of global shipments to 77 million units, surpassing Taiwan’s 25.5 percent market share for the first time and ranking second only to South Korea.

In terms of the area of shipment, the area of board shipment of JD accounted for only 8.3% in 2015, which has been greatly increased to 13.6% in the first half of 2016, while the area of shipment of hu xing optoelectronics in the first half of 2015 was only 5.1%, which has reached 7.8% in the first half of 2016. The panel factories in mainland China are expanding their capacity at an average rate of double-digit growth and transforming it into actual shipments and areas of shipment. On the other hand, although the market share of South Korea, Japan, and Taiwan is gradually decreasing, some South Korean and Japanese manufacturers have been inclined to the large-size HD panel and AMOLED market, and the production capacity of the high-end LCD panel is further concentrated in mainland China.

Domestic LCD panel production line capacity gradually released, overlay the decline in global economic growth, lead to panel makers from 15 in the second half began, in a low profit or loss, especially small and medium-sized production line, the South Korean manufacturers take the lead in transformation strategy, closed in medium and small size panel production line, South Korea’s 19-panel production line has shut down nine, and part of the production line is to research and development purposes. Some production lines are converted to LTPS production lines through process conversion. Korean manufacturers are turning to OLED panels in a comprehensive way, while Japanese manufacturers are basically giving up the LCD panel manufacturing business and turning to the core equipment and materials side. In addition to the technical direction of the research and judgment, more is the LCD panel business orders and profits have been severely compressed, Korean and Japanese manufacturers have no desire to fight. Since many OLED technologies are still in their infancy in mainland China, it is a priority to move to high-end panels such as OLED as soon as possible. Taiwanese manufacturers have not shut down factories on a large scale, but their advantages in LCD technology and OLED technology have been slowly eroded by the mainland.

STONE provides a full range of 3.5 inches to 15.1 inches of small and medium-size standard quasi TFT LCD module, LCD display, TFT display module, display industry, industrial LCD screen, under the sunlight visually highlight TFT LCD display, industrial custom TFT screen, TFT LCD screen-wide temperature, industrial TFT LCD screen, touch screen industry. The TFT LCD module is very suitable for industrial control equipment, medical instruments, POS system, electronic consumer products, vehicles, and other products.STONE provides a full range of 3.5 inches to 15.1 inches of small and medium-size standard quasi TFT LCD module, LCD display, TFT display module, display industry, industrial LCD screen, under the sunlight visually highlight TFT LCD display, industrial custom TFT screen, TFT LCD screen-wide temperature, industrial TFT LCD screen, touch screen industry. The TFT LCD module is very suitable for industrial control equipment, medical instruments, POS system, electronic consumer products, vehicles, and other products.

This market research report includes a detailed segmentation of the global large area LCD display market by application (TVs, notebooks, monitors, tablets, and others). It outlines the market shares for key regions such as the Americas, APAC, and EMEA. The key vendors analyzed in this report are AU Optronics, BOE Technology, Innolux, LG Display, and Samsung Display.

Technavio’s research analyst predicts the global large area LCD display market to grow at a CAGR of 3% during the forecast period. The formation of UHD alliances is the primary growth driver for this market. During 2015, supply chain members of the global UHD TV market announced the formation of the UHD Alliance to support innovative technologies including 4K and higher resolution, high dynamic range, immersive 3D audio, and wider color gamut.

The decline in ASP of the LCD panel is expected to boost the market growth during the forecast period. During 2014, per meter square, ASP of LCD panel was $472, which declined to $416 during 2015. Vendors reduced the ASP to reduce excess inventory. The declining per square meter ASP of LCD panel drove the shipment of LCD display in terms of area.

During 2015, the TV segment dominated the large area LCD display market with a market share of 38%. The primary reason for the growth of this product segment was the strong demand for 4K TVs of 40 inches and larger screen size. During 2015, several manufacturers introduced 4K TVs ranging from 50 inches and above.

During 2015, APAC accounted for 81% of the market share and is expected to grow at a CAGR of 1% during the forecast period. The high concentration of display device manufacturers and LCD panel manufacturers in this region are the primary growth drivers. Technavio expects that the well-established supply chain for display devices in APAC would continue to support the dominance of this region in the market during the forecast period. China is emerging fast as a leading hub for large area TFT LCD display manufacturers because of the rise in the number of display device manufacturers in the country.

Manufacturing LCD display panels require economies of scale because the equipment used to manufacture displays are expensive. This presents high entry barriers for LCD display panel manufacturers. Currently, the global large area LCD display market is dominated by China, Japan, South Korea, and Taiwan in terms of production and revenue contribution. Chinese manufacturers have the advantage of manufacturing LCD panels at a lower cost. This has resulted in price wars among LCD manufacturers and has accelerated the declining ASP of LCD panels. Vendors such as LG and Samsung are under a lot of pressure as profit margins have come down because of increased competition.

Other prominent vendors in the market include Chi Mei Optoelectronics, Chunghwa Picture Tube (CPT), HannsTouch Solution, HannStar Display, InfoVision Optoelectronics, Japan Display, Kaohsiung Opto-Electronics, NEC Display Solutions, Panasonic, and Sharp.

LCD TV Panel Market Size is projected to Reach Multimillion USD by 2027, In comparison to 2021, at unexpected CAGR during the Forecast Period 2022-2028.

Considering the economic change due to COVID-19 and Russia-Ukraine War Influence, LCD TV Panel accounted for % of the global market of LCD TV Panel in 2022.

This LCD TV Panel Market Report offers analysis and insights based on original consultations with important players such as CEOs, Managers, Department Heads of Suppliers, Manufacturers, Distributors, etc.

The Global LCD TV Panel Market is anticipated to rise at a considerable rate during the forecast period, between 2022 and 2027. In 2021, the market is growing at a steady rate and with the rising adoption of strategies by key players, the market is expected to rise over the projected horizon.

LCD displays utilize two sheets of polarizing material with a liquid crystal solution between them. An electric current passed through the liquid causes the crystals to align so that light cannot pass through them. Each crystal, therefore, is like a shutter, either allowing light to pass through or blocking the light. LCD panel is the key components of LCD display. And the price trends of LCD panel directly affect the price of liquid crystal displays. LCD panel consists of several components: Glass substrate, drive electronics, polarizers, color filters etc. Only LCD panel applied for TV will be counted in this report

Samsung Display, LG Display, Innolux Crop and AUO captured the top four revenue share spots in the LCD TV Panel market in 2015. Samsung Display dominated with 22.11 percent revenue share, followed by LG Display with 19.72 percent revenue share and Innolux Crop Display with 19.30 percent revenue share.

The global LCD TV Panel market is valued at USD 51130 million in 2019. The market size will reach USD 59640 million by the end of 2026, growing at a CAGR of 2.2% during 2021-2026.

LCD TV Panel market is segmented by Size, and by Application. Players, stakeholders, and other participants in the global LCD TV Panel market will be able to gain the upper hand as they use the report as a powerful resource. The segmental analysis focuses on production capacity, revenue and forecast by Size and by Application for the period 2016-2027.

The report focuses on the LCD TV Panel market size, segment size (mainly covering product type, application, and geography), competitor landscape, recent status, and development trends. The report considers key geographic segments and describes all the favorable conditions driving the market growth.

On the basis of the End Users/Applications, this report focuses on the status and outlook for major applications/end users, consumption (sales), market share, and growth rate for each application, including:

Geographically, the Major Regions Covered in LCD TV Panel Market Report Are:To comprehend LCD TV Panel market dynamics across major global regions. ● North America(United States, Canada)

Market is changing rapidly with the ongoing expansion of the industry. Advancement in technology has provided today’s businesses with multifaceted advantages resulting in daily economic shifts. Thus, it is very important for a company to comprehend the patterns of market movements in order to strategize better. An efficient strategy offers the companies a head start in planning and an edge over the competitors.Industry Researchis a credible source for gaining the market reports that will provide you with the lead your business needs.

Is there a problem with this press release? Contact the source provider Comtex at editorial@comtex.com. You can also contact MarketWatch Customer Service via our Customer Center.

This report includes all of DSCC"s content on OLED and LCD fab schedules, OLED and LCD capacity and LCD and OLED equipment market sizes, market share and forecasts for 79 different segments. All design wins and units by fab by equipment type are shown and quarterly revenues are provided for >130 different display equipment suppliers. Also included are typical process flows for each major process.

This report provides all of the market intelligence that a display equipment manufacturer, supplier to display equipment manufacturer or analysts covering display equipment suppliers would want. It is also ideal for panel suppliers tracking the market shares for all major display equipment segments. In total, 79 different equipment segments have been covered compared to 22 from other research firms.. Market share and design wins are provided for every segment as well on a quarterly, annual, billings and bookings basis, while other research firms don"t offer any market share data.

Quarterly and annual equipment market share provided from 2016 to as far as 2025 for all backplane, frontplane, color filter, cell and most module segments, >70 different segments.

Flat-panel displays are thin panels of glass or plastic used for electronically displaying text, images, or video. Liquid crystal displays (LCD), OLED (organic light emitting diode) and microLED displays are not quite the same; since LCD uses a liquid crystal that reacts to an electric current blocking light or allowing it to pass through the panel, whereas OLED/microLED displays consist of electroluminescent organic/inorganic materials that generate light when a current is passed through the material. LCD, OLED and microLED displays are driven using LTPS, IGZO, LTPO, and A-Si TFT transistor technologies as their backplane using ITO to supply current to the transistors and in turn to the liquid crystal or electroluminescent material. Segment and passive OLED and LCD displays do not use a backplane but use indium tin oxide (ITO), a transparent conductive material, to pass current to the electroluminescent material or liquid crystal. In LCDs, there is an even layer of liquid crystal throughout the panel whereas an OLED display has the electroluminescent material only where it is meant to light up. OLEDs, LCDs and microLEDs can be made flexible and transparent, but LCDs require a backlight because they cannot emit light on their own like OLEDs and microLEDs.

Liquid-crystal display (or LCD) is a thin, flat panel used for electronically displaying information such as text, images, and moving pictures. They are usually made of glass but they can also be made out of plastic. Some manufacturers make transparent LCD panels and special sequential color segment LCDs that have higher than usual refresh rates and an RGB backlight. The backlight is synchronized with the display so that the colors will show up as needed. The list of LCD manufacturers:

Organic light emitting diode (or OLED displays) is a thin, flat panel made of glass or plastic used for electronically displaying information such as text, images, and moving pictures. OLED panels can also take the shape of a light panel, where red, green and blue light emitting materials are stacked to create a white light panel. OLED displays can also be made transparent and/or flexible and these transparent panels are available on the market and are widely used in smartphones with under-display optical fingerprint sensors. LCD and OLED displays are available in different shapes, the most prominent of which is a circular display, which is used in smartwatches. The list of OLED display manufacturers:

MicroLED displays is an emerging flat-panel display technology consisting of arrays of microscopic LEDs forming the individual pixel elements. Like OLED, microLED offers infinite contrast ratio, but unlike OLED, microLED is immune to screen burn-in, and consumes less power while having higher light output, as it uses LEDs instead of organic electroluminescent materials, The list of MicroLED display manufacturers:

LCDs are made in a glass substrate. For OLED, the substrate can also be plastic. The size of the substrates are specified in generations, with each generation using a larger substrate. For example, a 4th generation substrate is larger in size than a 3rd generation substrate. A larger substrate allows for more panels to be cut from a single substrate, or for larger panels to be made, akin to increasing wafer sizes in the semiconductor industry.

"Samsung Display has halted local Gen-8 LCD lines: sources". THE ELEC, Korea Electronics Industry Media. August 16, 2019. Archived from the original on April 3, 2020. Retrieved December 18, 2019.

"TCL to Build World"s Largest Gen 11 LCD Panel Factory". www.businesswire.com. May 19, 2016. Archived from the original on April 2, 2018. Retrieved April 1, 2018.

"Panel Manufacturers Start to Operate Their New 8th Generation LCD Lines". 대한민국 IT포털의 중심! 이티뉴스. June 19, 2017. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"TCL"s Panel Manufacturer CSOT Commences Production of High Generation Panel Modules". www.businesswire.com. June 14, 2018. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"Samsung Display Considering Halting Some LCD Production Lines". 비즈니스코리아 - BusinessKorea. August 16, 2019. Archived from the original on April 5, 2020. Retrieved December 19, 2019.

Herald, The Korea (July 6, 2016). "Samsung Display accelerates transition from LCD to OLED". www.koreaherald.com. Archived from the original on April 1, 2018. Retrieved April 1, 2018.

"China"s BOE to have world"s largest TFT-LCD+AMOLED capacity in 2019". ihsmarkit.com. 2017-03-22. Archived from the original on 2019-08-16. Retrieved 2019-08-17.

TFT or thin-film transistor is combined with LCD to improve colour quality leading to a sharper image, as each pixel on a TFT-LCD is attached to a transistor. Due to the small sizes of each transistor, TFT-LCD display panels consume less power. They are widely used in computers, TVs, laptops, and mobile phones as it gives a more enhanced image than older technologies and prevents the distortion of image.

With the growing applications of TFT-LCD, there has been an increased competition among the manufacturers for the best cutting technology, i.e. ‘generations’, to produce TFT-LCD panels. In 2017, BOE, one of the major TFT-LCD manufacturers globally, put the world’s highest generation line, Generation 10.5 TFT-LCD production line, into production ahead of schedule in Hefei, China. With more Gen 10.5 facilities starting mass production, the market is primed for the production of 65 inches and larger TFT-LCD panels. More than 85.5% of the TFT-LCD display panels consumed in 2018 were large-sized panels sized over 10 inches.

Driven by the demand for TFT-LCD display panels in TV and monitor panels, the global shipment of large TFT-LCD panels grew again in 2018, despite over-supply concerns. The market is also driven by a rising demand for automotive displays. While automotive display systems were earlier reserved for luxury vehicles, cars for the mass-market are increasingly including high resolution display systems in their design due to a decline in prices along with the rising production and demand for automobiles. This growth in automotive displays has been supported by the rising investments in automotive display panels by big display panel manufacturers in Asia. The Asia Pacific countries like China and India are the fastest growing markets in the region due to rapid economic growth and a growing demand for consumer-based electronics. Currently, the global market for TFT-LCD display panel is dominated by North America.

Region-wise, the global market for TFT-LCD display panel can be divided into North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

The report also offers historical (2018-2022) and forecast (2023-2028) market information for the sizes, applications, and major regions of TFT-LCD display panel.

The report analyses the market dynamics, covering the key demand and price indicators in the market, along with providing an assessment of the SWOT and Porter’s Five Forces models.

The major players in the global TFT-LCD display panel market are Samsung Electronics Co., Ltd., LG Display Co., Ltd., Japan Disney Inc., Sharp Corporation, BOE Technology Group Co., Ltd., AUO Corporation, Raystar Optronics Inc., WINSTAR Display Co., Ltd., Kingtech Group Co., Ltd., and Tricomtek Co., Ltd., among others. The comprehensive report by EMR looks into the market share, capacity, and latest developments like mergers and acquisitions, plant turnarounds, and capacity expansions of the major players.

*At Expert Market Research, we strive to always give you current and accurate information. The numbers depicted in the description are indicative and may differ from the actual numbers in the final EMR report.

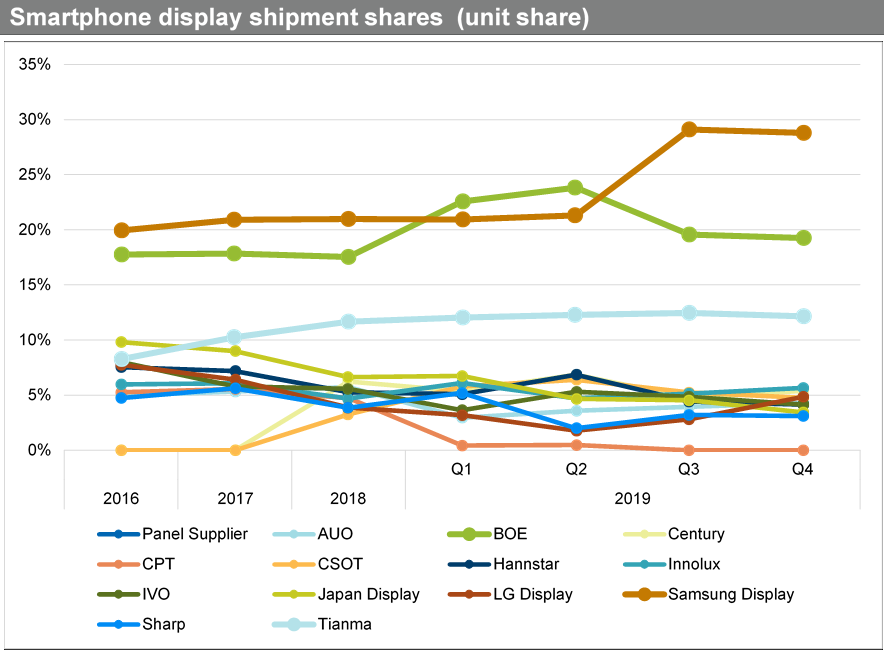

BOSTON, October 17, 2022--(BUSINESS WIRE)--According to the Strategy Analytics Handset Component Technologies service report, "Smartphone Display Panel Market Share Q2 2022: LCD Panel Revenues Plunge", the global smartphone display panel market registered a revenue of $20 billion in H1 2022.

The report finds that the smartphone display panel market posted a 5 percent revenue decline year-over-year in H1 2022. The market continues to be led by Samsung Display with 53 percent revenue share followed by BOE Technology with 15 percent and Tianma Microelectronics with 8 percent in H1 2022. The top-three display panel vendors captured nearly 76 percent revenue share in the global smartphone display panel market during the period.

Jeffrey Mathews, Senior Analyst at Strategy Analyticscommented, "The market for smartphone display panels was held back by sinking LCD panel demand while OLED adoption expanded across mid-tier smartphones to enable OEMs to drive momentum. Display vendors saw rising demand for Flexible OLED panels with high refresh rate specifications which drove OLED growth during the period. Samsung Display was strongly positioned to benefit from customer demand enabling a strong pipeline of design wins for its OLED panels. BOE, TCL CSOT and Tianma ramped their OLED production and captured orders to supply OLED panels to leading smartphone brands in H1 2022."

Stephen Entwistle, Vice President of the Strategic Technologies Practice at Strategy Analytics noted, "We expect momentum for OLED panels to continue and drive market growth enabled by stronger display supplier competition and increased panel yield for OLED displays. LCD panels are expected to be in oversupply leading to further price declines. The weak macroeconomic sentiments pose a strong risk to the overall prospects of growth for the smartphone display panel market."

Strategy Analytics, Inc. is a global leader in supporting companies across their planning lifecycle through a range of customized market research solutions. Our multi-discipline capabilities include industry research advisory services, customer insights, user experience design and innovation expertise, mobile consumer on-device tracking and business-to-business consulting competencies. With domain expertise in smart devices, connected cars, intelligent home, service providers, IoT, strategic components and media, Strategy Analytics can develop a solution to meet your specific planning need. For more information, visit us at www.strategyanalytics.com.

LG Display and Samsung Display are struggling to find their ways out of the deterioration of their performance even after withdrawing from production of liquid crystal display (LCD) panels. The high-priced organic light emitting diode (OLED) panel sector regarded as a future growth engine is not growing fast due to the economic downturn. Even in the OLED panel sector, Chinese display makers are within striking distance of Korean display makers, experts say.

On Aug. 30, Display Supply Chain Consultants (DSCC), a market research company, predicted that LCD TV panel prices hit an all-time low in August and that an L-shaped recession will continue in the fourth quarter. According to DSCC, the average price of a 65-inch ultra-high-definition (UHD) panel in August was only US$109, a 62 percent drop from the highest price of US$288 recorded in July in 2021. The average price of a 75-inch UHD panel was only US$218, which was only about half of the highest price of US$410 in July last year. DSCC predicted that the average panel price in the third quarter will fall by 15.7 percent. As Chinese companies’ price war and the effect of stagnation in consumption overlapped, the more LCD panels display makers produce, the more loss they suffer.

As panel prices fell, manufacturers responded by lowering facility utilization rates. DSCC said that the LCD factory utilization rate descended from 87 percent in April to 83 percent in May, 73 percent in June, and 70 percent in July.

Now that the LCD panel business has become no longer lucrative, Korean display makers have shut down their LCD business or shrunk their sizes. In the LCD sector, China has outpaced Korea since 2018. China’s LCD market share reached 50.9 percent in 2021, while that of Korea dropped to 14.4 percent, lower than Taiwan’s 31.6 percent.

Samsung Display already announced its withdrawal from the LCD business in June. Only 10 years have passed since the company was spun off from Samsung Electronics in 2012. LG Display has decided to halt domestic LCD TV panel production until 2023 and reorganize its business structure centering on OLED panels. Its Chinese LCD production line will be gradually converted to produce LCD panels for IT or commercial products. TrendForce predicted that LG Display will stop operating its P7 Plant in the first quarter of next year.

Korean display makers’ waning LCD business led to a situation in which Korea even lost first place in the display industry. Korea with a display market share of 33.2 percent was already overtaken by China with 41.5 percent) in 2021 according to market researcher Omdia and the Korea Display Industry Association. Korea’s market share has never rebounded in for five years since 2017 amid the Korean government’s neglect. Seventeen years have passed since 2004 when Korea overtook Japan to rise to the top of the world in the LCD industry. Korea’s LCD exports amounted to more than US$30 billion in 2014, but fell to US$21.4 billion last year.

A bigger problem is that Korean display makers may lose its leadership in the OLED panel sector although it is still standing at the top spot. While Korea’s OLED market share fell from 98.1 percent in 2016 to 82.8 percent last year, that of China rose from 1.1 percent to 16.6 percent. Considering that the high-end TV market is highly likely to shrink for the time being due to a full-fledged global consumption contraction, some analysts say that the technology gap between Korea and China can be sharply narrowed through this looming TV market slump. According to industry sources, the Chinese government is now focusing on giving subsidies to the development of OLED panel technology rather LCD technology. On the other hand, in Korea, displays were also wiped out from national strategic technology industry items under the Restriction of Special Taxation Act which can receive tax benefits for R&D activities on displays.

In both LCD and OLED displays, producing these cells – which are highly complex – is by far the most difficult element of the production process. Indeed, the complexity of these cells, combined with the levels of investment needed to achieve expertise in their production, explains why there are less than 30 companies in the whole world that can produce them. China, for instance, has invested more than 300 billion yuan (approximately $45 billion USD) in just one of these companies – BOE – over the past 14 years.

Panox Display has been involved in the display industry for many years and has built strong and long-term partner relationships with many of the biggest OLED and LCD panel manufacturers. As a result, we are able to offer our clients guaranteed access to display products from the biggest manufacturers.

LG Display was, until 2021, the No. 1 display panel manufacturer in the world. Owned by LG Group and headquartered in Seoul, South Korea, it has R&D, production, and trade institutions in China, Japan, South Korea, the United States, and Europe.

Founded in 2001, AUO – or AU Optronics – is the world’s leading TFT-LCD panel manufacturer (with a 16% market share) that designs, develops, and manufactures the world’s top three liquid crystal displays. With panels ranging from as small as 1.5 inches to 46 inches, it boasts one of the world"s few large-, medium -and small-sized product lines.

AUO offers advanced display integration solutions with innovative technologies, including 4K2K ultra-high resolution, 3D, ultra-thin, narrow bezel, transparent display, LTPS, OLED, and touch solutions. AOU has the most complete generation production line, ranging from 3.5G to 8.5G, offering panel products for a variety of LCD applications in a range of sizes, from as small as 1.2 inches to 71 inches.

Now Sharp is still top 10 TV brands all over the world. Just like BOE, Sharp produce LCDs in all kinds of size. Including small LCD (3.5 inch~9.1 inch), medium LCD (10.1 ~27 inch), large LCD (31.5~110 inch). Sharp LCD has been used on Iphone series for a long time.

Beside those current LCDs, the industrial LCD of Sharp is also excellent and widely used in public facilities, factories, and vehicles. The Sharp industrial LCD, just means solid, high brightness, super long working time, highest stability.

Since its establishment, Truly Semiconductors has focused on researching, developing, and manufacturing liquid crystal flat panel displays. Now, after twenty years of development, it is the biggest small- and medium-sized flat panel display manufacturer in China.

Truly’s factory in Shanwei City is enormous, covering an area of 1 million square meters, with a net housing area of more than 100,000 square meters. It includes five LCD production lines, one OLED production line, three touch screen production lines, and several COG, LCM, MDS, CCM, TAB, and SMT production lines.

Its world-class production lines produce LCD displays, liquid crystal display modules (LCMs), OLED displays, resistive and capacitive touch screens (touch panels), micro camera modules (CCMs), and GPS receiving modules, with such products widely used in the smartphone, automobile, and medical industries. The LCD products it offers include TFT, TN, Color TN with Black Mark (TN type LCD display for onboard machines), STN, FSTN, 65K color, and 262K color or above CSTN, COG, COF, and TAB modules.

In its early days, Innolux attached great importance to researching and developing new products. Mobile phones, portable and mounted DVD players, digital cameras, games consoles, PDA LCDs, and other star products were put into mass production and quickly captured the market, winning the company considerable market share.

Looking forward to the future, the group of photoelectric will continue to deep LCD display field, is committed to the development of plane display core technology, make good use of global operations mechanism and depth of division of labor, promise customers high-quality products and services, become the world"s top display system suppliers, in 2006 in the global mobile phone color display market leader, become "Foxconn technology" future sustained rapid growth of the engine.

Founded in June 1998, Hannstar specializes in producing thin-film transistor liquid crystal display panels, mainly for use in monitors, notebook displays and televisions. It was the first company in Taiwan to adopt the world’s top ultra-wide perspective technology (AS-IPS).

The company has three LCD factories and one LCM factory. It has acquired state-of-the-art TFT-LCD manufacturing technology, which enables it to achieve the highest efficiency in the mass production of thin-film transistor liquid crystal display production technology. Its customers include many of the biggest and most well-known electronics companies and computer manufacturers in Taiwan and overseas.

TCL CSOT – short for TCL China Star Optoelectronics Technology (TCL CSOT) – was founded in 2009 and is an innovative technology enterprise that focuses on the production of semiconductor displays. As one of the global leaders in semiconductor display market, it has bases in Shenzhen, Wuhan, Huizhou, Suzhou, Guangzhou, and India, with nine panel production lines and five large modules bases.

TCL CSOT actively produces Mini LED, Micro LED, flexible OLED, printing OLED, and other new display technologies. Its product range is vast – including large, medium, and small panels and touch modules, electronic whiteboards, splicing walls, automotive displays, gaming monitors, and other high-end display application fields – which has enabled it to become a leading player in the global panel industry.

In the first quarter of 2022, TCL CSOT’s TV panels ranked second in the market, 55 inches, 65 " and 75 inches second, 8K, 120Hz first, the first, interactive whiteboard and digital sign plate; LTPS flat panel, the second, LTPS and flexible OLED fourth.

EDO (also known as EverDisplay Optonics) was founded in October 2012 and focuses on the production of small- and medium-sized high-resolution AMOLED semiconductor display panels.

In order to ramp up production output, the company began construction of a 6th-generation AMOLED production line in December 2016, with a total investment of 27.3 billion yuan (almost $4 billion USD). The line, which has a production capacity of 30,000 glass substrates per month, produces flexible and rigid high-end AMOLED displays for use in smartphones, tablet pens, vehicle displays, and wearable devices.

Tianma Microelectronics was founded in 1983 and listed on the Shenzhen Stock Exchange in 1995. It is a high-tech enterprise specializing in the production of liquid crystal displays (LCD) and liquid crystal display modules (LCM).

After more than 30 years of development, it has grown into a large publicly listed company integrating LCD research and development, design, production, sales, and servicing. Over the years, it has expanded by investing in the construction of STN-LCD, CSTN-LCD, TFT-LCD and CF production lines and module factories across China (with locations in Shenzhen, Shanghai, Chengdu, Wuhan and Xiamen), as well R&D centers and offices in Europe, Japan, South Korea and the United States.

The company"s marketing network is all over the world, and its products are widely used in mobile phones, MP3/MP4 players, vehicle displays, instrumentation, household appliances, and other fields. In terms of technical level, product quality, product grade, and market share, it ranks at the forefront of the domestic industry and has become a leading enterprise in the field of small- and medium-sized displays.

JDI (Japan Display Inc.) was established on November 15, 2011, as a joint venture between the Industrial Innovation Corporation, Sony, Hitachi, and Toshiba. It is dedicated to the production and development of small-sized displays. It mainly produces small- and medium-sized LCD display panels for use in the automotive, medical, and industrial fields, as well as personal devices including smartphones, tablets, and wearables.

Although Sony’s TVs use display panels from TCL CSOT (VA panel), Samsung. Sony still produces the world’s best micro-OLED display panels. Sony has many micro OLED model such as 0.23 inch, 0.39 inch, 0.5 inch, 0.64 inch, 0.68 inch, 0.71 inch. Panox Display used to test and sell many of them, compare to other micro OLED manufacuturers, Sony`s micro OLEDs are with the best image quality and highest brightness (3000 nits max).

Total shipments of mobile phone displays, including thin-film transistor liquid crystal display (TFT LCD) and active matrix organic light-emitting diode (AMOLED) panels, reached 2.01 billion units in 2017, up 3 percent from 2016, according to preliminary estimate from business information provider IHS Markit (Nasdaq: INFO).

In the growing mobile phone display market, shipments of low-temperature-poly-silicon (LTPS) TFT LCD panels, which realize high-resolution images, increased by 21 percent to 620 million units in 2017 compared to the previous year. Shipments of amorphous silicon (a-Si) TFT LCD mobile phone panels declined 4 percent to 979 million units during the same period. Even though shipments of AMOLED panels jumped in the second half of 2017 thanks to the launch of the iPhone X, combined with the weak demand in the first half, its shipments were up just 3 percent to 402 million units in 2017.

In the smartphone-use LTPS TFT LCD market, Tianma, a leading small and medium panel supplier in China, has shown significant growth, expanding its shipments to Chinese smartphone set brands, such as Huawei and Xiaomi. In 2017, Tianma shipped 105 million LTPS TFT LCD panels for smartphones, almost double its shipments in 2016, with a market share of 17 percent, up 6 percentage points from 2016. It ranked the second largest LTPS TFT LCD supplier for smartphones in 2017, taking over LG Display with 16 percent, down 4 percentage points, and Sharp with 13 percent, down 1 percentage point. In 2017, Japan Display continued its market leader position but shed its share by 10 percentage points to 26 percent in 2017, according to the latest Smartphone Display Intelligent Service report by IHS Markit.

“LTPS TFT is a key technology to produce high-resolution displays for smartphones, and experience is required to optimize highly complex LTPS manufacturing process in each production fab. In terms of experience, Japanese and South Korean panel makers have a competitive advantage compared to Chinese makers,” said Hiroshi Hayase, senior director at IHS Markit. “However, Chinese LCD makers, such as Tianma and BOE, are catching up LTPS technology fast enough to support high demand from Chinese smartphone set makers.”

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey