lcd panel market share 2016 in stock

BOE was the leading LCD TV panel vendor during the first half of 2020, having shipped approximately 23.26 million units worldwide. In that period, global shipments of LCD TV panels totaled over 115 million units.

BOE Technology, founded in 1993, has become China’s largest TV panel maker and it continues to make a name for itself in the global consumer electronics market. It was the first company to introduce a gen 10.5 LCD plant in late 2017. Since then, BOE’s LCD panel production capacity has grown annually, surpassing former leading manufacturer LG Display. In recent years, BOE accounted for over 20 percent of large-area TFT LCD display unit shipments worldwide.

Chinese panel makers accelerate worldwide LCD TV panel shipmentsChina became the leading LCD panel producer worldwide in 2017, overtaking powerhouses South Korea and Taiwan. Chinese shipments of LCD TV panels 60-inch and larger have also increased significantly in recent years, with roughly 2.24 million units sold in the first quarter of 2019 worldwide, in comparison to just 117,000 units a year before. This figure is forecast to increase in the future, paving the way for Chinese panel makers’ worldwide success. At the same time, the concurrent specialization on large LCD panels by Chinese and South Korean suppliers will likely push down panel prices.Read moreGlobal LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor(in millions)tablecolumn chartCharacteristicBOELGDInnoluxCSOTSDCAUOCEC GroupOthers1H 202023.2611.7920.3421.312.1310.14-16.17

TrendForce. (July 28, 2020). Global LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor (in millions) [Graph]. In Statista. Retrieved January 29, 2023, from https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/

TrendForce. "Global LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor (in millions)." Chart. July 28, 2020. Statista. Accessed January 29, 2023. https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/

TrendForce. (2020). Global LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor (in millions). Statista. Statista Inc.. Accessed: January 29, 2023. https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/

TrendForce. "Global Lcd Tv Panel Unit Shipments from H1 2016 to H1 2020, by Vendor (in Millions)." Statista, Statista Inc., 28 Jul 2020, https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/

TrendForce, Global LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor (in millions) Statista, https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/ (last visited January 29, 2023)

Global LCD TV panel unit shipments from H1 2016 to H1 2020, by vendor (in millions) [Graph], TrendForce, July 28, 2020. [Online]. Available: https://www.statista.com/statistics/760270/global-market-share-of-led-lcd-tv-vendors/

LCD TV Panel Market Size is projected to Reach Multimillion USD by 2027, In comparison to 2021, at unexpected CAGR during the Forecast Period 2022-2028.

Considering the economic change due to COVID-19 and Russia-Ukraine War Influence, LCD TV Panel accounted for % of the global market of LCD TV Panel in 2022.

This LCD TV Panel Market Report offers analysis and insights based on original consultations with important players such as CEOs, Managers, Department Heads of Suppliers, Manufacturers, Distributors, etc.

The Global LCD TV Panel Market is anticipated to rise at a considerable rate during the forecast period, between 2022 and 2027. In 2021, the market is growing at a steady rate and with the rising adoption of strategies by key players, the market is expected to rise over the projected horizon.

LCD displays utilize two sheets of polarizing material with a liquid crystal solution between them. An electric current passed through the liquid causes the crystals to align so that light cannot pass through them. Each crystal, therefore, is like a shutter, either allowing light to pass through or blocking the light. LCD panel is the key components of LCD display. And the price trends of LCD panel directly affect the price of liquid crystal displays. LCD panel consists of several components: Glass substrate, drive electronics, polarizers, color filters etc. Only LCD panel applied for TV will be counted in this report

Samsung Display, LG Display, Innolux Crop and AUO captured the top four revenue share spots in the LCD TV Panel market in 2015. Samsung Display dominated with 22.11 percent revenue share, followed by LG Display with 19.72 percent revenue share and Innolux Crop Display with 19.30 percent revenue share.

The global LCD TV Panel market is valued at USD 51130 million in 2019. The market size will reach USD 59640 million by the end of 2026, growing at a CAGR of 2.2% during 2021-2026.

LCD TV Panel market is segmented by Size, and by Application. Players, stakeholders, and other participants in the global LCD TV Panel market will be able to gain the upper hand as they use the report as a powerful resource. The segmental analysis focuses on production capacity, revenue and forecast by Size and by Application for the period 2016-2027.

The report focuses on the LCD TV Panel market size, segment size (mainly covering product type, application, and geography), competitor landscape, recent status, and development trends. The report considers key geographic segments and describes all the favorable conditions driving the market growth.

On the basis of the End Users/Applications, this report focuses on the status and outlook for major applications/end users, consumption (sales), market share, and growth rate for each application, including:

Geographically, the Major Regions Covered in LCD TV Panel Market Report Are:To comprehend LCD TV Panel market dynamics across major global regions. ● North America(United States, Canada)

Market is changing rapidly with the ongoing expansion of the industry. Advancement in technology has provided today’s businesses with multifaceted advantages resulting in daily economic shifts. Thus, it is very important for a company to comprehend the patterns of market movements in order to strategize better. An efficient strategy offers the companies a head start in planning and an edge over the competitors.Industry Researchis a credible source for gaining the market reports that will provide you with the lead your business needs.

Is there a problem with this press release? Contact the source provider Comtex at editorial@comtex.com. You can also contact MarketWatch Customer Service via our Customer Center.

This market research report includes a detailed segmentation of the global large area LCD display market by application (TVs, notebooks, monitors, tablets, and others). It outlines the market shares for key regions such as the Americas, APAC, and EMEA. The key vendors analyzed in this report are AU Optronics, BOE Technology, Innolux, LG Display, and Samsung Display.

Technavio’s research analyst predicts the global large area LCD display market to grow at a CAGR of 3% during the forecast period. The formation of UHD alliances is the primary growth driver for this market. During 2015, supply chain members of the global UHD TV market announced the formation of the UHD Alliance to support innovative technologies including 4K and higher resolution, high dynamic range, immersive 3D audio, and wider color gamut.

The decline in ASP of the LCD panel is expected to boost the market growth during the forecast period. During 2014, per meter square, ASP of LCD panel was $472, which declined to $416 during 2015. Vendors reduced the ASP to reduce excess inventory. The declining per square meter ASP of LCD panel drove the shipment of LCD display in terms of area.

During 2015, the TV segment dominated the large area LCD display market with a market share of 38%. The primary reason for the growth of this product segment was the strong demand for 4K TVs of 40 inches and larger screen size. During 2015, several manufacturers introduced 4K TVs ranging from 50 inches and above.

During 2015, APAC accounted for 81% of the market share and is expected to grow at a CAGR of 1% during the forecast period. The high concentration of display device manufacturers and LCD panel manufacturers in this region are the primary growth drivers. Technavio expects that the well-established supply chain for display devices in APAC would continue to support the dominance of this region in the market during the forecast period. China is emerging fast as a leading hub for large area TFT LCD display manufacturers because of the rise in the number of display device manufacturers in the country.

Manufacturing LCD display panels require economies of scale because the equipment used to manufacture displays are expensive. This presents high entry barriers for LCD display panel manufacturers. Currently, the global large area LCD display market is dominated by China, Japan, South Korea, and Taiwan in terms of production and revenue contribution. Chinese manufacturers have the advantage of manufacturing LCD panels at a lower cost. This has resulted in price wars among LCD manufacturers and has accelerated the declining ASP of LCD panels. Vendors such as LG and Samsung are under a lot of pressure as profit margins have come down because of increased competition.

Other prominent vendors in the market include Chi Mei Optoelectronics, Chunghwa Picture Tube (CPT), HannsTouch Solution, HannStar Display, InfoVision Optoelectronics, Japan Display, Kaohsiung Opto-Electronics, NEC Display Solutions, Panasonic, and Sharp.

The upstream materials or components of the LCD panel industry mainly include liquid crystal materials, glass substrates, polarizing lenses, and backlight LEDs (or CCFL, which accounts for less than 5% of the market).

The middle reaches is the main panel factory processing and manufacturing, through the glass substrate TFT arrays and CF substrate, CF as upper and TFT self-built perfusion liquid crystal and the lower joint, and then put a polaroid, connection driver IC and control circuit board, and a backlight module assembling, eventually forming the whole piece of LCD module. The downstream is a variety of fields of application terminal-based brand, assembly manufacturers. At present, the United States, Japan, and Germany mainly focus on upstream raw materials, while South Korea, Taiwan, and the mainland mainly seek development in mid-stream panel manufacturing.

With the successive production of the high generation line in mainland China, the panel production capacity and technology level have been steadily improved, and the industrial competitiveness has been gradually enhanced. Nowadays, the panel industry is divided into three parts: South Korea, mainland China, and Taiwan, and mainland China is expected to become the no.1 in the world in 2019.

In the past decade, China’s panel display industryhas achieved leapfrog development, and the overall size of the industry has ranked among the top three in the world. Chinese mainland panel production capacity is expanding rapidly, although Japanese panel manufacturers master a large number of key technologies, gradually lose the price competitive advantage, compression panel production capacity. Panel production is concentrated in South Korea, Taiwan, and China, which is poised to become the world’s largest producer of LCD panels.

Up to 2016, BOE‘s global market share continued to increase: smartphone LCD, tablet PC display, and laptop display accounted for the world’s first market share, and display screen increased to the world’s second, while TV LCD remained the world’s third. In LCD TV panels, Chinese panel makers have accounted for 30 percent of global shipments to 77 million units, surpassing Taiwan’s 25.5 percent market share for the first time and ranking second only to South Korea.

In terms of the area of shipment, the area of board shipment of JD accounted for only 8.3% in 2015, which has been greatly increased to 13.6% in the first half of 2016, while the area of shipment of hu xing optoelectronics in the first half of 2015 was only 5.1%, which has reached 7.8% in the first half of 2016. The panel factories in mainland China are expanding their capacity at an average rate of double-digit growth and transforming it into actual shipments and areas of shipment. On the other hand, although the market share of South Korea, Japan, and Taiwan is gradually decreasing, some South Korean and Japanese manufacturers have been inclined to the large-size HD panel and AMOLED market, and the production capacity of the high-end LCD panel is further concentrated in mainland China.

Domestic LCD panel production line capacity gradually released, overlay the decline in global economic growth, lead to panel makers from 15 in the second half began, in a low profit or loss, especially small and medium-sized production line, the South Korean manufacturers take the lead in transformation strategy, closed in medium and small size panel production line, South Korea’s 19-panel production line has shut down nine, and part of the production line is to research and development purposes. Some production lines are converted to LTPS production lines through process conversion. Korean manufacturers are turning to OLED panels in a comprehensive way, while Japanese manufacturers are basically giving up the LCD panel manufacturing business and turning to the core equipment and materials side. In addition to the technical direction of the research and judgment, more is the LCD panel business orders and profits have been severely compressed, Korean and Japanese manufacturers have no desire to fight. Since many OLED technologies are still in their infancy in mainland China, it is a priority to move to high-end panels such as OLED as soon as possible. Taiwanese manufacturers have not shut down factories on a large scale, but their advantages in LCD technology and OLED technology have been slowly eroded by the mainland.

STONE provides a full range of 3.5 inches to 15.1 inches of small and medium-size standard quasi TFT LCD module, LCD display, TFT display module, display industry, industrial LCD screen, under the sunlight visually highlight TFT LCD display, industrial custom TFT screen, TFT LCD screen-wide temperature, industrial TFT LCD screen, touch screen industry. The TFT LCD module is very suitable for industrial control equipment, medical instruments, POS system, electronic consumer products, vehicles, and other products.STONE provides a full range of 3.5 inches to 15.1 inches of small and medium-size standard quasi TFT LCD module, LCD display, TFT display module, display industry, industrial LCD screen, under the sunlight visually highlight TFT LCD display, industrial custom TFT screen, TFT LCD screen-wide temperature, industrial TFT LCD screen, touch screen industry. The TFT LCD module is very suitable for industrial control equipment, medical instruments, POS system, electronic consumer products, vehicles, and other products.

This report includes all of DSCC"s content on OLED and LCD fab schedules, OLED and LCD capacity and LCD and OLED equipment market sizes, market share and forecasts for 79 different segments. All design wins and units by fab by equipment type are shown and quarterly revenues are provided for >130 different display equipment suppliers. Also included are typical process flows for each major process.

This report provides all of the market intelligence that a display equipment manufacturer, supplier to display equipment manufacturer or analysts covering display equipment suppliers would want. It is also ideal for panel suppliers tracking the market shares for all major display equipment segments. In total, 79 different equipment segments have been covered compared to 22 from other research firms.. Market share and design wins are provided for every segment as well on a quarterly, annual, billings and bookings basis, while other research firms don"t offer any market share data.

Quarterly and annual equipment market share provided from 2016 to as far as 2025 for all backplane, frontplane, color filter, cell and most module segments, >70 different segments.

This report provides strategists, marketers and senior management with the critical information they need to assess the global flexible display market.

The global flexible display market is expected to grow from $10.58 billion in 2021 to $14.34 billion in 2022 at a compound annual growth rate (CAGR) of 35.6%. The flexible display market is expected to grow to $44.72 billion in 2026 at a CAGR of 32.9%.

Major players in the flexible display market are BOE Technology Group Co., LG Display Co.Ltd, Royole Corporation, Samsung Electronics Co. Ltd, Japan Display Inc., AU Optronics Corp., Innolux Corporation, Corning Incorporated, Sharp Corporation, Visionox Company, E Ink Holdings Inc., and Koninklijke Philips N.V.

The flexible display market consists of sales of flexible displays by entities (organizations, sole traders, and partnerships) that are used in virtual reality (VR) headsets, digital cameras, laptops, and televisions. A flexible display refers to an electronic display printed on a foldable plastic membrane that can easily be twisted. These displays can withstand being folded, bent, and twisted, and they are more flexible as compared to a flat display. These have better durability and are lightweight in nature.

The main types of flexible display are OLED (organic light-emitting diodes), LCD (liquid-crystal display), EPD (electronic paper display), and others.

North America was the largest region in the flexible display market in 2021. The regions covered in the flexible display market report are Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East and Africa.

The rising demand for OLED-based devices is expected to propel the growth of the flexible display market going forward. An OLED refers to an organic electroluminescent (organic EL) diode, which is a light-emitting diode, that contains an emissive electroluminescent layer that gives good quality to the picture. Most flexible displays are made of OLED displays because they give better picture quality even when the screen is bent and twisted.

For instance, according to Displaydaily, a US-based technology news publisher, in 2019, there were 3.4 million OLED display TV units sold, and this number is expected to grow by 19% to $6.4 billion units by 2024. Also in 2019, 466 million units of OLED display phones were sold. Therefore, the rising use of OLED displays in devices such as smartphones and TV is driving the growth of the flexible display market.

Technological advancements have emerged as a key trend gaining popularity in the flexible display market. Major companies operating in the flexible display market are focused on technological advancements to strengthen their position in the market.

The countries covered in the flexible display market report are Australia, Brazil, China, France, Germany, India, Indonesia, Japan, Russia, South Korea, UK, USA.

6.1. Global Flexible Display Market, Segmentation By Display Type, Historic and Forecast, 2016-2021, 2021-2026F, 2031F, $ BillionOLED (Organic Light-Emitting Diodes)

LG Display’ shipments of 65" and 75" TV panels increased significantly by 38.5% and 132.7% respectively, indicating its preparation for further competition with BOE in large-size TV panel sector.

WitsView, a division of TrendForce, reports that global LCD TV panel shipments increased quarter by quarter in 2017. 1H17 showed less momentum for holiday sales due to the high prices, but shipments rebounded in 2H17 as the prices declined and TV makers prepared for the year-end sales. Moreover, the new production capacities of BOE’s Gen 8.5 fab in Fuqing and HKC’s Gen 8.6 fab in Chongqing have been focusing on middle-size TV panels (43" and 32" respectively), bringing the annual shipments beyond expectation to 263.83 million pieces, an increase of 1.3% compared with 2016.

As for 2018, Iris Hu, research manager of WitsView, points out that panel makers will continue to increase the production shares of large-size panels and UHD panels to boost the revenue and profit. “The penetration rate of UHD panels is expected to reach 42% this year, an increase of 7.4 percentage points compared with 2017”, says Hu. Regarding the new production capacity, BOE’s Gen 10.5 fab produces mainly large-size TV panels (65" and 75"), but CEC’s two fabs still put their priorities at middle-size ones (32" and 50"). Meanwhile, replacement of CRT TV sets with 32" and 23.6" LCD ones is still ongoing in emerging markets, making the average panel size grow slower to 45.8 inches, only 1.3 inches up from 2017. Overall speaking, global TV panel shipments this year will have chance to hit a second-highest number in history, reaching 269.49 million pieces, an annual increase of 2.2%.

In the global TV panel shipment ranking for 2017, LG Display (LGD) came first place with a shipment of around 50.85 million pieces last year, a decrease of 3.9%. LGD expanded its production capacity in Guangzhou fab for 50K sheet, but in terms of panel size, increasing the production capacity share of 65" and greater panels has been the trend. Particularly, LGD shipments of 65" and 75" panels have increased significantly by 38.5% and 132.7% respectively, indicating that LGD has been making efforts to retain its market share in large-size TV panel sector before BOE’s Gen 10.5 fab enter mass production.

BOE deliberately slowed down its 32" TV panel production growth in 2017, so the shipments of this size increased by only 0.4%, totaling 43.81 million pieces. But its total shipments climbed to second place for the first time as Samsung Display (SDC)’s closure of L7-1 fab influenced its production. As BOE’s Gen 8.5 fab in Fuqing entered mass production in 2Q17, BOE’s shipments of 43" TV panels grew remarkably by 247.6% last year.

Innolux’s Gen 8.6 fab entered mass production in early 2017, but the yield rate and output were less than expectation in the first half of 2017. In the second half, high pricing of panels led to shrinking demand, resulting in Innolux’s slow-moving and excess stocks. In addition, Innolux announced to enter the TV assembly market, which made its clients more conservative in making orders. Fortunately Innolux figured out the solutions of pricing and stock problems, and ended up with shipments of 41.8 million pieces, an increase of 0.2%, ranking the third.

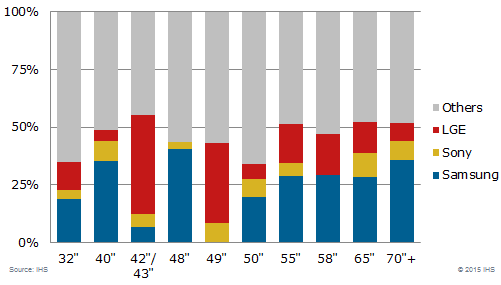

SDC’s shipments saw a substantial decline of 15.4% last year since the closure of its L7-1 fab. Its overall TV panel shipments turned out to be 39.6 million pieces, the highest decline among the six major panel makers. Although its shipments have dropped out of top 3, SDC has improved capacity utilization by simplifying its product mix, and has invested in production equipment of UHD and large-size panels to increase the value of its products. As for product portfolio, SDC took initiatives to develop UHD panels, whose proportion came to 54.6% among all of SDC’s products, and also remained a major supplier of large-size panels (55", 65" and 75"). Particularly, its market share of 65" sector was as high as 36.3%, showing definite advantages over its competitors.

China Star Optoelectronics Technology (CSOT) kept increasing the shipments after the capacity of the second phase of its second Gen 8.5 fab was expanded to 140K sheet. CSOT’s final shipments recorded 38.64 million pieces, an increase of 16.8% compared with the previous year. Particularly, 55" panels recorded a 19.4% shipment growth, as CSOT’s capacity expansion came mainly from this size. As for the growth by shipment area, CSOT recorded a 19.6% YoY increase, the highest among the six major panel makers.

TV panel shipments for AU Optronics (AUO) in 2017 came to around 27.21 million pieces, 0.1% down from the previous year. AUO continued to optimize its product portfolio and increased the proportion of large-size panels, so it finally recorded a 5.1% growth of shipment area. In addition, AUO also put focus on increasing the proportion of UHD products, reaching 44% of all its products, the third highest number following LGD and SDC.

Samsung Electronics Co., Ltd. (Korean: 삼성전자; Hanja: 三星電子; RR: Samseong Jeonja; lit. Tristar Electronics, sometimes shortened to SEC and stylized as SΛMSUNG) is a South Korean multinational electronics corporation headquartered in Yeongtong-gu, Suwon, South Korea.Samsung chaebol, accounting for 70% of the group"s revenue in 2012.circular ownership.assembly plants and sales networks in 74 countries and employs around 290,000 people.second-largest technology company by revenue, and its market capitalization stood at US$520.65 billion, the 12th largest in the world.

Samsung is a major manufacturer of Electronic Components such as lithium-ion batteries, semiconductors, image sensors, camera modules, and displays for clients such as Apple, Sony, HTC, and Nokia.smartphones, starting with the original Samsung SolsticeSamsung Galaxy line of devices.tablet computers, particularly its Android-powered Samsung Galaxy Tab collection, and is regarded for developing the phablet market with the Samsung Galaxy Note family of devices.Galaxy S22, and foldable phones including the Galaxy Z Fold 4. Samsung has been the world"s largest television manufacturer since 2006,memory chip manufacturerIntel, the decades-long champion.

As Samsung shifted away from consumer markets, the company devised a plan to sponsor major sporting events. One such sponsorship was for the 1998 Winter Olympics held in Nagano, Japan.

In April 2011, Samsung Electronics sold its HDD commercial operations to Seagate Technology for approximately US$1.4 billion. The payment was composed of 45.2 million Seagate shares (9.6 percent of shares), worth US$687.5 million, and a cash sum for the remainder.

In April 2013, Samsung Electronics" new entry into its Galaxy S series smartphone range, the Galaxy S4 was made available for retail. Released as the upgrade of the best-selling Galaxy S III, the S4 was sold in some international markets with the company"s Exynos processor.

Samsung"s mobile business chief Shin Jong-Kyun stated to the Korea Times on 11 September 2013 that Samsung Electronics will further develop its presence in China to strengthen its market position in relation to Apple. The Samsung executive also confirmed that a 64-bit smartphone handset will be released to match the ARM-based A7 processor of Apple"s iPhone 5s model that was released in September 2013.

Due to smartphone sales—especially sales of lower-priced handsets in markets such as India and China—Samsung achieved record earnings in the third quarter of 2013. The operating profit for this period rose to about ₩10.1 trillion (equivalent to ₩10.61 trillion or US$9.38 billion in 2017)2580.

On 16 June 2016, Samsung Electronics announced that it agreed to acquire cloud-computing company Joyent. They stated that the acquisition allowed Samsung to grow its cloud-based services for its smartphones and Internet-connected devices.

On 14 November 2016, Samsung Electronics announced an agreement to buy American automotive equipment manufacturer Harman International Industries for US$8 billion.

On 6 April 2017, Samsung Electronics reported that financials were up for the company in the quarter. The year prior, "memory chips and flexible displays accounted for about 68% of Samsung"s operating profit in the final quarter of 2016, a change from previous years when the smartphone business was the main contributor."

In mid-November 2021, Samsung Electronics was ranked second in the "Best Global Brands" by YouGov a market research firm, after placing fourth in the 2020 ranking.

In June 2022, PricewaterhouseCoopers ranked Samsung Electronics 22nd on their global top 100 companies by market capitalization. The company slid seven notches from the 2021 rankings due to global inflation, the war in Ukraine, and global monetary tightening.

Samsung Electronics produces LCD and LED panels, mobile phones, memory chips, NAND flash, solid-state drives, televisions, digital cinemas screen, and laptops and many more products. The company previously produced hard-drives and printers.

In October 2007, Samsung introducing a ten-millimeter thick, 40-inch LCD television panel, followed in October 2008 by the world"s first 7.9-mm panel.

At the end of the third quarter of 2010, the company had surpassed the 70 million unit mark in shipped phones, giving it a global market share of 22 percent, trailing Nokia by 12 percent.

During the third quarter of 2013, Samsung"s smartphone sales improved in emerging markets such as India and the Middle East, where cheaper handsets were most popular. As of October 2013, the company offers 40 smartphone models on its US website

Since the early 1990s, Samsung Electronics has commercially introduced a number of new memory technologies.SDRAM (synchronous dynamic random-access memory) in 1992,DDR SDRAM (double data rate SDRAM) and GDDR (graphics DDR) SGRAM (synchronous graphics RAM) in 1998.30 nm-class NAND flash memory,DRAM and 20 nm class NAND flash, both of which were for the first time in the world.TLC (triple-level cell) NAND flash memory in 2010,V-NAND flash in 2013,LPDDR4 SDRAM in 2013,HBM2 in 2016,GDDR6 in January 2018,LPDDR5 in June 2018.

According to market research firm Gartner, during the second quarter of 2010, Samsung Electronics took the top position in the DRAM segment due to brisk sales of the item on the world market. Gartner analysts said in their report, "Samsung cemented its leading position by taking a 35-percent market share. All the other suppliers had minimal change in their shares." The company took the top slot in the ranking, followed by Hynix, Elpida, and Micron, said Gartner.

In 2010, market researcher IC Insights predicted that Samsung would become the world"s-biggest semiconductor chip supplier by 2014, surpassing Intel. For the ten-year period from 1999 to 2009, Samsung"s compound annual growth rate in semiconductor revenues was 13.5 percent, compared with 3.4 percent for Intel.semiconductor company in 2017.

In 2016, Samsung also launched to market a 15.36TB SSD with a price tag of US$10,000 using a SAS interface, using a 2.5-inch form factor but with the thickness of 3.5-inch drives. This was the first time a commercially available SSD had more capacity than the largest currently available HDD.M.2 NVMe SSD with read speeds of 3500 MB/s and write speeds of 3300 MB/s in the same year.

In the area of storage media, in 2009 Samsung achieved a ten percent world market share, driven by the introduction of a new hard disk drive capable of storing 250Gb per 2.5-inch disk.Seagate in 2011 in return for a 9.6% ownership stake in Seagate.

In 2009, Samsung sold around 31 million flat-panel televisions, enabling to it to maintain the world"s largest market share for a fourth consecutive year.

Samsung sold more than one million 3D televisions within six months of its launch. This is the figure close to what many market researchers forecast for the year"s worldwide 3D television sales (1.23 million units).

In 2007, Samsung introduced the "Internet TV", enabling the viewer to receive information from the Internet while at the same time watching conventional television programming. Samsung later developed "Smart LED TV" (now renamed to "Samsung Smart TV"),smart television apps. In 2008, the company launched the Power Infolink service, followed in 2009 by a whole new Internet@TV. In 2010, it started marketing the 3D television while unveiling the upgraded Internet@TV 2010, which offers free (or for-fee) download of applications from its Samsung Apps Store, in addition to existing services such as news, weather, stock market, YouTube videos, and movies.

During the 1990s to the 2000s, Samsung started producing LCD monitors using TFT technology to which it still emphasizes on the budget market against the competition while at the same time starting to also focus on catering to the middle and upper markets through partnership with brands such as NEC and Sony via a joint venture.S-LCD Corporation respectively from its former joint venture partners.

Samsung has introduced several models of digital cameras and camcorders including the WB550 camera, the ST550 dual-LCD-mounted camera, and the HMX-H106 (64GB SSD-mounted full HD camcorder). In 2014, the company took the second place in the mirrorless camera segment.

Samsung entered the MP3 player (digital audio player, DAP) market in 1999 with its Yepp line. In the initial years the company struggled to gain a foothold because of emerging Korean startups iRiver, Cowon and Mpio. However by 2006, it had gained a significant share in the domestic market as well as Russia and parts of the Middle East, South East Asia and Europe.DivX MP3 player, the R1, in 2009.

The company added a new digital imaging business division in 2010, and consists of eight divisions, including the existing display, IT solutions, consumer electronics, wireless, networking, semiconductor, and LCD divisions.

Despite recent litigation activity, Samsung and Apple have been described as frenemies who share a love-hate relationship.Tim Cook originally opposed litigation against Samsung wary of the company"s critical component supply chain for Apple.

In April 2011, Apple Inc. announced that it was suing Samsung over the design of its Galaxy range of mobile phones. The lawsuit was filed on 15 April 2011 and alleges that Samsung infringed on Apple"s trademarks and patents of the iPhone and iPad.counterclaim against Apple of patent infringement.preliminary injunction against the sale and marketing of the Samsung Galaxy Tab 10.1 across the whole of Europe excluding the Netherlands.

All Samsung mobile phones and MP3 players introduced on the market after April 2010 are free from polyvinyl chloride (PVC) and brominated flame retardants (BFRs).

In December 2010, the European Commission fined six LCD panel producers, including Samsung, a total of €648 million for operating as a cartel. The company received a full reduction of the potential fine for being the first firm to assist EU anti-trust authorities.

On 19 October 2011, Samsung was fined €145.73 million for being part of a price cartel of ten companies for DRAMs, which lasted from 1 July 1998 to 15 June 2002. Like most of the other members of the cartel, the company received a 10% reduction for acknowledging the facts to investigators. Samsung had to pay 90% of their share of the settlement, but Micron avoided payment as a result of having initially revealed the case to investigators. Micron remains the only company that avoided all payments from reduction under the settlement notice.

On 31 August 2016, it was reported that Samsung was delaying shipments of the Galaxy Note 7 in some regions to perform "additional tests being conducted for product quality"; this came alongside user reports of batteries exploding while charging. On 2 September, Samsung suspended sales of the Note 7 and announced a worldwide "product exchange program"Galaxy S7, or an S7 Edge (the price difference being refunded). They would also receive a gift card from a participating carrier.product recall by the media, it was not an official government-issued recall by an organization such as the U.S. Consumer Product Safety Commission (CPSC), and only a voluntary measure.

On 14 October 2016, the U.S. Federal Aviation Administration and the Department of Transportation"s Pipeline and Hazardous Materials Safety Administration banned the Note 7 from being taken aboard any airline flight, even if powered off.Qantas, Virgin Australia and Singapore Airlines also banned the carriage of Note 7s on their aircraft with effect from midnight on 15 October.Aeromexico, Interjet, Volaris and VivaAerobus all banned the handset.

On 4 November 2016, Samsung recalled 2.8 million top-load washing machines sold at home appliance stores between 2011 and 2016 because the machine"s top could unexpectedly detach from the chassis during use due to excessive vibration.

In March 2016, soccer star Pelé filed a lawsuit against Samsung in the United States District Court for the Northern District of Illinois, seeking $30 million in damages, claiming violations under the Lanham Act for false endorsement and a state law claim for violation of his right of publicity.scissors-kick", perfected and famously used by Pelé.

Kim, Gil; Keon Han; Minseok Sinn; Hyung Cho; Ray Kim (18 June 2014). "Korea Market Strategy – How to untangle Samsung group"s ownership?". Credit Suisse. p. 36. Archived from the original on 5 February 2016. Retrieved 22 November 2015.

"Samsung Extends Sponsorship of Olympic Games until 2016". Sportbusiness. 24 April 2007. Archived from the original on 17 September 2011. Retrieved 23 November 2010.

Russell, Jon (14 November 2016). "Samsung is buying Harman for $8B to further its connected car push". TechCrunch. Archived from the original on 15 November 2016. Retrieved 14 November 2016.

Chung-un, Cho (1 May 2017). "Samsung denies re-entry to auto market despite autonomous car push". The Korea Herald. Archived from the original on 3 May 2017. Retrieved 3 May 2017.

Fernandes, Louella (8 June 2009). "Samsung Launches New Channel MPS Tools". Quocirca. Archived from the original on 23 September 2016. Retrieved 28 April 2016.

"New Samsung 3.9mm LED TV Panel Is World"s Thinnest". I4U. 28 October 2009. Archived from the original on 28 January 2011. Retrieved 16 November 2010.

"Nokia, LG Lose While ZTE, Apple Gain Q4 2010 Market Share". mobileburn.com. 28 January 2011. Archived from the original on 14 July 2011. Retrieved 19 February 2011.

"Samsung Remains Top DRAM Maker Amid Dramatic Market Growth". Dow Jones. 9 January 2010. Archived from the original on 21 November 2010. Retrieved 23 November 2010.

By David Steele, Android Headlines. "Samsung Now Fourth Largest Chipset Manufacturer Globally Archived 10 May 2016 at the Wayback Machine." 9 May 2016. 12 May 2016.

"KOREA: LG, Samsung Aim Upmarket To Reinforce Their TV Market Lead". What Hi-Fi? Sound and Vision. 24 August 2010. Archived from the original on 24 October 2010. Retrieved 16 November 2010.

"Samsung"s Tizen OS dominates global smart TV market". FierceVideo. 25 March 2019. Archived from the original on 23 August 2019. Retrieved 16 October 2019.

"SMD Enjoys Soaring Demand for AMOLED Panel". Maeil Business Newspaper. 1 July 2010. Archived from the original on 21 January 2012. Retrieved 26 November 2010.

"(Samsung"s share grows while Apple"s declines in Q3 smartphone market)". InfoWorld. 29 October 2013. Archived from the original on 4 December 2013. Retrieved 3 December 2013.

"Samsung Hands Out Hush Money to Occupational Disease Victims". Stop Samsung – No More Deaths!. 23 October 2015. Archived from the original on 11 October 2016. Retrieved 31 December 2016.

"Samsung Announces "Product Exchange Program" For Galaxy Note 7 – But Don"t Call It A Recall". The Consumerist. Consumer Reports. 2 September 2016. Archived from the original on 3 September 2016. Retrieved 3 September 2016.

"Samsung recalls Galaxy Note 7 worldwide due to exploding battery fears". The Verge. 2 September 2016. Archived from the original on 3 September 2016. Retrieved 2 September 2016.

"[Statement] Samsung Will Replace Current Note7 with New One". Samsung. 2 September 2016. Archived from the original on 16 September 2016. Retrieved 17 September 2016.

"Consumer Reports: Samsung Should Officially Recall the Galaxy Note7". Consumer Reports. Archived from the original on 4 September 2016. Retrieved 3 September 2016.

"Government Issues Official Recall of Samsung Galaxy Note 7". Forbes. 16 September 2016. Archived from the original on 17 September 2016. Retrieved 17 September 2016.

Bart, Jansen (5 October 2016). "Smoking, popping Samsung Galaxy Note 7 prompts Southwest evacuation". USA Today. Archived from the original on 5 October 2016. Retrieved 5 October 2016.

Golson, Jordan (8 October 2016). "Another replacement Galaxy Note 7 has reportedly caught fire". Archived from the original on 9 October 2016. Retrieved 9 October 2016.

Golson, Jordan (14 October 2016). "The Galaxy Note 7 will be banned from all US airline flights". The Verge. Archived from the original on 15 October 2016. Retrieved 14 October 2016.

Etherington, Darrell (14 October 2016). "U.S. Department of Transportation bans Galaxy Note 7 from all flights". TechCrunch. Archived from the original on 15 October 2016. Retrieved 14 October 2016.

"¿Tienes un Galaxy Note 7? Aerolíneas mexicanas prohíben volar con él". elfinanciero.com.mx. Archived from the original on 19 October 2016. Retrieved 18 October 2016.

Batterman, L. Robert (23 June 2016). "Soccer Legend Pelé Calls for a Yellow Card against Samsung". Archived from the original on 26 June 2016. Retrieved 23 June 2016.

Japan Display Inc. is a Japanese company that manufactures and supplies LCD panels for smartphones, tablets, automotive applications and laptops. The company was founded in 2010 and is headquartered in Tokyo, Japan. As of March 2016, the company had a market capitalization of US$2.4 billion.

Japan Display Inc."s products are used in a variety of electronic devices including smartphones, tablets, automotive applications and laptops. The company"s panels are used by major electronics manufacturers such as Apple Inc., Samsung Electronics Co., Ltd., LG Electronics Inc., HTC Corporation and Huawei Technologies Co., Ltd.

Japan Display Inc. (JDI) is a leading display panel manufacturer based in Tokyo, Japan. The company was formed in 2011 as a joint venture between Sony, Hitachi and Toshiba. JDI supplies LCD panels to some of the world’s largest electronics manufacturers, including Apple, LG and Samsung.

JDI’s cutting-edge technology has made it one of the leaders in the global display market. The company’s products are used in a wide range of devices, from smartphones and tablets to TVs and laptops. JDI has a strong R&D team that is constantly developing new display technologies. The company is publicly listed on the Tokyo Stock Exchange and had a revenue of US$5.6 billion in 2018.

Japan Display Inc. is a leading display panel manufacturer that designs, develops, and manufactures cutting-edge display panels and systems for smartphones, tablets, notebooks, automotive applications, digital cameras, camcorders and digital signage. The company has over 8,000 employees and operates 13 factories in 9 countries around the world.

Japan Display Inc. offers a wide range of products and services that are designed to meet the needs of its customers. The company’s product portfolio includes: LCD panels, OLED panels, touch panels, flexible displays and integrated modules. Japan Display Inc. also provides a variety of value-added services such as: design support, engineering support, production support and after-sales service. The company’s products are used in a variety of market segments including consumer electronics, automotive, industrial and medical. Japan Display Inc.

Japan Display Inc. (JDI) is a leading display manufacturer that designs, develops, and manufactures LCDs for smartphones, tablets, automotive applications, and other consumer electronics. The company went public in 2010 and is listed on the Tokyo Stock Exchange. JDI reported a net loss of ¥23.4 billion ($205 million) in the fiscal year ended March 31, 2016, compared to a net profit of ¥10.3 billion in the previous fiscal year. This was primarily due to lower sales of LCD panels for smartphones and increased competition from Chinese manufacturers.

Looking at Japan Display"s financial performance over the past few years, it"s clear that the company has been struggling to maintain profitability. In the fiscal year ended March 31, 2016, JDI reported a net loss of ¥23.4 billion ($205 million), compared to a net profit of ¥10.

One of the biggest challenges that Japan Display Inc. (JDI) is facing is the competition from South Korean and Chinese display manufacturers. JDI has been losing market share to these companies in recent years, and it is becoming increasingly difficult for JDI to compete on price. Additionally, JDI is also facing challenges from new technologies such as OLED and quantum dot displays. While JDI has developed its own OLED technology, it has yet to commercialize it on a large scale. And while quantum dot displays are not yet widely used in smartphones, they are expected to gain popularity in the coming years.

Dublin, Sept. 27, 2021 (GLOBE NEWSWIRE) -- The "Global TFT LCD Display Panel Market Report and Forecast 2021-2026" report has been added to ResearchAndMarkets.com"s offering.

The global TFT-LCD display market attained a value of approximately USD 164 billion in 2020. Aided by use of TFT-LCD displays in automotive, the market is projected to further grow at a CAGR of 5.2% between 2021-2026 to reach USD 223 billion by 2026.

TFT-LCD display is a kind of liquid crystal display where each pixel is attached to a film transistor to improve colour quality, as each pixel on a TFT-LCD is attached to a transistor. TFT is deployed in all computer screens television screens since the start of century, because the technology offers better response time and improved colour quality than older technologies and prevents distortion of image. With favourable properties like light weight, slim, and high-resolution features, and due to the small size of each transistor, they consume less power owing to which TFT-LCD displays find applications in nearly every electronic device with a display including smartphones, television screens, computers, and PCs.

The market demand for TFT-LCD display can be attributed to increasing deployment of TFT-LCD display in average and large sized flat panel TVs in the household sector. The growing demand for slim, high resolution smart phones among the younger generation, owing to the work from home trends is further invigorating market growth. Other electronic devices like PCs and desktops that deploy TFT-LCD display for better screen resolution, sharp, and vibrant colours are supporting the market growth.

Due to the rapidly expanding industrialisation and a subsequent rise in disposable incomes, especially in emerging economies of the Asia-Pacific region like India and China, the market demand for personal vehicles equipped with LCD displays for specific functions and entertainment purposes is positively impacting the market growth of TFT-LCD displays. Furthermore, transportation vehicles like aeroplanes, trains, and, buses are emerging as users of TFT-LCD displays, aided by government spending on public transport. Therefore, a rising demand for TFT-LCD displays from the automotive sector is providing lucrative industrial growth opportunities.

The report looks into the market shares, plant turnarounds, capacities, investments, and mergers and acquisitions, among other major developments of the key players in the industry.

ResearchAndMarkets.com is the world"s leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey