lcd panel price ihs supplier

(January 23, 2019) – Global shipments of large thin-film transistor (TFT) liquid crystal display (LCD) panels rose again in 2018 despite concerns of over-supply in the market. In particular, area shipments increased by 10.6 percent to 197.9 million square meters compared to the previous year, driven by TV and monitor panels, according to

Fierce price competition in large 65- and 75-inch display panels was ignited as Chinese panel maker BOE started the mass production of the panels in 2018 at its B9 10.5-generation facility. “With BOE operating the 10.5-generation line, panel makers have become more aggressive on pricing since early 2018 to digest their capacity,” said

Rising demand for gaming-PC and professional-purpose monitors boosted shipments of high-end, large panels. “Some panel makers have allocated more monitor panels to the fab, replacing existing TV panels, to make up for poor performance of that business,” Wu said.

Demand for other applications, which include public, automotive and industrial displays, recorded the highest growth rates of 17.5 percent by area and 28.6 percent by unit. “Panel makers view these applications as a new cash cow that can compensate for the sharp price erosion in main panels for TVs, monitors and notebook PCs,” Wu said.

LG Display led the area shipments of large display panels, with a 21 percent share in 2018, followed by BOE (17 percent) and Samsung Display (16 percent). BOE boasted the largest unit-shipment share of 23 percent, followed by LG Display (20 percent) and Innolux (17 percent), according to the

Large TFT LCD panel shipment growth is expected to continue in 2019. The preliminary forecast for unit shipments of three major products indicates that panel makers will continue to focus on the monitor and notebook PC panel businesses, increasing shipments by 5.3 percent and 6.6 percent, respectively, over the year, while shipments of TV panels are forecast to grow just 2.6 percent.

In 2019, three new 10.5-generation fabs – ChinaStar’s T6, BOE’s second fab and Foxconn/Sharp’s Guangzhou line – are expected to start mass production. All of them are assigned to manufacture TV panels, further boosting TV panel supply. “As the TV panel business is predicted to remain tough, panel makers, who enjoyed relatively better outcomes with monitor and notebook PC panels in 2018, will likely focus on the IT panel businesses,” Wu said.

IHS Markit provides information about the entire range of large display panels shipped worldwide and regionally, including monthly and quarterly revenues and shipments by display area, application, size and aspect ratio for each supplier.

IHS Markit (Nasdaq: INFO) is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers next-generation information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 business and government customers, including 80 percent of the Fortune Global 500 and the world’s leading financial institutions.

IHS Markit is a registered trademark of IHS Markit Ltd. and/or its affiliates. All other company and product names may be trademarks of their respective owners © 2019 IHS Markit Ltd. All rights reserved.

(2 November, 2017) – A major decrease in manufacturing cost gap between organic light-emitting diode (OLED) display and liquid crystal display (LCD) panel is expected to support the expansion of OLED TVs, according to new analysis from

analysis estimates that the total manufacturing cost of a 55-inch OLED ultra-high definition (UHD) TV panel -- at the larger end for OLED TVs -- stood at $582 per unit in the second quarter of 2017, a 55 percent drop from when it was first introduced in the first quarter of 2015. The cost is expected to decline further to $242 by the first quarter of 2021, IHS Markit said.

The manufacturing cost of a 55-inch OLED UHD TV panel has narrowed to 2.5 times that of an LCD TV panel with the same specifications, compared to 4.3 times back in the first quarter of 2015.

“Historically, a new technology takes off when the cost gap between a dominant technology and a new technology gets narrower,” said Jimmy Kim, principal analyst for display materials at IHS Markit. “The narrower gap in the manufacturing cost between the OLED and LCD panel will help the expansion of OLED TVs.”

However, it is not just the material that determines the cost gap. In fact, when the 55-inch UHD OLED TV panel costs were 2.5 times more than LCD TV panel, the gap in the material costs was just 1.7 times. Factors other than direct material costs, such as production yield, utilization rate, depreciation expenses and substrate size, do actually matter, IHS Markit said.

The total manufacturing cost difference will be reduced to 1.8 times from the current 2.5 times, when the yield is increased to a level similar to that of LCD panels. “However, due to the depreciation cost of OLED, there are limitations in cost reduction from just improving yield,” Kim said. “When the depreciation is completed, a 31 percent reduction in cost can be expected from now.”

by IHS Markit provides more detailed cost analysis of OLED panels, including details of boards, arrays, luminescent materials, encapsulants and direct materials such as driver ICs. The report also covers overheads such as occupancy rate, selling, general and depreciation costs. In addition, this report analyzes OLED panels in a wide range of sizes and applications.

IHS Markit (Nasdaq: INFO) is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers next-generation information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 key business and government customers, including 85 percent of the Fortune Global 500 and the world’s leading financial institutions. Headquartered in London, IHS Markit is committed to sustainable, profitable growth.

IHS Markit is a registered trademark of IHS Markit Ltd and/or its affiliates. All other company and product names may be trademarks of their respective owners © 2017 IHS Markit Ltd. All rights reserved.

At least five LCD display factories at the epicenter of the coronavirus outbreak are suffering production slowdowns, which is turn is expected to have an effect on the supply and pricing of displays used in PCs and LCD TVs.

Five LCD fabs reside in Wuhan, China, which has basically been shut down to prevent the coronavirus from spreading. Informa Tech’s IHS Markit service said Friday that they expect that the capacity utilization for all LCD fabs in China could fall by at least 10 percent and by as much as 20 percent during February.

As a result, LCD panel prices are expected to rise. IHS said that preliminary estimates say that per-panel prices could rise $1 to $2, but could go as high as $3 to $5. That might not sound like much, but manufacturers typically tack on extra profit margins at each stage of production, potentially raising sale prices somewhat higher.

IHS estimates that about 55 percent of all LCD panels in the world will ship from China in 2020, meaning that the Chinese outbreak will have worldwide effects on the supply chain. Five fabs are in Wuhan itself, including two fabs owned by China Star Optoelectronics Technology, two owned by Tianma, and one BOE fab.

“Display facilities in Wuhan currently are dealing with the very real impacts of the coronavirus outbreak,” said David Hsieh, senior director of displays, at IHS Markit technology research, in a statement. “These factories are facing shortages of both labor and key components as a result of mandates designed to limit the contagion’s spread. In the face of these challenges, top display suppliers in China have informed our experts that a near-term production decline is unavoidable.”

IHS reported seeing panic buying, including doublebooking, where a buyer will buy as much as they need from two suppliers just to ensure that they’ll be able to get the supplies they require. Even if the supplies are there, IHS also said that production at several key third-party LCD module suppliers has now ceased, severely impacting panel production throughout the country.Besides the slowdown in production at fabs that are already operating, IHS said that it expects new fabs to not come on line as quickly as expected.

All this is expected to have a direct effect on LCD panel pricing, and possibly ripple effects through laptop manufacturing as well. It’s worth noting that while Intel and AMD did not cite coronavirus effects among their forecasts, Microsoft did, with a broader than usual forecast for the second half of the year.

Since the beginning of the year, LCD panel prices showed varying degrees of growth, IHS announced the latest international market panel price trend, Which the highest increase of more than 17 dollars. However, because the LCD panel in the cost of the total TV cost accounted for about 80%, so the price of the overall trend of television also has been affected.

According to statistical data, both small-screen or large-screen TV panels have appeared in varying degrees of gains, it can be said to cover the full size. In fact, in addition to 720P and 1080P panel, 4K ultra-high-definition TV panels have not escaped the wave of price increases. Among them, 49-inch 4K ultra-high-definition panel, the maximum increase of 13 dollars, Whose maximum offer is163 dollars. 55-inch 4K ultra-high-definition TV panel, the maximum increase of 8 US dollars, whose maximum offer is 205 dollars.

Throughout the TV market, After Letv decided on increasing the price of 100-200 yuan on the parts of 4th generation super Letv, Storm Group will also be the third quarter net profit fell sharply attributed to the TV panel and other raw material prices.

When it comes to the increasing reseaon,there are two main aspects.On the one hand,the fourth quarter of each year is the sales season of the panel,meanwhile,TFT Display TV manufacturers’ increasing demands.So that TV manufacturers can just accept the panel prices.On the other hand,the supply of TV panels is very tight because of capacity,which led to increasing price.

For licensed IHS members only, this impressive 11" x17" wall display presents highlights from the IHS Code of Ethics that you, as a member, have sworn to uphold. Display this piece in your office to show your patients that you not only say you take your profession and their care seriously, but you are willing to back it up with a written, international code of ethics. Printed in IHS colors on quality stock, this piece truly elevates you as a professional and sets you apart from others. Framing is not included.

LONDON (June 21, 2018) – Despite better-than-expected first-quarter demand for thin-film transistor liquid-crystal display (TFT-LCD) TV sets and TV panels, market players would be well advised to adopt a more conservative outlook in demand growth for the coming quarters, according to IHS Markit (Nasdaq: INFO), a world leader in critical information, analytics and solutions.

Earlier market expectations assumed that demand would slow in the first quarter prompted by the observation that TV set makers would put a hold on panel purchases based on hopes that panel prices would drop further. Such a view was largely attributed by the development of Chinese panel makers planning aggressive investments over the next two to three years.

As it turned out, panel makers managed to sell more panels than originally forecasted in the first quarter because panel prices declined much faster than expected. According to IHS Markit, TV panel unit shipments increased by 13.3 percent in the first quarter compared to a year ago, while TV set shipments rose 7.9 percent during the same period.

“LCD TV panel shipments are expected to grow faster than the LCD TV set shipments, expanding the accumulated gap between the two even further,” said Ricky Park, director of display research at IHS Markit.

According to the latest Displaylong term demand forecast tracker by IHS Markit, the accumulated gap between LCD TV panel and set shipments in the second and third quarters of 2018 is expected to be higher than past 10 years, reaching 8.3 percent and 8.4 percent, respectively, from 7.9 percent in the first quarter. Furthermore, the gap is expected to remain high until 2019.

“The main reason for the higher gap is the aggressive investment in 10.5 generation fabs. TFT LCD capacity, in terms of area, will soar in the next four years,” Park said. “As capacity is expected to increase more than demand, panel suppliers will likely push to sell panels at lower prices while set makers are to hesitate buying panels expecting the price to drop even further.”

However, when the accumulated gap in panel-set shipments is high, an inventory correction should always follow. “TV makers should narrow the gap for healthy inventory control and reducing panel orders is a step in that direction,” Park said. “If TV set makers’ panel purchasing drops, it will likely cause a cash flow issue to panel suppliers, and they would need to reduce the utilization rate to control the supply.”

Research firm IHS Markit says the large format LCD display market is booming at the moment, with panel shipments hitting a record monthly high in July 2018 in terms of unit and area shipment.

London-based IHS says unit shipments increased by 10 percent in July compared to a year ago, to reach 64.3 million units, while area shipments jumped 19 percent during the same period to 17 million square meters.

“New facilities from China, such as BOE’s Gen 10.5, CHOT’s Gen 8.6 and CEC-Panda’s Gen 8.6, started mass production in the first half of this year. The production at the fabs has increased since the second quarter of 2018 as their glass inputs and production yield rates have improved,”says Robin Wu, principal analyst with the research firm.“Despite the growing production, panel makers have maintained the utilization rate and instead tried to push out panel shipments by lowering panel prices in the first half of 2018. That’s one of the reasons that panel shipments are continuously growing.”

The Large Area Display Market Tracker report is primarily about the TV, and not the commercial panel market, but gives a broader sense of what is going on and who the big players are in LCD.

IHS says The LCD TV panel contributed to the record high shipments of larger-than-9-inch LCD panels in July. Unit shipments of LCD TV panels increased by 15 percent in July year on year to 24.6 million units and area shipments jumped 21 percent to 13.3 million square meters, according to the by IHS Markit.

Panel makers suffered from high TV panel inventories in the first half of 2018 due to growing production capacities. Panel prices have been weak for a year and panel makers’ profit margins have plunged. “Therefore, panel makers wanted to clear up the inventory before the third quarter, high-demand season, when they aim to raise the panel price back again,” Wu said. “That has led to the fast growth in TV panel shipments lately, which as a result pulled the total large panel shipments to a historical high in July.” As the panel makers hoped, LCD TV panel prices rebounded in July 2018.

Chinese panel maker BOE led the large TFT LCD market in July 2018 in terms of unit shipments with a stake of 24 percent, followed by LG Display with 19 percent. However, in terms of area shipments, South Korea’s LG Display continued to lead with a 20 percent share, followed by BOE with 18 percent.

With Chinese panel makers accelerating the mass production of large thin-film transistor (TFT) liquid crystal display (LCD) TV panels faster than expected, they accounted for 33.9 percent of the 60-inch and larger LCD TV panel shipments in the first quarter of 2019. Their market share has expanded nearly 10 times from 3.6 percent in just over a year, according to business information provider IHS Markit (Nasdaq: INFO).

South Korean panel makers still accounted for the largest share in the 60-inch and larger LCD TV panel shipments, with a 45.1 percent share in the first quarter. However, Chinese panel makers’ share in the large LCD TV panel market is expected to continue to grow.

“When BOE’s B9 10.5G fab started its mass production in the first quarter of 2018, the industry expected that its full ramp-up would take quite a time due to a learning curve,” said Robin Wu, principal analyst at IHS Markit. “However, it did not take as long and BOE has become the largest supplier of 60-inch and larger LCD TV panels since the end of 2018.”

BOE accounted for 29 percent of the total 60-inch and larger LCD TV panel shipments in the first quarter of 2019. It is estimated that the B9 10.5G fab has reached its maximum capacity of 120,000 sheets in the first quarter of 2019.

ChinaStar also started to mass produce large LCD panels at its T6 10.5G fab in the first quarter. CEC-Panda and CHOT ramped up mass production at their 8.6G fabs to the maximum design capacity in the first quarter. Foxconn/Sharp is forecast to begin mass production at their Guangzhou 10.5G fab in the second half of 2019.

“As both Chinese and South Korean panel suppliers are focusing on large LCD TV panels, competition between them will become more intense, pressuring the price of large LCD TV panels even further throughout 2019,” Wu said.

BOE led the unit shipments of large TFT-LCD panels with a 24.6 percent share in the first quarter of 2019, followed by LG Display (18.8 percent) and Innolux (16 percent). By area shipments, LG Display accounted for the largest share of 20 percent, followed by BOE (19.9 percent) and Samsung Display (14.1 percent).

The Large Area Display Market TrackerbyIHS Markit provides information on the entire range of large display panels shipped worldwide and regionally, including monthly and quarterly revenues and shipments by display area, application, size and aspect ratio of each supplier.

Until about a year ago, active-matrix organic light-emitting diode (AMOLED)–based smartphones remained Samsung’s niche. Almost all the AMOLEDs Samsung was making went into Galaxy products. AMOLED prices were relatively high compared to equivalent liquid crystal displays (LCDs). Samsung’s AMOLED fab utilization was low, and it was struggling to ramp up its A3 flexible AMOLED dedicated fab. Its AMOLED business was challenged to raise profits.

What a difference a year makes! Now in June 2016, the outlook for AMOLED smartphones has dramatically shifted in a positive direction. Samsung’s AMOLED fab utilization is high, prices for external customers are on par with LCDs, and the company’s AMOLED business is profitable. Over the same period, it has become evident that Apple plans to transition the iPhone display from rigid LCDs to flexible AMOLEDs in the next couple of years. Meanwhile, more and more people are talking about the coming flexible or foldable OLED displays that will bring revolutionary change to the form factor of handheld devices.

These shifts in market outlook have created an unprecedented wave of new flexible AMOLED fab investment plans for makers in Korea, China, and Japan. Competitors are trying to replicate Samsung’s success, hoping to escape the commoditization and low profitability of LCDs—and chasing after potential Apple business. A large number of new fabs are now being built, and they are the most expensive ever made relative to glass size and input capacity.

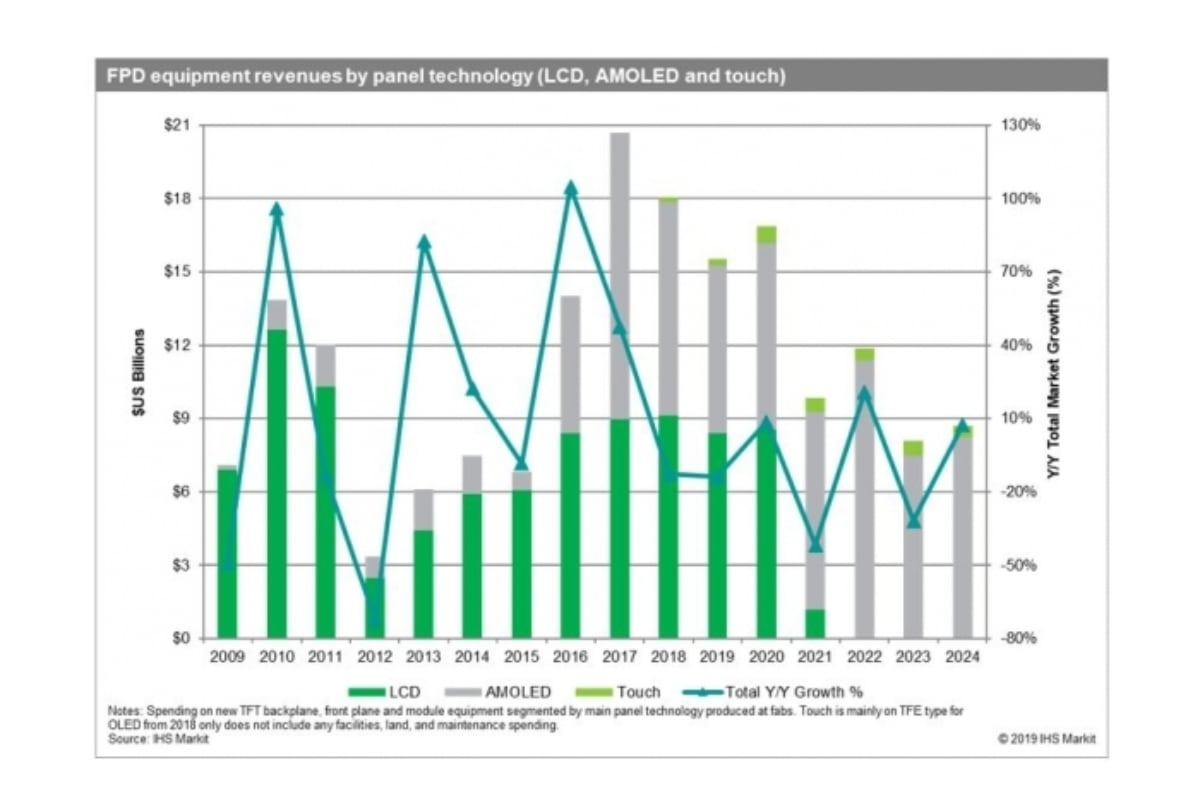

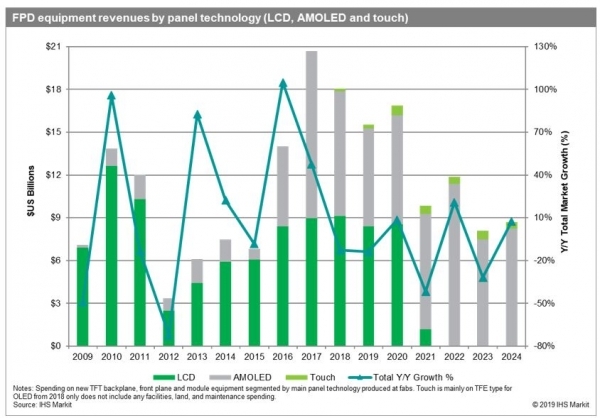

Although Samsung’s AMOLED process to date has used a simplified p-channel metal-oxide-semiconductor (PMOS) thin-film transistor (TFT) for the back plane, other makers and new lines targeting Apple demand appear to be preparing for processes that use up to 50% more mask steps. Low temperature polysilicon and oxide (LTPO) is one of the candidates. This drives significantly more TFT equipment, automation, and other spending. Furthermore, all the new AMOLED fabs will be designed to produce flexible AMOLEDs or will be hybrid rigid/flexible lines. Flexible capability adds costs to the TFT backplane process by requiring flexible substrate coating, curing, and encapsulation steps. Flexible capability adds cost to the front plane process by requiring thin-film encapsulation (TFE), laser lift-off (LLO), and a variety of other steps necessary to handle flexible panels. As shown below, the new flexible AMOLED fabs for mobile display production have a total costs that is almost 1.4x higher than previous rigid AMOLED lines, according to the IHS Technology Display Supply Demand & Equipment Tracker report.

In other words, pushed by a complex TFT process and flexible display requirements, the new AMOLED fabs are the most expensive flat-panel display (FPD) factories ever built, nearly 1.4x that of previously constructed rigid AMOLED lines.

Capital equipment markets tend to be highly cyclical, but the high cost of flexible AMOLED fabs is pushing the equipment market in 2016 and 2017 to near-historic two-year highs. Some concerns have been raised that equipment supply bottlenecks will restrict panel makers’ ability to build fabs according to schedule. Most of these concerns have focused on high-resolution photolithography machines, RGB evaporators, and some high-performance vacuum tools.

However, presented with the best business opportunity since 2010 and 2011, equipment makers are rapidly adding capacity as well as actively managing their suppliers and scheduling in order to meet customer requests. Although any unexpected supply chain disruption could delay some fab plans, it now appears that most of the new fabs will be built out in line with panel makers’ target schedules.

According to the IHS Technology Display Supply Demand & Equipment Tracker report, the large number of new flexible AMOLED investments, along with the high costs of these lines, is pushing the FPD equipment market to near-record two-year highs of $12.6 billion in 2016 and $12.3 billion in 2017.

Forecasting the supply and demand of flexible AMOLEDs in 2018 is a challenging task, not only due to the assumptions that must be made about both capacity and demand, but also the questions about yield rates, how long it will take fabs to ramp and begin commercial production, and the price competitiveness of these new fabs. Building rational forecasts of capacity is possible based on panel maker plans because new factories have lead times of up to two years.

In order to test supply and demand under the more optimistic scenario of faster adoption by Apple, the IHS forecast for total AMOLED smartphones was increased to 503 million units in 2017 and 653 million in 2018. This includes Samsung Galaxy phones, other brands such as Chinese cell phone makers, and a reasonable adoption forecast for Apple. Other mobile applications are also counted in demand. Relatively long ramp-up times and low yield rates for all makers, except Samsung, were assumed. Prices were presumed to be competitive and not directly tested in this analysis.

Analyzing all panel makers’ capacity plans and the comparatively aggressive demand forecast, the glut level is projected to increase from 2016 through 2018, suggesting a trend of growing oversupply.

Samsung’s strategy likely involves adding enough capacity to enable it to continue—for as long as possible and almost exclusively—to dominate the AMOLED market for mobile applications. Samsung Display has a substantial technology and cost lead over even its closest competitors. It controls much of its own process know-how, and it will be a difficult path for followers to catch up in the near- or even mid-term. According to our analysis, Samsung could potentially maintain its AMOLED monopoly through 2018 or longer, even when taking into consideration the large increase in demand as the iPhone transitions from LCD to AMOLED.

The shift from rigid LCD to flexible AMOLED is the most significant change in FPD process technology since the start of the LCD era almost 20 years ago. All panel makers are now scrambling to avoid being left behind during this technology revolution.

However, as supply/demand analysis suggests, all the capacity being added by new AMOLED players may well get ahead of how much the market can absorb. Demand could grow faster than the accelerated forecast; however, it is not clear by how much. In 2018 and 2019 the market for both rigid and flexible AMOLED may be restricted by prices. It is unlikely that many makers will be able to compete on price and performance with Samsung or even with low-cost, high-end LCDs without incurring financial losses.

In the long run, all the investment in AMOLED capacity will help reduce material prices, strengthen the equipment supply chain, and allow the market to trend towards balance. However, it would also not be surprising for new AMOLED entrants to struggle to ramp up new fabs in 2018 and 2019, and suffer from low utilization and profitability as the industry works through the currently forecast flexible AMOLED supply glut.

IHS has reported weeks of LCD TV panel inventory held by suppliers are set to increase to 5.0 in August, up from 4.9 in July and 4.8 in June. The last time the inventory reached this level was January 2012.

�LCD TV panel inventory is entering into above-normal territory in July and August,� said Ricky Park, senior manager for large-area displays at IHS. �Stockpiles are on the rise because of a delay in economic recovery for many areas of the world, along with growing uncertainty regarding domestic demand in China. The combination of a glut in panels and weak demand will cause price reductions to accelerate in the third quarter compared to the second.�

Average LCD TV panel prices are forecast to decline in a range from 3 to 6 percent in the third quarter, compared to a 1 to 2 percent decrease in the second quarter.

For one, Chinese TV brands overstocked panels in the first half. Moreover, the government in Beijing has terminated its subsidy program for energy-saving TVs, a development expected to dampen demand in the second half.

In light of the weak demand and rising inventory, Chinese TV manufacturers are cutting panel orders. These domestic TV brands account for more than 80 percent of shipments in China, the world�s largest TV market.

With the exception of February during the Lunar New Year holiday when they disposed of more panels than they actually purchased, China�s Top 6 television makers increased their LCD panel purchases significantly every month in 2013 compared to the same periods in 2012. However, they plan to purchase 24 percent fewer panels in July and 25 percent less in August than they did during the same months in 2012.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey