lcd panel price ihs factory

(2 November, 2017) – A major decrease in manufacturing cost gap between organic light-emitting diode (OLED) display and liquid crystal display (LCD) panel is expected to support the expansion of OLED TVs, according to new analysis from

analysis estimates that the total manufacturing cost of a 55-inch OLED ultra-high definition (UHD) TV panel -- at the larger end for OLED TVs -- stood at $582 per unit in the second quarter of 2017, a 55 percent drop from when it was first introduced in the first quarter of 2015. The cost is expected to decline further to $242 by the first quarter of 2021, IHS Markit said.

The manufacturing cost of a 55-inch OLED UHD TV panel has narrowed to 2.5 times that of an LCD TV panel with the same specifications, compared to 4.3 times back in the first quarter of 2015.

“Historically, a new technology takes off when the cost gap between a dominant technology and a new technology gets narrower,” said Jimmy Kim, principal analyst for display materials at IHS Markit. “The narrower gap in the manufacturing cost between the OLED and LCD panel will help the expansion of OLED TVs.”

However, it is not just the material that determines the cost gap. In fact, when the 55-inch UHD OLED TV panel costs were 2.5 times more than LCD TV panel, the gap in the material costs was just 1.7 times. Factors other than direct material costs, such as production yield, utilization rate, depreciation expenses and substrate size, do actually matter, IHS Markit said.

The total manufacturing cost difference will be reduced to 1.8 times from the current 2.5 times, when the yield is increased to a level similar to that of LCD panels. “However, due to the depreciation cost of OLED, there are limitations in cost reduction from just improving yield,” Kim said. “When the depreciation is completed, a 31 percent reduction in cost can be expected from now.”

by IHS Markit provides more detailed cost analysis of OLED panels, including details of boards, arrays, luminescent materials, encapsulants and direct materials such as driver ICs. The report also covers overheads such as occupancy rate, selling, general and depreciation costs. In addition, this report analyzes OLED panels in a wide range of sizes and applications.

IHS Markit (Nasdaq: INFO) is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers next-generation information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 key business and government customers, including 85 percent of the Fortune Global 500 and the world’s leading financial institutions. Headquartered in London, IHS Markit is committed to sustainable, profitable growth.

IHS Markit is a registered trademark of IHS Markit Ltd and/or its affiliates. All other company and product names may be trademarks of their respective owners © 2017 IHS Markit Ltd. All rights reserved.

by IHS Markit, manufacturing cost of the 5.9-inch organic light-emitting diode (OLED) panel with notch design, as in the Apple iPhone X, is estimated to be $29. It is found to be 25 percent higher than manufacturing cost of full-display OLED panel without the notch design used in the 5.8-inch display for the Samsung Galaxy S9. Similar cost gap is also found in the thin-film transistor liquid crystal display (TFT-LCD). Manufacturing cost of a 6-inch notch TFT-LCD panel is estimated to be $19, 20 percent higher than similar-sized non-notch, full-display LCD panel.

“Notch cutting should accompany yield loss, resulting in increases in manufacturing cost. In case of TFT-LCD, a notch design may push up the manufacturing cost even to the level of rigid, full-screen OLED’s,” said

Quarterly shipments of the iPhone X, Apple’s first smartphone model using OLED panels, have reportedly been smaller than previous iPhone models’ so far, mainly due to higher selling price, caused by expensive OLED panels. “Apple seems to be in the middle of manufacturing optimization,” Kim said.

“Eventually, manufacturing cost for notch OLED will fall more rapidly than that for notch TFT-LCD. The plastic substrate for OLED is not as brittle as glass used in TFT-LCD, so it should be easier to cut the notch, theoretically.”

by IHS Markit includes manufacturing cost analysis and forecasts of OLED display panels in mass production for smartwatch, smartphone, tablet PC and TV.

IHS Markit (Nasdaq: INFO) is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers next-generation information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 business and government customers, including 80 percent of the Fortune Global 500 and the world’s leading financial institutions.

IHS Markit is a registered trademark of IHS Markit Ltd. and/or its affiliates. All other company and product names may be trademarks of their respective owners © 2018 IHS Markit Ltd. All rights reserved.

LONDON(May 28, 2018) - Notch design of smartphone displays is estimated to raise manufacturing cost of display panels by more than 20 percent, according to IHS Markit (Nasdaq: INFO), a world leader in critical information, analytics and solutions.

According to the OLED Display Cost Model by IHS Markit, manufacturing cost of the 5.9-inch organic light-emitting diode (OLED) panel with notch design, as in the Apple iPhone X, is estimated to be $29. It is found to be 25 percent higher than manufacturing cost of full-display OLED panel without the notch design used in the 5.8-inch display for the Samsung Galaxy S9. Similar cost gap is also found in the thin-film transistor liquid crystal display (TFT-LCD). Manufacturing cost of a 6-inch notch TFT-LCD panel is estimated to be $19, 20 percent higher than similar-sized non-notch, full-display LCD panel.

"Notch cutting should accompany yield loss, resulting in increases in manufacturing cost. In case of TFT-LCD, a notch design may push up the manufacturing cost even to the level of rigid, full-screen OLED"s," said Jimmy Kim, Ph.D. and senior principal analyst for display materials at IHS Markit. "For OLED panels, cost increase caused by notch design seems to be even higher."

Quarterly shipments of the iPhone X, Apple"s first smartphone model using OLED panels, have reportedly been smaller than previous iPhone models" so far, mainly due to higher selling price, caused by expensive OLED panels. "Apple seems to be in the middle of manufacturing optimization," Kim said.

"Eventually, manufacturing cost for notch OLED will fall more rapidly than that for notch TFT-LCD. The plastic substrate for OLED is not as brittle as glass used in TFT-LCD, so it should be easier to cut the notch, theoretically."

The OLED Display Cost Model by IHS Markit includes manufacturing cost analysis and forecasts of OLED display panels in mass production for smartwatch, smartphone, tablet PC and TV.

IHS Markit (Nasdaq: INFO) is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers next-generation information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 business and government customers, including 80 percent of the Fortune Global 500 and the world"s leading financial institutions.

IHS Markit is a registered trademark of IHS Markit Ltd. and/or its affiliates. All other company and product names may be trademarks of their respective owners © 2018 IHS Markit Ltd. All rights reserved.

At least five LCD display factories at the epicenter of the coronavirus outbreak are suffering production slowdowns, which is turn is expected to have an effect on the supply and pricing of displays used in PCs and LCD TVs.

Five LCD fabs reside in Wuhan, China, which has basically been shut down to prevent the coronavirus from spreading. Informa Tech’s IHS Markit service said Friday that they expect that the capacity utilization for all LCD fabs in China could fall by at least 10 percent and by as much as 20 percent during February.

As a result, LCD panel prices are expected to rise. IHS said that preliminary estimates say that per-panel prices could rise $1 to $2, but could go as high as $3 to $5. That might not sound like much, but manufacturers typically tack on extra profit margins at each stage of production, potentially raising sale prices somewhat higher.

IHS estimates that about 55 percent of all LCD panels in the world will ship from China in 2020, meaning that the Chinese outbreak will have worldwide effects on the supply chain. Five fabs are in Wuhan itself, including two fabs owned by China Star Optoelectronics Technology, two owned by Tianma, and one BOE fab.

“Display facilities in Wuhan currently are dealing with the very real impacts of the coronavirus outbreak,” said David Hsieh, senior director of displays, at IHS Markit technology research, in a statement. “These factories are facing shortages of both labor and key components as a result of mandates designed to limit the contagion’s spread. In the face of these challenges, top display suppliers in China have informed our experts that a near-term production decline is unavoidable.”

IHS reported seeing panic buying, including doublebooking, where a buyer will buy as much as they need from two suppliers just to ensure that they’ll be able to get the supplies they require. Even if the supplies are there, IHS also said that production at several key third-party LCD module suppliers has now ceased, severely impacting panel production throughout the country.Besides the slowdown in production at fabs that are already operating, IHS said that it expects new fabs to not come on line as quickly as expected.

All this is expected to have a direct effect on LCD panel pricing, and possibly ripple effects through laptop manufacturing as well. It’s worth noting that while Intel and AMD did not cite coronavirus effects among their forecasts, Microsoft did, with a broader than usual forecast for the second half of the year.

A major decrease in manufacturing cost gap between organic light-emitting diode (OLED) display and liquid crystal display (LCD) panel is expected to support the expansion of OLED TVs, according to new analysis from IHS Markit (Nasdaq: INFO), a world leader in critical information, analytics and solutions.

The he OLED Display Cost Modelanalysis estimates that the total manufacturing cost of a 55-inch OLED ultra-high definition (UHD) TV panel — at the larger end for OLED TVs — stood at $582 per unit in the second quarter of 2017, a 55 percent drop from when it was first introduced in the first quarter of 2015. The cost is expected to decline further to $242 by the first quarter of 2021, IHS Markit said.

The manufacturing cost of a 55-inch OLED UHD TV panel has narrowed to 2.5 times that of an LCD TV panel with the same specifications, compared to 4.3 times back in the first quarter of 2015.

“Historically, a new technology takes off when the cost gap between a dominant technology and a new technology gets narrower,” said Jimmy Kim, principal analyst for display materials at IHS Markit. “The narrower gap in the manufacturing cost between the OLED and LCD panel will help the expansion of OLED TVs.”

However, it is not just the material that determines the cost gap. In fact, when the 55-inch UHD OLED TV panel costs were 2.5 times more than LCD TV panel, the gap in the material costs was just 1.7 times. Factors other than direct material costs, such as production yield, utilization rate, depreciation expenses and substrate size, do actually matter, IHS Markit said.

The total manufacturing cost difference will be reduced to 1.8 times from the current 2.5 times, when the yield is increased to a level similar to that of LCD panels. “However, due to the depreciation cost of OLED, there are limitations in cost reduction from just improving yield,” Kim said. “When the depreciation is completed, a 31 percent reduction in cost can be expected from now.”

The OLED Display Cost Model by IHS Markit provides more detailed cost analysis of OLED panels, including details of boards, arrays, luminescent materials, encapsulants and direct materials such as driver ICs. The report also covers overheads such as occupancy rate, selling, general and depreciation costs. In addition, ths report analyzes OLED panels in a wide range of sizes and applications.

For information about purchasing this report, contact the sales department at IHS in Americas at +1 (844) 301-7334 or [email protected]; in Europe, Middle East and Africa (EMEA) at +44 1344 328 300 or [email protected]; or Asia-Pacific (APAC) at +60 4 291 3600 or [email protected].

LONDON — Despite better-than-expected first-quarter demand for thin-film transistor liquid-crystal display (TFT-LCD) TV sets and TV panels, market players would be well advised to adopt a more conservative outlook in demand growth for the coming quarters, according to IHS Markit (Nasdaq: INFO), a world leader in critical information, analytics and solutions.

Earlier market expectations assumed that demand would slow in the first quarter prompted by the observation that TV set makers would put a hold on panel purchases based on hopes that panel prices would drop further. Such a view was largely attributed by the development of Chinese panel makers planning aggressive investments over the next two to three years.

As it turned out, panel makers managed to sell more panels than originally forecasted in the first quarter because panel prices declined much faster than expected. According to IHS Markit, TV panel unit shipments increased by 13.3 percent in the first quarter compared to a year ago, while TV set shipments rose 7.9 percent during the same period.

“LCD TV panel shipments are expected to grow faster than the LCD TV set shipments, expanding the accumulated gap between the two even further,” said Ricky Park, director of display research at IHS Markit.

According to the latest Display long term demand forecast tracker by IHS Markit, the accumulated gap between LCD TV panel and set shipments in the second and third quarters of 2018 is expected to be higher than past 10 years, reaching 8.3 percent and 8.4 percent, respectively, from 7.9 percent in the first quarter. Furthermore, the gap is expected to remain high until 2019.

“The main reason for the higher gap is the aggressive investment in 10.5 generation fabs. TFT LCD capacity, in terms of area, will soar in the next four years,” Park said. “As capacity is expected to increase more than demand, panel suppliers will likely push to sell panels at lower prices while set makers are to hesitate buying panels expecting the price to drop even further.”

However, when the accumulated gap in panel-set shipments is high, an inventory correction should always follow. “TV makers should narrow the gap for healthy inventory control and reducing panel orders is a step in that direction,” Park said. “If TV set makers’ panel purchasing drops, it will likely cause a cash flow issue to panel suppliers, and they would need to reduce the utilization rate to control the supply.”

LONDON –The large flat-panel display (FPD) market, which is currently experiencing oversupply, is expected to move towards a more balanced and even tight market by the third quarter of 2019, albeit briefly, according to IHS Markit (Nasdaq: INFO), a world leader in critical information, analytics and solutions.

The current imbalance for large FPDs, larger than 9 inches, is causing panel prices to fall, which is weighing heavily on profitability of panel makers. The declining profitability is already contributing to capacity rationalization and low prices are currently expected to stimulate demand. The large FPD glut is forecast to fall to 8.2 percent, below the 10-percent balance bar, in the third quarter.

With the exception of the third quarter of 2018, when demand was seasonally high, prices have deteriorated continuously since the second half of 2017. In the fourth quarter of 2018, weighted-average large-panel prices fell 2.7 percent. This price decline rate is expected to accelerate to 5.4 percent in the first quarter of 2019.

Falling prices have also decreased profits, even pushing long-time Taiwanese liquid crystal display (LCD) maker CPT to file for bankruptcy protection in December 2018. Since then, the company’s production has almost completely stopped and it is unclear when or if it will resume.

The combination of low prices and growing inventories is finally causing panel makers to lower factory utilization rates. The average industry-wide utilization rate is anticipated to drop to 84 percent in the first quarter of 2019, down 3.5 percentage points from the previous year, marking the lowest level since the first quarter of 2016.

Some panel makers will also either close legacy LCD facilities or convert them to organic light-emitting diode (OLED) lines while some others will postpone their planned investment in new facilities.

“Capacity reduction and shuttering of existing FPD factories, in addition to reduced utilization rates in the first quarter of 2019, looks like a harbinger of a growing trend,” said Charles Annis, senior director at IHS Markit. “With so much new capacity currently being built out, substantial amounts of uncompetitive legacy production capacity are expected to be taken offline, as the industry works to balance supply and demand.”

According to the AMOLED and LCD Supply Demand & Equipment Intelligence Serviceby IHS Markit, a more balanced supply of large FPD panels should lead to firmer pricing and profitability. Some TV makers are also now predicting tighter supply later this year and have begun to increase panel procurement, which is already encouraging panel makers to start negotiating price increases on some panel sizes. Demand for large FPD panels is expected to increase to 57 million square-meters in the third quarter of 2019, up about 10 percent from a year ago.

“Although there are caveats about the global economy, early year optimism and market timing, lower prices continue to spur demand expectations,” Annis said. “As excess capacity is shuttered and demand increases, supply and demand will self-correct over time.”

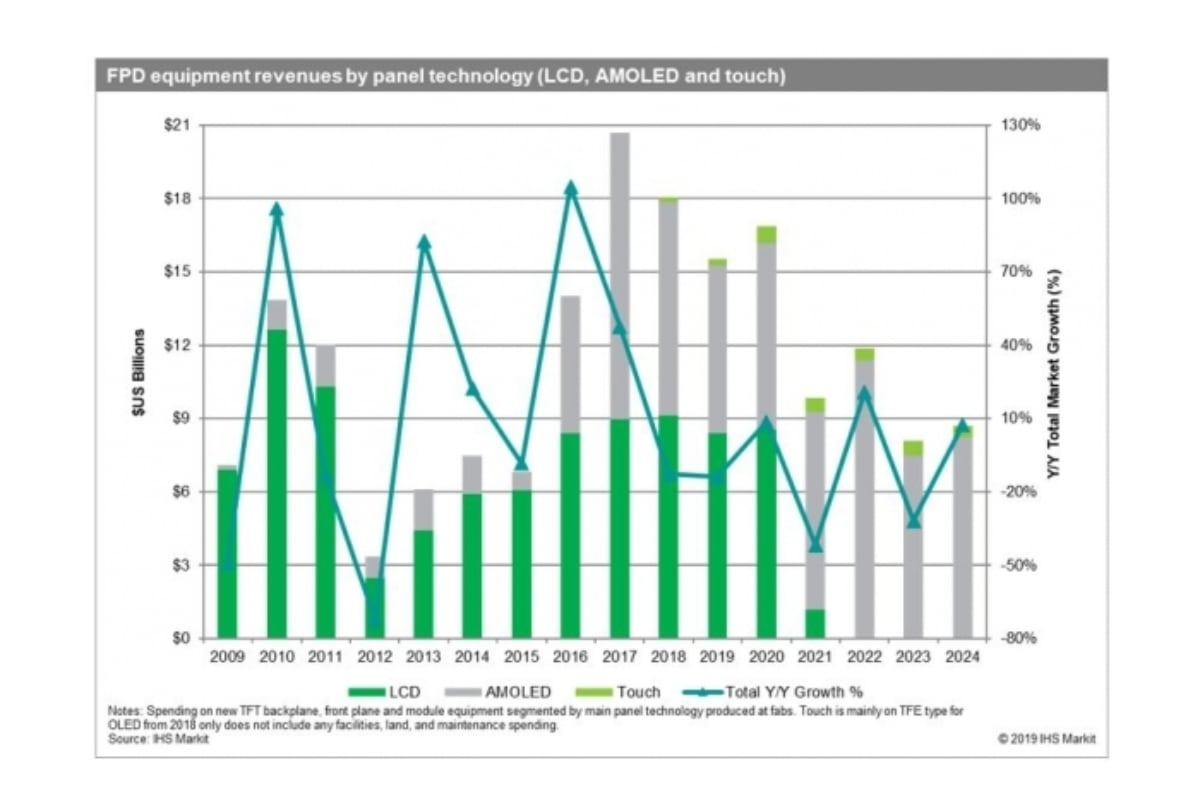

Global corporate investment into LCD displays is expected to become obscure beginning in 2022, triggering forecasts that suppliers producing LCD-related equipment will quickly have to switch their main area of business.

According to market research firm IHS Markit, the final investment into the sector will be next year when BOE expands its B17 line producing Gen-10.5 panels and CSOT makes investment into its T7 plant for Gen-10.5 displays.

Investment into OLED, on the other hand, will surge. IHS Markit said over the next five years, up to $8billion is to be poured into the sector. Chinese panel companies are likely to spend extensively on Gen-6 flexible OLEDs, Y-OCTA and TFE technology. Expenses on ink-jet equipment are also to rise.

The tech research firm IHS Markit says the day will come when big microLED display walls will not just be affordable by Arab royalty, Russian oligarchs and NBA free agents.

The global market for microLED displays is expected to grow to 15.5 million units by 2026, driven by steep declines in manufacturing costs, says the firm in the newly released IHS Markit Micro LED Display Technology & Market report.

At the moment, and into next year, microLED shipments are expected to total less than 1,000. “However,” says IHS, “with manufacturing costs plunging during the coming years, microLED pricing will drop as well, allowing the technology to gradually find acceptance in applications including smart watches, televisions, augmented-reality systems and smartphones.”

“Despite their extremely high price tag compared to conventional LCD and OLED panels, microLED displays offer advantages in brightness and energy efficiency that make them an attractive alternative for ultra-small and ultra-large applications,”says Jerry Kang, associate director at IHS Markit. “The manufacturing process for microLED will allow suppliers to reduce their production costs over time. Once the process matures, microLED sales will begin to rise.”

IHS suggests the manufacturing cost of a 75-inch display will drop to one-fifth of its current expense by 2026. I’m not sure that a 75-inch microLED display panel exists right now, but if it did, it would probably cost north of $50,000, maybe $100,000???

Mass transfer manufacturing, says IHS, is expected to reach a maturity threshold in 2024. “Despite the growth in acceptance, microLED shipments in 2026 will still amount to just 0.4 percent of the global flat-panel display market,” Kang says.“However, with shipments of nearly 16 million units that year, microLED will have entered mass-market territory, setting the stage for much wider acceptance during the following years.”

Global revenue for AMOLED TV displays will expand to $7.5 billion (€6.8bn) in 2025, up from $2.9 billion in 2019, as reported by the IHS Markit | Technology AMOLED & Flexible Display Intelligence Service. Although AMOLED TVs have only been on the market since 2013, they are rapidly gaining share, with these types of sets expected to account for 20.6 per cent of the $36 billion TV display market in 2025, up from just 8.6 per cent in 2019.

“Despite carrying a much higher average selling price (ASP) than LCD TVs, AMOLED TVs are extremely appealing to consumers because of their slim form factor, light weight and wide color gamut,” said Jerry Kang, associate director at IHS Markit | Technology. “Starting in 2020, AMOLED TV ASPs are expected to begin to decline due to increases in manufacturing capacity spurred by the adoption of a more advanced production process. This will pave the way for much more widespread adoption of AMOLED TVs.”

The AMOLED TV ASP currently is about four times more than the LCD TV ASP, based on a comparison of 65-inch panels with a 3840 by 2160 resolution. Because of this, TV brands are eager to reduce AMOLED prices to make them more attractive to consumers.

One development expected to result in major price declines is the use of multi-model glass (MMG) substrates in Gen 8 display manufacturing fabs. With its capability to support multiple display sizes on a single substrate, MMG can improve the efficiency of manufacturing, reduce product costs and help diversify product line-ups.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey