credit card with lcd display in stock

OK, this one gets a WOW. I have to admit I dont exactly get how it works, but Im loving that one of the FUTURE intended uses is to be able to check your balance right from the card… ok that freaked me out a little.

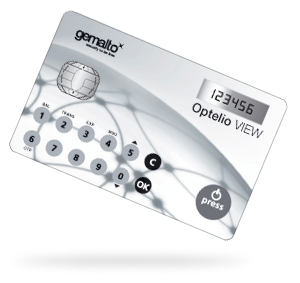

MasterCard has introduced a new high-tech credit card — — one that looks and functions almost exactly like an ordinary card, save for the integrated display and numerical keypad. The screen looks and acts like the display on a calculator; it should boost security by allowing the cardholder to generate single use numerical passwords for authentication.

“Instead of sending customers another bulky token, could we replace something which already exists in the customer’s wallet?” asked V. Subba, regional head of retail banking products for Standard Chartered Bank. “That was when credit, debit and ATM cards, immediately came to mind.”

Banks looking to boost security for online banking use a separate authentication token or device, the company noted. A Display Card could do both — and in the future it could incorporate additional functionalities and be able to indicate other real time information such as available credit balance, loyalty or reward points, recent transactions and so on.

“With the continued growth in online and now mobile initiated remote payments, consumers are naturally demanding increased security,” explained Matthew Driver, a regional president for MasterCard.

Pity the poor credit card. In these days of smartphones, tablets, and sharks with frickin" laser beams attached to their heads, they just seem so retro.

But they"re getting a makeover. In Singapore, MasterCard has unveiled a credit card to be released in January 2013 that includes "an embedded LCD display and touch-sensitive buttons," the company said this week. Eventually, this card might use its display to show "real time information such as available credit balance, loyalty or reward points, recent transactions, and other interactive information." But for now, the technology will be used to generate one-time passwords as an extra security measure.

"The MasterCard Display Card, manufactured by NagraID Security, looks and functions almost exactly like a regular credit, debit or ATM card, but features an embedded LCD display and touch-sensitive buttons which allow a cardholder to generate a One-Time Password (OTP) as an authentication security measure," MasterCard said. "From January 2013 onwards, all Standard Chartered Online Banking or Breeze Mobile Banking users will use the Standard Chartered security token card as a new personal security device for higher-risk transactions such as payments or transfers above a certain amount, adding third party payees, or changing personal details." Advertisement

The idea isn"t a new one. It"s not even MasterCard"s first attempt. The company actually unveiled very similar cards in June 2010 for use in Turkey, and they have been rolled out to other countries such as Romania. Visa launched almost identical cards in Europe last year, and a company called Dynamics showed off some newfangled credit cards with displays at this year"s Consumer Electronics Show. MasterCard touts the cards as a way to demand extra tokens from customers without making credit cards a hassle to use.

Stealing and using credit card data is far too easy, so adding two-factor authentication technology into the cards themselves strikes us as a good idea. But even without newfangled cards, the process of how we pay for stuff is getting an overhaul, albeit a slow one. NFC chips, Apple"s Passbook, and Google Wallet are among the options for higher-tech ways to pay. The ubiquity of smartphones may make it more likely that phone-based systems will outpace the adoption of new types of credit cards, especially as these display cards have been around a couple of years without spreading worldwide. But most of us are still using regular old credit cards—and if our next credit cards embed some modern technology to make them more secure, so much the better.

Credits cards and debit cards have chips in them to ward off fraud. But Dynamics is introducing a new Wallet Card today that can run circles around that technology.

The Wallet Card has the support of a consortium of financial companies, including MasterCard, which led the last financing round for Pittsburgh, Pennsylvania-based Dynamics. The Wallet Card has a cell phone chip and most of the working parts of a computer, including a display — all inside a piece of plastic that looks like any other credit card.

Dynamics is showing the Wallet Card at CES 2018, the big tech trade show in Las Vegas this week. Jeff Mullen, founder and CEO of Dynamics, said in an interview that the new card will provide an “unprecedented level of security.”

For instance, if you learn from the display on the card that the last purchase made on your card was fraudulent, you can request a new card from the bank and it will be issued on the spot, with proper authentication. You no longer have to call the bank to get a card reissued. Your new number account and card number are simply downloaded onto the card.

If you lose the card or report it stolen or forget your pin code, the bank can disable the card through the cell connection and send you a new card. Cards can be couriered to the consumer in a matter of hours, and the consumer can restore the wallet by downloading cards. The speed could reduce fraud losses and prevent purchase delays, Mullen said.

Another is that you can now have multiple cards on one Wallet Card. Consumers can access their debit, credit, prepaid, multicurrency, one-time use, or loyalty cards on a single card with the tap of a button. When you get to a checkout stand, you could choose to pay with points or credit simply by pressing a button on the card.

It is also easily distributed. Banks can distribute Wallet Card anytime and anywhere — such as in their retail branches, during events, or even in-flight, and consumers can activate it immediately. Card information can then be downloaded through a secure, over-the-air cellular connection. At the same time, Mullen said the cards have built-in security in hardware elements.

And the technology could lead to tighter connections between consumers, issuers, and retailers. Messages can be sent to the Wallet Card at any time. For example, after every purchase, a message may be sent to notify the consumer of the purchase and of their remaining balance if they used a debit or loyalty card.

Consumers can be notified of a suspicious purchase and click on “Not me” to have a fraud alert set and a new card number issued. They can also receive coupons directly on their cards.

The Wallet Card has more than 200 internal components, and it’s the latest rendition of electronic credit and debit cards that Mullen and his team dreamed up at Carnegie Mellon University. He started the company in 2007, beginning a long journey to replace the mag stripe credit card, which has been in use since the 1970s and is fraught with all kinds of security risks.

This new card has “organic harvesting,” which means it can use renewable energy sources to keep its battery charged. It has a card-programmable magnetic stripe, card-programmable EMV chip (the chip cards that have become so popular), and a card-programmable contactless chip. That means it could be used in just about any territory.

Dynamics has the support of the Wallet Card Consortium, which includes a number of big banks, payment networks, and carriers. Members include Visa, MasterCard, Sprint, and JCB (a Tokyo-based credit card company).

Dynamics has raised $110 million to date from investors that include MasterCard, CIBC, Adams Capital Management, and Bain Capital Ventures. The company’s earlier intelligent account cards are currently used by more than 10 million consumers. Customers include the big Canadian coffee chain Tim Horton’s, the Upper Deck Company, and CIBC.

Since then the Indiegogo crowdfunding campaign has been issued success and has already raised over $1.2 million with still 16 days remaining...Read more

Meet MasterCard"s new "Display Card," which basically combines the usual credit/debit or ATM card with an authentication token. The authentication portion features a touch-sensitive keypad and LCD display -- hence the name "Display Card" -- for reflecting a one-time password (OTP).

Currently, many banks issue a separate authentication token for online banking services, particularly high-risk transactions, such as payments or transfers above a certain amount, adding payees, or changing personal details. The new 2-in-1 cards would therefore eliminate the hassle of carrying a separate authentication device -- good news for people who carry their whole lives in their pockets.

Besides generating OTPs, the Display Card may in the future be able to show your available credit balance, reward points, or even recent transactions.

MasterCard has launched a credit card that incorporates an LCD screen and a small keyboard with the idea of eliminating the need to always carry an authentication device when verifying transactions made online.

The credit card brand MasterCard has introduced the MasterCard Display Card, the first card to feature a display and buttons. This card has been manufactured by NagraID Security and has the same appearance and operation as a normal and current credit or debit card, unlike LCD display and touch-sensitive buttons. this allows the user to generate a temporary password (OTP, for its acronym in English), something that various banking institutions request from customers who perform operations that need an additional layer of security. So far, to do this it was necessary to use another device, That which, in the opinion of MasterCard, ended up being a nuisance to the user. With this new card you can see the OTP without the need for another terminal.

In addition, as assured by the company, in the future it may also be possible to add functionalities such as making it display information in real time “as the available balance, loyalty points, recent transactions and other interactive information”.

From January 2013 all online or mobile banking customers (Breeze) Standard Chartered will use this card as a security device for high-risk transactions or to make payments that exceed a certain amount.

In the opinion of Matthew Driver, President of MasterCard in Southeast Asia, the continued growth of online banking and mobile banking has made customers demand greater security, a request to which they hope to respond with this card.

New: Manage bookings, payments, and staff on a powerful handheld device with Square Appointments on Square TerminalTake payments. Get paid. No surprises.

Chip cards (or EMV) are the new standard in payment cards. Insert chip cards into Terminal and complete the sale in just two seconds—one of the fastest you’ll find.

Get up and running in fewer than five minutes—no need to go through a bank. Square Terminal is an intuitively designed credit card machine so you, your team, and your customers can use it right away.Software solutions customized for your business

Square Terminal can integrate with your custom or third-party POS to automatically sync in-person payments with your software.It won’t let you down. And neither will we.

“With Square Terminal, everything is very simple and transparent. All things considered, we save money with Square.”Kerrie Volau, Practice Manager, Eye CarumbaThere’s so much more waiting for you.

If your business does more than $250,000 in credit card sales, talk to us about a custom processing rate and other ways we can save you money.Frequently asked questionsSquare Terminal is an all-in-one device for taking card payments and printing receipts. It comes with free Square Point-of-Sale software that’s easy to set up and easy to use, and a built-in battery that lasts all day, so you never miss a sale.

Square Terminal is a credit card terminal that makes it easy for any business to take card payments and run a point of sale. Customers simply tap, insert, or swipe their credit or debit cards for fast, efficient, and seamless payments.

Square Terminal costs $299 before taxes and fees, with hardware financing options available at checkout. To connect Square Terminal to the internet via ethernet, or to connect accessories such as a cash drawer, barcode scanner, or additional printers, you can add an optional Hub for $39.

Square Terminal requires an internet connection. Connect Square Terminal to the internet via Wi-Fi, or via Ethernet with an optional Hub. When you don’t have an internet connection, you can use Offline Mode to take payments.Available at local retailers*All credit sale plans are issued by Block, Inc. Not available to merchants in AL, DE, MS, MO, NH, and TN. Purchase amounts must be from $49 to $10,000. APR is 15%. Available plan lengths vary from 3, 6, 12, and/or 24 months installments depending on purchase amount. Sales tax, where applicable, will be due at checkout. All plans subject to credit approval and other factors.

Apple Card Monthly Installments (ACMI) is a 0% APR payment option available only in the U.S. to select at checkout for certain Apple products purchased at Apple Store locations, apple.com, the Apple Store app, or by calling 1-800-MY-APPLE and is subject to credit approval and credit limit. See support.apple.com/kb/HT211204 for more information about eligible products. Variable APRs for Apple Card other than ACMI range from 15.24% to 26.24% based on creditworthiness. Rates as of January 1, 2023.

If you choose the pay‑in‑full or one‑time‑payment option for an ACMI‑eligible purchase instead of choosing ACMI as the payment option at checkout, that purchase will be subject to the variable APR assigned to your Apple Card. Taxes and shipping are not included in ACMI and are subject to your card’s variable APR. See the Apple Card Customer Agreement for more information. ACMI is not available for purchases made online at the following special stores: Apple Employee Purchase Plan; participating corporate Employee Purchase Programs; Apple at Work for small businesses; Government, and Veterans and Military Purchase Programs, or on refurbished devices. iPhone activation required on iPhone purchases made at an Apple Store with one of these national carriers: AT&T, Sprint, Verizon, or T‑Mobile.

To access and use all the features of Apple Card, you must add Apple Card to Wallet on an iPhone or iPad with the latest version of iOS or iPadOS. Update to the latest version by going to Settings > General > Software Update. Tap Download and Install.

Apple Card Family Co-Owners will have full visibility into each other’s account activity, and Owners will have visibility into all Participant account activity.

An Apple Cash card is required to use Daily Cash, except if you do not have an Apple Cash card, in which case you can only apply your Daily Cash as a credit on your statement balance. The Apple Cash card is issued by Green Dot Bank, Member FDIC. See apple.com/apple-pay for more information. Daily Cash is earned on purchases after the transaction posts to your account. Actual posting times vary by merchant. Daily Cash is subject to exclusions, and additional details apply. See the Apple Card Customer Agreement for more information.

Credit limits can only be combined when an existing Apple Card customer requests to share merge their account with another existing Apple Card customer. Merging existing accounts is subject to credit approval and general eligibility requirements.

Each Co-Owner is individually liable for all balances on the co-owned Apple Card including amounts due on your Co-Owner’s account before the accounts are merged. Each Co-Owner will be reported to credit bureaus as an Owner on the account. In addition, Co-Owners will have full visibility into all account activity and each Co-Owner is responsible for the other Co-Owner’s instructions or requests. Co-ownership involves risk, including payment history and other information about your Apple Card, including negative items like missed payments. Addition of new Co-Owner or merging existing accounts is subject to credit approval and general eligibility requirements. For Apple Card eligibility requirements, see https://support.apple.com/en-us/HT209218. Either Co-Owner can close the account at any time which may negatively impact your credit and you will still be responsible for paying all balances on the account. For details on account sharing options including some of the risks and benefits, see https://support.apple.com/en-us/HT212020.

Building credit “equally” means that the payment history and other information about your Apple Card will be reported to credit bureaus for each co-owner. Each co-owner is individually liable for all balances on the co-owned Apple Card and each will be reported to credit bureaus as an owner on the account. Credit reporting includes payment history and other information about your Apple Card, including negative items like missed payments. Card usage and payment history may impact each co-owners credit score differently because each individual’s credit history will include information that is unique to them. Either co-owner can close the account at any time but you will still be responsible for paying all balances on the account. For details on account sharing options including some of the risks and benefits, see https://support.apple.com/en-us/HT212020.

If you are a Participant, you are able to spend on the account, but are not responsible for payments. Being a Participant who is reported to the credit bureaus on an account that has a negative payment history (e.g. the account goes past due) or is over utilized can have negative effects on your credit. The account owner remains responsible for all purchases made by a Participant. For more details including some risks and benefits of being a Participant, see https://support.apple.com/en-us/HT212271.

If you are a Participant, you are able to spend on the account, but are not responsible for payments. Being a Participant who is reported to the credit bureaus on an account that has a negative payment history (e.g. the account goes past due) or is over utilized can have negative effects on your credit. For details on credit reporting, see https://support.apple.com/en-us/HT212020. For more details including some risks and benefits of being a Participant, see https://support.apple.com/en-us/HT212271.

An Apple Cash card is required. Participants under 18 on Apple Card Family accounts must have the family organizer of their Apple Cash Family set up their own Apple Cash card. If you do not have an Apple Cash account, Daily Cash can be applied as a credit on account owner’s statement balance by contacting Goldman Sachs Bank USA. The Apple Cash card is issued by Green Dot Bank, Member FDIC.

Apple Card Monthly Installments (ACMI) is a 0% APR payment option available only in the U.S. to select at checkout for certain Apple products purchased at Apple Store locations, apple.com, the Apple Store app, or by calling 1-800-MY-APPLE and is subject to credit approval and credit limit. See support.apple.com/kb/HT211204 for more information about eligible products. Variable APRs for Apple Card other than ACMI range from 15.24% to 26.24% based on creditworthiness. Rates as of January 1, 2023.

If you choose the pay‑in‑full or one‑time‑payment option for an ACMI‑eligible purchase instead of choosing ACMI as the payment option at checkout, that purchase will be subject to the variable APR assigned to your Apple Card. Taxes and shipping are not included in ACMI and are subject to your card’s variable APR. See the Apple Card Customer Agreement for more information. ACMI is not available for purchases made online at the following special stores: Apple Employee Purchase Plan; participating corporate Employee Purchase Programs; Apple at Work for small businesses; Government, and Veterans and Military Purchase Programs, or on refurbished devices. iPhone activation required on iPhone purchases made at an Apple Store with one of these national carriers: AT&T, Sprint, Verizon, or T‑Mobile.

Trade-in values will vary based on the condition, year, and configuration of your eligible trade-in device. Not all devices are eligible for credit. You must be at least 18 years old to be eligible to trade in for credit or for an Apple Gift Card. Trade‑in value may be applied toward qualifying new device purchase, or added to an Apple Gift Card. Actual value awarded is based on receipt of a qualifying device matching the description provided when estimate was made. Sales tax may be assessed on full value of a new device purchase. In‑store trade‑in requires presentation of a valid photo ID (local law may require saving this information). Offer may not be available in all stores, and may vary between in‑store and online trade‑in. Some stores may have additional requirements. Apple or its trade‑in partners reserve the right to refuse or limit quantity of any trade‑in transaction for any reason. More details are available from Apple’s trade‑in partner for trade‑in and recycling of eligible devices. Restrictions and limitations may apply.

Nov. 6, 2012: The MasterCard Display Card, manufactured by NagraID Security, looks and functions almost exactly like a regular credit card but features an embedded LCD screen and touch-sensitive buttons. (MasterCard)

MasterCard has introduced a new high-tech credit card -- -- one that looks and functions almost exactly like an ordinary card, save for the integrated display and numerical keypad. The screen looks and acts like the display on a calculator; it should boost security by allowing the cardholder to generate single use numerical passwords for authentication.

“Instead of sending customers another bulky token, could we replace something which already exists in the customer’s wallet?” asked V. Subba, regional head of retail banking products for Standard Chartered Bank. “That was when credit, debit and ATM cards, immediately came to mind.”

Banks looking to boost security for online banking use a separate authentication token or device, the company noted. A Display Card could do both -- and in the future it could incorporate additional functionalities and be able to indicate other real time information such as available credit balance, loyalty or reward points, recent transactions and so on.

“With the continued growth in online and now mobile initiated remote payments, consumers are naturally demanding increased security,” explained Matthew Driver, a regional president for MasterCard.

La Chaux de Fonds, Switzerland, 10th June 2010 – NagraID Security, a subsidiary of the Kudelski Group (SIX:KUD), is pleased to announce that its families of display cards passed MasterCard"s (CSI – Card Structure & Integrity) approval process, thus demonstrating the required levels of durability, safety and compliance to ISO standards required for the commercial launch of banking cards and the introduction into MasterCard"s brand standards and rules.

The innovative Debit and Credit MasterCard Display Card looks and feels like a normal credit or debit card but comes with an additional small display and a button that enables card holders to use the same card for standard banking payment functionality and to generate second-factor one-time passwords (OTPs), thereby providing strong authentication.

The cards are very reliable and extremely simple to use. They offer optimal security to achieve banking transactions outside payment terminals using one single device.

This password generation technology complies with the requirements of MasterCard"s 3D Secure Chip Authentication Program (CAP). Optionally, a touch-sensitive keypad with twelve keys permits access to advanced functionality such as electronic signature and authentication modes, as well as to enhanced security features such as challenge-response applications and PIN code card protection.

"Cards were born from cardboard, they"ve been "mag striped" and "chipped" and now we enter their silicon age, with an LCD display and touchpad opening up a multitude of possibilities. With NagraID"s recent achievements to demonstrate compliance to industry standards, the stage has well and truly been set to deliver the next generation consumer"s card proposition" says Eric Tomlinson, MasterCard Europe.

"This display card is designed to provide a very high level of security and reliability as well as ease of use. Users simply press a button to generate an OTP for secure access to their online services," commented Philippe Guillaud, Executive Vice President and CTO of NagraID Security. He also added "The programmable nature of this platform makes it future proof and one can expect to see even more exciting and fantastic functionality in the near future."

MasterCard directed promotional initiatives and large scale roll-outs will ensure that market price expectations are achieved. "As the world evolves towards increasing online and cashless transactions, the timing of our partnership with MasterCard is ideal, as it enables the growing security expectations of a rapidly expanding base of digital technology users to be quickly addressed via a secure, reliable and unified solution in a familiar and convenient form-factor." said Cyril Lalo, President and CEO of NagraID Security.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey