lcd panel price index supplier

Prices for all TV panel sizes fluctuated and are forecast to fluctuate between 2020 and 2022. The period from March 2020 to July 2021 saw the biggest price increases, when a 65" UHD panel cost between 171 and 288 U.S. dollars. In the fourth quarter of 2021, such prices fell and are expected to drop to an even lower amount by March 2022.Read moreLCD TV panel prices worldwide from January 2020 to March 2022, by size(in U.S. dollars)Characteristic32" HD43" FHD49"/50" UHD55" UHD65" UHD------

DSCC. (January 10, 2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) [Graph]. In Statista. Retrieved January 11, 2023, from https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars)." Chart. January 10, 2022. Statista. Accessed January 11, 2023. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. (2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars). Statista. Statista Inc.. Accessed: January 11, 2023. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "Lcd Tv Panel Prices Worldwide from January 2020 to March 2022, by Size (in U.S. Dollars)." Statista, Statista Inc., 10 Jan 2022, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC, LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) Statista, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/ (last visited January 11, 2023)

LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) [Graph], DSCC, January 10, 2022. [Online]. Available: https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

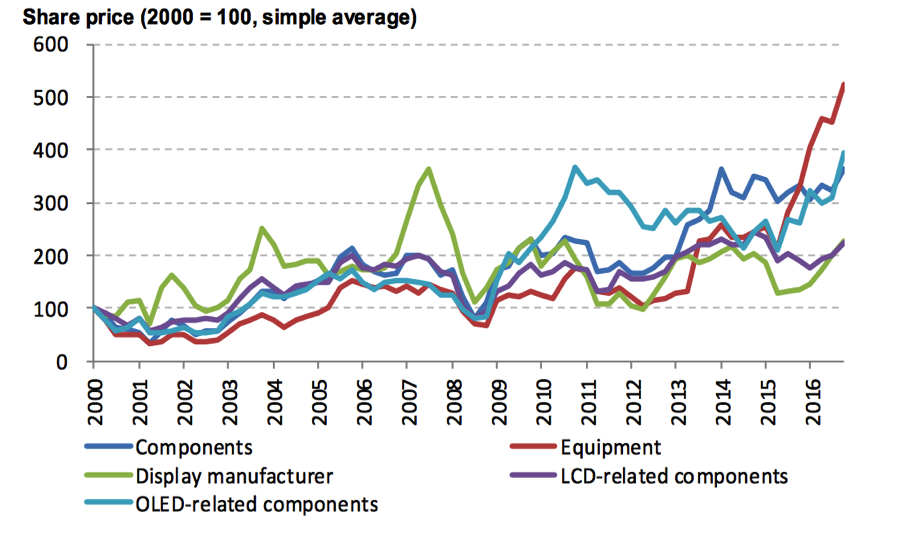

The worldwide large panel industry not only affects TV/monitor and notebook PC product costs but also represents a leading indicator of the worldwide TV/monitor and notebook PC market.

This tracker provides total market size and vendor share for the following technology areas. Measurement for this tracker is in shipments, prices, and capacities.

TFT 5.6" inch LCD screens 640*480 with T-con board 1. Display Type: TFT 5.6" inch LCD screens 2. Display mode: Transmissive 3. Resolution: 640x480 dots 4. Pin NO# : 40 5. Outline Dimensions: 126.5*100*5.71 mm 6.Luminous Intensity for LCM 300 Cd/m2 7. Interface Type: RGB 8. Backlight: White LED 9. Operating voltage: +2.6V~3.3V 10. Viewing Angle: 6 O’clock 11. Operating Temp: -20°C~+70°C 12. Storage Temp: -30°C~+80°C Product pictures: Company Strenghth: 1> ISO9001 certificated , Factory Direct S upplied 2> RoHS Compliant, Lead Free, Reach Compliant 3> Competitive P rice and Short L ead-time 4> Professional Team with Rich Experiences in Design/Mfg/Quality Control 5> Small MOQ Support & Fast Response to Customers 6> Long Product Life Time Our Clients: About Us: Found in 2007, SAEF TECH is an experienced LCD/LCM manufacturer. With good quality, professional service, and competitive price, we have been qualified by many wellknown companies around the world. Our strategic customers include LG in Korea(white goods & remote controller), Uniden in Japan(scanner), Cisco in USA(conference phone), Jabil in UK(industrial meter & instrument), Vtech in HK(IP phone in conference room), Ametek in Germany(bulldozer dash board), AML in USA(banking system), Spectrum mfg in Canada(meter), etc.

LCD TV panel prices, which peaked in summer 2021, fell through the second half of the year and are continuing to fall in the new year. The pace of price decreases is slowing, and we expect that pattern to continue through the first half of the year as prices approach cash cost for some panel makers.

In our updates in the summer of 2021, we referred to a series of events that suggested slowing demand and increasing supply, and no developments since have altered this outlook. The increasing panel prices led to an unprecedented increase in TV prices in the US and around the world, which hindered demand. Inventory is now more than sufficient across the LCD value chain from panel makers to retailers, which acts as a headwind for panel prices (or a tailwind for price declines!).

The first chart here highlights our latest TV panel price update, showing the both the biggest price increases in the history of the flat panel display industry, from May 2020 to June/July 2021 and then the fastest price decreases in the industry in the autumn of 2021. All sizes of panels have been at lower prices Y/Y since November.

In January 2022, prices for all TV panel sizes fell, and for the third month in a row, the largest percentage declines occurred in the two sizes that are optimized on Gen 8.5/Gen 8.6 fabs. Prices for both 49”/50” panels and 55” panels declined by 8% and 7%, respectively, while both smaller and larger sizes had smaller price declines M/M.

The fourth quarter of 2021 saw the biggest Q/Q price declines in the history of the flat panel display industry. Price declines ranged from 17% on 75” panels to 41% on 32” panels, with the general pattern of larger price declines for small sizes and vice versa. Across the six sizes we track, the Q4 price declines averaged 32%.

Although the declines are slowing down in Q1, they are still severe for panel makers. We expect Q/Q price declines in Q1 2022 to range between 9% and 23% and to average 14%. With the most severe price declines occurring on 49”/50” and 55” panels, those two sizes will see price declines exceeding 20%.

As we look at pricing on an area basis, we are now seeing that all sizes 55” and below seem to be equally commoditized and area prices for all these sizes are converging. In February 2022, 55” are the lowest priced panels on an area basis at $127 per square meter, but all the sizes below 65” are in a narrow range between $127 and $135.

While prices have converged for all the smaller size panels, 65” and 75” panels continue to have a premium on an area basis. For February 2022, 65” panels sell at a premium of $24 or 19% over 55”, and 75” panels have a premium of $54 or 50%. Panel makers with Gen 10.5 capacity (BOE, CSOT and Sharp SIO) are at a relative advantage in the current oversupply environment.

The last chart here shows our TV price index, set to 100 for prices in January 2014, and the Y/Y change of LCD TV panel prices. Our index increased from its all-time low of 42 in May 2020 to 87 in June 2021, but prices already declined to 45 in January. We now expect the index to decline to 41 by April, 50% lower than March 2021 and representing an all-time low for LCD TV panel prices. Although we don’t expect every screen size to hit all-time lows in Q1, 75” panels already hit an all-time low in January and we expect 65” to hit an all-time low by May.

With the COVID-19 demand surge assisted by shortages in glass and DDICs, we saw a historic year of increases in panel prices, and panel makers post their most profitable quarter ever in the second quarter of 2021. Profits declined in Q3 but not by much, and the third quarter of 2021 was the second-best quarter ever for panel maker profitability, surpassed only by its predecessor. For Q4, from the preliminary numbers available it appears there was a divergence in performance, with some panel makers feeling the full effects of lower prices while others managed to avoid the worst. As reported thus far:

The only panel maker to report full financial results, LGD reported revenues up 19% Q/Q but net income down 62% and net margin decreased from 6% to 2%. LGD’s revenue gain was attributed to increased shipments of mobile panels. The combination of lower TV prices and LGD’s loss-making mobile OLED business led to lower net income;

CSOT also gave a “forecast” with revenues of $2.7B, down 23% compared to Q3. Revenue from large-area panels declined by 31% Q/Q while shipment area increased 3% Q/Q. CSOT reported a net margin of 15% in Q3 but this likely fell dramatically in Q4 and perhaps went negative;

Caihong group, the parent of CHOT, released a “forecast” that implied a net loss of $120-$144M in Q4’21, compared to a profit of $96M in Q3. While the net loss may include one-time restructuring charges for Caihong’s glass business, the company clearly suffered from lower panel prices.

Large LCD panel prices have been continuously increasing for last 10 months due to an increase in demand and tight supply. This has helped the LCD industry to recover from drastic panel price reductions, revenue and profit loss in 2019. It has also contributed to the growth of QD and miniLED LCD TV. Strong LCD TV panel demand is expected to continue in 2021, but component shortages, supply constraints, and very high panel price increase can still create uncertainties.

It was earlier anticipated that price increases would decelerate in 2Q, but now the price increase is accelerating compared to 1Q, according to a research by DSCC. Panel prices increased by 27 percent in 4Q20 compared to 3Q and slowed down to 14.5 percent in 1Q21 compared to 4Q, but the current estimate is that average LCD TV panel prices in 2Q21 will increase by another 17 percent. The prices are expected to peak sometime in 3Q21.

There has been a surge in prices across the board from a low in May 2020 to a high point in June 2021 which does not represent the peak. There have been multiple inflection points for this cycle: the first inflection point, the month of the biggest MoM price increases, was passed in September 2020, and the price increase slowed down, then started to accelerate again in January 2021, and there is another slowdown starting in May 2021. Prices in May 2021 have reached levels last seen in July 2017.

Prices increased in 1Q21 for all sizes of TV panels, with double-digit percentage increases in sizes from 32- to 65-inch ranging from 12-18 percent. Prices for 75-inch increased by 8 percent as capacity has continued to increase on Gen 10.5 lines, where 75-inch is an efficient six-cut. Prices for every size of TV panel will continue to increase in 2Q at an even faster rate, ranging from 12 percent for 75-inch to 24 percent for 32-inch. The prices are expected to continue to increase in 3Q.

The current upturn in the crystal cycle has seen the biggest trough-to-peak price increases for LCD TV panels, and the recent acceleration of prices has further extended this record. Comparing the forecast for June 2021 panel prices with the prices in May 2020, there is a trough-to-peak increases from 34 percent for 75-inch to 181 percent for 32-inch, with an average of 111 percent. In comparison, the average trough-to-peak increase of the 2016 to 2017 cycle was 48 percent, and prior cycles saw smaller increases.

Before the current upswing, the largest panels sold with an area premium, but the current cycle has flipped that upside down. Whereas in May 2020, 75-inch panels sold at an area premium of USD 77 per square meter higher than the 32-inch panel price, as of May 2021, they are selling at a USD 65 discount on an area basis. This means that those Gen 10.5 fabs could earn higher revenues from making 32-inch panels than from 75-inch panels. The pattern for 65-inch is even more severe, and 65-inch is now selling at a USD 69 per square meter discount (alternately, a 22% area discount) compared to 32-inch.

The improved pricing for LCD TV panels has already improved the profitability of panel makers. It will continue to drive their profits even higher, especially the two prominent Taiwanese players, who have Gen 7.5 and Gen 8.5 fabs but no Gen 10.5 fabs. Chinese panel makers HKC and CHOT have a similar industrial profile and stand to benefit greatly as well. The leading companies with Gen 10.5 fabs (BOE, CSOT and Foxconn/Sharp) stand to benefit less because the price increases on the largest sizes are more modest, but every LCD panel maker is doing well.

TV price index has increased from its all-time low of 42 in May 2020 to 87 in May 2021, and it is expected to reach 89 in June and over 90 in 3Q21 before declining in 4Q. The YoY increase has surpassed 100 percent in May 2021. It will remain at elevated levels throughout the second half of 2021.

In addition to being an exceptionally large upcycle, the current upswing matches some of the longest stretches of increasing prices ever seen, more than a full year from trough to peak. The length of the upswing can be attributed to several factors: glass and driver IC shortages, the pandemic-driven demand or the potential for Korean fab downsizing.

TV makers continued to make strong profits in 1Q21 despite increasing panel prices. The TV market typically slows down in 1Q and 2Q. TV maker revenues declined seasonally in 1Q but less than usual, and the operating margins for both Samsung and LGE increased sequentially. Samsung’s CE division operating profits exceeded USD 1 billion for the quarter for only the second time ever. With demand remaining strong, TV makers have weathered the increase in panel prices and remained very profitable.

There is a surge in LCD equipment spending to respond to dramatically improved market conditions in the LCD market. DSCC sees LCD revenues rising 32 percent in 2021 to USD 112 billion on strong unit and area growth with prices and profitability rebounding to or even exceeding the 2017 levels. With LCD suppliers able to sell everything they can make at attractive margins; it should be no surprise that most LCD manufacturers are looking to expand capacity.

However, unlike previous upturns when many new fabs were built, in this upturn panel suppliers are looking to stretch their capacity through smaller investments, simplifying their processes and debottlenecking. Having said that, there will be two new Gen 8.6 mega fabs being built. The result versus last quarter is a 10 percent or a USD 2.2 billion increase in 2020-2024 LCD spending from USD 21.8 billion to USD 24 billion. The 2021 LCD equipment spending forecast is up 15 percent versus last quarter’s forecast to USD 10 billion, with 2021 LCD equipment spending up 125 percent versus 2021. In addition, 2022 was upgraded by 28 percent to USD 3.5 billion.

Although there is a healthy upgrade in LCD equipment spending in 2021 and 2022, the outlook for 2022-2024 spending is still significantly lower than in previous years, resulting in tighter capacity and slower price reductions in the next downturn. In addition, with Korean LCD suppliers expected to reduce their LCD capacity and convert to potentially higher margin OLEDs, the outlook for LCD pricing and profitability looks quite healthy, which may result in even more equipment spending, especially as miniLEDs gain acceptance.

An unfortunate and untimely string of accidents has created a historic tight glass market and caused a very unusual industry average price increase of several percent. In last few months top glass suppliers Corning, NEG, and AGC have all experienced production problems. A tank failure at Corning, a power outage at NEG, and an accident at an AGC glass plant all resulted in glass supply constraints when demand and production has been increasing.

In March 2021 Corning announced its plan to increase glass prices in 2Q21. Corning has also increased supply by starting glass tank in Korea to supply China’s Gen 10.5 fabs that are ramping up. Most of the growth in capacity is coming from Gen 8.6 and Gen 10.5 fabs in China.

Besides glass there have been other component shortages including driver ICs and polarizers. The lack of investment in polarizers and base films in 2019 caught the industry off guard when demand turned around in 2020. Multiple other materials are also in tight supply and are affecting different makers in different ways, supporting inflationary price trends.

Widespread component supply shortages could impact availability on LCD TV panels from CSOT and Innolux. The display panel manufacturers have warned that supplies of panels are expected to be tight throughout the year.

According to Li Dongsheng, chairman, TCL, panel shortages will continue in 1H21, following conditions already hampered last year during the start of the COVID-19 pandemic. The situation for 2H21 remains to be seen but for 2021 overall panel supply will be tight.

James Yang, president, Innolux, has warned of a shortage in LCD panels caused by strong demand for LCD coming out of the global crisis and the conditions are expected to continue through 2021. Innolux has seen shortages in LCD components including power semiconductors, driver ICs and glass substrates that have kept production below capacity. Shortages of ICs and semiconductors could continue right up to the 1H22.

Ironically, prior to the run-on LCD panel supplies, manufacturers were faced with the dilemma of overproduction causing a glut in inventory, which was driving prices artificially lower. This was the result of giant new LCD fabs coming online in China and other areas of Asia.

Panel makers, being cognizant of that threat, are expected to produce panels at a more tempered pace to keep margins healthy. LCD panel prices continued to rise in March after moving up in February.

Almost all Chinese panel makers are doing everything they can to incrementally increase their current factories’ capacities through productivity enhancements and new equipment purchases for debottlenecking or capacity expansions. For the same reasons, South Korean panel makers continue to delay shutting down their domestic LCD TV factories.

TV manufacturers have been moving aggressively to replenish inventories of LCD panels to meet strong sales of TVs and other devices to meeting escalating demand, particularly in the United States and Europe.

An increase in demand for larger size TVs in 2H20 combined with component shortages has pushed the market to supply constraint and caused continuous panel price increases from June 2020 to March 2021. The panel price increase resulting in higher costs for TV brands. It has also made it difficult for lower priced brands to acquire enough panels to offer lower priced TVs. Further, panel suppliers are giving priority to top brands with larger orders during supply constraint.

For 3 years, from 2017 to 2020, LCD panel makers suffered through a continuous pattern of price declines interrupted only with brief respites. With the COVID-19 demand surge assisted by shortages in glass and DDICs, panel prices are spiking. Korean, Taiwanese, and Chinese panel makers are reporting robust margins in 1Q 2021 and the good news is anticipated for panel makers to get even better in 2Q.

Although multiple caveats remain about how both supply and demand will trend over the coming months, the modeled glut level is a leading indicator that the next cycle is now on its way, which implies falling prices, utilization, and profitability. Industry players should consider the implications when planning business strategies for the next 2 years.

Vicpas provide lcd display screen of worldwide brand, such as Hitach, Mitsubishi, sharp, NEC, Kyocera, BOE, ALPS. there also have many special lcd screen display for siemens, lcd display for AB Allen bradlay, lcd display for B&R powerpanel, lcd display for Beckhoff, lcd display for proface, lcd display for Schneider, lcd display for Kuka, lcd display for ABB, lcd display for KEBA, lcd display for YASKAWA, lcd display for KAWASAKI, lcd display for FUJI Hakko, lcd display for Beijer, lcd display for Bosch, lcd display for Cutler-Hammar, lcd display for Delta, lcd display for Hitech, lcd display for eview, weinview, weintech, lcd display for Eaton Microinnovation, lcd display for ESA, lcd display for Uniop, lcd display for EZ automation, lcd display for Fujistu, lcd display for keyence, lcd display for lenze, lcd display for lauer, lcd display for IDEC, lcd display for KOYO, lcd display for Omron, lcd display for Panasonic, lcd display for Parker, lcd display for Red lion.

The upstream materials or components of the LCD panel industry mainly include liquid crystal materials, glass substrates, polarizing lenses, and backlight LEDs (or CCFL, which accounts for less than 5% of the market).

The middle reaches is the main panel factory processing and manufacturing, through the glass substrate TFT arrays and CF substrate, CF as upper and TFT self-built perfusion liquid crystal and the lower joint, and then put a polaroid, connection driver IC and control circuit board, and a backlight module assembling, eventually forming the whole piece of LCD module. The downstream is a variety of fields of application terminal-based brand, assembly manufacturers. At present, the United States, Japan, and Germany mainly focus on upstream raw materials, while South Korea, Taiwan, and the mainland mainly seek development in mid-stream panel manufacturing.

With the successive production of the high generation line in mainland China, the panel production capacity and technology level have been steadily improved, and the industrial competitiveness has been gradually enhanced. Nowadays, the panel industry is divided into three parts: South Korea, mainland China, and Taiwan, and mainland China is expected to become the no.1 in the world in 2019.

In the past decade, China’s panel display industryhas achieved leapfrog development, and the overall size of the industry has ranked among the top three in the world. Chinese mainland panel production capacity is expanding rapidly, although Japanese panel manufacturers master a large number of key technologies, gradually lose the price competitive advantage, compression panel production capacity. Panel production is concentrated in South Korea, Taiwan, and China, which is poised to become the world’s largest producer of LCD panels.

Up to 2016, BOE‘s global market share continued to increase: smartphone LCD, tablet PC display, and laptop display accounted for the world’s first market share, and display screen increased to the world’s second, while TV LCD remained the world’s third. In LCD TV panels, Chinese panel makers have accounted for 30 percent of global shipments to 77 million units, surpassing Taiwan’s 25.5 percent market share for the first time and ranking second only to South Korea.

In terms of the area of shipment, the area of board shipment of JD accounted for only 8.3% in 2015, which has been greatly increased to 13.6% in the first half of 2016, while the area of shipment of hu xing optoelectronics in the first half of 2015 was only 5.1%, which has reached 7.8% in the first half of 2016. The panel factories in mainland China are expanding their capacity at an average rate of double-digit growth and transforming it into actual shipments and areas of shipment. On the other hand, although the market share of South Korea, Japan, and Taiwan is gradually decreasing, some South Korean and Japanese manufacturers have been inclined to the large-size HD panel and AMOLED market, and the production capacity of the high-end LCD panel is further concentrated in mainland China.

Domestic LCD panel production line capacity gradually released, overlay the decline in global economic growth, lead to panel makers from 15 in the second half began, in a low profit or loss, especially small and medium-sized production line, the South Korean manufacturers take the lead in transformation strategy, closed in medium and small size panel production line, South Korea’s 19-panel production line has shut down nine, and part of the production line is to research and development purposes. Some production lines are converted to LTPS production lines through process conversion. Korean manufacturers are turning to OLED panels in a comprehensive way, while Japanese manufacturers are basically giving up the LCD panel manufacturing business and turning to the core equipment and materials side. In addition to the technical direction of the research and judgment, more is the LCD panel business orders and profits have been severely compressed, Korean and Japanese manufacturers have no desire to fight. Since many OLED technologies are still in their infancy in mainland China, it is a priority to move to high-end panels such as OLED as soon as possible. Taiwanese manufacturers have not shut down factories on a large scale, but their advantages in LCD technology and OLED technology have been slowly eroded by the mainland.

STONE provides a full range of 3.5 inches to 15.1 inches of small and medium-size standard quasi TFT LCD module, LCD display, TFT display module, display industry, industrial LCD screen, under the sunlight visually highlight TFT LCD display, industrial custom TFT screen, TFT LCD screen-wide temperature, industrial TFT LCD screen, touch screen industry. The TFT LCD module is very suitable for industrial control equipment, medical instruments, POS system, electronic consumer products, vehicles, and other products.STONE provides a full range of 3.5 inches to 15.1 inches of small and medium-size standard quasi TFT LCD module, LCD display, TFT display module, display industry, industrial LCD screen, under the sunlight visually highlight TFT LCD display, industrial custom TFT screen, TFT LCD screen-wide temperature, industrial TFT LCD screen, touch screen industry. The TFT LCD module is very suitable for industrial control equipment, medical instruments, POS system, electronic consumer products, vehicles, and other products.

TFT is an LCD Technology which adds a thin-film transistor at each pixel to supply common voltages to all elements. This voltage improves video content frame rates. Displays are predominantly utilizing color filter layers and white LED backlighting.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey