lcd panel manufacturers market share factory

The upstream materials or components of the LCD panel industry mainly include liquid crystal materials, glass substrates, polarizing lenses, and backlight LEDs (or CCFL, which accounts for less than 5% of the market).

The middle reaches is the main panel factory processing and manufacturing, through the glass substrate TFT arrays and CF substrate, CF as upper and TFT self-built perfusion liquid crystal and the lower joint, and then put a polaroid, connection driver IC and control circuit board, and a backlight module assembling, eventually forming the whole piece of LCD module. The downstream is a variety of fields of application terminal-based brand, assembly manufacturers. At present, the United States, Japan, and Germany mainly focus on upstream raw materials, while South Korea, Taiwan, and the mainland mainly seek development in mid-stream panel manufacturing.

With the successive production of the high generation line in mainland China, the panel production capacity and technology level have been steadily improved, and the industrial competitiveness has been gradually enhanced. Nowadays, the panel industry is divided into three parts: South Korea, mainland China, and Taiwan, and mainland China is expected to become the no.1 in the world in 2019.

In the past decade, China’s panel display industryhas achieved leapfrog development, and the overall size of the industry has ranked among the top three in the world. Chinese mainland panel production capacity is expanding rapidly, although Japanese panel manufacturers master a large number of key technologies, gradually lose the price competitive advantage, compression panel production capacity. Panel production is concentrated in South Korea, Taiwan, and China, which is poised to become the world’s largest producer of LCD panels.

Up to 2016, BOE‘s global market share continued to increase: smartphone LCD, tablet PC display, and laptop display accounted for the world’s first market share, and display screen increased to the world’s second, while TV LCD remained the world’s third. In LCD TV panels, Chinese panel makers have accounted for 30 percent of global shipments to 77 million units, surpassing Taiwan’s 25.5 percent market share for the first time and ranking second only to South Korea.

In terms of the area of shipment, the area of board shipment of JD accounted for only 8.3% in 2015, which has been greatly increased to 13.6% in the first half of 2016, while the area of shipment of hu xing optoelectronics in the first half of 2015 was only 5.1%, which has reached 7.8% in the first half of 2016. The panel factories in mainland China are expanding their capacity at an average rate of double-digit growth and transforming it into actual shipments and areas of shipment. On the other hand, although the market share of South Korea, Japan, and Taiwan is gradually decreasing, some South Korean and Japanese manufacturers have been inclined to the large-size HD panel and AMOLED market, and the production capacity of the high-end LCD panel is further concentrated in mainland China.

Domestic LCD panel production line capacity gradually released, overlay the decline in global economic growth, lead to panel makers from 15 in the second half began, in a low profit or loss, especially small and medium-sized production line, the South Korean manufacturers take the lead in transformation strategy, closed in medium and small size panel production line, South Korea’s 19-panel production line has shut down nine, and part of the production line is to research and development purposes. Some production lines are converted to LTPS production lines through process conversion. Korean manufacturers are turning to OLED panels in a comprehensive way, while Japanese manufacturers are basically giving up the LCD panel manufacturing business and turning to the core equipment and materials side. In addition to the technical direction of the research and judgment, more is the LCD panel business orders and profits have been severely compressed, Korean and Japanese manufacturers have no desire to fight. Since many OLED technologies are still in their infancy in mainland China, it is a priority to move to high-end panels such as OLED as soon as possible. Taiwanese manufacturers have not shut down factories on a large scale, but their advantages in LCD technology and OLED technology have been slowly eroded by the mainland.

STONE provides a full range of 3.5 inches to 15.1 inches of small and medium-size standard quasi TFT LCD module, LCD display, TFT display module, display industry, industrial LCD screen, under the sunlight visually highlight TFT LCD display, industrial custom TFT screen, TFT LCD screen-wide temperature, industrial TFT LCD screen, touch screen industry. The TFT LCD module is very suitable for industrial control equipment, medical instruments, POS system, electronic consumer products, vehicles, and other products.STONE provides a full range of 3.5 inches to 15.1 inches of small and medium-size standard quasi TFT LCD module, LCD display, TFT display module, display industry, industrial LCD screen, under the sunlight visually highlight TFT LCD display, industrial custom TFT screen, TFT LCD screen-wide temperature, industrial TFT LCD screen, touch screen industry. The TFT LCD module is very suitable for industrial control equipment, medical instruments, POS system, electronic consumer products, vehicles, and other products.

August 2, according to the Taiwan media “Economic Daily News” reported that the latest report of the research agency RUNTO (RUNTO) shows that the first half of 2022 Chinese mainland panel manufacturers to 84 million shipments as well as 67% market share claimed the title, a record high. Taiwan panel makers Guntron, AUO shipments have declined, a combined market share of 18%, slightly better than Japan and South Korea’s combined 15%. Market expectations, with the mainland domination of the LCD panel market, the next three years, the panel factory is afraid of a merger tide.

According to the “Global LCD TV panel market monthly tracking” released by LOTUS, the first half of this year, the world shipped 125 million LCD TV panels above 32 inches, an increase of 1.9% year-on-year, with mainland manufacturers BOE, Huaxing Optoelectronics and Huike firmly in the top three.

To strengthen the core position of the industry chain, the Chinese mainland TV panel factory to maintain a high crop rate, shipments in the first half of 84 million pieces, the global market share of 67%, an increase of 6.2 percentage points, compared with the second half of last year, an increase of 3.4 percentage points.

The top ten panel manufacturers in the analysis of the Luotu technology, land-based panel factory shipments are showing year-on-year growth, Huaxing photoelectric, rainbow photoelectric shipments were up 12% and 16%. Most of the non-China panel factory decline, Taiwan panel factory Grouptron decline by about 10%, AUO reduced by 14%, the two combined market share of 18% in the first half.

Samsung Display (SDC) began to gradually reduce production at the beginning of the year to a complete shutdown in June, resulting in a year-on-year reduction of 50%. Sharp because of the active adjustment of production capacity, production decreased by 28% year-on-year, Japan and South Korea panel factories in the first half of the combined market share fell to a low of 15%.

Accordingly, the top ten panel makers are divided into four camps, with BOE, which shipped more than 30 million pieces in the first half of the year, firmly taking the lead in the large-size LCD panel industry. Next, 20 million pieces of Huaxing photoelectric, Huike. 10 million pieces of camp for the grouptron and Lejin display (LGD). Million-chip rank AUO and Sharp, with 8 million and 6 million pieces shipped, fell to the tail camp with Rainbow Photoelectric, CEC Panda and Samsung Display SDC.

Looking ahead to the second half of the year, Luotu Technology expects that, as the TV panel each main size has fallen below the cash cost, the panel factory strives to stop bleeding, start large-scale production reduction operations, the panel market is expected to usher in a turnaround. It is expected that before September this year, the major panel factory crop rate will be less than 75%, as to whether the price can stabilize the key observation point also falls in September.

BOE Technology Group, the Chinese electronic components producer, is expected to be the leader in producing LCD display panels in the coming years, with a forecast capacity share of 24 percent by 2022. China is the country that has the largest LCD capacity, with a 56 percent share in 2020.Read moreLCD panel production capacity share from 2016 to 2022, by manufacturerCharacteristicBOEChina StarInnoluxAUOLGDHKCCEC PandaSharpSDCOther-----------

DSCC. (June 8, 2020). LCD panel production capacity share from 2016 to 2022, by manufacturer [Graph]. In Statista. Retrieved January 02, 2023, from https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. "LCD panel production capacity share from 2016 to 2022, by manufacturer." Chart. June 8, 2020. Statista. Accessed January 02, 2023. https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. (2020). LCD panel production capacity share from 2016 to 2022, by manufacturer. Statista. Statista Inc.. Accessed: January 02, 2023. https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. "Lcd Panel Production Capacity Share from 2016 to 2022, by Manufacturer." Statista, Statista Inc., 8 Jun 2020, https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC, LCD panel production capacity share from 2016 to 2022, by manufacturer Statista, https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/ (last visited January 02, 2023)

China is the leader in producing LCD display panels, with a forecast capacity share of 56 percent in 2020. China"s share is expected to increase in the coming years, stabilizing at 69 percent from 2023 onwards.Read moreLCD panel production capacity share from 2016 to 2025, by countryCharacteristicChinaJapanSouth KoreaTaiwan-----

DSCC. (June 8, 2020). LCD panel production capacity share from 2016 to 2025, by country [Graph]. In Statista. Retrieved January 02, 2023, from https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. "LCD panel production capacity share from 2016 to 2025, by country." Chart. June 8, 2020. Statista. Accessed January 02, 2023. https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. (2020). LCD panel production capacity share from 2016 to 2025, by country. Statista. Statista Inc.. Accessed: January 02, 2023. https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. "Lcd Panel Production Capacity Share from 2016 to 2025, by Country." Statista, Statista Inc., 8 Jun 2020, https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC, LCD panel production capacity share from 2016 to 2025, by country Statista, https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/ (last visited January 02, 2023)

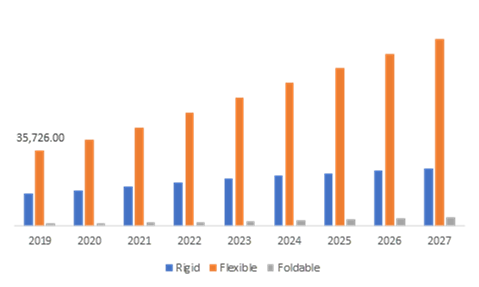

According to IMARC Group’s latest report, titled “TFT LCD Panel Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2022-2027”, the global TFT LCD panel market size reached US$ 157 Billion in 2021. Looking forward, IMARC Group expects the market to reach US$ 207.6 Billion by 2027, exhibiting a growth rate (CAGR) of 4.7% during 2022-2027.

A thin-film-transistor liquid-crystal display (TFT LCD) panel is a liquid crystal display that is generally attached to a thin film transistor. It is an energy-efficient product variant that offers a superior quality viewing experience without straining the eye. Additionally, it is lightweight, less prone to reflection and provides a wider viewing angle and sharp images. Consequently, it is generally utilized in the manufacturing of numerous electronic and handheld devices. Some of the commonly available TFT LCD panels in the market include twisted nematic, in-plane switching, advanced fringe field switching, patterned vertical alignment and an advanced super view.

We are regularly tracking the direct effect of COVID-19 on the market, along with the indirect influence of associated industries. These observations will be integrated into the report.

The global market is primarily driven by continual technological advancements in the display technology. This is supported by the introduction of plasma enhanced chemical vapor deposition (PECVD) technology to manufacture TFT panels that offers uniform thickness and cracking resistance to the product. Along with this, the widespread adoption of the TFT LCD panels in the production of automobiles dashboards that provide high resolution and reliability to the driver is gaining prominence across the globe. Furthermore, the increasing demand for compact-sized display panels and 4K television variants are contributing to the market growth. Moreover, the rising penetration of electronic devices, such as smartphones, tablets and laptops among the masses, is creating a positive outlook for the market. Other factors, including inflating disposable incomes of the masses, changing lifestyle patterns, and increasing investments in research and development (R&D) activities, are further projected to drive the market growth.

The competitive landscape of the TFT LCD panel market has been studied in the report with the detailed profiles of the key players operating in the market.

IMARC Group is a leading market research company that offers management strategy and market research worldwide. We partner with clients in all sectors and regions to identify their highest-value opportunities, address their most critical challenges, and transform their businesses.

IMARC’s information products include major market, scientific, economic and technological developments for business leaders in pharmaceutical, industrial, and high technology organizations. Market forecasts and industry analysis for biotechnology, advanced materials, pharmaceuticals, food and beverage, travel and tourism, nanotechnology and novel processing methods are at the top of the company’s expertise.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

The global TFT-LCD display panel market attained a value of USD 181.67 billion in 2022. It is expected to grow further in the forecast period of 2023-2028 with a CAGR of 5.2% and is projected to reach a value of USD 246.25 billion by 2028.

The current global TFT-LCD display panel market is driven by the increasing demand for flat panel TVs, good quality smartphones, tablets, and vehicle monitoring systems along with the growing gaming industry. The global display market is dominated by the flat panel display with TFT-LCD display panel being the most popular flat panel type and is being driven by strong demand from emerging economies, especially those in Asia Pacific like India, China, Korea, and Taiwan, among others. The rising demand for consumer electronics like LCD TVs, PCs, laptops, SLR cameras, navigation equipment and others have been aiding the growth of the industry.

TFT-LCD display panel is a type of liquid crystal display where each pixel is attached to a thin film transistor. Since the early 2000s, all LCD computer screens are TFT as they have a better response time and improved colour quality. With favourable properties like being light weight, slim, high in resolution and low in power consumption, they are in high demand in almost all sectors where displays are needed. Even with their larger dimensions, TFT-LCD display panel are more feasible as they can be viewed from a wider angle, are not susceptible to reflection and are lighter weight than traditional CRT TVs.

The global TFT-LCD display panel market is being driven by the growing household demand for average and large-sized flat panel TVs as well as a growing demand for slim, high-resolution smart phones with large screens. The rising demand for portable and small-sized tablets in the educational and commercial sectors has also been aiding the TFT-LCD display panel market growth. Increasing demand for automotive displays, a growing gaming industry and the emerging popularity of 3D cinema, are all major drivers for the market. Despite the concerns about an over-supply in the market, the shipments of large TFT-LCD display panel again rose in 2020.

North America is the largest market for TFT-LCD display panel, with over one-third of the global share. It is followed closely by the Asia-Pacific region, where countries like India, China, Korea, and Taiwan are significant emerging market for TFT-LCD display panels. China and India are among the fastest growing markets in the region. The growth of the demand in these regions have been assisted by the growth in their economy, a rise in disposable incomes and an increasing demand for consumer electronics.

The report gives a detailed analysis of the following key players in the global TFT-LCD display panel Market, covering their competitive landscape, capacity, and latest developments like mergers, acquisitions, and investments, expansions of capacity, and plant turnarounds:

*At Expert Market Research, we strive to always give you current and accurate information. The numbers depicted in the description are indicative and may differ from the actual numbers in the final EMR report.

Flat-panel displays are thin panels of glass or plastic used for electronically displaying text, images, or video. Liquid crystal displays (LCD), OLED (organic light emitting diode) and microLED displays are not quite the same; since LCD uses a liquid crystal that reacts to an electric current blocking light or allowing it to pass through the panel, whereas OLED/microLED displays consist of electroluminescent organic/inorganic materials that generate light when a current is passed through the material. LCD, OLED and microLED displays are driven using LTPS, IGZO, LTPO, and A-Si TFT transistor technologies as their backplane using ITO to supply current to the transistors and in turn to the liquid crystal or electroluminescent material. Segment and passive OLED and LCD displays do not use a backplane but use indium tin oxide (ITO), a transparent conductive material, to pass current to the electroluminescent material or liquid crystal. In LCDs, there is an even layer of liquid crystal throughout the panel whereas an OLED display has the electroluminescent material only where it is meant to light up. OLEDs, LCDs and microLEDs can be made flexible and transparent, but LCDs require a backlight because they cannot emit light on their own like OLEDs and microLEDs.

Liquid-crystal display (or LCD) is a thin, flat panel used for electronically displaying information such as text, images, and moving pictures. They are usually made of glass but they can also be made out of plastic. Some manufacturers make transparent LCD panels and special sequential color segment LCDs that have higher than usual refresh rates and an RGB backlight. The backlight is synchronized with the display so that the colors will show up as needed. The list of LCD manufacturers:

Organic light emitting diode (or OLED displays) is a thin, flat panel made of glass or plastic used for electronically displaying information such as text, images, and moving pictures. OLED panels can also take the shape of a light panel, where red, green and blue light emitting materials are stacked to create a white light panel. OLED displays can also be made transparent and/or flexible and these transparent panels are available on the market and are widely used in smartphones with under-display optical fingerprint sensors. LCD and OLED displays are available in different shapes, the most prominent of which is a circular display, which is used in smartwatches. The list of OLED display manufacturers:

MicroLED displays is an emerging flat-panel display technology consisting of arrays of microscopic LEDs forming the individual pixel elements. Like OLED, microLED offers infinite contrast ratio, but unlike OLED, microLED is immune to screen burn-in, and consumes less power while having higher light output, as it uses LEDs instead of organic electroluminescent materials, The list of MicroLED display manufacturers:

LCDs are made in a glass substrate. For OLED, the substrate can also be plastic. The size of the substrates are specified in generations, with each generation using a larger substrate. For example, a 4th generation substrate is larger in size than a 3rd generation substrate. A larger substrate allows for more panels to be cut from a single substrate, or for larger panels to be made, akin to increasing wafer sizes in the semiconductor industry.

"Samsung Display has halted local Gen-8 LCD lines: sources". THE ELEC, Korea Electronics Industry Media. August 16, 2019. Archived from the original on April 3, 2020. Retrieved December 18, 2019.

"TCL to Build World"s Largest Gen 11 LCD Panel Factory". www.businesswire.com. May 19, 2016. Archived from the original on April 2, 2018. Retrieved April 1, 2018.

"Panel Manufacturers Start to Operate Their New 8th Generation LCD Lines". 대한민국 IT포털의 중심! 이티뉴스. June 19, 2017. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"TCL"s Panel Manufacturer CSOT Commences Production of High Generation Panel Modules". www.businesswire.com. June 14, 2018. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"Samsung Display Considering Halting Some LCD Production Lines". 비즈니스코리아 - BusinessKorea. August 16, 2019. Archived from the original on April 5, 2020. Retrieved December 19, 2019.

Herald, The Korea (July 6, 2016). "Samsung Display accelerates transition from LCD to OLED". www.koreaherald.com. Archived from the original on April 1, 2018. Retrieved April 1, 2018.

"China"s BOE to have world"s largest TFT-LCD+AMOLED capacity in 2019". ihsmarkit.com. 2017-03-22. Archived from the original on 2019-08-16. Retrieved 2019-08-17.

LCDs find application in a wide range of devices such as smartphones, notebooks, televisions, curved TVs, tablets, digital signage and offer various other benefits with regard to performance and lightweight properties. These displays have higher resolution and more portable than traditional televisions and monitors ; they can produce high-quality digital images.

Prior to the Covid-19 pandemic outbreak in early 2020, the flat-panel display (FPD) market was gloomy. Oversupply, falling prices and losses were the common themes in the market.

It’s been a different story during the outbreak. In 2020, the FPD market rebounded. In the stay-at-home economy, consumers went on a buying spree for monitors, PCs, tablets and TVs. As a result, demand for displays exploded. And shortages soon surfaced for display driver ICs and other components.

2021 is expected to be another boom year, but the party may be over in 2022. The global flat panel display market is expected to jump 28% in 2021 to reach a record high of $ 151 billion. A performance drawn more by old LCD screens (liquid crystal display) than Oled screens.

In 2019 State-backed Chinese manufacturer BOE Technology Group has outstripped South Korea’s LG Display as the top maker of flat-panel displays this year, marking China’s growing dominance in the field. In 2021, another Chinese, CSOT, will climb to second place according to DSCC, and in 2024, a third Chinese, HKC, will climb to the third step of the podium.

Increasing use of flat panel display in healthcare industry is creating opportunities for manufacturers as the demand for high-pixel density display for diagnostic in healthcare is increasing. The demand is increasing for new surgical platforms that consists of ultra-high level of brightness to avoid glare and reflection in high light environment so there are opportunities for manufacturers to develop these platforms.

– Screen coating to protect the screen against scratches, touch, reflection, … this coating is applied to the substrate in liquid form and then cured in large oven. One problem with preferred coating compositions is that the temperature can not be tolerated by the glass substrate of the screen panel. For example one protective coating composition cures at about 800°C and the maximum temperature the glass substrate can withstand is about 550°C before it brings thermal damage. To compensate, the protective coating is “cured” in an oven set at a temperature lower than specified but for an extremely long period of time.

As the display mother glass area gets bigger and bigger,so does the equipment used in the display manufacturing process and the volume of gases required. In addition, the consumer’s desire for a better viewing experience such as more vivid color, higher resolution, and lower power consumption has also driven display manufacturers to develop and commercialize active matrix organic light emitting displays (AMOLED).

In general, there are two types of displays in the market today: active matrix liquid crystal display (AMLCD) and AMOLED. In its simplicity, the fundamental components required to make up the display are the same for AMLCD and AMOLED. There are four layers of a display device (FIGURE 1): a light source, switches that are the thin-film-transistor and where the gases are mainly used, a shutter to control the color selection, and the RGB (red, green, blue) color filter.

Technology trends TFT-LCD (thin-film-transistor liquid-crystal display) is the baseline technology. MO / White OLED (organic light emitting diode) is used for larger screens. LTPS / AMOLED is used for small / medium screens. The challenges for OLED are the effect of < 1 micron particles on yield, much higher cost compared to a-Si due to increased mask steps, and moisture impact to yield for the OLED step.

Although AMLCD displays are still dominant in the market today, AMOLED displays are growing quickly. Currently about 25% of smartphones are made with AMOLED displays and this is expected to grow to ~40% by 2021. OLED televisions are also growing rapidly, enjoying double digit growth rate year over year. Based on IHS data, the revenue for display panels with AMOLED technol- ogies is expected to have a CAGR of 18.9% in the next five years while the AMLCD display revenue will have a -2.8% CAGR for the same period with the total display panel revenue CAGR of 2.5%. With the rapid growth of AMOLED display panels, the panel makers have accel- erated their investment in the equipment to produce AMOLED panels.

There are three types of thin-film-transistor devices for display: amorphous silicon (a-Si), low temperature polysilicon (LTPS), and metal oxide (MO), also known as transparent amorphous oxide semiconductor (TAOS). AMLCD panels typically use a-Si for lower-resolution displays and TVs while high-resolution displays use LTPS transistors, but this use is mainly limited to small and medium displays due to its higher costs and scalability limitations. AMOLED panels use LTPS and MO transistors where MO devices are typically used for TV and large displays (FIGURE 3).

This shift in technology also requires a change in the gases used in production of AMOLED panels as compared with the AMLCD panels. As shown in FIGURE 4, display manufacturing today uses a wide variety of gases.

Nitrogen trifluoride: NF3 is the single largest electronic material from spend and volume standpoint for a-Si and LTPS display production while being surpassed by N2O for MO production. NF3 is used for cleaning the PECVD chambers. This gas requires scalability to get the cost advantage necessary for the highly competitive market.

Helium: H2 is used for cooling the glass during and after processing. Manufacturers are looking at ways to decrease the usage of helium because of cost and availability issues due it being a non-renewable gas.

To facilitate these increasing demands, display manufacturers must partner with gas suppliers to identify which can meet their technology needs, globally source electronic materials to provide customers with stable and cost- effective gas solutions, develop local sources of electronic materials, improve productivity, reduce carbon footprint, and increase energy efficiency through on-site gas plants. This is particularly true for the burgeoning China display manufacturing market, which will benefit from investing in on-site bulk gas plants and collaboration with global materials suppliers with local production facilities for high-purity gas and chemical manufacturing.

Panel manufacturers in the Chinese mainland ranked first with 84 million shipments and a 67% global market share a record high in the first half of 2022, according to the latest report of research agency RUNTO Technology.

The panel makers Innolux and AUO saw their shipments decline, with a combined market share of 18%, slightly higher than Japan and South Korea’s combined total of 15%, said RUNTO as reported by the Taiwan region"s Economic Daily. The market expects that panel makers are likely to set off a wave of mergers in the next three years.

The RUNTO’s “Monthly Tracker of the Global LCD TV Panel Market” said that in the first half of this year, the global shipments of LCD TV panels larger than 32 inches was 125 million, with manufacturers BOE(京东方), TCL CSOT(华星光电), and HKC(惠科) from the Chinese mainland in the top three positions.

The report gave four categories of the top ten manufacturers based on their shipments, where BOE ranks the first with more than 30 million shipments, TCL CSOT and HKC with more than 20 million shipments, Innolux and LG Display (LGD) with ten million shipments, and AUO(8 million), Sharp(6 million), and other three with less than 10 million shipments.

The report expects that before September this year, the utilization rate of major panel factories will be lower than 75% because main sizes of TV panels have fallen below the cash cost, and panel factories have started mass production cuts.

The global semiconductor market size was USD 527.88 billion in 2021. The market is projected to grow from USD 573.44 billion in 2022 to USD 1,380.79 billion in 2029, exhibiting a CAGR of 12.2% during the forecast period. The global COVID-19 pandemic has been unprecedented and staggering, with semiconductors experiencing a positive demand across all regions compared to pre-pandemic levels. Based on our analysis, the global semiconductor market exhibited a rise of 6.8% in 2020 compared to 2019.

The growth of this market is attributed to the increasing consumption of consumer electronics devices across the globe. Additionally, the emergence of artificial intelligence (AI), the Internet of Things (IoT), and machine learning (ML) technologies is providing new opportunities for market development. These technologies aid memory chips in processing large amounts of data in less time. Moreover, the increasing demand for faster and advanced memory chips in industrial applications will drive market growth over the forecast timeline.

The sudden outbreak of COVID-19 in Wuhan, China, which is also known as the “motor city,” has severely impacted automotive production in Asia, as it is the home to auto plants of General Motors, Honda, Nissan, Peugeot Group (PSA), Renault, and Toyota. The United Nations Conference on Trade and Development (UNCTAD) has estimated a 2% reduction in the export of automotive parts from China to other automotive manufacturers in the European Union (EU). Similarly, the U.S., South Korea, Japan, and many more could lead to automotive export reduction worth USD 7 billion from these economies to the rest of the world.

However, the rising need to work from home has drastically surged networking & communication, and data processing applications worldwide will lead to the moderate growth of the market for semiconductors in the long term.

Rising household disposable income levels, rapidly growing population, and increasing urbanization create massive demand for regular and advanced consumer electronics devices. Integrated Circuit (ICs) chips are present in several electronic devices, including smartphones, washing machines, TVs, and refrigerators for efficient and appropriate functioning. Several leading consumer electronics brands, including Samsung, Apple, and Huawei are making large investments in introducing new devices to cater to the increasing consumer demand for advanced devices, supporting the market growth.

China is expected to witness strong demand for mobile chips due to established manufacturing and assembling plants of several well-known smartphone manufacturers such as Apple and OnePlus. Moreover, Taiwan’s industry depicts significant growth, reflected by the number of Taiwanese personal computer manufacturers and their increasing investments in the research and development sector. The country is also renowned for manufacturing advanced technology-driven and compact integrated circuits, thus creating lucrative growth prospects for the market.

The industry is enormously dependent on the U.S. as it has been a prominent country holding a dominant share in the market. With changes in the country’s leadership, the U.S. has started to impose trade restrictions with China from 2018, and if the restrictions continue, the country is expected to suffer ~16% decrease in its market share. Therefore, the increasing tension with China is expected to diminish the dominance of the U.S. semiconductor market, and the focus is anticipated to shift to Asia Pacific in the coming years.

Memory devices are expected to drive overall market growth due to ongoing technological advancements such as virtual reality and cloud computing and their integration in end-user devices. The high average selling price for NAND flash chips and DRAM would generate revenue.

The microprocessors (MPU) and microcontroller (MCU) segments would depict stagnant growth owing to frail shipments and investments for notebook PCs, computers, and standard desktops. In the current market scenario, the increasing popularity of IoT-based electronics is stoking the demand for powerful processors and controllers. Hybrid MPU and MCU offer real-time embedded processing and control for the topmost IoT-based applications, thus leading to substantial market growth.

Based on application, the market can be broken down into networking & communications, data processing, industrial, consumer electronics, automotive, and government.

The data processing application segment holds a considerable semiconductor market share owing to the strong need and sales of smartphones and other connected devices, accelerating the demand for memory and storage devices.

Consumer electronics, such as gaming consoles, wearable devices, and other electronic devices, play an important role in this market, enabling the usage of electronic gaming across various countries.

The automotive application segment is estimated to witness a moderate growth rate due to the limited penetration rate of hybrid and electric vehicles. However, the market potential may be enhanced with promising autonomous driving advancements.

Asia Pacific holds the largest share and is projected to exhibit the highest growth in the market across the globe. The increasing adoption of high-end technology-based devices, coupled with the minimum electronics prices, is leading to an upswing in the consumption of consumer electronics. Additionally, technological advancements, such as IoT and LTE, support electronics products, thereby allowing the region to dominate the market share.

China holds the largest share in the global market and is projected to witness a moderate CAGR in the upcoming years, owing to the surging presence of local semiconductor component manufacturers. These local market players tend toward offering a wide range of products at discounted rates in bulk quantity. Thus, it would augment the market growth in China over the forecast period.

The North America market is estimated to exhibit dynamic growth driven by increasing investments in R&D activities. According to the Semiconductor Industry Association (SIA), the U.S. industry’s expenditures in R&D increased at a compound annual growth rate of about 6.6 percent from 1999 to 2019. Expenditures in R&D activities by U.S. companies tend to be consistently high, regardless of cycles in annual sales, which reflects the importance of investing in R&D production. In 2019, the R&D investments totaled USD 39.8 billion.

The market in Europe will witness substantial growth backed by the telecom and the automotive industry. Companies across the region are investing in innovating new technologies and increasing their production capacities to cater to the surging demand for advanced devices and components in the semiconductor industry. Moreover, the rising consumption of consumer goods across the U.K., France, and Germany will support the growth of this industry in Europe over the forecast timeline.

The availability of skilled labor forces and rapid innovations in technologies will drive the Middle East & Africa semiconductor industry growth. Increasing demand for advanced industrial electronics and high-end computing technologies is expected to propel the regional market growth over the forecast timeline.

Furthermore, the Latin America market will witness healthy growth, owing to increasing consumption of smartphones, TVs, and laptops across Brazil and Mexico. Consumers across the region are making investments in purchasing high-end electronic devices, owing to their steadily rising disposable income levels.

The report offers an in-depth analysis and further provides details on the product adoption across several regions. Information on trends, drivers, opportunities, threats, and market restraints can further help stakeholders gain valuable insights. The report offers a detailed competitive landscape by presenting information on key players, along with their strategies, in the market.

SHANGHAI - China"s BOE Technology Group, one of the world"s largest display manufacturers, plans to build a massive new factory in Beijing, as it looks to next-generation technology for new revenue streams.

BOE will invest 29 billion yuan ($4 billion) in the 600,000 sq. meter factory, according to Sunday"s announcement, with an eye toward expanding into markets for new technologies, such as panels for virtual reality (VR) devices, and a new type of high-end panel called mini-LED.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey