lcd panel manufacturers market share made in china

China is the leader in producing LCD display panels, with a forecast capacity share of 56 percent in 2020. China"s share is expected to increase in the coming years, stabilizing at 69 percent from 2023 onwards.Read moreLCD panel production capacity share from 2016 to 2025, by countryCharacteristicChinaJapanSouth KoreaTaiwan-----

DSCC. (June 8, 2020). LCD panel production capacity share from 2016 to 2025, by country [Graph]. In Statista. Retrieved January 02, 2023, from https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. "LCD panel production capacity share from 2016 to 2025, by country." Chart. June 8, 2020. Statista. Accessed January 02, 2023. https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. (2020). LCD panel production capacity share from 2016 to 2025, by country. Statista. Statista Inc.. Accessed: January 02, 2023. https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. "Lcd Panel Production Capacity Share from 2016 to 2025, by Country." Statista, Statista Inc., 8 Jun 2020, https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC, LCD panel production capacity share from 2016 to 2025, by country Statista, https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/ (last visited January 02, 2023)

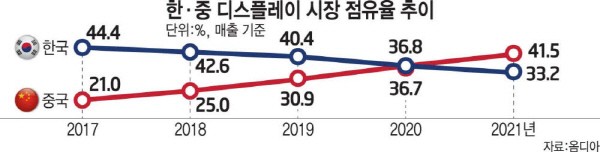

It is the first time that China took over the No. 1 spot in the display market, which Korea has always been a leader in. The title of “the strongest country in display market” is lost after 17 years. It would not be possible to reclaim the No. 1 spot if Korea cannot find a way to expand investment in next-generation displays such as organic light emitting diodes (OLED).

According to market research firm Omdia, China recorded $64.8 billion in sales including LCD and OLED in the global display market last year. China took over Korea’s No. 1 spot with a market share of 41.5%. Korea"s market share fell 8.3 points (p) to 33.2%. This is the first time since 2004, in 17 years, that Korea had to hand over the No. 1 spot. Korea had a 9.4 p advantage in market share over China up until 2019.

China overtook Korea and seized power in the LCD market by offering a low-priced products. BOE, China"s largest panel manufacturer, has become the world"s largest LCD manufacturer with help of the subsidy from the Chinese government. LCD sales was $28.6 billion last year, accounting for 26.3% of the total LCD market. The sales of Chinese companies such as BOE, CSOT, Tianma, and Visionox increased significantly as demand for TV and information technology (IT) devices increased with the prolonged COVID 19 and increased price of LCD panel.

After taken over in the LCD market, Korea is focusing on the highly-valued OLED market. Samsung Display and LG Display are transforming their LCD production lines to OLED. Korea is the No. 1 with 82.3% of the global OLED market shares according to Omdia, and China’s market share only accounts for16.6%.

China"s dominance is expected to continue for some time because the large display market such as TVs and laptops still depends on LCD. Only when Korea starts to reduce OLED panel prices by mass producing OLED, then Korea can replace the LCD market led by China.

China has also started to narrow the gap with Korea in OLED industry. BOE and other companies have commercialized OLED for small and medium-sized displays such as mobile, laptop, and tablet. Following LCD market, China is threatening Korea in OLED market as well as China expands OLED market share mainly in the Chinese smartphone market.

Critics are pointing out that Korea needs to expand in OLED market and develop new technologies in order to maintain the OLED gap with China. Korea must take control over the large TV panel market, which has a large technological gap with China, and create a new form factor with new technologies such as flexible, rollable, and bendable panels.

An official from the display industry said, “With the government-led industrial promotion policy and copious domestic market, China is making an effort to solidify its leading position in the display industry. There is a neglect on display industry in Korea since the display promotion policy is almost non-existent compared to semiconductors and batteries.”

August 2, according to the Taiwan media “Economic Daily News” reported that the latest report of the research agency RUNTO (RUNTO) shows that the first half of 2022 Chinese mainland panel manufacturers to 84 million shipments as well as 67% market share claimed the title, a record high. Taiwan panel makers Guntron, AUO shipments have declined, a combined market share of 18%, slightly better than Japan and South Korea’s combined 15%. Market expectations, with the mainland domination of the LCD panel market, the next three years, the panel factory is afraid of a merger tide.

According to the “Global LCD TV panel market monthly tracking” released by LOTUS, the first half of this year, the world shipped 125 million LCD TV panels above 32 inches, an increase of 1.9% year-on-year, with mainland manufacturers BOE, Huaxing Optoelectronics and Huike firmly in the top three.

To strengthen the core position of the industry chain, the Chinese mainland TV panel factory to maintain a high crop rate, shipments in the first half of 84 million pieces, the global market share of 67%, an increase of 6.2 percentage points, compared with the second half of last year, an increase of 3.4 percentage points.

The top ten panel manufacturers in the analysis of the Luotu technology, land-based panel factory shipments are showing year-on-year growth, Huaxing photoelectric, rainbow photoelectric shipments were up 12% and 16%. Most of the non-China panel factory decline, Taiwan panel factory Grouptron decline by about 10%, AUO reduced by 14%, the two combined market share of 18% in the first half.

Samsung Display (SDC) began to gradually reduce production at the beginning of the year to a complete shutdown in June, resulting in a year-on-year reduction of 50%. Sharp because of the active adjustment of production capacity, production decreased by 28% year-on-year, Japan and South Korea panel factories in the first half of the combined market share fell to a low of 15%.

Accordingly, the top ten panel makers are divided into four camps, with BOE, which shipped more than 30 million pieces in the first half of the year, firmly taking the lead in the large-size LCD panel industry. Next, 20 million pieces of Huaxing photoelectric, Huike. 10 million pieces of camp for the grouptron and Lejin display (LGD). Million-chip rank AUO and Sharp, with 8 million and 6 million pieces shipped, fell to the tail camp with Rainbow Photoelectric, CEC Panda and Samsung Display SDC.

Looking ahead to the second half of the year, Luotu Technology expects that, as the TV panel each main size has fallen below the cash cost, the panel factory strives to stop bleeding, start large-scale production reduction operations, the panel market is expected to usher in a turnaround. It is expected that before September this year, the major panel factory crop rate will be less than 75%, as to whether the price can stabilize the key observation point also falls in September.

In recent time, China domestic companies like BOE have overtaken LCD manufacturers from Korea and Japan. For the first three quarters of 2020, China LCD companies shipped 97.01 million square meters TFT LCD. And China"s LCD display manufacturers expect to grab 70% global LCD panel shipments very soon.

BOE started LCD manufacturing in 1994, and has grown into the largest LCD manufacturers in the world. Who has the 1st generation 10.5 TFT LCD production line. BOE"s LCD products are widely used in areas like TV, monitor, mobile phone, laptop computer etc.

TianMa Microelectronics is a professional LCD and LCM manufacturer. The company owns generation 4.5 TFT LCD production lines, mainly focuses on making medium to small size LCD product. TianMa works on consult, design and manufacturing of LCD display. Its LCDs are used in medical, instrument, telecommunication and auto industries.

TCL CSOT (TCL China Star Optoelectronics Technology Co., Ltd), established in November, 2009. TCL has six LCD panel production lines commissioned, providing panels and modules for TV and mobile products. The products range from large, small & medium display panel and touch modules.

Established in 1996, Topway is a high-tech enterprise specializing in the design and manufacturing of industrial LCD module. Topway"s TFT LCD displays are known worldwide for their flexible use, reliable quality and reliable support. More than 20 years expertise coupled with longevity of LCD modules make Topway a trustworthy partner for decades. CMRC (market research institution belonged to Statistics China before) named Topway one of the top 10 LCD manufactures in China.

The Company engages in the R&D, manufacturing, and sale of LCD panels. It offers LCD panels for notebook computers, desktop computer monitors, LCD TV sets, vehicle-mounted IPC, consumer electronics products, mobile devices, tablet PCs, desktop PCs, and industrial displays.

The upstream materials or components of the LCD panel industry mainly include liquid crystal materials, glass substrates, polarizing lenses, and backlight LEDs (or CCFL, which accounts for less than 5% of the market).

The middle reaches is the main panel factory processing and manufacturing, through the glass substrate TFT arrays and CF substrate, CF as upper and TFT self-built perfusion liquid crystal and the lower joint, and then put a polaroid, connection driver IC and control circuit board, and a backlight module assembling, eventually forming the whole piece of LCD module. The downstream is a variety of fields of application terminal-based brand, assembly manufacturers. At present, the United States, Japan, and Germany mainly focus on upstream raw materials, while South Korea, Taiwan, and the mainland mainly seek development in mid-stream panel manufacturing.

With the successive production of the high generation line in mainland China, the panel production capacity and technology level have been steadily improved, and the industrial competitiveness has been gradually enhanced. Nowadays, the panel industry is divided into three parts: South Korea, mainland China, and Taiwan, and mainland China is expected to become the no.1 in the world in 2019.

In the past decade, China’s panel display industryhas achieved leapfrog development, and the overall size of the industry has ranked among the top three in the world. Chinese mainland panel production capacity is expanding rapidly, although Japanese panel manufacturers master a large number of key technologies, gradually lose the price competitive advantage, compression panel production capacity. Panel production is concentrated in South Korea, Taiwan, and China, which is poised to become the world’s largest producer of LCD panels.

Up to 2016, BOE‘s global market share continued to increase: smartphone LCD, tablet PC display, and laptop display accounted for the world’s first market share, and display screen increased to the world’s second, while TV LCD remained the world’s third. In LCD TV panels, Chinese panel makers have accounted for 30 percent of global shipments to 77 million units, surpassing Taiwan’s 25.5 percent market share for the first time and ranking second only to South Korea.

In terms of the area of shipment, the area of board shipment of JD accounted for only 8.3% in 2015, which has been greatly increased to 13.6% in the first half of 2016, while the area of shipment of hu xing optoelectronics in the first half of 2015 was only 5.1%, which has reached 7.8% in the first half of 2016. The panel factories in mainland China are expanding their capacity at an average rate of double-digit growth and transforming it into actual shipments and areas of shipment. On the other hand, although the market share of South Korea, Japan, and Taiwan is gradually decreasing, some South Korean and Japanese manufacturers have been inclined to the large-size HD panel and AMOLED market, and the production capacity of the high-end LCD panel is further concentrated in mainland China.

Domestic LCD panel production line capacity gradually released, overlay the decline in global economic growth, lead to panel makers from 15 in the second half began, in a low profit or loss, especially small and medium-sized production line, the South Korean manufacturers take the lead in transformation strategy, closed in medium and small size panel production line, South Korea’s 19-panel production line has shut down nine, and part of the production line is to research and development purposes. Some production lines are converted to LTPS production lines through process conversion. Korean manufacturers are turning to OLED panels in a comprehensive way, while Japanese manufacturers are basically giving up the LCD panel manufacturing business and turning to the core equipment and materials side. In addition to the technical direction of the research and judgment, more is the LCD panel business orders and profits have been severely compressed, Korean and Japanese manufacturers have no desire to fight. Since many OLED technologies are still in their infancy in mainland China, it is a priority to move to high-end panels such as OLED as soon as possible. Taiwanese manufacturers have not shut down factories on a large scale, but their advantages in LCD technology and OLED technology have been slowly eroded by the mainland.

STONE provides a full range of 3.5 inches to 15.1 inches of small and medium-size standard quasi TFT LCD module, LCD display, TFT display module, display industry, industrial LCD screen, under the sunlight visually highlight TFT LCD display, industrial custom TFT screen, TFT LCD screen-wide temperature, industrial TFT LCD screen, touch screen industry. The TFT LCD module is very suitable for industrial control equipment, medical instruments, POS system, electronic consumer products, vehicles, and other products.STONE provides a full range of 3.5 inches to 15.1 inches of small and medium-size standard quasi TFT LCD module, LCD display, TFT display module, display industry, industrial LCD screen, under the sunlight visually highlight TFT LCD display, industrial custom TFT screen, TFT LCD screen-wide temperature, industrial TFT LCD screen, touch screen industry. The TFT LCD module is very suitable for industrial control equipment, medical instruments, POS system, electronic consumer products, vehicles, and other products.

LCD manufacturers are mainly located in China, Taiwan, Korea, Japan. Almost all the lcd or TFT manufacturers have built or moved their lcd plants to China on the past decades. Top TFT lcd and oled display manufactuers including BOE, COST, Tianma, IVO from China mainland, and Innolux, AUO from Tianwan, but they have established factories in China mainland as well, and other small-middium sizes lcd manufacturers in China.

China flat display revenue has reached to Sixty billion US Dollars from 2020. there are 35 tft lcd lines (higher than 6 generation lines) in China,China is the best place for seeking the lcd manufacturers.

The first half of 2021, BOE revenue has been reached to twenty billion US dollars, increased more than 90% than thesame time of 2020, the main revenue is from TFT LCD, AMoled. BOE flexible amoled screens" output have been reach to 25KK pcs at the first half of 2021.the new display group Micro LED revenue has been increased to 0.25% of the total revenue as well.

Established in 1993 BOE Technology Group Co. Ltd. is the top1 tft lcd manufacturers in China, headquarter in Beijing, China, BOE has 4 lines of G6 AMOLED production lines that can make flexible OLED, BOE is the authorized screen supplier of Apple, Huawei, Xiaomi, etc,the first G10.5 TFT line is made in BOE.BOE main products is in large sizes of tft lcd panel,the maximum lcd sizes what BOE made is up to 110 inch tft panel, 8k resolution. BOE is the bigger supplier for flexible AM OLED in China.

As the market forecast of 2022, iPhone OLED purchasing quantity would reach 223 million pcs, more 40 million than 2021, the main suppliers of iPhone OLED screen are from Samsung display (61%), LG display (25%), BOE (14%). Samsung also plan to purchase 3.5 million pcs AMOLED screen from BOE for their Galaxy"s screen in 2022.

Technology Co., Ltd), established in 2009. CSOT is the company from TCL, CSOT has eight tft LCD panel plants, four tft lcd modules plants in Shenzhen, Wuhan, Huizhou, Suzhou, Guangzhou and in India. CSOTproviding panels and modules for TV and mobile

three decades.Tianma is the leader of small to medium size displays in technologyin China. Tianma have the tft panel factories in Shenzhen, Shanhai, Chendu, Xiamen city, Tianma"s Shenzhen factory could make the monochrome lcd panel and LCD module, TFT LCD module, TFT touch screen module. Tianma is top 1 manufactures in Automotive display screen and LTPS TFT panel.

Tianma and BOE are the top grade lcd manufacturers in China, because they are big lcd manufacturers, their minimum order quantity would be reached 30k pcs MOQ for small sizes lcd panel. price is also top grade, it might be more expensive 50%~80% than the market price.

Panda electronics is established in 1936, located in Nanjing, Jiangshu, China. Panda has a G6 and G8.6 TFT panel lines (bought from Sharp). The TFT panel technologies are mainly from Sharp, but its technology is not compliance to the other tft panels from other tft manufactures, it lead to the capacity efficiency is lower than other tft panel manufacturers. the latest news in 2022, Panda might be bougt to BOE in this year.

Established in 2005, IVO is located in Kunsan,Jiangshu province, China, IVO have more than 3000 employee, 400 R&D employee, IVO have a G-5 tft panel production line, IVO products are including tft panel for notebook, automotive display, smart phone screen. 60% of IVO tft panel is for notebook application (TOP 6 in the worldwide), 23% for smart phone, 11% for automotive.

Besides the lcd manufacturers from China mainland,inGreater China region,there are other lcd manufacturers in Taiwan,even they started from Taiwan, they all have built the lcd plants in China mainland as well,let"s see the lcd manufacturers in Taiwan:

Innolux"s 14 plants in Taiwan possess a complete range of 3.5G, 4G, 4.5G, 5G, 6G, 7.5G, and 8.5G-8.6G production line in Taiwan and China mainland, offering a full range of large/medium/small LCD panels and touch-control screens.including 4K2K ultra-high resolution, 3D naked eye, IGZO, LTPS, AMOLED, OLED, and touch-control solutions,full range of TFT LCD panel modules and touch panels, including TV panels, desktop monitors, notebook computer panels, small and medium-sized panels, and medical and automotive panels.

AUO is the tft lcd panel manufacturers in Taiwan,AUO has the lcd factories in Tianma and China mainland,AUOOffer the full range of display products with industry-leading display technology,such as 8K4K resolution TFT lcd panel, wide color gamut, high dynamic range, mini LED backlight, ultra high refresh rate, ultra high brightness and low power consumption. AUO is also actively developing curved, super slim, bezel-less, extreme narrow bezel and free-form technologies that boast aesthetic beauty in terms of design.Micro LED, flexible and foldable AMOLED, and fingerprint sensing technologies were also developed for people to enjoy a new smart living experience.

Hannstar was found in 1998 in Taiwan, Hannstar display hasG5.3 TFT-LCD factory in Tainan and the Nanjing LCM/Touch factories, providing various products and focus on the vertical integration of industrial resources, creating new products for future applications and business models.

driver, backlight etc ,then make it to tft lcd module. so its price is also more expensive than many other lcd module manufacturers in China mainland.

Maclight is a China based display company, located in Shenzhen, China. ISO9001 certified, as a company that more than 10 years working experiences in display, Maclight has the good relationship with top tft panel manufacturers, it guarantee that we could provide a long term stable supply in our products, we commit our products with reliable quality and competitive prices.

Maclight products included monochrome lcd, TFT lcd module and OLED display, touch screen module, Maclight is special in custom lcd display, Sunlight readable tft lcd module, tft lcd with capacitive touch screen. Maclight is the leader of round lcd display. Maclight is also the long term supplier for many lcd companies in USA and Europe.

If you want tobuy lcd moduleorbuy tft screenfrom China with good quality and competitive price, Maclight would be a best choice for your glowing business.

The panel supply chain has seen oversupply with prices falling. In consequence of the waning epidemic, TV sales which could have been boosted by WFH economy can hardly regain momentum in the fourth quarter. On top of that, Samsung and LG are gradually fading out the traditional panel industry. Taiwanese firms on the other hand focus on cockpit panels, advanced TV models, gaming businesses and IT products. The global panel industry structure is transforming.

Chinese presence in the LCD panel industry continues its expansion. Samsung used to dominate in the high-end panel market but is now no longer obsessed with the business as before. Samsung has sold its panel production line to China"s CSOT. China-made panels are expected to dominate the market before OLED panel is mature enough to erode the market share of LCD panels. It is predicted China-made panels will account for over 70% of the global panel market share.

In terms of applications, cockpit dashboards and central control systems both maintain double-digit growth. Interactive digital signage displays also perform well with good sales. The market preference is tilting towards the large-sized models. After taking over Samsung"s production line, CSOT is to be a significant player and poses threats to Taiwanese firms.

Since the pandemic is waning, the global TV market as a panel end-user segment is facing a downturn in demand. Components shortage, port congestion, China"s policy on power restrictions, coupled with typhoons in Asia have exacerbated the issues. Considering quarterly output between 7-8 million units, Taiwanese TV makers like TPV and Hon Hai (Foxconn) willl report moderate sequential growths in third-quarter and fourth-quarter 2021, but will see declines of about 15% year-on-year. Apparently, the big demand cycle of panels has come to an end.

As for the demand of tablets, since people are going back to normal life in the fourth quarter, supply-and-demand imbalance is slightly diminishing. High hopes of peak season expected in the fourth quarter may result in a let-down. However, normal shipments of some manufacturers are affected due to shortages of PMIC, TDDI and application processors.

This indicates that China"s development of its own semiconductor industry remains a significant part of its national development plan. The semiconductor industry is different from the panel industry. There is no telling if China"s semiconductor can duplicate the model of its panel industry to capitalize on domestic support with massive capital funds.

BOE Technology Group and TCL China Star Optoelectronics Technology (TCL CSOT) are among the Chinese panel makers to have ramped up output since around 2019 with generous state subsidies. China is gaining on South Korea, whose share of capacity is seen reaching 55% for 2022 in an October estimate by U.S. market intelligence firm Display Supply Chain Consultants (DSCC).

LCD manufacturers are mainly located in China, Taiwan, Korea, Japan. Almost all the lcd or TFT manufacturers have built or moved their lcd plants to China on the past decades. Top TFT lcd and oled display manufactuers including BOE, COST, Tianma, IVO from China mainland, and Innolux, AUO from Tianwan, but they have established factories in China mainland as well, and other small-middium sizes lcd manufacturers in China.

China flat display revenue has reached to Sixty billion US Dollars from 2020. there are 35 tft lcd lines (higher than 6 generation lines) in China,China is the best place for seeking the lcd manufacturers.

The first half of 2021, BOE revenue has been reached to twenty billion US dollars, increased more than 90% than thesame time of 2020, the main revenue is from TFT LCD, AMoled. BOE flexible amoled screens" output have been reach to 25KK pcs at the first half of 2021.the new display group Micro LED revenue has been increased to 0.25% of the total revenue as well.

Established in 1993 BOE Technology Group Co. Ltd. is the top1 tft lcd manufacturers in China, headquarter in Beijing, China, BOE has 4 lines of G6 AMOLED production lines that can make flexible OLED, BOE is the authorized screen supplier of Apple, Huawei, Xiaomi, etc,the first G10.5 TFT line is made in BOE.BOE main products is in large sizes of tft lcd panel,the maximum lcd sizes what BOE made is up to 110 inch tft panel, 8k resolution. BOE is the bigger supplier for flexible AM OLED in China.

As the market forecast of 2022, iPhone OLED purchasing quantity would reach 223 million pcs, more 40 million than 2021, the main suppliers of iPhone OLED screen are from Samsung display (61%), LG display (25%), BOE (14%). Samsung also plan to purchase 3.5 million pcs AMOLED screen from BOE for their Galaxy"s screen in 2022.

Technology Co., Ltd), established in 2009. CSOT is the company from TCL, CSOT has eight tft LCD panel plants, four tft lcd modules plants in Shenzhen, Wuhan, Huizhou, Suzhou, Guangzhou and in India. CSOTproviding panels and modules for TV and mobile

three decades.Tianma is the leader of small to medium size displays in technologyin China. Tianma have the tft panel factories in Shenzhen, Shanhai, Chendu, Xiamen city, Tianma"s Shenzhen factory could make the monochrome lcd panel and LCD module, TFT LCD module, TFT touch screen module. Tianma is top 1 manufactures in Automotive display screen and LTPS TFT panel.

Tianma and BOE are the top grade lcd manufacturers in China, because they are big lcd manufacturers, their minimum order quantity would be reached 30k pcs MOQ for small sizes lcd panel. price is also top grade, it might be more expensive 50%~80% than the market price.

Panda electronics is established in 1936, located in Nanjing, Jiangshu, China. Panda has a G6 and G8.6 TFT panel lines (bought from Sharp). The TFT panel technologies are mainly from Sharp, but its technology is not compliance to the other tft panels from other tft manufactures, it lead to the capacity efficiency is lower than other tft panel manufacturers. the latest news in 2022, Panda might be bougt to BOE in this year.

Established in 2005, IVO is located in Kunsan,Jiangshu province, China, IVO have more than 3000 employee, 400 R&D employee, IVO have a G-5 tft panel production line, IVO products are including tft panel for notebook, automotive display, smart phone screen. 60% of IVO tft panel is for notebook application (TOP 6 in the worldwide), 23% for smart phone, 11% for automotive.

Besides the lcd manufacturers from China mainland,inGreater China region,there are other lcd manufacturers in Taiwan,even they started from Taiwan, they all have built the lcd plants in China mainland as well,let"s see the lcd manufacturers in Taiwan:

Innolux"s 14 plants in Taiwan possess a complete range of 3.5G, 4G, 4.5G, 5G, 6G, 7.5G, and 8.5G-8.6G production line in Taiwan and China mainland, offering a full range of large/medium/small LCD panels and touch-control screens.including 4K2K ultra-high resolution, 3D naked eye, IGZO, LTPS, AMOLED, OLED, and touch-control solutions,full range of TFT LCD panel modules and touch panels, including TV panels, desktop monitors, notebook computer panels, small and medium-sized panels, and medical and automotive panels.

AUO is the tft lcd panel manufacturers in Taiwan,AUO has the lcd factories in Tianma and China mainland,AUOOffer the full range of display products with industry-leading display technology,such as 8K4K resolution TFT lcd panel, wide color gamut, high dynamic range, mini LED backlight, ultra high refresh rate, ultra high brightness and low power consumption. AUO is also actively developing curved, super slim, bezel-less, extreme narrow bezel and free-form technologies that boast aesthetic beauty in terms of design.Micro LED, flexible and foldable AMOLED, and fingerprint sensing technologies were also developed for people to enjoy a new smart living experience.

Hannstar was found in 1998 in Taiwan, Hannstar display hasG5.3 TFT-LCD factory in Tainan and the Nanjing LCM/Touch factories, providing various products and focus on the vertical integration of industrial resources, creating new products for future applications and business models.

driver, backlight etc ,then make it to tft lcd module. so its price is also more expensive than many other lcd module manufacturers in China mainland.

Maclight is a China based display company, located in Shenzhen, China. ISO9001 certified, as a company that more than 10 years working experiences in display, Maclight has the good relationship with top tft panel manufacturers, it guarantee that we could provide a long term stable supply in our products, we commit our products with reliable quality and competitive prices.

Maclight products included monochrome lcd, TFT lcd module and OLED display, touch screen module, Maclight is special in custom lcd display, Sunlight readable tft lcd module, tft lcd with capacitive touch screen. Maclight is the leader of round lcd display. Maclight is also the long term supplier for many lcd companies in USA and Europe.

If you want tobuy lcd moduleorbuy tft screenfrom China with good quality and competitive price, Maclight would be a best choice for your glowing business.

Chinese display panel makers accounted for nearly half of the share in the global liquid crystal display TV panel market in the first half of this year, dominating the industry.

Beijing-based market researcher Sigmaintell Consulting said shipments of LCD TV panels worldwide totaled 140 million pieces in the year"s first half, up 3.6 percent compared with the same period a year ago.

The supply of TV panels though has surpassed demand due to the slowdown in the global economy and weaker consumer purchasing power. Manufacturers are facing severe challenges from falling panel prices, the Sigmaintell report said.

The shipment of BOE"s LCD TV panels stood at 27.6 million in the Jan-June period while LG Display followed with 22.7 million, down 4.5 percent year-on-year. Innolux Display Group was in third place, having shipped 21.9 million units.

Shenzhen China Star Optoelectronics Technology Co Ltd, a subsidiary of consumer electronics giant TCL Corp, ranked fourth, shipping 19.3 million pieces of TV panels. Chinese panel makers accounted for a 45.8 percent share in the global LCD TV panel market.

Sigmaintell estimated that the gap between supply and demand would widen further, and the panel market may face a long-term risk of oversupply. The industry may have to undergo a reshuffle given fierce market competition, it said.

The panel makers must reduce costs, optimize their internal structures, promote technological innovation and explore more innovative applications, the report by the consultancy said.

Separately, BOE"s Gen 10.5 TFTLCD production line has entered operation in Hefei, Anhui province. The plant will produce high-definition LCD screens of 65 inches and above.

"China"s semiconductor display industry has taken large steps forward in the past decade, changing the display industry"s global competitive landscape. China has transformed into the world"s largest consumer market and manufacturing base for display terminals, with huge market potential," said BOE Vice-President Zhang Yu.

CSOT also announced in November last year that its Gen 11 TFT-LCD and active-matrix OLED production line had officially began operation. The project will produce 43-inch, 65-inch and 75-inch liquid crystal display screens.

China is expected to replace South Korea as the world"s largest flat-panel display producer in 2019, a report from the China Video Industry Association and the China Optics and Optoelectronics Manufacturers Association said.

"The average size of TV panels is likely to increase 1.4 inches in 2019. The 65-inch dimension will become the most popular size of TV," Li Yaqin, general manager of Sigmaintell, said while adding the 65-inch TV will become the mainstream screen in people"s living rooms in the future.

Compared with traditional LCD display panels, OLED has a fast response rate, wide viewing angles, high-contrast images and richer colors. It is thinner and can be made flexible.

Attendees visit the booth of TV panel maker Shenzhen China Star Optoelectronics Technology during an international exhibition in Shanghai on July 11, 2019. [Photo by Lyu Liang/For China Daily]

Chinese companies have gained a competitive edge in the large-screen display industry and the exit of South Korean counterparts such as Samsung Electronics and LG Display from the liquid crystal display market will bring opportunities for China"s panel makers despite the challenges posed by the COVID-19 pandemic.

Market research firm Sigmaintell said BOE Technology Group Co Ltd-a leading Chinese supplier of display products and solutions-became the world"s largest shipper of LCD TV panels for the first time in 2019.

The Beijing-based company shipped 53.3 million units of LCD panels in 2019, with production capacity increasing by more than 20 percent on a yearly basis.

The consultancy said the LCD TV panel production area of Chinese manufacturers will account for more than 50 percent of the global total this year, surpassing South Korean competitors who are accelerating the shutdown of large-sized LCD panel production capacity due to competition from Chinese manufacturers.

It estimated the production capacity of large-sized LCD panels will continue to increase in China over the next three years. In addition, global LCD TV panel shipments stood at 283 million pieces last year, a slight decrease of 0.2 percent year-on-year. Meanwhile, the shipment area was 160 million square meters, an increase of 6.3 percent year-on-year.

"Chinese companies have gained an upper hand in large-screen LCD displays. Samsung and LG"s decision to exit from the LCD sector means Chinese panel makers will take a dominant position in this field," said Li Dongsheng, founder and chairman of Chinese tech giant TCL Technology Group Corp.

Li said South Korean firms will focus on organic LED screens and quantum dot LED displays, while Chinese TV panel makers are catching up at a rapid pace.

"The outbreak has caused a periodic drop in demand in the global display market and sped up the restructuring of the entire industry. Chinese enterprises are in a favorable position, and I believe that they will further enhance their competitiveness," Li said.

Data consultancy Digitimes Research said it comes as little surprise that Samsung has opted to withdraw from the LCD panel sector as its LCD business was losing money in every quarter of 2019 due to challenges from Chinese competitors.

"China"s semiconductor display industry has made large advances in the past decade, changing the display industry"s global competitive landscape. China has transformed into the world"s largest consumer market and manufacturing base for display terminals, with huge market potential," said BOE Vice-President Zhang Yu.

BOE said its Gen 10.5 TFTLCD production line achieved mass production in Hefei, Anhui province, in March 2018. The plant mainly produces high-definition LCD screens of 65 inches and above. With a total investment of 46 billion yuan ($6.5 billion), the company"s second Gen 10.5 TFT-LCD production line launched operations in Wuhan, Hubei province, in December.

The Gen 11 TFT-LCD and active-matrix OLED production line of Shenzhen China Star Optoelectronics Technology, a subsidiary of TCL, officially entered operations in November 2018, producing 43-inch, 65-inch and 75-inch LCD screens.

Chen Lijuan, an analyst at Sigmaintell, said panel manufacturers should not just invest in production lines, but also pay more attention to the establishment of the whole supply chain, including raw materials, equipment and technology.

Bian Zheng, deputy director of research at AVC Revo, a unit of market consultancy firm AVC, said China will have a 51 percent market share in global TV shipments in 2020, while South Korea will have 25 percent, adding that large-screen TV panels will bolster healthy development of the industry.

Bian said the OLED and QLED will be the next-generation flat-panel display technologies to be in the spotlight. LG Display is currently the world"s only supplier of large-screen OLED TV panels.

OLED is a relatively new technology and part of recent display innovation. It has a fast response rate, wide viewing angles, super high-contrast images and richer colors. It is much thinner and can be made flexible, compared with traditional LCD display panels.

Chinese display manufacturers are chasing their South Korean rivals closely by planning to release a larger volume of liquid-crystal panels over 32 inches this year, said a market researcher Sunday.

According to a report on the 2017 shipment strategies of Chinese TV panel makers by IHS Markit, Chinese LCD panel suppliers are forecast to ship out a total of 320,000 large-size panels larger than 32 inches by the end of this year, a 33 percent surge from last year.

In the report, Wu mentioned the plans of major Chinese panel firms such as BOE, CSOT, CEC-Panda and HKC to focus on expanding production of 43, 55 and 58-inch panels, adding that demand for 32-inch panels will gradually decrease.

“By the end of 2018, China will be the largest region for TFT LCD capacity, and larger-sized products may make their factories more efficient and profitable than they have been when producing 32-inch panels,” he said.

The strategy shift of the Chinese players suggests that they might outstrip Korean display makers in the global large-size display market, the analyst said.

“The strategies of Chinese panel makers will significantly influence global supply and demand,” Wu said. “In 2015 and 2016, the Chinese companies shipped 33.2 percent of worldwide LCD TV panel, trailing only Korean panel makers at 36.4 percent.”

The competition structure has been advantageous for the Korean players, since their Chinese rivals had been focusing on small LCD panels until last year. But now the Korean firms are facing fiercer competition in prices.

Although demand for organic-light emitting diode panels in the TV market is gradually rising, dominance of LCD panels is projected to continue for the foreseeable future.

“While OLEDs are expected to post sharp growth, they will not be able to usurp LCD as the panels of choice for upper-end TVs,” another report by IHS Markit said.

China’s display market share is expected to rise to 43% this year from 41.5% in 2021. Korean companies logged a market share of 33.2% in 2021, losing the No. 1 position they have maintained for 17 years since 2004 to Chinese manufacturers, reported Business Korea on November 3.

In the LCD market, China"s market share reached 50.9% in 2021, while South Korea posted a mere 14.4%. As profitability deteriorated due to a price war waged by Chinese companies, Samsung Display decided to suspend LCD production in the second quarter of this year. LG Display implemented an LCD exit strategy ahead of schedule after recording a loss for two consecutive quarters.

China is also in hot pursuit of South Korea in the OLED sector. While South Korea’s OLED market share fell from 98.1% in 2016 to 82.8% in 2021, China rose from 1.1% to 16.6% during the same period, said the Business Korea report.

Due to the COVID-19 pandemic and Russia-Ukraine War Influence, the global market for Product Name estimated at USD million in the year 2022, is projected to reach a revised size of USD million by 2028, growing at a CAGR during the forecast period 2022-2028.

The USA market for LCD Panel is estimated to increase from USD million in 2022 to reach USD million by 2028, at a CAGR during the forecast period of 2023 through 2028.

The China market for LCD Panel is estimated to increase from USD million in 2022 to reach USD million by 2028, at a CAGR during the forecast period of 2023 through 2028.

The Europe market for LCD Panel is estimated to increase from USD million in 2022 to reach USD million by 2028, at a CAGR during the forecast period of 2023 through 2028.

The global key manufacturers of LCD Panel include Samsung, SONY, Sharp, Panasonic, Toshiba, LG, Seiki, Christie and NEC, etc. In 2021, the global top five players had a share approximately in terms of revenue.

This report aims to provide a comprehensive presentation of the global market for LCD Panel, with both quantitative and qualitative analysis, to help readers develop business/growth strategies, assess the market competitive situation, analyze their position in the current marketplace, and make informed business decisions regarding LCD Panel.

The LCD Panel market size, estimations, and forecasts are provided in terms of output/shipments (K Tons) and revenue (USD millions), considering 2021 as the base year, with history and forecast data for the period from 2017 to 2028. This report segments the global LCD Panel market comprehensively. Regional market sizes, concerning products by types, by application, and by players, are also provided. The influence of COVID-19 and the Russia-Ukraine War were considered while estimating market sizes.

In this section, the readers will gain an understanding of the key players competing. This report has studied the key growth strategies, such as innovative trends and developments, intensification of product portfolio, mergers and acquisitions, collaborations, new product innovation, and geographical expansion, undertaken by these participants to maintain their presence. Apart from business strategies, the study includes current developments and key financials. The readers will also get access to the data related to global revenue, price, and sales by manufacturers for the period 2017-2022. This all-inclusive report will certainly serve the clients to stay updated and make effective decisions in their businesses.

The market has been segmented into various major geographies, including North America, Europe, Asia-Pacific, South America. Detailed analysis of major countries such as the USA, Germany, the U.K., Italy, France, China, Japan, South Korea, Southeast Asia, and India will be covered within the regional segment. For market estimates, data are going to be provided for 2021 because of the base year, with estimates for 2022 and forecast value for 2028.

This report will help the readers to understand the competition within the industries and strategies for the competitive environment to enhance the potential profit. The report also focuses on the competitive landscape of the global LCD Panel market, and introduces in detail the market share, industry ranking, competitor ecosystem, market performance, new product development, operation situation, expansion, and acquisition. etc. of the main players, which helps the readers to identify the main competitors and deeply understand the competition pattern of the market.

This report will help stakeholders to understand the global industry status and trends of LCD Panel and provides them with information on key market drivers, restraints, challenges, and opportunities.

Chapter 1: Introduces the report scope of the report, executive summary of different market segments (by region, product type, application, etc), including the market size of each market segment, future development potential, and so on. It offers a high-level view of the current state of the market and its likely evolution in the short to mid-term, and long term.

Chapter 2: Detailed analysis of LCD Panel manufacturers competitive landscape, price, output and revenue market share, latest development plan, merger, and acquisition information, etc.

Chapter 3: Production/output, value of LCD Panel by region/country. It provides a quantitative analysis of the market size and development potential of each region in the next six years.

Chapter 4: Consumption of LCD Panel in regional level and country level. It provides a quantitative analysis of the market size and development potential of each region and its main countries and introduces the market development, future development prospects, market space, and capacity of each country in the world.

Chapter 5: Provides the analysis of various market segments according to product type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments.

Chapter 6: Provides the analysis of various market segments according to application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product production/output, revenue, , price, gross margin, product introduction, recent development, etc.

Chapter 10: Introduces the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry.

Chapter 13: Forecast by type and by application. It provides a quantitative analysis of the market size and development potential of each market segment in the next six years.

Our Other Reports:Global Cetrimonium Chlorides Market Size 2022 with Company Profile, Sales, Revenue, Average Selling Price, Gross Margin and Forecast to 2025| Research Report by Absolute Reports

Is there a problem with this press release? Contact the source provider Comtex at editorial@comtex.com. You can also contact MarketWatch Customer Service via our Customer Center.

China has become the world"s largest LCD panel manufacturing base and is investing in a complete Mini/Micro-LED industry chain. Li Leiguang, JW Insights" chief analyst of the display industry, shared this information at a Mini/Micro-LED industry forum held in Shenzhen in late October.

With over 16 years of experience in the display industry, Li Leiguang has a deep understanding of China"s domestic display industry from materials and panel technologies to industrial policies. He has written industrial research and planning reports for various government departments in Shenzhen, Zhaoqing, Meishan, and Chengdu as well as customized reports for corporate clients in the display industry chain. This article is an excerpt from his speech.

China had long depended on imports of IC and display screens in the manufacturing of display products. IC and display screens are the two pillar sectors of the ICT Industry. The trend has been changing. With the continuous increase of high-generation production lines and capacity of domestic panel manufacturers and the gradual closure of LCD production lines by South Korean manufacturers, China"s LCD panel market share has increased year by year.

In 2020, China achieved a trade surplus in LCD panels for the first time. Meanwhile, the TFT-LCD has become a mainstream choice in the display panel industry after nearly 30 years of development.

JW Insights data shows that China has invested a total of RMB1.2 trillion($187.56 billion) in TFT-LCD and AMOLED panel production lines; Some 50 TFT-LCD and AMOLED panel production lines have been built, with 197 million m2/year TFT-LCD production capacity, 8.9 million m2/year AMOLED production capacity.

China"s LCD production capacity accounted for 50% of the global production capacity in 2020, becoming the world"s largest LCD panel production center; It will reach more than 75% of the world"s total by 2025.

China"s mainland is currently the only region that maintains continuous growth in LCD panel production capacity. With Japanese and South Korean manufacturers gradually withdrawing from the LCD panel, China is becoming the dominant player.

Chinese domestic display panel manufacturers are also embracing new display technologies such as Mini LED, Mirco LED, OLED and Micro OLED (silicon-based OLED), which are in an explosive market growth phase.

Chinese screen manufacturers plan to invest nearly RMB 30 billion($4.7 billion) in silicon-based OLED products lines, with more than 15 planned production lines and the total production capacity equivalent to 95 million units 1-inch screen, according to JW Insights statistics.

Unlike LCD technology that originated overseas, China has kept pace with the world in Mini/Micro-LED and has established a relatively complete industrial chain in it. Currently, the Mini LED is mainly used for LCD panel backlighting; It will be an inevitable trend for the direct LED display with Mini LED in large-screen in the future.

Regarding the Micro-LED technological progress choices, Chinese display manufacturers are facing challenges in mass transfer and full-color display. They are exploring and verifying multiple technical routes.

However, TFT-LCD technology will remain the mainstay for a long time in the future, because of its maturity and competitive prices. Multiple display technologies will coexist in the future; Micro-LED panels mass production will not be achieved in the short term.

Latest research from Omdia has found that Chinese display maker BOE has led the market in shipments of large area TFT LCD displays in December 2021, both in units and total area shipped. This accounts for nearly one-third of whole unit shipments, as the industry set new records for shipments for the month and year.

Pandemic restrictions impacted demand for and spending across home entertainment products with display shipments of TV and IT devices experiencing a growth surge. The total of large area TFT display shipments rose to a record 89.4 million square meters in December, reflecting a 4 percent month-on-month increase over November, as well as 5 percent Year on Year growth (YoY), Omdia reported in its latest Large Area Display Market Tracker.

For the full year, large area TFT LCD shipments increased with 9 percent YoY by units and 4 percent YoY by area, reaching 962.7 million units and 228.8 million square meters shipped in 2021, both historical highs and marking the first time the industry has ever shipped more than 900 million units in a year.

Among display makers, China"s BOE took the largest shares for both units and total area shipped in 2021. BOE took 31.5 percent for units shipped and 26.2 percent for area shipped, marking the first time one maker has captured over 31 percent market share for whole unit shipments and 26 percent share for whole area shipments in large area TFT LCD history.

Beyond BOE, Innolux took 15.4 percent market share for large area TFT LCD unit shipments, followed by LG Display with 13.4 percent in 2021. For total area shipped, China Star took 15.8 percent as second largest maker after BOE, followed by LG Display in third with 11.9 percent in 2021.

Strong demand particularly for mobile PC LCD during the pandemic increased notebook PC LCD unit shipments in 2021, rising 26 percent YoY. Tablet PC LCD unit shipments also rose 7 percent YoY last year. On the other hand, the LCD TV display segment saw unit shipments fall 4 percent YoY due to a slowdown in demand in 3Q21. But ongoing LCD TV size migration in favor of larger screens meant that total LCD TV display area shipped increased 2 percent YoY in 2021 despite the drop in unit shipments.

Large area TFT LCD revenue increased 34 percent YoY in 2021 and reached US$85.2 billion, also setting a record and the first time large area TFT LCD revenue has ever exceeded $80 billion. Strong demand and size migration to larger screens during COVID-19 pandemic combined with display price hikes up until 3Q21 to drive the high revenue number.

YoonSung Chung, senior research manager for large area displays and supply chain at Omdia, commented: "Display makers waited for results from Black Friday sales to set their early 2022 sales and pricing strategies. However, results seem to fall short of expectations for LCD TVs. LCD TV display buyers will price LCD TV displays more aggressively in the coming months.

"While demand for IT displays is weakening, panel makers’ supply plans are ambitious. Unless panel makers adjust their fab utilisation, price erosions could imminently worsen for large area display applications, including monitor and notebook PC LCDs. Omdia expects the LCD TV panel prices to reach the price bottom in 1H 2022 and then gradually rebound based on the market demand recovery."

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey