lcd panel manufacturers market share pricelist

The upstream materials or components of the LCD panel industry mainly include liquid crystal materials, glass substrates, polarizing lenses, and backlight LEDs (or CCFL, which accounts for less than 5% of the market).

The middle reaches is the main panel factory processing and manufacturing, through the glass substrate TFT arrays and CF substrate, CF as upper and TFT self-built perfusion liquid crystal and the lower joint, and then put a polaroid, connection driver IC and control circuit board, and a backlight module assembling, eventually forming the whole piece of LCD module. The downstream is a variety of fields of application terminal-based brand, assembly manufacturers. At present, the United States, Japan, and Germany mainly focus on upstream raw materials, while South Korea, Taiwan, and the mainland mainly seek development in mid-stream panel manufacturing.

With the successive production of the high generation line in mainland China, the panel production capacity and technology level have been steadily improved, and the industrial competitiveness has been gradually enhanced. Nowadays, the panel industry is divided into three parts: South Korea, mainland China, and Taiwan, and mainland China is expected to become the no.1 in the world in 2019.

In the past decade, China’s panel display industryhas achieved leapfrog development, and the overall size of the industry has ranked among the top three in the world. Chinese mainland panel production capacity is expanding rapidly, although Japanese panel manufacturers master a large number of key technologies, gradually lose the price competitive advantage, compression panel production capacity. Panel production is concentrated in South Korea, Taiwan, and China, which is poised to become the world’s largest producer of LCD panels.

Up to 2016, BOE‘s global market share continued to increase: smartphone LCD, tablet PC display, and laptop display accounted for the world’s first market share, and display screen increased to the world’s second, while TV LCD remained the world’s third. In LCD TV panels, Chinese panel makers have accounted for 30 percent of global shipments to 77 million units, surpassing Taiwan’s 25.5 percent market share for the first time and ranking second only to South Korea.

In terms of the area of shipment, the area of board shipment of JD accounted for only 8.3% in 2015, which has been greatly increased to 13.6% in the first half of 2016, while the area of shipment of hu xing optoelectronics in the first half of 2015 was only 5.1%, which has reached 7.8% in the first half of 2016. The panel factories in mainland China are expanding their capacity at an average rate of double-digit growth and transforming it into actual shipments and areas of shipment. On the other hand, although the market share of South Korea, Japan, and Taiwan is gradually decreasing, some South Korean and Japanese manufacturers have been inclined to the large-size HD panel and AMOLED market, and the production capacity of the high-end LCD panel is further concentrated in mainland China.

Domestic LCD panel production line capacity gradually released, overlay the decline in global economic growth, lead to panel makers from 15 in the second half began, in a low profit or loss, especially small and medium-sized production line, the South Korean manufacturers take the lead in transformation strategy, closed in medium and small size panel production line, South Korea’s 19-panel production line has shut down nine, and part of the production line is to research and development purposes. Some production lines are converted to LTPS production lines through process conversion. Korean manufacturers are turning to OLED panels in a comprehensive way, while Japanese manufacturers are basically giving up the LCD panel manufacturing business and turning to the core equipment and materials side. In addition to the technical direction of the research and judgment, more is the LCD panel business orders and profits have been severely compressed, Korean and Japanese manufacturers have no desire to fight. Since many OLED technologies are still in their infancy in mainland China, it is a priority to move to high-end panels such as OLED as soon as possible. Taiwanese manufacturers have not shut down factories on a large scale, but their advantages in LCD technology and OLED technology have been slowly eroded by the mainland.

STONE provides a full range of 3.5 inches to 15.1 inches of small and medium-size standard quasi TFT LCD module, LCD display, TFT display module, display industry, industrial LCD screen, under the sunlight visually highlight TFT LCD display, industrial custom TFT screen, TFT LCD screen-wide temperature, industrial TFT LCD screen, touch screen industry. The TFT LCD module is very suitable for industrial control equipment, medical instruments, POS system, electronic consumer products, vehicles, and other products.STONE provides a full range of 3.5 inches to 15.1 inches of small and medium-size standard quasi TFT LCD module, LCD display, TFT display module, display industry, industrial LCD screen, under the sunlight visually highlight TFT LCD display, industrial custom TFT screen, TFT LCD screen-wide temperature, industrial TFT LCD screen, touch screen industry. The TFT LCD module is very suitable for industrial control equipment, medical instruments, POS system, electronic consumer products, vehicles, and other products.

Prices for all TV panel sizes fluctuated and are forecast to fluctuate between 2020 and 2022. The period from March 2020 to July 2021 saw the biggest price increases, when a 65" UHD panel cost between 171 and 288 U.S. dollars. In the fourth quarter of 2021, such prices fell and are expected to drop to an even lower amount by March 2022.Read moreLCD TV panel prices worldwide from January 2020 to March 2022, by size(in U.S. dollars)Characteristic32" HD43" FHD49"/50" UHD55" UHD65" UHD------

DSCC. (January 10, 2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) [Graph]. In Statista. Retrieved January 02, 2023, from https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars)." Chart. January 10, 2022. Statista. Accessed January 02, 2023. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. (2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars). Statista. Statista Inc.. Accessed: January 02, 2023. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "Lcd Tv Panel Prices Worldwide from January 2020 to March 2022, by Size (in U.S. Dollars)." Statista, Statista Inc., 10 Jan 2022, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC, LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) Statista, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/ (last visited January 02, 2023)

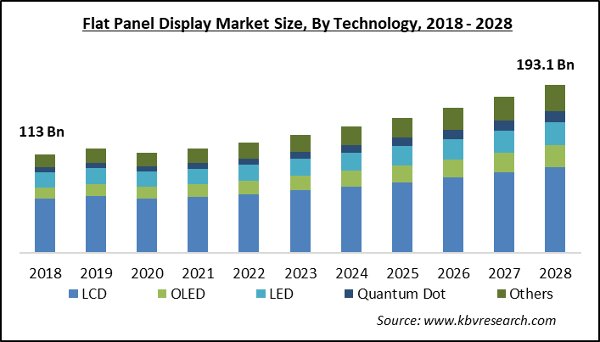

The global display device market reached a value of about USD 131.78 billion in 2021. The industry is further expected to grow at a CAGR of 5.2% in the forecast period of 2023-2028.

The Asia Pacific is expected to emerge as one of the world"s leading markets for display devices. Factors like the growth in the number of tech giants in the region and the availability of manufacturing resources at low cost contribute to the development of the display device industry in the Asia Pacific region.

The residential sector is projected to hold a significant market share in the coming years. The demand for electronic goods, including television, smartphones, laptops, tablets, as well as smart watches, has risen as technological developments continue, which is aiding the growth of the display device industry in the residential sector. Key players are now shifting to implement effective and luminous displays, leading to growth of microdisplay technology, which is expected to aid the global market growth in the coming years.

The remarkable rise in the usage of various consumer electronic products using state-of-the-art technologies is the main driving force behind the industry growth. The rising demand in the gaming and entertainment sector for high-quality displays as well as the increasing popularity of OLED-based technologies are notable factors that are boosting the market growth. The widespread adoption of flexible OLED display technologies is also increasing the demand for display devices. It is also anticipated that the advanced functions of display device will propel the market growth further in the coming years. Other factors boosting the market growth are the rising urbanisation, rising economies, as well as the rising disposable incomes of the consumers.

The report gives a detailed analysis of the following key players in the global display device market, covering their competitive landscape, capacity, and latest developments like mergers, acquisitions, and investments, expansions of capacity, and plant turnarounds:

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- Display Type, Technology, Application, End Use, Region

*At Expert Market Research, we strive to always give you current and accurate information. The numbers depicted in the description are indicative and may differ from the actual numbers in the final EMR report.

According to CINNO Research"s monthly LCD TV LCD panel shipment report, in February 2020, global LCD TV panel shipments were 19.64 million, a 5.1% month-on-month decrease from January 2020 and a 5.6% year-on-year decrease from February 2019. Problems such as tight logistics resources and poor supply chain operation caused by the COVID-19 epidemic were one of the main reasons for the decline in LCD TV shipments in February.

Starting from the end of 2019, LCD TV panel prices gradually stopped falling and began to rebound. Due to the impact of the COVID-19 epidemic on the supply chains of China and South Korea, the tension in panel supply has been further exacerbated in the short term, which has contributed to the rebound in panel prices. On the other hand, as the spread of the international epidemic continues to deteriorate, sports events that were originally considered to be crucial to TV sales such as the Champions League, European Cup, NBA, E3 2020, etc. have been cancelled or postponed, and the Tokyo Olympics also faced serious delays. Risks have added many variables to 2020, and the reduction in demand is expected to be difficult to support the continued increase in panel prices.

As Korean companies gradually withdrew from the LCD TV market, and the new capacity of mainland Chinese manufacturers has gradually achieved success, according to CINNO Research"s monthly LCD TV LCD panel shipment report, in terms of shipments, mainland China panel manufacturers in February 2020, it has accounted for 59.4% of total shipments, close to 60%. TCL CSOT became the world"s largest LCD TV panel supplier for the first time with 18.8% share, BOE ranked second with 17.4% market share, and HKC shipments also grew rapidly, ranking third with 13.4% share, Innolux and Samsung Display SDC ranked 4-5 with 12.3% and 10.5%.

According to CINNO Research"s monthly LCD TV LCD panel shipment report, in terms of shipment area, panel manufacturers in mainland China accounted for 56.6% of the total shipment area. CSOT also won the first place with a share of 19.6%, BOE, Samsung Display SDC, CEC (including Panda, Rainbow), LG Display LGD ranked 18.7%, 12.6%, 10.8% and 10.2% respectively. 2nd to 5th.

Westford,USA, Oct. 19, 2022 (GLOBE NEWSWIRE) -- The primary factors driving the growth of the Display Market are increasing demand from smartphone and tablet manufacturers, rising expenditure on smart Infra-Red (IR) sensors, and rapid expansion of digital media content. Smartphones are becoming more sophisticated and are using larger screens that require higher resolutions for better user experience. Tablets are also becoming increasingly popular as they offer a single device that can serve as both a computer and a mobile phone. This increase in demand for high-resolution displays is expected to drive the adoption of LED displays in the coming years.

Manufacturers in the global display market are starting to see the potential in displays as an important part of their product lines. Device manufacturers are looking for displays that can be used on a variety of devices, from laptops to smartphones and even cars. In addition, developers are creating more applications that require high-quality displays.

One key challenge facing manufacturers is making sure that their displays meet the requirements of multiple market segments. They need to make sure that their displays are suitable for usage on tablets as well as laptops, yet they also need to create displays that look good on smaller devices like smartphones and digital assistants.

The growth in demand for display market across various verticals such as healthcare, retail, automotive, appliance and others has led to an increasing demand for large sizes screens which can be cost effective owing to their mass production capabilities. Display manufacturers are also exploring new technologies such as flexible displays that can be rolled up like a traditional newspaper

Our report considers several factors such as market size estimation techniques, product segmentation analysis, expenditure Breakdown by Country and region; Porter"s Five Forces Analysis; and price trends analysis to give you a comprehensive view of the global display market.

Some of the key players in the global display market include LG Display Co., Ltd., Samsung Electronics Co., Ltd., and Sharp Corporation. These companies are focused on developing innovative products that meet the needs of various consumers in the marketplace. They also strive to improve their competitiveness by expanding their product lines into new markets and by creating partnerships with other companies to share technology and manufacturing resources.

Among global display market leaders, Samsung is presently dominating the industry with a share of 38% of the market. However, Apple is looming large as one of the largest competitors in smartphone sector. Other prominent players in this segment include LG Display, Sony Corp, and Toshiba Corporation. Among these companies, LG Display has been fastest expanding its business over recent years owing to its focus on emerging markets such as China and India.

For one, it"s heavily invested in research and development in the display market. According to analysts at SkyQuest, Samsung spends more than $13.7 billion a year on R&D, more than any other company in the world. That investment has paid off: The company"s displays are consistently among the best on the market.

Samsung also makes good use of its deep pockets. The company has poured money into forming joint ventures with major chipmakers like Qualcomm and Intel, which allows it to quickly bring new technologies to market. It doesn"t just rely on partnerships; Samsung also invests in its own technology centers, such as the foundry that produces screens for its smartphones.

One important technology that Samsung is investing in is AMOLED and QLED screens. QLEDs are generally considered to be more environmentally friendly than LCDs, since they use less power and create fewer byproducts.

The main drivers for Samsung"s strong performance in the display market are its diversification across product lines, continuous innovation across product categories, and excellent execution capabilities. The company has been able to expand into new markets such as automotive displays and smart watches, while continuing to focus on profitable core products.

Samsung has also been successful in pushing down prices for OLED displays over the past few years. This has made OLED panels more accessible to a wider range of customers, supporting growth at rival companies such as LG Electronics and Sony.

In recent years, there has been a shift in display technology as manufacturers across the global display market experiment with new and more innovative ways to create displays. The trend observed by SkyQuest worldwide is that display technologies are moving towards OLEDs and quantum dots, both of which have a number of advantages.

Quantum dots or QLED offer many advantages over traditional LCDs in the display market, such as better color reproduction, enhanced viewing angles, better response time, and lower power consumption. Their small size also makes them ideal for applications where sliding or tilting LCD panels are not possible or desirable. Quantum dot displays have already begun appearing in consumer electronics and will eventually replace traditional LCDs as the predominant type of display in devices like smartphones and tablets.

SkyQuest Technology is leading growth consulting firm providing market intelligence, commercialization and technology services. It has 450+ happy clients globally.

As people emerge from their Covid-19 hideouts, demand for screens is likely to drop, and this is happening as Chinese makers dominate the business and threaten to dump screens and wreck the market.

For LCD panels for 65-inch UHD TVs, the average price has increased 4 percent from $274 to $285 month-on-month. When compared to a year ago, that price surged 72 percent from $165.

According to market research company DSCC, the first quarter revenue of 13 LCD companies globally is estimated at $34.8 billion. That’s a 52 percent increase over the same period in 2020.

The possibility of a drop coming with the end of the pandemic brings back memories of the nightmare of two years ago, when the average price of LCD panels dropped from $143 to $100 in nine months as Chinese makers dumped product into the market.

“Because of Covid-19, LCD panels unexpectedly became a hot item,” said an industry official, who requested anonymity. “But as more people are inoculated and spending time outdoors, TV demand is dropping, and this could result in supply exceeding demand.”

Samsung Display CEO Choi Joo-sun said the company is currently reviewing whether to continued LCD production in an e-mail recently sent to employees in the LCD department.

LG Display, which initially planned to fold its LCD TV panel business by end of 2020, is currently running the production plant but without any additional investment or new equipment being installed.

“Already LCD prices when compared to a year ago have more than doubled,” said an industry insider, who wished to remain anonymous. “With China already completely dominating the market, it is unlikely they would repeat low-cost mass production similar to 2019.”

“It is possible that the LCD panel price could fall between the second half of this year and through the first half of next year as demand falls,” said Kim Hyun-soo, Hana Financial Investment analyst. “But as the likelihood of Chinese companies playing a game of chicken is reduced, the prices will likely stabilize in the second half of next year.”

Flat-panel displays are thin panels of glass or plastic used for electronically displaying text, images, or video. Liquid crystal displays (LCD), OLED (organic light emitting diode) and microLED displays are not quite the same; since LCD uses a liquid crystal that reacts to an electric current blocking light or allowing it to pass through the panel, whereas OLED/microLED displays consist of electroluminescent organic/inorganic materials that generate light when a current is passed through the material. LCD, OLED and microLED displays are driven using LTPS, IGZO, LTPO, and A-Si TFT transistor technologies as their backplane using ITO to supply current to the transistors and in turn to the liquid crystal or electroluminescent material. Segment and passive OLED and LCD displays do not use a backplane but use indium tin oxide (ITO), a transparent conductive material, to pass current to the electroluminescent material or liquid crystal. In LCDs, there is an even layer of liquid crystal throughout the panel whereas an OLED display has the electroluminescent material only where it is meant to light up. OLEDs, LCDs and microLEDs can be made flexible and transparent, but LCDs require a backlight because they cannot emit light on their own like OLEDs and microLEDs.

Liquid-crystal display (or LCD) is a thin, flat panel used for electronically displaying information such as text, images, and moving pictures. They are usually made of glass but they can also be made out of plastic. Some manufacturers make transparent LCD panels and special sequential color segment LCDs that have higher than usual refresh rates and an RGB backlight. The backlight is synchronized with the display so that the colors will show up as needed. The list of LCD manufacturers:

Organic light emitting diode (or OLED displays) is a thin, flat panel made of glass or plastic used for electronically displaying information such as text, images, and moving pictures. OLED panels can also take the shape of a light panel, where red, green and blue light emitting materials are stacked to create a white light panel. OLED displays can also be made transparent and/or flexible and these transparent panels are available on the market and are widely used in smartphones with under-display optical fingerprint sensors. LCD and OLED displays are available in different shapes, the most prominent of which is a circular display, which is used in smartwatches. The list of OLED display manufacturers:

MicroLED displays is an emerging flat-panel display technology consisting of arrays of microscopic LEDs forming the individual pixel elements. Like OLED, microLED offers infinite contrast ratio, but unlike OLED, microLED is immune to screen burn-in, and consumes less power while having higher light output, as it uses LEDs instead of organic electroluminescent materials, The list of MicroLED display manufacturers:

LCDs are made in a glass substrate. For OLED, the substrate can also be plastic. The size of the substrates are specified in generations, with each generation using a larger substrate. For example, a 4th generation substrate is larger in size than a 3rd generation substrate. A larger substrate allows for more panels to be cut from a single substrate, or for larger panels to be made, akin to increasing wafer sizes in the semiconductor industry.

"Samsung Display has halted local Gen-8 LCD lines: sources". THE ELEC, Korea Electronics Industry Media. August 16, 2019. Archived from the original on April 3, 2020. Retrieved December 18, 2019.

"TCL to Build World"s Largest Gen 11 LCD Panel Factory". www.businesswire.com. May 19, 2016. Archived from the original on April 2, 2018. Retrieved April 1, 2018.

"Panel Manufacturers Start to Operate Their New 8th Generation LCD Lines". 대한민국 IT포털의 중심! 이티뉴스. June 19, 2017. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"TCL"s Panel Manufacturer CSOT Commences Production of High Generation Panel Modules". www.businesswire.com. June 14, 2018. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"Samsung Display Considering Halting Some LCD Production Lines". 비즈니스코리아 - BusinessKorea. August 16, 2019. Archived from the original on April 5, 2020. Retrieved December 19, 2019.

Herald, The Korea (July 6, 2016). "Samsung Display accelerates transition from LCD to OLED". www.koreaherald.com. Archived from the original on April 1, 2018. Retrieved April 1, 2018.

"China"s BOE to have world"s largest TFT-LCD+AMOLED capacity in 2019". ihsmarkit.com. 2017-03-22. Archived from the original on 2019-08-16. Retrieved 2019-08-17.

In the recently released Quarterly OLED Shipment Report , DSCC reveals that 2023 OLED panel revenues are expected to increase 2% Y/Y to $42B after declining 2% Y/Y in 2022. This recovery is the result of expected triple digit growth for monitors, AR/VR and automotive applications and double-digit growth for notebook PCs, TVs and tablets.

As reported by Italian newspaper DDay, the EU Commission has confirmed that its much stricter Energy Efficiency Index (EEI) will be implemented as planned in March 2023 without revision. The new EEI will make it much more challenging to sell 8K TVs in Europe in 2023; all 8K TVs on the market there currently fail to meet the requirements.

After upgrading display capacity for six straight issues on improved market conditions in LCDs, DSCC has now lowered its display capacity forecast for four consecutive quarters on delays and cancellations as conditions worsen and remain weak. Prices were recently at marginal costs for LCD TV panels and it is projected that it will take until 2H’23 for prices to rise above cash costs.

After a weak Q2’22, the combination of macroeconomic and geopolitical events continued to hinder growth for the Advanced TV market, according to the latest update of DSCC’s Quarterly Advanced TV Shipment and Forecast Report, now available to subscribers. Samsung struggled through a difficult quarter, losing both unit and revenue share while its three biggest competitors – LG, Sony and TCL – all gained share.

Panel suppliers are mostly delaying new capacity decisions given the weak market conditions in the display market. The situation is particularly dire in LCDs where LCD TV panel prices approached marginal cost levels and BOE’s Chairman indicated they won’t build any more LCD TV fabs, resulting in the cancellation of B17+ and its removal from our forecast. The weakness in LCDs also spread to OLED spending since there is an oversupply there also and most OLED manufacturers also produce LCDs and are currently losing money. Samsung Display is the exception as it earned record OLED operating profits and operating margins in Q4’22 helped by strong iPhone 14 Pro/Pro Max demand and LG Display’s challenges getting qualified for the 14 Pro Max.

The central promotional event of the holiday season happens this week, and retailers will be offering all-time low prices for TVs during Black Friday. The unprecedented decline in LCD TV panel prices continues to flow through to retail prices in the US, and the competition from LCD is also pulling down OLED TV prices, which are also hitting all-time lows.

Now that all of the industry’s flat panel display makers have reported their Q3’22 financial results, we update our industry profile. The third quarter showed a gaping chasm between OLED-focused display makers, especially Samsung Display, and the companies focused on LCD technology. For LCD makers, it was the worst quarter in years and perhaps the worst ever. Meanwhile, Samsung Display recorded its highest profits ever in the first quarter after it discontinued LCD production.

As revealed in DSCC’s latest release of the OLED Shipment Report – Flash Edition, OLED panel revenues decreased 11% Y/Y on a 17% Y/Y decline in panel shipments. Smartphones, tablets and TVs, which have a combined 70% unit share and 85% panel revenue share, decline while other categories had Y/Y unit growth.

In another ominous sign for global TV industry supply, both demand and prices for TV-sized LCD panels continue to fall at the same time, recent reports from two display market analysts revealed.

Display industry market analysts TrendForce and Omdia each issued potentially troubling LCD TV display panel business updates this week as the global economic outlook continues to impact discretionary spending for non-essential items like TV sets.

According to TrendForce, the outlook for purchases by TV makers of LCD TV display panels — the major component part for LCD-based TVs that represent the vast majority of the TV sets — continues to decline even as prices for most panel sizes have fallen to record lows.

Recently, it was announced that the 32-inch and 43-inch panels fell by approximately $5-$6 in early June, 55-inch panels fell approximately $7, and prices for 65-inch and 75-inch panels, which face mounting overcapacity pressure, were down $12 to $14, TrendForce said.

“In order to alleviate pressure caused by price decline and inventory, panel makers are successively planning to initiate more significant production control in [the third quarter of 2022],” TrendForce said. “..Overall LCD TV panel production capacity in [the third quarter] will be reduced by 12% compared with original planning.”

According Omdia prices for TV-sized LCD display panels have been falling for the first year since Covid-19 appeared, while the increase in display demand area is expected to be up just 3%, half of the previous year.

Similarly, Omdia’s forecast released Thursday showed global display sales this year would decrease by 15% from last year to $133.18 billion. That compares to the global display sales increases of 14% in 2020 and 26% in 2021 due to the surge in demand for LCD panels and TVs generated by lockdowns forced by the pandemic.

LCD TV panel sales this year are expected to drop by 32% from last year ($38.3 billion) to $25.8 billion, according to Omdia’s predictions. The LCD TV panel demand area is expected to increase by 2% this year from last year, but the panel price decline is large.

“When there is an imbalance in supply and demand, a focus on strategic direction is prioritized,” TrendForce said. “TV panel production capacity of the three aforementioned companies in [Q3 2022] is expected to decrease by 15.8% compared with their original planning, and 2% compared with [the second quarter.]

TrendForce said Taiwanese manufacturers account for nearly 20% of TV panel shipments, and allocation of production capacity among those factories is now subject to “dynamic adjustment.”

The firm said TV sizes 55 inches and below have “fallen below their cash cost in May (which is seen as the last line of defense for panel makers) and is even flirting with the cost of materials, coupled with production capacity reduction from panel makers, the price of TV panels has a chance to bottom out at the end of June and be flat in July.”

TrendForce said that as panel makers continue to significant reduce production, the price of TV panels 55 inches and under is expected to remain flat in through the third quarter.

“Panel manufacturers cutting production in the traditional peak season also means that a disappointing [second half 2022] peak season is a foregone conclusion and it will not be easy for panel prices to reverse,” according to TrendForce.

It is possible that if the supply/pricing pressures continue, the number, scale and duration of manufacturers cutting panel production output will grow in an effort to generate momentum for a rebound in TV panel quotations, TrendForce said.

As reported by S. Korean technology trade news site The Elec, Omdia said the LCD TV panel shipment targets for BOE were lowered to 60 million units this year from the original 65.5 million units. HKC decreased its targets from 49.5 million to 42 million, CSOT from 45 to 44.8 million, and LG Display from 23.5 million to 18 million. Innolux’s shipment target increased slightly from 34.5 million units to 34.6 million units.

On the other hand, organic light emitting diode (OLED) TV panel sales this year are expected to reach $5.4 billion, up 12% from last year ($4.8 billion), according to Omdia.

OLED TV panels are being mass-produced by LG Display and Samsung Display, as both manufacturers reduce their exposure in LCDs. Samsung Display will end LCD TV panel production entirly this summer. However, LG Display’s OLED panel production forecast is 10 times that of Samsung Display.

Meanwhile, Samsung Display hiked yield rates for its new large-size QD-OLED panels from 30% of capacity initially, 50% in 2021, 75% in April-May 2022 to 80% now, according to South Korea-based publication The Bell.

Westford,USA, Oct. 19, 2022 (GLOBE NEWSWIRE) -- The primary factors driving the growth of the Display Market are increasing demand from smartphone and tablet manufacturers, rising expenditure on smart Infra-Red (IR) sensors, and rapid expansion of digital media content. Smartphones are becoming more sophisticated and are using larger screens that require higher resolutions for better user experience. Tablets are also becoming increasingly popular as they offer a single device that can serve as both a computer and a mobile phone. This increase in demand for high-resolution displays is expected to drive the adoption of LED displays in the coming years.

Manufacturers in the global display market are starting to see the potential in displays as an important part of their product lines. Device manufacturers are looking for displays that can be used on a variety of devices, from laptops to smartphones and even cars. In addition, developers are creating more applications that require high-quality displays.

One key challenge facing manufacturers is making sure that their displays meet the requirements of multiple market segments. They need to make sure that their displays are suitable for usage on tablets as well as laptops, yet they also need to create displays that look good on smaller devices like smartphones and digital assistants.

The growth in demand for display market across various verticals such as healthcare, retail, automotive, appliance and others has led to an increasing demand for large sizes screens which can be cost effective owing to their mass production capabilities. Display manufacturers are also exploring new technologies such as flexible displays that can be rolled up like a traditional newspaper

Our report considers several factors such as market size estimation techniques, product segmentation analysis, expenditure Breakdown by Country and region; Porter"s Five Forces Analysis; and price trends analysis to give you a comprehensive view of the global display market.

Some of the key players in the global display market include LG Display Co., Ltd., Samsung Electronics Co., Ltd., and Sharp Corporation. These companies are focused on developing innovative products that meet the needs of various consumers in the marketplace. They also strive to improve their competitiveness by expanding their product lines into new markets and by creating partnerships with other companies to share technology and manufacturing resources.

Among global display market leaders, Samsung is presently dominating the industry with a share of 38% of the market. However, Apple is looming large as one of the largest competitors in smartphone sector. Other prominent players in this segment include LG Display, Sony Corp, and Toshiba Corporation. Among these companies, LG Display has been fastest expanding its business over recent years owing to its focus on emerging markets such as China and India.

For one, it"s heavily invested in research and development in the display market. According to analysts at SkyQuest, Samsung spends more than $13.7 billion a year on R&D, more than any other company in the world. That investment has paid off: The company"s displays are consistently among the best on the market.

Samsung also makes good use of its deep pockets. The company has poured money into forming joint ventures with major chipmakers like Qualcomm and Intel, which allows it to quickly bring new technologies to market. It doesn"t just rely on partnerships; Samsung also invests in its own technology centers, such as the foundry that produces screens for its smartphones.

One important technology that Samsung is investing in is AMOLED and QLED screens. QLEDs are generally considered to be more environmentally friendly than LCDs, since they use less power and create fewer byproducts.

The main drivers for Samsung"s strong performance in the display market are its diversification across product lines, continuous innovation across product categories, and excellent execution capabilities. The company has been able to expand into new markets such as automotive displays and smart watches, while continuing to focus on profitable core products.

Samsung has also been successful in pushing down prices for OLED displays over the past few years. This has made OLED panels more accessible to a wider range of customers, supporting growth at rival companies such as LG Electronics and Sony.

In recent years, there has been a shift in display technology as manufacturers across the global display market experiment with new and more innovative ways to create displays. The trend observed by SkyQuest worldwide is that display technologies are moving towards OLEDs and quantum dots, both of which have a number of advantages.

Quantum dots or QLED offer many advantages over traditional LCDs in the display market, such as better color reproduction, enhanced viewing angles, better response time, and lower power consumption. Their small size also makes them ideal for applications where sliding or tilting LCD panels are not possible or desirable. Quantum dot displays have already begun appearing in consumer electronics and will eventually replace traditional LCDs as the predominant type of display in devices like smartphones and tablets.

SkyQuest Technology is leading growth consulting firm providing market intelligence, commercialization and technology services. It has 450+ happy clients globally.

1.1. THE POLICY COVERS THE HANDLING OF THE PRIVATE INFORMATION EACH USER SHARES WITH TRENDFORCE WHILE VISITING OUR WEBSITES. IF A DIFFERENT PRIVATE POLICY HAS BEEN REFERED TO FOR SPECIFIC TRENDFORCE WEBSITES AND SERVICES, THAT POLICY WILL REPLACE OR SUPPLEMENT THE PRIVACY POLICY MENTIONED IN THIS DOCUMENT. THIS POLICY ALSO COVERS INDIVIDUALS LEGALLY RESIDING IN OR ORGANIZATIONS LEGALLY BASED IN MEMBER COUNTRIES OF THE EUROPEAN UNION (EU) AND ARE SUBJECTED TO EU GENERAL DATA PROTECTION REGULATION (GDPR) WITH REGARD TO PROVISION OF SERVICES AND PERSONAL DATA PROTECTION.

2.1 THE WEBSITE WILL COLLECT AND USE USER INFORMATION FOR PURPOSES SUCH AS MARKETING, CONSUMER PROTECTION, CONSUMER/CLIENT MANAGEMENT, E-COMMERCE SERVICES, FINANCIAL ACCOUNTING, CONTRACTUAL MATTERS, RESEARCH ANALYSIS, AND DATA PROCESSING. WHEN REQUIRED BY LAW, THE WEBSITE MAY ALSO PROVIDE PERSONAL INFORMATION TO NON-GOVERNMENT AGENCIES.

THE WEBSITE WILL NOT DISCLOSE OR SHARE ANY PERSONAL INFORMATION EXCPET PER SPECIAL REQUEST OR WHEN PERMISSION IS RECEIVED FROM THE USER. OTHER EXCEPTIONS INCLUDE:

IN ACCORDANCE WITH ARTICLE 3 OF THE PERSONAL INFORMATION PROTECTION LAW, YOU WILL HAVE THE OPTION TO EXERCISE THE FOLLOWING RIGHTS WITH REGARD TO THE PERSONAL INFORMATION SHARED WITH THE WEBSITE:

a. TO PREVENT UNAUTHORIZED PARTIES FROM ACCESSING, MODIFYING, OR LEAKING PERSONAL USER DATA, THE WEBSITE WILL TAKE STEPS TO IMPLEMENT PROPER SAFETY MEASURES. THE DATA SEARCHED AND RECORDED ON THE WEBSITE AND THE APPROPRIATE SAFETY MEASURES CHOSEN WILL ALL BE REVIEWED CAREFULLY. CONSIDERING HOW THE SAFETY OF TRANSMITTING DATA ON THE INTERNET CAN NEVER BE GUARANTEED COMPLETELY, USERS SHOULD KEEP IN MIND ALL POSSIBLE RISKS ASSOCIATED WITH ONLINE DATA TRANSFERS AND TAKE RESPONSIBILITY FOR ANY INFORMATION SHARED WITH OR OBTAINED FROM THE WEBSITE.

BE SURE TO PROTECT ALL PASSWORDS AND PERSONAL INFORMATION, REFRAIN FROM DISCLOSING PRIVATE USER INFORMATION TO ANY THIRD PARTY, AND REGISTER WITH THE WEBSITE UPON COMPLETING ALL NECESSARY MEMBERSHIP PROCEDURES. WHEN USING A SHARED OR PUBLIC COMPUTER, PLEASE MAKE SURE TO PROPERLY CLOSE ALL RELEVANT BROWSERS TO PREVENT OTHERS FROM READING YOUR PERSONAL E-MAILS OR INFORMATION.

1.1. THE POLICY COVERS THE HANDLING OF THE PRIVATE INFORMATION EACH USER SHARES WITH TRENDFORCE WHILE VISITING OUR WEBSITES. IF A DIFFERENT PRIVATE POLICY HAS BEEN REFERED TO FOR SPECIFIC TRENDFORCE WEBSITES AND SERVICES, THAT POLICY WILL REPLACE OR SUPPLEMENT THE PRIVACY POLICY MENTIONED IN THIS DOCUMENT. THIS POLICY ALSO COVERS INDIVIDUALS LEGALLY RESIDING IN OR ORGANIZATIONS LEGALLY BASED IN MEMBER COUNTRIES OF THE EUROPEAN UNION (EU) AND ARE SUBJECTED TO EU GENERAL DATA PROTECTION REGULATION (GDPR) WITH REGARD TO PROVISION OF SERVICES AND PERSONAL DATA PROTECTION.

2.1 THE WEBSITE WILL COLLECT AND USE USER INFORMATION FOR PURPOSES SUCH AS MARKETING, CONSUMER PROTECTION, CONSUMER/CLIENT MANAGEMENT, E-COMMERCE SERVICES, FINANCIAL ACCOUNTING, CONTRACTUAL MATTERS, RESEARCH ANALYSIS, AND DATA PROCESSING. WHEN REQUIRED BY LAW, THE WEBSITE MAY ALSO PROVIDE PERSONAL INFORMATION TO NON-GOVERNMENT AGENCIES.

THE WEBSITE WILL NOT DISCLOSE OR SHARE ANY PERSONAL INFORMATION EXCPET PER SPECIAL REQUEST OR WHEN PERMISSION IS RECEIVED FROM THE USER. OTHER EXCEPTIONS INCLUDE:

IN ACCORDANCE WITH ARTICLE 3 OF THE PERSONAL INFORMATION PROTECTION LAW, YOU WILL HAVE THE OPTION TO EXERCISE THE FOLLOWING RIGHTS WITH REGARD TO THE PERSONAL INFORMATION SHARED WITH THE WEBSITE:

a. TO PREVENT UNAUTHORIZED PARTIES FROM ACCESSING, MODIFYING, OR LEAKING PERSONAL USER DATA, THE WEBSITE WILL TAKE STEPS TO IMPLEMENT PROPER SAFETY MEASURES. THE DATA SEARCHED AND RECORDED ON THE WEBSITE AND THE APPROPRIATE SAFETY MEASURES CHOSEN WILL ALL BE REVIEWED CAREFULLY. CONSIDERING HOW THE SAFETY OF TRANSMITTING DATA ON THE INTERNET CAN NEVER BE GUARANTEED COMPLETELY, USERS SHOULD KEEP IN MIND ALL POSSIBLE RISKS ASSOCIATED WITH ONLINE DATA TRANSFERS AND TAKE RESPONSIBILITY FOR ANY INFORMATION SHARED WITH OR OBTAINED FROM THE WEBSITE.

BE SURE TO PROTECT ALL PASSWORDS AND PERSONAL INFORMATION, REFRAIN FROM DISCLOSING PRIVATE USER INFORMATION TO ANY THIRD PARTY, AND REGISTER WITH THE WEBSITE UPON COMPLETING ALL NECESSARY MEMBERSHIP PROCEDURES. WHEN USING A SHARED OR PUBLIC COMPUTER, PLEASE MAKE SURE TO PROPERLY CLOSE ALL RELEVANT BROWSERS TO PREVENT OTHERS FROM READING YOUR PERSONAL E-MAILS OR INFORMATION.

According to CINNO Research"s monthly LCD TV LCD panel shipment report, in February 2020, global LCD TV panel shipments were 19.64 million, a 5.1% month-on-month decrease from January 2020 and a 5.6% year-on-year decrease from February 2019. Problems such as tight logistics resources and poor supply chain operation caused by the COVID-19 epidemic were one of the main reasons for the decline in LCD TV shipments in February.

Starting from the end of 2019, LCD TV panel prices gradually stopped falling and began to rebound. Due to the impact of the COVID-19 epidemic on the supply chains of China and South Korea, the tension in panel supply has been further exacerbated in the short term, which has contributed to the rebound in panel prices. On the other hand, as the spread of the international epidemic continues to deteriorate, sports events that were originally considered to be crucial to TV sales such as the Champions League, European Cup, NBA, E3 2020, etc. have been cancelled or postponed, and the Tokyo Olympics also faced serious delays. Risks have added many variables to 2020, and the reduction in demand is expected to be difficult to support the continued increase in panel prices.

As Korean companies gradually withdrew from the LCD TV market, and the new capacity of mainland Chinese manufacturers has gradually achieved success, according to CINNO Research"s monthly LCD TV LCD panel shipment report, in terms of shipments, mainland China panel manufacturers in February 2020, it has accounted for 59.4% of total shipments, close to 60%. TCL CSOT became the world"s largest LCD TV panel supplier for the first time with 18.8% share, BOE ranked second with 17.4% market share, and HKC shipments also grew rapidly, ranking third with 13.4% share, Innolux and Samsung Display SDC ranked 4-5 with 12.3% and 10.5%.

According to CINNO Research"s monthly LCD TV LCD panel shipment report, in terms of shipment area, panel manufacturers in mainland China accounted for 56.6% of the total shipment area. CSOT also won the first place with a share of 19.6%, BOE, Samsung Display SDC, CEC (including Panda, Rainbow), LG Display LGD ranked 18.7%, 12.6%, 10.8% and 10.2% respectively. 2nd to 5th.

SEOUL, April 27 (Reuters) - LG Display Co Ltd (034220.KS) saw first-quarter profit plummet far below forecasts and warned of a further drop in panel prices as pandemic-driven demand for TVs, smartphones and laptops fades and competition heats up.

The South Korean Apple Inc (AAPL.O) supplier said it would shift its focus to higher-end products and gradually lower production of more commoditised LCD TV panels where it lacked a competitive advantage over cheaper Chinese rivals.

The LCD TV market shrank by more than 10% in the first quarter and Chinese competitors are pricing their products lower than LG Display"s expectations, Lee Tai-jong, head of the company"s large display marketing division, said on a call with analysts.

"Margins have been squeezed chiefly due to panel price declines and weaker demand, as consumers have already bought many screens during COVID-19 in the past two years," said Kim Yang-jae, an analyst at DAOL Investment & Securities.

In the first quarter, prices of 55-inch liquid crystal display (LCD) panels for TV sets fell 16% from the previous quarter while prices of LCD panels for notebooks and monitors dropped by around 7% to 11%, according to data from TrendForce"s WitsView.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey