lcd panel manufacturers market share quotation

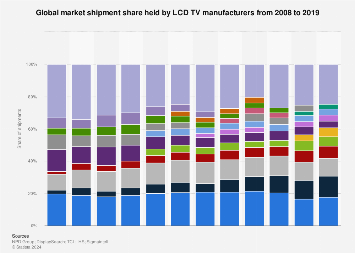

The global LCD TV (Liquid Crystal Display Television) market was dominated by Samsung and remained so in 2021 with a market share of over 19 percent by sales volume. LG Electronics takes second place with close to 13 percent in the same year, to beat TLC, one of the well-established brands in this segment.Read moreMarket share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volumeCharacteristic202120202019----

TCL. (March 11, 2022). Market share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volume [Graph]. In Statista. Retrieved January 02, 2023, from https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/

TCL. "Market share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volume." Chart. March 11, 2022. Statista. Accessed January 02, 2023. https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/

TCL. (2022). Market share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volume. Statista. Statista Inc.. Accessed: January 02, 2023. https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/

TCL. "Market Share of Leading Lcd Tv Manufacturers Worldwide from 2019 to 2021, by Sales Volume." Statista, Statista Inc., 11 Mar 2022, https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/

TCL, Market share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volume Statista, https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/ (last visited January 02, 2023)

In 2019 and 2020, BOE was the leading manufacturer in the monitor display panel market, holding 25 and 26 percent of the market, respectively. LG Display, the South Korean panel maker, ranked second, with a 21 percent share. The market share of another South Korean company, Samsung Display, was forecast to drop to one percent in 2021.Read moreMonitor display panel market share worldwide from 2019 to 2021, by supplierCharacteristicLGDBOESDCINXAUOCECCSOTHKC---------

TrendForce. (January 11, 2021). Monitor display panel market share worldwide from 2019 to 2021, by supplier [Graph]. In Statista. Retrieved January 02, 2023, from https://www.statista.com/statistics/1124858/global-display-panel-vendor-monitor/

TrendForce. "Monitor display panel market share worldwide from 2019 to 2021, by supplier." Chart. January 11, 2021. Statista. Accessed January 02, 2023. https://www.statista.com/statistics/1124858/global-display-panel-vendor-monitor/

TrendForce. (2021). Monitor display panel market share worldwide from 2019 to 2021, by supplier. Statista. Statista Inc.. Accessed: January 02, 2023. https://www.statista.com/statistics/1124858/global-display-panel-vendor-monitor/

TrendForce. "Monitor Display Panel Market Share Worldwide from 2019 to 2021, by Supplier." Statista, Statista Inc., 11 Jan 2021, https://www.statista.com/statistics/1124858/global-display-panel-vendor-monitor/

TrendForce, Monitor display panel market share worldwide from 2019 to 2021, by supplier Statista, https://www.statista.com/statistics/1124858/global-display-panel-vendor-monitor/ (last visited January 02, 2023)

LCD TV Panel Market Size is projected to Reach Multimillion USD by 2027, In comparison to 2021, at unexpected CAGR during the Forecast Period 2022-2028.

Considering the economic change due to COVID-19 and Russia-Ukraine War Influence, LCD TV Panel accounted for % of the global market of LCD TV Panel in 2022.

This LCD TV Panel Market Report offers analysis and insights based on original consultations with important players such as CEOs, Managers, Department Heads of Suppliers, Manufacturers, Distributors, etc.

The Global LCD TV Panel Market is anticipated to rise at a considerable rate during the forecast period, between 2022 and 2027. In 2021, the market is growing at a steady rate and with the rising adoption of strategies by key players, the market is expected to rise over the projected horizon.

LCD displays utilize two sheets of polarizing material with a liquid crystal solution between them. An electric current passed through the liquid causes the crystals to align so that light cannot pass through them. Each crystal, therefore, is like a shutter, either allowing light to pass through or blocking the light. LCD panel is the key components of LCD display. And the price trends of LCD panel directly affect the price of liquid crystal displays. LCD panel consists of several components: Glass substrate, drive electronics, polarizers, color filters etc. Only LCD panel applied for TV will be counted in this report

Samsung Display, LG Display, Innolux Crop and AUO captured the top four revenue share spots in the LCD TV Panel market in 2015. Samsung Display dominated with 22.11 percent revenue share, followed by LG Display with 19.72 percent revenue share and Innolux Crop Display with 19.30 percent revenue share.

The global LCD TV Panel market is valued at USD 51130 million in 2019. The market size will reach USD 59640 million by the end of 2026, growing at a CAGR of 2.2% during 2021-2026.

LCD TV Panel market is segmented by Size, and by Application. Players, stakeholders, and other participants in the global LCD TV Panel market will be able to gain the upper hand as they use the report as a powerful resource. The segmental analysis focuses on production capacity, revenue and forecast by Size and by Application for the period 2016-2027.

The report focuses on the LCD TV Panel market size, segment size (mainly covering product type, application, and geography), competitor landscape, recent status, and development trends. The report considers key geographic segments and describes all the favorable conditions driving the market growth.

On the basis of the End Users/Applications, this report focuses on the status and outlook for major applications/end users, consumption (sales), market share, and growth rate for each application, including:

Geographically, the Major Regions Covered in LCD TV Panel Market Report Are:To comprehend LCD TV Panel market dynamics across major global regions. ● North America(United States, Canada)

Market is changing rapidly with the ongoing expansion of the industry. Advancement in technology has provided today’s businesses with multifaceted advantages resulting in daily economic shifts. Thus, it is very important for a company to comprehend the patterns of market movements in order to strategize better. An efficient strategy offers the companies a head start in planning and an edge over the competitors.Industry Researchis a credible source for gaining the market reports that will provide you with the lead your business needs.

Is there a problem with this press release? Contact the source provider Comtex at editorial@comtex.com. You can also contact MarketWatch Customer Service via our Customer Center.

LCD TV Panel Market Research Report is spread wide in terms of pages and provides exclusive data, information, vital statistics with tables and figures, trends, and competitive landscape details in this niche sector.

The outbreak of COVID-19 has severely impacted the overall supply chain of the LCD TV Panel market. The halt in production and end use sector operations have affected the LCD TV Panel market. The pandemic has affected the overall growth of the industry In 2020 and at the start of 2021, Sudden outbreak of the COVID-19 pandemic had led to the implementation of stringent lockdown regulations across several nations resulting in disruptions in import and export activities of LCD TV Panel.

COVID-19 can affect the global economy in three main ways: by directly affecting production and demand, by creating supply chain and market disruption, and by its financial impact on firms and financial markets. Our analysts monitoring the situation across the globe explains that the market will generate remunerative prospects for producers post COVID-19 crisis. The report aims to provide an additional illustration of the latest scenario, economic slowdown, and COVID-19 impact on the overall industry.

Considering the economic change due to COVID-19 and Russia-Ukraine War Influence, LCD TV Panel, which accounted for % of the global market of LCD TV Panel in 2021

The report covers the major players operating in the LCD TV Panel market. In terms of market share, the companies in the global LCD TV Panel market do not have a considerable amount of market share, as the market is highly competitive and fragmented.

The Global LCD TV Panel Market is anticipated to rise at a considerable rate during the forecast period, between 2022 and 2028. In 2020, the market is growing at a steady rate and with the rising adoption of strategies by key players, the market is expected to rise over the projected horizon.

This report focuses on global and United States LCD TV Panel market, also covers the segmentation data of other regions in regional level and county level.

Due to the COVID-19 pandemic, the global LCD TV Panel market size is estimated to be worth USD million in 2022 and is forecast to a readjusted size of USD million by 2028 with a Impressive CAGR during the review period. Fully considering the economic change by this health crisis, by Type, LCD TV Panel accounting for % of the LCD TV Panel global market in 2021, is projected to value USD million by 2028, growing at a revised % CAGR in the post-COVID-19 period. While by Application, LCD TV Panel was the leading segment, accounting for over percent market share in 2021, and altered to an % CAGR throughout this forecast period.

The global LCD TV Panel market is projected to reach USD million by 2028 from an estimated USD million in 2022, at a magnificent CAGR during 2023 and 2028.

This report aims to provide a comprehensive presentation of the global market for LCD TV Panel, with both quantitative and qualitative analysis, to help readers develop business/growth strategies, assess the market competitive situation, analyze their position in the current marketplace, and make informed business decisions regarding LCD TV Panel.

The LCD TV Panel market size, estimations, and forecasts are provided in terms of output/shipments (K Units) and revenue (USD millions), considering 2021 as the base year, with history and forecast data for the period from 2017 to 2028. This report segments the global LCD TV Panel market comprehensively. Regional market sizes, concerning products by types, by application, and by players, are also provided. The influence of COVID-19 and the Russia-Ukraine War were considered while estimating market sizes.

For a more in-depth understanding of the market, the report provides profiles of the competitive landscape, key competitors, and their respective market ranks. The report also discusses technological trends and new product developments.

The report will help the LCD TV Panel manufacturers, new entrants, and industry chain related companies in this market with information on the revenues, production, and average price for the overall market and the sub-segments across the different segments, by company, product type, application, and regions.

In this section, the readers will gain an understanding of the key players competing. This report has studied the key growth strategies, such as innovative trends and developments, intensification of product portfolio, mergers and acquisitions, collaborations, new product innovation, and geographical expansion, undertaken by these participants to maintain their presence. Apart from business strategies, the study includes current developments and key financials. The readers will also get access to the data related to global revenue, price, and sales by manufacturers for the period 2017-2022. This all-inclusive report will certainly serve the clients to stay updated and make effective decisions in their businesses.

LCD TV Panel Market 2022 is segmented as per type of product and application. Each segment is carefully analyzed for exploring its market potential. All of the segments are studied in detail on the basis of market size, CAGR, market share, consumption, revenue and other vital factors.

This LCD TV Panel Market Research/Analysis Report Contains Answers to your following Questions ● What are the global trends in the LCD TV Panel market? Would the market witness an increase or decline in the demand in the coming years?

● What is the estimated demand for different types of products in LCD TV Panel? What are the upcoming industry applications and trends for LCD TV Panel market?

● What Are Projections of Global LCD TV Panel Industry Considering Capacity, Production and Production Value? What Will Be the Estimation of Cost and Profit? What Will Be Market Share, Supply and Consumption? What about Import and Export?

● How big is the opportunity for the LCD TV Panel market? How will the increasing adoption of LCD TV Panel for mining impact the growth rate of the overall market?

Our research analysts will help you to get customized details for your report, which can be modified in terms of a specific region, application or any statistical details. In addition, we are always willing to comply with the study, which triangulated with your own data to make the market research more comprehensive in your perspective.

360 Research Reports is the credible source for gaining the market reports that will provide you with the lead your business needs. At 360 Research Reports, our objective is providing a platform for many top-notch market research firms worldwide to publish their research reports, as well as helping the decision makers in finding most suitable market research solutions under one roof. Our aim is to provide the best solution that matches the exact customer requirements. This drives us to provide you with custom or syndicated research reports.

Is there a problem with this press release? Contact the source provider Comtex at editorial@comtex.com. You can also contact MarketWatch Customer Service via our Customer Center.

The Liquid Crystal Display (LCD)-enabled electronic devices, such as television, mobile phones and others, is creating potential opportunities for the LCD panel market. In the past couple of years, LCD panels have gained popularity owing to their advanced properties that include less power consumption, compact size and low price.

Moreover, over the past two decades, the LCD technology of has made impressive progress. The electronic displays available at present make use of a wide variety of active LCD panels. The LCD panel market is one of the significantly growing markets due to the increasing demand for LCD displays & low power consumption electronic goods, as well as increase in the demand for touch-enabled displays.

An LCD panel is designed to project on-screen information. At present, LCD panels are suited with high-mobility electronic equipment. LCDs with improved video quality are gaining momentum in all developed and developing economies. These factors are projected to propel the global LCD panel market.

The major growth drivers of the LCD panel market include an increase in the demand for energy-efficient electronic products as well as for larger and 4K televisions. Furthermore, growth in the demand for energy-efficient electronic devices is surging the global LCD panel market.

Demand for high-quality screens, coupled with improving standards of living and inflating disposable income, are among key factors boosting the LCD Panel market. In addition, increase in the adoption of consumer electronic devices is projected to drive the global LCD panel market.

However, one of the major challenges of the LCD panel market are the higher cost and thickness of the display of these devices as compared to other modules. The LCD panel market is expected to witness sluggish and unpredictable growth owing to a quantitative decline in the number of LCD displays.

Moreover, financial uncertainty and macroeconomic situations around the world, such as fluctuating currency exchange rates and economic difficulties, are some of the major factors hindering the growth of the LCD panel market. However, increased competition from alternative technologies and LCD panel complex structure is likely to limit the growth of the LCD panel market.

At present, North America holds the largest market share for the LCD panel market due an increase in the demand for consumer electronic devices. Due to the presence of key LCD panel manufacturers in China and Japan, Asia Pacific is expected to become the prominent region for the LCD panel market.

In addition, the unorganized market of LCD panels in China, Japan and India is creating a competitive environment for global LCD panel manufacturers. Moreover, Europe is the fastest-growing market for LCD panels due to an increase in the adoption of consumer electronics devices. The demand for LCD panels has risen dramatically over the past 12 months globally. The usage of LCD displays in various industries in these regions is boosting the LCD panel market.

The report is a compilation of first-hand information, qualitative and quantitative assessment by industry analysts, inputs from industry experts and industry participants across the value chain. The report provides in-depth analysis of parent market trends, macro-economic indicators and governing factors along with market attractiveness as per segments. The report also maps the qualitative impact of various market factors on market segments and geographies.

Due to an increase in the demand for large LCD displays, the large size LCD panel sub-segment is expected to register double-digit growth rate in the global market. In addition, due to an increase in the demand for portable electronic devices, the small size LCD panel sub-segment is projected to be the most attractive market sub-segment of the global LCD panel market.

The smart phones and tablets sub-segment held the largest market share for the LDC panel market in 2017, and the wearable devices sub-segment is expected to grow with a high CAGR during the forecast period.

The upstream materials or components of the LCD panel industry mainly include liquid crystal materials, glass substrates, polarizing lenses, and backlight LEDs (or CCFL, which accounts for less than 5% of the market).

The middle reaches is the main panel factory processing and manufacturing, through the glass substrate TFT arrays and CF substrate, CF as upper and TFT self-built perfusion liquid crystal and the lower joint, and then put a polaroid, connection driver IC and control circuit board, and a backlight module assembling, eventually forming the whole piece of LCD module. The downstream is a variety of fields of application terminal-based brand, assembly manufacturers. At present, the United States, Japan, and Germany mainly focus on upstream raw materials, while South Korea, Taiwan, and the mainland mainly seek development in mid-stream panel manufacturing.

With the successive production of the high generation line in mainland China, the panel production capacity and technology level have been steadily improved, and the industrial competitiveness has been gradually enhanced. Nowadays, the panel industry is divided into three parts: South Korea, mainland China, and Taiwan, and mainland China is expected to become the no.1 in the world in 2019.

In the past decade, China’s panel display industryhas achieved leapfrog development, and the overall size of the industry has ranked among the top three in the world. Chinese mainland panel production capacity is expanding rapidly, although Japanese panel manufacturers master a large number of key technologies, gradually lose the price competitive advantage, compression panel production capacity. Panel production is concentrated in South Korea, Taiwan, and China, which is poised to become the world’s largest producer of LCD panels.

Up to 2016, BOE‘s global market share continued to increase: smartphone LCD, tablet PC display, and laptop display accounted for the world’s first market share, and display screen increased to the world’s second, while TV LCD remained the world’s third. In LCD TV panels, Chinese panel makers have accounted for 30 percent of global shipments to 77 million units, surpassing Taiwan’s 25.5 percent market share for the first time and ranking second only to South Korea.

In terms of the area of shipment, the area of board shipment of JD accounted for only 8.3% in 2015, which has been greatly increased to 13.6% in the first half of 2016, while the area of shipment of hu xing optoelectronics in the first half of 2015 was only 5.1%, which has reached 7.8% in the first half of 2016. The panel factories in mainland China are expanding their capacity at an average rate of double-digit growth and transforming it into actual shipments and areas of shipment. On the other hand, although the market share of South Korea, Japan, and Taiwan is gradually decreasing, some South Korean and Japanese manufacturers have been inclined to the large-size HD panel and AMOLED market, and the production capacity of the high-end LCD panel is further concentrated in mainland China.

Domestic LCD panel production line capacity gradually released, overlay the decline in global economic growth, lead to panel makers from 15 in the second half began, in a low profit or loss, especially small and medium-sized production line, the South Korean manufacturers take the lead in transformation strategy, closed in medium and small size panel production line, South Korea’s 19-panel production line has shut down nine, and part of the production line is to research and development purposes. Some production lines are converted to LTPS production lines through process conversion. Korean manufacturers are turning to OLED panels in a comprehensive way, while Japanese manufacturers are basically giving up the LCD panel manufacturing business and turning to the core equipment and materials side. In addition to the technical direction of the research and judgment, more is the LCD panel business orders and profits have been severely compressed, Korean and Japanese manufacturers have no desire to fight. Since many OLED technologies are still in their infancy in mainland China, it is a priority to move to high-end panels such as OLED as soon as possible. Taiwanese manufacturers have not shut down factories on a large scale, but their advantages in LCD technology and OLED technology have been slowly eroded by the mainland.

STONE provides a full range of 3.5 inches to 15.1 inches of small and medium-size standard quasi TFT LCD module, LCD display, TFT display module, display industry, industrial LCD screen, under the sunlight visually highlight TFT LCD display, industrial custom TFT screen, TFT LCD screen-wide temperature, industrial TFT LCD screen, touch screen industry. The TFT LCD module is very suitable for industrial control equipment, medical instruments, POS system, electronic consumer products, vehicles, and other products.STONE provides a full range of 3.5 inches to 15.1 inches of small and medium-size standard quasi TFT LCD module, LCD display, TFT display module, display industry, industrial LCD screen, under the sunlight visually highlight TFT LCD display, industrial custom TFT screen, TFT LCD screen-wide temperature, industrial TFT LCD screen, touch screen industry. The TFT LCD module is very suitable for industrial control equipment, medical instruments, POS system, electronic consumer products, vehicles, and other products.

In terms of the current mainstream display market, common display technologies include LCD (liquid crystal display), organic light-emitting diode displays (OLED), electrophoretic displays, and the emerging MicroLED (micro light-emitting diode) display technology, etc., a variety of display technologies have unique characteristics and application areas. Among them, LCD and OLED is currently the most widely used technology, electrophoretic displays are mainly used in the field of reading, and micro light-emitting diode display technology has many problems have not been solved.

LCD, also known as liquid crystal display, the mainstream technology is TFT-LCD, consisting of two parallel glass substrates on the top and bottom and the liquid crystal box between the polar plates, LCD’s upper substrate is set with a color filter, the lower substrate is equipped with a thin film transistor (TFT). oled, also known as organic light emitting diode, OLED display can be divided into active (AMOLED) and passive (PMOLED) according to the driving method. AMOLED is different from LCD in that AMOLED can achieve self-illumination, so there is no need for additional backlight modules.

Among the many downstream applications, the main application areas of LCD and OLED are relatively different. TFT-LCD accounts for the largest application area is TV, accounting for 67%, followed by display, accounting for 13%, cell phones, commercial LCD, computer and automotive accounted for 3%, 5%, 4%, 1% respectively. OLED is currently relatively small in average size, the largest application area is smart phones, accounting for 69%, followed by wearable devices and household appliances and TV, accounting for 10%, 8% respectively. 69%, followed by wearable devices and household appliances and TVs, accounting for 10% and 8% respectively.

The Daily Beast captures that the concept of display represented by OLED has been very active in the capital market recently, and this article will give you an overview of this emerging technology field.

The LCD panel industry chain is divided into upstream materials, such as glass substrates, color filters, driver ICs, polarizers, liquid crystals, etc.; midstream assembly is power management, control ICs, LCD panels (arrays, into boxes, modules); downstream is TVs, smartphones, notebooks and other user-oriented end products, and we will focus our discussion on midstream manufacturers.

The upstream area of the semiconductor display industry has high technical barriers and industry concentration, and some products are more dependent on foreign suppliers. At present, the world can provide glass substrates on a large scale manufacturers are mainly U.S. companies Corning, Japanese companies Asahi Glass, Electric Glass and Anhan Vision Special, China’s domestic supply of glass substrates is insufficient, still need to import a large number of. Color filters, polarizers, liquid crystal materials, driver IC and organic light-emitting materials supply is also mainly concentrated in a few foreign manufacturers.

In 2019, the global display industry output value is about $197.2 billion, of which the global share of China’s display device (panel) output value is about 37%, while the global share of upstream materials is only 15%, and the global share of upstream equipment is only 6%. .

Midstream manufacturers are the most important part of the display panel industry production, the current panel manufacturers are mainly from mainland China, Taiwan, Japan and South Korea. In addition to the traditional strong Japanese and Korean companies and the earlier emergence of Chinese companies in Taiwan, the Chinese mainland companies are also catching up. At present, there are two very obvious trends in the industry, firstly, the manufacturers are gradually upgrading the production capacity of large size TFT-LCD, already excess capacity of small and medium size gradually cut, secondly, with the OLED display technology in cell phones and high-end TV penetration rate is increasing, the major manufacturers are actively expanding OLED panel production capacity, including BOE, Huaxing photoelectric, deep Tianma, Wearnes, etc. The expansion of mainland Chinese manufacturers is particularly significant. According to IHSMarkit’s estimates, by 2022, the share of South Korean panel makers in global AMOLED production capacity will fall from 93% in 2017 to 71%, while the market share of Chinese manufacturers will increase from 5% in 2017 to 26% in 2022.

As smartphones continue to grow in popularity, the market dividend of OLED is obvious, and the market share of OLED in smartphone touch panels is expected to reach 37.7% in 2020. As a third-generation display technology, OLED is in a rapid growth period, and its application market is mainly to replace LCD. The penetration rate of OLED is directly related to its cost, which in turn is directly related to production yields. In addition, in terms of TV panels, OLED has become synonymous with high-end TV products.

At present, the manufacturing cost of 55-inch UHDOLED is 2.5 times that of LCD panels, if the defect rate can be controlled below 10%, then the price difference can be further reduced to 1.8 times, that is, at present, LCD panels in large size TV applications still have a higher cost competitive advantage.

Display panel industry chain downstream is mainly Huawei, HP, Dell, Samsung, Sony, LG, Lenovo, Hisense and other global first-line consumer electronics brands, not much to mention here.

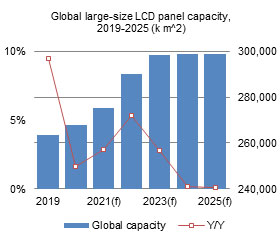

According to CINNORearch’s research, the global LCD panel production line, China panel factory capacity area share will be 54% in 2019, further increase to 63% in 2020, South Korea panel factory market share will slide to less than 20%.

For foreign competitors, Japanese companies Panasonic and Sharp performance is not outstanding, the main competitors of domestic manufacturers for South Korean companies Samsung and LGD. while Samsung and LGD are gradually withdrawing from LCD production capacity, LCD panel revenue in 2019 declined, at the same time, BOE, Huaxing photoelectric and deep Tianma TFT-LCD operating income is to maintain the upward trend. From the perspective of competition level, in the layout of large size TFT-LCD production line, the domestic BOE, Huaxing, Huike, etc. are in the leading position.

In the OLED field, Samsung is the only one in the world and is the deserved leader. As the second largest producer of cell phones in the world, Samsung’s self-sufficient panel supply still dominates the market. According to the 2019 global OLED panel shipment ranking released by Group Intelligence Consulting, Samsung Display, BOE, and Hophitsu Display shipments ranked among the top three globally, with Samsung topping the list with a market share of 85.4%. Domestic manufacturers in addition to BOE, and Hui Optoelectronics, Wearnes and Shen Tianma’s performance is also relatively good.

The domestic companies focus on BOE, which shipped a total of 39.1 million OLED panels in 2019. Among them, rigid displays amounted to 22.1 million units and flexible displays were 17 million units. Compared with 2018, the company’s rigid panel shipments grew by 12 times, while the growth of flexible panel shipments was more than four times. BOE is actively laying out high-generation production lines, and has independently planned and built 15 semiconductor display device production lines in multiple locations across the country, with products covering the full size of TFT-LCD, as well as AMOLED and MicroOLED and other technology types. If we simply look at the competitive strength, in TFT-LCD, BOE is gradually replacing the production capacity of Samsung and LG, and further achieve the leading position, while in OLED manufacturing and South Korean companies Samsung gap, in addition, BOE in the global OLED production line layout is still in a relatively leading position.

In addition, with the continuous expansion of domestic display panel production capacity, related local manufacturing equipment companies are also beginning to rise, in the field of laser, testing equipment and assembly equipment there are a number of local listed companies are forming their own technical advantages, but in some high-end equipment, local companies have obvious shortcomings. In the panel detection link, precision measurement electronics has grown into a leading domestic panel detection equipment, products covering LCD, OLED and other types of flat panel display devices, but the need to objectively recognize that the highest barriers Array section detection equipment is still basically monopolized by foreign and Taiwan manufacturers. Domestic OLED production line in the high-end laser equipment is still dominated by Korean companies, Grand Nation Laser and other local laser equipment companies continue to invest in research and development, in the field of laser cutting, laser repair, laser stripping and other equipment has penetrated into the domestic panel manufacturers production line, but in the field of ELA equipment with the highest technical content, the market is basically APSystems, Terasemicon, Viatron Three Korean companies occupy.

To sum up, the world’s mainstream manufacturers are accelerating the development and production of OLED, and in this field to Samsung as the absolute leader, the most competitive domestic enterprises is BOE, small and medium-sized LCD panels are being replaced, large size LCD by virtue of cost advantage to participate in the market competition, BOE as the representative of local enterprises in this field does not fall behind.

Westford, USA, Sept. 27, 2022 (GLOBE NEWSWIRE) -- 4K Display Market has become extremely popular in recent years, as users have come to appreciate their high-resolution quality. 4K displays offer a much higher resolution than the current mainstream displays, which is why they are so appealing to consumers. Today, 4K displays are not just for TV, Desktop and Laptop usage anymore. Companies are now starting to install 4K displays in their Commercial Locations such as Hospitals, Schools, and Airports. Manufacturers are also producing them in large quantity and selling them at an exponential rate.

The growing demand for 4K display market is raising expectations about the next big thing in display technology. With improvements in resolution and color, 4K displays are already transforming how we view content. With prices dropping and more content being created in 4K, the demand for these screens only continues to grow.

Currently, 2160p (4K) displays are dominant in the 4K display market. But this is only the beginning—as technology improves, SkyQuest’s analyst predict that UHD (3840x2160) displays will become prevalent by 2020.

Why are 4K Displays So Effective? There are many benefits of using 4K displays over traditional displays: - They Offer Higher Resolution: When it comes to resolution, 4K Displays consistently deliver smoother lines and sharper pictures than traditional displays. This means that graphics and images look smoother and more realistic than ever before in the 4K display market.

Global shipments of 4K display were totaled at 127.4 million units in 2021 and is projected to reach 405 million by 2028. Moreover, OLED and QLED TV shipments continue to dominate with a share of above 58%. The global 4K display market revenue is forecast to grow at a CAGR of 23.20% through 2028.

In terms of application areas, gaming continues to be an early adopter of 4K displays with gaming mic and headsets releasing in Q4/2021 with more devices set to release in 2022. In addition, commercial buildings are starting to upgrade their signage systems from HD to 4K for added clarity and detail especially for high dynamic range (HDR) content, which is projected to add fuel to the growth of the 4K display market.

These findings in the 4K display market confirm that 4KTV is becoming the must-have television technology for enthusiasts who want the best possible images. However, it is not just ultra-high-definition televisions that are gaining popularity among consumers; Our research shows that sales of 3D TVs are growing as well. In fact, we expect 4K 3DTV penetration to reach 50% by 2025, up from just 44% at present. This is due to the increasing popularity of premium viewing platforms such as Netflix, Hulu, and Amazon Prime Video that support 4K content.

4K displays are becoming increasingly popular as consumers in the 4K display market become more demanding for better picture quality. This is especially true for video and gaming as 4K offers a sharper image than traditional HD displays.

The top five global brands in the 4K display market namely Samsung, Sony, Hisense, TCL, and LG are holding over 55% share of the global 4K display market. With Samsung leading the pack with a market share of over 19%. The top three global brands generated revenues that were greater than their combined total from 2018–2021.

In addition to QLEDs, Samsung, a largest player in 4K display market, also offers other types of 4K displays, including quoted LCD panels and WQHD+ AMOLED panels. But QLEDs continue to dominate the market because they can offer “significantly higher resolution and brightness levels as well as better color performance than any other type of panel.”

It seems like Korean brands are dominating not only in terms of sales but also in terms of R&D and innovation in the 4K display market. We will have to see how this competitive landscape will shift in coming years as newer brands are launching their products in the market.

SkyQuest Technology is leading growth consulting firm providing market intelligence, commercialization and technology services. It has 450+ happy clients globally.

Thanks to TV manufacturers’ aggressive procurement activities, global TV panel shipment for 1H21 reached 135.2 million pcs, a 3.5% YoY increase, according to TrendForce’s latest investigations. Notably, high-end OLED TV panels and 8K LCD TV panels showed diametrically opposed movements. The former product category reached a 2.6% market share in 1H21 (with room for further growth going forward) due to LGD’s capacity expansion as well as the narrowing gap between OLED panel prices and LCD panel prices. On the other hand, the latter’s market share fell to a mere 0.2% in 1H21 as panel suppliers were generally reluctant to manufacture 8K LCD TV panels due to these panels’ poor yield rates.

TrendForce’s findings indicate that Chinese panel suppliers were able to achieve a 58.3% share in the TV panel market, which was nearly 5 percentage points higher than their 1H20 market share, thanks to their growing number of production lines. Conversely, Taiwanese suppliers saw their market share drop by 2.2 percentage points from 1H20 levels to 21.1% in 1H21. This decline took place because of their limited production capacities and because they reallocated some of their production capacities for TV panels to IT products instead. Korean suppliers likewise experienced a decline in market share to 14.3% after SDC shuttered its Korea-based LCD fabs L7-2 and L8-1-2 and sold its Suzhou-based Gen 8.5 fab to CSOT. Finally, Japanese suppliers’ market shares increased to 6.3% as a result of SDPC’s Gen 10.5 capacity expansion.

Regarding OLED TV panels, which are relatively high-end products, it should be pointed out that LGD is the sole supplier of these panels. Not only did LGD expand the production capacity of its Guangzhou-based OLED panel fab, but LGD’s clients in the TV sector were also increasingly willing to procure OLED panels in light of the narrowing gap between OLED panel prices and LCD panel prices. Hence, the penetration rate of OLED panels in the TV panel market grew to 2.6% in 1H21, with about 3.556 million pcs shipped throughout the period. Furthermore, now that the Guangzhou fab’s OLED panel capacity reached 90k sheets/month in 2Q21, TrendForce expects annual OLED TV panel shipment for 2021 to reach 8 million pcs, with a 3% penetration rate in the overall TV panel market.

On the other hand, 8K LCD TV panels reached a mere 0.2% penetration rate in the TV panel market in 1H21 because panel suppliers’ concerns about profit and yield maximization resulted in their relatively low willingness to manufacture these products. On the demand side, clients were also unwilling to procure these panels due to persistently high quotes from suppliers. With regards to panel suppliers, CSOT in particular benefitted from the unique structure of its client base, which allowed it to dominate more than half of the 8K LCD TV panel market, with AUO taking second place. The respective market shares of CSOT and AUO currently sit at 54.4% and 22.6%. TrendForce forecasts a 0.2% penetration rate for 8K LCD TV panels for 2021 as the growth of these products is constrained by their relatively high prices and the current paucity of 8K content.

For more information on reports and market data from TrendForce’s Department of Display Research, please clickhere, or email Ms. Vivie Liu from the Sales Department atvivieliu@trendforce.com

According to TrendForce, LCD TV panel quotations bore the brunt of continuous downgrades in the purchase volume of TV brands and pricing for most panel sizes have fallen to record lows. Recently, it was announced that the 32-inch and 43-inch panels fell by approximately US$5~US$6 in early June, 55-inch panels fell approximately US$7, and 65-inch and 75-inch panels are also facing overcapacity pressure, down US$12 to US$14. In order to alleviate pressure caused by price decline and inventory, panel makers are successively planning to initiate more significant production control in 3Q22. According to TrendForce’s latest research, overall LCD TV panel production capacity in 3Q22 will be reduced by 12% compared with original planning.

As Chinese panel makers account for nearly 66% of TV panel shipments, BOE, CSOT, and HKC are industry leaders. When there is an imbalance in supply and demand, a focus on strategic direction is prioritized. According to TrendForce, TV panel production capacity of the three aforementioned companies in 3Q22 is expected to decrease by 15.8% compared with their original planning, and 2% compared with 2Q22. Taiwanese manufacturers account for nearly 20% of TV panel shipments so, under pressure from falling prices, allocation of production capacity is subject to dynamic adjustment. On the other hand, Korean factories have gradually shifted their focus to high-end products such as OLED, QDOLED, and QLED, and are backed by their own brands. However, in the face of continuing price drops, they too must maintain operations amenable to flexible production capacity adjustments.

TrendForce indicates, in order to reflect real demand, Chinese panel makers have successively reduced production capacity. However, facing a situation in which terminal demand has not improved, it may be difficult to reverse the decline of panel pricing in June. However, as TV sizes below 55 inches (inclusive) have fallen below their cash cost in May (which is seen as the last line of defense for panel makers) and is even flirting with the cost of materials, coupled with production capacity reduction from panel makers, the price of TV panels has a chance to bottom out at the end of June and be flat in July. However, demand for large sizes above 65 inches (inclusive) originates primarily from Korean brands. Due to weak terminal demand, TV brands revising their shipment targets for this year downward, and purchase volume in 3Q22 being significantly cut down, it is difficult to see a bottom for large-size panel pricing. TrendForce expects that, optimistically, this price decline may begin to dissipate month by month starting in June but supply has yet to reach equilibrium, so the price of large sizes above 65 inches (inclusive) will continue to decline in 3Q22.

TrendForce states, as panel makers plan to reduce production significantly, the price of TV panels below 55 inches (inclusive) is expected to remain flat in 3Q22. However, panel manufacturers cutting production in the traditional peak season also means that a disappointing 2H22 peak season is a foregone conclusion and it will not be easy for panel prices to reverse. However, it cannot be ruled out, as operating pressure grows, the number and scale of manufacturers participating in production reduction will expand further and it timeframe extended, enacting more effective suppression on the supply side, so as to accumulate greater momentum for a rebound in TV panel quotations.

For more information on reports and market data from TrendForce’s Department of Display Research, please click here, or email Ms. Vivie Liu from the Sales Department at vivieliu@trendforce.com

1.1. THE POLICY COVERS THE HANDLING OF THE PRIVATE INFORMATION EACH USER SHARES WITH TRENDFORCE WHILE VISITING OUR WEBSITES. IF A DIFFERENT PRIVATE POLICY HAS BEEN REFERED TO FOR SPECIFIC TRENDFORCE WEBSITES AND SERVICES, THAT POLICY WILL REPLACE OR SUPPLEMENT THE PRIVACY POLICY MENTIONED IN THIS DOCUMENT. THIS POLICY ALSO COVERS INDIVIDUALS LEGALLY RESIDING IN OR ORGANIZATIONS LEGALLY BASED IN MEMBER COUNTRIES OF THE EUROPEAN UNION (EU) AND ARE SUBJECTED TO EU GENERAL DATA PROTECTION REGULATION (GDPR) WITH REGARD TO PROVISION OF SERVICES AND PERSONAL DATA PROTECTION.

2.1 THE WEBSITE WILL COLLECT AND USE USER INFORMATION FOR PURPOSES SUCH AS MARKETING, CONSUMER PROTECTION, CONSUMER/CLIENT MANAGEMENT, E-COMMERCE SERVICES, FINANCIAL ACCOUNTING, CONTRACTUAL MATTERS, RESEARCH ANALYSIS, AND DATA PROCESSING. WHEN REQUIRED BY LAW, THE WEBSITE MAY ALSO PROVIDE PERSONAL INFORMATION TO NON-GOVERNMENT AGENCIES.

THE WEBSITE WILL NOT DISCLOSE OR SHARE ANY PERSONAL INFORMATION EXCPET PER SPECIAL REQUEST OR WHEN PERMISSION IS RECEIVED FROM THE USER. OTHER EXCEPTIONS INCLUDE:

IN ACCORDANCE WITH ARTICLE 3 OF THE PERSONAL INFORMATION PROTECTION LAW, YOU WILL HAVE THE OPTION TO EXERCISE THE FOLLOWING RIGHTS WITH REGARD TO THE PERSONAL INFORMATION SHARED WITH THE WEBSITE:

a. TO PREVENT UNAUTHORIZED PARTIES FROM ACCESSING, MODIFYING, OR LEAKING PERSONAL USER DATA, THE WEBSITE WILL TAKE STEPS TO IMPLEMENT PROPER SAFETY MEASURES. THE DATA SEARCHED AND RECORDED ON THE WEBSITE AND THE APPROPRIATE SAFETY MEASURES CHOSEN WILL ALL BE REVIEWED CAREFULLY. CONSIDERING HOW THE SAFETY OF TRANSMITTING DATA ON THE INTERNET CAN NEVER BE GUARANTEED COMPLETELY, USERS SHOULD KEEP IN MIND ALL POSSIBLE RISKS ASSOCIATED WITH ONLINE DATA TRANSFERS AND TAKE RESPONSIBILITY FOR ANY INFORMATION SHARED WITH OR OBTAINED FROM THE WEBSITE.

BE SURE TO PROTECT ALL PASSWORDS AND PERSONAL INFORMATION, REFRAIN FROM DISCLOSING PRIVATE USER INFORMATION TO ANY THIRD PARTY, AND REGISTER WITH THE WEBSITE UPON COMPLETING ALL NECESSARY MEMBERSHIP PROCEDURES. WHEN USING A SHARED OR PUBLIC COMPUTER, PLEASE MAKE SURE TO PROPERLY CLOSE ALL RELEVANT BROWSERS TO PREVENT OTHERS FROM READING YOUR PERSONAL E-MAILS OR INFORMATION.

LCD panel prices are poised to stabilize in January 2023 despite the ongoing inventory adjustments at terminal device vendors, according to industry sources.

AU Optronics (AUO) has seen the average utilization rate of its LCD fabs rise to above 60% in the fourth quarter of 2022, up from 50% in the prior quarter, according to company chairman Paul Peng.

China-based OLED panel makers" production capacity as a percentage of the global total will see slower growth as utilization of their existing lines has decreased to low levels, prompting them to decelerate capacity expansions, according to The Elec.

LG Display (LGD) will end the production of TV LCD panels at its P7 plant in Paju, South Korea, ahead of the original schedule in late January 2023, ending production of all such panels in South Korea, according to South Korea-based Aju Business Daily.

The panel industry is going through its worst downturn in a decade, caused by a sharp decline in demand in a short period of time. With major losses in 2022 and ongoing global uncertainties, the industry expects market recovery to be slow in 2023.

The industrial and public displays market has been growing from 7.6% of total market share in 2020 to 8.5% in 2021, and is expected to grow to 8.7% in 2022. Chinese panel makers have taken the lead for industrial display, in which Tianma tops the first place with 37% share in 2022, followed by BOE, AUO, Innolux and Truly, according to Omdia.

Global factors have had a major impact on LCD panel demand in 2022, causing industry players to expect demand to remain weak through the first half of 2023. Taiwan-based LCD panel makers such as AU Optronics (AUO) and Innolux are making moves to boost their market share by targeting smart markets and creating value-added services.

Though demand for LCD panels has nosedived in 2022, automotive displays will drive global LCD panel output value to continually increase to over US$70 billion in 2030, according to DIGITIMES Research director Tony Huang.

LCD panel maker AUO has disclosed it has cooperated with VFX (visual effects) specialist Renovatio Pictures to set up an LED virtual studio at Central Motion Picture"s film studio in Taipei to provide integrated services consisting of shooting scenes and stages, content production, technical counseling and rental equipment.

While global sales of smartphones have decreased, global shipments of smartphone-use flexible OLED panels keep increasing but those of rigid OLED panels have slipped, according to industry sources.

As global demand for XR (extended reality) headsets is expected to take off in 2023, microLED panels tend to surpass LCD and OLED panels to become mainstream, specifically for XR devices, according to South Korea-based Money Today.

LCD panel maker Innolux has reported consolidated revenue of NT$16.182 billion (US$529.25 million) for November, growing 3.61% sequentially but slipping 39.15% on year.

Samsung Electronics continues to hold the top spot in the global TV market in terms of unit sales, while LG Electronics and China-based Hisense and TCL strive for second place, according to market sources.

LG Display (LGD) will bring to an end production of LCD panels at its P7 plant in Paju, northern South Korea, sooner in mid-December 2022 or later at the end of the month, and thus end production of all LCD panels in South Korea, according to South Korea-based TheElec.

New York, NY, Jan. 11, 2021 (GLOBE NEWSWIRE) -- Facts and Factors have published a new research report titled “E-Paper Display Market by Product (Auxiliary Displays, Electronic Shelf Labels, E-Readers, and Others), and By End User (Consumer Electronics, Automotive & Transportation, Retail, Institutional, Media and Entertainment, and Others): Global Industry Perspective, Comprehensive Analysis, and Forecast, 2019 - 2026”.

According to the research study, the global E-Paper Display Market was estimated at USD 2,000 Million in 2019 and is expected to reach USD 11,400 Million by 2026. The global E-Paper Display Market is expected to grow at a compound annual growth rate (CAGR) of 28% from 2019 to 2026.

In recent years developing countries have adopted the new technologies significantly. The essential factor for driving market development is the ascent in the number of electronic readers and the improvement of display gadgets in electronics. An extra advantage of low power utilization of e-paper display is a key factor in impelling the development of the e-paper display industry. In recent years, the utilization of progressing data devices has expanded significantly. In addition, developing the retail area is making open doors for e-paper display in applications, for example, customer gadgets cost marking, electronic announcements, advanced mobile phones, and so forth. The utilization of e-paper displays to offer paper-like visuals has been a significant factor in driving the development of the market.

The high assembling cost of e-paper display has been a growth hampering element of the e-paper display industry. Also, the e-paper displays must be coordinated with different frameworks this builds the general expense of the e-paper display framework. In addition, the absence of a range of color pallets alongside restricted video output is probably going to obstruct market development. Expanding interests in innovations by breaking down patterns in electronics to grow newly adaptable, and large format displays. In addition, developing ecological mindfulness has affected the purchaser to take activities to lessen paper utilization. This thusly is foreseen to put e-paper display as a substitute for paper. Low power utilization is seen in e-paper display which is foreseen to make open doors for solar oriented controlled e-paper display lessening light contamination and empower green versatility.

E-paper display is bifurcated on the basis of product and end-user. Based on the product, the market is segmented into electronic shelf labels, e-readers, auxiliary displays, and others. The e-readers type is accounted for the market share of 40% in 2019. Based on the end-user, the market is segmented into automotive & transportation, institutional, media and entertainment, consumer electronics, automotive & transportation, retail, and others. The institutional application has dominated the market share with around 35% in 2019.

High adoption of e-display devices in developed countries and also the expansion in versatile e-paper display is the essential factor that is driving the development of the market. Technological innovation is additionally one of the central points in driving the development of the market. Increasing investment in economically emerging countries and exploring the potential of an untapped market can be an open door for the e-display market worldwide. The high cost involved in the production of e-display devices is one of the factors which is hampering the growth of the market.

E-paper display is bifurcated on the basis of product and end-user. Based on the product, the market is segmented into electronic shelf labels, e-readers, auxiliary displays, and others. The e-readers type is accounted for the market share of 40% in 2019. Based on the end-user, the market is segmented into automotive & transportation, institutional, media and entertainment, consumer electronics, automotive & transportation, retail, and others. The institutional application has dominated the market share with around 35% in 2019.

Browse the full “E-Paper Display Market By Product (Auxiliary Displays, Electronic Shelf Labels, E-Readers, and Others), and By End User (Consumer Electronics, Automotive & Transportation, Retail, Institutional, Media and Entertainment, and Others): Global Industry Perspective, Comprehensive Analysis, and Forecast, 2019 - 2026" report at https://www.fnfresearch.com/global-e-paper-display-market-by-product-auxiliary

Geographically market is categorized as Europe, North America, Latin America, APAC, and the MEA regions. In terms of revenue, North America is projected to rule the world market with around 40% market share. The adoption rate of advanced technology in North America is very high hence, North America has a major market share for the e-paper display market.

Key Insights from Primary Research As per our primary respondents, the global e-paper display market is set to grow annually at a rate of around 25%.

On the basis of end user segmentation, the “institutional application” category was the leading revenue-generating category accounting for around 35% share, in 2019.

Key Recommendations from Analysts As per our analysis, the global e-paper display market is growing at a high CAGR and various end-use industries are aware of this potential market and applications of the e-paper display.

Growing at a CAGR of around 28%, the global e-paper display market provides numerous opportunities for all of the involved stakeholders across the entire value chain.

Our analysts have identified-readers and institutional application segments will be dominating for global e-paper display market in terms of product and end user segmentation respectively.

Facts & Factors is a leading market research organization offering industry expertise and scrupulous consulting services to clients for their business development. The reports and services offered by Facts and Factors are used by prestigious academic institutions, start-ups, and companies globally to measure and understand the changing international and regional business backgrounds.

(April 30, 2019) – With Chinese panel makers accelerating the mass production of large thin-film transistor (TFT) liquid crystal display (LCD) TV panels faster than expected, they accounted for 33.9 percent of the 60-inch and larger LCD TV panel shipments in the first quarter of 2019. Their market share has expanded nearly 10 times from 3.6 percent in just over a year, according to business information provider

South Korean panel makers still accounted for the largest share in the 60-inch and larger LCD TV panel shipments, with a 45.1 percent share in the first quarter. However, Chinese panel makers’ share in the large LCD TV panel market is expected to continue to grow.

BOE accounted for 29 percent of the total 60-inch and larger LCD TV panel shipments in the first quarter of 2019. It is estimated that the B9 10.5G fab has reached its maximum capacity of 120,000 sheets in the first quarter of 2019.

ChinaStar also started to mass produce large LCD panels at its T6 10.5G fab in the first quarter. CEC-Panda and CHOT ramped up mass production at their 8.6G fabs to the maximum design capacity in the first quarter. Foxconn/Sharp is forecast to begin mass production at their Guangzhou 10.5G fab in the second half of 2019.

“As both Chinese and South Korean panel suppliers are focusing on large LCD TV panels, competition between them will become more intense, pressuring the price of large LCD TV panels even further throughout 2019,” Wu said.

by IHS Markit, shipments of larger than 9-inch TFT-LCD panels reached 178.3 million units in the first quarter of 2019, down 1 percent from a year ago. By area, the shipment increased by 6.7 percent to 49.1 million square meters during the same period.

BOE led the unit shipments of large TFT-LCD panels with a 24.6 percent share in the first quarter of 2019, followed by LG Display (18.8 percent) and Innolux (16 percent). By area shipments, LG Display accounted for the largest share of 20 percent, followed by BOE (19.9 percent) and Samsung Display (14.1 percent).

IHS Markit provides information on the entire range of large display panels shipped worldwide and regionally, including monthly and quarterly revenues and shipments by display area, application, size and aspect ratio of each supplier.

IHS Markit (Nasdaq: INFO) is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers next-generation information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 business and government customers, including 80 percent of the Fortune Global 500 and the world’s leading financial institutions.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey