lcd module market outlook manufacturer

With the evolutionary changes in consumer electronics from past few years, the demand for the electronic parts is increasing rapidly. LCD display modules are electronically modulated optical device or flat-panel display and use the light-modulating properties of liquid crystals.

LCD display modules display arbitrary image or fixed images and low content information. The information can be displayed or kept hidden including digits, preset words, and seven-segment displays, as in a digital clock.

Increasing production of electronic devices such as aircraft cockpit displays, computer monitors, LCD televisions, indoor and outdoor signage and instrument panels is responsible for the increasing demand for the LCD display module. Manufacturers of the LCD display modules are focusing on developing innovative products to attract more customers to increase the revenue generation by sales of displays.

Manufacturers of the LCD display modules are coming up with the product innovations such as background display colors, character sizes, number of rows, and others and these features are fueling the increasing integration of the LCD display modules.

Constant advancements in the LCD display modules and improvement in the functionality of displays is the primary factor driving the growth of the LCD display module market.

The manufacturers are also focusing on the delivering a LCD display modules are per the end user requirements as these displays are primarily used for the consumer electronic devices which are produced in bulk quantity.

The increasing production of small electronic devices such as cameras, watches, calculators, clocks, mobile telephones, DVD players, clocks, and other devices is creating a huge demand from manufacturers of these products for the LCD display modules as per their product requirements.

On the other hand, availability of LCD display modules at low prices due to the entry of new players from developing countries, shortage of electronic components is a significant challenge for the established players in this market.

The global vendors for LCD Display Module include RAYSTAR OPTRONICS, INC., WINSTAR Display Co., Ltd., Newhaven Display International, Inc., Sharp Microelectronics, 4D Systems, ELECTRONIC ASSEMBLY GmbH, Kyocera International, Inc., Displaytech, and others. LCD display manufacturers are coming up with the new features and more advanced functionalities of the displays for sustaining in the global competition.

In February 2018, Displaytech, LCD display module manufacturer released DT070CTFT, a 7 inch 800 x 480 TFT display. The company is offering LCD displays with a resistive touch as well as a capacitive touch panel.

The global market for LCD Display Module is divided on the basis of regions into North America, Latin America, Western Europe, Eastern Europe, the Asia Pacific Excluding Japan, Japan, China, and Middle East & Africa. Among these regions, the countries such as Taiwan, South Korea, and China holds major market share in terms of revenue generation from the sale of LCD display module because of the higher presence of manufacturers for these displays as well as the dense presence of the consumer electronics manufacturers.

North America, Western Europe is the second largest market for the LCD display module due to increasing demand from consumer electronics manufacturers. MEA region is expected to grow at moderate CAGR.

The report provides in-depth analysis of parent market trends, macro-economic indicators and governing factors along with market attractiveness as per segments. The report also maps the qualitative impact of various market factors on market segments and geographies.

The expansion of production LCD displays and their increased importance in automotive products drive the growth of the global automotive LCD display market.

The expansion of production LCD displays and their increased importance in automotive products drive the growth of the global automotive LCD display market. However, restricted view angle of LCD displays restricts the market growth. Moreover, increase in use of AR and VR devices in displays present new opportunities for the market in the coming years.

COVID-19 Scenario:The outbreak of the COVID-19 pandemic had a negative impact on the global automotive LCD display market, owing to temporary closure of manufacturing firms and disruptions in the supply chain during the prolonged lockdown.

European countries under lockdowns suffered major loss of businesses and revenues due to shutdown of manufacturing units in the region. Operations of production and manufacturing industries were heavily impacted by the outbreak of COVID-19, which led to the slowdown in the market growth.

Partnership/collaboration agreements with key stakeholders acted as a key strategy to sustain in the market. In the recent past, many leading players opted for product launch or partnership strategies to strengthen their foothold in the market.

Based on display size, the upto 7 inch segment held the highest market share in 2021, accounting for more than half of the global automotive LCD display market, and is estimated to maintain its leadership status throughout the forecast period. Moreover, the same segment is projected to manifest the

Based on vehicle type, the passenger car segment held the highest market share in 2021, accounting for nearly two-thirds of the global automotive LCD display market, and is estimated to maintain its leadership status throughout the forecast period. This is attributed to the huge demand for passenger cars throughout the world. However, the light commercial vehicle segment is projected to manifest the highest CAGR of 7.2% from 2022 to 2031, due to the adoption of advanced technologies.

Based on region, Asia-Pacific held the highest market share in terms of revenue in 2021, accounting for more than one-third of the global automotive LCD display market, and is likely to dominate the market during the forecast period. Moreover, the same region is expected to witness the fastest CAGR of 6.2% from 2022 to 2031. Surge in demand for interactive display, video walls, and touchscreen technology in this region, is expected to boost the market growth. The report also discusses other regions including the North America, Europe, and LAMEA.

Key Benefits For Stakeholders:This study comprises an analytical depiction of the market size along with the current trends and future estimations to depict the imminent investment pockets.

By Application (Smartphone & Tablet, Smart Wearable, Television & Digital Signage, PC & Laptop, Vehicle Display, and Others), Technology (OLED, Quantum Dot, LED, LCD, E-PAPER, and Others), Industry Vertical (Healthcare, Consumer Electronics, BFSI, Retail, Military & Defense, Automotive, and Others), Display Type (Flat Panel Display, Flexible Panel Display, and Transparent Panel Display): Global Opportunity Analysis and Industry Forecast, 2021-2031

Allied Market Research (AMR) is a full-service market research and business-consulting wing of Allied Analytics LLP based in Portland, Oregon. Allied Market Research provides global enterprises as well as medium and small businesses with unmatched quality of "

We are in professional corporate relations with various companies and this helps us in digging out market data that helps us generate accurate research data tables and confirms utmost accuracy in our market forecasting. Allied Market Research CEO Pawan Kumar is instrumental in inspiring and encouraging everyone associated with the company to maintain high quality of data and help clients in every way possible to achieve success. Each and every data presented in the reports published by us is extracted through primary interviews with top officials from leading companies of domain concerned. Our secondary data procurement methodology includes deep online and offline research and discussion with knowledgeable professionals and analysts in the industry.

GlobalLiquid Crystal Display (LCD) Market, By Product (LCD Character Drivers, LCD Graphic Drivers, LCC Segment Drivers), Application (Automotive, Industrial, Medical, Small Appliance, Others) – Industry Trends and Forecast to 2029

Liquid crystal display (LCD) are widely being used in various sectors such as entertainment, corporate, transport, retail, hospitality, education, and healthcare, among others. These allow organizations in engaging with a broader audience. They also help in creating a centralized network for digital communications.

Global Liquid Crystal Display (LCD) Market was valued at USD 148.60 billion in 2021 and is expected to reach USD 1422.83 billion by 2029, registering a CAGR of 32.63% during the forecast period of 2022-2029. Small Appliance is expected to witness high growth owing to the rise in demand for devices such as smartphones. The market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis.

This section deals with understanding the market drivers, advantages, opportunities, restraints and challenges. All of this is discussed in detail as below:

The increase in demand for the digitized promotion of products and services for attracting attention of the target audience acts as one of the major factors driving the growth of liquid crystal display (LCD) digital market.

The rise in demand for 4K digitized sign displays with the embedded software and media player accelerate the market growth. These signs deliver customers an affordable Ultra HD digital signage solution has a positive impact on the market.

The emergence of innovative products, such as leak detector systems, home monitoring systems and complicated monetary products further influence the market.

Additionally, rapid urbanization, change in lifestyle, surge in investments and increased consumer spending positively impact the liquid crystal display (LCD)digital market.

Furthermore, adoption of AMOLED displays, especially due to introduction of 5G and adoption of foldable and flexible displays extend profitable opportunities to the market players in the forecast period of 2022 to 2029. Also, rise in demand for Micro-LED and mini-LED technologies will further expand the market.

On the other hand, decline in demand for displays from retail sector due to drastic shift towards online advertisement, and high costs associated with new display technology-based products are expected to obstruct market growth. Also, deployment of widescreen alternatives, such as projectors and screenless displays is projected to challenge the liquid crystal display (LCD) digital market in the forecast period of 2022-2029.

This liquid crystal display(LCD) digital market report provides details of new recent developments, trade regulations, import-export analysis, production analysis, value chain optimization, market share, impact of domestic and localized market players, analyses opportunities in terms of emerging revenue pockets, changes in market regulations, strategic market growth analysis, market size, category market growths, application niches and dominance, product approvals, product launches, geographic expansions, technological innovations in the market. To gain more info on liquid crystal display (LCD) digital market contact Data Bridge Market Research for an Analyst Brief, our team will help you take an informed market decision to achieve market growth.

The COVID-19 has impacted liquid crystal display (LCD) digital market. The limited investment costs and lack of employees hampered sales and production of liquid crystal display (LCD) technology. However, government and market key players adopted new safety measures for developing the practices. The advancements in the technology escalated the sales rate of the li liquid crystal display (LCD) digital as it targeted the right audience. The increase in sales of devices across the globe is expected to further drive the market growth in the post-pandemic scenario.

Sharp launched the new massive 8K Ultra-HD professional LCD in November’2020. This display packs in 33 million pixels and employs a wide color gamut color filter coupled with optimized LED backlight phosphors.

The liquid crystal display (LCD) digital market is segmented on the basis of product and application. The growth amongst these segments will help you analyze meager growth segments in the industries and provide the users with a valuable market overview and market insights to help them make strategic decisions for identifying core market applications.

The liquid crystal display (LCD) digital market is analysed and market size insights and trends are provided by country, type, component, location, content category, end-user, size, display technology, brightness, and application as referenced above.

The countries covered in the liquid crystal display (LCD) digital market report are U.S., Canada, Mexico, Brazil, Argentina, Rest of South America, Germany, Italy, U.K., France, Spain, Netherlands, Belgium, Switzerland, Turkey, Russia, Rest of Europe, Japan, China, India, South Korea, Australia, Singapore, Malaysia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific, Saudi Arabia, U.A.E, South Africa, Egypt, Israel, Rest of Middle East and Africa (MEA).

North America dominates the liquid crystal display (LCD) digital market because of the presence of dedicated suppliers of the product and rise in demand for these displays in the retail industry within the region.

Asia-Pacific is expected to witness significant growth during the forecast period of 2022 to 2029 because of the rise in awareness regarding the benefits of LCD in the region.

The country section of the report also provides individual market impacting factors and changes in regulation in the market domestically that impacts the current and future trends of the market. Data points like down-stream and upstream value chain analysis, technical trends and porter"s five forces analysis, case studies are some of the pointers used to forecast the market scenario for individual countries. Also, the presence and availability of global brands and their challenges faced due to large or scarce competition from local and domestic brands, impact of domestic tariffs and trade routes are considered while providing forecast analysis of the country data.

The liquid crystal display (LCD) digital market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies" focus related to liquid crystal display (LCD) digital market.

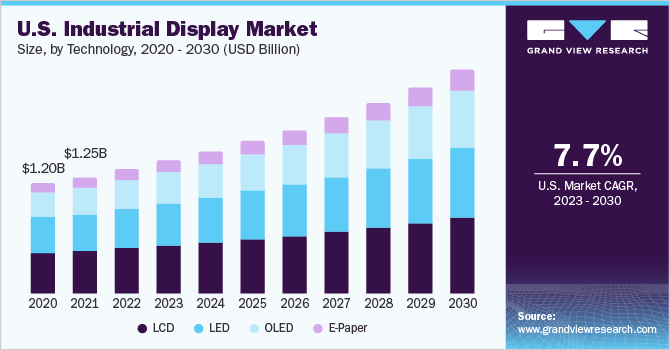

New York, Aug. 18, 2022 (GLOBE NEWSWIRE) -- Reportlinker.com announces the release of the report "Global Industrial Display Market Size, Share & Industry Trends Analysis Report By Technology, By Type, By End-use, By Panel Size, By Application, By Regional Outlook and Forecast, 2022 - 2028" - https://www.reportlinker.com/p06315021/?utm_source=GNW

Furthermore, the global shift in technology and automated systems drive market growth. Moreover, robust display wireless connection, and technologically advanced push market growth during the forecast period.

The increasing adoption of multi-featured Human-Machine Interface (HMI) devices, the Industrial Internet of Things (IIoT), and the popularity of smart industrial displays are some of the factors driving market growth. The displays’ innovative features, such as touchpad frames and fully automated touch detection systems; RFIDs; Ethernet connectivity; and ability to withstand high temperature changes, shock, motion, dust, scrape, and chemicals, are catapulting the industry forward.

Even though displays are a viable substitute for manual methods and outdated push-button technology, the industry offers a large investment opportunity. To keep up with changing industrial needs, the market is differentiated by continuous technological developments. Low-Temperature Poly-Silicon (LTPS), Liquid Crystal Display (LCD), Thin-Film-Transistor (TFT), Digital Light Processing (DLP), and Color Filter (CF) are some of the most recent industry innovations.

Society and the global economy are suffering greatly as a result of the COVID-19 pandemic. The supply chain is being impacted by the outbreak, whose effects are growing every day. Stock market turbulence, a decline in corporate confidence, a considerable delay in the distribution chain, and a rise in customer apprehension are all being brought on by it. European nations under lockdown have suffered major losses in trade and revenue as a result of the suspension of manufacturing operations in the area. The COVID-19 pandemic has had a substantial impact on manufacturing and production processes, slowing the growth of the industrial display sector in 2020.

The creation of thin, effective, and bright displays is made possible by the thin films of organic light-emitting (OLED) materials that emit light when electricity is applied to them. It is anticipated that OLEDs would replace prevailing technologies in the display ecosystem. As a result, a sizable number of businesses have started to increase their investment in OLED study and innovation. OLED industrial displays are dominating the market because to their cutting-edge features, such as higher contrast, quicker response times, and a broader operating temperature range than LCDs. OLED micro displays are now often used in EVFs and HMDs because they outperform conventional LCD and LCoS micro display technologies.

On the basis of technology, the industrial display market is classified into LCD, LED, OLED and E-paper. The LCD segment acquired the highest revenue share in the Industrial Display Market in 2021. A flat panel display called a liquid crystal display (LCD) makes use of the liquid crystals’ capacity to modulate light. Instead of emitting light directly to create images in color or monochrome, liquid crystals use a backlight or reflector. There are two primary categories of LCDs used in electronic devices like digital clocks and video players and those used in computers.

Based on type, the industrial display market is segmented into Rugged Displays, Open-frame Monitors, Panel-Mount Monitors, Marine Displays and Video Walls. The open-frame monitor segment registered a substantial revenue share in the Industrial Display Market in 2021. Open Frame Monitor (OFM) is primarily housed in a bare-metal container and typically does not have a bezel. Instead, it is normally delivered with a mounting metal flange on the outside. Electronic parts, such as the display controller A/D board, the harnesses, and maybe the internal power supply, are secured to the inside of the metal chassis.

By end-use, the industrial display market is categorized into Manufacturing, Mining & Metals, Chemical, Oil, and Gas, Energy & Power, and Others. The Chemical, Oil, and Gas segment registered a promising revenue share in the Industrial Display Market in 2021. Oil and gas have played an important role in the economic transformation, but the industry is entering a new era. Digital transformation can improve productivity and workplace safety while reducing the industry’s environmental impact. Large industrial displays are especially important in the oil and gas industry, where comprehend rough environmental parameters, extreme temperatures, high levels of pollution, and operation is critical not only for safety but also for improving profitability.

Based on panel size, the industrial display market is fragmented into Up to 14”, 14-21”, 21-40”, and 40” and above. The 21-40" segment witnessed a substantial revenue share in the Industrial Display Market in 2021. It is due to the demand for touch screen computer parts in heavy-duty workplaces expected to drive the 21-40" panel size segment’s growth. The anodized coatings on the monitors and touch screen panels, combined with the stainless-steel chassis, are intended to provide operators with greater durability and operation across a wide temperature range.

By application, the industrial display market is divided into HMI, Remote Monitoring, Interactive Display and Digital Signage. The HMI segment garnered the highest revenue share in the Industrial Display Market in 2021. This is because multinational HMI manufacturers are expanding their presence in emerging markets such as China and India. The particular technology is expected to combine the internet’s reach with the ability to control industrial equipment, infrastructural facilities, and operating procedures in factories directly.

Region-wise, the industrial display market is analyzed across North America, Europe, Asia Pacific and LAMEA. The North America region procured the highest revenue share in the Industrial Display Market in 2021. With high demand coming from monitoring system, HMI, and interactive display applications. Increased use of digital displays and HMIs in North America is expected to generate new business opportunities over the forecast period. Furthermore, the growing popularity of industrial automation, rising investment in IIoT applications, and multi-featured HMI gadgets may expedite the use of industrial display capabilities in this market.

The market research report covers the analysis of key stake holders of the market. Key companies profiled in the report include Samsung Display Co., Ltd. (Samsung Electronics Co. Ltd.), LG Display Co., Ltd. (LG Corporation), Leyard Optoelectronic Co. (Planar Systems, Inc.), Advantech Co., Ltd., Siemens AG, Sharp NEC Display Solutions, Ltd. (Sharp Corporation), Pepperl + Fuchs Group, Japan Display, Inc., Winmate, Inc., and Maple Systems, Inc.

ReportLinker is an award-winning market research solution. Reportlinker finds and organizes the latest industry data so you get all the market research you need - instantly, in one place.

The global TFT-LCD display panel market attained a value of USD 181.67 billion in 2022. It is expected to grow further in the forecast period of 2023-2028 with a CAGR of 5.2% and is projected to reach a value of USD 246.25 billion by 2028.

The current global TFT-LCD display panel market is driven by the increasing demand for flat panel TVs, good quality smartphones, tablets, and vehicle monitoring systems along with the growing gaming industry. The global display market is dominated by the flat panel display with TFT-LCD display panel being the most popular flat panel type and is being driven by strong demand from emerging economies, especially those in Asia Pacific like India, China, Korea, and Taiwan, among others. The rising demand for consumer electronics like LCD TVs, PCs, laptops, SLR cameras, navigation equipment and others have been aiding the growth of the industry.

TFT-LCD display panel is a type of liquid crystal display where each pixel is attached to a thin film transistor. Since the early 2000s, all LCD computer screens are TFT as they have a better response time and improved colour quality. With favourable properties like being light weight, slim, high in resolution and low in power consumption, they are in high demand in almost all sectors where displays are needed. Even with their larger dimensions, TFT-LCD display panel are more feasible as they can be viewed from a wider angle, are not susceptible to reflection and are lighter weight than traditional CRT TVs.

The global TFT-LCD display panel market is being driven by the growing household demand for average and large-sized flat panel TVs as well as a growing demand for slim, high-resolution smart phones with large screens. The rising demand for portable and small-sized tablets in the educational and commercial sectors has also been aiding the TFT-LCD display panel market growth. Increasing demand for automotive displays, a growing gaming industry and the emerging popularity of 3D cinema, are all major drivers for the market. Despite the concerns about an over-supply in the market, the shipments of large TFT-LCD display panel again rose in 2020.

North America is the largest market for TFT-LCD display panel, with over one-third of the global share. It is followed closely by the Asia-Pacific region, where countries like India, China, Korea, and Taiwan are significant emerging market for TFT-LCD display panels. China and India are among the fastest growing markets in the region. The growth of the demand in these regions have been assisted by the growth in their economy, a rise in disposable incomes and an increasing demand for consumer electronics.

The report gives a detailed analysis of the following key players in the global TFT-LCD display panel Market, covering their competitive landscape, capacity, and latest developments like mergers, acquisitions, and investments, expansions of capacity, and plant turnarounds:

*At Expert Market Research, we strive to always give you current and accurate information. The numbers depicted in the description are indicative and may differ from the actual numbers in the final EMR report.

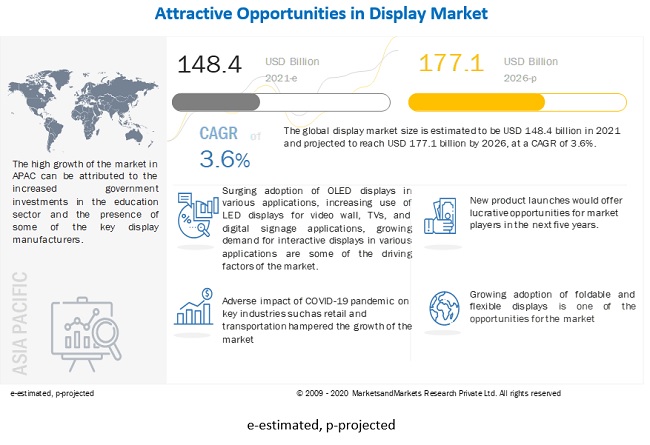

The global display market size was valued at $114.9 billion in 2021, and is projected to reach $216.3 billion by 2031, growing at a CAGR of 6.7% from 2022 to 2031.

Display includes screen, computer output surface, and a projection surface that displays content, mainly test, graphics, pictures, and videos utilizing cathode ray tube (CRT), light-emitting diode (LED), liquid crystal display (LCD), and other technologies. These displays are majorly incorporated in devices such as televisions, smartphones, tablets, laptops, vehicles, and others. Emergence of advanced technologies offer enhanced visualizations in several industry verticals, which include consumer electronics, retail, sports & entertainment, and transportation. 3D displays are in trend in consumer electronics and entertainment sector.

In addition, flexible display technologies witness popularity at a high pace. Moreover, display technologies such as organic light-emitting diode (OLED) have gained increased importance in products such as televisions, smart wearables, smartphones, and other devices. Smartphone manufacturers plan to incorporate flexible OLED displays to attract consumers. Furthermore, the market is also in the process of producing energy saving devices, primarily in wearable devices. However, high cost of the transparent and quantum dot display technologies. Hence, need for such high costs associated with display products may hamper growth of the market. Furthermore, adoption of AR/VR devices and commercialization of autonomous vehicles are expected to provide lucrative display market opportunity for the growth of the market.

The COVID-19 pandemic is impacting the society and overall economy across the global. The impact of this outbreak is growing day-by-day as well as affecting the supply chain. It is creating uncertainty in the massive slowing of supply chain, and increasing panic among customers. European countries under lockdowns have suffered major loss of business and revenue due to shutdown of manufacturing units in the region. Operations of production and manufacturing industries have been heavily impacted by the outbreak of COVID-19, which led to slowdown in the display market growth.

By display type, the display market outlook is divided into flat panel display, flexible panel display, and transparent panel display. Flat panel display segment was the highest revenue contributor to the market, in 2021. The flexible panel display segment dominated the display market growth, in terms of revenue, in 2021, and is expected to follow the same trend during the forecast period.

By industry vertical, the market it is divided into healthcare, consumer electronics, retail, BFSI, military & defense, transportation, and others.Consumer electronics accounted for largest display market share in 2021.

Region wise, the display market trends are analyzed across North America (the U.S., Canada, and Mexico), Europe (UK, Germany, France, and rest of Europe), Asia-Pacific China, Japan, India, South Korea, and rest of Asia-Pacific), and LAMEA (Latin America, the Middle East, and Africa). Asia-Pacific, specifically the China, remains a significant participant in the global display industry. Major organizations and government institutions in the country are intensely putting resources into these displays.

Top impacting factors of the market include high demand for flexible display technology in consumer electronic devices, increase in adoption of electronic components in the automotive sector, and rise in trend of touch-based devices. Surge in adoption of displays in touch screen devices, rise in need for AR/VR devices, and commercialization of autonomous vehicles are expected to create lucrative in the future. Moreover, stagnant growth of desktop PCs, notebooks, and tablets hampers growth of the display market. However, each of these factors is expected to have a definite impact on growth of the display industry in the coming years.

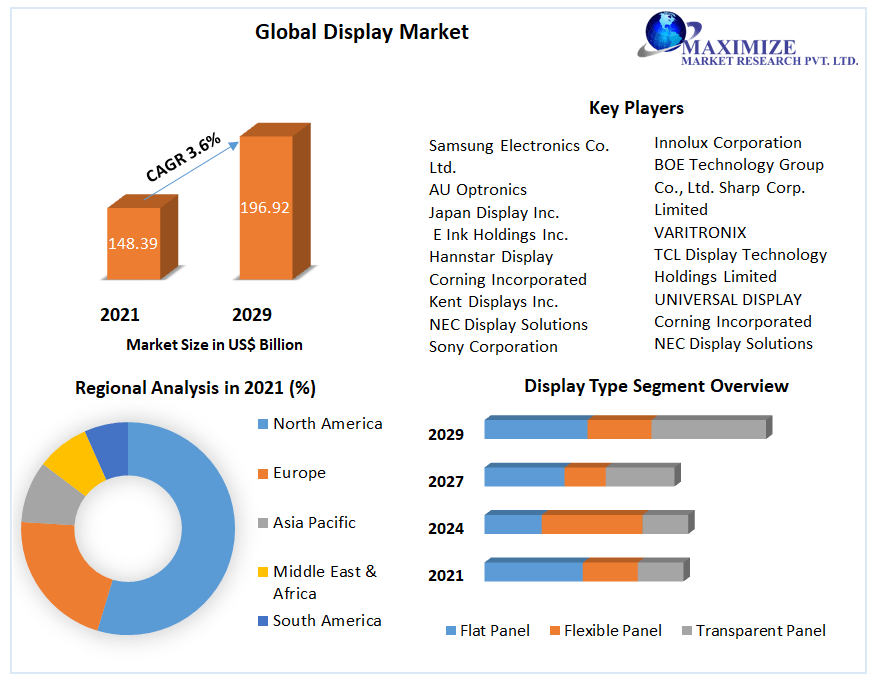

The key players profiled in this report include LG Display Co. Ltd., Samsung Electronics Co. Ltd., AU Optronics, Japan Display Inc., E Ink Holdings Inc., Hannstar Display Corporation, Corning Incorporated, Kent Displays Inc., NEC Display Solutions, and Sony Corporation. These key players have adopted strategies, such as product portfolio expansion, mergers & acquisitions, agreements, regional expansion, and collaborations to enhance their market penetration.

KEY BENEFITSFOR STAKEHOLDERSThis study comprises analytical depiction of the display market forecast along with the current trends and future estimations to depict the imminent investment pockets.

Key Market Players Samsung Electronics Co Ltd, Sharp Corporation, Japan Display Inc, Innolux Corporation, NEC CORPORATION, Panasonic Corporation, BOE Technology Group Co., Ltd., AUO Corporation, Sony Corporation, Leyard Optoelectronic Co., Ltd, LG Display Co Ltd

The quantum dot display market is forecast to be valued at over US$ 4 Bnin 2022, experiencing a Y-o-Y increase of 30%as compared to 2021. Future projections indicate that the market will surge over 17xto reach US$ 69.79 Bnby 2032.

Over the historical period 2017-2021, the global quantum dot display surged at approximately 30%CAGR. Growing demand in downstream markets for energy-efficient display panels such as televisions, smartphones, tablets, personal computers and other electronics has forced OEMs and display manufacturers to build state-of-the-art displays capable of delivering maximum energy efficiency and increasing color quality.

During the height of the COVID-19 pandemic crisis, the market experienced significant turbulence. Given the imposition of strict lockdowns, manufacturing units were compelled to cease operations temporarily, affecting output of essential equipment required for quantum dot displays such as cadmium. However, prospects began rebounding once these restrictions were lifted.

Quantum dot displays are well suited for displays due to properties such as high luminous efficacy, high brightness, and low power consumption. The use of inorganic materials prevents burn-ins, which are common in other types of displays. The numerous benefits of using quantum dot displays will be a major factor driving market growth, with Fact.MR projecting a 33%CAGR through 2032.

Modern displays not only offer higher brightness and contrast ratios but are also available in higher resolutions and consume less power than conventional displays. Display manufacturers are developing displays with improved specifications to strengthen their position in the market.

In recent years, there has been a significant rise in the demand for large-size and high-resolution displays owing to the enhanced visual experience and the decreasing prices of LCDs.

Big-screen displays have become more affordable due to the reduced LCD prices. Owing to the growing focus of display manufacturers on the production of 4K and 8k displays, there has been an increasing demand for quantum dots due to their ability to enhance the display. The adoption of quantum dots in displays provides advantages such as higher image frame rates, greater bit depth, and a wider color gamut.

However, many companies and research associations are producing alternatives for cadmium-based quantum dots. Elements such as indium and zinc are suitable substitutes for cadmium for the development of quantum dots. Soon, cadmium-free quantum dots are expected to be widely available and are expected to dominate the market as a result of their safety, strong performance, and environmental benefits.

North America dominates the global quantum dots market, owing primarily to the high demand for QLEDs and early adoption of the technology. Furthermore, the population"s increased awareness of health and fitness drives the quantum dots market size.

Furthermore, the presence of technology providers, as well as increasing investments by government agencies and aerospace & defense in research and development of machine learning technology, influence market growth. A market share worth 40%is projected for the North American market.

The global quantum dot display market across APAC is estimated to grow at a CAGR of over 32% over the forecast period. Increasing demand for energy-efficient technologies are the primary factors for increased demand for quantum dot displays in countries like China and India.

Rising internet penetration and large tech-savvy younger population have underpinned robust demand for television sets and smartphones. This presents a great potential for the quantum dot display market.

The introduction of quantum display devices into the display industry has the potential to create a new model that could replace LCD panels. Top-tier competitors in the quantum dot display market are developing devices that use cadmium-free quantum dot technology.

The quantum dot display market is consolidated with a few prominent manufacturers namely Samsung Electronics Co. Ltd., LG Display Co. Ltd., Sony Corporation, Sharp Corporation and CSOT (China Star Optoelectronics Technology), acquiring a share of more than 70%. Numerous approaches, such as expansion, introduction of new products, joint ventures, agreements, alliances and acquisitions, are being employed by top competitors. Some of the other developments in the market are:

The global displays marketsize was estimated at USD 156.9 billion in 2021 and is expected to be worth around USD 297.1 billion by 2030 and anticipated to expand at a CAGR of 7.35% during the forecast period 2022 to 2030.

Screens that project information like pictures, movies, and messages are referred to as displays. Numerous technologies, including light-emitting diodes (LEDs), liquid crystal displays (LCDs), organic light emitting diodes (OLEDs), and others, are used in these display panels. Additionally, it plays a significant role in

Furthermore, display technologies like organic light-emitting diode (OLED) have become more crucial in items like televisions, smart clothing, cell phones, and other gadgets. In order to draw customers, smartphone makers also want to use flexible OLED screens. In addition, the market is also developing energy-saving gadgets, mainly for

The worldwide display market is expanding as a result of advancements in flexible displays, rising OLED display device demand, and the growing popularity of touch-based devices. However, barriers to market expansion include the expensive cost of cutting-edge display technologies like quantum dot and transparent displays, as well as the stalling growth of desktop, notebook, and tablet PCs. In addition, substantial development possibilities for the global display market are anticipated from new applications in flexible display technologies.

One of the key reasons fuelling the growth of the display market is the rise in demand for digital product and service promotion to get the attention of the target audience. The emergence of smart wearable gadgets, technical developments, and rising demand for OLED-based goods are all contributing to the market further.

Innovative items like leak detecting systems, home monitoring systems, and complex financial solutions are starting to appear, which has an additional impact on the industry. The industry is growing thanks to the use of organic light-emitting diode panels in televisions and smartphones. Additionally, the display market benefits from rising urbanisation, a shift in lifestyle, an increase in expenditures, and higher consumer spending.

The adoption of automated equipment by many industries for a variety of uses has a significant influence on displays, which are available with high efficiency at cheap cost and are anticipated to accelerate market expansion. Because they offer a long lifespan, great scalability, high intensity, high brightness, and more, embedded devices are widely utilised. The organic light emitting diode and liquid crystal display markets are supported by aspects like reasonable pricing, effective brightness, and longer life and are expected to expand at the quickest rate in the industry over the projected period. The increased usage of Displays by the healthcare, educational, and automotive sectors is anticipated to fuel market expansion.

The usage of Displays in 3D systems is another factor boosting the market"s expansion. The user can employ the sophisticated technologies in Displays for the 3 systems due to their quick development. The market is anticipated to increase significantly as a result of the adoption of 3D systems in the consumer, industrial, medical, automotive, and other sectors. These systems require displays to project the dimensions.

Since touch-based gadgets are more accessible, the number of devices with touch sensors has grown tremendously in recent years. The proliferation of display devices is aided by the fact that touch-based gadgets need a display panel to function. As a result, a broad variety of home appliances, including the refrigerator, washing machine, microwave, etc., are enabled with the help of touch screens. The provision of cutting-edge display devices in automobiles, like the navigation system, heads-up display, digital rear-view mirrors, digital dashboard, and others, has also increased in the automotive sector. As a result, the market for displays is expanding due to the move toward touch-based technology.

Innovations in flexible displays, a growth in the demand for OLED display products, and a rise in the popularity of touch-based gadgets are what are driving the worldwide display market. However, the market is constrained by the expensive cost of cutting-edge display technologies like quantum dot and transparent displays, as well as the slow expansion of desktop, laptop, and tablet computers.Additionally, new applications for flexible display technologies, which are anticipated to produce profitable growth possibilities, are likely to boost the worldwide display market.

LCD technology has been widely utilised in display items during the preceding several decades. Currently, a number of settings, including retail, corporate offices, and banks, employ LCD-based gadgets. But it"s anticipated that LED technology will advance quickly throughout the course of the predicted period. The development of LED technology and its energy-efficiency are what are driving the demand for it. A disturbance in the supply-demand ratio, a decline in LCD display panel ASPs, and intense competition from emerging technologies are anticipated to push the LCD display sector into negative growth during the course of the projection period.

LED technology is predicted to drive market expansion because to its high pixel-pitch, brightness, improved efficiency, high light intensity, improved power efficiency, extended lifespan, and high scalability. Due to increased usage of displays in the automotive and medical sectors, where LED Displays are being utilised increasingly, the LED display market is anticipated to develop at a large and rapid 6.5% between 2022 and 2030.

The smartphones will make up a large percentage of the market. This rise will be fueled by the growing use of OLED and flexible displays by smartphone manufacturers. Shipments of expensive flexible OLED displays are growing quickly, and the forecast year is expected to see this trend continue. The market"s new development path has been identified as the smart wearables category. The demand for these gadgets is expected to soar throughout the projected period due to the fast-growing market for these products and the widespread use of AR/VR technology.

At 68%, the fixed device is anticipated to have the biggest market share over the projection period. Fixed devices are more widely accepted on the market than portable ones because of their low pricing, high scalability, longer life, contrast, and pixel quality, among other factors.

The aforementioned factors have increased the market adoption of fixed device, which is projected to drive the Display market. Both LED displays and Organic Light Emitting Diode are frequently used in these stationary devices.

In 2021, APAC will hold a 41% share of the global display market, followed by Europe. The industry-level research and development efforts in North America are constantly growing and advancing automated embedded device technology, which is raising the adoption rate of Display devices in industries including as healthcare, automotive, industrial, defence, and others. The market is anticipated to be stimulated by the huge number of end device makers in APAC. Since emerging nations like India, Japan, China, and others are constantly expanding the use of displays in a variety of industrial verticals, including wearables, smartphones, digital signage, medical, automotive, and other areas, the APAC region is thought to have the fastest growth for liquid crystal displays.

Other factors contributing to the market"s growth in the area include the expansion of display panel production facilities and the quick uptake of OLED displays. APAC has low labour expenses, which lowers the overall cost of producing display panels. The market is also being supported by the increasing use of display devices across a variety of sectors, particularly in China, India, and South Korea.

Samsung Electronics launched the first 15.6-inch OLED panel in the notebook industry in January 2019. Additionally, compared to 4K LCD-based displays, the panel will produce richer colours and deeper blacks.

The LCD is a transmissive technology. All LCDs require a reflected light source or backlighting. The LCD industry is characterized by rapid technological advances. Traditionally, applications for LCDs are notebook computer and desktop monitors. LCDs are expected to be used more across various applications, and this study focuses on the trends, challenges, and factors driving market growth. Also included are product, technology, and regional market analyses, along with a competitive analysis. This research service provides the necessary business intelligence to accelerate growth in a fast-paced market. The scope includes a market forecast for the geographic regions of Asia-Pacific (APAC), North America, Europe, and Rest of World.

MicroLED display technology is making rapid progress and is now at an early stage of commercialization. However, there are still challenges to establish a reliable supply chain and lower the manufacturing cost, despite the push by companies such as Apple, Samsung and Facebook. The report addresses the technical hurdles which depend mostly on the choice of manufacturing technology. Included in the report are market forecasts to 2027, based on DSCC’s analysis of the competitive landscape in the display industry. This report will be useful to every company in the microLED supply chain: LED manufacturers, panel makers, technology developers, OEMs, assembly houses, and end users.

DSCC’s Quarterly Advanced IT Display Shipment and Technology Report tracks advanced display shipments and forecasts shipments for all high-end displays into the tablet, notebook PC and desktop monitor markets. We are now in an age of display technology and form factor competition in the IT markets where brands and OEMs can choose between a wide variety of display technologies and alternative form factors.

MiniLED backlights in LCDs can potentially offer numerous advantages over other flat panel display technologies, most notably in high brightness, high contrast ratio, lower power consumption than WOLED TV and higher efficiency. The superior performance makes MiniLED backlights attractive for use in a variety of applications, ranging from large TVs to IT applications. Automotive and industrial applications are also advantageously addressed by MiniLED backlight technologies due to their higher brightness and higher contrast ratio.

The production of flat panel displays requires many different materials. In this report, we examine the market and trends for various gases, metal targets, liquid crystal, photoresist and PI alignment. This report reviews vital materials used in display production and provides estimates of consumption and revenues for each category of materials. The report also profiles major suppliers for each material and a forecast for material consumption and revenue. As the display industry becomes dominated by production in China, local suppliers are emerging to provide a domestic material supply chain and the report includes profiles of China"s domestic material suppliers.

The Quarterly FPD Supply/Demand Report provides its users with some of the most valuable content that DSCC offers including deep insights into market turning points, price forecasts, panel margins and more. The report is divided into four parts. The first covers display demand by application with units, revenues, area and ASPs provided for eight different applications for both LCDs and OLEDs.

Although OLEDs have grown rapidly recently, they are far from a mature technology which still has significant potential for more growth. OLEDs are still evolving and growing from several different perspectives including features, performance, architecture, end markets and manufacturing technologies. OLED revenues are expected to grow nearly 50% from 2020 to 2025 for a number of reasons. For these reasons, DSCC decided it would be valuable to create this report, The Future of OLED Manufacturing, to examine how OLED technology, manufacturing and performance are likely to evolve.

DSCC’s Quarterly FPD Forecast Report tracks the display market on a quarterly basis from 2018 through 2025. It reveals units, area, average selling price (ASP), revenue, average diagonal, and resolution (pixels per inch or PPI) for eight different applications by technology (LCD vs. OLED). It covers eight different markets.

Displays will play a vital role in Augmented Reality (AR) and Virtual Reality (VR) headsets. As big brands launch flagship AR/VR devices, the display manufacturers are pushing the technology to increase brightness, contrast and resolution. This updated report covers all the display categories, including LCD, AMOLED, LCoS, DLP, laser beam scanning, MicroLED and OLED on Silicon, and gives details on the key suppliers and their roadmaps. A description of the various optical configurations and waveguide types is included. Market forecasts for both AR and VR are segmented by display types and show the technologies that will generate the most revenues.

Due to the expectation that OLEDs and MiniLED backlit LCDs will see growing penetration into the tablet, notebook and desktop monitor markets, DSCC has developed a cost model that compares all existing and emerging advanced display technologies entering these markets. These include a-Si LCD/Oxide LCD/LTPS LCD/ MiniLED backlit LCD/rigid OLED/flexible OLED/foldable OLED/WOLED/Inkjet OLED IT panel display costs. The OLED cost model examines all of the different form factors currently sold into, or coming into, the IT Panel market. In addition, the cost model differentiates between panels made in China, Taiwan and Korea. Panels covered range from 10.9” to 32”. More displays will be added as these categories continue to emerge. The report Includes detailed BOM breakdown, costs and margins and forecasts these parameters out to 2025.

The report covers extensive analysis of the key market players in the market, along with their business overview, expansion plans, and strategies. The key players studied in the report include:

The report focuses on the LCD Display Panel market size, segment size (mainly covering product type, application, and geography), competitor landscape, recent status, and development trends. Furthermore, the report provides detailed cost analysis, supply chain. Technological innovation and advancement will further optimize the performance of the product, making it more widely used in downstream applications. Moreover, Consumer behavior analysis and market dynamics (drivers, restraints, opportunities) provides crucial information for knowing the LCD Display Panel market.

The Research Report delivers knowledge about sales quality, sales value and different brands related to top market players with highest number of market tables and figures at a guaranteed best price. Additionally, it comes with exhaustive coverage of post pandemic forces that are likely to impact the LCD Display Panel Market growth. The overview of report contents includes market dynamics, market share information, analysis of smaller companies, investment plans, merger and acquisition, gross margin, demand supply, import-export, covering key market segmentation that includes by types, applications, end-user, and regions.

Chapter 1 provides an overview of LCD Display Panel market, containing global revenue and CAGR. The forecast and analysis of LCD Display Panel market by type, application, and region are also presented in this chapter.

Chapter 2 is about the market landscape and major players. It provides competitive situation and market concentration status along with the basic information of these players.

Chapter 3 introduces the industrial chain of LCD Display Panel. Industrial chain analysis, raw material (suppliers, price, supply and demand, market concentration rate) and downstream buyers are analyzed in this chapter.

Chapter 6 provides a full-scale analysis of major players in LCD Display Panel industry. The basic information, as well as the profiles, applications and specifications of products market performance along with Business Overview are offered.

Chapter 7 pays attention to the sales, revenue, price and gross margin of LCD Display Panel in markets of different regions. The analysis on sales, revenue, price and gross margin of the global market is covered in this part.

Chapter 10 prospects the whole LCD Display Panel market, including the global sales and revenue forecast, regional forecast. It also foresees the LCD Display Panel market by type and application.

Geographically, the report includes the research on production, consumption, revenue, market share and growth rate, and forecast (2016 -2026) of the following regions: ● United States

The report delivers a comprehensive study of all the segments and shares information regarding the leading regions in the market. This report also states import/export consumption, supply and demand Figures, cost, industry share, policy, price, revenue, and gross margins.

The report delivers a comprehensive study of all the segments and shares information regarding the leading regions in the market. This report also states import/export consumption, supply and demand Figures, cost, industry share, policy, price, revenue, and gross margins.

Is there a problem with this press release? Contact the source provider Comtex at editorial@comtex.com. You can also contact MarketWatch Customer Service via our Customer Center.

This market research report includes a detailed segmentation of the global large area LCD display market by application (TVs, notebooks, monitors, tablets, and others). It outlines the market shares for key regions such as the Americas, APAC, and EMEA. The key vendors analyzed in this report are AU Optronics, BOE Technology, Innolux, LG Display, and Samsung Display.

Technavio’s research analyst predicts the global large area LCD display market to grow at a CAGR of 3% during the forecast period. The formation of UHD alliances is the primary growth driver for this market. During 2015, supply chain members of the global UHD TV market announced the formation of the UHD Alliance to support innovative technologies including 4K and higher resolution, high dynamic range, immersive 3D audio, and wider color gamut.

The decline in ASP of the LCD panel is expected to boost the market growth during the forecast period. During 2014, per meter square, ASP of LCD panel was $472, which declined to $416 during 2015. Vendors reduced the ASP to reduce excess inventory. The declining per square meter ASP of LCD panel drove the shipment of LCD display in terms of area.

During 2015, the TV segment dominated the large area LCD display market with a market share of 38%. The primary reason for the growth of this product segment was the strong demand for 4K TVs of 40 inches and larger screen size. During 2015, several manufacturers introduced 4K TVs ranging from 50 inches and above.

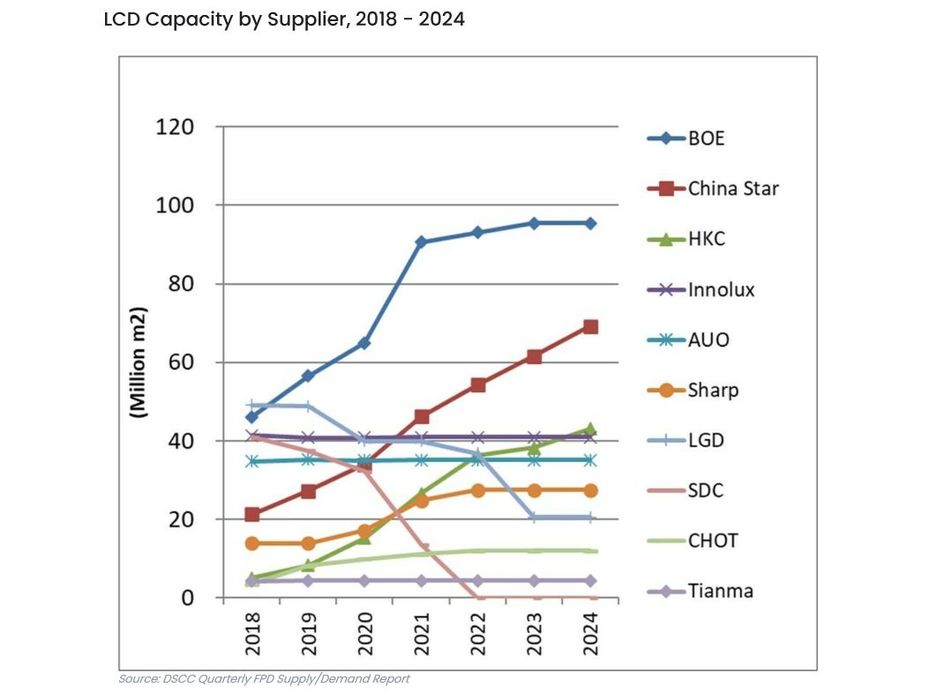

During 2015, APAC accounted for 81% of the market share and is expected to grow at a CAGR of 1% during the forecast period. The high concentration of display device manufacturers and LCD panel manufacturers in this region are the primary growth drivers. Technavio expects that the well-established supply chain for display devices in APAC would continue to support the dominance of this region in the market during the forecast period. China is emerging fast as a leading hub for large area TFT LCD display manufacturers because of the rise in the number of display device manufacturers in the country.

Manufacturing LCD display panels require economies of scale because the equipment used to manufacture displays are expensive. This presents high entry barriers for LCD display panel manufacturers. Currently, the global large area LCD display market is dominated by China, Japan, South Korea, and Taiwan in terms of production and revenue contribution. Chinese manufacturers have the advantage of manufacturing LCD panels at a lower cost. This has resulted in price wars among LCD manufacturers and has accelerated the declining ASP of LCD panels. Vendors such as LG and Samsung are under a lot of pressure as profit margins have come down because of increased competition.

Other prominent vendors in the market include Chi Mei Optoelectronics, Chunghwa Picture Tube (CPT), HannsTouch Solution, HannStar Display, InfoVision Optoelectronics, Japan Display, Kaohsiung Opto-Electronics, NEC Display Solutions, Panasonic, and Sharp.

The quantum dot display market is forecast to be valued at over US$ 4 Bnin 2022, experiencing a Y-o-Y increase of 30%as compared to 2021. Future projections indicate that the market will surge over 17xto reach US$ 69.79 Bnby 2032.

Over the historical period 2017-2021, the global quantum dot display surged at approximately 30%CAGR. Growing demand in downstream markets for energy-efficient display panels such as televisions, smartphones, tablets, personal computers and other electronics has forced OEMs and display manufacturers to build state-of-the-art displays capable of delivering maximum energy efficiency and increasing color quality.

During the height of the COVID-19 pandemic crisis, the market experienced significant turbulence. Given the imposition of strict lockdowns, manufacturing units were compelled to cease operations temporarily, affecting output of essential equipment required for quantum dot displays such as cadmium. However, prospects began rebounding once these restrictions were lifted.

Quantum dot displays are well suited for displays due to properties such as high luminous efficacy, high brightness, and low power consumption. The use of inorganic materials prevents burn-ins, which are common in other types of displays. The numerous benefits of using quantum dot displays will be a major factor driving market growth, with Fact.MR projecting a 33%CAGR through 2032.

Modern displays not only offer higher brightness and contrast ratios but are also available in higher resolutions and consume less power than conventional displays. Display manufacturers are developing displays with improved specifications to strengthen their position in the market.

In recent years, there has been a significant rise in the demand for large-size and high-resolution displays owing to the enhanced visual experience and the decreasing prices of LCDs.

Big-screen displays have become more affordable due to the reduced LCD prices. Owing to the growing focus of display manufacturers on the production of 4K and 8k displays, there has been an increasing demand for quantum dots due to their ability to enhance the display. The adoption of quantum dots in displays provides advantages such as higher image frame rates, greater bit depth, and a wider color gamut.

However, many companies and research associations are producing alternatives for cadmium-based quantum dots. Elements such as indium and zinc are suitable substitutes for cadmium for the development of quantum dots. Soon, cadmium-free quantum dots are expected to be widely available and are expected to dominate the market as a result of their safety, strong performance, and environmental benefits.

North America dominates the global quantum dots market, owing primarily to the high demand for QLEDs and early adoption of the technology. Furthermore, the population"s increased awareness of health and fitness drives the quantum dots market size.

Furthermore, the presence of technology providers, as well as increasing investments by government agencies and aerospace & defense in research and development of machine learning technology, influence market growth. A market share worth 40%is projected for the North American market.

The global quantum dot display market across APAC is estimated to grow at a CAGR of over 32% over the forecast period. Increasing demand for energy-efficient technologies are the primary factors for increased demand for quantum dot displays in countries like China and India.

Rising internet penetration and large tech-savvy younger population have underpinned robust demand for television sets and smartphones. This presents a great potential for the quantum dot display market.

The introduction of quantum display devices into the display industry has the potential to create a new model that could replace LCD panels. Top-tier competitors in the quantum dot display market are developing devices that use cadmium-free quantum dot technology.

The quantum dot display market is consolidated with a few prominent manufacturers namely Samsung Electronics Co. Ltd., LG Display Co. Ltd., Sony Corporation, Sharp Corporation and CSOT (China Star Optoelectronics Technology), acquiring a share of more than 70%. Numerous approaches, such as expansion, introduction of new products, joint ventures, agreements, alliances and acquisitions, are being employed by top competitors. Some of the other developments in the market are:

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey