lcd panel manufacturers market share 2018 brands

The global LCD TV (Liquid Crystal Display Television) market was dominated by Samsung and remained so in 2021 with a market share of over 19 percent by sales volume. LG Electronics takes second place with close to 13 percent in the same year, to beat TLC, one of the well-established brands in this segment.Read moreMarket share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volumeCharacteristic202120202019----

TCL. (March 11, 2022). Market share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volume [Graph]. In Statista. Retrieved December 24, 2022, from https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/

TCL. "Market share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volume." Chart. March 11, 2022. Statista. Accessed December 24, 2022. https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/

TCL. (2022). Market share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volume. Statista. Statista Inc.. Accessed: December 24, 2022. https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/

TCL. "Market Share of Leading Lcd Tv Manufacturers Worldwide from 2019 to 2021, by Sales Volume." Statista, Statista Inc., 11 Mar 2022, https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/

TCL, Market share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volume Statista, https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/ (last visited December 24, 2022)

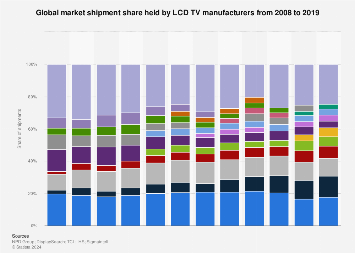

This statistic shows the global market share held by TV manufacturers from 2008 to 2019 (measured from shipments). In 2019, Samsung held a share of 17.8 percent of the worldwide TV shipments.

In 2019, Samsung was the market leader in the manufacture of TVs in terms of its share of global shipments. The South Korean company held approximately18 percent of worldwide shipments in 2019, almost five percent more than the share of its closest competitor, TCL Electronics. As a result of Samsung’s continued success in this market, as well as its significant share in the smartphone market, the company’s global revenue exceeded 200 billion U.S. dollars three years in a roll in 2019.

Although Sony remains amongst the largest TV manufacturers, it has seen its market share more than halve from 13.7 percent in 2008 to just 4.2 percent in 2019. Yet LCD TVs remain a key segment, which is the largest sector for Sony in its consumer electronics business segment.Read moreGlobal market shipment share held by LCD TV manufacturers from 2008 to 2019CharacteristicSamsungTCLLG ElectronicsHisenseSkyworthXiaomiSonyChanghongAOC/TP VisionKonkaSharpHaierPanasonicVizioToshibaOthers-----------------

DisplaySearch, & TCL, & IHS. (May 4, 2020). Global market shipment share held by LCD TV manufacturers from 2008 to 2019 [Graph]. In Statista. Retrieved December 24, 2022, from https://www.statista.com/statistics/267095/global-market-share-of-lcd-tv-manufacturers/

DisplaySearch, und TCL, und IHS. "Global market shipment share held by LCD TV manufacturers from 2008 to 2019." Chart. May 4, 2020. Statista. Accessed December 24, 2022. https://www.statista.com/statistics/267095/global-market-share-of-lcd-tv-manufacturers/

DisplaySearch, TCL, IHS. (2020). Global market shipment share held by LCD TV manufacturers from 2008 to 2019. Statista. Statista Inc.. Accessed: December 24, 2022. https://www.statista.com/statistics/267095/global-market-share-of-lcd-tv-manufacturers/

DisplaySearch, and TCL, and IHS. "Global Market Shipment Share Held by Lcd Tv Manufacturers from 2008 to 2019." Statista, Statista Inc., 4 May 2020, https://www.statista.com/statistics/267095/global-market-share-of-lcd-tv-manufacturers/

DisplaySearch & TCL & IHS, Global market shipment share held by LCD TV manufacturers from 2008 to 2019 Statista, https://www.statista.com/statistics/267095/global-market-share-of-lcd-tv-manufacturers/ (last visited December 24, 2022)

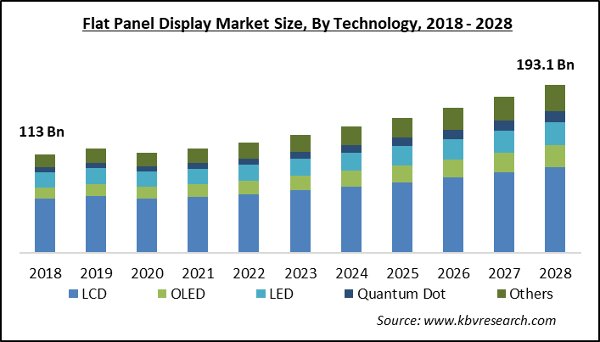

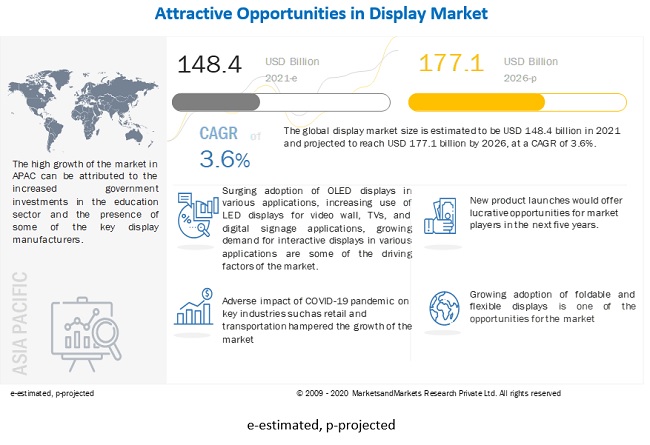

Chicago, Oct. 31, 2022 (GLOBE NEWSWIRE) -- The report "Display MarketDisplay Market by Product (Smartphones, Wearables, Television Sets, Signage, Tablets), Resolution, Display Technology (LCD, OLED, Direct-View LED, Micro-LED), Panel Size, Vertical, and Geography (2021-2026)", The global display market size was valued at USD 148.4 billion in 2021 and is projected to reach USD 177.1 billion by 2026. It is expected to grow at a CAGR of 3.6% during the forecast period. Surging adoption of OLED displays in various applications, increasing use of LED displays for video wall, TVs, and digital signage applications, growing demand for interactive displays in various applications, and rising demand for display-based medical equipment, including ventilators and respirators, due to COVID-19 pandemic are the key driving factors for the display market.

The display market comprises major players such as Samsung Electronics (South Korea), LG Display (South Korea), Sharp (Foxconn) (Japan), Japan Display (Japan), Innolux (Taiwan), NEC Corporation (Japan), Panasonic Corporation (Japan), Leyard Optoelectronic (Planar) (China), BOE Technology (China), AU Optronics (Taiwan), and Sony (Japan). These top players have strong portfolios of display products and presence in both mature and emerging markets.

The device solutions business division comprises memory systems, large-scale integrated circuits, and light emitting diode. The Display Panels division designs and manufactures LED-LCD, QD-LCD, and OLED display panels. The Consumer Electronics (CE) and IT & Mobile Communications (IM) divisions fall under Samsung Research, which is the advanced research and development (R&D) hub of Samsung Electronics. The hub leads the development of future technologies with more than 10,000 researchers and developers working in overseas R&D centers.

LG Display is a leading player in the LCD display segment. It has expanded its manufacturing capabilities in recent years by installing new manufacturing plants for LCD and OLED panels. Recently, the company set up a new development center in China. LG Display offers a wide range of display panels for televisions, smartphones, tablets, desktop computers, automobiles, and smart wearables. It is focused on offering cost-competitive display products and maintains stable and long-term relationships with its customers. The company is more focused on the development of automotive OLED display panels for autonomous cars.

LED displays are among the most used type of display technology for various applications. It holds a larger size of the market as compared to other technologies. In recent years, the LED display industry has matured, but not in terms of innovation. One of the recent advancements in LED displays is the miniaturization of the parts needed to build an LED screen. Miniaturization has enabled LED screens to become ultra-thin and grow to huge sizes, allowing screens to rest on any surface, inside or outside. Applications of LEDs have multiplied, largely in part due to technological advancements, including enhanced resolution, greater brightness capabilities, product versatility, and the development of hardened surface LEDs and micro LEDs.

LED displays are also widely used for digital signage applications, such as for advertising, and digital billboards, which helps brands to stand out from the rest. For instance, in August 2018, Peppermill Casino in Reno, Nevada, mounted a curved LED digital signage video wall from Samsung. Thus, LED displays are widely used to improve customer experience. Some of the leaders in this field are Samsung Electronics (South Korea) and Sony (Japan), followed by LG Corporation (South Korea) and NEC Corporation (Japan).

Foldable displays have become popular in tablets, smartphones, and notebooks in recent years. Flexible display panels are bendable owing to the flexible substrates used to manufacture them. The flexible substrate can be plastic, metal, or flexible glass; plastic and metal panels are light, thin, and durable and are virtually shatterproof. Foldable phones are based on flexible display technology, which is built around OLED screens. Companies like Samsung and LG are mass-producing flexible OLED display panels for smartphones, television sets, and smartwatches. However, these displays are not exactly flexible from end users’ perspective; manufacturers bend or curve these display panels and use them in end products. Some of the major developers of foldable OLED technologies include Samsung and BOE Technology. In May 2018, BOE demonstrated several new technologies, including a 6.2-inch 1440x3008 foldable (1R) OLED display with a touch layer and a foldable 7.56" 2048x1535 OLED.

Many countries had imposed or are continuing to impose lockdowns to contain the spread of COVID-19. This has disrupted the supply chain of various markets, including the display market. Supply chain hindrances are creating challenges for display manufacturers in manufacturing and supplying their products. China is the worst-hit country in terms of display manufacturing due to COVID-19. The manufacturers were allowed only 70% to 75% of capacity utilization compared to the normal rate of 90% to 95%. For instance, Omdia Display, a display manufacturer in China, expects a 40% to 50% drop in its overall display production due to a shortage of labor, shortage of logistics support, and quarantine procedures.

The market for equipment to manufacture LCD and OLED displays for smartphones and TVs grew 28% in 2018 following a growth of 33% in 2017. Applied Materials" (NASDAQ:AMAT) revenues grew 36%. A key driver for AMAT"s strong performance was the sale of equipment to Chinese LCD manufacturers BOE Technology and China Star Optoelectronics Technology to manufacture 10.5G panels for the production of 75-inch LCD TVs.

While the 10.5G market will be strong again in 2019, AMAT will face headwinds in sectors that utilize equipment for the production of smaller displays, primarily smartphones.

During Applied Materials’ recent Q1 earnings call, CEO Gary Dickerson noted: "In display, weakness in emerging markets is also impacting the timing of customers’ investment plans. We see some TV factory projects pushing out of year and into 2020. As a result, we now believe our display equipment revenue in 2019 will decline by about a third from 2018"s record levels. We also expect revenue in the second fiscal quarter to be significantly lower than our average run rate for the year."

Figure 1 shows market shares among the top five equipment companies. AMAT’s market share increased from 29% to 30%. Lithography equipment supplier Nikon (OTCPK:NINOY) increased 1% while competitor Canon (CAJ) decreased 1%. The biggest gainer was deposition company Tokyo Electron (OTCPK:TOELY), which gained 4% at the expense of fellow Japanese deposition equipment supplier Ulvac, which dropped 5%.

Providing more granularity, market share growth ofAMAT and Nikon is primarily attributed to the investments by BOE in its 10.5G LCD. Both equipment companies are the only suppliers of equipment (AMAT for deposition and Nikon for lithography) that can fabricate the large 10.5G panels. So even though AMAT is a deposition company, its tool, acquired about 20 years ago from the acquisition of AKT, is the only one on the market big enough to accommodate 10.5G panels.

The display market can be segmented into three general segments – (1) LCD panels for TVs, (2) OLED panels for smartphones, and (3) LCD panels for Smartphones. Each of these has its own headwinds and tailwinds, which are impacting capital equipment expenditures. These issues I detail below. There are numerous ways to segment this industry, but I am detailing this segmentation for this article.

A driving force for 10.5G plant construction is that a 10.5G mother glass is 1.8 times larger than an 8.5G one in area and can be cut into six 75-inch panels. In comparison, a 7.5G glass substrate can be cut into only two 75-inch TV panels. Thus, there is a significant cost benefit of moving to the larger substrates.

AMAT’s deposition tools are used to form the backplane for LCD displays. The company’s deposition tools are the only ones capable of uniform coating of panels this size, which measure 3370mm x 2940mm. AMAT’s equipment can deposit various materials for the backplane.

Shown in Table 1 are the number of 10.5G panels being manufactured through 2018, with forecasts for panel production in 2019 and 2020, according to The Information Network’s report “OLED and LCD Markets: Technology, Directions and Market Analysis.”

10.5G represented a strong tailwind for AMAT and Nikon in 2018. For example, Nikon sold 13, 10.5G lithography systems in CY2018 representing 18% of systems sold. This compares to only one 10.5G system sold in CY2017.

BOE Technology’s first 10.5G fab, located in Hefei, entered volume production in the first half of 2018. China Star Optoelectronics Technology (CSOT) plans to build to kick off commercial operations of its 10.5G plant in March 2019, having installed equipment in 2018. Capex spends by these companies for these plants provided a significant portion of AMAT"s revenues for 2018.

For 2019, BOE’s second 10.5G line, to be located in Wuhan, is slated for volume production in 2020, with equipment installation in mid-2019. Sharp (OTCPK:SHCAY) will start equipment install at its new 10.5G LCD plant in Guangzhou in early 2019, with plans to kick off the first phase of the facility in Aug 2019 and to begin volume production in October 2019. LG Display (LPL) is building its 10.5G OLED P10 fab in Paju, Korea, but volume production is now scheduled at the beginning of 2021. Originally, the company planned to install equipment in 3Q 2018, but it may be pushed back to the beginning of 2020. With an oversupply of 10.5G panels as a result of BOE and CSOT production, display manufacturers are closely monitoring the market.

In addition to 10.5G mother glass for TVs, most LCD TVs are made using 8G glass. In 2018, LCD panel shipments increased 9% while TV area increased 11%, meaning that the average size of a TV is increasing. While some of the increase was due to shipments from BOE’s 10.5G plant, 8G plants were responsible for most of the growth. LG Display, for example, which makes LCD TVs from 8G mother glass, witnessed a 21% increase in area shipments, whereas Innolux, also without a 10.5G plant, reported an increase of 17% in area shipments. BOE, with both 8G and 10.5G plants, reported an area shipment increase of 17%.

I am neutral on AMAT in the OLED panel for smartphones. There are two issues. One is that AMAT’s equipment used in the production of OLEDs is being supplanted by competitor’s differentiating technology.

A second factor contributing to my neutral stance for AMAT in this OLED market is a sluggish smartphone market – the largest application for 6G OLED panels. Investment was minimal in 2018 as shown in Table 3. Also tied to sluggish smartphone sales is product distinction. Rigid OLED panels are not significantly better than lower-cost LTPS-LCD panels. With the capacity built up through 2018, utilization rates averaged 60%.

Table 4 presents The Information Network’s forecast of 6G OLED panel output to 2020. Again, panel output only increased 32,000 panels per month in 2018, but is expected to increase 138,000 panels per month in 2019, followed by a more moderate growth of 121,000 panels per month in 2020.

Flexible smartphones will drive the 6G market in 2019 and 2020. Samsung Electronics (OTCPK:SSNLF) introduced its Galaxy Fold and Huawei its Mate X in February 2018. Details of the two smartphones are described here. A significant difference between the two is the display.

In addition to the two, there are several other smartphone manufacturers that will introduce foldable models in the next two years. These include Oppo, Motorola (MSI), LG, Xiaomi (OTCPK:XIACF), and even Apple (AAPL).

I am bearish for AMAT on LCD panels for smartphones. Table 2 illustrates the drop in 6G plant expansion in 2018 showing Nikon’s lithography system sales by panel generation in 2017 and 2018. 6G systems dropped from 42 units in 2017 to 18 in 2018

Although flexible OLED has been gaining market share in the smartphone market in the last few years for its thinner form factor, higher performance, and differentiating design, the high utilization rates of 90% is minimizing the need for plant expansion and resulting in an oversupply of 20% for LCDs. Combined, these contribute to a 20% discount in LCD cost per smartphone compared to a rigid OLED display. Tianma is the top supplier of LTPS TFT-LCDs for smartphones with shipments of 149 million units in 2018, an increase of 49% YoY.

High-end smartphones like Apple"s current iPhone XS and iPhone XS Max use OLED screens to deliver better image quality, faster pixel response times. The XR uses an LCD display. It is likely we will see a similar lineup in 2019 - a continuation of both the iPhone XS and XR devices, with rumors suggesting 5.8 and 6.5-inch OLED iPhones along with a 6.1-inch LCD iPhone.

AMAT capitalized on the size of its deposition tools to generate strong revenue growth in the 10.5G market. In the other segments of the display production market (6G and 8G), its deposition tools for backplane and OLED encapsulation do not offer any advantages over competitors. In fact, the company is losing share to better technology.

The primary claim for AMAT"s display tools is its size. If 6G LCD factory expansion is dropping and 10.5G factories make panels with better economies of scale than 8G factories to make TVs, then it is only a matter of time before a competitor makes equipment that can deposit the backplanes on 10.5G panels.

With a market share of over 20%, Samsung has been the world’s largest TV manufacturer since 2006. It was the first TV company to launch a fully HD LED TV in 2010 at the Consumer Electronics Show (CES), Las Vegas. Samsung also accounts for almost 50% of total 75-inch TV sales worldwide. Samsung’s LCD display technology, QLED, uses quantum dots to enhance colors, enabling the viewer to see minute details on extremely bright or dark scenes. With increasing demand for large-screen TVs, the company is strengthening its QLED TV portfolio by incorporating additional features such as HDR 2000 and a 4K Q Engine, which optimizes high-resolution content for screens larger than 65 inches.

LG is the second-largest TV manufacturer in the world, accounting for about 12% of the market. The company offers a wide range of OLED TVs, UHD TVs, super UHD TVs, smart TVs, and LED TVs. It has been the world’s bestselling OLED TV brand since 2013. With extensive experience in television manufacturing under its belt, LG has been a pioneer in the innovation of new technologies. For instance, LG OLED TVs are loaded with AI ThinQ technology, which integrates Natural Language Processing (NLP) to deliver intelligent voice activated control. LG Super UHD TVs come with full array dimming technology, which produces clear and crisp images with superb contrast by controlling backlight units individually.

Sony is one of the leading TV manufacturing companies in the world and makes up close to 7% of the market. Sony focuses on innovation and technological advancements to improve the viewer’s overall experience. Bravia, Sony’s flagship TV product line, comes fitted with an X1 Extreme processor that controls over 8 million self-illuminating pixels to provide 4K HDR (High Dynamic Range) display. It also employs Acoustic Surface technology, wherein sound comes directly from the screen, so that sound and special effects can be heard precisely from the right place.

TCL is one of the fastest growing TV manufacturers offering 2K LED TVs, UHD Android TVs, UHD Smart TVs, FHD/HD Smart TVs, and FHD/HD Slim Led TVs at low prices. Companies such as Alcatel and Samsung have outsourced the manufacturing of some models of LCD television to TCL because of its strategic location to lower the production costs. To spread their brand name, TCL have partnered with many companies in the fields of sports, entertainment, music and technology. The company uses TCL Wide Color Gamut technology to deliver the purest LED backlight, which in turn helps to improve display performance and the vividness of the picture. Moreover, TCL brand TVs come equipped with built-in Chromecast that allows users to cast videos or games directly to their TVs.

Skyworth ranks among the top ten TV manufacturers in the world and is expected to increase its market share in the coming years. The company specializes in the development and manufacturing of consumer electronics, display devices, digital set top boxes, security monitors, semiconductors, refrigerators, washing machines, cell phones, and ED lighting. The company offers a wide range of televisions, including OLED TVs, 4K Android TVs, 4K Smart TVs, 2K Android TVs, and digital LED TVs. Q3 is Skyworth’s latest high-end TV series offering, with modern design, excellent picture performance, exquisite sound, and artificial intelligence functions.

Panasonic is one of the best TV brands in the world, leading the evolution of televisions from colorization and digitization to flat panels and higher resolutions. The company is focusing on the research and development of visual image processing technologies to provide end-to-end ultra HD solutions. The company has incorporated its technology and extensive knowledge of TV manufacturing into its Studio Color HCX2 Processor to deliver detailed HDR pictures in bright and dark areas in its latest 4K OLED television series.

Vizio is a relatively new TV manufacturing company and is best known as a producer of flat screen HDTVs. To compete against the heavyweights of the consumer electronics market, the company is concentrating on aggressive pricing of its products. Vizio is investing in research and development to deliver high-performance products with the least energy usage, thereby reducing the overall cost of their products for their customers. Vizio TVs support voice control and can be paired with Amazon Echo and Google Assistant. Users can also mirror their laptops or mobile devices to their television sets with the help of a built-in Chromecast.

BOSTON, October 17, 2022--(BUSINESS WIRE)--According to the Strategy Analytics Handset Component Technologies service report, "Smartphone Display Panel Market Share Q2 2022: LCD Panel Revenues Plunge", the global smartphone display panel market registered a revenue of $20 billion in H1 2022.

The report finds that the smartphone display panel market posted a 5 percent revenue decline year-over-year in H1 2022. The market continues to be led by Samsung Display with 53 percent revenue share followed by BOE Technology with 15 percent and Tianma Microelectronics with 8 percent in H1 2022. The top-three display panel vendors captured nearly 76 percent revenue share in the global smartphone display panel market during the period.

Jeffrey Mathews, Senior Analyst at Strategy Analyticscommented, "The market for smartphone display panels was held back by sinking LCD panel demand while OLED adoption expanded across mid-tier smartphones to enable OEMs to drive momentum. Display vendors saw rising demand for Flexible OLED panels with high refresh rate specifications which drove OLED growth during the period. Samsung Display was strongly positioned to benefit from customer demand enabling a strong pipeline of design wins for its OLED panels. BOE, TCL CSOT and Tianma ramped their OLED production and captured orders to supply OLED panels to leading smartphone brands in H1 2022."

Stephen Entwistle, Vice President of the Strategic Technologies Practice at Strategy Analytics noted, "We expect momentum for OLED panels to continue and drive market growth enabled by stronger display supplier competition and increased panel yield for OLED displays. LCD panels are expected to be in oversupply leading to further price declines. The weak macroeconomic sentiments pose a strong risk to the overall prospects of growth for the smartphone display panel market."

Strategy Analytics, Inc. is a global leader in supporting companies across their planning lifecycle through a range of customized market research solutions. Our multi-discipline capabilities include industry research advisory services, customer insights, user experience design and innovation expertise, mobile consumer on-device tracking and business-to-business consulting competencies. With domain expertise in smart devices, connected cars, intelligent home, service providers, IoT, strategic components and media, Strategy Analytics can develop a solution to meet your specific planning need. For more information, visit us at www.strategyanalytics.com.

Flat-panel displays are thin panels of glass or plastic used for electronically displaying text, images, or video. Liquid crystal displays (LCD), OLED (organic light emitting diode) and microLED displays are not quite the same; since LCD uses a liquid crystal that reacts to an electric current blocking light or allowing it to pass through the panel, whereas OLED/microLED displays consist of electroluminescent organic/inorganic materials that generate light when a current is passed through the material. LCD, OLED and microLED displays are driven using LTPS, IGZO, LTPO, and A-Si TFT transistor technologies as their backplane using ITO to supply current to the transistors and in turn to the liquid crystal or electroluminescent material. Segment and passive OLED and LCD displays do not use a backplane but use indium tin oxide (ITO), a transparent conductive material, to pass current to the electroluminescent material or liquid crystal. In LCDs, there is an even layer of liquid crystal throughout the panel whereas an OLED display has the electroluminescent material only where it is meant to light up. OLEDs, LCDs and microLEDs can be made flexible and transparent, but LCDs require a backlight because they cannot emit light on their own like OLEDs and microLEDs.

Liquid-crystal display (or LCD) is a thin, flat panel used for electronically displaying information such as text, images, and moving pictures. They are usually made of glass but they can also be made out of plastic. Some manufacturers make transparent LCD panels and special sequential color segment LCDs that have higher than usual refresh rates and an RGB backlight. The backlight is synchronized with the display so that the colors will show up as needed. The list of LCD manufacturers:

Organic light emitting diode (or OLED displays) is a thin, flat panel made of glass or plastic used for electronically displaying information such as text, images, and moving pictures. OLED panels can also take the shape of a light panel, where red, green and blue light emitting materials are stacked to create a white light panel. OLED displays can also be made transparent and/or flexible and these transparent panels are available on the market and are widely used in smartphones with under-display optical fingerprint sensors. LCD and OLED displays are available in different shapes, the most prominent of which is a circular display, which is used in smartwatches. The list of OLED display manufacturers:

MicroLED displays is an emerging flat-panel display technology consisting of arrays of microscopic LEDs forming the individual pixel elements. Like OLED, microLED offers infinite contrast ratio, but unlike OLED, microLED is immune to screen burn-in, and consumes less power while having higher light output, as it uses LEDs instead of organic electroluminescent materials, The list of MicroLED display manufacturers:

LCDs are made in a glass substrate. For OLED, the substrate can also be plastic. The size of the substrates are specified in generations, with each generation using a larger substrate. For example, a 4th generation substrate is larger in size than a 3rd generation substrate. A larger substrate allows for more panels to be cut from a single substrate, or for larger panels to be made, akin to increasing wafer sizes in the semiconductor industry.

"Samsung Display has halted local Gen-8 LCD lines: sources". THE ELEC, Korea Electronics Industry Media. August 16, 2019. Archived from the original on April 3, 2020. Retrieved December 18, 2019.

"TCL to Build World"s Largest Gen 11 LCD Panel Factory". www.businesswire.com. May 19, 2016. Archived from the original on April 2, 2018. Retrieved April 1, 2018.

"Panel Manufacturers Start to Operate Their New 8th Generation LCD Lines". 대한민국 IT포털의 중심! 이티뉴스. June 19, 2017. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"TCL"s Panel Manufacturer CSOT Commences Production of High Generation Panel Modules". www.businesswire.com. June 14, 2018. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"Business Place Information – Global Operation | SAMSUNG DISPLAY". www.samsungdisplay.com. Archived from the original on 2018-03-26. Retrieved 2018-04-01.

"Samsung Display Considering Halting Some LCD Production Lines". 비즈니스코리아 - BusinessKorea. August 16, 2019. Archived from the original on April 5, 2020. Retrieved December 19, 2019.

Herald, The Korea (July 6, 2016). "Samsung Display accelerates transition from LCD to OLED". www.koreaherald.com. Archived from the original on April 1, 2018. Retrieved April 1, 2018.

Byeonghwa, Yeon. "Business Place Information – Global Operation – SAMSUNG DISPLAY". Samsungdisplay.com. Archived from the original on 2018-03-26. Retrieved 2018-04-01.

www.wisechip.com.tw. "WiseChip History – WiseChip Semiconductor Inc". www.wisechip.com.tw. Archived from the original on 2018-02-17. Retrieved 2018-02-17.

"China"s BOE to have world"s largest TFT-LCD+AMOLED capacity in 2019". ihsmarkit.com. 2017-03-22. Archived from the original on 2019-08-16. Retrieved 2019-08-17.

The global display market size was valued at $114.9 billion in 2021, and is projected to reach $216.3 billion by 2031, growing at a CAGR of 6.7% from 2022 to 2031.

Display includes screen, computer output surface, and a projection surface that displays content, mainly test, graphics, pictures, and videos utilizing cathode ray tube (CRT), light-emitting diode (LED), liquid crystal display (LCD), and other technologies. These displays are majorly incorporated in devices such as televisions, smartphones, tablets, laptops, vehicles, and others. Emergence of advanced technologies offer enhanced visualizations in several industry verticals, which include consumer electronics, retail, sports & entertainment, and transportation. 3D displays are in trend in consumer electronics and entertainment sector.

In addition, flexible display technologies witness popularity at a high pace. Moreover, display technologies such as organic light-emitting diode (OLED) have gained increased importance in products such as televisions, smart wearables, smartphones, and other devices. Smartphone manufacturers plan to incorporate flexible OLED displays to attract consumers. Furthermore, the market is also in the process of producing energy saving devices, primarily in wearable devices. However, high cost of the transparent and quantum dot display technologies. Hence, need for such high costs associated with display products may hamper growth of the market. Furthermore, adoption of AR/VR devices and commercialization of autonomous vehicles are expected to provide lucrative display market opportunity for the growth of the market.

The COVID-19 pandemic is impacting the society and overall economy across the global. The impact of this outbreak is growing day-by-day as well as affecting the supply chain. It is creating uncertainty in the massive slowing of supply chain, and increasing panic among customers. European countries under lockdowns have suffered major loss of business and revenue due to shutdown of manufacturing units in the region. Operations of production and manufacturing industries have been heavily impacted by the outbreak of COVID-19, which led to slowdown in the display market growth.

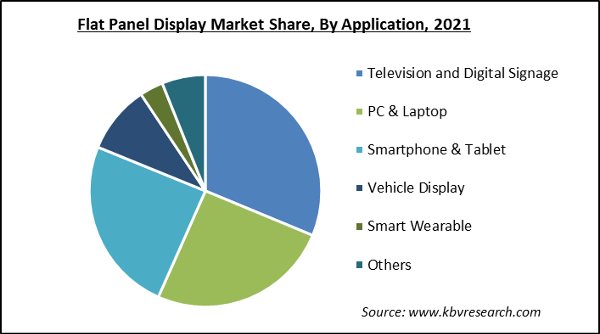

By display type, the display market outlook is divided into flat panel display, flexible panel display, and transparent panel display. Flat panel display segment was the highest revenue contributor to the market, in 2021. The flexible panel display segment dominated the display market growth, in terms of revenue, in 2021, and is expected to follow the same trend during the forecast period.

By industry vertical, the market it is divided into healthcare, consumer electronics, retail, BFSI, military & defense, transportation, and others.Consumer electronics accounted for largest display market share in 2021.

Region wise, the display market trends are analyzed across North America (the U.S., Canada, and Mexico), Europe (UK, Germany, France, and rest of Europe), Asia-Pacific China, Japan, India, South Korea, and rest of Asia-Pacific), and LAMEA (Latin America, the Middle East, and Africa). Asia-Pacific, specifically the China, remains a significant participant in the global display industry. Major organizations and government institutions in the country are intensely putting resources into these displays.

Top impacting factors of the market include high demand for flexible display technology in consumer electronic devices, increase in adoption of electronic components in the automotive sector, and rise in trend of touch-based devices. Surge in adoption of displays in touch screen devices, rise in need for AR/VR devices, and commercialization of autonomous vehicles are expected to create lucrative in the future. Moreover, stagnant growth of desktop PCs, notebooks, and tablets hampers growth of the display market. However, each of these factors is expected to have a definite impact on growth of the display industry in the coming years.

The key players profiled in this report include LG Display Co. Ltd., Samsung Electronics Co. Ltd., AU Optronics, Japan Display Inc., E Ink Holdings Inc., Hannstar Display Corporation, Corning Incorporated, Kent Displays Inc., NEC Display Solutions, and Sony Corporation. These key players have adopted strategies, such as product portfolio expansion, mergers & acquisitions, agreements, regional expansion, and collaborations to enhance their market penetration.

KEY BENEFITSFOR STAKEHOLDERSThis study comprises analytical depiction of the display market forecast along with the current trends and future estimations to depict the imminent investment pockets.

Key Market Players Samsung Electronics Co Ltd, Sharp Corporation, Japan Display Inc, Innolux Corporation, NEC CORPORATION, Panasonic Corporation, BOE Technology Group Co., Ltd., AUO Corporation, Sony Corporation, Leyard Optoelectronic Co., Ltd, LG Display Co Ltd

Samsung Electronics Co., Ltd. (Korean: 삼성전자; Hanja: 三星電子; RR: Samseong Jeonja; lit. Tristar Electronics, sometimes shortened to SEC and stylized as SΛMSUNG) is a South Korean multinational electronics corporation headquartered in Yeongtong-gu, Suwon, South Korea.Samsung chaebol, accounting for 70% of the group"s revenue in 2012.circular ownership.assembly plants and sales networks in 74 countries and employs around 290,000 people.second-largest technology company by revenue, and its market capitalization stood at US$520.65 billion, the 12th largest in the world.

Samsung is a major manufacturer of Electronic Components such as lithium-ion batteries, semiconductors, image sensors, camera modules, and displays for clients such as Apple, Sony, HTC, and Nokia.smartphones, starting with the original Samsung SolsticeSamsung Galaxy line of devices.tablet computers, particularly its Android-powered Samsung Galaxy Tab collection, and is regarded for developing the phablet market with the Samsung Galaxy Note family of devices.Galaxy S22, and foldable phones including the Galaxy Z Fold 4. Samsung has been the world"s largest television manufacturer since 2006,memory chip manufacturerIntel, the decades-long champion.

In 2012, Kwon Oh-Hyun was appointed the company"s CEO. He announced in October 2017 that he would resign in March 2018, citing an “unprecedented crisis”.

As Samsung shifted away from consumer markets, the company devised a plan to sponsor major sporting events. One such sponsorship was for the 1998 Winter Olympics held in Nagano, Japan.

In 2009 and 2010, the US and EU fined the company, along with eight other memory chip manufacturers, for its part in a price-fixing scheme that occurred between 1999 and 2002. Other companies fined included Infineon Technologies, Elpida Memory, and Micron Technology.immunity to Samsung Electronics for acting as an informant during the investigation (LG Display, AU Optronics, Chimei InnoLux, Chunghwa Picture Tubes, and HannStar Display were implicated as a result of the company"s intelligence).

In April 2011, Samsung Electronics sold its HDD commercial operations to Seagate Technology for approximately US$1.4 billion. The payment was composed of 45.2 million Seagate shares (9.6 percent of shares), worth US$687.5 million, and a cash sum for the remainder.

In April 2013, Samsung Electronics" new entry into its Galaxy S series smartphone range, the Galaxy S4 was made available for retail. Released as the upgrade of the best-selling Galaxy S III, the S4 was sold in some international markets with the company"s Exynos processor.

Samsung"s mobile business chief Shin Jong-Kyun stated to the Korea Times on 11 September 2013 that Samsung Electronics will further develop its presence in China to strengthen its market position in relation to Apple. The Samsung executive also confirmed that a 64-bit smartphone handset will be released to match the ARM-based A7 processor of Apple"s iPhone 5s model that was released in September 2013.

Due to smartphone sales—especially sales of lower-priced handsets in markets such as India and China—Samsung achieved record earnings in the third quarter of 2013. The operating profit for this period rose to about ₩10.1 trillion (equivalent to ₩10.61 trillion or US$9.38 billion in 2017)2580.

In mid-November 2021, Samsung Electronics was ranked second in the "Best Global Brands" by YouGov a market research firm, after placing fourth in the 2020 ranking.

In June 2022, PricewaterhouseCoopers ranked Samsung Electronics 22nd on their global top 100 companies by market capitalization. The company slid seven notches from the 2021 rankings due to global inflation, the war in Ukraine, and global monetary tightening.

Samsung Electronics produces LCD and LED panels, mobile phones, memory chips, NAND flash, solid-state drives, televisions, digital cinemas screen, and laptops and many more products. The company previously produced hard-drives and printers.

In October 2007, Samsung introducing a ten-millimeter thick, 40-inch LCD television panel, followed in October 2008 by the world"s first 7.9-mm panel.

While many other handset manufacturers focused on one or two operating systems, Samsung for a time used several of them: Symbian, Windows Phone, Linux-based LiMo, and Samsung"s proprietary TouchWiz, Bada and Tizen.

At the end of the third quarter of 2010, the company had surpassed the 70 million unit mark in shipped phones, giving it a global market share of 22 percent, trailing Nokia by 12 percent.

During the third quarter of 2013, Samsung"s smartphone sales improved in emerging markets such as India and the Middle East, where cheaper handsets were most popular. As of October 2013, the company offers 40 smartphone models on its US website

Since the early 1990s, Samsung Electronics has commercially introduced a number of new memory technologies.SDRAM (synchronous dynamic random-access memory) in 1992,DDR SDRAM (double data rate SDRAM) and GDDR (graphics DDR) SGRAM (synchronous graphics RAM) in 1998.30 nm-class NAND flash memory,DRAM and 20 nm class NAND flash, both of which were for the first time in the world.TLC (triple-level cell) NAND flash memory in 2010,V-NAND flash in 2013,LPDDR4 SDRAM in 2013,HBM2 in 2016,GDDR6 in January 2018,LPDDR5 in June 2018.

Another area where the company has had significant business in for years is the foundry segment. It had begun investment in the foundry business since 2006, and positioned it as one of the strategic pillars for semiconductor growth.semiconductor device fabrication. Samsung began mass-production of a 20 nm class semiconductor manufacturing process in 2010,10 nm class FinFET process in 2013,7 nm FinFET nodes in 2018. They also began production of the first 5 nm nodes in late 2018,3 nm GAAFET nodes by 2021.

According to market research firm Gartner, during the second quarter of 2010, Samsung Electronics took the top position in the DRAM segment due to brisk sales of the item on the world market. Gartner analysts said in their report, "Samsung cemented its leading position by taking a 35-percent market share. All the other suppliers had minimal change in their shares." The company took the top slot in the ranking, followed by Hynix, Elpida, and Micron, said Gartner.

In 2010, market researcher IC Insights predicted that Samsung would become the world"s-biggest semiconductor chip supplier by 2014, surpassing Intel. For the ten-year period from 1999 to 2009, Samsung"s compound annual growth rate in semiconductor revenues was 13.5 percent, compared with 3.4 percent for Intel.semiconductor company in 2017.

In 2016, Samsung also launched to market a 15.36TB SSD with a price tag of US$10,000 using a SAS interface, using a 2.5-inch form factor but with the thickness of 3.5-inch drives. This was the first time a commercially available SSD had more capacity than the largest currently available HDD.M.2 NVMe SSD with read speeds of 3500 MB/s and write speeds of 3300 MB/s in the same year.

In the area of storage media, in 2009 Samsung achieved a ten percent world market share, driven by the introduction of a new hard disk drive capable of storing 250Gb per 2.5-inch disk.Seagate in 2011 in return for a 9.6% ownership stake in Seagate.

In 2009, Samsung sold around 31 million flat-panel televisions, enabling to it to maintain the world"s largest market share for a fourth consecutive year.

Samsung sold more than one million 3D televisions within six months of its launch. This is the figure close to what many market researchers forecast for the year"s worldwide 3D television sales (1.23 million units).

In 2007, Samsung introduced the "Internet TV", enabling the viewer to receive information from the Internet while at the same time watching conventional television programming. Samsung later developed "Smart LED TV" (now renamed to "Samsung Smart TV"),smart television apps. In 2008, the company launched the Power Infolink service, followed in 2009 by a whole new Internet@TV. In 2010, it started marketing the 3D television while unveiling the upgraded Internet@TV 2010, which offers free (or for-fee) download of applications from its Samsung Apps Store, in addition to existing services such as news, weather, stock market, YouTube videos, and movies.

During the 1990s to the 2000s, Samsung started producing LCD monitors using TFT technology to which it still emphasizes on the budget market against the competition while at the same time starting to also focus on catering to the middle and upper markets through partnership with brands such as NEC and Sony via a joint venture.S-LCD Corporation respectively from its former joint venture partners.

In 2019, Samsung announced that they will be bringing the Apple TV app (formally iTunes Movies and TV Shows app) and AirPlay 2 support to its 2019 and 2018 smart TVs (via firmware update).

Samsung has introduced several models of digital cameras and camcorders including the WB550 camera, the ST550 dual-LCD-mounted camera, and the HMX-H106 (64GB SSD-mounted full HD camcorder). In 2014, the company took the second place in the mirrorless camera segment.

Samsung entered the MP3 player (digital audio player, DAP) market in 1999 with its Yepp line. In the initial years the company struggled to gain a foothold because of emerging Korean startups iRiver, Cowon and Mpio. However by 2006, it had gained a significant share in the domestic market as well as Russia and parts of the Middle East, South East Asia and Europe.DivX MP3 player, the R1, in 2009.

The company added a new digital imaging business division in 2010, and consists of eight divisions, including the existing display, IT solutions, consumer electronics, wireless, networking, semiconductor, and LCD divisions.

Despite recent litigation activity, Samsung and Apple have been described as frenemies who share a love-hate relationship.Tim Cook originally opposed litigation against Samsung wary of the company"s critical component supply chain for Apple.

In April 2011, Apple Inc. announced that it was suing Samsung over the design of its Galaxy range of mobile phones. The lawsuit was filed on 15 April 2011 and alleges that Samsung infringed on Apple"s trademarks and patents of the iPhone and iPad.counterclaim against Apple of patent infringement.preliminary injunction against the sale and marketing of the Samsung Galaxy Tab 10.1 across the whole of Europe excluding the Netherlands.

All Samsung mobile phones and MP3 players introduced on the market after April 2010 are free from polyvinyl chloride (PVC) and brominated flame retardants (BFRs).

The company is listed in Greenpeace"s Guide to Greener Electronics, which rates electronics companies on policies and practices to reduce their impact on the climate, produce greener products, and make their operations more sustainable. In November 2011, Samsung was ranked seventh out of 15 leading electronics manufacturers with a score of 4.1/10.

In December 2010, the European Commission fined six LCD panel producers, including Samsung, a total of €648 million for operating as a cartel. The company received a full reduction of the potential fine for being the first firm to assist EU anti-trust authorities.

On 19 October 2011, Samsung was fined €145.73 million for being part of a price cartel of ten companies for DRAMs, which lasted from 1 July 1998 to 15 June 2002. Like most of the other members of the cartel, the company received a 10% reduction for acknowledging the facts to investigators. Samsung had to pay 90% of their share of the settlement, but Micron avoided payment as a result of having initially revealed the case to investigators. Micron remains the only company that avoided all payments from reduction under the settlement notice.

In Canada, the price fix was investigated in 2002. A recession started to occur that year, and the price fix ended. However, in 2014, the Canadian government reopened the case and investigated silently after the EU"s success. Sufficient evidence was found and presented to Samsung and two other manufacturers during a class action lawsuit hearing. The companies agreed upon a $120 million agreement, with $40 million as a fine, and $80 million to be paid back to Canadian citizens who purchased a computer, printer, MP3 player, gaming console or camera between April 1999 and June 2002.

On 1 April 2013, several documents were shown on TaiwanSamsungLeaks.org saying that the advertising company OpenTide (Taiwan) and its parent company Samsung were hiring students to attack its competitors by spreading harmful comments and biased opinions/reviews about the products of other phone manufacturers, such as Sony and HTC, in several famous forums and websites in Taiwan to improve its brand image. Hacker "0xb", the uploader of the documents, said that they were intercepted from an email between OpenTide and Samsung.

Kim, Gil; Keon Han; Minseok Sinn; Hyung Cho; Ray Kim (18 June 2014). "Korea Market Strategy – How to untangle Samsung group"s ownership?". Credit Suisse. p. 36. Archived from the original on 5 February 2016. Retrieved 22 November 2015.

Chung-un, Cho (1 May 2017). "Samsung denies re-entry to auto market despite autonomous car push". The Korea Herald. Archived from the original on 3 May 2017. Retrieved 3 May 2017.

"New Samsung 3.9mm LED TV Panel Is World"s Thinnest". I4U. 28 October 2009. Archived from the original on 28 January 2011. Retrieved 16 November 2010.

"Nokia, LG Lose While ZTE, Apple Gain Q4 2010 Market Share". mobileburn.com. 28 January 2011. Archived from the original on 14 July 2011. Retrieved 19 February 2011.

"Samsung Remains Top DRAM Maker Amid Dramatic Market Growth". Dow Jones. 9 January 2010. Archived from the original on 21 November 2010. Retrieved 23 November 2010.

Killian, Zak (18 January 2018). "Samsung fires up its foundries for mass production of GDDR6 memory". Tech Report. Archived from the original on 19 January 2018. Retrieved 18 January 2018.

"Samsung Begins Producing The Fastest GDDR6 Memory in the World". Wccftech. 18 January 2018. Archived from the original on 3 July 2019. Retrieved 16 July 2019.

"Top 20 Semi Manufacturers from IC Insights". Electronics Weekly/EE Times. 30 July 2010. Archived from the original on 9 October 2010. Retrieved 23 November 2010.

"Samsung Lets You Store 500 Movies on a Laptop Hard Drive". VentureBeat. 7 April 2010. Archived from the original on 15 November 2018. Retrieved 11 September 2017.

"KOREA: LG, Samsung Aim Upmarket To Reinforce Their TV Market Lead". What Hi-Fi? Sound and Vision. 24 August 2010. Archived from the original on 24 October 2010. Retrieved 16 November 2010.

"삼성전자, IFA2012서 신규 스마트 TV앱 대거 공개 | SAMSUNG NEWSROOM". SAMSUNG NEWSROOM (in Korean). 3 September 2012. Archived from the original on 23 April 2018. Retrieved 22 April 2018.

"Samsung"s Tizen OS dominates global smart TV market". FierceVideo. 25 March 2019. Archived from the original on 23 August 2019. Retrieved 16 October 2019.

"SMD Enjoys Soaring Demand for AMOLED Panel". Maeil Business Newspaper. 1 July 2010. Archived from the original on 21 January 2012. Retrieved 26 November 2010.

"(Samsung"s share grows while Apple"s declines in Q3 smartphone market)". InfoWorld. 29 October 2013. Archived from the original on 4 December 2013. Retrieved 3 December 2013.

"Samsung offers apology and compensation to workers who got leukemia". The Verge. 14 May 2014. Archived from the original on 2 March 2018. Retrieved 11 September 2017.

Nair, Drishya (11 July 2013). "Samsung Galaxy S3 Explosion in Swiss Teenager"s Pocket Leaves Her Thigh Numb". International Business Times UK. Archived from the original on 15 July 2013. Retrieved 30 December 2018.

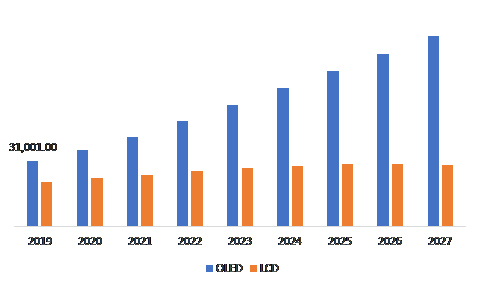

The global flexible display market size was accounted for USD 6.98 billion in 2018 and expected to grow with a CAGR of 28.1% over the forecast period, from 2019 to 2025. Factors such as the growing adoption of display-based consumer electronic devices and increasing demand for lightweight, flexible, and energy-efficient gadgets are driving the market growth. Further, advancement in technology has led to the introduction of state-of-the-art flexible displays, which is expected to open new business growth opportunities for industry players operating in this industry.

The growing adoption of flexible displays in automotive, healthcare, and other industries is expected to open new avenues for market growth. Further, automakers are concentrating on integrating this display in vehicle interiors. For instance, in 2019, Samsung Corporation and Audi AG partnered to promote the Audi Prologue A9 Prototype car. This car includes a high-resolution and flexible Samsung OLED display nearby its gear stick to control the vehicle settings.

Based on type, the market is segmented into OLED, EPD, LCD, and others. In 2018, OLED accounted for more than 60% market share and is projected to grow with a significant CAGR over the forecast period. OLED-based displays have high flexibility, are energy-efficient, and therefore are widely used in smartphones. In addition, they are lightweight and sleek in design as compared to LCD flexible displays. However, the growing adoption of flexible display-based e-readers is expected to boost the demand for Electronic Paper Displays (EPD) in the next few years.

Based on the application, the market is fragmented into wearable, televisions, smartphones, E-readers, automotive, and others. The smartphone application segment is projected to grow with a significant CAGR of more than 12% during the forecast period. Government initiatives for smart city projects, the introduction of

Based on material type, the market is segmented into plastic, glass, and metal. In 2018, the plastic segment accounted for the largest market share and further, expected to grow with a CAGR of 25% during the forecast period, from 2019 to 2025. This growth can be attributed to the increasing shift from glass to plastic substrates, as it provides added advantages like lightweight, robustness, and size.

Asia Pacific is expected to lead the global flexible display market and is projected to grow with a CAGR of more than 25% over the forecast period. This high revenue share can be attributed to the growing demand for lightweight and compact electronic devices. Further, the growing number of smartphone users coupled with the adoption of advanced technologies such as

In 2018, North America held a market share of over 20% and expected to witness robust growth during the forecast period due to the growing demand for durable and lightweight electronic devices. Europe"s market for flexible displays is projected to witness significant growth over the forecast period due to increasing demand for flexible displays from the automotive industry.

The outbreak of COVID-19 is adversely impacting flexible display market growth. This pandemic has forced many companies to halt their business operations for reducing the effect of virus infection. This halt in business operations has directly decreased the sales of consumer electronics devices as well as affected consumer demand and the availability of the supply chain. Furthermore, COVID-19 is also adversely impacting the automotive sector. Thus the demand for flexible displays is expected to decrease to some extent during a pandemic situation.

However, smartphone manufacturers are expected to expand their product line which contains OLED flexible displays. Further, Chinese smartphone manufacturers are focusing to resume their flexible display production integrated with OLED panels, which is expected to surge the market growth during the pandemic situation.

Key players are adopting strategies such as partnerships, collaborations, mergers, and acquisitions to strengthen their position in the competitive market. For example, in 2018, Royole Corporation introduced a foldable device FlexPai integrated with a flexible display. This device can be rolled, bent, and operated as both tablets and smartphones.

Leading players are investing in R&D to develop advanced designs in flexible displays for different consumer electronic devices. To sustain in competitive edge, they are also registering their patents. The major players include in this market are as follows:

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2014 to 2025. For this study, Million Insights has segmented the global flexible display market report based on type, material type, application, and region:

Japan Display Inc. is a Japanese company that manufactures and supplies LCD panels for smartphones, tablets, automotive applications and laptops. The company was founded in 2010 and is headquartered in Tokyo, Japan. As of March 2016, the company had a market capitalization of US$2.4 billion.

Japan Display Inc."s products are used in a variety of electronic devices including smartphones, tablets, automotive applications and laptops. The company"s panels are used by major electronics manufacturers such as Apple Inc., Samsung Electronics Co., Ltd., LG Electronics Inc., HTC Corporation and Huawei Technologies Co., Ltd.

Japan Display Inc. (JDI) is a leading display panel manufacturer based in Tokyo, Japan. The company was formed in 2011 as a joint venture between Sony, Hitachi and Toshiba. JDI supplies LCD panels to some of the world’s largest electronics manufacturers, including Apple, LG and Samsung.

JDI’s cutting-edge technology has made it one of the leaders in the global display market. The company’s products are used in a wide range of devices, from smartphones and tablets to TVs and laptops. JDI has a strong R&D team that is constantly developing new display technologies. The company is publicly listed on the Tokyo Stock Exchange and had a revenue of US$5.6 billion in 2018.

Japan Display Inc. is a leading display panel manufacturer that designs, develops, and manufactures cutting-edge display panels and systems for smartphones, tablets, notebooks, automotive applications, digital cameras, camcorders and digital signage. The company has over 8,000 employees and operates 13 factories in 9 countries around the world.

Japan Display Inc. offers a wide range of products and services that are designed to meet the needs of its customers. The company’s product portfolio includes: LCD panels, OLED panels, touch panels, flexible displays and integrated modules. Japan Display Inc. also provides a variety of value-added services such as: design support, engineering support, production support and after-sales service. The company’s products are used in a variety of market segments including consumer electronics, automotive, industrial and medical. Japan Display Inc.

Japan Display Inc. (JDI) is a leading display manufacturer that designs, develops, and manufactures LCDs for smartphones, tablets, automotive applications, and other consumer electronics. The company went public in 2010 and is listed on the Tokyo Stock Exchange. JDI reported a net loss of ¥23.4 billion ($205 million) in the fiscal year ended March 31, 2016, compared to a net profit of ¥10.3 billion in the previous fiscal year. This was primarily due to lower sales of LCD panels for smartphones and increased competition from Chinese manufacturers.

One of the biggest challenges that Japan Display Inc. (JDI) is facing is the competition from South Korean and Chinese display manufacturers. JDI has been losing market share to these companies in recent years, and it is becoming increasingly difficult for JDI to compete on price. Additionally, JDI is also facing challenges from new technologies such as OLED and quantum dot displays. While JDI has developed its own OLED technology, it has yet to commercialize it on a large scale. And while quantum dot displays are not yet widely used in smartphones, they are expected to gain popularity in the coming years.

1.1. THE POLICY COVERS THE HANDLING OF THE PRIVATE INFORMATION EACH USER SHARES WITH TRENDFORCE WHILE VISITING OUR WEBSITES. IF A DIFFERENT PRIVATE POLICY HAS BEEN REFERED TO FOR SPECIFIC TRENDFORCE WEBSITES AND SERVICES, THAT POLICY WILL REPLACE OR SUPPLEMENT THE PRIVACY POLICY MENTIONED IN THIS DOCUMENT. THIS POLICY ALSO COVERS INDIVIDUALS LEGALLY RESIDING IN OR ORGANIZATIONS LEGALLY BASED IN MEMBER COUNTRIES OF THE EUROPEAN UNION (EU) AND ARE SUBJECTED TO EU GENERAL DATA PROTECTION REGULATION (GDPR) WITH REGARD TO PROVISION OF SERVICES AND PERSONAL DATA PROTECTION.

2.1 THE WEBSITE WILL COLLECT AND USE USER INFORMATION FOR PURPOSES SUCH AS MARKETING, CONSUMER PROTECTION, CONSUMER/CLIENT MANAGEMENT, E-COMMERCE SERVICES, FINANCIAL ACCOUNTING, CONTRACTUAL MATTERS, RESEARCH ANALYSIS, AND DATA PROCESSING. WHEN REQUIRED BY LAW, THE WEBSITE MAY ALSO PROVIDE PERSONAL INFORMATION TO NON-GOVERNMENT AGENCIES.

THE WEBSITE WILL NOT DISCLOSE OR SHARE ANY PERSONAL INFORMATION EXCPET PER SPECIAL REQUEST OR WHEN PERMISSION IS RECEIVED FROM THE USER. OTHER EXCEPTIONS INCLUDE:

IN ACCORDANCE WITH ARTICLE 3 OF THE PERSONAL INFORMATION PROTECTION LAW, YOU WILL HAVE THE OPTION TO EXERCISE THE FOLLOWING RIGHTS WITH REGARD TO THE PERSONAL INFORMATION SHARED WITH THE WEBSITE:

a. TO PREVENT UNAUTHORIZED PARTIES FROM ACCESSING, MODIFYING, OR LEAKING PERSONAL USER DATA, THE WEBSITE WILL TAKE STEPS TO IMPLEMENT PROPER SAFETY MEASURES. THE DATA SEARCHED AND RECORDED ON THE WEBSITE AND THE APPROPRIATE SAFETY MEASURES CHOSEN WILL ALL BE REVIEWED CAREFULLY. CONSIDERING HOW THE SAFETY OF TRANSMITTING DATA ON THE INTERNET CAN NEVER BE GUARANTEED COMPLETELY, USERS SHOULD KEEP IN MIND ALL POSSIBLE RISKS ASSOCIATED WITH ONLINE DATA TRANSFERS AND TAKE RESPONSIBILITY FOR ANY INFORMATION SHARED WITH OR OBTAINED FROM THE WEBSITE.

BE SURE TO PROTECT ALL PASSWORDS AND PERSONAL INFORMATION, REFRAIN FROM DISCLOSING PRIVATE USER INFORMATION TO ANY THIRD PARTY, AND REGISTER WITH THE WEBSITE UPON COMPLETING ALL NECESSARY MEMBERSHIP PROCEDURES. WHEN USING A SHARED OR PUBLIC COMPUTER, PLEASE MAKE SURE TO PROPERLY CLOSE ALL RELEVANT BROWSERS TO PREVENT OTHERS FROM READING YOUR PERSONAL E-MAILS OR INFORMATION.

The Global Flexible Displays Market size is expected to reach $31.5 billion by 2025, rising at a market growth of 25.9% CAGR during the forecast period. Flexible displays are mainly OLED and AMOLED displays that are curved, bended, or fully foldable. Consumer electronics manufacturers have offered numerous smartphones, TV sets and other display devices in a rigid curved form factor in the current market scenario. Although these displays are curved in comparison to traditional rigid flat displays, these displays do not give the end-users true versatility.

Growth is driven by increased demand for display-based consumer electronics coupled with consumer inclination towards energy-efficient, flexible gadgets. Technological advances in display technology have resulted in the introduction of advanced flexible displays, creating opportunities for growth for the market"s key players. In terms of portability, non-fragility and weight, the superior features offer

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey