lcd panel manufacturers market share 2018 made in china

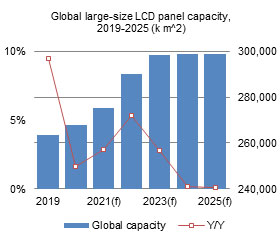

China is the leader in producing LCD display panels, with a forecast capacity share of 56 percent in 2020. China"s share is expected to increase in the coming years, stabilizing at 69 percent from 2023 onwards.Read moreLCD panel production capacity share from 2016 to 2025, by countryCharacteristicChinaJapanSouth KoreaTaiwan-----

DSCC. (June 8, 2020). LCD panel production capacity share from 2016 to 2025, by country [Graph]. In Statista. Retrieved December 24, 2022, from https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. "LCD panel production capacity share from 2016 to 2025, by country." Chart. June 8, 2020. Statista. Accessed December 24, 2022. https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. (2020). LCD panel production capacity share from 2016 to 2025, by country. Statista. Statista Inc.. Accessed: December 24, 2022. https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. "Lcd Panel Production Capacity Share from 2016 to 2025, by Country." Statista, Statista Inc., 8 Jun 2020, https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC, LCD panel production capacity share from 2016 to 2025, by country Statista, https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/ (last visited December 24, 2022)

BOE Technology Group, the Chinese electronic components producer, is expected to be the leader in producing LCD display panels in the coming years, with a forecast capacity share of 24 percent by 2022. China is the country that has the largest LCD capacity, with a 56 percent share in 2020.Read moreLCD panel production capacity share from 2016 to 2022, by manufacturerCharacteristicBOEChina StarInnoluxAUOLGDHKCCEC PandaSharpSDCOther-----------

DSCC. (June 8, 2020). LCD panel production capacity share from 2016 to 2022, by manufacturer [Graph]. In Statista. Retrieved December 24, 2022, from https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. "LCD panel production capacity share from 2016 to 2022, by manufacturer." Chart. June 8, 2020. Statista. Accessed December 24, 2022. https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. (2020). LCD panel production capacity share from 2016 to 2022, by manufacturer. Statista. Statista Inc.. Accessed: December 24, 2022. https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. "Lcd Panel Production Capacity Share from 2016 to 2022, by Manufacturer." Statista, Statista Inc., 8 Jun 2020, https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC, LCD panel production capacity share from 2016 to 2022, by manufacturer Statista, https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/ (last visited December 24, 2022)

Chinese display panel makers accounted for nearly half of the share in the global liquid crystal display TV panel market in the first half of this year, dominating the industry.

Beijing-based market researcher Sigmaintell Consulting said shipments of LCD TV panels worldwide totaled 140 million pieces in the year"s first half, up 3.6 percent compared with the same period a year ago.

The supply of TV panels though has surpassed demand due to the slowdown in the global economy and weaker consumer purchasing power. Manufacturers are facing severe challenges from falling panel prices, the Sigmaintell report said.

The shipment of BOE"s LCD TV panels stood at 27.6 million in the Jan-June period while LG Display followed with 22.7 million, down 4.5 percent year-on-year. Innolux Display Group was in third place, having shipped 21.9 million units.

Shenzhen China Star Optoelectronics Technology Co Ltd, a subsidiary of consumer electronics giant TCL Corp, ranked fourth, shipping 19.3 million pieces of TV panels. Chinese panel makers accounted for a 45.8 percent share in the global LCD TV panel market.

Sigmaintell estimated that the gap between supply and demand would widen further, and the panel market may face a long-term risk of oversupply. The industry may have to undergo a reshuffle given fierce market competition, it said.

The panel makers must reduce costs, optimize their internal structures, promote technological innovation and explore more innovative applications, the report by the consultancy said.

Separately, BOE"s Gen 10.5 TFTLCD production line has entered operation in Hefei, Anhui province. The plant will produce high-definition LCD screens of 65 inches and above.

"China"s semiconductor display industry has taken large steps forward in the past decade, changing the display industry"s global competitive landscape. China has transformed into the world"s largest consumer market and manufacturing base for display terminals, with huge market potential," said BOE Vice-President Zhang Yu.

CSOT also announced in November last year that its Gen 11 TFT-LCD and active-matrix OLED production line had officially began operation. The project will produce 43-inch, 65-inch and 75-inch liquid crystal display screens.

China is expected to replace South Korea as the world"s largest flat-panel display producer in 2019, a report from the China Video Industry Association and the China Optics and Optoelectronics Manufacturers Association said.

"The average size of TV panels is likely to increase 1.4 inches in 2019. The 65-inch dimension will become the most popular size of TV," Li Yaqin, general manager of Sigmaintell, said while adding the 65-inch TV will become the mainstream screen in people"s living rooms in the future.

Compared with traditional LCD display panels, OLED has a fast response rate, wide viewing angles, high-contrast images and richer colors. It is thinner and can be made flexible.

BOE Technology Group and TCL China Star Optoelectronics Technology (TCL CSOT) are among the Chinese panel makers to have ramped up output since around 2019 with generous state subsidies. China is gaining on South Korea, whose share of capacity is seen reaching 55% for 2022 in an October estimate by U.S. market intelligence firm Display Supply Chain Consultants (DSCC).

TOKYO -- In the past two years, eight plants have been set up in China to produce smartphone panels. Five more are scheduled to start operating in the next two years.

Backed by massive state funding, Chinese panel makers are taking a bigger bite of the market for smartphone display panels, which has so far been dominated by Japanese and South Koreans makers.

Workers manufacture display panels on an assembly line in Huainan High-Tech Industrial Development Zone in East China"s Anhui Province, on April 24, 2022. Photo: VCG

The news outlets proclaimed that South Korea"s title of "the strongest country in display market" was lost after 17 years and that it would not be possible for South Korea to reclaim the No. 1 spot if it cannot find a way to ramp up investment in next-generation displays such as organic light emitting diodes (OLED).

The year 2021 was a milestone for China"s display panel industry. Chinese display panel makers, led by companies such as BOE Technology Group Co, Shenzhen China Star Optoelectronics Technology Co, Tianma, and Visionox, accounted a combined 40.4 percent of global market share in turnover, outstripping South Korea"s 36.3 percent, data from Beijing-based market research provider Sigmaintell revealed.

It is the first time that Chinese companies held a larger market share that their South Korean rivals, mainly Samsung Display and LG Display, as in 2020, South Korean companies led with 39.8 percent of market share, 4.8 percentage points higher than China.

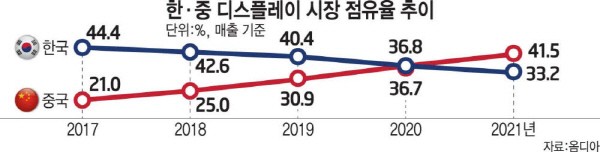

A different set of data published by market research firm Omdia showed the same pattern. China recorded $64.8 billion in sales including liquid crystal display (LCD) and OLED in the global display market in 2021. China overtook South Korea"s No. 1 spot with a market share of 41.5 percent while South Korea"s market share fell to 33.2 percent.

On March 30, BOE, the world"s largest flat-panel display manufacturer, said its total revenue stood at 219.31 billion yuan ($33.57 billion) in 2021, up 61.79 percent from a yearly basis, while its net profit surged 412.96 percent year-on-year to hit 25.83 billion yuan.

Market competition in display panel, an indispensable part for consumer electronics, is fierce. And the competing relations between Chinese and South Korean companies exist in display panels for smartphones, televisions, monitors, among other product segments.

Display panel are comparable to today"s high-end semiconductors, for years the production of display panels had been monopolized by foreign companies. But after a decade of strenuous work to catchup, experts said that Chinese players now dominate today"s display panel manufacturing and the proliferation of display panel technology benefited global consumers by reducing the cost of a wide range of downstream electronic components and has in recent years caused domestic upstream business such as material-supplying company to flourish.

In terms of LCD, Chinese companies have long surpassed their South Korean counterparts in shipments, and in recent years Chinese companies also invested heavily in advanced production lines for small-size OLED screens that is used in smartphones.

Etnews suggested South Koran companies reduce OLED panel prices by mass producing OLED, which requires substantial investment in production capacity, only then can South Korea replace the LCD market led by China. The battlefield of choice for South Korean firms would be in large TV panel market, in which they still enjoy large technological gap with China.

Even as South Korean companies seek to entrench their lead position in large-size OLED, their efforts may not turn out to be as effective as imagined, Lee said, as large OLED may not prove to be a worthy barrier behind which South Korean companies could fall back upon as it does not have unique functions that could not be fulfilled by LCD.

In 2021, shipments of large-size OLED display panels were just 6.7 million units while in the same period the shipments of LCD reached 210 million units.

"Back in the days of LCD phasing out cathode ray tube and plasma display panel, LCD could fulfill unique functions the other two types could not. That is something we don"t see in OLED. The things OLED can do, LCD can also do and are being constantly perfected," Lee said. "That means fall back behind the OLED castles may not be enough to fend off challenges lurched out by Chinese players."

Lee said as the display panel industry moves forward, Chinese companies are betting big on research & development in new emerging display technologies such as mini-LED and micro-LED.

South Korean companies would be increasingly willing to export their advanced technology once they realized they are losing market shares, according to Lee.

Flat-panel displays are thin panels of glass or plastic used for electronically displaying text, images, or video. Liquid crystal displays (LCD), OLED (organic light emitting diode) and microLED displays are not quite the same; since LCD uses a liquid crystal that reacts to an electric current blocking light or allowing it to pass through the panel, whereas OLED/microLED displays consist of electroluminescent organic/inorganic materials that generate light when a current is passed through the material. LCD, OLED and microLED displays are driven using LTPS, IGZO, LTPO, and A-Si TFT transistor technologies as their backplane using ITO to supply current to the transistors and in turn to the liquid crystal or electroluminescent material. Segment and passive OLED and LCD displays do not use a backplane but use indium tin oxide (ITO), a transparent conductive material, to pass current to the electroluminescent material or liquid crystal. In LCDs, there is an even layer of liquid crystal throughout the panel whereas an OLED display has the electroluminescent material only where it is meant to light up. OLEDs, LCDs and microLEDs can be made flexible and transparent, but LCDs require a backlight because they cannot emit light on their own like OLEDs and microLEDs.

Liquid-crystal display (or LCD) is a thin, flat panel used for electronically displaying information such as text, images, and moving pictures. They are usually made of glass but they can also be made out of plastic. Some manufacturers make transparent LCD panels and special sequential color segment LCDs that have higher than usual refresh rates and an RGB backlight. The backlight is synchronized with the display so that the colors will show up as needed. The list of LCD manufacturers:

Organic light emitting diode (or OLED displays) is a thin, flat panel made of glass or plastic used for electronically displaying information such as text, images, and moving pictures. OLED panels can also take the shape of a light panel, where red, green and blue light emitting materials are stacked to create a white light panel. OLED displays can also be made transparent and/or flexible and these transparent panels are available on the market and are widely used in smartphones with under-display optical fingerprint sensors. LCD and OLED displays are available in different shapes, the most prominent of which is a circular display, which is used in smartwatches. The list of OLED display manufacturers:

MicroLED displays is an emerging flat-panel display technology consisting of arrays of microscopic LEDs forming the individual pixel elements. Like OLED, microLED offers infinite contrast ratio, but unlike OLED, microLED is immune to screen burn-in, and consumes less power while having higher light output, as it uses LEDs instead of organic electroluminescent materials, The list of MicroLED display manufacturers:

LCDs are made in a glass substrate. For OLED, the substrate can also be plastic. The size of the substrates are specified in generations, with each generation using a larger substrate. For example, a 4th generation substrate is larger in size than a 3rd generation substrate. A larger substrate allows for more panels to be cut from a single substrate, or for larger panels to be made, akin to increasing wafer sizes in the semiconductor industry.

"Samsung Display has halted local Gen-8 LCD lines: sources". THE ELEC, Korea Electronics Industry Media. August 16, 2019. Archived from the original on April 3, 2020. Retrieved December 18, 2019.

"TCL to Build World"s Largest Gen 11 LCD Panel Factory". www.businesswire.com. May 19, 2016. Archived from the original on April 2, 2018. Retrieved April 1, 2018.

"Panel Manufacturers Start to Operate Their New 8th Generation LCD Lines". 대한민국 IT포털의 중심! 이티뉴스. June 19, 2017. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"TCL"s Panel Manufacturer CSOT Commences Production of High Generation Panel Modules". www.businesswire.com. June 14, 2018. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"Business Place Information – Global Operation | SAMSUNG DISPLAY". www.samsungdisplay.com. Archived from the original on 2018-03-26. Retrieved 2018-04-01.

"Samsung Display Considering Halting Some LCD Production Lines". 비즈니스코리아 - BusinessKorea. August 16, 2019. Archived from the original on April 5, 2020. Retrieved December 19, 2019.

Herald, The Korea (July 6, 2016). "Samsung Display accelerates transition from LCD to OLED". www.koreaherald.com. Archived from the original on April 1, 2018. Retrieved April 1, 2018.

Byeonghwa, Yeon. "Business Place Information – Global Operation – SAMSUNG DISPLAY". Samsungdisplay.com. Archived from the original on 2018-03-26. Retrieved 2018-04-01.

www.wisechip.com.tw. "WiseChip History – WiseChip Semiconductor Inc". www.wisechip.com.tw. Archived from the original on 2018-02-17. Retrieved 2018-02-17.

"China"s BOE to have world"s largest TFT-LCD+AMOLED capacity in 2019". ihsmarkit.com. 2017-03-22. Archived from the original on 2019-08-16. Retrieved 2019-08-17.

Latest research from Omdia has found that Chinese display maker BOE has led the market in shipments of large area TFT LCD displays in December 2021, both in units and total area shipped. This accounts for nearly one-third of whole unit shipments, as the industry set new records for shipments for the month and year.

Pandemic restrictions impacted demand for and spending across home entertainment products with display shipments of TV and IT devices experiencing a growth surge. The total of large area TFT display shipments rose to a record 89.4 million square meters in December, reflecting a 4 percent month-on-month increase over November, as well as 5 percent Year on Year growth (YoY), Omdia reported in its latest Large Area Display Market Tracker.

For the full year, large area TFT LCD shipments increased with 9 percent YoY by units and 4 percent YoY by area, reaching 962.7 million units and 228.8 million square meters shipped in 2021, both historical highs and marking the first time the industry has ever shipped more than 900 million units in a year.

Among display makers, China"s BOE took the largest shares for both units and total area shipped in 2021. BOE took 31.5 percent for units shipped and 26.2 percent for area shipped, marking the first time one maker has captured over 31 percent market share for whole unit shipments and 26 percent share for whole area shipments in large area TFT LCD history.

Beyond BOE, Innolux took 15.4 percent market share for large area TFT LCD unit shipments, followed by LG Display with 13.4 percent in 2021. For total area shipped, China Star took 15.8 percent as second largest maker after BOE, followed by LG Display in third with 11.9 percent in 2021.

Strong demand particularly for mobile PC LCD during the pandemic increased notebook PC LCD unit shipments in 2021, rising 26 percent YoY. Tablet PC LCD unit shipments also rose 7 percent YoY last year. On the other hand, the LCD TV display segment saw unit shipments fall 4 percent YoY due to a slowdown in demand in 3Q21. But ongoing LCD TV size migration in favor of larger screens meant that total LCD TV display area shipped increased 2 percent YoY in 2021 despite the drop in unit shipments.

Large area TFT LCD revenue increased 34 percent YoY in 2021 and reached US$85.2 billion, also setting a record and the first time large area TFT LCD revenue has ever exceeded $80 billion. Strong demand and size migration to larger screens during COVID-19 pandemic combined with display price hikes up until 3Q21 to drive the high revenue number.

YoonSung Chung, senior research manager for large area displays and supply chain at Omdia, commented: "Display makers waited for results from Black Friday sales to set their early 2022 sales and pricing strategies. However, results seem to fall short of expectations for LCD TVs. LCD TV display buyers will price LCD TV displays more aggressively in the coming months.

"While demand for IT displays is weakening, panel makers’ supply plans are ambitious. Unless panel makers adjust their fab utilisation, price erosions could imminently worsen for large area display applications, including monitor and notebook PC LCDs. Omdia expects the LCD TV panel prices to reach the price bottom in 1H 2022 and then gradually rebound based on the market demand recovery."

Latest research from Omdia has found that Chinese display maker BOE has led the market in shipments of large area TFT LCD displays in December 2021, both in units and total area shipped. This accounts for nearly one-third of whole unit shipments, as the industry set new records for shipments for the month and year.

Pandemic restrictions impacted demand for and spending across home entertainment products with display shipments of TV and IT devices experiencing a growth surge. The total of large area TFT display shipments rose to a record 89.4 million square meters in December, reflecting a 4 percent month-on-month increase over November, as well as 5 percent Year on Year growth (YoY), Omdia reported in its latest Large Area Display Market Tracker.

For the full year, large area TFT LCD shipments increased with 9 percent YoY by units and 4 percent YoY by area, reaching 962.7 million units and 228.8 million square meters shipped in 2021, both historical highs and marking the first time the industry has ever shipped more than 900 million units in a year.

Among display makers, China"s BOE took the largest shares for both units and total area shipped in 2021. BOE took 31.5 percent for units shipped and 26.2 percent for area shipped, marking the first time one maker has captured over 31 percent market share for whole unit shipments and 26 percent share for whole area shipments in large area TFT LCD history.

Beyond BOE, Innolux took 15.4 percent market share for large area TFT LCD unit shipments, followed by LG Display with 13.4 percent in 2021. For total area shipped, China Star took 15.8 percent as second largest maker after BOE, followed by LG Display in third with 11.9 percent in 2021.

Strong demand particularly for mobile PC LCD during the pandemic increased notebook PC LCD unit shipments in 2021, rising 26 percent YoY. Tablet PC LCD unit shipments also rose 7 percent YoY last year. On the other hand, the LCD TV display segment saw unit shipments fall 4 percent YoY due to a slowdown in demand in 3Q21. But ongoing LCD TV size migration in favor of larger screens meant that total LCD TV display area shipped increased 2 percent YoY in 2021 despite the drop in unit shipments.

Large area TFT LCD revenue increased 34 percent YoY in 2021 and reached US$85.2 billion, also setting a record and the first time large area TFT LCD revenue has ever exceeded $80 billion. Strong demand and size migration to larger screens during COVID-19 pandemic combined with display price hikes up until 3Q21 to drive the high revenue number.

YoonSung Chung, senior research manager for large area displays and supply chain at Omdia, commented: "Display makers waited for results from Black Friday sales to set their early 2022 sales and pricing strategies. However, results seem to fall short of expectations for LCD TVs. LCD TV display buyers will price LCD TV displays more aggressively in the coming months.

"While demand for IT displays is weakening, panel makers’ supply plans are ambitious. Unless panel makers adjust their fab utilisation, price erosions could imminently worsen for large area display applications, including monitor and notebook PC LCDs. Omdia expects the LCD TV panel prices to reach the price bottom in 1H 2022 and then gradually rebound based on the market demand recovery."

► When the leading Korean players Samsung Display and LG Display exit LCD production, BOE will be the most significant player in the LCD market. Though OLED can replace the LCD, it will take years for it to be fully replaced.

► As foreign companies control evaporation material and machines, panel manufacturers seek a cheaper way to mass-produce OLED panels – inkjet printing.

When mainstream consumer electronics brands choose their device panels, the top three choices are Samsung Display, LG Display (LGD) and BOE (000725:SZ) – the first two from Korea and the third from China. From liquid-crystal displays (LCD) to active-matrix organic light-emitting diode (AMOLED), display panel technology has been upgrading with bigger screen products.

From the early 1990s, LCDs appeared and replaced cathode-ray tube (CRT) screens, which enabled lighter and thinner display devices. Japanese electronics companies like JDI pioneered the panel technology upgrade while Samsung Display and LGD were nobodies in the field. Every technology upgrade or revolution is a chance for new players to disrupt the old paradigm.

The landscape was changed in 2001 when Korean players firstly made a breakthrough in the Gen 5 panel technology – the later the generation, the bigger the panel size. A large panel size allows display manufacturers to cut more display screens from one panel and create bigger-screen products. "The bigger the better" is a motto for panel makers as the cost can be controlled better and they can offer bigger-size products to satisfy the burgeoning middle-class" needs.

LCD panel makers have been striving to realize bigger-size products in the past four decades. The technology breakthrough of Gen 5 in 2002 made big-screen LCD TV available and it sent Samsung Display and LGD to the front row, squeezing the market share of Japanese panel makers.

The throne chair of LCD passed from Japanese companies to Korean enterprises – and now Chinese players are clinching it, replacing the Koreans. After twenty years of development, Chinese panel makers have mastered LCD panel technology and actively engage in large panel R&D projects. Mass production created a supply surplus that led to drops in LCD price. In May 2020, Samsung Display announced that it would shut down all LCD fabs in China and Korea but concentrate on quantum dot LCD (Samsung calls it QLED) production; LGD stated that it would close LCD TV panel fabs in Korea and focus on organic LED (OLED). Their retreats left BOE and China Stars to digest the LCD market share.

Consumer preference has been changing during the Korean fab"s recession: Bigger-or-not is fine but better image quality ranks first. While LCD needs the backlight to show colors and substrates for the liquid crystal layer, OLED enables lighter and flexible screens (curvy or foldable), higher resolution and improved color display. It itself can emit lights – no backlight or liquid layer is needed. With the above advantages, OLED has been replacing the less-profitable LCD screens.

Samsung Display has been the major screen supplier for high-end consumer electronics, like its own flagship cell phone products and Apple"s iPhone series. LGD dominated the large OLED TV market as it is the one that handles large-size OLED mass production. To further understand Korean panel makers" monopolizing position, it is worth mentioning fine metal mask (FMM), a critical part of the OLED RGB evaporation process – a process in OLED mass production that significantly affects the yield rate.

Prior to 2018, Samsung Display and DNP"s monopolistic supply contract prevented other panel fabs from acquiring quality FMM products as DNP bonded with Hitachi Metal, the "only" FMM material provider choice for OLED makers. After the contract expired, panel makers like BOE could purchase FFM from DNP for their OLED R&D and mass production. Except for FFM materials, vacuum evaporation equipment is dominated by Canon Tokki, a Japanese company. Its role in the OLED industry resembles that of ASML in the integrated circuit space. Canon Tokki"s annual production of vacuum evaporation equipment is fewer than ten and thereby limits the total production of OLED panels that rely on evaporation technology.

The shortage of equipment and scarcity of materials inspired panel fabs to explore substitute technology; they discovered that inkjet printing has the potential to be the thing to replace evaporation. Plus, evaporation could be applied to QLED panels as quantum dots are difficult to be vaporized. Inkjet printing prints materials (liquefied organic gas or quantum dots) to substrates, saving materials and breaking free from FMM"s size restriction. With the new tech, large-size OLED panels can theoretically be recognized with improved yield rate and cost-efficiency. However, the tech is at an early stage when inkjet printing precision could not meet panel manufacturers" requirements.

Display and LGD are using evaporation on their OLED products. To summarize, OLED currently adopts evaporation and QLED must go with inkjet printing, but evaporation is a more mature tech. Technology adoption will determine a different track for the company to pursue. With inkjet printing technology, players are at a similar starting point, which is a chance for all to run to the front – so it is for Chinese panel fabs. Certainly, panel production involves more technologies (like flexible panels) than evaporation or inkjet printing and only mastering all required technologies can help a company to compete at the same level.

Presently, Chinese panel fabs are investing heavily in OLED production while betting on QLED. BOE has four Gen 6 OLED product lines, four Gen 8.5 and one Gen 10.5 LCD lines; China Star, controlled by the major appliance titan TCL, has invested two Gen 6 OLED fabs and four large-size LCD product lines.

Remembering the last "regime change" that occurred in 2005 when Korean fabs overtook Japanese" place in the LCD market, the new phase of panel technology changed the outlook of the industry. Now, OLED or QLED could mark the perfect time for us to expect landscape change.

After Samsung Display and LGD ceding from LCD TV productions, the vacant market share will be digested by BOE, China Star and other LCD makers. Indeed, OLED and QLED have the potential to take over the LCD market in the future, but the process may take more than a decade. Korean companies took ten years from panel fab"s research on OLED to mass production of small- and medium-size OLED electronics. Yet, LCD screen cell phones are still available in the market.

LCD will not disappear until OLED/QLED"s cost control can compete with it. The low- to middle-end panel market still prefers cheap LCD devices and consumers are satisfied with LCD products – thicker but cheaper. BOE has been the largest TV panel maker since 2019. As estimated by Informa, BOE and China Star will hold a duopoly on the flat panel display market.

BOE"s performance seems to have ridden on a roller coaster ride in the past several years. Large-size panel mass production like Gen 8.5 and Gen 10.5 fabs helped BOE recognize the first place in production volume. On the other side, expanded large-size panel factories and expenses of OLED product lines are costly: BOE planned to spend CNY 176.24 billion (USD 25.92 billion) – more than Tibet"s 2019 GDP CNY 169.78 billion – on Chengdu and Mianyang"s Gen 6 AMOLED lines and Hefei and Wuhan"s Gen 10.5 LCD lines.

Except for making large-size TVs, bigger panels can cut out more display screens for smaller devices like laptops and cell phones, which are more profitable than TV products. On its first-half earnings concall, BOE said that it is shifting its production focus to cell phone and laptop products as they are more profitable than TV products. TV, IT and cell phone products counted for 30%, 44% and 33% of its productions respectively and the recent rising TV price may lead to an increased portion of TV products in the short term.

Except for outdoor large screens, TV is another driver that pushes panel makers to research on how to make bigger and bigger screens. A research done by CHEARI showed that Chinese TV sales dropped by 10.6% to CNY 128.2 billion from 2018 to 2019. Large-size TV sales increased as a total but the unit price decreased; high-end products like laser TV and OLED TV saw a strong growth of 131.2% and 34.1%, respectively.

The demand for different products may vary as lifestyles change and panel fabs need to make on-time judgments and respond to the change. For instance, the coming Olympics is a new driving factor to boost TV sales; "smart city" projects around the world will need more screens for data visualization; people will own more screens and better screens when life quality improves. Flexible screens, cost-efficient production process, accessible materials, changing market and all these problems are indeed the next opportunity for the industry.

(April 30, 2019) – With Chinese panel makers accelerating the mass production of large thin-film transistor (TFT) liquid crystal display (LCD) TV panels faster than expected, they accounted for 33.9 percent of the 60-inch and larger LCD TV panel shipments in the first quarter of 2019. Their market share has expanded nearly 10 times from 3.6 percent in just over a year, according to business information provider

South Korean panel makers still accounted for the largest share in the 60-inch and larger LCD TV panel shipments, with a 45.1 percent share in the first quarter. However, Chinese panel makers’ share in the large LCD TV panel market is expected to continue to grow.

“When BOE’s B9 10.5G fab started its mass production in the first quarter of 2018, the industry expected that its full ramp-up would take quite a time due to a learning curve,” said

BOE accounted for 29 percent of the total 60-inch and larger LCD TV panel shipments in the first quarter of 2019. It is estimated that the B9 10.5G fab has reached its maximum capacity of 120,000 sheets in the first quarter of 2019.

ChinaStar also started to mass produce large LCD panels at its T6 10.5G fab in the first quarter. CEC-Panda and CHOT ramped up mass production at their 8.6G fabs to the maximum design capacity in the first quarter. Foxconn/Sharp is forecast to begin mass production at their Guangzhou 10.5G fab in the second half of 2019.

“As both Chinese and South Korean panel suppliers are focusing on large LCD TV panels, competition between them will become more intense, pressuring the price of large LCD TV panels even further throughout 2019,” Wu said.

by IHS Markit, shipments of larger than 9-inch TFT-LCD panels reached 178.3 million units in the first quarter of 2019, down 1 percent from a year ago. By area, the shipment increased by 6.7 percent to 49.1 million square meters during the same period.

BOE led the unit shipments of large TFT-LCD panels with a 24.6 percent share in the first quarter of 2019, followed by LG Display (18.8 percent) and Innolux (16 percent). By area shipments, LG Display accounted for the largest share of 20 percent, followed by BOE (19.9 percent) and Samsung Display (14.1 percent).

IHS Markit provides information on the entire range of large display panels shipped worldwide and regionally, including monthly and quarterly revenues and shipments by display area, application, size and aspect ratio of each supplier.

IHS Markit (Nasdaq: INFO) is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers next-generation information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 business and government customers, including 80 percent of the Fortune Global 500 and the world’s leading financial institutions.

[Introduction]: This paper analyzes the competitive pattern of the panel display industry from both supply and demand sides. On the supply side, the optimization of the industry competition pattern by accelerating the withdrawal of Samsung’s production capacity is deeply discussed. Demand-side focuses on tracking global sales data and industry inventory changes.

Since April 2020, the display device sector rose 4.81%, ranking 11th in the electronic subsectors, 3.39 percentage points behind the SW electronic sector, 0.65 percentage points ahead of the Shanghai and Shenzhen 300 Index. Of the top two domestic panel display companies, TCL Technology is up 11.35 percent in April and BOE is up 4.85 percent.

Specific to the panel display plate, we still do the analysis from both ends of supply and demand: supply-side: February operating rate is insufficient, especially panel display module segment grain rate is not good, limited capacity to boost the panel display price. Since March, effective progress has been made in the prevention and control of the epidemic in China. Except for some production lines in Wuhan that have been delayed, other domestic panels show that the production lines have returned to normal. In South Korea, Samsung announced recently that it would accelerate its withdrawal from all LCD production lines. This round of output withdrawal exceeded market expectations both in terms of pace and amplitude. We will make a detailed analysis of it in Chapter 2.

Demand-side: We believe that people spend more time at home under the epidemic situation, and TV, as an important facility for family entertainment, has strong demand resilience. In our preliminary report, we have interpreted the pick-up trend of domestic TV market demand in February, which also showed a good performance in March. At present, the online market in China maintains a year-on-year growth of about 30% every week, while the offline market is still weak, but its proportion has been greatly reduced. At present, people are more concerned about the impact of the epidemic overseas. According to the research of Cinda Electronics Industry Chain, in the first week, after Italy was closed down, local TV sales dropped by about 45% from the previous week. In addition, Media Markt, Europe’s largest offline consumer electronics chain, also closed in mid-March, which will affect terminal sales to some extent, and panel display prices will continue to be under pressure in April and May. However, we believe that as the epidemic is brought under control, overseas market demand is expected to return to the pace of China’s recovery.

From a price perspective, the panel shows that prices have risen every month through March since the bottom of December 19 reversed. However, according to AVC’s price bulletin of TV panel display in early April, the price of TV panel display in April will decrease slightly, and the price of 32 “, 39.5 “, 43 “, 50 “and 55” panels will all decrease by 1 USD.65 “panel shows price down $2; The 75 “panel shows the price down by $3.The specific reasons have been described above, along with the domestic panel display production line stalling rate recovery, supply-side capacity release; The epidemic spread rapidly in Europe and the United States, sports events were postponed, local blockades were gradually rolled out, and the demand side declined to a certain extent.

Looking ahead to Q2, we think prices will remain under pressure in May, but prices are expected to pick up in June as Samsung’s capacity is being taken out and the outbreak is under control overseas. At the same time, from the perspective of channel inventory, the current all-channel inventory, including the inventory of all panel display factories, has fallen to a historical low. The industry as a whole has more flexibility to cope with market uncertainties. At the same time, low inventory is also the next epidemic warming panel show price foreshadowing.

In terms of valuation level, due to the low concentration and fierce competition in the panel display industry in the past ten years, the performance of sector companies is cyclical to a certain extent. Therefore, PE, PB, and other methods should be comprehensively adopted for valuation. On the other hand, the domestic panel shows that the leading companies in the past years have sustained large-scale capital investment, high depreciation, and a long period of poor profitability, leading to the inflated TTM PE in the first half of 2014 to 2017. Therefore, we will display the valuation level of the sector mainly through the PB-band analysis panel in this paper.

In 2017, due to the combined impact of panel display price rise and OLED production, the valuation of the plate continued to expand, with the highest PB reaching 2.8 times. Then, with the price falling, the panel shows that PB bottomed out at the end of January 2019 at only 1.11 times. From the end of 2019 to February, the panel shows that rising prices have driven PB all the way up, the peak PB reached 2.23 times. Since entering March, affected by the epidemic, in the short term panel prices under pressure, the valuation of the plate once again fell back to 1.62 times. In April, the epidemic situation in the epidemic country was gradually under control, and the valuation of the sector rebounded to 1.68 times.

We believe the sector is still at the bottom of the stage as Samsung accelerates its exit from LCD capacity and industry inventories remain low. Therefore, once the overseas epidemic is under control and the domestic demand picks up, the panel shows that prices will rise sharply. In addition, the plate will also benefit from Ultra HD drive in the long term. Panel display plate medium – and long-term growth logic is still clear. Coupled with the optimization of the competitive pattern, industry volatility will be greatly weakened. The current plate PB compared to the historical high has sufficient space, optimistic about the plate leading company’s investment value.

1). share market, in April in addition to Zhiyun shares, Tiantong shares, Yizhi technology fell, the rest of the stock plate rose, precision test electronics, Lebao high-tech and TCL technology rose larger, reaching 22.38%, 11.45%, and 11.35% respectively.

In the overseas market, benefiting from the control of the epidemic in Japan and South Korea, all stocks except UDC rose. Among them, Innolux Optoelectronics, Finetek, AU Optoelectronics rose more than 10%.

Revenue at Innolux and AU Optronics has been sluggish for several months and improved in March. Since the third quarter of 2017, Innolux’s monthly revenue growth has been negative, while AU Optronics has only experienced revenue growth in a very few months.AU Optronics recorded a record low revenue in January and increased in February and March. Innolux’s revenue returned to growth in March after falling to its lowest in recent years in February. However, because the panel display manufacturers in Taiwan have not put in new production capacity for many years, the production process of the existing production line is relatively backward, and the competitiveness is not strong.

On March 31, Samsung Display China officially sent a notice to customers, deciding to terminate the supply of all LCD products by the end of 2020.LGD had earlier announced that it would close its local LCDTV panel display production by the end of this year. In the following, we will analyze the impact of the accelerated introduction of the Korean factory on the supply pattern of the panel display industry from the perspective of the supply side.

The early market on the panel display plate is controversial, mainly worried about the exit of Korean manufacturers, such as LCD display panel price rise, or will slow down the pace of capacity exit as in 17 years. And we believe that this round of LCD panel prices and 2017 prices are essentially different, the LCD production capacity of South Korean manufacturers exit is an established strategy, will not be transferred because of price warming. Investigating the reasons, we believe that there are mainly the following three factors driving:

(1) Under the localization, scale effect, and aggregation effect, the Chinese panel leader has lower cost and stronger profitability than the Japanese and Korean manufacturers. In terms of cost structure, according to IHS data, material cost accounts for 70% of the cost displayed by the LCD panel, while depreciation accounts for 17%, so the material cost has a significant impact on it. At present, the upstream LCD, polarizer, PCB, mold, and key target material line of the mainland panel display manufacturers are fully imported into the domestic, effectively reducing the material cost. In addition, at the beginning of the factory, manufacturers not only consider the upstream glass and polarizer factory but also consider the synergy between the downstream complete machine factory, so as to reduce the labor cost, transportation cost, etc., forming a certain industrial clustering effect. The growing volume of shipments also makes the economies of scale increasingly obvious. In the long run, the profit gap between the South Korean plant and the mainland plant will become even wider.

(2) The 7 and 8 generation production lines of the Korean plant cannot adapt to the increasing demand for TV in average size. Traditionally, the 8 generation line can only cut the 32 “, 46 “, and 60” panel displays. In order to cut the other size panel displays economically and effectively, the panel display factory has made small adjustments to the 8 generation line size, so there are the 8.5, 8.6, 8.6+, and 8.7 generation lines. But from the cutting scheme, 55 inches and above the size of the panel display only part of the generation can support, and the production efficiency is low, hindering the development of large size TV. Driven by the strong demand for large-size TV, the panel display generation line is also constantly breaking through. In 2018, BOE put into operation the world’s first 10.5 generation line, the Hefei B9 plant, with a designed capacity of 120K/ month. The birth of the 10.5 generation line is epoch-making. It solves the cutting problem of large-size panel displays and lays the foundation for the outbreak of large-size TV. From the cutting method, one 10.5 generation line panel display can effectively cut 18 43 inches, 8 65 inches, 6 75 inches panel display, and can be more efficient in hybrid mode cutting, with half of the panel display 65 inches, the other half of the panel display 75 inches, the yield is also guaranteed. Currently, there are a total of five 10.5 generation lines in the world, including two for domestic panel display companies BOE and Huaxing Optoelectronics. Sharp has a 10.5 generation line in Guangzhou, which is mainly used to produce its own TV. Korean manufacturers do not have the 10.5 generation line. In the context of the increasing size of the TV, Korean manufacturers are obviously at a disadvantage in competitiveness.

(3) As the large-size OLED panel display technology has become increasingly mature, Samsung and LGD hope to transfer production to large-size OLED with better profit prospects as soon as possible. Apart from the price factor, the reason why South Korean manufacturers are exiting LCD production is more because the large-size OLED panel display technology is becoming mature, and Samsung and LGD hope to switch to large-size OLED production as soon as possible, which has better profit prospects. At present, there are three major large-scale OLED solutions including WOLED, QD OLED, and printed OLED, while there is only WOLED with a mass production line at present.

According to statistics, shipments of OLED TVs totaled 2.8 million in 2018 and increased to 3.5 million in 2019, up 25 percent year on year. But it accounted for only 1.58% of global shipments. The capacity gap has greatly limited the volume of OLED TV.LG alone consumes about 47% of the world’s OLED TV panel display capacity, thanks to its own capacity. Other manufacturers can only purchase at a high price. According to the industry chain survey, the current price of a 65-inch OLED panel is around $800-900, while the price of the same size LCD panel is currently only $171.There is a significant price difference between the two.

Samsung and LGD began to shut down LCD production lines in Q3 last year, leading to the recovery of the panel display sector. Entering 2020, the two major South Korean plants have announced further capacity withdrawal planning. In the following section, we will focus on its capacity exit plan and compare it with the original plan. It can be seen that the pace and magnitude of Samsung’s exit this round is much higher than the market expectation:

(1) LGD: LGD currently has three large LCD production lines of P7, P8, and P9 in China, with a designed capacity of 230K, 240K, and 90K respectively. At the CES exhibition at the beginning of this year, the company announced that IT would shut down all TV panel display production capacity in South Korea in 2020, mainly P7 and P8 lines, while P9 is not included in the exit plan because IT supplies IT panel display for Apple.

(2) Samsung: At present, Samsung has L8-1, L8-2, and L7-2 large-size LCD production lines in South Korea, with designed production capacities of 200K, 150K, and 160K respectively. At the same time in Suzhou has a 70K capacity of 8 generation line.

This round of capacity withdrawal of South Korean plants began in June 2019. Based on the global total production capacity in June 2019, Samsung will withdraw 1,386,900 square meters of production capacity in 2019-2020, equivalent to 9.69% of the global production capacity, according to the previous two-year withdrawal expectation. In 2021, 697,200 square meters of production capacity will be withdrawn, which is equivalent to 4.87% of the global production capacity, and a total of 14.56% will be withdrawn in three years. After the implementation of the new plan, Samsung will eliminate 2.422 million square meters of production capacity by the end of 2020, equivalent to 16.92 percent of the global capacity. This round of production plans from the pace and range are far beyond the market expectations.

Global shipments of TV panel displays totaled 281 million in 2019, down 1.06 percent year on year, according to Insight. In fact, TV panel display shipments have been stable since 2015 at between 250 and 300 million units. At the same time, from the perspective of the structure of sales volume, the period from 2005 to 2010 was the period when the size of China’s TV market grew substantially. Third-world sales also leveled off in 2014. We believe that the sales volume of the TV market has stabilized and there is no big fluctuation. The impact of the epidemic on the overall demand may be more optimistic than the market expectation.

In contrast to the change in volume, we believe that the core driver of the growth in TV panel display demand is actually the increase in TV size. According to the data statistics of Group Intelligence Consulting, the average size of TV panel display in 2014 was 0.47 square meters, equivalent to the size of 41 inches screen. In 2019, the average TV panel size is 0.58 square meters, which is about the size of a 46-inch screen. From 2014 to 2019, the average CAGR of TV panel display size is 4.18%. Meanwhile, the shipment of TV in 2019 also increased compared with that in 2014. Therefore, from 2014 to 2019, the compound growth rate of the total area demand for TV panel displays is 6.37%.

It is assumed that 4K screen and 8K screen will accelerate the penetration and gradually become mainstream products in the next 2-3 years. The pace of screen size increase will accelerate. We have learned through industry chain research that the average size growth rate of TV will increase to 6-8% in 2020. Driven by the growth of the average size, the demand area of global TV panel displays is expected to grow even if TV sales decline, and the upward trend of industry demand remains unchanged.

Meanwhile, the global LCDTV panel display demand will increase significantly in 2021, driven by the recovery of terminal demand and the continued growth of the average TV size. In 2021, the whole year panel display will be in a short supply situation, the mainland panel shows that both males will enjoy the price elasticity.

This paper analyzes the competition pattern of the panel display industry from both supply and demand sides. On the supply side, the optimization of the industry competition pattern by accelerating the withdrawal of Samsung’s production capacity is deeply discussed. Demand-side focuses on tracking global sales data and industry inventory changes. Overall, we believe that the current epidemic has a certain impact on demand, and the panel shows that prices may be under short-term pressure in April or May. But as Samsung’s exit from LCD capacity accelerates, industry inventories remain low. So once the overseas epidemic is contained and domestic demand picks up, the panel suggests prices will surge. We are firmly optimistic about the A-share panel display plate investment value, maintain the industry “optimistic” rating. Suggested attention: BOE A, TCL Technology.

LG Display and Samsung Display are struggling to find their ways out of the deterioration of their performance even after withdrawing from production of liquid crystal display (LCD) panels. The high-priced organic light emitting diode (OLED) panel sector regarded as a future growth engine is not growing fast due to the economic downturn. Even in the OLED panel sector, Chinese display makers are within striking distance of Korean display makers, experts say.

On Aug. 30, Display Supply Chain Consultants (DSCC), a market research company, predicted that LCD TV panel prices hit an all-time low in August and that an L-shaped recession will continue in the fourth quarter. According to DSCC, the average price of a 65-inch ultra-high-definition (UHD) panel in August was only US$109, a 62 percent drop from the highest price of US$288 recorded in July in 2021. The average price of a 75-inch UHD panel was only US$218, which was only about half of the highest price of US$410 in July last year. DSCC predicted that the average panel price in the third quarter will fall by 15.7 percent. As Chinese companies’ price war and the effect of stagnation in consumption overlapped, the more LCD panels display makers produce, the more loss they suffer.

As panel prices fell, manufacturers responded by lowering facility utilization rates. DSCC said that the LCD factory utilization rate descended from 87 percent in April to 83 percent in May, 73 percent in June, and 70 percent in July.

Now that the LCD panel business has become no longer lucrative, Korean display makers have shut down their LCD business or shrunk their sizes. In the LCD sector, China has outpaced Korea since 2018. China’s LCD market share reached 50.9 percent in 2021, while that of Korea dropped to 14.4 percent, lower than Taiwan’s 31.6 percent.

Samsung Display already announced its withdrawal from the LCD business in June. Only 10 years have passed since the company was spun off from Samsung Electronics in 2012. LG Display has decided to halt domestic LCD TV panel production until 2023 and reorganize its business structure centering on OLED panels. Its Chinese LCD production line will be gradually converted to produce LCD panels for IT or commercial products. TrendForce predicted that LG Display will stop operating its P7 Plant in the first quarter of next year.

Korean display makers’ waning LCD business led to a situation in which Korea even lost first place in the display industry. Korea with a display market share of 33.2 percent was already overtaken by China with 41.5 percent) in 2021 according to market researcher Omdia and the Korea Display Industry Association. Korea’s market share has never rebounded in for five years since 2017 amid the Korean government’s neglect. Seventeen years have passed since 2004 when Korea overtook Japan to rise to the top of the world in the LCD industry. Korea’s LCD exports amounted to more than US$30 billion in 2014, but fell to US$21.4 billion last year.

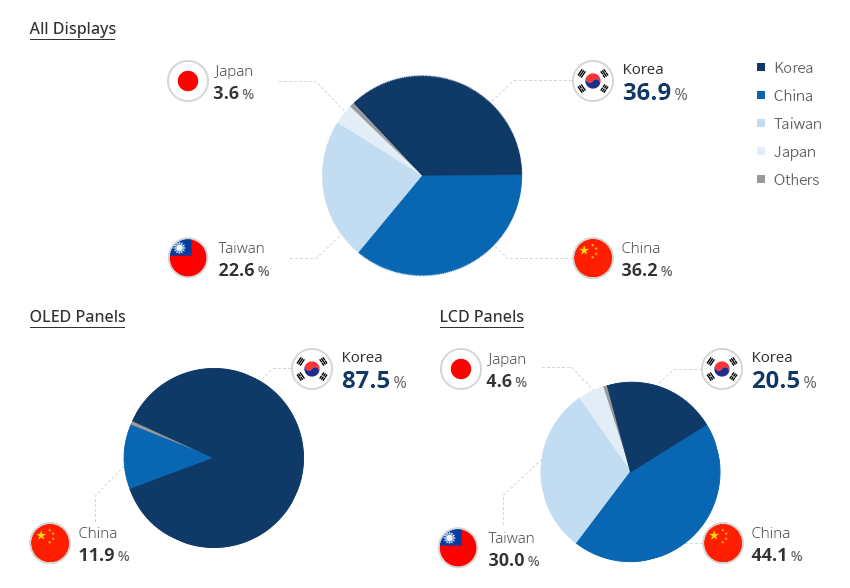

A bigger problem is that Korean display makers may lose its leadership in the OLED panel sector although it is still standing at the top spot. While Korea’s OLED market share fell from 98.1 percent in 2016 to 82.8 percent last year, that of China rose from 1.1 percent to 16.6 percent. Considering that the high-end TV market is highly likely to shrink for the time being due to a full-fledged global consumption contraction, some analysts say that the technology gap between Korea and China can be sharply narrowed through this looming TV market slump. According to industry sources, the Chinese government is now focusing on giving subsidies to the development of OLED panel technology rather LCD technology. On the other hand, in Korea, displays were also wiped out from national strategic technology industry items under the Restriction of Special Taxation Act which can receive tax benefits for R&D activities on displays.

Chinese display manufacturers are chasing their South Korean rivals closely by planning to release a larger volume of liquid-crystal panels over 32 inches this year, said a market researcher Sunday.

According to a report on the 2017 shipment strategies of Chinese TV panel makers by IHS Markit, Chinese LCD panel suppliers are forecast to ship out a total of 320,000 large-size panels larger than 32 inches by the end of this year, a 33 percent surge from last year.

In the report, Wu mentioned the plans of major Chinese panel firms such as BOE, CSOT, CEC-Panda and HKC to focus on expanding production of 43, 55 and 58-inch panels, adding that demand for 32-inch panels will gradually decrease.

“By the end of 2018, China will be the largest region for TFT LCD capacity, and larger-sized products may make their factories more efficient and profitable than they have been when producing 32-inch panels,” he said.

The strategy shift of the Chinese players suggests that they might outstrip Korean display makers in the global large-size display market, the analyst said.

“The strategies of Chinese panel makers will significantly influence global supply and demand,” Wu said. “In 2015 and 2016, the Chinese companies shipped 33.2 percent of worldwide LCD TV panel, trailing only Korean panel makers at 36.4 percent.”

The competition structure has been advantageous for the Korean players, since their Chinese rivals had been focusing on small LCD panels until last year. But now the Korean firms are facing fiercer competition in prices.

Although demand for organic-light emitting diode panels in the TV market is gradually rising, dominance of LCD panels is projected to continue for the foreseeable future.

“While OLEDs are expected to post sharp growth, they will not be able to usurp LCD as the panels of choice for upper-end TVs,” another report by IHS Markit said.

It is the first time that China took over the No. 1 spot in the display market, which Korea has always been a leader in. The title of “the strongest country in display market” is lost after 17 years. It would not be possible to reclaim the No. 1 spot if Korea cannot find a way to expand investment in next-generation displays such as organic light emitting diodes (OLED).

According to market research firm Omdia, China recorded $64.8 billion in sales including LCD and OLED in the global display market last year. China took over Korea’s No. 1 spot with a market share of 41.5%. Korea"s market share fell 8.3 points (p) to 33.2%. This is the first time since 2004, in 17 years, that Korea had to hand over the No. 1 spot. Korea had a 9.4 p advantage in market share over China up until 2019.

China overtook Korea and seized power in the LCD market by offering a low-priced products. BOE, China"s largest panel manufacturer, has become the world"s largest LCD manufacturer with help of the subsidy from the Chinese government. LCD sales was $28.6 billion last year, accounting for 26.3% of the total LCD market. The sales of Chinese companies such as BOE, CSOT, Tianma, and Visionox increased significantly as demand for TV and information technology (IT) devices increased with the prolonged COVID 19 and increased price of LCD panel.

After taken over in the LCD market, Korea is focusing on the highly-valued OLED market. Samsung Display and LG Display are transforming their LCD production lines to OLED. Korea is the No. 1 with 82.3% of the global OLED market shares according to Omdia, and China’s market share only accounts for16.6%.

China"s dominance is expected to continue for some time because the large display market such as TVs and laptops still depends on LCD. Only when Korea starts to reduce OLED panel prices by mass producing OLED, then Korea can replace the LCD market led by China.

China has also started to narrow the gap with Korea in OLED industry. BOE and other companies have commercialized OLED for small and medium-sized displays such as mobile, laptop, and tablet. Following LCD market, China is threatening Korea in OLED market as well as China expands OLED market share mainly in the Chinese smartphone market.

Critics are pointing out that Korea needs to expand in OLED market and develop new technologies in order to maintain the OLED gap with China. Korea must take control over the large TV panel market, which has a large technological gap with China, and create a new form factor with new technologies such as flexible, rollable, and bendable panels.

An official from the display industry said, “With the government-led industrial promotion policy and copious domestic market, China is making an effort to solidify its leading position in the display industry. There is a neglect on display industry in Korea since the display promotion policy is almost non-existent compared to semiconductors and batteries.”

In 1991, a business unit called Samsung Display was formed to produce the panels used in products made by its parent company, Samsung Electronics. Afterward, it was a leading supplier of LCD panels not just for Samsung Electronics but for other companies in the industry as well.

The business received a stay of execution when the pandemic led to a global surge in demand for consumer electronics, but that demand is now declining, and projections aren"t good for LCD panel revenue.

Add to that the fact that emerging technologies l

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey