lcd panel manufacturers market share 2018 pricelist

The global LCD TV (Liquid Crystal Display Television) market was dominated by Samsung and remained so in 2021 with a market share of over 19 percent by sales volume. LG Electronics takes second place with close to 13 percent in the same year, to beat TLC, one of the well-established brands in this segment.Read moreMarket share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volumeCharacteristic202120202019----

TCL. (March 11, 2022). Market share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volume [Graph]. In Statista. Retrieved December 24, 2022, from https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/

TCL. "Market share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volume." Chart. March 11, 2022. Statista. Accessed December 24, 2022. https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/

TCL. (2022). Market share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volume. Statista. Statista Inc.. Accessed: December 24, 2022. https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/

TCL. "Market Share of Leading Lcd Tv Manufacturers Worldwide from 2019 to 2021, by Sales Volume." Statista, Statista Inc., 11 Mar 2022, https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/

TCL, Market share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volume Statista, https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/ (last visited December 24, 2022)

Prices for all TV panel sizes fluctuated and are forecast to fluctuate between 2020 and 2022. The period from March 2020 to July 2021 saw the biggest price increases, when a 65" UHD panel cost between 171 and 288 U.S. dollars. In the fourth quarter of 2021, such prices fell and are expected to drop to an even lower amount by March 2022.Read moreLCD TV panel prices worldwide from January 2020 to March 2022, by size(in U.S. dollars)Characteristic32" HD43" FHD49"/50" UHD55" UHD65" UHD------

DSCC. (January 10, 2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) [Graph]. In Statista. Retrieved December 24, 2022, from https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars)." Chart. January 10, 2022. Statista. Accessed December 24, 2022. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. (2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars). Statista. Statista Inc.. Accessed: December 24, 2022. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "Lcd Tv Panel Prices Worldwide from January 2020 to March 2022, by Size (in U.S. Dollars)." Statista, Statista Inc., 10 Jan 2022, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC, LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) Statista, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/ (last visited December 24, 2022)

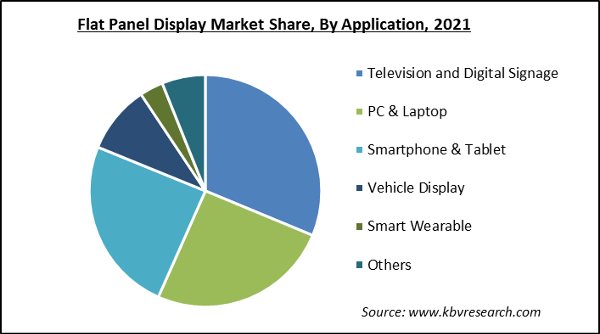

The global TFT-LCD display panel market attained a value of USD 181.67 billion in 2022. It is expected to grow further in the forecast period of 2023-2028 with a CAGR of 5.2% and is projected to reach a value of USD 246.25 billion by 2028.

The current global TFT-LCD display panel market is driven by the increasing demand for flat panel TVs, good quality smartphones, tablets, and vehicle monitoring systems along with the growing gaming industry. The global display market is dominated by the flat panel display with TFT-LCD display panel being the most popular flat panel type and is being driven by strong demand from emerging economies, especially those in Asia Pacific like India, China, Korea, and Taiwan, among others. The rising demand for consumer electronics like LCD TVs, PCs, laptops, SLR cameras, navigation equipment and others have been aiding the growth of the industry.

TFT-LCD display panel is a type of liquid crystal display where each pixel is attached to a thin film transistor. Since the early 2000s, all LCD computer screens are TFT as they have a better response time and improved colour quality. With favourable properties like being light weight, slim, high in resolution and low in power consumption, they are in high demand in almost all sectors where displays are needed. Even with their larger dimensions, TFT-LCD display panel are more feasible as they can be viewed from a wider angle, are not susceptible to reflection and are lighter weight than traditional CRT TVs.

The global TFT-LCD display panel market is being driven by the growing household demand for average and large-sized flat panel TVs as well as a growing demand for slim, high-resolution smart phones with large screens. The rising demand for portable and small-sized tablets in the educational and commercial sectors has also been aiding the TFT-LCD display panel market growth. Increasing demand for automotive displays, a growing gaming industry and the emerging popularity of 3D cinema, are all major drivers for the market. Despite the concerns about an over-supply in the market, the shipments of large TFT-LCD display panel again rose in 2020.

North America is the largest market for TFT-LCD display panel, with over one-third of the global share. It is followed closely by the Asia-Pacific region, where countries like India, China, Korea, and Taiwan are significant emerging market for TFT-LCD display panels. China and India are among the fastest growing markets in the region. The growth of the demand in these regions have been assisted by the growth in their economy, a rise in disposable incomes and an increasing demand for consumer electronics.

The report gives a detailed analysis of the following key players in the global TFT-LCD display panel Market, covering their competitive landscape, capacity, and latest developments like mergers, acquisitions, and investments, expansions of capacity, and plant turnarounds:

*At Expert Market Research, we strive to always give you current and accurate information. The numbers depicted in the description are indicative and may differ from the actual numbers in the final EMR report.

[Introduction]: This paper analyzes the competitive pattern of the panel display industry from both supply and demand sides. On the supply side, the optimization of the industry competition pattern by accelerating the withdrawal of Samsung’s production capacity is deeply discussed. Demand-side focuses on tracking global sales data and industry inventory changes.

Since April 2020, the display device sector rose 4.81%, ranking 11th in the electronic subsectors, 3.39 percentage points behind the SW electronic sector, 0.65 percentage points ahead of the Shanghai and Shenzhen 300 Index. Of the top two domestic panel display companies, TCL Technology is up 11.35 percent in April and BOE is up 4.85 percent.

Specific to the panel display plate, we still do the analysis from both ends of supply and demand: supply-side: February operating rate is insufficient, especially panel display module segment grain rate is not good, limited capacity to boost the panel display price. Since March, effective progress has been made in the prevention and control of the epidemic in China. Except for some production lines in Wuhan that have been delayed, other domestic panels show that the production lines have returned to normal. In South Korea, Samsung announced recently that it would accelerate its withdrawal from all LCD production lines. This round of output withdrawal exceeded market expectations both in terms of pace and amplitude. We will make a detailed analysis of it in Chapter 2.

Demand-side: We believe that people spend more time at home under the epidemic situation, and TV, as an important facility for family entertainment, has strong demand resilience. In our preliminary report, we have interpreted the pick-up trend of domestic TV market demand in February, which also showed a good performance in March. At present, the online market in China maintains a year-on-year growth of about 30% every week, while the offline market is still weak, but its proportion has been greatly reduced. At present, people are more concerned about the impact of the epidemic overseas. According to the research of Cinda Electronics Industry Chain, in the first week, after Italy was closed down, local TV sales dropped by about 45% from the previous week. In addition, Media Markt, Europe’s largest offline consumer electronics chain, also closed in mid-March, which will affect terminal sales to some extent, and panel display prices will continue to be under pressure in April and May. However, we believe that as the epidemic is brought under control, overseas market demand is expected to return to the pace of China’s recovery.

From a price perspective, the panel shows that prices have risen every month through March since the bottom of December 19 reversed. However, according to AVC’s price bulletin of TV panel display in early April, the price of TV panel display in April will decrease slightly, and the price of 32 “, 39.5 “, 43 “, 50 “and 55” panels will all decrease by 1 USD.65 “panel shows price down $2; The 75 “panel shows the price down by $3.The specific reasons have been described above, along with the domestic panel display production line stalling rate recovery, supply-side capacity release; The epidemic spread rapidly in Europe and the United States, sports events were postponed, local blockades were gradually rolled out, and the demand side declined to a certain extent.

Looking ahead to Q2, we think prices will remain under pressure in May, but prices are expected to pick up in June as Samsung’s capacity is being taken out and the outbreak is under control overseas. At the same time, from the perspective of channel inventory, the current all-channel inventory, including the inventory of all panel display factories, has fallen to a historical low. The industry as a whole has more flexibility to cope with market uncertainties. At the same time, low inventory is also the next epidemic warming panel show price foreshadowing.

In terms of valuation level, due to the low concentration and fierce competition in the panel display industry in the past ten years, the performance of sector companies is cyclical to a certain extent. Therefore, PE, PB, and other methods should be comprehensively adopted for valuation. On the other hand, the domestic panel shows that the leading companies in the past years have sustained large-scale capital investment, high depreciation, and a long period of poor profitability, leading to the inflated TTM PE in the first half of 2014 to 2017. Therefore, we will display the valuation level of the sector mainly through the PB-band analysis panel in this paper.

In 2017, due to the combined impact of panel display price rise and OLED production, the valuation of the plate continued to expand, with the highest PB reaching 2.8 times. Then, with the price falling, the panel shows that PB bottomed out at the end of January 2019 at only 1.11 times. From the end of 2019 to February, the panel shows that rising prices have driven PB all the way up, the peak PB reached 2.23 times. Since entering March, affected by the epidemic, in the short term panel prices under pressure, the valuation of the plate once again fell back to 1.62 times. In April, the epidemic situation in the epidemic country was gradually under control, and the valuation of the sector rebounded to 1.68 times.

We believe the sector is still at the bottom of the stage as Samsung accelerates its exit from LCD capacity and industry inventories remain low. Therefore, once the overseas epidemic is under control and the domestic demand picks up, the panel shows that prices will rise sharply. In addition, the plate will also benefit from Ultra HD drive in the long term. Panel display plate medium – and long-term growth logic is still clear. Coupled with the optimization of the competitive pattern, industry volatility will be greatly weakened. The current plate PB compared to the historical high has sufficient space, optimistic about the plate leading company’s investment value.

1). share market, in April in addition to Zhiyun shares, Tiantong shares, Yizhi technology fell, the rest of the stock plate rose, precision test electronics, Lebao high-tech and TCL technology rose larger, reaching 22.38%, 11.45%, and 11.35% respectively.

In the overseas market, benefiting from the control of the epidemic in Japan and South Korea, all stocks except UDC rose. Among them, Innolux Optoelectronics, Finetek, AU Optoelectronics rose more than 10%.

Revenue at Innolux and AU Optronics has been sluggish for several months and improved in March. Since the third quarter of 2017, Innolux’s monthly revenue growth has been negative, while AU Optronics has only experienced revenue growth in a very few months.AU Optronics recorded a record low revenue in January and increased in February and March. Innolux’s revenue returned to growth in March after falling to its lowest in recent years in February. However, because the panel display manufacturers in Taiwan have not put in new production capacity for many years, the production process of the existing production line is relatively backward, and the competitiveness is not strong.

On March 31, Samsung Display China officially sent a notice to customers, deciding to terminate the supply of all LCD products by the end of 2020.LGD had earlier announced that it would close its local LCDTV panel display production by the end of this year. In the following, we will analyze the impact of the accelerated introduction of the Korean factory on the supply pattern of the panel display industry from the perspective of the supply side.

The early market on the panel display plate is controversial, mainly worried about the exit of Korean manufacturers, such as LCD display panel price rise, or will slow down the pace of capacity exit as in 17 years. And we believe that this round of LCD panel prices and 2017 prices are essentially different, the LCD production capacity of South Korean manufacturers exit is an established strategy, will not be transferred because of price warming. Investigating the reasons, we believe that there are mainly the following three factors driving:

(1) Under the localization, scale effect, and aggregation effect, the Chinese panel leader has lower cost and stronger profitability than the Japanese and Korean manufacturers. In terms of cost structure, according to IHS data, material cost accounts for 70% of the cost displayed by the LCD panel, while depreciation accounts for 17%, so the material cost has a significant impact on it. At present, the upstream LCD, polarizer, PCB, mold, and key target material line of the mainland panel display manufacturers are fully imported into the domestic, effectively reducing the material cost. In addition, at the beginning of the factory, manufacturers not only consider the upstream glass and polarizer factory but also consider the synergy between the downstream complete machine factory, so as to reduce the labor cost, transportation cost, etc., forming a certain industrial clustering effect. The growing volume of shipments also makes the economies of scale increasingly obvious. In the long run, the profit gap between the South Korean plant and the mainland plant will become even wider.

(2) The 7 and 8 generation production lines of the Korean plant cannot adapt to the increasing demand for TV in average size. Traditionally, the 8 generation line can only cut the 32 “, 46 “, and 60” panel displays. In order to cut the other size panel displays economically and effectively, the panel display factory has made small adjustments to the 8 generation line size, so there are the 8.5, 8.6, 8.6+, and 8.7 generation lines. But from the cutting scheme, 55 inches and above the size of the panel display only part of the generation can support, and the production efficiency is low, hindering the development of large size TV. Driven by the strong demand for large-size TV, the panel display generation line is also constantly breaking through. In 2018, BOE put into operation the world’s first 10.5 generation line, the Hefei B9 plant, with a designed capacity of 120K/ month. The birth of the 10.5 generation line is epoch-making. It solves the cutting problem of large-size panel displays and lays the foundation for the outbreak of large-size TV. From the cutting method, one 10.5 generation line panel display can effectively cut 18 43 inches, 8 65 inches, 6 75 inches panel display, and can be more efficient in hybrid mode cutting, with half of the panel display 65 inches, the other half of the panel display 75 inches, the yield is also guaranteed. Currently, there are a total of five 10.5 generation lines in the world, including two for domestic panel display companies BOE and Huaxing Optoelectronics. Sharp has a 10.5 generation line in Guangzhou, which is mainly used to produce its own TV. Korean manufacturers do not have the 10.5 generation line. In the context of the increasing size of the TV, Korean manufacturers are obviously at a disadvantage in competitiveness.

(3) As the large-size OLED panel display technology has become increasingly mature, Samsung and LGD hope to transfer production to large-size OLED with better profit prospects as soon as possible. Apart from the price factor, the reason why South Korean manufacturers are exiting LCD production is more because the large-size OLED panel display technology is becoming mature, and Samsung and LGD hope to switch to large-size OLED production as soon as possible, which has better profit prospects. At present, there are three major large-scale OLED solutions including WOLED, QD OLED, and printed OLED, while there is only WOLED with a mass production line at present.

According to statistics, shipments of OLED TVs totaled 2.8 million in 2018 and increased to 3.5 million in 2019, up 25 percent year on year. But it accounted for only 1.58% of global shipments. The capacity gap has greatly limited the volume of OLED TV.LG alone consumes about 47% of the world’s OLED TV panel display capacity, thanks to its own capacity. Other manufacturers can only purchase at a high price. According to the industry chain survey, the current price of a 65-inch OLED panel is around $800-900, while the price of the same size LCD panel is currently only $171.There is a significant price difference between the two.

Samsung and LGD began to shut down LCD production lines in Q3 last year, leading to the recovery of the panel display sector. Entering 2020, the two major South Korean plants have announced further capacity withdrawal planning. In the following section, we will focus on its capacity exit plan and compare it with the original plan. It can be seen that the pace and magnitude of Samsung’s exit this round is much higher than the market expectation:

(1) LGD: LGD currently has three large LCD production lines of P7, P8, and P9 in China, with a designed capacity of 230K, 240K, and 90K respectively. At the CES exhibition at the beginning of this year, the company announced that IT would shut down all TV panel display production capacity in South Korea in 2020, mainly P7 and P8 lines, while P9 is not included in the exit plan because IT supplies IT panel display for Apple.

(2) Samsung: At present, Samsung has L8-1, L8-2, and L7-2 large-size LCD production lines in South Korea, with designed production capacities of 200K, 150K, and 160K respectively. At the same time in Suzhou has a 70K capacity of 8 generation line.

This round of capacity withdrawal of South Korean plants began in June 2019. Based on the global total production capacity in June 2019, Samsung will withdraw 1,386,900 square meters of production capacity in 2019-2020, equivalent to 9.69% of the global production capacity, according to the previous two-year withdrawal expectation. In 2021, 697,200 square meters of production capacity will be withdrawn, which is equivalent to 4.87% of the global production capacity, and a total of 14.56% will be withdrawn in three years. After the implementation of the new plan, Samsung will eliminate 2.422 million square meters of production capacity by the end of 2020, equivalent to 16.92 percent of the global capacity. This round of production plans from the pace and range are far beyond the market expectations.

Global shipments of TV panel displays totaled 281 million in 2019, down 1.06 percent year on year, according to Insight. In fact, TV panel display shipments have been stable since 2015 at between 250 and 300 million units. At the same time, from the perspective of the structure of sales volume, the period from 2005 to 2010 was the period when the size of China’s TV market grew substantially. Third-world sales also leveled off in 2014. We believe that the sales volume of the TV market has stabilized and there is no big fluctuation. The impact of the epidemic on the overall demand may be more optimistic than the market expectation.

In contrast to the change in volume, we believe that the core driver of the growth in TV panel display demand is actually the increase in TV size. According to the data statistics of Group Intelligence Consulting, the average size of TV panel display in 2014 was 0.47 square meters, equivalent to the size of 41 inches screen. In 2019, the average TV panel size is 0.58 square meters, which is about the size of a 46-inch screen. From 2014 to 2019, the average CAGR of TV panel display size is 4.18%. Meanwhile, the shipment of TV in 2019 also increased compared with that in 2014. Therefore, from 2014 to 2019, the compound growth rate of the total area demand for TV panel displays is 6.37%.

It is assumed that 4K screen and 8K screen will accelerate the penetration and gradually become mainstream products in the next 2-3 years. The pace of screen size increase will accelerate. We have learned through industry chain research that the average size growth rate of TV will increase to 6-8% in 2020. Driven by the growth of the average size, the demand area of global TV panel displays is expected to grow even if TV sales decline, and the upward trend of industry demand remains unchanged.

Meanwhile, the global LCDTV panel display demand will increase significantly in 2021, driven by the recovery of terminal demand and the continued growth of the average TV size. In 2021, the whole year panel display will be in a short supply situation, the mainland panel shows that both males will enjoy the price elasticity.

This paper analyzes the competition pattern of the panel display industry from both supply and demand sides. On the supply side, the optimization of the industry competition pattern by accelerating the withdrawal of Samsung’s production capacity is deeply discussed. Demand-side focuses on tracking global sales data and industry inventory changes. Overall, we believe that the current epidemic has a certain impact on demand, and the panel shows that prices may be under short-term pressure in April or May. But as Samsung’s exit from LCD capacity accelerates, industry inventories remain low. So once the overseas epidemic is contained and domestic demand picks up, the panel suggests prices will surge. We are firmly optimistic about the A-share panel display plate investment value, maintain the industry “optimistic” rating. Suggested attention: BOE A, TCL Technology.

1.1. THE POLICY COVERS THE HANDLING OF THE PRIVATE INFORMATION EACH USER SHARES WITH TRENDFORCE WHILE VISITING OUR WEBSITES. IF A DIFFERENT PRIVATE POLICY HAS BEEN REFERED TO FOR SPECIFIC TRENDFORCE WEBSITES AND SERVICES, THAT POLICY WILL REPLACE OR SUPPLEMENT THE PRIVACY POLICY MENTIONED IN THIS DOCUMENT. THIS POLICY ALSO COVERS INDIVIDUALS LEGALLY RESIDING IN OR ORGANIZATIONS LEGALLY BASED IN MEMBER COUNTRIES OF THE EUROPEAN UNION (EU) AND ARE SUBJECTED TO EU GENERAL DATA PROTECTION REGULATION (GDPR) WITH REGARD TO PROVISION OF SERVICES AND PERSONAL DATA PROTECTION.

2.1 THE WEBSITE WILL COLLECT AND USE USER INFORMATION FOR PURPOSES SUCH AS MARKETING, CONSUMER PROTECTION, CONSUMER/CLIENT MANAGEMENT, E-COMMERCE SERVICES, FINANCIAL ACCOUNTING, CONTRACTUAL MATTERS, RESEARCH ANALYSIS, AND DATA PROCESSING. WHEN REQUIRED BY LAW, THE WEBSITE MAY ALSO PROVIDE PERSONAL INFORMATION TO NON-GOVERNMENT AGENCIES.

THE WEBSITE WILL NOT DISCLOSE OR SHARE ANY PERSONAL INFORMATION EXCPET PER SPECIAL REQUEST OR WHEN PERMISSION IS RECEIVED FROM THE USER. OTHER EXCEPTIONS INCLUDE:

IN ACCORDANCE WITH ARTICLE 3 OF THE PERSONAL INFORMATION PROTECTION LAW, YOU WILL HAVE THE OPTION TO EXERCISE THE FOLLOWING RIGHTS WITH REGARD TO THE PERSONAL INFORMATION SHARED WITH THE WEBSITE:

a. TO PREVENT UNAUTHORIZED PARTIES FROM ACCESSING, MODIFYING, OR LEAKING PERSONAL USER DATA, THE WEBSITE WILL TAKE STEPS TO IMPLEMENT PROPER SAFETY MEASURES. THE DATA SEARCHED AND RECORDED ON THE WEBSITE AND THE APPROPRIATE SAFETY MEASURES CHOSEN WILL ALL BE REVIEWED CAREFULLY. CONSIDERING HOW THE SAFETY OF TRANSMITTING DATA ON THE INTERNET CAN NEVER BE GUARANTEED COMPLETELY, USERS SHOULD KEEP IN MIND ALL POSSIBLE RISKS ASSOCIATED WITH ONLINE DATA TRANSFERS AND TAKE RESPONSIBILITY FOR ANY INFORMATION SHARED WITH OR OBTAINED FROM THE WEBSITE.

BE SURE TO PROTECT ALL PASSWORDS AND PERSONAL INFORMATION, REFRAIN FROM DISCLOSING PRIVATE USER INFORMATION TO ANY THIRD PARTY, AND REGISTER WITH THE WEBSITE UPON COMPLETING ALL NECESSARY MEMBERSHIP PROCEDURES. WHEN USING A SHARED OR PUBLIC COMPUTER, PLEASE MAKE SURE TO PROPERLY CLOSE ALL RELEVANT BROWSERS TO PREVENT OTHERS FROM READING YOUR PERSONAL E-MAILS OR INFORMATION.

1.1. THE POLICY COVERS THE HANDLING OF THE PRIVATE INFORMATION EACH USER SHARES WITH TRENDFORCE WHILE VISITING OUR WEBSITES. IF A DIFFERENT PRIVATE POLICY HAS BEEN REFERED TO FOR SPECIFIC TRENDFORCE WEBSITES AND SERVICES, THAT POLICY WILL REPLACE OR SUPPLEMENT THE PRIVACY POLICY MENTIONED IN THIS DOCUMENT. THIS POLICY ALSO COVERS INDIVIDUALS LEGALLY RESIDING IN OR ORGANIZATIONS LEGALLY BASED IN MEMBER COUNTRIES OF THE EUROPEAN UNION (EU) AND ARE SUBJECTED TO EU GENERAL DATA PROTECTION REGULATION (GDPR) WITH REGARD TO PROVISION OF SERVICES AND PERSONAL DATA PROTECTION.

2.1 THE WEBSITE WILL COLLECT AND USE USER INFORMATION FOR PURPOSES SUCH AS MARKETING, CONSUMER PROTECTION, CONSUMER/CLIENT MANAGEMENT, E-COMMERCE SERVICES, FINANCIAL ACCOUNTING, CONTRACTUAL MATTERS, RESEARCH ANALYSIS, AND DATA PROCESSING. WHEN REQUIRED BY LAW, THE WEBSITE MAY ALSO PROVIDE PERSONAL INFORMATION TO NON-GOVERNMENT AGENCIES.

THE WEBSITE WILL NOT DISCLOSE OR SHARE ANY PERSONAL INFORMATION EXCPET PER SPECIAL REQUEST OR WHEN PERMISSION IS RECEIVED FROM THE USER. OTHER EXCEPTIONS INCLUDE:

IN ACCORDANCE WITH ARTICLE 3 OF THE PERSONAL INFORMATION PROTECTION LAW, YOU WILL HAVE THE OPTION TO EXERCISE THE FOLLOWING RIGHTS WITH REGARD TO THE PERSONAL INFORMATION SHARED WITH THE WEBSITE:

a. TO PREVENT UNAUTHORIZED PARTIES FROM ACCESSING, MODIFYING, OR LEAKING PERSONAL USER DATA, THE WEBSITE WILL TAKE STEPS TO IMPLEMENT PROPER SAFETY MEASURES. THE DATA SEARCHED AND RECORDED ON THE WEBSITE AND THE APPROPRIATE SAFETY MEASURES CHOSEN WILL ALL BE REVIEWED CAREFULLY. CONSIDERING HOW THE SAFETY OF TRANSMITTING DATA ON THE INTERNET CAN NEVER BE GUARANTEED COMPLETELY, USERS SHOULD KEEP IN MIND ALL POSSIBLE RISKS ASSOCIATED WITH ONLINE DATA TRANSFERS AND TAKE RESPONSIBILITY FOR ANY INFORMATION SHARED WITH OR OBTAINED FROM THE WEBSITE.

BE SURE TO PROTECT ALL PASSWORDS AND PERSONAL INFORMATION, REFRAIN FROM DISCLOSING PRIVATE USER INFORMATION TO ANY THIRD PARTY, AND REGISTER WITH THE WEBSITE UPON COMPLETING ALL NECESSARY MEMBERSHIP PROCEDURES. WHEN USING A SHARED OR PUBLIC COMPUTER, PLEASE MAKE SURE TO PROPERLY CLOSE ALL RELEVANT BROWSERS TO PREVENT OTHERS FROM READING YOUR PERSONAL E-MAILS OR INFORMATION.

LG Display and Samsung Display are struggling to find their ways out of the deterioration of their performance even after withdrawing from production of liquid crystal display (LCD) panels. The high-priced organic light emitting diode (OLED) panel sector regarded as a future growth engine is not growing fast due to the economic downturn. Even in the OLED panel sector, Chinese display makers are within striking distance of Korean display makers, experts say.

On Aug. 30, Display Supply Chain Consultants (DSCC), a market research company, predicted that LCD TV panel prices hit an all-time low in August and that an L-shaped recession will continue in the fourth quarter. According to DSCC, the average price of a 65-inch ultra-high-definition (UHD) panel in August was only US$109, a 62 percent drop from the highest price of US$288 recorded in July in 2021. The average price of a 75-inch UHD panel was only US$218, which was only about half of the highest price of US$410 in July last year. DSCC predicted that the average panel price in the third quarter will fall by 15.7 percent. As Chinese companies’ price war and the effect of stagnation in consumption overlapped, the more LCD panels display makers produce, the more loss they suffer.

As panel prices fell, manufacturers responded by lowering facility utilization rates. DSCC said that the LCD factory utilization rate descended from 87 percent in April to 83 percent in May, 73 percent in June, and 70 percent in July.

Now that the LCD panel business has become no longer lucrative, Korean display makers have shut down their LCD business or shrunk their sizes. In the LCD sector, China has outpaced Korea since 2018. China’s LCD market share reached 50.9 percent in 2021, while that of Korea dropped to 14.4 percent, lower than Taiwan’s 31.6 percent.

Samsung Display already announced its withdrawal from the LCD business in June. Only 10 years have passed since the company was spun off from Samsung Electronics in 2012. LG Display has decided to halt domestic LCD TV panel production until 2023 and reorganize its business structure centering on OLED panels. Its Chinese LCD production line will be gradually converted to produce LCD panels for IT or commercial products. TrendForce predicted that LG Display will stop operating its P7 Plant in the first quarter of next year.

Korean display makers’ waning LCD business led to a situation in which Korea even lost first place in the display industry. Korea with a display market share of 33.2 percent was already overtaken by China with 41.5 percent) in 2021 according to market researcher Omdia and the Korea Display Industry Association. Korea’s market share has never rebounded in for five years since 2017 amid the Korean government’s neglect. Seventeen years have passed since 2004 when Korea overtook Japan to rise to the top of the world in the LCD industry. Korea’s LCD exports amounted to more than US$30 billion in 2014, but fell to US$21.4 billion last year.

A bigger problem is that Korean display makers may lose its leadership in the OLED panel sector although it is still standing at the top spot. While Korea’s OLED market share fell from 98.1 percent in 2016 to 82.8 percent last year, that of China rose from 1.1 percent to 16.6 percent. Considering that the high-end TV market is highly likely to shrink for the time being due to a full-fledged global consumption contraction, some analysts say that the technology gap between Korea and China can be sharply narrowed through this looming TV market slump. According to industry sources, the Chinese government is now focusing on giving subsidies to the development of OLED panel technology rather LCD technology. On the other hand, in Korea, displays were also wiped out from national strategic technology industry items under the Restriction of Special Taxation Act which can receive tax benefits for R&D activities on displays.

Flat-panel displays are thin panels of glass or plastic used for electronically displaying text, images, or video. Liquid crystal displays (LCD), OLED (organic light emitting diode) and microLED displays are not quite the same; since LCD uses a liquid crystal that reacts to an electric current blocking light or allowing it to pass through the panel, whereas OLED/microLED displays consist of electroluminescent organic/inorganic materials that generate light when a current is passed through the material. LCD, OLED and microLED displays are driven using LTPS, IGZO, LTPO, and A-Si TFT transistor technologies as their backplane using ITO to supply current to the transistors and in turn to the liquid crystal or electroluminescent material. Segment and passive OLED and LCD displays do not use a backplane but use indium tin oxide (ITO), a transparent conductive material, to pass current to the electroluminescent material or liquid crystal. In LCDs, there is an even layer of liquid crystal throughout the panel whereas an OLED display has the electroluminescent material only where it is meant to light up. OLEDs, LCDs and microLEDs can be made flexible and transparent, but LCDs require a backlight because they cannot emit light on their own like OLEDs and microLEDs.

Liquid-crystal display (or LCD) is a thin, flat panel used for electronically displaying information such as text, images, and moving pictures. They are usually made of glass but they can also be made out of plastic. Some manufacturers make transparent LCD panels and special sequential color segment LCDs that have higher than usual refresh rates and an RGB backlight. The backlight is synchronized with the display so that the colors will show up as needed. The list of LCD manufacturers:

Organic light emitting diode (or OLED displays) is a thin, flat panel made of glass or plastic used for electronically displaying information such as text, images, and moving pictures. OLED panels can also take the shape of a light panel, where red, green and blue light emitting materials are stacked to create a white light panel. OLED displays can also be made transparent and/or flexible and these transparent panels are available on the market and are widely used in smartphones with under-display optical fingerprint sensors. LCD and OLED displays are available in different shapes, the most prominent of which is a circular display, which is used in smartwatches. The list of OLED display manufacturers:

MicroLED displays is an emerging flat-panel display technology consisting of arrays of microscopic LEDs forming the individual pixel elements. Like OLED, microLED offers infinite contrast ratio, but unlike OLED, microLED is immune to screen burn-in, and consumes less power while having higher light output, as it uses LEDs instead of organic electroluminescent materials, The list of MicroLED display manufacturers:

LCDs are made in a glass substrate. For OLED, the substrate can also be plastic. The size of the substrates are specified in generations, with each generation using a larger substrate. For example, a 4th generation substrate is larger in size than a 3rd generation substrate. A larger substrate allows for more panels to be cut from a single substrate, or for larger panels to be made, akin to increasing wafer sizes in the semiconductor industry.

"Samsung Display has halted local Gen-8 LCD lines: sources". THE ELEC, Korea Electronics Industry Media. August 16, 2019. Archived from the original on April 3, 2020. Retrieved December 18, 2019.

"TCL to Build World"s Largest Gen 11 LCD Panel Factory". www.businesswire.com. May 19, 2016. Archived from the original on April 2, 2018. Retrieved April 1, 2018.

"Panel Manufacturers Start to Operate Their New 8th Generation LCD Lines". 대한민국 IT포털의 중심! 이티뉴스. June 19, 2017. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"TCL"s Panel Manufacturer CSOT Commences Production of High Generation Panel Modules". www.businesswire.com. June 14, 2018. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"Business Place Information – Global Operation | SAMSUNG DISPLAY". www.samsungdisplay.com. Archived from the original on 2018-03-26. Retrieved 2018-04-01.

"Samsung Display Considering Halting Some LCD Production Lines". 비즈니스코리아 - BusinessKorea. August 16, 2019. Archived from the original on April 5, 2020. Retrieved December 19, 2019.

Herald, The Korea (July 6, 2016). "Samsung Display accelerates transition from LCD to OLED". www.koreaherald.com. Archived from the original on April 1, 2018. Retrieved April 1, 2018.

Byeonghwa, Yeon. "Business Place Information – Global Operation – SAMSUNG DISPLAY". Samsungdisplay.com. Archived from the original on 2018-03-26. Retrieved 2018-04-01.

www.wisechip.com.tw. "WiseChip History – WiseChip Semiconductor Inc". www.wisechip.com.tw. Archived from the original on 2018-02-17. Retrieved 2018-02-17.

"China"s BOE to have world"s largest TFT-LCD+AMOLED capacity in 2019". ihsmarkit.com. 2017-03-22. Archived from the original on 2019-08-16. Retrieved 2019-08-17.

It may seem odd in the face of stalled economies and stalled AV projects, but the costs of LCD display products are on the rise, according to a report from Digital Supply Chain Consulting, or DSCC.

Demand for LCD products remains strong , says DSCC, at the same time as shortages are deepening for glass substrates and driver integrated circuits. Announcements by the Korean panel makers that they will maintain production of LCDs and delay their planned shutdown of LCD lines has not prevented prices from continuing to rise.

I assume, but absolutely don’t know for sure, that panel pricing that affects the much larger consumer market must have a similar impact on commercial displays, or what researchers seem to term public information displays.

Panel prices increased more than 20% for selected TV sizes in Q3 2020 compared to Q2, and by 27% in Q4 2020 compared to Q3, we now expect that average LCD TV panel prices in Q1 2021 will increase by another 12%.

The first chart shows our latest TV panel price update, with prices increasing across the board from a low in May 2020 to an expected peak in May/June of this year. Last month’s update predicted a peak in February/March. However, our forecast for the peak has been increased and pushed out after AGC reported a major accident at a glass plant in Korea and amid continuing problems with driver IC shortages.

The inflection point for this cycle, the month of the most significant M/M price increases, was passed in September 2020, and the price increases have been slowing down each month since then, but the January increase averaged 4.1%. Prices in February 2021 have reached levels last seen exactly three years ago in February 2018.

Prices increased in Q4 for all sizes of TV panels, with massive percentage increases in sizes from 32” to 55” ranging from 28% to 38%. Prices for 65” and 75” increased at a slower rate, by 19% and 8% respectively, as capacity has continued to increase on those sizes with Gen 10.5 expansions.

Prices for every size of TV panel will increase in Q1 at a slower rate, ranging from 5% for 75” to 16% for 43”, and we now expect that prices will continue to increase in Q2, with the increases ranging from 3% to 6% on a Q/Q basis. We now expect that prices will peak in Q2 and will start to decline in Q3, but the situation remains fluid.

All that said, LCD panels are way less costly, way lighter and slimmer, and generally look way better than the ones being used 10 years ago, so prices is a relative problem.

In the recently released Quarterly OLED Shipment Report , DSCC reveals that 2023 OLED panel revenues are expected to increase 2% Y/Y to $42B after declining 2% Y/Y in 2022. This recovery is the result of expected triple digit growth for monitors, AR/VR and automotive applications and double-digit growth for notebook PCs, TVs and tablets.

As reported by Italian newspaper DDay, the EU Commission has confirmed that its much stricter Energy Efficiency Index (EEI) will be implemented as planned in March 2023 without revision. The new EEI will make it much more challenging to sell 8K TVs in Europe in 2023; all 8K TVs on the market there currently fail to meet the requirements.

After upgrading display capacity for six straight issues on improved market conditions in LCDs, DSCC has now lowered its display capacity forecast for four consecutive quarters on delays and cancellations as conditions worsen and remain weak. Prices were recently at marginal costs for LCD TV panels and it is projected that it will take until 2H’23 for prices to rise above cash costs.

After a weak Q2’22, the combination of macroeconomic and geopolitical events continued to hinder growth for the Advanced TV market, according to the latest update of DSCC’s Quarterly Advanced TV Shipment and Forecast Report, now available to subscribers. Samsung struggled through a difficult quarter, losing both unit and revenue share while its three biggest competitors – LG, Sony and TCL – all gained share.

Panel suppliers are mostly delaying new capacity decisions given the weak market conditions in the display market. The situation is particularly dire in LCDs where LCD TV panel prices approached marginal cost levels and BOE’s Chairman indicated they won’t build any more LCD TV fabs, resulting in the cancellation of B17+ and its removal from our forecast. The weakness in LCDs also spread to OLED spending since there is an oversupply there also and most OLED manufacturers also produce LCDs and are currently losing money. Samsung Display is the exception as it earned record OLED operating profits and operating margins in Q4’22 helped by strong iPhone 14 Pro/Pro Max demand and LG Display’s challenges getting qualified for the 14 Pro Max.

The central promotional event of the holiday season happens this week, and retailers will be offering all-time low prices for TVs during Black Friday. The unprecedented decline in LCD TV panel prices continues to flow through to retail prices in the US, and the competition from LCD is also pulling down OLED TV prices, which are also hitting all-time lows.

Now that all of the industry’s flat panel display makers have reported their Q3’22 financial results, we update our industry profile. The third quarter showed a gaping chasm between OLED-focused display makers, especially Samsung Display, and the companies focused on LCD technology. For LCD makers, it was the worst quarter in years and perhaps the worst ever. Meanwhile, Samsung Display recorded its highest profits ever in the first quarter after it discontinued LCD production.

As revealed in DSCC’s latest release of the OLED Shipment Report – Flash Edition, OLED panel revenues decreased 11% Y/Y on a 17% Y/Y decline in panel shipments. Smartphones, tablets and TVs, which have a combined 70% unit share and 85% panel revenue share, decline while other categories had Y/Y unit growth.

**Please note that this price list may be abbreviated. For the most comprehensive view of the NASDAQ Stock Market fee and rebate schedule, please refer to the Order Execution and Routing section of the NASDAQ Rule Book.

All percentages below are Firm or MPID share volumes expressed as a percentage of consolidated U.S. average daily share volume. Note that on December 9th, 2013, NASDAQ began excluding odd-lot transactions from industry volume calculations. However,odd lots are always included as part of any Firm or MPID"s volume for purposes of tier calculations.

Increases average daily volume of Midpoint Extended Life Orders (including midpoint orders that execute against Midpoint Extended Life Orders) by 1 million shares or more versus the firm’s June 2021 Midpoint Extended Life Orders (including midpoint orders that execute against Midpoint Extended Life Orders) ADV; or

Firm adds a minimum average daily volume of 3 million shares through midpoint orders (midpoint add + MELO) and grows midpoint add ADV (midpoint add + MELO) by 100% or more vs June 2021 midpoint add ADV (midpoint add + MELO)

M-ELO Supplemental Credit B: Firm adds a minimum ADV of 5 million shares through midpoint and Midpoint Extended Life Orders (that execute against Midpoint Extended Life Orders)

Add NOM Market Maker liquidity in Penny Pilot Options and/or Non- Penny Pilot Options of 0.20% or more of total industry ADV in the customer clearing range for Equity and ETF option contracts per day in a month on NOM; and

Add Customer, Professional, Firm, Non-NOM Market Maker and/or Broker-Dealer liquidity in Penny Pilot Options and/or Non- Penny Pilot Options of 1.50% or more of total industry ADV in the customer clearing range for Equity and ETF option contracts per day in a month on NOM

Add Customer, Professional, Firm, Non-NOM Market Maker and/or Broker-Dealer liquidity in Penny Pilot Options and/or Non- Penny Pilot Options of 1.15% or more of total industry ADV in the customer clearing range for Equity and ETF option contracts per day in a month on NOM

Members with shares executed in the Opening and Closing Cross comprised of imbalance orders and/or limit on close orders entered after 3:55pm that represent more than 0.01% Consolidated Volume during the month

Firm adds greater than 4 million shares per day, of which 1.5 million share per day are non-displayed liquidity (excluding midpoint orders) or Midpoint Extended Life Orders

NASDAQ rewards market makers who actively quote at the National Best Bid or Offer (NBBO) in a broad set of securities through the QMM program. A Member attains QMM status by meeting certain quoting requirements each month. By meeting affirmative standards, QMMs receive meaningful benefits to further encourage broad-based liquidity provision.

Maintain a one- or two-sided quote, of at least one round lot at the NBBO in an average of 1,000 securities for at least 25% of market hours each month through one or more Nasdaq Market Center MPIDs.

QMM rebate incentives for achieving the QMM criteria are as follows: A rebate per share executed (as defined in the below table) for all displayed orders (other than Designated Retail Orders) in securities priced at $1 or more per share that provide liquidity and were for securities listed on NYSE ("Tape A QMM Incentive"), securities listed on exchanges other than Nasdaq and NYSE ("Tape B QMM Incentive"), or securities listed on Nasdaq (“Tape C QMM Incentive”). Such rebate for executions will be in addition to any rebate payable under Rule 7018 (existing add displayed liquidity rebates):

Member adds liquidity (displayed, non-displayed, and midpoint) provided in all securities through one or more of its Nasdaq Market Center MPIDs that represents 0.70% up to and including 0.90% of Consolidated Volume during the month or 70 million shares ADV during the month.

Member adds liquidity (displayed, non-displayed, and midpoint) provided in all securities through one or more of its Nasdaq Market Center MPIDs that represents 0.80% up to and including 0.90% (in securities priced at or greater than $1) of Consolidated Volume (in securities priced at or greater than $1) during the month.

Member adds liquidity (displayed, non-displayed, and midpoint) provided in all securities through one or more of its Nasdaq Market Center MPIDs above 0.90% of Consolidated Volume during the month.

Member adds liquidity (displayed, non-displayed, and midpoint) provided in all securities through one or more of its Nasdaq Market Center MPIDs above 0.90% (in securities priced at or greater than $1) of Consolidated Volume (in securities priced at or greater than $1) during the month.

In addition to the above rebate incentives, QMMs that execute shares of liquidity provided in all securities through one or more of its Nasdaq Market Center MPIDs that represent 1.00% or more of Consolidated Volume during the month will be assessed a discounted remove fee of $0.00295 in Tapes A and B for shares executed (in securities priced at or greater than $1). QMMs that meet the criteria of Tier 2 and 1) have a combined Consolidated Volume (adding and removing liquidity) of at least 3.7%; 2) execute 0.35% MOC/LOC; and 3) provide 0.15% liquidity using midpoint orders during the month will be assessed a discounted remove fee of $0.0029 in Tapes A and B for shares executed (in securities priced at or greater than $1).

A Member"s MPIDs may qualify for an additional rebate of $0.000075 in Tapes A and C, and an additional rebate of $0.00005 in Tape B in addition to the Tier 2 QMM incentive by the 1. MPID adding greater than 1.25% TCV; 2. MPID maintaining a one- or two-sided quote, of at least one round lot at the NBBO in an average of at least 2,700 securities for at least 50% of market hours each month through one or more Nasdaq Market Center MPIDs of which at least 1,200 securities are in Tape A securities; and 3. MPID Increasing add volume as a percentage of TCV in Tape A securities by 0.50% versus the MPID’s May 2020 baseline.

Nasdaq will provide a rebate per share executed with respect to all other displayed orders (other than Designated Retail Orders, as defined in Rule 7018) in securities priced at $1 or more per share that provide liquidity and establish the NBBO. The rebate will be in addition to any rebate or credit payable under Rule 7018(a) and the QMM and NBBO Program under Rule 7014.

To qualify for the $0.0004 per share executed in Tape A and B securities, a member must add 1.0% or more of Consolidated Volume during the month and the order must have been entered on a port that has a monthly ratio of NBBO liquidity provided* to total liquidity provided of at least 25%.

Designated Liquidity Providers (DLPs) are market makers who have been selected to increase Market Quality and liquidity provisioning NASDAQ-listed ETPs.

Effective May 2021 The Nasdaq Stock Market (“Nasdaq”) will offer new Designated Liquidity Provider (DLP) program for exchange traded products (ETPs). The program offers additional standard and enhanced rebates given all the Market Quality requirements (see below) are met.

The Nasdaq ETF Team identified 5 key Market Quality Requirements for ETF liquidity DLPs will need to meet including time @ NBBO, time within 5bps of NBBO, notional depth, average spread, and auction quality. Please see the link in the end for more details.

The new DLP program will also offer a secondary DLP program to further increase liquidity support for ETP issuers in lower ADV ETPs. Secondary DLP will need to hit at least 2 Enhanced Market Quality Requirements to qualify for the rebates. Nasdaq will offer the following rebates to secondary DLPs, based on ETP Industry ADV from the prior month:

All routing strategies that check the NASDAQ book (i.e. STGY, SCAN, SKIP, SKNY, DOTA, DOTM) except for shares that route and execute on NYSE. (See “Rates to Route to NYSE” for shares that route and execute on NYSE)

Fee for shares executed in excess of 4 million shares in the month that remove liquidity on Nasdaq or execute on other protected Reg NMS venues, excluding taker-maker venues

1. Fee for shares executed below 4 million shares in the month that remove liquidity on Nasdaq or execute on other protected Reg NMS venues, excluding taker-maker venues; or

2. above 4 million shares executed in the month that remove liquidity on Nasdaq or execute on other protected Reg NMS venues than Nasdaq Center during regular market hours, provided that the member grows its regular market hours volume during the month by at least 100% vs March 2022, excluding taker-maker venues

The NASDAQ Stock Market (NASDAQ), NASDAQ BX (BX) and NASDAQ PSX (PSX) have introduced an Excessive Messaging Policy that encourages active quoting near the NBBO while discouraging excessive order activity away from the inside.

There is a $500 fee for unsuccessful appeals of Clearly Erroneous Rule 11890 adjudications. The party initiating the appeal shall be assessed the $500 fee if the Market Operations Review Committee (MORC) upholds the decision of the NASDAQ official who made the initial determination. The fee will be reflected in the monthly invoice.

Each firm"s Opening Cross charges from Market-On-Open (MOO) and Limit-On-Open (LOO) orders will be capped at $35,000 per month, provided that firm adds one million shares of liquidity, on average, during the month.

Tier A: Shares of added liquidity provided in all Tapes through one or more of its MPIDs that represent above 1.75% of Consolidated Volume or MOC/LOC volume above 0.50% of Consolidated Volume: $0.0008 per executed share

Tier B: Shares of added liquidity provided in all Tapes through one or more of its MPIDs that represent above 0.80% to 1.75% of Consolidated Volume or MOC/LOC volume above 0.30% to 0.50% of Consolidated Volume: $0.0011 per executed share

Tier C: Shares of added liquidity provided in all Tapes through one or more of its MPIDs that represent above 0.50% to 0.80% of Consolidated Volume or MOC/LOC volume above 0.10% to 0.30% of Consolidated Volume: $0.0012 per executed share

Tier D: Shares of added liquidity provided in all Tapes through one or more of its MPIDs that represent above 0.30% to 0.50% of Consolidated Volume: $0.00135 per executed share

Tier E: Shares of added liquidity provided in all Tapes through one or more of its MPIDs that represent above 0.015% to 0.30% of Consolidated Volume: $0.00145 per executed share

Tier F: Shares of added liquidity provided in all Tapes through one or more of its MPIDs that represent 0.00% to 0.015% of Consolidated Volume: $0.0016 per executed share

Tier G: Member adds NOM Customer and/or Professional liquidity in Penny Pilot Options and/or Non-Penny Pilot Options of 0.80% or more of national customer volume in multiply-listed equity and ETF option classes in a month: $0.0010 per executed share

FINRA members reporting over-the-counter (“OTC”) transactions in NMS stocks to a FINRA/Nasdaq TRF for public dissemination or “media” purposes may receive quarterly transaction credits. Firms qualify for tiers on a per tape basis according to each firm"s reported market share volume for trades reported to the FINRA/Nasdaq Trade Reporting Facility (TRF) as a percent of the entire reported volume for each period in each Tape. Firms" tier qualifications will be evaluated each quarter for that period"s payout.

Participants making markets in alternative trading systems registered pursuant to Regulation ATS will qualify for a fee cap applied to all trades under Rule 7620A if they meet the following criteria on a monthly basis:

Participants making markets in alternative trading systems registered pursuant to Regulation ATS that are engaged in Executing Party and Contra Party activities will qualify for a fee cap applied to all trades under Rule 7620A if they meet the following criteria on a monthly basis:

A participant that qualifies for the ATS Market Maker Combined Media Activity fee cap shall pay for that month, on a per Tape basis, the lesser of $7,500 or the sum of all the participant"s combined regular monthly Executing Party and Contra Party fees for that Tape during the month.

Please note that this price list is abbreviated. For the most comprehensive view of The Nasdaq Stock Market connectivity options and fee schedule please review rules 7015, 7034, and 7051 of the Rule Book.

Westford,USA, Oct. 19, 2022 (GLOBE NEWSWIRE) -- The primary factors driving the growth of the Display Market are increasing demand from smartphone and tablet manufacturers, rising expenditure on smart Infra-Red (IR) sensors, and rapid expansion of digital media content. Smartphones are becoming more sophisticated and are using larger screens that require higher resolutions for better user experience. Tablets are also becoming increasingly popular as they offer a single device that can serve as both a computer and a mobile phone. This increase in demand for high-resolution displays is expected to drive the adoption of LED displays in the coming years.

Manufacturers in the global display market are starting to see the potential in displays as an important part of their product lines. Device manufacturers are looking for displays that can be used on a variety of devices, from laptops to smartphones and even cars. In addition, developers are creating more applications that require high-quality displays.

One key challenge facing manufacturers is making sure that their displays meet the requirements of multiple market segments. They need to make sure that their displays are suitable for usage on tablets as well as laptops, yet they also need to create displays that look good on smaller devices like smartphones and digital assistants.

The growth in demand for display market across various verticals such as healthcare, retail, automotive, appliance and others has led to an increasing demand for large sizes screens which can be cost effective owing to their mass production capabilities. Display manufacturers are also exploring new technologies such as flexible displays that can be rolled up like a traditional newspaper

Our report considers several factors such as market size estimation techniques, product segmentation analysis, expenditure Breakdown by Country and region; Porter"s Five Forces Analysis; and price trends analysis to give you a comprehensive view of the global display market.

Some of the key players in the global display market include LG Display Co., Ltd., Samsung Electronics Co., Ltd., and Sharp Corporation. These companies are focused on developing innovative products that meet the needs of various consumers in the marketplace. They also strive to improve their competitiveness by expanding their product lines into new markets and by creating partnerships with other companies to share technology and manufacturing resources.

Among global display market leaders, Samsung is presently dominating the industry with a share of 38% of the market. However, Apple is looming large as one of the largest competitors in smartphone sector. Other prominent players in this segment include LG Display, Sony Corp, and Toshiba Corporation. Among these companies, LG Display has been fastest expanding its business over recent years owing to its focus on emerging markets such as China and India.

For one, it"s heavily invested in research and development in the display market. According to analysts at SkyQuest, Samsung spends more than $13.7 billion a year on R&D, more than any other company in the world. That investment has paid off: The company"s displays are consistently among the best on the market.

Samsung also makes good use of its deep pockets. The company has poured money into forming joint ventures with major chipmakers like Qualcomm and Intel, which allows it to quickly bring new technologies to market. It doesn"t just rely on partnerships; Samsung also invests in its own technology centers, such as the foundry that produces screens for its smartphones.

One important technology that Samsung is investing in is AMOLED and QLED screens. QLEDs are generally considered to be more environmentally friendly than LCDs, since they use less power and create fewer byproducts.

The main drivers for Samsung"s strong performance in the display market are its diversification across product lines, continuous innovation across product categories, and excellent execution capabilities. The company has been able to expand into new markets such as automotive displays and smart watches, while continuing to focus on profitable core products.

Samsung has also been successful in pushing down prices for OLED displays over the past few years. This has made OLED panels more accessible to a wider range of customers, supporting growth at rival companies such as LG Electronics and Sony.

In recent years, there has been a shift in display technology as manufacturers across the global display market experiment with new and more innovative ways to create displays. The trend observed by SkyQuest worldwide is that display technologies are moving towards OLEDs and quantum dots, both of which have a number of advantages.

Quantum dots or QLED offer many advantages over traditional LCDs in the display market, such as better color reproduction, enhanced viewing angles, better response time, and lower power consumption. Their small size also makes them ideal for applications where sliding or tilting LCD panels are not possible or desirable. Quantum dot displays have already begun appearing in consumer electronics and will eventually replace traditional LCDs as the predominant type of display in devices like smartphones and tablets.

SkyQuest Technology is leading growth consulting firm providing market intelligence, commercialization and technology services. It has 450+ happy clients globally.

At present, markets such as large-screen TVs are still inseparable from LCD panels. Several Chinese panel manufacturers have surpassed Samsung and LG to become the main LCD panel manufacturers in recent years. Korean companies are no longer able to compete. Samsung will stop the production of LCD panels half a year ahead of schedule. Samsung used to be the largest LCD panel manufacturer, but in recent years, Chinese companies such as BOE and CSOT have rapidly expanded their market shares. Samsung and LG have continued to retreat, making BOE surpass LGD in 2018. As of now, BOE is now the world’s largest manufacturer of LCD panels.

Samsung originally planned to stop the production of LCD panels by the end of 2020. However, the LCD panel market started to increase prices in the past year or so. This made Samsung’s LCD factory continue to operate for another two years. However, the company originally plans to exit the market at the end of 2022. Nevertheless, the LCD panel market has changed since the end of last year. The price has been falling significantly and it is now on a free fall. By January this year, the average price

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey