lcd panel manufacturers market share 2018 quotation

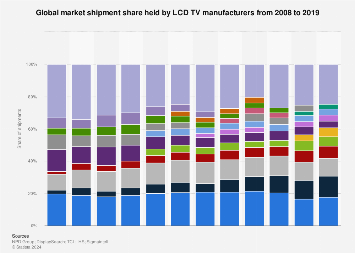

The global LCD TV (Liquid Crystal Display Television) market was dominated by Samsung and remained so in 2021 with a market share of over 19 percent by sales volume. LG Electronics takes second place with close to 13 percent in the same year, to beat TLC, one of the well-established brands in this segment.Read moreMarket share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volumeCharacteristic202120202019----

TCL. (March 11, 2022). Market share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volume [Graph]. In Statista. Retrieved December 24, 2022, from https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/

TCL. "Market share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volume." Chart. March 11, 2022. Statista. Accessed December 24, 2022. https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/

TCL. (2022). Market share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volume. Statista. Statista Inc.. Accessed: December 24, 2022. https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/

TCL. "Market Share of Leading Lcd Tv Manufacturers Worldwide from 2019 to 2021, by Sales Volume." Statista, Statista Inc., 11 Mar 2022, https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/

TCL, Market share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volume Statista, https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/ (last visited December 24, 2022)

In 2019 and 2020, BOE was the leading manufacturer in the monitor display panel market, holding 25 and 26 percent of the market, respectively. LG Display, the South Korean panel maker, ranked second, with a 21 percent share. The market share of another South Korean company, Samsung Display, was forecast to drop to one percent in 2021.Read moreMonitor display panel market share worldwide from 2019 to 2021, by supplierCharacteristicLGDBOESDCINXAUOCECCSOTHKC---------

TrendForce. (January 11, 2021). Monitor display panel market share worldwide from 2019 to 2021, by supplier [Graph]. In Statista. Retrieved December 24, 2022, from https://www.statista.com/statistics/1124858/global-display-panel-vendor-monitor/

TrendForce. "Monitor display panel market share worldwide from 2019 to 2021, by supplier." Chart. January 11, 2021. Statista. Accessed December 24, 2022. https://www.statista.com/statistics/1124858/global-display-panel-vendor-monitor/

TrendForce. (2021). Monitor display panel market share worldwide from 2019 to 2021, by supplier. Statista. Statista Inc.. Accessed: December 24, 2022. https://www.statista.com/statistics/1124858/global-display-panel-vendor-monitor/

TrendForce. "Monitor Display Panel Market Share Worldwide from 2019 to 2021, by Supplier." Statista, Statista Inc., 11 Jan 2021, https://www.statista.com/statistics/1124858/global-display-panel-vendor-monitor/

TrendForce, Monitor display panel market share worldwide from 2019 to 2021, by supplier Statista, https://www.statista.com/statistics/1124858/global-display-panel-vendor-monitor/ (last visited December 24, 2022)

(January 23, 2019) – Global shipments of large thin-film transistor (TFT) liquid crystal display (LCD) panels rose again in 2018 despite concerns of over-supply in the market. In particular, area shipments increased by 10.6 percent to 197.9 million square meters compared to the previous year, driven by TV and monitor panels, according to

Fierce price competition in large 65- and 75-inch display panels was ignited as Chinese panel maker BOE started the mass production of the panels in 2018 at its B9 10.5-generation facility. “With BOE operating the 10.5-generation line, panel makers have become more aggressive on pricing since early 2018 to digest their capacity,” said

Rising demand for gaming-PC and professional-purpose monitors boosted shipments of high-end, large panels. “Some panel makers have allocated more monitor panels to the fab, replacing existing TV panels, to make up for poor performance of that business,” Wu said.

Demand for other applications, which include public, automotive and industrial displays, recorded the highest growth rates of 17.5 percent by area and 28.6 percent by unit. “Panel makers view these applications as a new cash cow that can compensate for the sharp price erosion in main panels for TVs, monitors and notebook PCs,” Wu said.

LG Display led the area shipments of large display panels, with a 21 percent share in 2018, followed by BOE (17 percent) and Samsung Display (16 percent). BOE boasted the largest unit-shipment share of 23 percent, followed by LG Display (20 percent) and Innolux (17 percent), according to the

Large TFT LCD panel shipment growth is expected to continue in 2019. The preliminary forecast for unit shipments of three major products indicates that panel makers will continue to focus on the monitor and notebook PC panel businesses, increasing shipments by 5.3 percent and 6.6 percent, respectively, over the year, while shipments of TV panels are forecast to grow just 2.6 percent.

In 2019, three new 10.5-generation fabs – ChinaStar’s T6, BOE’s second fab and Foxconn/Sharp’s Guangzhou line – are expected to start mass production. All of them are assigned to manufacture TV panels, further boosting TV panel supply. “As the TV panel business is predicted to remain tough, panel makers, who enjoyed relatively better outcomes with monitor and notebook PC panels in 2018, will likely focus on the IT panel businesses,” Wu said.

IHS Markit provides information about the entire range of large display panels shipped worldwide and regionally, including monthly and quarterly revenues and shipments by display area, application, size and aspect ratio for each supplier.

IHS Markit (Nasdaq: INFO) is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers next-generation information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 business and government customers, including 80 percent of the Fortune Global 500 and the world’s leading financial institutions.

The Liquid Crystal Display (LCD)-enabled electronic devices, such as television, mobile phones and others, is creating potential opportunities for the LCD panel market. In the past couple of years, LCD panels have gained popularity owing to their advanced properties that include less power consumption, compact size and low price.

Moreover, over the past two decades, the LCD technology of has made impressive progress. The electronic displays available at present make use of a wide variety of active LCD panels. The LCD panel market is one of the significantly growing markets due to the increasing demand for LCD displays & low power consumption electronic goods, as well as increase in the demand for touch-enabled displays.

An LCD panel is designed to project on-screen information. At present, LCD panels are suited with high-mobility electronic equipment. LCDs with improved video quality are gaining momentum in all developed and developing economies. These factors are projected to propel the global LCD panel market.

The major growth drivers of the LCD panel market include an increase in the demand for energy-efficient electronic products as well as for larger and 4K televisions. Furthermore, growth in the demand for energy-efficient electronic devices is surging the global LCD panel market.

Demand for high-quality screens, coupled with improving standards of living and inflating disposable income, are among key factors boosting the LCD Panel market. In addition, increase in the adoption of consumer electronic devices is projected to drive the global LCD panel market.

However, one of the major challenges of the LCD panel market are the higher cost and thickness of the display of these devices as compared to other modules. The LCD panel market is expected to witness sluggish and unpredictable growth owing to a quantitative decline in the number of LCD displays.

Moreover, financial uncertainty and macroeconomic situations around the world, such as fluctuating currency exchange rates and economic difficulties, are some of the major factors hindering the growth of the LCD panel market. However, increased competition from alternative technologies and LCD panel complex structure is likely to limit the growth of the LCD panel market.

At present, North America holds the largest market share for the LCD panel market due an increase in the demand for consumer electronic devices. Due to the presence of key LCD panel manufacturers in China and Japan, Asia Pacific is expected to become the prominent region for the LCD panel market.

In addition, the unorganized market of LCD panels in China, Japan and India is creating a competitive environment for global LCD panel manufacturers. Moreover, Europe is the fastest-growing market for LCD panels due to an increase in the adoption of consumer electronics devices. The demand for LCD panels has risen dramatically over the past 12 months globally. The usage of LCD displays in various industries in these regions is boosting the LCD panel market.

The report is a compilation of first-hand information, qualitative and quantitative assessment by industry analysts, inputs from industry experts and industry participants across the value chain. The report provides in-depth analysis of parent market trends, macro-economic indicators and governing factors along with market attractiveness as per segments. The report also maps the qualitative impact of various market factors on market segments and geographies.

Due to an increase in the demand for large LCD displays, the large size LCD panel sub-segment is expected to register double-digit growth rate in the global market. In addition, due to an increase in the demand for portable electronic devices, the small size LCD panel sub-segment is projected to be the most attractive market sub-segment of the global LCD panel market.

The smart phones and tablets sub-segment held the largest market share for the LDC panel market in 2017, and the wearable devices sub-segment is expected to grow with a high CAGR during the forecast period.

This report focuses on global and United States LCD Display market, also covers the segmentation data of other regions in regional level and county level.

Due to the COVID-19 pandemic, the global LCD Display market size is estimated to be worth USD million in 2023 and is forecast to a readjusted size of USD million by 2028 with a CAGR of % during the review period. Fully considering the economic change by this health crisis, by Type, Static accounting for % of the LCD Display global market in 2021, is projected to value USD million by 2028, growing at a revised % CAGR in the post-COVID-19 period. While by Application, Mobile Phone was the leading segment, accounting for over percent market share in 2021, and altered to an % CAGR throughout this forecast period.

In United States the LCD Display market size is expected to grow from USD million in 2021 to USD million by 2028, at a CAGR of % during the forecast period.

LCD Display market is segmented by region (country), players, by Type and by Application. Players, stakeholders, and other participants in the global LCD Display market will be able to gain the upper hand as they use the report as a powerful resource. The segmental analysis focuses on revenue and forecast by region (country), by Type and by Application for the period 2017-2028.

For United States market, this report focuses on the LCD Display market size by players, by Type and by Application, for the period 2017-2028. The key players include the global and local players, which play important roles in United States.

Which are the prominent LCD Display Market players across the Globe? ● Along with this survey you also get their Product Information Types (Static, Simple Matrix, Active Matrix), Applications (Mobile Phone, Computer, TV), and Specification. Detailed profiles of the Top major players in the industry:LG Display, Samsung, InnoLux, AUO, BOE, TCL, Sharp, Japan Display, Panasonic

● LCD Display Market research contains an in-depth analysis of report complete data on factors influencing demand, growth, opportunities, challenges, and restraints, and Analysis of Pre and Post COVID-19 Market.

What Overview LCD Display Market Says? ● This Overview Includes Diligent Analysis of Scope, Types, Application, Sales by region, types and applications.

LCD Display Market Manufacturing Cost Analysis ● This Analysis is done by considering prime elements like Key RAW Materials, Price Trends, Market Concentration Rate of Raw Materials, Proportion of Raw Materials and Labour Cost in Manufacturing Cost Structure.

The Global LCD Display market is expected to rise at a considerable rate during the forecast period, between 2023 and LCD Display. In 2021, the market is rising at a steady rate and with the expanding adoption of strategies by key players, the market is expected to rise over the projected horizon.

Moreover, it helps new businesses perform a positive assessment of their business plans because it covers a range of topics market participants must be aware of to remain competitive.

LCD Display Market Report identifies various key players in the market and sheds light on their strategies and collaborations to combat competition. The comprehensive report provides a two-dimensional picture of the market. By knowing the global revenue of manufacturers, the global price of manufacturers, and the production by manufacturers during the forecast period of 2023 to LCD Display, the reader can identify the footprints of manufacturers in the LCD Display industry.

As well as providing an overview of successful marketing strategies, market contributions, and recent developments of leading companies, the report also offers a dashboard overview of leading companies" past and present performance. Several methodologies and analyses are used in the research report to provide in-depth and accurate information about the LCD Display Market.

The current market dossier provides market growth potential, opportunities, drivers, industry-specific challenges and risks market share along with the growth rate of the global LCD Display market. The report also covers monetary and exchange fluctuations, import-export trade, and global market

status in a smooth-tongued pattern. The SWOT analysis, compiled by industry experts, Industry Concentration Ratio and the latest developments for the global LCD Display market share are covered in a statistical way in the form of tables and figures including graphs and charts for easy understanding.

Research report world follows a primary and secondary methodology that involves data based on top-down, bottom-up approaches, and validation of the estimated numbers through research. The information used to estimate market size, share, and forecast of various segments-sub segments at the global, country level, regional level is derived from the unique sources and the right stakeholders.

LCD Display Market Growth rate or CAGR exhibited by a market certain forecast period is calculate on the basic types, application, company profile and their impact on the market. Secondary Research Information is collected from a number of publicly available as well as paid databases. Public sources involve publications by different associations and governments, annual reports and statements of companies, white papers and research publications by recognized industry experts and renowned academia, etc. Paid data sources include third-party authentic industry databases.

On the basis of the end users/applicationsthis report focuses on the status and outlook for major applications/end users, consumption (sales), market share and growth rate for each application, including:

Geographically, this report is segmented into several key regions, with sales, revenue, market share and growth Rate of LCD Display in these regions, from 2015 to 2028, covering ● North America (United States, Canada and Mexico)

This LCD Display Market Research/Analysis Report give Answers to following Questions: ● How Porter"s Five Forces model helps you to study LCD Display Market?

● Which Manufacturing Technology is used for LCD Display? What Developments Are Going On in That Technology? Which Trends Are Causing These Developments?

Our research analysts will help you to get customized details for your report, which can be modified in terms of a specific region, application or any statistical details. In addition, we are always willing to comply with the study, which triangulated with your own data to make the market research more comprehensive in your perspective.

With tables and figures helping analyse worldwide Global LCD Display market trends, this research provides key statistics on the state of the industry and is a valuable source of guidance and direction for companies and individuals interested in the market.

Is there a problem with this press release? Contact the source provider Comtex at editorial@comtex.com. You can also contact MarketWatch Customer Service via our Customer Center.

1.1. THE POLICY COVERS THE HANDLING OF THE PRIVATE INFORMATION EACH USER SHARES WITH TRENDFORCE WHILE VISITING OUR WEBSITES. IF A DIFFERENT PRIVATE POLICY HAS BEEN REFERED TO FOR SPECIFIC TRENDFORCE WEBSITES AND SERVICES, THAT POLICY WILL REPLACE OR SUPPLEMENT THE PRIVACY POLICY MENTIONED IN THIS DOCUMENT. THIS POLICY ALSO COVERS INDIVIDUALS LEGALLY RESIDING IN OR ORGANIZATIONS LEGALLY BASED IN MEMBER COUNTRIES OF THE EUROPEAN UNION (EU) AND ARE SUBJECTED TO EU GENERAL DATA PROTECTION REGULATION (GDPR) WITH REGARD TO PROVISION OF SERVICES AND PERSONAL DATA PROTECTION.

2.1 THE WEBSITE WILL COLLECT AND USE USER INFORMATION FOR PURPOSES SUCH AS MARKETING, CONSUMER PROTECTION, CONSUMER/CLIENT MANAGEMENT, E-COMMERCE SERVICES, FINANCIAL ACCOUNTING, CONTRACTUAL MATTERS, RESEARCH ANALYSIS, AND DATA PROCESSING. WHEN REQUIRED BY LAW, THE WEBSITE MAY ALSO PROVIDE PERSONAL INFORMATION TO NON-GOVERNMENT AGENCIES.

THE WEBSITE WILL NOT DISCLOSE OR SHARE ANY PERSONAL INFORMATION EXCPET PER SPECIAL REQUEST OR WHEN PERMISSION IS RECEIVED FROM THE USER. OTHER EXCEPTIONS INCLUDE:

IN ACCORDANCE WITH ARTICLE 3 OF THE PERSONAL INFORMATION PROTECTION LAW, YOU WILL HAVE THE OPTION TO EXERCISE THE FOLLOWING RIGHTS WITH REGARD TO THE PERSONAL INFORMATION SHARED WITH THE WEBSITE:

a. TO PREVENT UNAUTHORIZED PARTIES FROM ACCESSING, MODIFYING, OR LEAKING PERSONAL USER DATA, THE WEBSITE WILL TAKE STEPS TO IMPLEMENT PROPER SAFETY MEASURES. THE DATA SEARCHED AND RECORDED ON THE WEBSITE AND THE APPROPRIATE SAFETY MEASURES CHOSEN WILL ALL BE REVIEWED CAREFULLY. CONSIDERING HOW THE SAFETY OF TRANSMITTING DATA ON THE INTERNET CAN NEVER BE GUARANTEED COMPLETELY, USERS SHOULD KEEP IN MIND ALL POSSIBLE RISKS ASSOCIATED WITH ONLINE DATA TRANSFERS AND TAKE RESPONSIBILITY FOR ANY INFORMATION SHARED WITH OR OBTAINED FROM THE WEBSITE.

BE SURE TO PROTECT ALL PASSWORDS AND PERSONAL INFORMATION, REFRAIN FROM DISCLOSING PRIVATE USER INFORMATION TO ANY THIRD PARTY, AND REGISTER WITH THE WEBSITE UPON COMPLETING ALL NECESSARY MEMBERSHIP PROCEDURES. WHEN USING A SHARED OR PUBLIC COMPUTER, PLEASE MAKE SURE TO PROPERLY CLOSE ALL RELEVANT BROWSERS TO PREVENT OTHERS FROM READING YOUR PERSONAL E-MAILS OR INFORMATION.

The global military displays market size reached USD 1.23 Billion in 2020 and is expected to register a revenue CAGR of 5.6% during the forecast period. Increasing integration of new technologies with military displays, increasing need for more advanced systems in military displays for improving military activities, and increase in defense spending in countries across the globe are some key factors projected to continue to drive global military displays market revenue growth between 2021 and 2028. Rising demand for military displays in aerospace & defense sectors is also contributing to revenue growth of the market.

Military users require displays that are inexpensive yet tough enough to withstand various climatic and weather conditions and wrench-drop and boot-kicks. Such displays have to be more than physically rugged, displays must meet advanced military standards and to act as a shield against electromagnetic radiation, safeguard against surges on power supply lines, manage thermal emissions, and offer good power efficiency. Availability of the latest technologies enable production of displays that offer high performance in a range of circumstances and situations. Increasing focus on modernization of forces and on replacement of existing traditional soldier protection and situational awareness systems. Increase in demand for technologically advanced systems to counter special threats such as terrorism that cannot be met by conventional warfighting forces, and advanced systems to detect threats to a country by enhancing intelligence capabilities are expected to boost market revenue growth.

However, concerns regarding SWaP-C (stringent size requirements, weight, power, and cost) of military displays and decreasing availability of logistics are some factors expected to hamper global military displays market revenue growth over the forecast period. Military displays are built to survive in any tough environment. Military display designers face a major challenge when it comes to cost, quality, and latency. Managing the tradeoffs for cost versus power versus ruggedness of military displays are expected to hamper market growth.

On the basis of product type, the global military displays market is segmented into handheld, wearables, vehicle mounted, simulators, and computer displays. Vehicle mounted segment is expected to lead in terms of revenue contribution to the global military displays market during the forecast period. Increasing usage of vehicle mounted displays in military vehicles for surveillance and to track the location of potential enemies and vehicles are major factors driving revenue growth of this segment. In addition, rising demand for rugged vehicle mounted military displays from armed forces is expected to boost revenue growth of this segment. Military can use rugged vehicle mounted displays to have a more focused targeting approach, among others.

On the basis of type, the global military displays market is segmented into smart displays and conventional displays. Smart displays segment is expected to lead in terms of revenue contribution during the forecast period due to increasing demand for smart displays. Smart displays are advantageous owing to various benefits such as size and resolution as commands from the control room should be highly visible. Smart displays are used in military owing to lightweight and flexibility as these displays are designed to function outdoors. As a result, rising demand for smart displays is expected to augment revenue growth of this segment going ahead.

On the basis of technology, the global military displays market is segmented into Light Emitting Diode (LED), Light Emitting Diode (LED), Liquid Crystal Display (LCD), Active Matrix Organic Light Emitting Diode (AMOLED), and Organic Light Emitting Diode (OLED). LCD segment is expected to lead in terms of revenue contribution to the global military displays market during the forecast period. Military has started using LCD displays as it is lower cost as compared to all other forms of displays and also sustain in tough conditions.

On the basis of computer displays, the global military displays market is segmented into microdisplays, small & medium-sized panels, and large panels. Small & medium-sized panels segment is expected to lead in terms of revenue contribution to the global military displays market during the forecast period. Small & medium-sized panels are designed to provide a clear surveillance view in order to maintain robust defense capability and help in tracking and precise location of targets. Growth of this segment is attributed to rising need for improved visibility of targets.

On the basis of end-use, the global military displays market is segmented into naval, airborne, and land. Naval segment is expected to lead in terms of revenue contribution to the market over the forecast period. Military displays are designed to work as surveillance systems and help in launching weapons to targets. These act as situational awareness systems in emergency situations and connects to the command room or center to enable deployment of better strategy for a war fight. Different types of displays can be combined to offer better video feeds from an external sensor. Therefore, military displays assist in the improvement of a country’s security. Increasing adoption of military displays in naval applications owing to high efficiency is expected to drive revenue growth of this segment over the forecast period.

North America is expected to account for larger revenue share among other regional markets during the forecast period. Significantly large revenue share is primarily attributable to growing usage of technologically advanced systems. Additionally, increasing demand for military displays across countries such as the U.S., Canada, and Mexico for better strategizing is expected to continue to boost North America market revenue growth.

Europe is expected to register a significantly rapid revenue growth rate during the forecast period. Rising demand for military displays from naval uses in counties such as Germany, France, the U.K, Italy, and Spain is expected to boost revenue growth of the Europe market.

The global military displays market is fairly fragmented, with a number of large and medium-sized market players accounting for majority market revenue. Key players are deploying various strategies, entering into mergers & acquisitions, strategic agreements & contracts, developing, testing, and introducing more effective military displays. Some major companies included in the military displays market report are:

This report offers historical data and forecasts revenue growth at a global, regional, and country level, and provides analysis of the market trends in each segment from 2018 to 2028.

For the purpose of this report, Emergen Research has segmented global military displays market on the basis of product type, type, technology, computer displays, end-use and region:

SHANGHAI, Feb 6 (Reuters) - Samsung Electronics Co. Ltd., the world"s top LCD maker, plans to double the output of its liquid crystal display module plant in eastern China"s Suzhou city to meet growing demand, industry sources said on Tuesday.

The South Korean company has already started on the project, which currently assembles around 1 million LCD units per month to be used in flat screen TVs and PC monitors, said the sources, who are familiar with the plan.

Foreign and domestic companies are racing to expand LCD production in China, with demand expected to increase rapidly for notebook computers and flat screen TVs.

Last month, Japan"s Nitto Denko Corp.said it would spend about $165 million to build a new factory in China to make LCD panels to meet demand for flat screen TVs.

Local players are adding to the competition. TCL Corp., a major Chinese electronic appliance maker, is in talks with partners for a possible LCD plant in the booming southern town of Shenzhen near Hong Kong, industry sources said.

Samsung manufactures the LCD screens themselves only in South Korea, but runs overseas plants to assemble the screens and other parts to make LCD modules for televisions and other display units.

“So, the expansion is necessary for Samsung at the current stage, otherwise its rivals will catch up,” the source said, adding that Samsung now controls 20-30 percent of domestic market share for its sales of PC monitors.

The electronics giant aims to boost the market share for its PC monitor sales to 50 percent in China after the plant expansion is finished, said the source, who did not want to be identified.

Samsung is trying to consolidate its position as the world"s biggest LCD maker amid fierce market competition from rivals including LG.Philips LCD Co. Ltd.and Taiwan"s AU Optronics Corp..

Global demand for LCD TVs is expected to grow 56 percent to 69.7 million units in 2007, and a further 35 percent to 93.8 million units in 2008, according to DisplaySearch.

Samsung’s latest plan to expand its Suzhou LCD plant could be just the beginning of a new round of investment in China by the company, the sources said.

Samsung has another LCD module factory in the northern city of Tianjin, near Beijing. The sources said Samsung was also considering increasing its investment in the Tianjin plant.

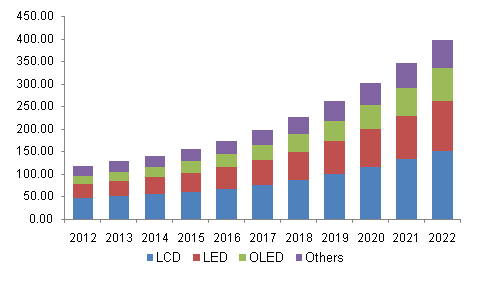

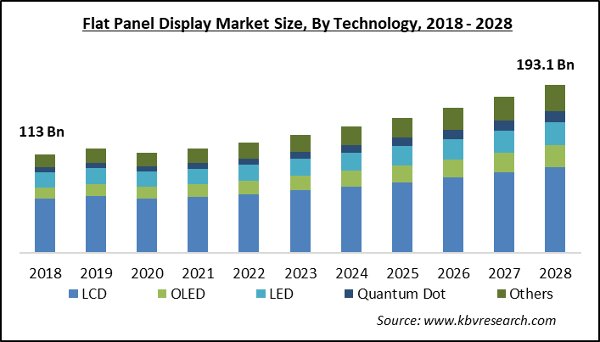

According to a recent report published by Allied Market Research, titled, "Global Flat Panel Display Market by Technology, Application, and Industry Vertical: Global Opportunity Analysis and Industry Forecast, 2019-2026," the global flat panel display market size was valued at $116.80 billion in 2018, and is projected to reach $189.60 billion by 2026, growing at a CAGR of 6.10% from 2019 to 2026.

Flat panel display is a successor of Cathode Ray Tube (CRT) display that includes Liquid Crystal Display (LCD) or Light-Emitting Diode (LED) screens, which makes them much lighter and thinner than other displays. These displays are used for advertisements, educational purposes, and in the corporate sector. These display screens utilize numerous technologies such as Light-Emitting Diode (LED), Liquid Crystal Display (LCD), Organic Light-Emitting Diode (OLED), and other technologies. In addition, the display technologies such as organic light-emitting diode (OLED) have gained increased importance in products such as televisions, smart wearables, smartphones, and other devices.

A smartphone and tablet are handheld personal computers with a mobile operating system. These devices are enabled with a LED or OLED touchscreen display with a graphical user interface, processor, and a rechargeable battery in a single thin flat structure. The flat panel display specially used in small devices including mobile phones, smartphone, digital cameras, laptops, and pocket video cameras. These devices run a variety of software. Smartphones are pocket-sized as opposed to tablets.

Region-wise, the flat panel display industry trends are analyzed across North America Europe, Asia-Pacific, and LAMEA. In 2018, in terms of revenue, North America accounted for 38.7% of the total flat panel display market revenue and is expected to retain its dominant position. However, the Asia-Pacific region is expected to grow at the highest CAGR, owing to advancements in display technologies and rise in purchasing capacity of people.

High demand for vehicle display technology in the automotive sector, increase in demand for OLED display devices in smartphones and tablets, and rise in adoption of interactive touch-based devices in the education sector drive the growth of the market. In addition, high adoption of flexible flat panel display is anticipated to provide potential growth opportunities for the market. However, high cost of new display technologies and stagnant growth of desktop PCs, notebooks, and tablets is expected to restrain the flat panel display market growth.

Moreover, the display technology such as OLED has various advantages over conventional display technologies such as being light in weight and its flexibility, which have enabled it to gain competitive advantage over other segments. The OLED technology is recognized as a lighter and thinner alternative than conventional LED and LCD systems. In addition, OLED panels do not require any type of backlighting compared to LCD. A stable performance in sunlight is an additional advantage of OLEDs.

In August 2019, Sharp Corporation launched Sharp 8M-B80AX1U 80" Class 8K Ultra HD LCD display. This display offers ultimate high definition, conforming to the 8K Ultra HD standards and pixel resolution 16 times greater than Full HD and four times greater than 4K.

According to Ankit Prajapati, Lead Analyst, Semiconductor & Electronics at Allied Market Research, “In 2018, the LCD segment dominated the flat panel display market in the technology category, in terms of revenue. However, the Quantum Dot (QD) segment is expected to grow at the highest CAGR during the forecast period. By application, the smartphone & tablet segment is anticipated to dominate the market throughout the forecast period (2019–2026). Moreover, the healthcare segment dominates the overall flat panel display market, in terms of industry vertical. The flat panel display market signifies a promising future for the technological industry. The companies are adopting innovative techniques to provide customers with advanced and innovated product offerings.”

Key Finding of The Flat Panel Display Market:By technology, the LCD segment led the flat panel display market share in 2018. However, the Quantum Dot (QD) segment is anticipated to grow at the highest CAGR during the forecast period (2019–2026).

By industry vertical, the healthcare segment dominated the flat panel display market in 2018. However, the automotive segment is expected to grow at the highest CAGR during the forecast period (2019–2026).

The key players operating in the flat panel display industry include G Display Co., Ltd., NEC Corporation, Sharp Corporation, Samsung Electronics Co. Ltd, AU Optronics Corp., Sony Corporation, Panasonic Corporation, Japan Display Inc., Crystal Display Systems Ltd, and E ink Holdings Inc.

TPV Technology Limited (informally TPV, Chinese: 冠捷科技) is a Fortune China 500 multinational electronics manufacturing company headquartered in Kwun Tong, Hong Kong, and incorporated in Bermuda.computer monitors with a 33% market share.CRT and TFT LCD monitors as well as LCD TVs for distribution globally.AOC, Envision, and Philips for some products (TPV obtained the brand name of Philips from Koninklijke Philips N.V.). It is also an original design manufacturer for other companies.

In June 2009 MMD (Multimedia Displays) as a wholly owned company of TPV was established through a brand license agreement with Philips, and its role is to exclusively market and sell Philips branded LCD monitors and displays worldwide. Three categories of Philips product lines are included under the agreement: the Business and Consumer Range of LCD monitors, Public Signage and Hotel/Hospitality TV.

"TPV Technology Limited Annual Report 2017 – Notes to the Consolidated Financial Statements" (PDF). TPV-Tech.com. TPV Technology Limited. April 2018. p. 81 (PDF p. 83). Retrieved 4 November 2018.

"Dr Jason Hsuan Executive Director of TPV Technology | The CEO Magazine". TheCEOMagazine.com. Australia: The CEO Magazine. 19 April 2017. Retrieved 4 November 2018.

Sayer, Peter (20 June 2005). "Philips deal makes TPV world"s biggest monitor maker". www.arnnet.com.au. IDG Communications. Retrieved 4 November 2018.

The global touch screen display market size was valued at USD 59.57 billion in 2021. The market is projected to grow from USD 66.91 billion in 2022 to USD 166.12 billion by 2029, exhibiting a CAGR of 13.9% during the forecast period. Based on our analysis, the global market exhibited an average growth of 9.3% in 2020 as compared to 2019.

In addition, capacitive touch screens, unlike resistive touch screens, do not rely on finger pressure to function. These, on the other hand, operate with everything that has an electrical charge, which includes human skin. Capacitive touch screens do not operate with most gloves as they are electrically insulating and rely on electrical interference from a conductive source. Furthermore, the technology has been so popular in consumer gadgets and now in commercial/industrial applications. Inanimate items hitting the screen can impact resistive touch screens, which need more pressure than capacitive touch screens. Therefore, the rise in projected capacitive touch screens is further contributing toward the touch screen display market growth.

Human interaction with voice, gesture, or direct touch, with the choice to switch between them occurs naturally and seamlessly. Nowadays, people rely on direct touch only by pressing the button on the keyboard or swiping the screen; however, now these touchless systems allow the consumer to communicate with a computer by using voice or gesture, which is expected to hamper the market in future.

In addition, touch screen technology, in some way, has decreased human interaction; now, the current voice recognition technology has made it easier along with the current pandemic situation encouraging people for less human interaction, further limiting the market growth.

Based on screen type, the market is divided into resistive touch screens, capacitive touch screens, infrared touch screens, optical, and others (surface acoustic wave type displays).

Infrared touch screens are experiencing a strong upsurge in the display market. They use light-beam interruption, generally referred to as beam break, to determine the position of touch events. ATMs, industrial automation, plant control systems, ticketing machines, medical equipment, kiosks, POS, interactive whiteboards, various large-size applications, and office automation employ infrared touch displays.

Also, the optical segment is showing dynamic growth in the market. It is due to its working model as two or more image sensors are positioned around the screen"s edges (usually the corners) in this type of touch screen, a relatively new advancement in touch screen technology. Due to its scalability, adaptability, and affordability for bigger touch screens, this technology is gaining appeal.

Furthermore, the kiosks segment is anticipated to depict progressive growth during the touch screen display market forecast period. The growth is attributed to enhanced shopping experience for customers. The growing demand for self-service in banking & financial services along with improved applications over services & innovations in display technology is enhancing the market growth.

In addition, the display/digital signage segment is expected to have a significant rise in the coming years. This is owing to lower display costs & increased consumer experiences. Additionally, the rise of government entities, as well as the rapidly expanding educational industry, is further aiding the market growth.

Whereas, the commercial segment is projected to experience major growth during the forecast period. The commercial use of PCAP touch panels in outdoor public places must withstand the elements while heavy traffic regions will put PCAP touchscreen durability to the test. In addition, kiosks, POS machines, payment systems, voting machines, ATMs, interactive digital signage, electronic billboards, and other public commercial systems are further enhancing the commercial market.

Asia Pacific is predicted to develop at a progressive rate during the forecast period. In the market, the smart wearables industry is being driven by the region"s developing electronics sector as well as a substantial development in disposable income. The touch screen display industry in China has taken on a new shape, fueled in part by the purchases of more affluent customers. One of the primary factors contributing toward the growth is the rise in smartphone and tablet adoption.

Furthermore, China is witnessing phenomenal growth in this industry. The country is a manufacturing hub for these kinds of displays. The supplying of components and subcomponents is the major factor driving the market. One of the important trends driving sales in the market is the increasing usage of optical touchscreens in the hospitality industry and brand advertising in the country. End-use industry demands, particularly in capacitive touch and sensor technologies, have accelerated the speed of technical breakthroughs, further increasing the touch screen display market share globally.

In North America, this market is expected to witness progressive growth during the forecast period. It is attributed to the availability of raw materials & high smartphone adoption rate. Furthermore, the adoption of infrared touchscreen display & gesture sensing might also deliver revenues for market growth. Additionally, its comprehensive application in the television, DVD, and automobile sectors is also expected to surge the demand, which will further propel the market share globally.

Additionally, the Europe region is anticipated to have significant growth in the foreseeable future owing to the high-end demand in professional applications such as education and government. In addition, owing to the rise in penetration rates of urbanization, the demand for advanced featured products with the capability to aid consumers’ daily requirements, such as time schedules, is further driving the market in the region.

Moreover, the Middle East & Africa region is witnessing a steady growth in the market. Major manufacturers are slowly establishing their businesses due to growing opportunities in the region.

South America is projected to grow moderately compared to other regions, owing to less presence of the market players in the region. However, it has been projected that the region will witness steady growth in the forecast period, owing to the growing demand for smartphones and digitalization.

The market is fragmented with a significant number of key players compared to other markets in optoelectronics solutions. These major players are constantly developing their product segments and expanding their businesses. For instance, BOE Technology offers some of its flagship products, such as interactive whiteboard displays with 65” enabled with multi-touch technology, a built-in conferencing system with a slim and clean design.

The research report provides a detailed analysis of the type, application, and industries. It provides information about leading companies and their business overview, types, and leading applications of the product. Besides, it offers insights into the competitive landscape, SWOT analysis, and current market trends and highlights key drivers and restraints. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the market"s growth in recent years.

Westford,USA, Oct. 19, 2022 (GLOBE NEWSWIRE) -- The primary factors driving the growth of the Display Market are increasing demand from smartphone and tablet manufacturers, rising expenditure on smart Infra-Red (IR) sensors, and rapid expansion of digital media content. Smartphones are becoming more sophisticated and are using larger screens that require higher resolutions for better user experience. Tablets are also becoming increasingly popular as they offer a single device that can serve as both a computer and a mobile phone. This increase in demand for high-resolution displays is expected to drive the adoption of LED displays in the coming years.

Manufacturers in the global display market are starting to see the potential in displays as an important part of their product lines. Device manufacturers are looking for displays that can be used on a variety of devices, from laptops to smartphones and even cars. In addition, developers are creating more applications that require high-quality displays.

One key challenge facing manufacturers is making sure that their displays meet the requirements of multiple market segments. They need to make sure that their displays are suitable for usage on tablets as well as laptops, yet they also need to create displays that look good on smaller devices like smartphones and digital assistants.

The growth in demand for display market across various verticals such as healthcare, retail, automotive, appliance and others has led to an increasing demand for large sizes screens which can be cost effective owing to their mass production capabilities. Display manufacturers are also exploring new technologies such as flexible displays that can be rolled up like a traditional newspaper

Our report considers several factors such as market size estimation techniques, product segmentation analysis, expenditure Breakdown by Country and region; Porter"s Five Forces Analysis; and price trends analysis to give you a comprehensive view of the global display market.

Some of the key players in the global display market include LG Display Co., Ltd., Samsung Electronics Co., Ltd., and Sharp Corporation. These companies are focused on developing innovative products that meet the needs of various consumers in the marketplace. They also strive to improve their competitiveness by expanding their product lines into new markets and by creating partnerships with other companies to share technology and manufacturing resources.

Among global display market leaders, Samsung is presently dominating the industry with a share of 38% of the market. However, Apple is looming large as one of the largest competitors in smartphone sector. Other prominent players in this segment include LG Display, Sony Corp, and Toshiba Corporation. Among these companies, LG Display has been fastest expanding its business over recent years owing to its focus on emerging markets such as China and India.

For one, it"s heavily invested in research and development in the display market. According to analysts at SkyQuest, Samsung spends more than $13.7 billion a year on R&D, more than any other company in the world. That investment has paid off: The company"s displays are consistently among the best on the market.

Samsung also makes good use of its deep pockets. The company has poured money into forming joint ventures with major chipmakers like Qualcomm and Intel, which allows it to quickly bring new technologies to market. It doesn"t just rely on partnerships; Samsung also invests in its own technology centers, such as the foundry that produces screens for its smartphones.

One important technology that Samsung is investing in is AMOLED and QLED screens. QLEDs are generally considered to be more environmentally friendly than LCDs, since they use less power and create fewer byproducts.

The main drivers for Samsung"s strong performance in the display market are its diversification across product lines, continuous innovation across product categories, and excellent execution capabilities. The company has been able to expand into new markets such as automotive displays and smart watches, while continuing to focus on profitable core products.

Samsung has also been successful in pushing down prices for OLED displays over the past few years. This has made OLED panels more accessible to a wider range of customers, supporting growth at rival companies such as LG Electronics and Sony.

In recent years, there has been a shift in display technology as manufacturers across the global display market experiment with new and more innovative ways to create displays. The trend observed by SkyQuest worldwide is that display technologies are moving towards OLEDs and quantum dots, both of which have a number of advantages.

Quantum dots or QLED offer many advantages over traditional LCDs in the display market, such as better color reproduction, enhanced viewing angles, better response time, and lower power consumption. Their small size also makes them ideal for applications where sliding or tilting LCD panels are not possible or desirable. Quantum dot displays have already begun appearing in consumer electronics and will eventually replace traditional LCDs as the predominant type of display in devices like smartphones and tablets.

SkyQuest Technology is leading growth consulting firm providing market intelligence, commercialization and technology services. It has 450+ happy clients globally.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey