lcd panel shortage supplier

We wanted to give you a quick update on the global component shortage that is affecting displays and other products in this rapidly changing scenario and the issues we are all facing.

CDS is working very closely with our manufacturing partners and factories, who are putting in a huge amount of effort to try to secure TFT panels, interface boards, touchscreens, panel PC and the driver ICs needed for all those products to keep shipping schedules on time and reduce any delays that may become evident. Now there are constant negotiations and bartering to get the best allocation of product that we possibly can, and our factories are doing their best to secure all the stock they and we require.

The lockdowns brought on by this crisis had caused many manufacturers to temporarily shut down. With the increasing amount of products incorporating LCDs and many productions lines down, it has become more difficult to meet

and has spent much of the past year ramping production on LCDs to keep up with overwhelming demand from consumer and industrial buyers. This is being done

amidst a global supply shortage due to legislation and viral spread from the pandemic hitting manufacturing centers. In addition, the shift to working

Global monitor panel shipments declined in the first quarter of the year, a report showed on Wednesday, mainly due to Samsung Displays exit from the monitor LCD display manufacturing business and a shortage of semiconductors.

The worldwide monitor panel shipments fell 8.6 percent on-quarter to 39.9 million units in the January-March period, according to the latest report from market researcher TrendForce.

"TrendForce indicates that SDC will exit the monitor LCD panel manufacturing business after it reaches its shipment target of 1.2 million panels in 1H21," it said. "This figure represents a staggering 93.8 percent decline compared to the 19.3 million units of LCD panels that SDC shipped throughout last year."

Samsung Display, the world"s top mobile display panel maker, has been focusing on its migration to next-generation quantum-dot (QD) displays, while withdrawing from the LCD business, reports Yonhap news agency.

But for large LCD panels for TVs, the company recently said it is mulling extending its manufacturing for one more year due to soaring demand from TV makers and rising panel prices.

TrendForce said the global monitor panel market also suffered a setback in the first quarter due to a shortage of components, such as integrated circuits and timing controllers.

"In addition, since TV and notebook (laptop) panels have higher profit margins compared to monitor panels, panel suppliers generally allocate less of their production capacities for manufacturing monitor panels relative to other products," it said.

"TrendForce believes that panel suppliers will likely in turn allocate more production capacities to clients in the monitor segment in 4Q21," it said.

"More specifically, the current shortage of components in the upstream supply chain, which has been exerting significant downward pressure on monitor panel shipments, will be gradually alleviated in 2H21."

Based on Omdia’s Large Area Display Price Tracker, April 2021, Sanju Khatri, director of consulting for displays, ProAV and consumer devices at research and consultancy firm Omdia, provided some analysis on disruption in the display supply chain due to component shortage and high demand. Impact will be mostly felt on LCD technology, as strong demand and component shortage will lead to the following price cycles for LCD panels.

EDITOR’S NOTE: Three distinct terms are used below. Components (display driver IC, glass, and polarizer); panel (raw LCD panels) and brands/finished sets/device vendors (TV, monitor/laptops/ProAV vendors).

Strong consumer demand for TVs/IT displays. The “at home” trends are including work at home, learn at home, entertain at home and shop at home. The LCD TV, Notebook, LCD monitor, and tablet PC products continue to have the strong demand thanks to the “at home” trends.

Display panel makers are increasing prices sharply to take the fast turnaround on profitability. The LCD TV open cell prices have been increasing by 40%-50% from June 2020 to December 2020. And it is expected there will be another 20% increase from January 2021 to May 2021.

Component shortage(Glass substrate, Display Driver IC, T-con, PMIC, Polarizer films) are frustrating the supply chain from time to time, making the set makers to be more nervous thus giving more orders. Three display components are especially tight in 2021, represented by “P.I.G.”

P: Polarizer, protective/release films and surface treatment capacity are in tightness due to the production bottleneck and the retreat of the makers. However, the polarizer shortage is viewed as a short term as the long-term polarizer supply is sufficient.

I: IC, Display Driver IC supply is expected to loosen from 2H21however, limited foundry capacity and allocation competition with other IC applications may continue to complicate display panel shipments into the future. Even with the incremental display driver IC wafer foundry in the second half of 2021 (2H21), it is possible the wafer capacity allocation will be shifting to other IC applications.

G: Glass substrate is in tightness due to the unexpected accidents happened in the suppliers from 4Q20 to 1Q21. The glass substrate shortage is viewed as a short term but especially serious within these couple of months due to some accidents that happened in NEG and AGC. The recovery schedule is expected to take 6 months in Omdia’s estimation. In April 2021, there were also some yield rate challenges in glass tanks in Korea, which caused the short-term tightness in 2Q21.

The start of a new year is normally a busy time for computer manufacturers and technology companies, and 2021 has proven no different. What has proven different this year is the availability of some crucial supplies. with the COVID-19 pandemic in full swing, people have made a major shift to working at home. This shift has had a severe impact on computer and component manufacturers worldwide. The workforce has spent much of the past year buying new LCD monitors and laptops while investing in various work-from-home solutions to make it a little easier to keep things running even when they can’t make it to the office.

Outside of business concerns, the demand for leisure devices has also increased. People who cannot go out and socialize are instead purchasing gaming systems, PCs, and TVs, while parents are buying their children tablets and notebooks as entertainment. The pandemic has created an increase in demand and industry-wide shortages of both display panels and power management IC components, including phones. The shortage isn’t just due to the pandemic, of course. Many component manufacturers were already seeing an increase in demand generated by the rollout of 5G technology and the release of two new major game consoles. That the pandemic just happened to hit during a time of significant technological change simply increased existing demand that much more. This sudden demand for all of the components parts in display screens, computers, and TVs brought about a unique situation. Not only is it unnecessary for component manufacturers to market to clients this year, but many are also having to actively turn business away or schedule it for months down the line.

For manufacturers higher up in the supply chain, this is good news. TSMC’s share prices have risen by 50% in 2020 alone; United Microtechnology’s value has more than doubled. While they are working on expanding their capacity, the current demand for new devices and their associated components is likely to continueexceeding supplyfor the rest of the calendar year.However, for people and businesses that need these delayed devices, the shortage is moreserious.

Component and computer shortages affect many more parties than simply the manufacturers. Consumers and businesses at the end of the supply chain see effects as well when it is so difficult to get new machines produced. The problem is that none of these components are used in isolation. The microchips, LCD components, touchscreen elements, and even glass for screens are all utilized in a wide variety of technology, including things that your business may use. Indeed, as demand for phones increases, it becomes harder to source chips for all devices. The result is that it’s simply harder and more expensive to get any type of computing technology. From phones to laptops to desktops, the chip shortage makes it more challenging to find the technology you may need.

IT products like desktop PCs are slightly less impacted by the current shortages than many other products. In general, people who made the switch to working from home have been more likely to purchase a laptop instead of a desktop. Even so, desktop machines are still being affected by shortages and long wait times. In addition, the increased demand for gaming PCs is keeping

When this pressure is combined with the need for functional work laptops, it entails that mobile devices and LCD panels may be facing delivery times as long as three months. It is possible to obtain devices on a shorter timeline, but at present, it appears that end-users like businesses will pay the price. Early estimates suggest that PC prices might rise by as much as 30% in 2021 to account for the shortages. When all these delays and shortages are combined, it spells a clear message: this is not the time to upgrade your hardware. Instead, focus on improving and securing the hardware you already have.

COVID-19 has had a dramatic effect on the electronics industry. The worldwide drive for people to work and educate from home and the increase in demand for medical products have taken the supply of electronics components from overcapacity to shortage and extended lead times. This was multiplied by the shutdown of manufacturing and the attempt to catch up with previous demand. The industrial market has also gotten hit by the loss of small gen fab capacity due to the shutting down of older, less competitive fabs.

Before COVID-19, the display market had been in an oversupply with the slowdown in cell phone demand. With the increased demand for laptops, monitors, and even TVs has backfilled this capacity and driven us into a shortage situation. This shortage of electronic components is not only in the display market but extends to basic components like resistors and capacitors.

The outlook for your ability to get the 2021 model TV you might have your eyes on, and the price you might have to pay for it isn’t good right now, following reports of component shortages limiting production yields this year.

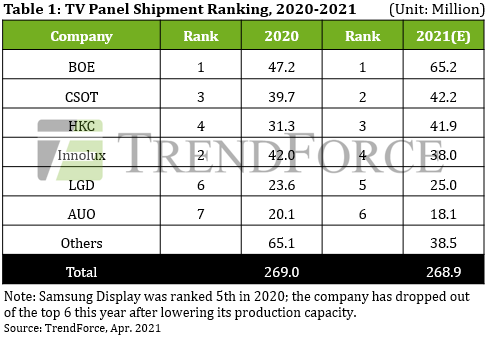

According to reports out of Asia, widespread component supply shortages could impact availability on LCD TV panels from TCL owned panel maker China Star Optoelectronics Technology (CSoT) and Innolux, two of the world’s largest LCD panel suppliers.

The display panel manufacturers were reported by Korean electronics business news site The Elec on Mondayas warning that supplies of panels are expected to be “tight throughout the year.”

TCL chairman Li Dongsheng used a media briefing last week to announce that panel shortages will continue in the first half of 2021, following conditions already hampered last year during the start of the Covid-19 pandemic.

The Elec article also cited Innolux president James Yang warning of a shortage in LCD panels caused by strong demand for LCD coming out of the global Covid-19 crisis, and he also added the conditions are expected to continue through 2021.

Innolux has seen shortages in LCD components including power semiconductors, driver ICs and glass substrates that have kept production below capacity. Shortages of integrated circuits and semiconductors could continue right up to the first half of 2022, Yan cautioned.

Ironically, prior to the run on LCD panel supplies, manufacturers were also faced with the dilemma of overproduction causing a glut in inventory, which was driving prices artificially lower. This was the result of giant new LCD fabs coming online in China and other areas of Asia.

TV manufacturers reportedly have been moving aggressively to replenish inventories of LCD panels to meet strong sales of TVs and other devices to meeting escalating demand, particularly in the United States and Europe.

At the same time, Samsung Display LCD monitor panel supplies for monitors are on course to terminate by the end of the first quarter 2021, and supply of IT panels overall will only continue to tighten up as demand increases for TVs and notebook panels, according to Asian analyst reports.

China-based Sigmaintell last week estimated the average selling price for a 21.5-inch LCD module for monitors would rise $3 to $55 this month, compared to a $2.50 increase for 23.8-inch panels and $2 increase for 27-inch monitor panels.

A shortage of large LCDs, which has lasted for almost a year, and which has resulted in the biggest panel price increases in the history of the industry, has begun to turn into an oversupply, according to research by consulting firm DSCC.

The shortage was driven by strong demand for TVs in the US during the Covid-19 pandemic, but increasing vaccination rates and higher inventory levels have led to a weakening in this market.

While every country has been affected by the pandemic and demand for LCD panels in IT applications remains high, the surge in demand for big TVs at premium prices in the US has had the biggest impact on LCD panel prices, feeding healthy profit margins at all major TV brands. But the surge of demand that started in Q2, 2020 is now slowing, as US consumers begin to spend more on travel and other activities that were restricted during lockdown.

DSCC expects the panel price for LCD TVs to begin to fall during the second half of 2021, but tight supply for various components such as driver ICs and glass substrates will continue for the time being.

Why it matters: The global semiconductor industry was worth $439 billion in 2020, and is on track to grow even bigger this year. However, that growth potential is being eroded by a shortage of $1 chips that are essential for every display panel that needs to be manufactured.

A global shortage of chips has wreaked havoc on the supply chains of the tech and auto industries. This has caused many companies to scale back production at a time when demand is soaring for their products. This is the result of a combination of factors, and the current situation will probably not change until the end of next year.

According to a Bloomberg report, there is now a serious shortage of display driver chips that is creating headaches for manufacturers of LCD and OLED panels. This in turn will affect all manner of consumer devices, from the lowly smartwatch to smartphones, tablets, laptops, computer monitors, TVs, smart appliances, and infotainment systems. Every new car or plane comes with one or more display panels, which only adds to the demand.

Nevertheless, the shortage of these driver chips will likely cause further delays and price hikes for products that are currently in high demand, and the manufacturers of these chips don"t see a solution in sight.

The shortfall is already visible in the doubling of prices for large LCD panels over the last year. Himax Technologies CEO Jordan WU told Bloomberg "I have never seen anything like this in the past 20 years since our company"s founding."

Digitimes’ reports LCD panel makers continue to feel the impact of chip shortages, which will likely persist for the next 2-3 years, according to industry sources. The price of LCD TV panels below 55 inches has been further declined by US$3-4 in August, compared with the month earlier. Larger LCD TVs of 65 or 75-inch ended their rising ASP streak in August; the price of IT panels continues to rise but by smaller increases. AUO, HannStar, and Coretronics have reiterated at their shareholder meetings that the shortage isn"t going away in 2-3 years. Paul Peng, AUO" chairman said the demand for commercial panels will start growing in the second half of the year while materials are nowhere to be found, and the chip shortage could persist for a few years more. Panel production will still be limited due to the chip shortage. Hsu-Ho Wu, HannStar vice president said the shortage will continue to impact the IC industry as chips are needed for mobile phones, tablets, and notebooks. Sarah Lin, president of Coretronics said the supply of driver IC is still tight. On top of material shortage, the lack of shipping containers causes another impact on shipments. LCD panel makers have seen orders picking up, in turn boosting their demand for driver ICs. But supply of LCD driver ICs has fallen far short of demand, prompting vendors to consider raising prices. Many other components are also in short supply, including networking chips. Some networking chip vendors, such as Broadcom, have had to extend their delivery lead times. At TSMC, its foundry services are expected to see strong demand from 5G, HPC and automotive sectors during second-quarter 2021. LCD driver IC supply fell short of demand by over 20% prompting suppliers to initiate price hikes, according to industry sources. Some networking chip vendors, such as Broadcom, have extended their delivery lead times to as long as 50 weeks due to the tight supply of critical parts and components, heralding the tight supply of networking chips in H221, according to industry sources. TSMC has seen its production capacity during the second quarter filled by a strong pull-in of orders for 5G, HPC and automotive electronics chips, according to industry sources.

With LCD prices surging, many customers on allocation due to tight panel supply and component shortages and LCD manufacturers enjoying strong financial performance and stock price appreciation, LCD manufacturers are now projected to embark on a new wave of capacity growth.

What exactly is short in the market? Your iPhone’s screen is one solid unit made up of several elements that are fused together with OCA (optically clear adhesive). The exterior glass, the digitizer panel (touch sensor), the polarizer and LCD panel. The LCD panel is the key component that is in short supply. Originally Apple had 3 manufacturers to produce LCD panels (LG, Sharp and Toshiba). Apple’s authorized manufacturers have the exclusive technology to produce LCD panels. Other Chinese manufacturers can copy the glass, digitizer, polarizers, OCA, flex cables, backlights, frames and everything except for the main component of the LCD assembly.

How were we getting these parts before? A big leak in Apple’s supply chain. The iPhone 5, 5S and 5C all share most of the same raw components including the LCD panel, the only difference is the flex cable and plastic frame. Independent factories in China can produce these components and can manufacture any 5 series assembly from an LCD panel. Shown on the left is a pulse pressing machine, used to connect the flex cable to the LCD. We use one of these to repair LCDs with damaged flex cables.

So what’s happening?A few things, first Apple has cut off LG and Toshiba, making Sharp their exclusive supplier for iPhone LCD panels and implemented very tight security. Secondly, they have had Foxconn destroy stockpiles of series 5 LCD panels to reduce the parts and material leakage to factories that re-engineer them for the independent repair industry. Along with this strategy, Apple has instructed Foxconn to reduce series 6 materials leakage from their manufacturing centers. Lastly, Apple is working aggressively with US Customs to seize inbound parts.

How long is this shortage going to last? In short,we have no idea. At the time of this writing, LCD prices have been steadily rising for 6 months and replacement iPhone 6S LCDs cost twice what Apple charges for their repair service. Apple does not intend to compete with independent repair shops, instead they are squeezing the profit out of the industry. LCD refurbishing may help shops cut cost but without new LCD panels entering the system it won’t last long.

What does this mean for the independent repair community?Apple is the only repair operation that is immune. Even the Chinese LCD refurbishing plants used by the large chain repair companies are running out of LCDs. Continually rising costs may push out the big chains but with lower overhead and clever problem-solving, the owner-operated shops stand a fighting chance.

Strong demand for LCD panels in the wake of the coronavirus pandemic has created shortages that will remain in the entire 2021, according to Innolux president James Yang.

Global production capacity for LCD panels exceeds global demand currently, but actual output is much less than the capacity due to continued shortages of key components including polarizers, power ICs, driver ICs and glass substrates, Yang said at a March 3 investors conference.

Shortage of ICs is the most serious and may remain until first-half 2022, Yang noted. Japan-based Nippon Electric Glass and Asahi Glass, two main suppliers of glass substrates, have seen factory accidents and the glass supply is expected to be tight in first-half 2021, Yang indicated.

In view of potential demand for high value-added automotive displays along with development of smart cockpits and integration of various digital information, Innolux has worked with clients developing high-end free-form miniLED-backlit LCD automotive displays of over 20 inches for use in high-end car models, Yang said, adding Innolux has begun small-volume shipments for such displays, and aims to become the market leader in 2023.

Due to the pandemic and along with increasing deployments of 5G infrastructure, global demand for online education is growing fast, and Innolux"s shipment for notebook-use LCD panels in 2020 hiked 50% on year to become the second-largest supplier worldwide, Yang indicated.

Of global demand for Chromebooks used in online education, 30% was met in 2020 and 70% is not yet satisfied, and Innolux is optimistic about shipments for notebook-use LCD panels in 2021, Yang noted.

In view of fast increasing application of AI, IoT and 5G, Innolux has stepped into business other than LCD panels. Based on TFT-LCD manufacturing technology, Innolux has worked with US-based Kymeta to produce liquid crystal meta-surface antennas and with InnoCare Optoelectronics, its subsidiary, to produce X-ray flat panel detectors for medical diagnosis.

– Pandemic:The direct and root cause of causing the crisis is the pandemic. In March 2020, a lot of countries issued executive orders for people to stay at home. The demand for various products dropped sharply. A lot of manufacturers cancelled or pushed out orders. The world 1st and 2nd biggest LCD manufacturers Samsung and LG declared the plan to stop all the LCD production. A lot of LCD panel and IC manufacturers cut the production because of order drop or executive orders to stay at home. They use stock instead of the fresh production to fill the demands.

– Chaos of Executive orders and planning:Because of the pandemic, nobody knew what was ahead. Executive orders were updated monthly, the same as the planning for schools, plants, companies and other organizations. By July, a lot of schools started to realize that it was not practical to open the schools in personal and needed every student to have online classes which suddenly boosted the orders of laptops, monitors, TVs and other entertainment devices. The LCD panel manufacturers couldn’t ramp up for so fast increased demands. The stock was cleared quickly and LCD factories had been running 7/24 starting last fall which still couldn’t keep up the order speed. The price increase followed right after.

– Zero Stock Policies: LCD panel and IC prices had been inclined for more than a decade. There had been a fixed mindset for a lot of commodity executives and managers that the prices will fall ever. Because the competition was tough for suppliers, the big customers demand for OTD (On Time Delivery), especially for automotive makers. They don’t hold much or any stock in order to improve the cost down and cash flow. The result is that they totally rely on suppliers to hold the inventory. With the pandemic, a lot of customers first pushed out orders which made the supplier chill in spine. The suppliers tried to cut their inventory in order to prepare enough cash for industrial winter.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey