lcd panel production 2018 made in china

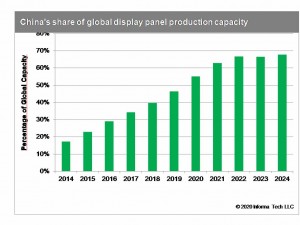

China is the leader in producing LCD display panels, with a forecast capacity share of 56 percent in 2020. China"s share is expected to increase in the coming years, stabilizing at 69 percent from 2023 onwards.Read moreLCD panel production capacity share from 2016 to 2025, by countryCharacteristicChinaJapanSouth KoreaTaiwan-----

DSCC. (June 8, 2020). LCD panel production capacity share from 2016 to 2025, by country [Graph]. In Statista. Retrieved December 16, 2022, from https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. "LCD panel production capacity share from 2016 to 2025, by country." Chart. June 8, 2020. Statista. Accessed December 16, 2022. https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. (2020). LCD panel production capacity share from 2016 to 2025, by country. Statista. Statista Inc.. Accessed: December 16, 2022. https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. "Lcd Panel Production Capacity Share from 2016 to 2025, by Country." Statista, Statista Inc., 8 Jun 2020, https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC, LCD panel production capacity share from 2016 to 2025, by country Statista, https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/ (last visited December 16, 2022)

BOE Technology Group, the Chinese electronic components producer, is expected to be the leader in producing LCD display panels in the coming years, with a forecast capacity share of 24 percent by 2022. China is the country that has the largest LCD capacity, with a 56 percent share in 2020.Read moreLCD panel production capacity share from 2016 to 2022, by manufacturerCharacteristicBOEChina StarInnoluxAUOLGDHKCCEC PandaSharpSDCOther-----------

DSCC. (June 8, 2020). LCD panel production capacity share from 2016 to 2022, by manufacturer [Graph]. In Statista. Retrieved December 16, 2022, from https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. "LCD panel production capacity share from 2016 to 2022, by manufacturer." Chart. June 8, 2020. Statista. Accessed December 16, 2022. https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. (2020). LCD panel production capacity share from 2016 to 2022, by manufacturer. Statista. Statista Inc.. Accessed: December 16, 2022. https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. "Lcd Panel Production Capacity Share from 2016 to 2022, by Manufacturer." Statista, Statista Inc., 8 Jun 2020, https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC, LCD panel production capacity share from 2016 to 2022, by manufacturer Statista, https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/ (last visited December 16, 2022)

LG Display and Samsung Display are struggling to find their ways out of the deterioration of their performance even after withdrawing from production of liquid crystal display (LCD) panels. The high-priced organic light emitting diode (OLED) panel sector regarded as a future growth engine is not growing fast due to the economic downturn. Even in the OLED panel sector, Chinese display makers are within striking distance of Korean display makers, experts say.

On Aug. 30, Display Supply Chain Consultants (DSCC), a market research company, predicted that LCD TV panel prices hit an all-time low in August and that an L-shaped recession will continue in the fourth quarter. According to DSCC, the average price of a 65-inch ultra-high-definition (UHD) panel in August was only US$109, a 62 percent drop from the highest price of US$288 recorded in July in 2021. The average price of a 75-inch UHD panel was only US$218, which was only about half of the highest price of US$410 in July last year. DSCC predicted that the average panel price in the third quarter will fall by 15.7 percent. As Chinese companies’ price war and the effect of stagnation in consumption overlapped, the more LCD panels display makers produce, the more loss they suffer.

As panel prices fell, manufacturers responded by lowering facility utilization rates. DSCC said that the LCD factory utilization rate descended from 87 percent in April to 83 percent in May, 73 percent in June, and 70 percent in July.

Now that the LCD panel business has become no longer lucrative, Korean display makers have shut down their LCD business or shrunk their sizes. In the LCD sector, China has outpaced Korea since 2018. China’s LCD market share reached 50.9 percent in 2021, while that of Korea dropped to 14.4 percent, lower than Taiwan’s 31.6 percent.

Samsung Display already announced its withdrawal from the LCD business in June. Only 10 years have passed since the company was spun off from Samsung Electronics in 2012. LG Display has decided to halt domestic LCD TV panel production until 2023 and reorganize its business structure centering on OLED panels. Its Chinese LCD production line will be gradually converted to produce LCD panels for IT or commercial products. TrendForce predicted that LG Display will stop operating its P7 Plant in the first quarter of next year.

Korean display makers’ waning LCD business led to a situation in which Korea even lost first place in the display industry. Korea with a display market share of 33.2 percent was already overtaken by China with 41.5 percent) in 2021 according to market researcher Omdia and the Korea Display Industry Association. Korea’s market share has never rebounded in for five years since 2017 amid the Korean government’s neglect. Seventeen years have passed since 2004 when Korea overtook Japan to rise to the top of the world in the LCD industry. Korea’s LCD exports amounted to more than US$30 billion in 2014, but fell to US$21.4 billion last year.

A bigger problem is that Korean display makers may lose its leadership in the OLED panel sector although it is still standing at the top spot. While Korea’s OLED market share fell from 98.1 percent in 2016 to 82.8 percent last year, that of China rose from 1.1 percent to 16.6 percent. Considering that the high-end TV market is highly likely to shrink for the time being due to a full-fledged global consumption contraction, some analysts say that the technology gap between Korea and China can be sharply narrowed through this looming TV market slump. According to industry sources, the Chinese government is now focusing on giving subsidies to the development of OLED panel technology rather LCD technology. On the other hand, in Korea, displays were also wiped out from national strategic technology industry items under the Restriction of Special Taxation Act which can receive tax benefits for R&D activities on displays.

Panel makers are cutting production by 16 percent on average from this month, Rong Chaoping, senior researcher at market research firm AVC Revo, told Yicai Global. Television panel makers are expected to ship 3.6 million less panels than last month.

Panel makers will reduce capacity by between 15 and 20 percent this month, said Wu Rongbing, chief analyst at Chinese semiconductor intelligence service Omdia.

TCL China Star intends to continue with its production cuts until September, while Beijing-based BOE and HKC Optoelectronics Technology have not yet decided how long they will reduce output, Rong said. None of the three companies responded when contacted by Yicai Global.

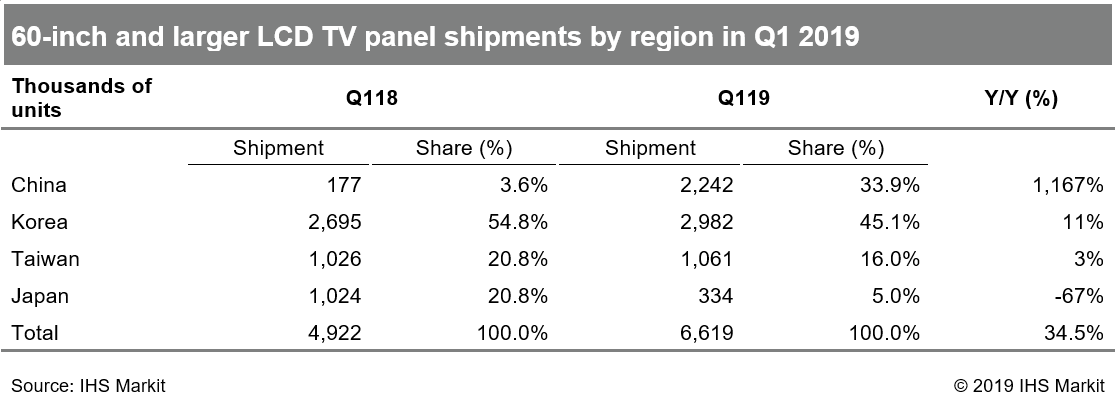

LCD TV display shipments from China’s five largest panel manufacturers accounted for 68.5 percent of the global market in April, a new high, and they were expected to exceed 70 percent this year, according to Omdia.

The global panel industry is expected to slash production by about 20 percent this year, according to Beijing-based Sigmaintell. It is the first time since 2013 that the worldwide sector has implemented such a large-scale and wide-ranging cut in manufacturing. But it should help to slow the fall in prices, Li said.

“Tumbling prices are squeezing profits,” Li said. “The price of a TV panel is now below cost price and that of some data panels is also below the manufacturing cost.”

“Panel makers are facing rising liquidity pressure and bigger losses as prices are now below cost price, so the display industry is likely to undergo another big reshuffle,” Rong said.

Panel prices are likely to stop dropping this month or next as output falls, Wu said. Whether prices will start to pick up soon depends on when demand improves.

BOE Technology Group and TCL China Star Optoelectronics Technology (TCL CSOT) are among the Chinese panel makers to have ramped up output since around 2019 with generous state subsidies. China is gaining on South Korea, whose share of capacity is seen reaching 55% for 2022 in an October estimate by U.S. market intelligence firm Display Supply Chain Consultants (DSCC).

China"s first 8.5-generation TFT-LCD production line was launched in Bengbu, East China"s Anhui province, on June 18, 2019, representing a breakthrough in the production of high-definition LCD screen, Science and Technology Daily reported.

TFT-LCD, or Thin Film Transistor Liquid Crystal Display, is key strategic material of the electronic information display industry. The Gen 8.5 TFT-LCD production line, launched by the Bengbu Glass Industry Design and Research Institute of the China National Building Material Group, will produce high-definition LCD screens of 55 inches, the report said.

According to the Liquid Crystal Branch of the China Optics and Optoelectronics Manufactures Association, the demand for TFT-LCD in the Chinese mainland was about 260 million square meters in 2018, including 233 million square meters" Gen 8.5 TFT-LCD. However, the annual supply of domestically made TFT-LCD is less than 40 million square meters, with all of them Gen 6 or below, which cannot meet the demand in scale and quantity.

The association predicted that China"s market demand for Gen 8.5 TFT-LCD or above will exceed 300 million square meters by 2020, accounting for 49.6 percent of the total global demand.

The production and control precision of Gen 8.5 TFT-LCD is comparable to that of the semiconductor industry, representing a higher level of large-scale manufacturing of modern glass industry.

The institute in Bengbu, with 60 years of expertise in glass, has finally made a breakthrough in the production of Gen 8.5 TFT-LCD, and will provide key raw material guarantee for China"s LCD panel industry after it goes into mass production in September, the report said.

Flat-panel displays are thin panels of glass or plastic used for electronically displaying text, images, or video. Liquid crystal displays (LCD), OLED (organic light emitting diode) and microLED displays are not quite the same; since LCD uses a liquid crystal that reacts to an electric current blocking light or allowing it to pass through the panel, whereas OLED/microLED displays consist of electroluminescent organic/inorganic materials that generate light when a current is passed through the material. LCD, OLED and microLED displays are driven using LTPS, IGZO, LTPO, and A-Si TFT transistor technologies as their backplane using ITO to supply current to the transistors and in turn to the liquid crystal or electroluminescent material. Segment and passive OLED and LCD displays do not use a backplane but use indium tin oxide (ITO), a transparent conductive material, to pass current to the electroluminescent material or liquid crystal. In LCDs, there is an even layer of liquid crystal throughout the panel whereas an OLED display has the electroluminescent material only where it is meant to light up. OLEDs, LCDs and microLEDs can be made flexible and transparent, but LCDs require a backlight because they cannot emit light on their own like OLEDs and microLEDs.

Liquid-crystal display (or LCD) is a thin, flat panel used for electronically displaying information such as text, images, and moving pictures. They are usually made of glass but they can also be made out of plastic. Some manufacturers make transparent LCD panels and special sequential color segment LCDs that have higher than usual refresh rates and an RGB backlight. The backlight is synchronized with the display so that the colors will show up as needed. The list of LCD manufacturers:

Organic light emitting diode (or OLED displays) is a thin, flat panel made of glass or plastic used for electronically displaying information such as text, images, and moving pictures. OLED panels can also take the shape of a light panel, where red, green and blue light emitting materials are stacked to create a white light panel. OLED displays can also be made transparent and/or flexible and these transparent panels are available on the market and are widely used in smartphones with under-display optical fingerprint sensors. LCD and OLED displays are available in different shapes, the most prominent of which is a circular display, which is used in smartwatches. The list of OLED display manufacturers:

MicroLED displays is an emerging flat-panel display technology consisting of arrays of microscopic LEDs forming the individual pixel elements. Like OLED, microLED offers infinite contrast ratio, but unlike OLED, microLED is immune to screen burn-in, and consumes less power while having higher light output, as it uses LEDs instead of organic electroluminescent materials, The list of MicroLED display manufacturers:

LCDs are made in a glass substrate. For OLED, the substrate can also be plastic. The size of the substrates are specified in generations, with each generation using a larger substrate. For example, a 4th generation substrate is larger in size than a 3rd generation substrate. A larger substrate allows for more panels to be cut from a single substrate, or for larger panels to be made, akin to increasing wafer sizes in the semiconductor industry.

"Samsung Display has halted local Gen-8 LCD lines: sources". THE ELEC, Korea Electronics Industry Media. August 16, 2019. Archived from the original on April 3, 2020. Retrieved December 18, 2019.

"TCL to Build World"s Largest Gen 11 LCD Panel Factory". www.businesswire.com. May 19, 2016. Archived from the original on April 2, 2018. Retrieved April 1, 2018.

"Panel Manufacturers Start to Operate Their New 8th Generation LCD Lines". 대한민국 IT포털의 중심! 이티뉴스. June 19, 2017. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"TCL"s Panel Manufacturer CSOT Commences Production of High Generation Panel Modules". www.businesswire.com. June 14, 2018. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"Business Place Information – Global Operation | SAMSUNG DISPLAY". www.samsungdisplay.com. Archived from the original on 2018-03-26. Retrieved 2018-04-01.

"Samsung Display Considering Halting Some LCD Production Lines". 비즈니스코리아 - BusinessKorea. August 16, 2019. Archived from the original on April 5, 2020. Retrieved December 19, 2019.

Herald, The Korea (July 6, 2016). "Samsung Display accelerates transition from LCD to OLED". www.koreaherald.com. Archived from the original on April 1, 2018. Retrieved April 1, 2018.

Byeonghwa, Yeon. "Business Place Information – Global Operation – SAMSUNG DISPLAY". Samsungdisplay.com. Archived from the original on 2018-03-26. Retrieved 2018-04-01.

www.wisechip.com.tw. "WiseChip History – WiseChip Semiconductor Inc". www.wisechip.com.tw. Archived from the original on 2018-02-17. Retrieved 2018-02-17.

"China"s BOE to have world"s largest TFT-LCD+AMOLED capacity in 2019". ihsmarkit.com. 2017-03-22. Archived from the original on 2019-08-16. Retrieved 2019-08-17.

In recent time, China domestic companies like BOE have overtaken LCD manufacturers from Korea and Japan. For the first three quarters of 2020, China LCD companies shipped 97.01 million square meters TFT LCD. And China"s LCD display manufacturers expect to grab 70% global LCD panel shipments very soon.

BOE started LCD manufacturing in 1994, and has grown into the largest LCD manufacturers in the world. Who has the 1st generation 10.5 TFT LCD production line. BOE"s LCD products are widely used in areas like TV, monitor, mobile phone, laptop computer etc.

TianMa Microelectronics is a professional LCD and LCM manufacturer. The company owns generation 4.5 TFT LCD production lines, mainly focuses on making medium to small size LCD product. TianMa works on consult, design and manufacturing of LCD display. Its LCDs are used in medical, instrument, telecommunication and auto industries.

TCL CSOT (TCL China Star Optoelectronics Technology Co., Ltd), established in November, 2009. TCL has six LCD panel production lines commissioned, providing panels and modules for TV and mobile products. The products range from large, small & medium display panel and touch modules.

Everdisplay Optronics (Shanghai) Co.,Ltd.(EDO) is a company dedicated to production of small-to-medium AMOLED display and research of next generation technology. The company currently has generation 4.5 OLED line.

Established in 1996, Topway is a high-tech enterprise specializing in the design and manufacturing of industrial LCD module. Topway"s TFT LCD displays are known worldwide for their flexible use, reliable quality and reliable support. More than 20 years expertise coupled with longevity of LCD modules make Topway a trustworthy partner for decades. CMRC (market research institution belonged to Statistics China before) named Topway one of the top 10 LCD manufactures in China.

The Company engages in the R&D, manufacturing, and sale of LCD panels. It offers LCD panels for notebook computers, desktop computer monitors, LCD TV sets, vehicle-mounted IPC, consumer electronics products, mobile devices, tablet PCs, desktop PCs, and industrial displays.

Chinese companies have gained a competitive edge in the large-screen display industry and the exit of South Korean counterparts such as Samsung Electronics and LG Display from the liquid crystal display market will bring opportunities for China"s panel makers despite the challenges posed by the COVID-19 pandemic.

Market research firm Sigmaintell said BOE Technology Group Co Ltd-a leading Chinese supplier of display products and solutions-became the world"s largest shipper of LCD TV panels for the first time in 2019.

The Beijing-based company shipped 53.3 million units of LCD panels in 2019, with production capacity increasing by more than 20 percent on a yearly basis.Chinese companies have gained an upper hand in large-screen LCD displays. Samsung and LG"s decision to exit from the LCD sector means Chinese panel makers will take a dominant position in this field

The consultancy said the LCD TV panel production area of Chinese manufacturers will account for more than 50 percent of the global total this year, surpassing South Korean competitors who are accelerating the shutdown of large-sized LCD panel production capacity due to competition from Chinese manufacturers.

It estimated the production capacity of large-sized LCD panels will continue to increase in China over the next three years. In addition, global LCD TV panel shipments stood at 283 million pieces last year, a slight decrease of 0.2 percent year-on-year. Meanwhile, the shipment area was 160 million square meters, an increase of 6.3 percent year-on-year.

"Chinese companies have gained an upper hand in large-screen LCD displays. Samsung and LG"s decision to exit from the LCD sector means Chinese panel makers will take a dominant position in this field," said Li Dongsheng, founder and chairman of Chinese tech giant TCL Technology Group Corp.

Li said South Korean firms will focus on organic LED screens and quantum dot LED displays, while Chinese TV panel makers are catching up at a rapid pace.

Data consultancy Digitimes Research said it comes as little surprise that Samsung has opted to withdraw from the LCD panel sector as its LCD business was losing money in every quarter of 2019 due to challenges from Chinese competitors.

BOE said its Gen 10.5 TFTLCD production line achieved mass production in Hefei, Anhui province, in March 2018. The plant mainly produces high-definition LCD screens of 65 inches and above. With a total investment of 46 billion yuan (US$6.5 billion), the company"s second Gen 10.5 TFT-LCD production line launched operations in Wuhan, Hubei province, in December.

The Gen 11 TFT-LCD and active-matrix OLED production line of Shenzhen China Star Optoelectronics Technology, a subsidiary of TCL, officially entered operations in November 2018, producing 43-inch, 65-inch and 75-inch LCD screens.

Chen Lijuan, an analyst at Sigmaintell, said panel manufacturers should not just invest in production lines, but also pay more attention to the establishment of the whole supply chain, including raw materials, equipment and technology.

Bian Zheng, deputy director of research at AVC Revo, a unit of market consultancy firm AVC, said China will have a 51 percent market share in global TV shipments in 2020, while South Korea will have 25 percent, adding that large-screen TV panels will bolster healthy development of the industry.

Bian said the OLED and QLED will be the next-generation flat-panel display technologies to be in the spotlight. LG Display is currently the world"s only supplier of large-screen OLED TV panels.

OLED is a relatively new technology and part of recent display innovation. It has a fast response rate, wide viewing angles, super high-contrast images and richer colors. It is much thinner and can be made flexible, compared with traditional LCD display panels.

► When the leading Korean players Samsung Display and LG Display exit LCD production, BOE will be the most significant player in the LCD market. Though OLED can replace the LCD, it will take years for it to be fully replaced.

► As foreign companies control evaporation material and machines, panel manufacturers seek a cheaper way to mass-produce OLED panels – inkjet printing.

When mainstream consumer electronics brands choose their device panels, the top three choices are Samsung Display, LG Display (LGD) and BOE (000725:SZ) – the first two from Korea and the third from China. From liquid-crystal displays (LCD) to active-matrix organic light-emitting diode (AMOLED), display panel technology has been upgrading with bigger screen products.

From the early 1990s, LCDs appeared and replaced cathode-ray tube (CRT) screens, which enabled lighter and thinner display devices. Japanese electronics companies like JDI pioneered the panel technology upgrade while Samsung Display and LGD were nobodies in the field. Every technology upgrade or revolution is a chance for new players to disrupt the old paradigm.

The landscape was changed in 2001 when Korean players firstly made a breakthrough in the Gen 5 panel technology – the later the generation, the bigger the panel size. A large panel size allows display manufacturers to cut more display screens from one panel and create bigger-screen products. "The bigger the better" is a motto for panel makers as the cost can be controlled better and they can offer bigger-size products to satisfy the burgeoning middle-class" needs.

LCD panel makers have been striving to realize bigger-size products in the past four decades. The technology breakthrough of Gen 5 in 2002 made big-screen LCD TV available and it sent Samsung Display and LGD to the front row, squeezing the market share of Japanese panel makers.

The throne chair of LCD passed from Japanese companies to Korean enterprises – and now Chinese players are clinching it, replacing the Koreans. After twenty years of development, Chinese panel makers have mastered LCD panel technology and actively engage in large panel R&D projects. Mass production created a supply surplus that led to drops in LCD price. In May 2020, Samsung Display announced that it would shut down all LCD fabs in China and Korea but concentrate on quantum dot LCD (Samsung calls it QLED) production; LGD stated that it would close LCD TV panel fabs in Korea and focus on organic LED (OLED). Their retreats left BOE and China Stars to digest the LCD market share.

Consumer preference has been changing during the Korean fab"s recession: Bigger-or-not is fine but better image quality ranks first. While LCD needs the backlight to show colors and substrates for the liquid crystal layer, OLED enables lighter and flexible screens (curvy or foldable), higher resolution and improved color display. It itself can emit lights – no backlight or liquid layer is needed. With the above advantages, OLED has been replacing the less-profitable LCD screens.

Samsung Display has been the major screen supplier for high-end consumer electronics, like its own flagship cell phone products and Apple"s iPhone series. LGD dominated the large OLED TV market as it is the one that handles large-size OLED mass production. To further understand Korean panel makers" monopolizing position, it is worth mentioning fine metal mask (FMM), a critical part of the OLED RGB evaporation process – a process in OLED mass production that significantly affects the yield rate.

Prior to 2018, Samsung Display and DNP"s monopolistic supply contract prevented other panel fabs from acquiring quality FMM products as DNP bonded with Hitachi Metal, the "only" FMM material provider choice for OLED makers. After the contract expired, panel makers like BOE could purchase FFM from DNP for their OLED R&D and mass production. Except for FFM materials, vacuum evaporation equipment is dominated by Canon Tokki, a Japanese company. Its role in the OLED industry resembles that of ASML in the integrated circuit space. Canon Tokki"s annual production of vacuum evaporation equipment is fewer than ten and thereby limits the total production of OLED panels that rely on evaporation technology.

The shortage of equipment and scarcity of materials inspired panel fabs to explore substitute technology; they discovered that inkjet printing has the potential to be the thing to replace evaporation. Plus, evaporation could be applied to QLED panels as quantum dots are difficult to be vaporized. Inkjet printing prints materials (liquefied organic gas or quantum dots) to substrates, saving materials and breaking free from FMM"s size restriction. With the new tech, large-size OLED panels can theoretically be recognized with improved yield rate and cost-efficiency. However, the tech is at an early stage when inkjet printing precision could not meet panel manufacturers" requirements.

Display and LGD are using evaporation on their OLED products. To summarize, OLED currently adopts evaporation and QLED must go with inkjet printing, but evaporation is a more mature tech. Technology adoption will determine a different track for the company to pursue. With inkjet printing technology, players are at a similar starting point, which is a chance for all to run to the front – so it is for Chinese panel fabs. Certainly, panel production involves more technologies (like flexible panels) than evaporation or inkjet printing and only mastering all required technologies can help a company to compete at the same level.

Presently, Chinese panel fabs are investing heavily in OLED production while betting on QLED. BOE has four Gen 6 OLED product lines, four Gen 8.5 and one Gen 10.5 LCD lines; China Star, controlled by the major appliance titan TCL, has invested two Gen 6 OLED fabs and four large-size LCD product lines.

Remembering the last "regime change" that occurred in 2005 when Korean fabs overtook Japanese" place in the LCD market, the new phase of panel technology changed the outlook of the industry. Now, OLED or QLED could mark the perfect time for us to expect landscape change.

After Samsung Display and LGD ceding from LCD TV productions, the vacant market share will be digested by BOE, China Star and other LCD makers. Indeed, OLED and QLED have the potential to take over the LCD market in the future, but the process may take more than a decade. Korean companies took ten years from panel fab"s research on OLED to mass production of small- and medium-size OLED electronics. Yet, LCD screen cell phones are still available in the market.

LCD will not disappear until OLED/QLED"s cost control can compete with it. The low- to middle-end panel market still prefers cheap LCD devices and consumers are satisfied with LCD products – thicker but cheaper. BOE has been the largest TV panel maker since 2019. As estimated by Informa, BOE and China Star will hold a duopoly on the flat panel display market.

BOE"s performance seems to have ridden on a roller coaster ride in the past several years. Large-size panel mass production like Gen 8.5 and Gen 10.5 fabs helped BOE recognize the first place in production volume. On the other side, expanded large-size panel factories and expenses of OLED product lines are costly: BOE planned to spend CNY 176.24 billion (USD 25.92 billion) – more than Tibet"s 2019 GDP CNY 169.78 billion – on Chengdu and Mianyang"s Gen 6 AMOLED lines and Hefei and Wuhan"s Gen 10.5 LCD lines.

Except for making large-size TVs, bigger panels can cut out more display screens for smaller devices like laptops and cell phones, which are more profitable than TV products. On its first-half earnings concall, BOE said that it is shifting its production focus to cell phone and laptop products as they are more profitable than TV products. TV, IT and cell phone products counted for 30%, 44% and 33% of its productions respectively and the recent rising TV price may lead to an increased portion of TV products in the short term.

Except for outdoor large screens, TV is another driver that pushes panel makers to research on how to make bigger and bigger screens. A research done by CHEARI showed that Chinese TV sales dropped by 10.6% to CNY 128.2 billion from 2018 to 2019. Large-size TV sales increased as a total but the unit price decreased; high-end products like laser TV and OLED TV saw a strong growth of 131.2% and 34.1%, respectively.

The demand for different products may vary as lifestyles change and panel fabs need to make on-time judgments and respond to the change. For instance, the coming Olympics is a new driving factor to boost TV sales; "smart city" projects around the world will need more screens for data visualization; people will own more screens and better screens when life quality improves. Flexible screens, cost-efficient production process, accessible materials, changing market and all these problems are indeed the next opportunity for the industry.

China-based OLED panel producers BOE Technology Group and TCL China Star Optoelectronics Technology have steadily boosted their output of high-end OLED panels. By next year they’ll control some 43 per cent of global demand for OLEDs.

“Starting from around 2018, Chinese companies have hired a host of engineers from Samsung Electronics and other South Korean companies, which made up for the shortfall,” said Yoshio Tamura, president of Asian operations at DSCC.

DSCC adds that if China overtakes South Korea in its share of OLED production, China will dominate virtually the entire display industry. Most Chinese-made OLED panels are small to midsize ones for smartphones, so the focus will then be on whether Chinese companies acquire capabilities for manufacturing large OLED panels for TV manufacturing.

South Korean companies have already lost out to China in the race to invest in producing large LCD panels. In large OLED panels, South Korean companies are steadily going on the defensive, suggests DSCC.

LCD display module refers to the modular module formed by assembling the LCD display panel with the relevant driver circuit, backlight source, integrated circuit, and other components.

Upstream materials or components mainly include TFT LCD materials, a glass substrate, a polarizing plate, backlight, automation equipment, photoresistive materials, membrane materials, target materials, chemical materials, etc.Midstream is mainly panel manufactory processing manufacturing, the main process including cleaning, coating, exposure, etching, electroplating and so on. Subsequent manufacturing processes include inspection, cutting, placement, molding, boxing, and so on. Through the glass substrate TFT arrays and CF substrate, CF as upper and TFT self-built perfusion TFT LCD and the lower joint, and then put a polaroid, connection driver IC and control circuit board, and a backlight module assembling, eventually forming the whole piece of LCD module, including LCD module, LCD TV panels, feature phones, tablets, smartphones, panel; The downstream is a variety of fields of application terminal-based brands, assembly manufacturers, etc., including television, mobile phone, display, advertising, and other.

The LCD module is the core component of many electronic products. More and more electronics manufacturers in Japan, South Korea, and Taiwan have transferred their production lines of LCD modules to the Chinese mainland, making the production capacity of LCD modules in China increase exponentially every year. Since 2009, more than 80% of the world’s LCD module production has been provided by the Chinese mainland, with southern China playing an important role.

According to the China LCD module industry development prospects and investment strategy analysis report, statistics show that 2011-2014, the domestic LCD display module industry continues to rise in output whole range, 2011 domestic LCD display module industry output reached 3.641 billion sets, domestic LCD display module industry output growth in 2014 to 8.446 billion. In 2016, the industry capacity was adjusted, and the output of LCD modules decreased to 5.525 billion sets. By the end of 2017, the output of the LCD module industry in China reached 5.565 billion sets. As the output of smartphones, tablets, and other products increased, the demand for LCD modules also expanded. By 2018, the output of the LCD module industry in China reached 6.75 billion sets. Statistics on the output of LCD module industry in China from 2011 to 2018.

The output of LCD terminal applications has a direct impact on the demand for LCD screens and backlight display modules. Mobile phones, especially smartphones, as the largest application field of LCD modules, have an important impact on the growth of the demand for backlight display modules.

According to relevant data, Chinese enterprises have invested more than 70 billion us dollars in the whole industry chain of flat panel displays. It is estimated that by 2020, the scale of display panel production in China will jump from third place in the world to first place in the world. Imagination is huakai industrial screen manufacturers for the whole series of 1.4 inches to 15.6 inch TFT LCD module of small and medium-size standard and LCD display, LCD display module, industrial screen, industrial LCD screen, under the sunlight visually highlight LCD display, industrial custom screen, LCD screen-wide temperature, industrial IPS LCD screen, touch screen industry, high and low-temperature industrial screen, screen defense industry. The TFT LCD module is very suitable for industrial control devices, medical devices, POS systems, consumer electronics products, vehicle or GPS navigation products.

Foxconn, which received controversial state and local incentives for the project, initially planned to manufacture advanced large screen displays for TVs and other consumer and professional products at the facility, which is under construction. It later said it would build smaller LCD screens instead.

Rather than a focus on LCD manufacturing, Foxconn wants to create a "technology hub" in Wisconsin that would largely consist of research facilities along with packaging and assembly operations, Woo said. It would also produce specialized tech products for industrial, healthcare, and professional applications, he added.

Rather than manufacturing LCD panels in the United States, Woo said it would be more profitable to make them in greater China and Japan, ship them to Mexico for final assembly, and import the finished product to the United States.

Currently, to qualify for the tax credits Foxconn must meet certain hiring and capital investment goals. It fell short of the employment goal in 2018 - hiring 178 full-time jobs rather than the 260 targeted - failing to earn a tax credit of up to $9.5 million.

Chinese display manufacturers are chasing their South Korean rivals closely by planning to release a larger volume of liquid-crystal panels over 32 inches this year, said a market researcher Sunday.

According to a report on the 2017 shipment strategies of Chinese TV panel makers by IHS Markit, Chinese LCD panel suppliers are forecast to ship out a total of 320,000 large-size panels larger than 32 inches by the end of this year, a 33 percent surge from last year.

In the report, Wu mentioned the plans of major Chinese panel firms such as BOE, CSOT, CEC-Panda and HKC to focus on expanding production of 43, 55 and 58-inch panels, adding that demand for 32-inch panels will gradually decrease.

“By the end of 2018, China will be the largest region for TFT LCD capacity, and larger-sized products may make their factories more efficient and profitable than they have been when producing 32-inch panels,” he said.

“The strategies of Chinese panel makers will significantly influence global supply and demand,” Wu said. “In 2015 and 2016, the Chinese companies shipped 33.2 percent of worldwide LCD TV panel, trailing only Korean panel makers at 36.4 percent.”

The competition structure has been advantageous for the Korean players, since their Chinese rivals had been focusing on small LCD panels until last year. But now the Korean firms are facing fiercer competition in prices.

Although demand for organic-light emitting diode panels in the TV market is gradually rising, dominance of LCD panels is projected to continue for the foreseeable future.

“While OLEDs are expected to post sharp growth, they will not be able to usurp LCD as the panels of choice for upper-end TVs,” another report by IHS Markit said.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey