lcd panel price trend 2020 made in china

LCD TV panel prices have stopped falling after sliding below suppliers" cash-cost levels, according to industry sources. Additionally, aggressive production cuts by panel makers also have helped bring a stop to falling prices.

According to Pan Tai-chi, general manager of the TV Business Center of Innolux, TV panel inventories at most TV vendors and channel operators have bottomed out, and correspondent TV panel prices have risen since the second half of October.

Sales dynamics for TVs and monitors with high CP (cost-performance) ratios have started gaining momentum recently as current panel prices have made high CP display products more affordable, Pan said.

It was the supply side that drove the recent price hikes instead of being pushed up by increasing demand, Pan noted, noting that the price increases will sustain for a more extended period only when demand is solid enough to soak up the output.

It is worth observing whether the sales of consumer electronics products during the forthcoming year-end shopping season in China, the US and Europe are robust enough to stir up panel demand in the first quarter of 2023, Pan commented.

Prices for all TV panel sizes fluctuated and are forecast to fluctuate between 2020 and 2022. The period from March 2020 to July 2021 saw the biggest price increases, when a 65" UHD panel cost between 171 and 288 U.S. dollars. In the fourth quarter of 2021, such prices fell and are expected to drop to an even lower amount by March 2022.Read moreLCD TV panel prices worldwide from January 2020 to March 2022, by size(in U.S. dollars)Characteristic32" HD43" FHD49"/50" UHD55" UHD65" UHD------

DSCC. (January 10, 2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) [Graph]. In Statista. Retrieved December 15, 2022, from https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars)." Chart. January 10, 2022. Statista. Accessed December 15, 2022. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. (2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars). Statista. Statista Inc.. Accessed: December 15, 2022. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "Lcd Tv Panel Prices Worldwide from January 2020 to March 2022, by Size (in U.S. Dollars)." Statista, Statista Inc., 10 Jan 2022, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC, LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) Statista, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/ (last visited December 15, 2022)

We believe that panel prices will close this year on a decline, expecting LCD panel prices to slip from the start of the holiday shopping season in November. China’s LCD industry appears to now be entering its heyday. Going forward, Chinese panel makers are likely to offer low panel prices to set makers as it is essential to establish an entry barrier as they enter the oligopoly stage.

In 3Q20, LCD panel prices rose as set makers increased their panel purchases in preparation for end-year holiday shopping (Black Friday in the US, the Gwanggun Festival in China, etc). We estimate that major TV set makers’ panel purchases climbed 34% q-q during the quarter, exceeding 50mn units. In 3Q20, we believe that on an area basis, LCD demand expanded around 10% q-q, exceeding supply growth of about 8% q-q. However, with low seasonality to be in play on both the supply side and the demand side, the uptrend in LCD panel prices is unlikely to sustain in 4Q20. Although it is difficult to predict the exact timing of the decline in panel prices, they are highly likely to begin falling from the start of the holiday shopping season in November. Expecting the likely 4Q20 drop in LCD demand to surpass the decrease in supply, we estimate that LCD demand will fall around 5% q-q, with supply growth to narrow 2% q-q.

The global LCD industry appears to have entered an oligopolistic phase centered upon China. This oligopoly is being accompanied by a decrease in the number of LCD makers. In fact, China Star acquired Samsung Display’s Suzhou LCD facility in Aug 2020, and BOE acquired CEC Panda in Sep 2020. Moreover, Chinese players are known to be planning to continue expanding capacity and making new investments with the aim of increasing their M/Ss. Of particular note, the combined global market share (by production capacity) of China Star and BOE is projected to climb from 34% this year to 40% in 2021.

In addition, Chinese makers are expected to lower their LCD panel prices, in turn leading to set makers’ appetite for Chinese-made LCDs. We view such price cuts as being essential for Chinese makers if they are to build high entry barriers now that they have reached the oligopoly stage.

LCD panel prices have risen for 4 months in a row because of your home gaming? Since this year, the whole LCD panel market has smoked. Whether after the outbreak of the epidemic, LCD panel market prices rose for four months, or the panel giants in Japan and South Korea successively sold production lines, or the Chinese mainland listed companies frequently integrated acquisition, investment, and plant construction, all make the industry full of interesting.

LCD panel prices are already a fact. Since May this year, LCD panel prices have risen for four months in a row, making the whole industry chain dynamic. Why are LCD panels going up in price in a volatile 2020? The key factor lies in the imbalance between supply and demand.

For larger sizes, overseas stocks remained strong, with prices for 65 inches and 75 inches rising $10 on average to $200 and $305 respectively in September.

The price of LCDS for large-size TVs of 70 inches or more hasn’t budged much. In addition, LTPS screens and AMOLED screens used in high-end phones have seen little or no increase in price.

As for October, LCD panel price increases are expected to moderate. The data shows that in October 32 inches or 2 dollars; Gains of 39.5 to 43 inches will shrink to $3;55 inches will fall back below $10; The 65-inch gain will narrow to $5.

During the epidemic, people stayed at home and had no way to go out for entertainment. They relied on TV sets, PCS, and game consoles for entertainment. After the resumption of economic work and production, the market of traditional home appliances picked up rapidly, and LCD production capacity was quickly digested.

However, due to the shutdown of most factories lasting 1-2 months during the epidemic period, LCD panel production capacity was limited, leading to insufficient production capacity in the face of the market outbreak, which eventually led to the market shortage and price increase for 4 consecutive months.

In fact, the last round of price rise of LCD panels was from 2016 to 2017, and its overall market price has continued to fall since 2018. Even in 2019, individual types have fallen below the material cost, and the whole industry has experienced a general operating loss. As a result, LCD makers have been looking for ways to improve margins since last year.

A return to a reasonable price range is the most talked about topic among panel makers in 2019, according to one practitioner. Some manufacturers for the serious loss of the product made the decision to reduce production or even stop production; Some manufacturers planned to raise the price, but due to the epidemic in 2020, the downstream demand was temporarily suppressed and the price increase was postponed. After the outbreak was contained in April, LCD prices began to rise in mid-to-late May.

This kind of price correction is in line with the law of industrial development. Only with reasonable profit space can the whole industry be stimulated to move forward.

In fact, the market price of LCD panels continued to decline in 2018-2019 because of the accelerated rise of China’s LCD industry and the influx of a large number of local manufacturers, which doubled the global LCD panel production capacity within a few years, but there was no suitable application market to absorb it. The result of excess capacity is oversupply, ultimately making LCD panel prices remain depressed.

Against this background, combined with the impact of the epidemic in 2020, the operating burden of LCD companies in Japan and South Korea has been further aggravated, and it is difficult to make profits in the production of LCD panels, so they have to announce the withdrawal of LCD business.

business in June 2022. In August, Sharp bought JDI Baishan, a plant in Ishikawa prefecture that makes liquid crystal display panels for smartphones. In early September, Samsung Display sold a majority stake in its SUZHOU LCD production plant to Starlight Electronics Technology, a unit of TCL Technology Group. LGD has not only pulled out of some of its production capacity but has announced that it will close its local production line in 2020. According to DSCC, a consultancy, the share of LCD production capacity in South Korea alone will fall from 19% to 7% between 2020 and 2021.

It is worth mentioning that in industry analysis, in view of the fact that Korean companies are good at using “dig through old bonus – selling high price – the development of new technology” the cycle of development mode, another 2020 out of the LCD production capacity, the main reason may be: taking the advantage of China’s expanding aggressively LCD manufacturers, Korean companies will own LCD panel production line hot sell, eliminating capacity liquid to extract its final value, and turning to the more profitable advantage of a new generation of display technologies, such as thinner, color display better OLED, etc. Samsung, for example, has captured more than 80% of the OLED market with its first-mover advantage.

From the perspective of production capacity, the launch of LCD tracks by major manufacturers in Japan and South Korea must reduce some production capacity in the short term, which to some extent induces market price fluctuations. In the long run, some of the Japanese and Korean LCD production capacity has been bought by Chinese manufacturers, coupled with frequent investment in recent years, the overall capacity is sure to recover as before, or even more than before. But now it will take time to expand the production layout, which more or less will cause supply imbalance, the industry needs to be cautious.

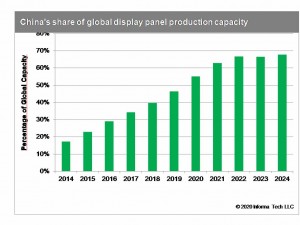

The LCD panel industry started in the United States and then gradually moved to Japan, South Korea, China, and Taiwan. At present, the proportion of production capacity in The Chinese mainland has reached 52% in 2020, and there are leading LCD panel products in China represented by BOE, Huxing Optoelectronics. Meanwhile, the production capacity layout of BOE, Huike, Huxing Optoelectronics, and other manufacturers has been basically completed, making industrial integration a necessity.

On the one hand, South Korean enterprises out of the LCD track, the domestic factory horse enclosure, plant expansion action. While LCDs may not sell as well as “upstart” flexible screens, respondents believe they are still strong enough in the traditional home appliance market to warrant continued investment. Zhao Bin, general manager of TCL Huaxing Development Center, has said publicly that the next-generation display technology will be mature in four to five years, but the commercialization of products may not take place until a decade later. “LCD will still be the mainstream in this decade,” he said.

On the other hand, there is no risk of neck jam in China’s LCD panel industry, which is generally controllable. In mainland China, there will be 21 production lines capable of producing 32-inch or larger LCD panels by 2021, accounting for about two-thirds of the global total. In terms of the proportion of production capacity, the Chinese mainland accounted for 42% of the global LCD panel in 2019, 51% this year, and will continue to climb to 63% next year.

Of course, building factories and expanding production cannot be accomplished overnight. In the process of production capacity recovery, it is predicted that there will be several price fluctuations, and the cost may be passed on to the downstream LCD panel manufacturers or consumers when the price rises greatly, which requires continuous attention.

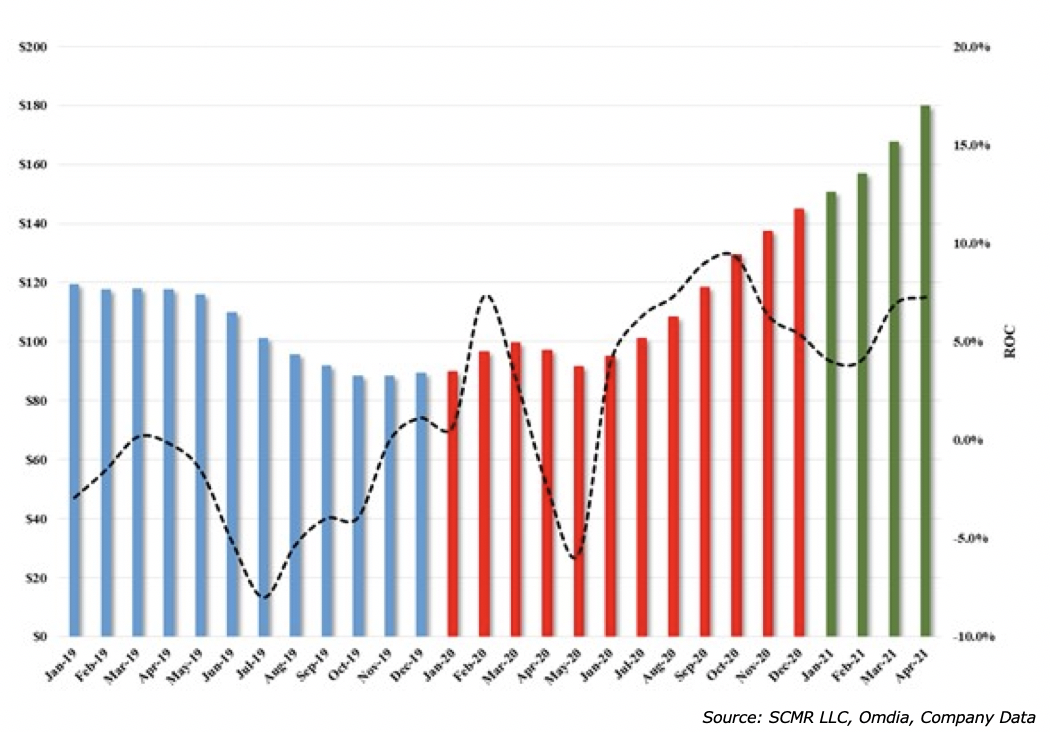

Large LCD panel prices have been continuously increasing for last 10 months due to an increase in demand and tight supply. This has helped the LCD industry to recover from drastic panel price reductions, revenue and profit loss in 2019. It has also contributed to the growth of Quantum Dot and MiniLED LCD TV.

Strong LCD TV panel demand is expected to continue in 2021, but component shortages, supply constraints and very high panel price increase can still create uncertainties.

LCD TV panel capacity increased substantially in 2019 due to the expansion in the number of Gen 10.5 fabs. After growth in 2018, LCD TV demand weakened in 2019 caused by slower economic growth, trade war and tariff rate increases. Capacity expansion and higher production combined with weaker demand resulted in considerable oversupply of LCD TV panels in 2019 leading to drastic panel price reductions. Some panel prices went below cash cost, forcing suppliers to cut production and delay expansion plans to reduce losses.

Panel over-supply also brought down panel prices to way lower level than what was possible through cost improvement. Massive 10.5 Gen capacity that can produce 8-up 65" and 6-up 75" panels from a single mother glass substrate helped to reduce larger size LCD TV panel costs. Also extremely low panel price in 2019 helped TV brands to offer larger size LCD TV (>60-inch size) with better specs and technology (Quantum Dot & MiniLED) at more competitive prices, driving higher shipments and adoption rates in 2019 and 2020.

While WOLED TV had higher shipment share in 2018, Quantum Dot and MiniLED based LCD TV gained higher unit shares both in 2019 and 2020 according to Omdia published data. This trend is expected to continue in 2021 and in the next few years with more proliferation of Quantum Dot and MiniLED TVs.

Panel suppliers’ financial results suffered in 2019 as they lost money. Suppliers from China, Korea and Taiwan all lowered their utilization rates in the second half of 2019 to reduce over-supply. Very low prices combined with lower utilization rates made the revenue and profitability situation for panel suppliers difficult in 2019. BOE and China Star cut the utilization rates of their Gen 10.5 fabs. Sharp delayed the start of production at its 10.5 Gen fab in China. LGD and Samsung display decided to shift away from LCD more towards OLED and QDOLED respectively. Both companies cut utilization rates in their 7, 7.5 and 8.5 Gen fabs. Taiwanese suppliers also cut their 8.5 Gen fab utilization rates.

Some suppliers also shifted capacity away from TV to other applications. In summary, drastic price reduction resulted in a cut in utilization rates, delays in fab construction and ramp-ups and the closing down of older fabs, or conversion to OLED or QDOLED fabs. This helped to reduce oversupply.

An increase in demand for larger size TVs in the second half of 2020 combined with component shortages has pushed the market to supply constraint and caused continuous panel price increases from June 2020 to March 2021. Market demand for tablets, notebooks, monitors and TVs increased in 2020 especially in the second half of the year due to the impact of "stay at home" regulations, when work from home, education from home and more focus on home entertainment pushed the demand to higher level.

With stay at home continuing in the firts half of 2021 and expected UEFA Europe football tournaments and the Olympic in Japan (July 23), TV brands are expecting stronger demand in 2021. The panel price increase resulting in higher costs for TV brands. It has also made it difficult for lower priced brands (Tier2/3) to acquire enough panels to offer lower priced TVs. Further, panel suppliers are giving priority to top brands with larger orders during supply constraint. In recent quarters, the top five TV brands including Samsung, LG, and TCL have been gaining higher market share.

From June 2020 to January 2021, the 32" TV panel price has increased more than 100%, whereas 55" TV panel prices have increased more than 75% and the 65" TV panel price has increased more than 38% on average according to DSCC data. Panel prices continued to increase through Q1 and the trend is expected to continue in Q2 2021 due to component shortages.

In last few months top glass suppliers Corning, NEG and AGC have all experienced production problems. A tank failure at Corning, a power outage at NEG and an accident at an AGC glass plant all resulted in glass supply constraints when demand and production has been increasing. In March this year Corning announced its plan to increase glass prices in Q2 2021. Corning has also increased supply by starting glass tank in Korea to supply China’s 10.5 Gen fabs that are ramping up. Most of the growth in capacity is coming from Gen 8.6 and Gen 10.5 fabs in China.

Major increases in panel prices from June 2020, have increased costs and reduced profits for TV brand manufacturers. TV brands are starting to increase TV set prices slowly in certain segments. Notebook brands are also planning to raise prices for new products to reflect increasing costs. Monitor prices are starting to increase in some segments. Despite this, buyers are still unable to fullfill orders due to supply issues.

TV panel prices increased in Q4 2020 and are also expected to increase in the first half of 2021. This can create challenges for brand manufacturers as it reduces their ability to offer more attractive prices in coming months to drive demand. Still, set-price increases up to March have been very mild and only in certain segments. Some brands are still offering price incentives to consumers in spite of the cost increases. For example, in the US market retailers cut prices of big screen LCD and OLED TV to entice basketball fans in March.

Higher LCD price and tight supply helped LCD suppliers to improve their financial performance in the second half of 2020. This caused a number of LCD suppliers especially in China to decide to expand production and increase their investment in 2021.

New opportunities for MiniLED based products that reduce the performance gap with OLED, enabling higher specs and higher prices are also driving higher investment in LCD production. Suppliers from China already have achieved a majority share of TFT-LCD capacity.

BOE has acquired Gen 8.5/8.6 fabs from CEC Panda. ChinaStar has acquired a Gen 8.5 fab in Suzhou from Samsung Display. Recent panel price increases have also resulted in Samsung and LGD delaying their plans to shut down LCD production. These developments can all help to improve supply in the second half of 2021. Fab utilization rates in Taiwan and China stayed high in the second half of 2020 and are expected to stay high in the first half of 2021.

Price increases for TV sets are still not widespread yet and increases do not reflect the full cost increase. However, if set prices continue to increase to even higher levels, there is the potential for an impact on demand.

QLED and MiniLED gained share in the premium TV market in 2019, impacting OLED shares and aided by low panel prices. With the LCD panel price increases in 2020 the cost gap between OLED TV and LCD has gone down in recent quarters.

OLED TV also gained higher market share in the premium TV market especially sets from LG and Sony in the last quarter of 2020, according to industry data. LG Display is implimenting major capacity expansion of its OLED TV panels with its Gen 8.5 fab in China.Strong sales in Q4 2020 and new product sizes such as 48-inch and 88-inch have helped LG Display’s OLED TV fabs to have higher utilization rates.

Samsung is also planning to start production of QDOLED in 2021. Higher production and cost reductions for OLED TV may help OLED to gain shares in the premium TV market if the price gap continues to reduce with LCD.

Lower tier brands are not able to offer aggressive prices due to the supply constraint and panel price increases. If these conditions continue for too long, TV demand could be impacted.

Strong LCD TV demand especially for Quantum Dot and MiniLED TV is expected to continue in 2021. The economic recovery and sports events (UEFA Europe footbal and the Olympics in Japan) are expected to drive demand for TV, but component shortages, supply constraints and too big a price increase could create uncertainties. Panel suppliers have to navigate a delicate balance of capacity management and panel prices to capture the opportunity for higher TV demand. (SD)

Chinese manufacturers are expected to raise their market share from 39% this year to 52% next year in the monitor panel market, and 36% to 39% in the notebook panel market

Chinese manufacturers are expected to raise their market share from 39% this year to 52% next year in the monitor panel market, and 36% to 39% in the notebook panel market, according to TrendForce’s preliminary shipment forecast of panel makers for 2021. As such, these manufacturers are expected to maintain their plans of transitioning some production capacities from TV panel manufacturing to IT panel manufacturing in spite of the TV panel shortage in 2H20 caused by various factors such as the closedown of SDC’s LCD panel manufacturing operations, the rise of the stay-at-home economy, and the stimulus policies instituted by governments worldwide.

TrendForce indicates that, with regards to the standing of Chinese manufacturers in the IT panel industry, BOE has long established itself as the market leader, while CSOT and HKC are each also catching up fast. After acquiring SDC’s Suzhou-based Gen 8.5 fab, CSOT will possess even more production capacities for monitor panels. At the same time, HKC currently maintains three Gen 8.6 fabs, located in Chongqing, Chuzhou, and Mianyang, and plans to capture additional shares in the monitor panel and notebook panel markets.

Chinese panel makers have been gradually transitioning their current panel capacities to monitor panel production. Most significantly, as more Gen 10.5 production lines become available, TV panel production will most likely take place in Gen 10.5 fabs instead of Gen 8.5 fabs in the future, while the existing Gen 8.5 and Gen 8.6 production lines will be reallocated to monitor panel production in order to expend the excess capacity made available after TV panel production moves to Gen 10.5 fabs. In addition, after SDC’s forecasted closing of LCD panel manufacturing operations at the end of this year, CSOT and HKC will look to capture the resultant supply share of SDC’s absence in the market. On the other hand, since both TCL, which is CSOT’s parent company, and HKC possess monitor ODM operations, should the two companies decide to vertically integrate by making panels for their own monitor products, they will be able to effectively optimize their cost structures.

Although CSOT’s Wuhan-based T3 LTPS Gen 6 production line is primarily dedicated to smartphone and notebook panel manufacturing, the considerable reduction of LTPS smartphone panel demand from Huawei caused by U.S. sanctions means CSOT is expected to make plans for an increase in notebook panel shipment in order to make up for the shortfall. As well, thanks to high demand for TV panels this year, HKC’s production lines have been operating at maximum capacity utilization rates, in turn slowing down its notebook panel business. However, in light of the fact that the COVID-19 pandemic has brought about a rapid surge in TN notebook panel demand, HKC is therefore looking to TN panels as a new commercial opportunity in the notebook display market and subsequently prioritizing TN panel development over IPS panel development as its product strategy. Not only will this reprioritization allow HKC to align its strategy with the current market trend, but it will also quickly raise the yield rate of HKC’s Mianyang-based fab, which had never manufactured NB panels, by instead having the fab manufacture TN panels, which have a relatively simpler manufacturing process.

TrendForce analyst Jeff Yang indicates that, despite Chinese panel makers’ strong intention to enter the IT panel manufacturing business, success in the IT panel market is not solely decided by a company’s production capacity. For instance, with regards to monitor panels, CSOT’s technical competency is mostly focused on VA panels, meaning the company is constrained in its product mixes due to its lack of mainstream IPS offerings. Although HKC is equipped with both IPS and VA technologies, it lacks experience in manufacturing curved VA panels, leading its clients to take on a wait-and-see approach before placing additional orders. For notebook panels, although CSOT is primarily focusing on the mid-range and high-end LTPS notebook panel market, it faces intense competition from Samsung’s OLED notebook panels, which are gradually extending from the high-end segment to the mid-range segment as well. Likewise, HKC will have to take time in order to make headways in the notebook panel market, since it has not reached any production milestones, and it requires time to cultivate a significant client base.

Flat-panel displays are thin panels of glass or plastic used for electronically displaying text, images, or video. Liquid crystal displays (LCD), OLED (organic light emitting diode) and microLED displays are not quite the same; since LCD uses a liquid crystal that reacts to an electric current blocking light or allowing it to pass through the panel, whereas OLED/microLED displays consist of electroluminescent organic/inorganic materials that generate light when a current is passed through the material. LCD, OLED and microLED displays are driven using LTPS, IGZO, LTPO, and A-Si TFT transistor technologies as their backplane using ITO to supply current to the transistors and in turn to the liquid crystal or electroluminescent material. Segment and passive OLED and LCD displays do not use a backplane but use indium tin oxide (ITO), a transparent conductive material, to pass current to the electroluminescent material or liquid crystal. In LCDs, there is an even layer of liquid crystal throughout the panel whereas an OLED display has the electroluminescent material only where it is meant to light up. OLEDs, LCDs and microLEDs can be made flexible and transparent, but LCDs require a backlight because they cannot emit light on their own like OLEDs and microLEDs.

Liquid-crystal display (or LCD) is a thin, flat panel used for electronically displaying information such as text, images, and moving pictures. They are usually made of glass but they can also be made out of plastic. Some manufacturers make transparent LCD panels and special sequential color segment LCDs that have higher than usual refresh rates and an RGB backlight. The backlight is synchronized with the display so that the colors will show up as needed. The list of LCD manufacturers:

Organic light emitting diode (or OLED displays) is a thin, flat panel made of glass or plastic used for electronically displaying information such as text, images, and moving pictures. OLED panels can also take the shape of a light panel, where red, green and blue light emitting materials are stacked to create a white light panel. OLED displays can also be made transparent and/or flexible and these transparent panels are available on the market and are widely used in smartphones with under-display optical fingerprint sensors. LCD and OLED displays are available in different shapes, the most prominent of which is a circular display, which is used in smartwatches. The list of OLED display manufacturers:

MicroLED displays is an emerging flat-panel display technology consisting of arrays of microscopic LEDs forming the individual pixel elements. Like OLED, microLED offers infinite contrast ratio, but unlike OLED, microLED is immune to screen burn-in, and consumes less power while having higher light output, as it uses LEDs instead of organic electroluminescent materials, The list of MicroLED display manufacturers:

LCDs are made in a glass substrate. For OLED, the substrate can also be plastic. The size of the substrates are specified in generations, with each generation using a larger substrate. For example, a 4th generation substrate is larger in size than a 3rd generation substrate. A larger substrate allows for more panels to be cut from a single substrate, or for larger panels to be made, akin to increasing wafer sizes in the semiconductor industry.

"Samsung Display has halted local Gen-8 LCD lines: sources". THE ELEC, Korea Electronics Industry Media. August 16, 2019. Archived from the original on April 3, 2020. Retrieved December 18, 2019.

"TCL to Build World"s Largest Gen 11 LCD Panel Factory". www.businesswire.com. May 19, 2016. Archived from the original on April 2, 2018. Retrieved April 1, 2018.

"Panel Manufacturers Start to Operate Their New 8th Generation LCD Lines". 대한민국 IT포털의 중심! 이티뉴스. June 19, 2017. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"TCL"s Panel Manufacturer CSOT Commences Production of High Generation Panel Modules". www.businesswire.com. June 14, 2018. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"Samsung Display Considering Halting Some LCD Production Lines". 비즈니스코리아 - BusinessKorea. August 16, 2019. Archived from the original on April 5, 2020. Retrieved December 19, 2019.

Herald, The Korea (July 6, 2016). "Samsung Display accelerates transition from LCD to OLED". www.koreaherald.com. Archived from the original on April 1, 2018. Retrieved April 1, 2018.

"China"s BOE to have world"s largest TFT-LCD+AMOLED capacity in 2019". ihsmarkit.com. 2017-03-22. Archived from the original on 2019-08-16. Retrieved 2019-08-17.

New York, Jan. 24, 2022 (GLOBE NEWSWIRE) -- Reportlinker.com announces the release of the report "Global and China Automotive LCD Cluster and Center Console Industry Report, 2021" - https://www.reportlinker.com/p06219667/?utm_source=GNW

The statistics from our automotive database show that in 2020 China shipped more than 35 million sets of passenger car displays (cluster, center console, entertainment display, HUD, etc.), up over 4% more than in the previous year.

Automotive display is a key booster to the digital transformation of automotive cockpits. The better performance of on-board computers enables the central computing unit to support LCD cluster, high-resolution infotainment display, HUD, electronic rearview mirror and other display systems, and provides technical support for multi-display systems.

From the new models launched in recent two years, it can be seen that large-size display and multi-screen display have been trends for automotive displays. High-end models have begun to pack at least 4 displays. Products like co-pilot seat entertainment display, control display, rear row entertainment display and streaming media rearview mirror have started finding application, and the demand for large-size displays has been soaring.

The installation of clusters shows that about 60% of new vehicles carry LCD clusters. In the first three quarters of 2021, 6.544 million LCD clusters were installed in passenger cars, a like-on-like spurt of 44.5%, of which 12.0-inch (incl.) to 13.0-inch (excl.) LCD clusters were most installed, up to 2.512 million units, up by 35.0%, and 10.0-inch (incl.) to 12.0-inch (excl.) LCD clusters grew at the fastest pace with the installations rocketing by 173.8% to 1.186 million units.

Cockpit electronics are heading in the direction of multi-display integration. Early in 2019, emerging carmakers have rolled out mass-produced models like LiXiang One and ENOVATE ME7 with 4 and even 5-screen displays. Traditional OEMs also step up efforts to deploy, having introduced multi-screen display products since 2020.

FAW Hongqi H9 unveiled in August 2020 bears dashboard, center console, and co-pilot seat entertainment displays, 2 rear row entertainment displays, and HUD. In addition, it also packs an electronic image acquisition and display system (i.e., streaming media rearview mirror) which consists of digital camera, image processing and high-definition digital display. The system uses the rear camera to project images onto the display, and displays them on the rearview mirror in digital format.

The soaring demand for vehicle displays give impetus to development of new vehicle display technologies. In current stage, a-Si TFT LCD still prevail in vehicle display market, but advanced display technologies such as LTPS TFT LCD, OLED, mini LED backlight and micro LED are making their way into the market.

The year of 2020 saw the start of production of automotive OLED. Due to high cost, OLED, often larger than 7.2 inches, is largely used in high-end models, with applications including cluster, center console and copilot seat entertainment displays. Suppliers are led by LGD, Samsung Display and BOE.

2021 Mercedes-Benz S-Class sedans differ greatly from the previous generations in application of displays, changing the original siamesed center console display into a large waterfall display, a 12.8-inch vertical waterfall OLED screen with resolution of 1888×1728. They also pack a glasses-free 3D full LCD dashboard, HUD and rear row entertainment display, which connect with each other.

Tianma Microelectronics: in 2020 it first outran JDI and became the world’s largest vehicle display company in terms of shipments. The company supplies through Tier1s, covering 92% of global customers (top 24 Tier1s) and 100% of Chinese brands (top 10).

China automotive display market (installation of LCD/HUD/center console/rear seat entertainment displays, display technologies of major suppliers, vehicle display installation schemes of major OEMs, etc.);

Chinese display panel makers accounted for nearly half of the share in the global liquid crystal display TV panel market in the first half of this year, dominating the industry.

Beijing-based market researcher Sigmaintell Consulting said shipments of LCD TV panels worldwide totaled 140 million pieces in the year"s first half, up 3.6 percent compared with the same period a year ago.

The supply of TV panels though has surpassed demand due to the slowdown in the global economy and weaker consumer purchasing power. Manufacturers are facing severe challenges from falling panel prices, the Sigmaintell report said.

The shipment of BOE"s LCD TV panels stood at 27.6 million in the Jan-June period while LG Display followed with 22.7 million, down 4.5 percent year-on-year. Innolux Display Group was in third place, having shipped 21.9 million units.

Shenzhen China Star Optoelectronics Technology Co Ltd, a subsidiary of consumer electronics giant TCL Corp, ranked fourth, shipping 19.3 million pieces of TV panels. Chinese panel makers accounted for a 45.8 percent share in the global LCD TV panel market.

Sigmaintell estimated that the gap between supply and demand would widen further, and the panel market may face a long-term risk of oversupply. The industry may have to undergo a reshuffle given fierce market competition, it said.

The panel makers must reduce costs, optimize their internal structures, promote technological innovation and explore more innovative applications, the report by the consultancy said.

Separately, BOE"s Gen 10.5 TFTLCD production line has entered operation in Hefei, Anhui province. The plant will produce high-definition LCD screens of 65 inches and above.

CSOT also announced in November last year that its Gen 11 TFT-LCD and active-matrix OLED production line had officially began operation. The project will produce 43-inch, 65-inch and 75-inch liquid crystal display screens.

China is expected to replace South Korea as the world"s largest flat-panel display producer in 2019, a report from the China Video Industry Association and the China Optics and Optoelectronics Manufacturers Association said.

"The average size of TV panels is likely to increase 1.4 inches in 2019. The 65-inch dimension will become the most popular size of TV," Li Yaqin, general manager of Sigmaintell, said while adding the 65-inch TV will become the mainstream screen in people"s living rooms in the future.

Compared with traditional LCD display panels, OLED has a fast response rate, wide viewing angles, high-contrast images and richer colors. It is thinner and can be made flexible.

Wen Jianping, president of All View Cloud, a Beijing-based consultancy specializing in home appliances, said the price of OLED TVs will continue to fall in the next two years, with sales rising to 380,000 units this year, and reaching 800,000 units in 2020.

China With a Production Capacity Share of 35.7% Will Supplant South Korea This Year as Top Producing Region for Large-Size LCD Panels, Says TrendForce

The latest analysis by WitsView, a division of TrendForce, reveals that China is set to overtake South Korea this year as the leading producing region for large-size LCD panels. In terms of area, China’s share of the global production capacity for large-size panels will surpass South Korea’s in 2017. By 2020, China’s share of the global capacity area may reach around 50%.

“Both domestic and foreign panel makers continue to build and expand their fabs in China because of the country’s enormous market and the financial support from the Chinese government, said Anita Wang, senior research manager of WitsView. “At the same time, the capacity share of South Korea has shrunk. Samsung Display (SDC) closed its Gen-7 fab L7-1 at the end of 2016, and both SDC and LG Display (LGD) have lowered their Gen-5 capacity.”

According to WitsView’s latest estimate, China’s share of global capacity area for large-size panels will reach 35.7% for 2017, up from 30.1% for 2016. Taiwan’s capacity share is projected to jump from 28.9% in 2016 to 29.8% in 2017, making the island the second-largest producing region. South Korea will slide down to third place in the 2017 capacity share ranking with 28.8%, a significant drop from its leading share of 34.1% in 2016.

With the South Korean panel makers lowering their production capacity, the global production capacity in area for large-size panels is estimated to reach 246.6 million square meters, representing an annual increase of just 1.3%. This year’s capacity area growth rate is also the lowest within the recent two- to three-year period. Over the next three years, however, six new Gen-10.5 fabs are expected to be in operation, and capacity area growth will again take off. WitsView forecast that the global capacity area for large-size panels will expand by 8% to 9% annually from 2018 and 2020, totaling around 317.8 million square meters per year by the end of the period.

Wang added: “Looking ahead, investments in production capacity among competing panel makers will reach a new level. Next year, a Gen-10.5 fab in Hefei, China, owned by BOE Technology (BOE) will be entering mass production, thus replacing Sharp’s Gen-10 fab in Japan’s Sakai as the world’s largest-generation panel fab. Nonetheless, other major panel makers are also planning to establish their own Gen-10.5 lines within the next several years.”

A survey of Gen-10.5 fabs that are under planning or construction shows that in China, domestic panel maker China Star Optoelectronics Technology (CSOT) will build a plant in Shenzhen, while BOE plans to set up another line in Wuhan. There is also a Gen-10.5 facility that is being built in Guangzhou by Sakai Display Products (SDP). In the U.S., the Wisconsin project that was announced by Foxconn is expected to include a Gen-10.5 line as well. As for South Korea, there are reports of LGD planning to build a plant Paju for processing Gen-10.5 glass substrates.

Comparatively, the area size of a piece of Gen-10.5 glass substrate is about 1.8 times as large as that of a piece of Gen-8.5 glass substrate. Given the size difference, the risk of oversupply for large-size panels is going to be much greater as more Gen-10.5 capacity becomes available.

WitsView points out that the panel industry over the past several years has worked to raise the demand for large-size TV sets as to help consume the production capacity of fabrication lines of larger generations. With more Gen-10.5 facilities entering mass production, the industry will be pushing panels sized 65 inches or larger as the main products for the TV market. There will also be corresponding promotional activities from panel makers and TV brands to have consumer demand concentrate on that ultra-large size range as well.

WitsView furthermore anticipates that panel makers with Gen-10.5 capacity will be under pressure to lower their prices, and this in turn will affect prices of panels that come from fabs of smaller generations. Currently, most 65-inch panels are made on Gen-6 lines, while 75-inch panels mainly roll out from Gen-7.5 lines. When the new Gen-10.5 fabs enter operation, products made in Gen-6 and Gen-7.5 plants will be facing intense price competition and have slimmer profit margins.

WitsView also notes that a few panel makers still have not invested in a Gen-10.5 fab due to the potential financial burden. Going forward, the generational divide in the manufacturing process will significantly influence the competition in the panel industry. However, the ability to adjust product mix quickly will be key to the survival of panel makers in the future as they encounter oversupply resulting from the capacity expansion.

WITH COVID‐19 INFECTIONS REPORTED IN MORE THAN 100 countries by early March 2020, the health crisis" impact on the display manufacturing industry was being felt well beyond Wuhan, China, where the first cases of the illness were reported.

Faced with a reduced workforce caused by travel bans and quarantine conditions, LCD and OLED fabrication plants (fabs) across China struggled to resume normal operations in early‐ to mid‐February. Chinese LCD fabs were only expected to have a capacity utilization of 70 to 75 percent for the month compared to a normal rate of 90 to 95 percent, according to research from Omdia Display.

The biggest impact is in LCD displays for TVs and notebook computers. By late 2019, the prolonged issue of LCD panel over‐supply driven by Chinese fabs had begun to reverse course as Korean manufacturers restructured their capacity, shutting down some fabs and converting others to OLED production. According to Hsieh, concerns about an LCD panel supply going forward already had spurred some TV manufacturers to increase orders, and now that LCD production in China is slowing as a result of the COVID‐19 outbreak, LCD panel makers are seeking sharp price increases from their original equipment manufacturer (OEM) customers, with a month‐to‐month jump of as much as 10 percent in some cases.

Omdia had originally forecast that the price for an open‐cell LCD TV panel was going to rise by $1 or $2 per month in February, but the actual increase may wind up being $3 to $5 for the month. “The problem is the coronavirus is coming so fast [that] the panel maker has been given a very good reason to increase the price radically,” Hsieh says. He also expects prices to increase for notebook displays, for which he predicts a 30–40 percent decrease in production for 2020"s first financial quarter (Q1), because of shortages in LCD modules.

While concerns over COVID‐19 caused the cancellation of the Mobile World Congress (MWC) tradeshow in Barcelona, Spain, the near‐term impact of the epidemic on smartphone display production appears to be minimal. Q1 production of smartphone displays is generally slow, notes Hsieh, with OEMs traditionally announcing new smartphone models at MWC, but not placing orders for displays until Q2 or Q3. And the bulk of OLED displays, which dominate the market for new high‐end phones, also are made by Korean manufacturers such as Samsung Display. Last year, Korean fabs shipped 433 million smartphone displays, while China was at 54 million. Hsieh said initial targets for 2020 were 476 million smartphone OLEDs shipped from Korea and 128 million from China, which would more than double China"s total from last year. Although the coronavirus will cause a “short‐term setback” for Chinese smartphone OLED makers, he still has a target of more than 100 million Chinese OLEDs.

In Wuhan itself, there are five major fabs, with four making smartphone displays. China Star and Tianma each operate a low‐temperature polycrystalline silicon LCD fab and a flexible OLED fab in the city, while BOE has a new Gen 10.5 LCD plant aimed at TV panels. Hsieh says that the China Star and Tianma OLED fabs are both in the ramping‐up stages, and the new BOE fab also is moving slowly. The biggest impact of COVID‐19 in Wuhan may be on the China Star Gen 6 OLED plant. Along with BOE, it"s slated to be a key supplier of flexible OLED panels for Lenovo"s new Motorola Razr foldable phone. “It"s unfortunate timing,” Hsieh says. —Glen Dickson

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey