future of lcd displays pricelist

One of the reasons Samsung decided to make the leap to OLED was because the price of LCD panels was going up so much., that it was worth betting on a technology that offers better quality and for the same money. But it seems that things are changing.

And it is that, in recent years the cost of LCD panels skyrocketed due to the production problems caused by the coronavirus, plus a notable increase in demand (people are at home, so the consumption of televisions increases). But the market is merciless, and has begun to regulate itself.

According to Display Supply Chain Consulting (DSCC), a renowned market research firm in the industry, the expected price of LCD TV panels this month was $ 38 for a 32-inch HD model. This is a 56.8% drop compared to June of last year at $ 88.

This impacted the user, sincethe price of this type of television increased significantly. And it was a turning point for Samsung, which saw how it had to stop its own LCD panel production as it could not compete with so many Chinese rivals. And this has been the reason why it has decided to take the leap and present its QD-OLED technology.

It should be noted that, as the DSCC has indicated in its report “In the fourth quarter of last year, the price fell the most compared to the previous quarter in the history of the flat panel display industry.This can translate into a very possible reduction in the price of LCD televisions, but that does not mean that it is the path that firms such as LG and Samsung will follow. Nothing is further from reality.

Samsung Display, which is estimated to account for around 4% of LCD TV panels in total sales, is also considering a plan to withdraw from business.. Samsung Display responded to a conference call in the third quarter of last year and said: “In a situation where prices for LCD panels are falling rapidly, we are internally reviewing whether to produce additional LCDs. ‘

The two Korean giants know that they cannot compete with Chinese companies that make LCD panels at lower prices. than the Samsung and LG factories. So they have decided to focus their efforts on OLED technology.

Kim Dong-won, a researcher at KB Securities, said: “Samsung’s new entry into the OLED TV market is an opportunity to expand and popularize the OLED ecosystem, and it will shake up the global market for supply and strategic partnership between the two. companies will expand from large LCD screens to OLED screens. ‘

LG is the only supplier of this type of panel, to the point that Samsung has preferred to give its arm to twist against its great rival and become LG’s largest customer, which makes it clear that the future of both brands is to be understood. And that Samsung is less and less interested in LCD technology.

Most modern computer monitors, and even televisions, have an edge-lit LCD display that’s fundamentally similar to the first such displays sold decades ago, but that’s not where the future is headed. The twin threats of Mini-LED and OLED want to conquer the world of PC displays for themselves.

Which will win, and where is the future headed? I spoke with Ross Young, CEO of Display Supply Chain Consultants, and David Wyatt, CTO of Pixel Display (and inventor of Nvidia G-Sync), for the inside scoop.

Modern OLED displays rarely exceed 1,000 nits of brightness, and when they do, are incapable of sustaining it. LG’s C9 OLED television, for example, can’t sustain a peak brightness above 160 nits (according to testing by Rtings). Mini-LED displays like Apple’s Liquid Retina XDR, Samsung’s Odyssey Neo G9, and Samsung’s QN90A television can hit peak brightness well above 1,000 nits and sustain at least 600 nits.

Wyatt points to this as a key advantage. The best HDR standards call for up to 10,000 nits of brightness. Current consumer Mini-LED displays don’t achieve this, but it’s possible future displays will.

And Micro-LED, which uses individual LEDs as per-pixel lighting elements, can reach even greater heights. Wyatt says his company’s VividColor NanoBright technology will be capable of reaching up to one million nits.

Such brightness is not necessary for computer monitors or home televisions and instead targets demanding niche components, such as avionics displays. Still, it hints that we’ve only seen a sliver of HDR’s real potential – and that Mini-LED and Micro-LED, not OLED, will lead the charge.

OLED’s greatest strength is the opposite of Mini-LED’s incredible brightness. The self-emissive nature of OLED means each pixel can be turned on or off individually, providing a deep, inky, perfect black level.

“Mini-LED has clear advantages in sources of supply and brightness,” Young said in an email, “but OLEDs have advantages in regards to contrast, particularly off-axis contrast, response times, and no halo effect.” The “halo effect,” also known as blooming, is the halo of luminance that often surrounds bright objects on a Mini-LED display.

The advantages of OLED add up to superior contrast and depth. You’ve likely noticed this when viewing an OLED television at your local retailer. High-quality content has an almost three-dimensional look, as if the display is not a flat panel but a window into another world.

Modern Mini-LED displays often claim to rival OLED. Apple’s Liquid Retina Display XDR, for example, lists a maximum contrast ratio of 1,000,000:1. In reality, Mini-LED still noticeably lags the contrast performance of OLED because it can’t light pixels individually. This will remain true at least until Micro-LED, which can light pixels individually, goes mainstream.

Mini-LED improves on traditional edge-lit LCD displays by improving the backlight. The LCD panel itself, however, is much the same as before and retains some flaws common to the technology.

Display quality can shift significantly depending on viewing angle, and significant blur will be visible when displaying fast motion. Both problems are inherent to LCD technology. The liquid crystals do not block light uniformly, so the image looks different from different angles, and require a few milliseconds to respond to a charge, causing blur or ghosting in rapidly changing images.

OLED is different from LCD technology. There’s no liquid crystals to twist or move. Each pixel is an organic element that creates its own light when a charge is applied. The light is emitted in a relatively uniform pattern and can turn on or off extremely quickly, removing the viewing angle and motion performance issues of LCD entirely.

The last few points—contrast, black levels, viewing angles, and response times—highlight the strengths of OLED technology. But, OLED has a weakness: durability.

This problem is most often discussed in the context of burn-in or image retention. Burn-in happens when specific pixels on an OLED panel degrade differently from those around them, creating a persistent shadow in the image.

Want to see the effects yourself? I recommend Rting’s burn-in testing page, which shows results over a period of eight years (though, unfortunately, Rtings has not updated its result since February of 2020). This testing shows OLED degradation is indeed a thing, though its severity depends on how you use your display.

Monitor pricing remains a sore point for PC enthusiasts. As explained in my deep-dive on upcoming OLED monitors, pricing is tied to the efficiency of production.

This advantage will likely continue in the near future. OLED pricing is reliant on availability of OLED panels, which are not as widely produced as LCD panels. Companies looking to build Mini-LED displays can design the backlight somewhat independently of the LCD panel and choose panels as needed based on the panel’s capabilities and pricing.

Because of this, there’s more ways for manufacturers to deliver Mini-LED displays in notebooks and monitors, which may lead to a more aggressive reduction in price.

The current OLED vs. Mini-LED battle is give-and-take. Mini-LED wins in brightness, HDR, durability, and pricing (of full-sized monitors). OLED wins in contrast, black levels, viewing angles, and motion performance.

OLED’s big break may come with the introduction of new fabs. Young says they will “lower costs significantly for 10-inch to 32-inch panels, giving OLED fabs the same flexibility as G8.5 LCD fabs, meaning the ability to target multiple applications from a single fab.” The first of these new fabs should start producing panels by 2024.

Affordable OLED seems alluring, but Wyatt champions a different approach. He believes the Micro-LED technology championed by Pixel Display will meld the strengths of LCD and OLED while ditching the weaknesses of both.

However, Micro-LED is a technology more relevant to the latter half of this decade. The more immediate fight will see OLED attempt to improve brightness and durability while Mini-LED pursues increasingly sophisticated backlights to mimic the contrast of OLED.

Personally, I think Mini-LED shows more promise—when it comes to PC displays, at least. The static images, long hours, and sustained brightness of Mini-LED displays pinches on OLED pain points, which will remain even if pricing becomes more affordable.

Since no backlight is used, the display requires very little energy in order to operate. This means: a lot of money can be saved over time. Think about the costs of a drive thru menu that stays running all year for sixteen whole hours a day. Those costs add up. Can you imagine spending $20k a year – just to power your display? That would cut your profits in a very noticeable way. So, I bet you’d be pretty pleased to find such a low-energy alternative.

Reflective displays really are a unique thing. You don’t have to hide them from the sun. You don’t have to shield your screen with your hand in order to eliminate glare. You don’t have to tilt it at funny angles that cause your neck to throb in pain, just so that you can read what’s on the screen. Funny, because those are our natural reactions whenever LCD and sunlight combine. Not with a reflective display though.

You could almost compare a reflective display to a piece of paper in the way that it becomes more visible when light is shining directly on it. It’s really bizarre to see, and you almost have to witness it in order to wrap your head around it, because it’s totally unlike what you’re used to.

AfghanistanAlbaniaAlgeriaAmerican SamoaAndorraAngolaAnguillaAntigua and BarbudaArgentinaArmeniaArubaAscensionAustraliaAustriaAzerbaijanBahamasBahrainBangladeshBarbadosBelarusBelgiumBelizeBeninBermudaBhutanBoliviaBosnia-HercegovinaBotswanaBrazilBritish Indian Ocean TerritoryBruneiBulgariaBurkina FasoBurundiCambodiaCameroonCanadaCape VerdeCayman IslandsCentral African RepublicChadChileChinaChristmas IslandCocos (Keeling) IslandsColombiaComorosCongoCongo, Dem Rep ofCook IslandsCosta RicaCroatiaCubaCyprusCzech RepublicDenmarkDjiboutiDominicaDominican RepublicEast TimorEcuadorEgyptEl SalvadorEquatorial GuineaEritreaEstoniaEthiopiaFalkland IslandsFaroe IslandsFijiFinlandFranceFrench GuianaFrench PolynesiaFrench Southern TerritoriesGabonGambiaGeorgiaGermanyGhanaGibraltarGreeceGreenlandGrenadaGuadeloupeGuamGuatemalaGuineaGuinea-BissauGuyanaHaitiHeard Island and McDonald IsHondurasHungaryIcelandIndiaIndonesiaIranIraqIrelandIsraelItalyIvory CoastJamaicaJapan 曰本JordanKazakhstanKenyaKirgizstanKiribatiKosovoKuwaitLaosLatviaLebanonLeeward IslesLesothoLiberiaLibyaLiechtensteinLithuaniaLuxembourgMacauMacedonia, FYRMadagascarMalawiMalaysiaMaldivesMaliMaltaMarshall IslandsMartiniqueMauritaniaMauritiusMayotteMexicoMicronesia, Fed States ofMoldovaMonacoMongoliaMontenegroMontserratMoroccoMozambiqueMyanmarNamibiaNauruNepalNetherlandsNetherlands AntillesNew CaledoniaNew ZealandNicaraguaNigerNigeriaNorfolk IslandNorth KoreaNorthern Mariana IslandsNorwayOmanPakistanPalauPalestinePanamaPapua New GuineaParaguayPeruPhilippinesPitcairn IslandPolandPortugalPuerto RicoQatarReunionRomaniaRussiaRwandaST MartinSaint HelenaSaint Kitts and NevisSaint LuciaSaint Vincent and GrenadinesSamoaSao Tome and PrincipeSaudi ArabiaSenegalSerbiaSeychellesSierra LeoneSlovakiaSloveniaSolomon IslandsSomaliaSouth AfricaSouth GeorgiaSpainSri LankaSudanSurinameSwazilandSwedenSwitzerlandSyriaTaiwanTajikistanTanzaniaThailandTogoTokelauTongaTrinidad and TobagoTunisiaTurkeyTurkmenistanTurks and Caicos IslandsTuvaluUS Minor Outlying IsUgandaUkraineUnited Arab EmiratesUnited KingdomUruguayUzbekistanVanuatuVenezuelaVietnamVirgin Islands, BritishVirgin Islands, USWallis and FutunaYemenZambiaZimbabwe

Some panel makers have raised LCD monitor panel prices for January, marking an end (perhaps temporarily) of continually lower price points on the retail level.

Both LCD TV and LCD computer prices are expected to be flat this month, bringing to a halt a trend of falling prices that has occurred over the past six months, according to analyst David Hsieh of DisplaySearch. But the leveling of panel prices right now is not because of any surge in demand over the recent holiday season, but for other reasons, including the fact that panel makers are holding “capacity utilization to low levels, and some plan to cut production further in January,” said Hsieh in a new study.

Panel makers, he said, also are rejecting some orders because LCD panel prices are lower than their cash costs—what the analyst refers to as “BTTO” (Build To Tolerable Orders).

Also, because there has been a reduction in orders by retailers and wholesalers over the past six months, LCD TV and PC makers consequently have low inventories, and for some sizes (mostly large PC monitor panels) there are some shortages.

The DisplaySearch report concludes that panel makers are expecting the panel prices paid by manufacturers to rebound at least back to the cash-cost level sometime in 2009.

In January 2010, Taiwanese AU Optronics Corporation (AUO) announced that it had acquired assets from Sony"s FET and FET Japan, including "patents, know-how, inventions, and relevant equipment related to FED technology and materials".Nikkei reported that AUO plans to start mass production of FED panels in the fourth quarter of 2011, however AUO commented that the technology is still in the research stage and there are no plans to begin mass production at this moment.

IMOD displays are now available in the commercial marketplace. QMT"s displays, using IMOD technology, are found in the Acoustic Research ARWH1 Stereo Bluetooth headset device, the Showcare Monitoring system (Korea), the Hisense C108,Freestyle Audio and Skullcandy. In the mobile phone marketplace, Taiwanese manufacturers Inventec and Cal-Comp have announced phones with Mirasol displays, and LG claims to be developing "one or more" handsets using Mirasol technology. These products all have only 2-color (black plus one other) "bi-chromic" displays. UniPixel"s TMOS and Pixtronix"s DMS display technologies utilize vertically and horizontally moving MEMS structures to modulate a backlight, respectively.

The technology is still in its nascent stages, and the project is unusual for Microsoft, which is not in the display business. There is a possibility that Microsoft will collaborate with a display manufacturer, but commercial production will not begin until at least 2013.

Although MicroLED displays have not been mass-produced for home use, after pioneering the technology in 2012,China Star Optoelectronics Technology (CSoT) demonstrated a 3.3" transparent microLED display with around 45% transparency, also co-developed with PlayNitride.Plessey Semiconductors Ltd demonstrated a GaN-on-Silicon wafer to CMOS backplane wafer bonded native Blue monochrome 0.7" active-matrix microLED display with an 8-micron pixel pitch.Ostendo Technologies, Inc. demonstrated a vertically integrated LED that can emit light from red to blue, including white – from a monolithic InGaN-based LED device.

Many expect that quantum dot display technology can compete or even replace liquid crystal displays (LCDs) in near future, including the desktop and notebook computer spaces and televisions. These initial applications alone represent more than a $8-billion addressable market by 2023 for quantum dot-based components. Other than display applications, several companies are manufacturing QD-LED light bulbs; these promise greater energy efficiency and longer lifetime.

It may seem odd in the face of stalled economies and stalled AV projects, but the costs of LCD display products are on the rise, according to a report from Digital Supply Chain Consulting, or DSCC.

Demand for LCD products remains strong , says DSCC, at the same time as shortages are deepening for glass substrates and driver integrated circuits. Announcements by the Korean panel makers that they will maintain production of LCDs and delay their planned shutdown of LCD lines has not prevented prices from continuing to rise.

I assume, but absolutely don’t know for sure, that panel pricing that affects the much larger consumer market must have a similar impact on commercial displays, or what researchers seem to term public information displays.

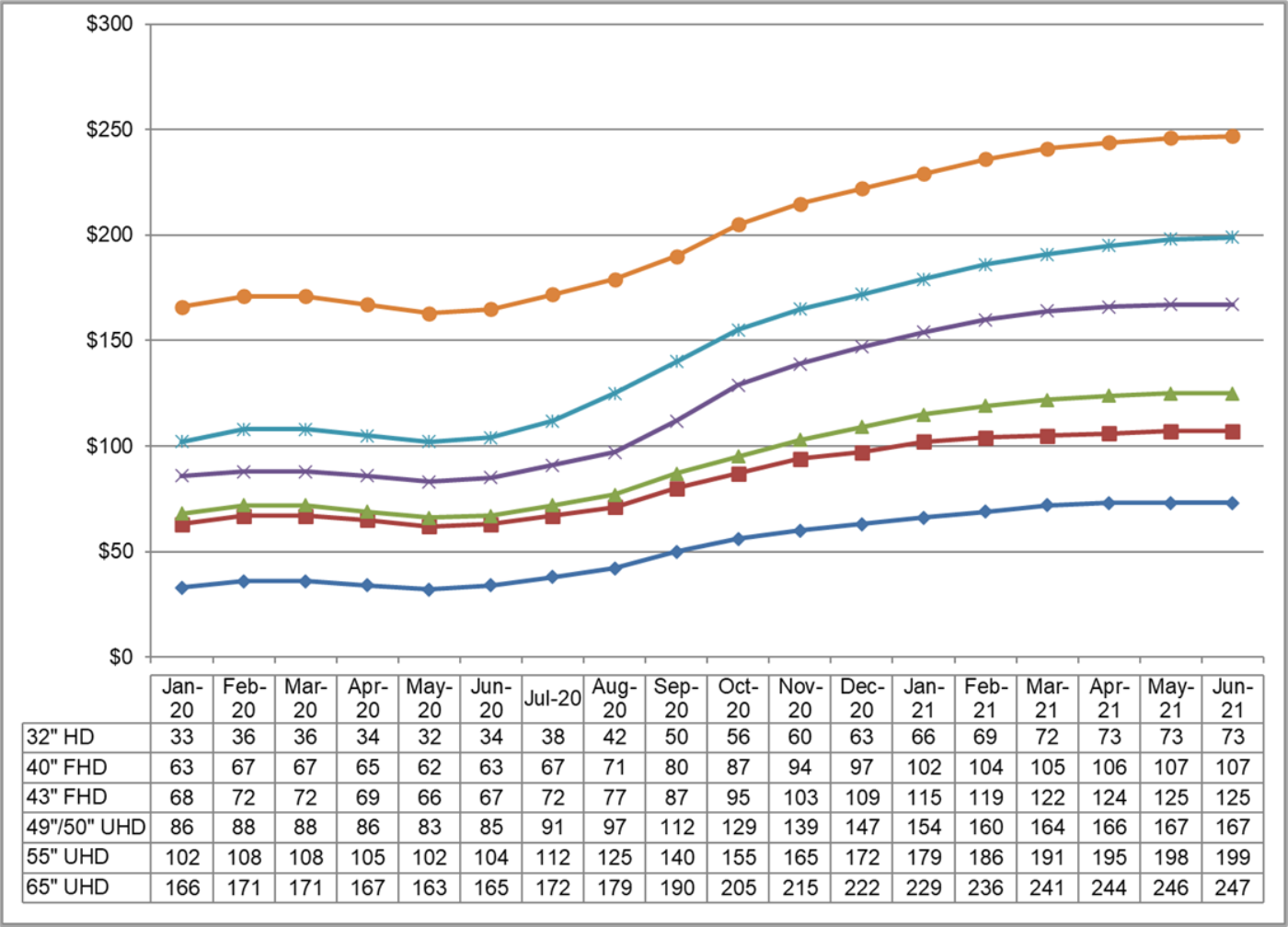

Panel prices increased more than 20% for selected TV sizes in Q3 2020 compared to Q2, and by 27% in Q4 2020 compared to Q3, we now expect that average LCD TV panel prices in Q1 2021 will increase by another 12%.

The first chart shows our latest TV panel price update, with prices increasing across the board from a low in May 2020 to an expected peak in May/June of this year. Last month’s update predicted a peak in February/March. However, our forecast for the peak has been increased and pushed out after AGC reported a major accident at a glass plant in Korea and amid continuing problems with driver IC shortages.

The inflection point for this cycle, the month of the most significant M/M price increases, was passed in September 2020, and the price increases have been slowing down each month since then, but the January increase averaged 4.1%. Prices in February 2021 have reached levels last seen exactly three years ago in February 2018.

Prices increased in Q4 for all sizes of TV panels, with massive percentage increases in sizes from 32” to 55” ranging from 28% to 38%. Prices for 65” and 75” increased at a slower rate, by 19% and 8% respectively, as capacity has continued to increase on those sizes with Gen 10.5 expansions.

Prices for every size of TV panel will increase in Q1 at a slower rate, ranging from 5% for 75” to 16% for 43”, and we now expect that prices will continue to increase in Q2, with the increases ranging from 3% to 6% on a Q/Q basis. We now expect that prices will peak in Q2 and will start to decline in Q3, but the situation remains fluid.

All that said, LCD panels are way less costly, way lighter and slimmer, and generally look way better than the ones being used 10 years ago, so prices is a relative problem.

As consumers expectations for televisions increase, panel makers are utilizing technology and process improvements to design brighter, higher resolution, and larger displays.

For example, panel makers are economically achieving 8K resolution with backplanes that seemed impossible only a few years ago, such as oxide TFTs. And to improve the color and light output of LCD TVs, panel makers are using increasingly advanced quantum dot films to augment traditional LCD designs, as seen in QLED sets.

In the past few years, the global center of LCD panel manufacturing has shifted from Korea to China. The shift was somewhat expedited because of COVID-19, but this dynamic did not happen overnight.

Korean panel manufacturers adjusted to industry and macroeconomic dynamics by sourcing LCD panels from other locations and turning their resources toward next-generation display technologies.

Ultimately, what drives end-market demand drives glass demand – which is what we at Corning are focused on. As we continue to expand glass capacity, with supply agreements for three out of four announced Gen 10.5 plants, Corning is well positioned to support our customers’ market growth.

Samsung Display will stop producing LCD panels by the end of the year. The display maker currently runs two LCD production lines in South Korea and two in China, according to Reuters. Samsung tells The Verge that the decision will accelerate the company’s move towards quantum dot displays, while ZDNetreports that its future quantum dot TVs will use OLED rather than LCD panels.

The decision comes as LCD panel prices are said to be falling worldwide. Last year, Nikkei reported that Chinese competitors are ramping up production of LCD screens, even as demand for TVs weakens globally. Samsung Display isn’t the only manufacturer to have closed down LCD production lines. LG Display announced it would be ending LCD production in South Korea by the end of the 2020 as well.

Last October Samsung Display announced a five-year 13.1 trillion won (around $10.7 billion) investment in quantum dot technology for its upcoming TVs, as it shifts production away from LCDs. However, Samsung’s existing quantum dot or QLED TVs still use LCD panels behind their quantum dot layer. Samsung is also working on developing self-emissive quantum-dot diodes, which would remove the need for a separate layer.

Although Samsung Display says that it will be able to continue supplying its existing LCD orders through the end of the year, there are questions about what Samsung Electronics, the largest TV manufacturer in the world, will use in its LCD TVs going forward. Samsung told The Vergethat it does not expect the shutdown to affect its LCD-based QLED TV lineup. So for the near-term, nothing changes.

One alternative is that Samsung buys its LCD panels from suppliers like TCL-owned CSOT and AUO, which already supply panels for Samsung TVs. Last year The Elec reported that Samsung could close all its South Korean LCD production lines, and make up the difference with panels bought from Chinese manufacturers like CSOT, which Samsung Display has invested in.

Samsung has also been showing off its MicroLED display technology at recent trade shows, which uses self-emissive LED diodes to produce its pixels. However, in 2019 Samsung predicted that the technology was two or three years away from being viable for use in a consumer product.

Electronic displays are an underappreciated yet integral feature of our digital economy—they are literally all around us. A quiet revolution is taking place in this market, as the dominant liquid crystal display (LCD) technology yields ground to a superior substitute: the organic light-emitting diode (OLED).

OLED displays produce more vibrant colors than LCDs and can be used to make flexible screens. Although OLEDs are still relatively expensive, rising demand is expected to increase production and drive down prices. By most industry indications, the OLED display seems to be the future.

It is therefore imperative to understand the concentration of OLED supply chains in East Asia, even as the United States remains a significant source of OLED inputs. We begin by examining the market ascendancy of OLEDs.

The key demand driver for OLED displays is the smartphone market. In addition to being a mini-computer in your pocket, improvements in processing power and larger screen sizes are turning smartphones into the “ultimate TV” for streaming content and playing games.

OLED technology is superior to LCDs for smartphone displays because OLEDs use organic materials to illuminate displays that are thinner, brighter, and higher contrast, are faster but more power-efficient, and are viewable from wider angles. OLED smartphone shipments are expected to skyrocket from 390.6 million units in 2016 to 812.4 million units in 2021, with the proportion of OLED displays rising from 17% in 2015 to 43% by 2024.

Beyond smartphones, OLED displays are also penetrating smart wearables (like watches), head-mounted displays for virtual reality, televisions, and tablets. The latest applications include digital signage, interactive kiosks, and automobile displays, particularly in autonomous vehicles. These OLED products are expected to achieve a compound annual growth rate (CAGR) of 23%, even higher than the 15.7% CAGR projected for OLED smartphones.

Stronger demand for OLED displays will also translate into greater revenue for OLED producers. The market for OLED flat panel displays is forecast to increase from $12.2 billion in 2015 to $58.7 billion in 2024, when OLEDs will constitute over 40% of flat panel revenues, up from 10.7% in 2015.

A key distinguishing feature of OLED displays compared to LCDs is their potential flexibility, as OLED displays are lighter and thinner and can be engineered to bend, curve, and fold.

Flexible OLED displays are only just starting to emerge, and their full commercial potential is still unrealized. But industry observers seem confident that flexible displays will soon become a common choice. Shipments are anticipated to surge from 1.5 million units in 2019 to 53.4 million units in 2025, with the market hitting $24.5 billion by 2023.

OLED technology has not yet displaced LCDs mainly because it is costlier to produce. But as demand for superior displays and flexible devices increases, OLED production will invariably grow, creating greater economies of scale.

For example, from 1Q 2015 to 2Q 2017, the cost of manufacturing a 55-inch UHD TV panel with an OLED display fell from 426% of LCD costs to 245% of LCD costs. If this trend persists, as seems likely, then OLEDs could reach cost parity with LCDs in the coming decade, accelerating OLED’s adoption as the preferred display technology by major producers.

If costs continue to fall—and lingering technical issues like “burn-in” are resolved—then demand for OLED technology should rise accordingly. As such, OLED displays will be ubiquitous in the coming decades of our digital future, touched every few minutes by billions around the world.

Because electronic displays are a capital-intensive, volume-based business, OLED manufacturing will naturally concentrate in regions and countries that can produce these displays at the largest scale and at the lowest cost.

The industry was until recently dominated by South Korean companies, especially Samsung, but China’s BOE is now the world’s second-largest producer of OLED smartphone displays. Corning and UDC are the major American players in the sector because they control market-leading technologies for key inputs like high-tech glass and organic materials.

Mapping the highly-concentrated OLED supply chain is thus essential to understanding the risks and opportunities for a product that is becoming a crucial component of consumer lifestyles, workplace productivity, and even military hardware.

Photo: A trick of the polarized light: rotate one pair of polarizing sunglasses past another and you can block out virtually all the light that normally passes through.

Photo: A less well known trick of polarized light: it makes crystals gleam with amazing spectral colors due to a phenomenon called pleochroism. Photo of protein and virus crystals, many of which were grown in space. Credit: Dr. Alex McPherson, University of California, Irvine. Photo courtesy of NASA Marshall Space Flight Center (NASA-MSFC).

Photo: Prove to yourself that an LCD display uses polarized light. Simply put on a pair of polarizing sunglasses and rotate your head (or the display). You"ll see the display at its brightest at one angle and at its darkest at exactly 90 degrees to that angle.

Photo: How liquid crystals switch light on and off. In one orientation, polarized light cannot pass through the crystals so they appear dark (left side photo). In a different orientation, polarized light passes through okay so the crystals appear bright (right side photo). We can make the crystals change orientation—and switch their pixels on and off—simply by applying an electric field. Photo from liquid crystal research by David Weitz courtesy of NASA Marshall Space Flight Center (NASA-MSFC).

Quantum Dot (QD) display technology has the potential to be a disruptive force to enable next generation LCD, MicroLED and OLED. It can ultimately create an emissive display to compete directly with OLED display.

Quantum dot enhancement films are already commercialized and mostly used in the high-end TV and gaming monitor markets. Quantum dot display can meet BT 2020 color gamut requirements; bring high brightness and energy efficiency. In future, many more new technology solutions are coming as shown below.

QD enhancement film contains trillions red and green emitting quantum dots. QD film sheets can be dropped into a blue LED LCD backlight in place of a diffuser sheet, creating quantum dot enhanced display with high brightness, wide color gamut and energy efficiency. QDEF process needs barrier films that can be higher costs.

QDs on a glass LGP can enable thinner, better and possibly lower cost solutions for the TV market (Will QDOG Have its Day?). Nanosys has introduced QDOG materials that can be made on master glass sheet LGP, and then cut into panel sizes. This process can lead to higher yield rates and much thinner products, with higher efficiency. Panel suppliers can offer QDOG LCD panels to TV brand manufacturers, reducing supply chain complexity. TV based on QD glass LGP is expected in the 2nd half of 2018. With higher volume, cost can go down and increase QD TV adoption rates. If QD TV can reach the sweet spot of a below-$1000 price, it could greatly increase mainstream market adoption.

Photo emissive products can replace the color filter array in LCDs with a layer of active QD emitters, increasing efficiency even further with wider viewing angles and higher brightness (up to 5000 cd/m² peak luminance) without increasing power. It can improve LCD, MicroLED and OLED architecture. Products are expected to be available by 2019. But the need for an in-cell polarizer for LCD can be a challenge.

MicroLED is considered to be next generation display technology for small size displays as well as TV. They are more reliable, produce brighter image and have faster response time. But manufacturing is a challenge due to the difficulty of mass transfer of microLED onto the backplane. With Photo emissive QDs, display makers can start with blue MicroLED array and then pattern red and green QDs on top, improving the process and yield. This type of MicroLED display is expected to come in two or three years. It may still have challenges with full color conversion, and manufacturing process.

Electro emissive QD display will have similar properties to OLED (perfect black and viewing angle), but with higher color gamut and higher brightness. It uses solution-printed QD as the emitter material to make AM QLED displays. Printable, low cost QD materials with superior performance have the potential to directly compete with OLED displays even in the flexible segment. Electro emissive printed QD displays may come to market in three to five years. There are still many challenges. Blue emitting materials still have efficiency and lifetime issues.

The biggest advantage of Ink jet printing is its lower production cost. Nanosys and DIC recently reported a breakthrough in producing quantum dot color conversion devices. These could be used for LCD as well as MicroLED. The process would require LCD panel markers to add new inkjet machines to mass production lines, which could be a roadblock for adoption rates. Printed QD can help manufacturing yield issues in MicroLED, accelerating its path to production. If successful, this could lead to low cost mass production of QD display.

Nanosys is the leader in QD display materials with commercialized products. It also licenses its technology to Samsung. It introduced its low cadmium Hyperion product in 2017 and is also producing non-cadmium products. Its current partners are Hitachi chemical, Exciton, DIC and others. Nanoco is focusing on only non-cadmium materials and is in the process of commercializing products with partners (Merck, Dow Wah Hong industrial). QD materials are moving away from cadmium, which is considered to be an environmental hazard. Some non-cadmium based materials are lagging in cost and performance even though it is constantly improving.

The first generation QD enhancement film enabled LCD to have better color purity, wider color gamut, brighter and more immersive HDR experience while maintaining power efficiency for TV applications. But challenges such as higher price, narrow viewing angle, relatively slow switching speed, lower black level and environmental concern about cadmium-based products have resulted in low adoption rates. Samsung has been focusing on QLED TV. QD TV has lost market-share to OLED in 2017 due to high price. Vizio’s introduction of 65" QD TV with competitive price of $2190, compared to $3000 for a 65" OLED TV, may open up some new opportunities in 2018. Samsung also introduced higher performance QLED TV in 2018 with more aggressive prices (75" for $2999 and 65" for $2099). Chinese brands, TCL and Hisense have also joined in. New lower pricing, better performance and more products from more brands might help sales in 2018.

Nvidia introduced the idea of a G-Sync HDR PC gaming 4K QD monitor with stunning wider color gamut, higher contrast, better color saturation and higher brightness in 2017. Philips, HP, ASUS, Acer, Samsung, and others have now introduced 4K HDR gaming monitors with QD technology. These high-end monitors were geared towards gamer, video editors, graphic designers, and professional photographers available in different sizes and price points. Harman-Samsung has shown a prototype of cadmium free automotive grade QD display that can meet design needs.

Mainstream application markets such as notebook, tablets, and smart phones still have very little or no presence of QD display. This may be due to the need for thinner form factors, higher performance and more environmental friendly QD products at a lower cost. If these challenges can be resolved, QD could be ideal for the mobile market (due to energy efficiency/low power consumption, higher brightness and better HDR). These features can even help LTPS LCD to compete with OLED for smartphones.

QD display technology definitely has the potential to be a disruptive force in the industry as an enabler for next generation, LCD, MicroLED and even OLED. If it can create emissive QD flexible display and it can have mass market appeal. But technology innovations, and new solutions are not enough. They must be combined with lower cost, a more efficient supply chain, mainstream product offering and mass market pricing. Otherwise it will stay as a high-end niche solution serving a limited market. - Sweta Dash

Sweta Dash is the founding president of Dash-Insights, a market research and consulting company specializing in the display industry. For more information, contact This email address is being protected from spambots. You need JavaScript enabled to view it. or visit www.dash-insight.com

LG Display and Samsung Display are struggling to find their ways out of the deterioration of their performance even after withdrawing from production of liquid crystal display (LCD) panels. The high-priced organic light emitting diode (OLED) panel sector regarded as a future growth engine is not growing fast due to the economic downturn. Even in the OLED panel sector, Chinese display makers are within striking distance of Korean display makers, experts say.

On Aug. 30, Display Supply Chain Consultants (DSCC), a market research company, predicted that LCD TV panel prices hit an all-time low in August and that an L-shaped recession will continue in the fourth quarter. According to DSCC, the average price of a 65-inch ultra-high-definition (UHD) panel in August was only US$109, a 62 percent drop from the highest price of US$288 recorded in July in 2021. The average price of a 75-inch UHD panel was only US$218, which was only about half of the highest price of US$410 in July last year. DSCC predicted that the average panel price in the third quarter will fall by 15.7 percent. As Chinese companies’ price war and the effect of stagnation in consumption overlapped, the more LCD panels display makers produce, the more loss they suffer.

As panel prices fell, manufacturers responded by lowering facility utilization rates. DSCC said that the LCD factory utilization rate descended from 87 percent in April to 83 percent in May, 73 percent in June, and 70 percent in July.

Now that the LCD panel business has become no longer lucrative, Korean display makers have shut down their LCD business or shrunk their sizes. In the LCD sector, China has outpaced Korea since 2018. China’s LCD market share reached 50.9 percent in 2021, while that of Korea dropped to 14.4 percent, lower than Taiwan’s 31.6 percent.

Samsung Display already announced its withdrawal from the LCD business in June. Only 10 years have passed since the company was spun off from Samsung Electronics in 2012. LG Display has decided to halt domestic LCD TV panel production until 2023 and reorganize its business structure centering on OLED panels. Its Chinese LCD production line will be gradually converted to produce LCD panels for IT or commercial products. TrendForce predicted that LG Display will stop operating its P7 Plant in the first quarter of next year.

Korean display makers’ waning LCD business led to a situation in which Korea even lost first place in the display industry. Korea with a display market share of 33.2 percent was already overtaken by China with 41.5 percent) in 2021 according to market researcher Omdia and the Korea Display Industry Association. Korea’s market share has never rebounded in for five years since 2017 amid the Korean government’s neglect. Seventeen years have passed since 2004 when Korea overtook Japan to rise to the top of the world in the LCD industry. Korea’s LCD exports amounted to more than US$30 billion in 2014, but fell to US$21.4 billion last year.

A bigger problem is that Korean display makers may lose its leadership in the OLED panel sector although it is still standing at the top spot. While Korea’s OLED market share fell from 98.1 percent in 2016 to 82.8 percent last year, that of China rose from 1.1 percent to 16.6 percent. Considering that the high-end TV market is highly likely to shrink for the time being due to a full-fledged global consumption contraction, some analysts say that the technology gap between Korea and China can be sharply narrowed through this looming TV market slump. According to industry sources, the Chinese government is now focusing on giving subsidies to the development of OLED panel technology rather LCD technology. On the other hand, in Korea, displays were also wiped out from national strategic technology industry items under the Restriction of Special Taxation Act which can receive tax benefits for R&D activities on displays.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey