lcd panel market free sample

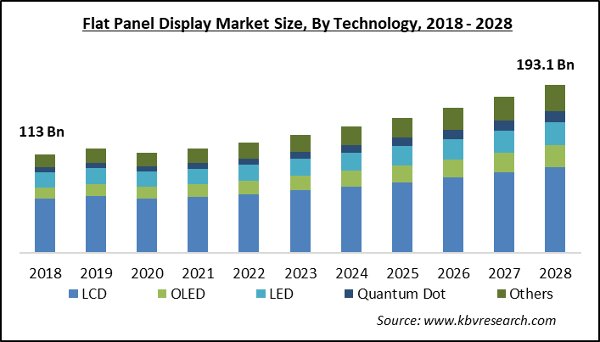

The global TFT-LCD display panel market attained a value of USD 148.3 billion in 2022. It is expected to grow further in the forecast period of 2023-2028 with a CAGR of 4.9% and is projected to reach a value of USD 197.6 billion by 2028.

The current global TFT-LCD display panel market is driven by the increasing demand for flat panel TVs, good quality smartphones, tablets, and vehicle monitoring systems along with the growing gaming industry. The global display market is dominated by the flat panel display with TFT-LCD display panel being the most popular flat panel type and is being driven by strong demand from emerging economies, especially those in Asia Pacific like India, China, Korea, and Taiwan, among others. The rising demand for consumer electronics like LCD TVs, PCs, laptops, SLR cameras, navigation equipment and others have been aiding the growth of the industry.

TFT-LCD display panel is a type of liquid crystal display where each pixel is attached to a thin film transistor. Since the early 2000s, all LCD computer screens are TFT as they have a better response time and improved colour quality. With favourable properties like being light weight, slim, high in resolution and low in power consumption, they are in high demand in almost all sectors where displays are needed. Even with their larger dimensions, TFT-LCD display panel are more feasible as they can be viewed from a wider angle, are not susceptible to reflection and are lighter weight than traditional CRT TVs.

The global TFT-LCD display panel market is being driven by the growing household demand for average and large-sized flat panel TVs as well as a growing demand for slim, high-resolution smart phones with large screens. The rising demand for portable and small-sized tablets in the educational and commercial sectors has also been aiding the TFT-LCD display panel market growth. Increasing demand for automotive displays, a growing gaming industry and the emerging popularity of 3D cinema, are all major drivers for the market. Despite the concerns about an over-supply in the market, the shipments of large TFT-LCD display panel again rose in 2020.

North America is the largest market for TFT-LCD display panel, with over one-third of the global share. It is followed closely by the Asia-Pacific region, where countries like India, China, Korea, and Taiwan are significant emerging market for TFT-LCD display panels. China and India are among the fastest growing markets in the region. The growth of the demand in these regions have been assisted by the growth in their economy, a rise in disposable incomes and an increasing demand for consumer electronics.

The report gives a detailed analysis of the following key players in the global TFT-LCD display panel Market, covering their competitive landscape, capacity, and latest developments like mergers, acquisitions, and investments, expansions of capacity, and plant turnarounds:

*At Expert Market Research, we strive to always give you current and accurate information. The numbers depicted in the description are indicative and may differ from the actual numbers in the final EMR report.

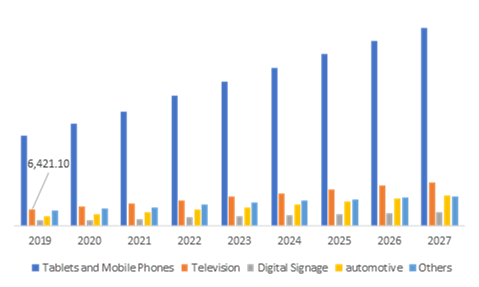

New York, USA, May 12, 2021 (GLOBE NEWSWIRE) -- A report was recently published by Research Dive titled, “Display Panel Market, By Type (LCD, OLED), By Product Type (Rigid, Flexible, and Foldable), Application (Tablets and Mobile Phones, Television, Digital Signage, Automotive, Others), Regional Outlook (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2019–2027”.

Increasing demand for display panels for various electronic devices is predicted to be the major driving factor for the display panel market in the forecast period. Display panels are mostly used in various devices such as television, smartphones, smart watches, infotainment systems in automobile and many more. The advancement in technology for flexible panels is predicted to be one of the major driving factors for the display panel market in the forecast period. Many manufacturers are focusing more on developing a variety of products to the consumers, which is predicted to create more investment opportunities in the market during the forecast period. For instance, Nubia’s launched a 4-inch flexible smartphone which can be adjusted on your wrist and can function as a phone as well as a watch at the same time.

Production cost of display panels is very high which is predicted to be the biggest restraint for the display panel market in the forecast period. Due to the increase in the production cost the average selling price of devices increases, which affects the profitability of the manufacturer and predicted to hinder the market growth in the forecast period.

OLED sub-segment is predicted to grow by generating a revenue of $ 90,079.4 million by 2027 at a CAGR of 13.9% in the forecast period. Rise in the demand of OLED screens for the manufacturing of various electronic devices is predicted to drive the sub-segment market in the forecast period. Moreover, the advanced technology in OLED is predicted to create more investment opportunity in the forecast period.

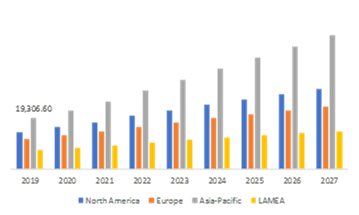

The Asia-Pacific Market is predicted to witness significant growth with revenue of $19,306.6 million at a CAGR of 12.5% in the forecast period. The rising numbers of manufacture units and industries has helps in pushing the market further towards growth.

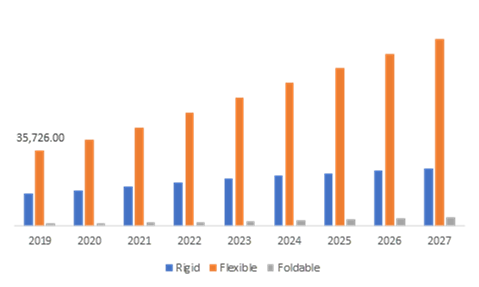

Key Market Segment By type, the OLED sub-segment is set to dominate the market with a revenue of $31,001.0 million at a CAGR if 13.9% in 2019. This is due to the rising demand from consumers to implement OLED screens in varied devices such as televisions, smartphones, and more.

Checkout How COVID-19 impacts the Display Panel Market. Click Here to Speak our Expertise before buying Report & Get More Market Insights @ https://www.researchdive.com/connect-to-analyst/390 By product type, the flexible panel sub-segment is predicted to see significant growth with a revenue of $35.726.0 million at a CAGR of 11.7% in 2019. The need to implement lighter yet durable panels that are also thinner in dimensions is preferred today, which has added to the growth of the market.

With the panels of the screens getting thinner, it risks the chances of damaged without the appropriate professional help. The complicated process along with high cost of production can be a hindrance to the growth of the market.

New York, United States, Nov. 10, 2022 (GLOBE NEWSWIRE) -- A Smart Display is a sophisticated digital product controlled by the Internet of Things (IoT)-enabled gadgets or voice-activated remote controls. The smart mirror is one cutting-edge tool that might track customer personal information and buying behavior in the retail and automobile industries. Smart devices are also getting interactive and advanced controlling features, expanding as a cutting-edge technical solution. Applications for smart displays project the desired content onto the display using technologies like LED, LCD, and others. A smart display is often used in retail, sport and entertainment, and healthcare due to the rise in demand for cutting-edge advertising and monitoring systems. Additionally, smart display applications like signage and mirrors designed to enhance consumer shopping experiences, welcome customers, and display advertisements in retail establishments drive the use of machine vision technology in the medical and healthcare sector.

Over the forecast year, it is predicted that the smart display market will grow due to the demand for the Internet of Things and artificial intelligence-based smart applications in the residential sector brought on by rising purchasing power in developing countries. The market for smart displays is also expected to benefit from the rising demand for smart mirror systems in the automotive sector. The demand for smart displays is also expected to increase as digital advertising becomes more and more popular in the corporate, retail, and healthcare sectors. Due to these factors, the market will likely grow in the following years.

There has been a rise in the use of smart home apps due to advances in basic technology and fast internet globally. The rise in smartphone usage has facilitated the emergence of smart home apps. Another outcome of global home automation improvement is using smart home application technologies, such as smart displays in the residential sector, to control digital applications like smart lights, thermostats, and more. The development of AI-powered smart display technology in the home market, which will further fuel demand for smart display technology internationally, is also expected to increase demand for smart automation technology for controlling lights, fans, security cameras, and other devices.

The need for increased safety, comfort, and convenience has led to the global expansion of smart mirror applications, which are now a crucial part of the automotive industry. The smart displays used in the automotive sector are designed for various purposes, including Bluetooth and wi-fi, temperature, navigation, turn signals, back cameras, and more. Owing to the rising demand for smart display mirrors in the automotive industry, it is projected that the market for smart displays will grow. Additionally, because the required hardware is easily accessible, the growth of electronically connected cars is swiftly adopting smart display technology. Consequently, expected to fuel the development of the smart display market in the upcoming years.

The E-commerce platform has wholly destroyed the retail industry because of accessibility and the internet. Customers" increasing purchasing power and disposable income on a global scale have raised the demand for smart signage solutions, such as smart displays. Major retailers like Alibaba, Walmart, and Amazon are integrating digital solutions like smart signage. Additionally, the smart display can be utilized as a payment method to reduce line waiting during checkout because clients can use their cell phones to pay at the sign. Therefore, it is projected that each of these factors will create opportunities for the market for smart displays in the coming years.

The Asia Pacific will command the market with the largest share. One of the factors boosting the growth of the smart display market in Asia-Pacific is the rise in the use of smart signage and mirror displays in the retail, residential, and healthcare sectors. Additionally, it is predicted that the market will expand significantly throughout the projection period due to increased demand for digital communication systems. In addition, it is projected that the Asia-Pacific smart display market will gain from the high demand for surveillance and smart home displays in the automobile sector. Furthermore, it is projected that the future growth of smart display technology in this region will be influenced by the technological advancements made in smart signs and mirrors by China, Japan, South Korea, and others, including the digital wall and 8K signage technology. The market for smart displays is expanding in Asia-Pacific due to these forces working together.

North America is anticipated to maintain a dominant position in the global market for smart displays due to the presence of major competitors and the accessibility of cutting-edge smart home solutions. The market for smart displays has recently been driven by the adoption of smart signage technology across the commercial and industrial sectors. For instance, it is anticipated that over the forecast period, a rise in government initiatives in North America to build smart infrastructure across airports, railway stations, and other commercial sectors will be a crucial driver of the smart display market.

The area"s rise has also been aided by the creation of new smart display technology by significant industry participants like Google, Amazon, Apple, and Facebook. The demand for customer contact and digital communication in the healthcare, retail, sports, and entertainment industries is one factor driving the growth of smart signage solutions in this region"s smart display market.

Key Highlights The global smart display market had a revenue share of USD 1.80 billion in 2021, presumed to reach USD 17.81 billion, expanding at a CAGR of 29% during the forecast period.

Market News In 2022, Samsung launched a second-generation SmartSSD. Samsung"s SmartSSD can analyze data directly, reducing the time that data must be transferred between the CPU, GPU, and RAM compared to other SSDs.

Smart Transportation Market: Information by Product Type, Transportation Mode (Roadways, Railways, Airways and Maritime), and Region — Forecast till 2030

Smart Card Market: Information by Type (Contact, Contactless), Component (Software, Hardware), Access Type (Physical, Logical), Industry Vertical, and Region — Forecast till 2030

Smart Lock Market: Information by Lock Type (Deadbolts, Lever Handles, Padlocks), Communication Protocol, Application, and Region — Forecast till 2030

StraitsResearch is a market intelligence company providing global business information reports and services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insight for thousands of decision-makers. Straits Research Pvt. Ltd. provides actionable market research data, especially designed and presented for decision making and ROI.

Whether you are looking at business sectors in the next town or crosswise over continents, we understand the significance of being acquainted with the client’s purchase. We overcome our clients’ issues by recognizing and deciphering the target group and generating leads with utmost precision. We seek to collaborate with our clients to deliver a broad spectrum of results through a blend of market and business research approaches.

The global next-generation display materials market size was valued at USD 185.92 billion in 2021 and is projected to register a valuation of USD 430.03 billion by 2030, at a Compound Annual Growth Rate (CAGR) of 10.8% over the forecast period 2022-2030.

Increasing demand for laptops, smartphones, Televisions, tablet devices, and other display devices are driving the revenue growth of the global next-generation display market.

Rising preference for more thin and light display systems and devices and rapid technological advancements in the electronics industry are some of the vital factors that are currently driving the growth of the next-generation display market.

Other factors projected to drive the revenue growth of the global next-generation display market include changing trends in the display market, wide viewing angles and high-resolution tablets, smartphones and displays, projectors, digital cameras, smart TVs, and camcorders.

The Global next generation display materials market is segmented by product type, application, and region. On the basis of product type, the market is segmented as, Thin-Film Transistors LCD (TFT-LCD), Organic Light Emitting Diode (OLED), and others. On the basis of application, the market is segmented as Smartphones, Automotive Displays, Laptops and Tablets, and Others.

The Asia-Pacific presents a very lucrative market for the holographic display market due to the presence of highly advanced countries in developing economies as well as consumer electronics industries such as China, Taiwan, and South Korea.

Market Business Insights is a leading global market research and consulting firm. We focus on business consulting, industry chain research, and consumer research to help customers provide non-linear revenue models. We believe that quality is the soul of the business and that is why we always strive for high-quality products. Over the years, with our efforts and support from customers, we have collected inventive design methods in various high-quality market research and research teams with extensive experience.

The key factors that drive the market of a display factory are mother glass size, product size, panels per sheet, process yield, and operating efficiency. For example, to manufacture 820 million smartphone displays per year of 6-in diagonal size in Gen 6 fabs, approximately 380,000 (or 380K) MG sheets per month will be required to be processed at 85% yield and 85% operating efficiency. As an additional example, to manufacture 35 million TV displays per year of 55-in diagonal size in Gen 8.5 fabs, approximately 640,000 (640K) MG sheets per month will be required to be processed at 90% yield and 85% operating efficiency

Also, surging demand for smart consumer electronics, the emerging number of manufacturing facilities, and the low cost of labor in counties such as India, Pakistan, Bangladesh, etc., are some of the factors that are supporting the market growth of the display panel in the countries. Moreover, due to the low cost of manufacturing in the countries, numerous companies announced the establishment of their new OLED and LCD panel manufacturing plants.

Furthermore, the rising adoption of display devices in various industries, especially in countries such as China, India, and South Korea, is a key factor supporting the market growth. Moreover, due to the COVID-19 pandemic, the demand for smartphones and laptops has increased because of work-from-home norms. Also, financial and education institutions are adopting digital teaching methods. These factors are contributing to the increased demand for small- and large-scale displays for commercial and business purposes.

are AU Optronics Corporation, BOE Japan Co. Ltd, Innolux Corporation, LG Display Co. Ltd, Samsung Electronics Co. Ltd, Panasonic Corporation, Sharp Corporation, Hisense Co. Ltd, Toshiba Corporation, Sony Corporation, etc., are some of the prominent players operating in the display panel market. Several M&As along with partnerships have been undertaken by these players to facilitate customers with innovative products.

Based on the type of display, the market is fragmented into LCD, OLED, and Others (AMOLED, MicroLED, etc) The OLED segment grabbed major market share in 2020 and dominated the market. The advantage of OLED displays such as s being light in weight and their flexibility, have enabled them to gain a competitive advantage over other segments. The OLED technology is recognized as a lighter and thinner alternative than conventional LED and LCD systems. In addition, OLED panels do not require any type of backlighting compared to LCD. Stable performance in sunlight is an additional advantage of OLEDs.

Based on the resolution, the market is fragmented into 8K, 4K, HD, and Others. The 8K segment grabbed the major market share and dominated the market. 8k TVs have 4 times as many pixels as their 4k counterparts and a shocking 16 times as many pixels as a 1080p TV. These extra pixels should make a significant difference in picture quality. Moreover, the player is launching products with 8K resolution, n August 2019, Sharp Corporation launched the Sharp 8M-B80AX1U 80″ Class 8K Ultra HD LCD. This display offers ultimate high definition, conforming to the 8K Ultra HD standards and pixel resolution 16 times greater than Full HD and four times greater than 4K.

Based on the application, the market is fragmented into Smartphones & Tablets, PC & laptops, televisions, and Others. The smartphones & tablets segment grabbed the XX% market share in 2020. and dominated the market. The growing adoption of smartphones coupled with the availability of phones and tablets at reasonable prices leads to the growth of the segment.

For a better understanding of the market adoption of the display panel market, the market is analyzed based on its worldwide presence in the countries such as North America (the United States and Canada), Europe (Germany, France, Italy, Spain, United Kingdom, and Rest of Europe), Asia-Pacific (China, Japan, India, Australia, and Rest of APAC), and Rest of World. Asia Pacific region grabbed XX% market for the display panel Market industry and generated revenue of USD XX Million in 2020. However, the North America region would witness the highest CAGR during the forthcoming years

The display panel market can further be customized as per the requirement or any other market segment. Besides this, UMI understands that you may have your own business needs, hence feel free to connect with us to get a report that completely suits your requirements.

TOKYO, Feb. 26, 2023 (GLOBE NEWSWIRE) -- The Global 3D Display Market Size accounted for USD 107.8 Billion in 2022 and is estimated to achieve a market size of USD 595.2 Billion by 2032 growing at a CAGR of 18.9% from 2023 to 2032.

3D Display Market Research Report Highlights and Statistics:The Global 3D Display Market Size in 2022 stood at USD 107.8 Billion and is set to reach 595.2 Billion by 2032, growing at a CAGR of 18.9%

The Market is driven by factors such as the growing demand for 3D displays in advertising and gaming, the increasing adoption of 3D displays in the healthcare industry for medical imaging, and the rising demand for 3D displays in the automotive industry for advanced driver assistance systems (ADAS) and in-car entertainment systems.

North America currently dominates the 3D display market. Europe is also a huge market for 3D displays and the Asia Pacific region is the fastest growing region worldwide.

The 3D Display Market is a rapidly growing market that offers a wide range of applications across various industries, from entertainment and healthcare to automotive and aerospace. A 3D display is a device that displays images in three dimensions, providing an immersive visual experience to the viewer. The market is driven by factors such as the increasing demand for 3D displays in advertising, gaming, and medical imaging, as well as the rising adoption of 3D displays in the automotive industry for advanced driver assistance systems and in-car entertainment systems. The market is highly competitive and includes major players such as LG Electronics, Samsung Electronics, Sony Corporation, and Toshiba Corporation, as well as smaller players offering specialized 3D display technologies for specific applications. The demand for 3D displays is expected to continue to grow in the coming years as new and innovative applications are developed, driving the growth of the market.

Trends in the 3D Display Market:Adoption of glasses-free 3D displays: One of the emerging trends in the 3D display market is the adoption of glasses-free 3D displays, which eliminates the need for viewers to wear 3D glasses, providing a more immersive experience.

Development of glasses-free 3D projection systems: The development of glasses-free 3D projection systems is an emerging trend, which is expected to drive the growth of the market.

3D Display Market Dynamics:Increasing adoption of 3D displays in education: The education sector is increasingly adopting 3D displays for a more engaging and interactive learning experience.

Growing demand for head-mounted displays: The market for head-mounted displays is growing as these devices offer an immersive 3D viewing experience, particularly in gaming and entertainment.

Growth Hampering Factors inthe Market for 3D Display:High cost of 3D displays: The high cost of 3D displays can hamper the growth of the market, as it may limit adoption among budget-conscious consumers and businesses.

Competition from alternative technologies: The 3D display market may face competition from alternative technologies, such as virtual and augmented reality, which could hamper market growth.

Limited viewing angles: Some 3D displays have limited viewing angles, which may limit their appeal to certain audiences and could hamper market growth.

Limited spatial resolution: Some 3D displays have limited spatial resolution, which may limit their usefulness for certain applications and could hamper market growth.

The Asia-Pacific region’s 3D Display Market share is the highest, owing to the increasing adoption of 3D displays in the healthcare and entertainment sectors. The region has witnessed significant growth in the healthcare sector, where 3D displays are being used for various applications such as medical imaging, virtual surgeries, and 3D printing. Moreover, the entertainment industry in the region is using 3D display technology to enhance the overall user experience for viewers.

North America’s 3D Display market share is also huge and is growing at the fastest pace, owing to the presence of major players and technological advancements in the region. The increasing demand for 3D displays in the entertainment and gaming industries is also driving growth in the region. For instance, the demand for 3D display technology is growing in the gaming industry, as it enhances the overall gaming experience for users. Moreover, the region has witnessed significant growth in the healthcare sector, where 3D displays are used for applications such as medical imaging and surgical simulations.

Europe is another key market for 3D Display, owing to the increasing adoption of 3D displays in the automotive and advertising industries. The automotive industry in the region is using 3D displays for various applications such as virtual dashboard displays, heads-up displays, and infotainment systems. Furthermore, the region has witnessed a significant increase in the use of 3D displays in the advertising industry, which is driving growth in the region.

The South American and MEA regions have a smaller 3D display market share, however it is expected to grow at a steady pace. The healthcare sector in the region is also adopting 3D displays for various applications such as medical imaging and virtual surgeries.

Sony Corporation, Panasonic Corporation, Samsung Electronics Co., Ltd., LG Display Co., Ltd., Toshiba Corporation, Sharp Corporation, Innolux Corporation, HannStar Display Corporation, AU Optronics Corp., BOE Technology Group Co., Ltd., Japan Display Inc., Universal Display Corporation, Corning Incorporated, Fujifilm Holdings Corporation, Mitsubishi Electric Corporation, Canon Inc., 3D Systems Corporation, Autodesk Inc., Dassault Systèmes SE, and Barco NV. These companies offer a variety of 3D display technologies and solutions, and are constantly innovating and investing in research and development to stay competitive in the market.

The Global Biometric Sensors Market Size gathered USD 1,319.5 Million in 2021 and is set to garner a market size of USD 3,582.9 Million by 2030 growing at a CAGR of 11.9% from 2022 to 2030.

The Global Satellite Internet Market Size accounted for USD 3,985 Million in 2021 and is estimated to achieve a market size of USD 17,431 Million by 2030 growing at a CAGR of 18.2%from 2022 to 2030.

The Global Telecom API Market Size was valued at USD 221 Billion in 2021 and is predicted to be worth USD 1,113 Billion by 2030, with a CAGR of 20.2% from 2022 to 2030.

Acumen Research and Consulting is a global provider of market intelligence and consulting services to information technology, investment, telecommunication, manufacturing, and consumer technology markets. ARC helps investment communities, IT professionals, and business executives to make fact-based decisions on technology purchases and develop firm growth strategies to sustain market competition. With the team size of 100+ Analysts and collective industry experience of more than 200 years, Acumen Research and Consulting assures to deliver a combination of industry knowledge along with global and country level expertise.

Most of the Smartphone Displays of modern phones, when initially introduced, were in the range of 3 to 4 inches that were sleek with a lesser resolution and high pixel density. Currently, the consumer demands smartphones with a high-quality display which is similar to the display and resolution of laptops, with higher brightness, amazing displaying HD images and HD videos. The primary smartphone displays are divided into resistive and capacitive. An Advanced capacitive screen is a typical control display that has the conductive touch of a human finger. And when the user tries a capacitor display to touch, the amount of electrostatic field or charge passed to the varied point of contact becomes a functional capacitor. However, the advanced resistive screen is actually made up of two thin layers of extra polyethylene terephthalate (PET) coated with indium tin oxide (ITO). When these two particular layers connect to each other, a high voltage is surpassed through the advanced system that actually initiates the monitor touch process at the desired point. Presently, the advanced capacitive touchscreen display shows a larger market size than the traditional type due to rising touch sensitivity and high clarity.

The COVID 19 has affected 215 countries. To combat the negative effects, countries lead lockdown, which has adversely affected the smartphone display market share brands. The pandemic leads to numerous challenges. There are many factors like the risk of continuing production, supply, distribution of work, lack of workforce, and fewer development activities that have affected the demand and supply. North America and Asia account for 68% of the total world production of smartphones.

The TV Display Market is a huge topic, but to sum it up in short, one can expect significant growth during the forecast period till 2030. There are many attributes linked with the consumption of smartphones and the rising demand for them. It is one of the best to connect to each other, and prototypes are readily available in the market today. It is a proven scientific fact the market for smartphone displays is huge. It is like an addiction. Also, a very amazing alternative for entertainment. People are getting more conscious. This is also boosting the market for smartphone displays.

The market is booming for Smartphone displays. The consumer market is expected to rise at a CAGR of 8.30%; the estimated value is around USD 123.7 billion by 2030. The packaging of phones is a very important and integral part of the whole process. There is a growing demand for smartphones and tablets along with usual comfort and possible convenience features that drive the smartphone display market significantly. However, the demand-supply ratio equilibrium has been well balanced. Without a doubt, in the coming years, the consumption of phones is expected to grow; thus, boosting the market in taking over the existing growth constraints.

The outbreak of COVID-19 has hard severely knocked out the growing pace of the Smartphone Display Market 2020 market share. Because of mandatory closures of consumer markets and farming across the globe, the revenues of the companies have been falling apart. COVID19 has disrupted the entire supply chain. Continuous lockdown created a negative impact and affected the morale of the manufacturers. The major retailers, such as supermarkets & hypermarkets whose main job is selling the phones, have gone through acute shortage despite having demand in certain areas across the globe.

During the forecasted period, there has been an estimated to reach USD 123.7 billion by 2030. The global market has been divided on the basis of type, packaging type, distribution channel, and region. The 3D display market can be divided as follows: On the basis of technology, the market is divided into different types such as light-emitting diode (LED), advanced organic LED (OLED), modern digital light processing (DLP), and the affordable plasma display panel (PDP). On the basis of applications, the market is divided into modern TV, super trendy Smartphones, high-quality display Monitors, Head-mounted displays, and others. On the basis of region, the market is divided into a big portion of North America, Europe, major countries of Asia-Pacific, and the rest of the world.

The primary market claims to have a CAGR of 8.30% to reach USD 123.7 billion by 2030. The demand for smartphones has risen because of globalization. The Asian and North American countries are focusing on expanding the production of smartphone displays to meet the demand and supply chain.

There has been a growing demand for the TV Display Market, the demand for these types of products is rising everywhere, including the U.S., Canada, Mexico in North America, Germany, Sweden, Poland, Denmark, Italy, U.K., France, Spain, etc. North America was the biggest market in 2016 and is estimated to rise at the highest CAGR of 8.30% during the forecast period. Europe imports these types of products. Europeans and Americans love buying HQ phones and TV, which is accelerating the growth of the market in Europe. Another lucrative market in North America.

The major geographical distribution of the modern smartphone display market consisting of Big portion of North America, major parts of Asia Pacific (APAC), Europe, along with Rest of the World (RoW).

Samsung has recently launched Galaxy On8, a not very expensive smartphone in the Indian market that has an advanced 6-inch HD+ Super AMOLED display with better flexibility, high-resolution image quality, and advanced image resolution. Samsung has also innovated an advance buy a remarkable unbreakable screen for its Samsung Galaxy Note 8 new smartphone.

The primary stakeholders in the phone market are manufacturers who are the suppliers and traders, Government agencies, partners and industrial bodies, Investors, and Trade experts.

The global market for smartphone displays is projected to develop at an advanced rate during the estimated period. The growing geographical analysis of the modern smartphone display market is huge for North America, Europe, Asia-Pacific, and the rest of the countries of the world. The major Asia-Pacific is projected to dominate the smartphone market for advanced smartphone display during the forecast period for the coming years. The development in the Asia-Pacific region is primarily dominated by the countries of China, Japan, and India because of the prime focus on a large number of smartphone manufacturing organizations.

The recent market in North America is also projected to rise during the estimated period due to the existence of the big players in North America such as Apple Inc. and Google. But because of the early adoption of advanced technologies such as OLED, AMOLED, the most prominent region of North America is projected to grow at a faster rate, following Asia-Pacific.

The global commercial display market size was valued at USD 51.17 billion in 2021. It is projected to reach USD 88.90 billion by 2030, growing at a CAGR of 7.2% during the forecast period (2022–2030). The commercial display is a subset of electronic displays that can manage centrally and individually to display text, animation, or video messages to an international audience. Commercial displays use technologies such as organic light-emitting diode (OLED), liquid crystal display (LCD), light-emitting diode (LED), quantum light-emitting diode (QLED), and projection for showing media and digital material, web pages, weather data, and text in a professional setting. Commercial displays are utilized extensively in the retail and hotel industries due to their extended warranties and ability to operate between 16 and 24 hours daily. In addition, this technology optimizes brightness in high-ambient-light circumstances and is integrated with a specific technology that contributes to superior onboard cooling, picture preservation, and resolution concerns.

In the commercial display industry, technological breakthroughs such as holographic displays, tactile touchscreens, and outdoor 3D screens raise product quality requirements and outweigh financial benefits. The commercial display market share is anticipated to increase steadily due to technological advancements and the widespread adoption of new technologies such as OLED and QLED.

The increasing need for digital signage in the healthcare and transportation industries is anticipated to propel the worldwide commercial display market"s expansion. Rapid industrialization, rising government spending on infrastructure development, and changing consumer lifestyles all contribute to the global expansion of the commercial display industry. Moreover, the increasing adoption of digital technologies by market participants for advertising products and services to make a strong impression on customers" minds is a major factor boosting the demand for commercial displays. In addition, the increasing integration of technologies such as AI and machine learning into commercial displays is driving the global market growth. The introduction of 4K and 8K displays accelerates the manufacturing of ultra-HD advertising content, contributing significantly to market expansion.

Increased urbanization and population growth, rising government spending on infrastructure building, and shifting consumer lifestyles are driving the rise of the commercial display market. Display technology developments and rising demand for energy-efficient panels are driving the expansion of the global commercial display industry. In addition, the increasing incorporation of technologies such as artificial intelligence and deep learning into commercial displays contributes to the market"s global growth.

The significant financial and energy costs associated with maintaining displays could impede the market growth. In addition, COVID-19 and its negative impact are a significant barrier to market expansion. As a result of these factors, display manufacturing has been halted all over the world. It is anticipated that an increase in commercial displays in industries such as hospitality, entertainment, banking, healthcare, education, and transportation will fuel the expansion of the market. Due to technological advancements and significant investments in research and development made by important companies to produce distinctive displays with sophisticated features, there is a sizable potential for market expansion.

In addition, the most recent low-cost display solutions are projected to penetrate a variety of commercial units such as restaurants, bars, and cafes at a faster rate. This is anticipated to give lucrative opportunities for the market. The growing popularity of contemporary technologies such as QLED, OLED, mini-LED, and micro-LED will give the sector multiple opportunities for growth in the years to come.

The digital signage segment dominates the market during the forecast period. The market category is divided into video walls, displays, transit LED screens, digital posters, and kiosks. In addition, the increasing preference for digital display solutions in business settings is also fueling the segment"s growth. The segment of display televisions is anticipated to grow at a CAGR of 4.23% during the forecast period. Manufacturers like SAMSUNG and LG Display Co., Ltd. are incorporating cutting-edge technology such as mini-LED and micro-LED into their most recent commercial-grade televisions. In addition, competitors are introducing many forms of TV panels, including rollable and flexible panels. These products are utilized extensively in hospitals, clinics, and multi-specialty healthcare institutions.

LCD is the most dominant segment during the forecast period. Several industry sectors, including corporate offices and banks, currently utilize LCD-based devices. One of the principal factors driving the widespread use of LCD technology is the decline in LCD production costs. However, the LED technology category is anticipated to account for a sizable market revenue share by 2030. LED technology improvements have led to the development of numerous LED displays, including OLED and QLED. Manufacturers widely employ these energy-efficient solutions in their commercial displays.

The hardware category retained the most significant market share during the forecast period. The segment"s expansion can be attributable to the greater demand for hardware than software. Displays, extenders and cables, accessories, and installation equipment are examples of hardware components. With the introduction of new and advanced software for digital signage, the software category had a significant market share. The software segment is expected to grow at an impressive CAGR of 6.26% during the forecast period. Due to the higher maintenance and repair requirements of commercial televisions and monitors, the services category experienced a substantially greater demand in 2021 than the software segment.

The flat panel display sector dominates the market during the forecast period. Numerous end-use sectors extensively employ flat-panel displays such as video walls, digital posters, monitors, and televisions. Entertainment, gaming, design, automotive, and manufacturing applications utilize curved panels extensively. These panels are widely utilized in TVs, monitors, smartphones, and wearable devices to satisfy various consumer demands.

Based on application, the market has been categorized into retail, hotel, entertainment, stadiums and playgrounds, corporate, banking, healthcare, education, and transportation.

The retail sector held the most significant market share during the forecast period. The central area requires digital advertisements for product and service marketing and promotion. Retailers are implementing a contemporary advertising strategy which is causing an increase in demand for commercial-grade televisions and digital signage. Due to the increasing number of hotels, motels, restaurants, QSRs, cafes, and bars, the hospitality industry is another significant contributor to the market expansion.

The sub-32-inch and 32-to-52-inch categories are expected to dominate the market during the forecast period. Customers prefer huge displays because of enhanced display clarity, energy-efficient technologies like OLED and micro-LED, and superior content quality. However, the sector of displays more significant than 75 inches is anticipated to have the highest CAGR due to the increasing demand for large-format displays. Retail, transportation, and healthcare industries use huge displays for signage purposes. In the past few years, leading players like SAMSUNG and LG Display Co., Ltd. have developed a plethora of commercial-grade televisions with displays more significant than 75 inches due to their growing popularity.

The global market for commercial displays has been classified by geography into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa.

North America accounted for more than 32.45% of the market share and is anticipated to dominate during the forecast period. Companies such as SAMSUNG, TCL North America, and others have developed a substantial consumer base in the area. In addition, the widespread usage of advanced display solutions across various industries is anticipated to stimulate regional market growth further. Asia-Pacific will experience the highest CAGR of 7.23% during the forecast period. Rapid urbanization and the increasing use of commercial displays in the healthcare, hotel, transportation, and retail sectors have contributed to the region"s expansion. In addition, the region is distinguished by the presence of manufacturers, original equipment manufacturers, and an extensive client base.

There is a dramatic increase in the number of automated equipment and systems in various types of industries that has contributed to the growth of the embedded displays market. Besides, the technological advancements in the embedded display arena has contributed to the latest products with high end displays entering the market and contributing to the growth of such products. In addition, greater efficacy and low cost are also responsible for the growth of this market. Moreover, there is an increased usage of embedded display in the 3D systems and this is creating a lot of opportunities for growth in the embedded displays market.

According to the assessment of Persistence Market Research, the global embedded display market is forecasted to reach a figure of about US$ 18,800 Mn in 2022 and is poised to exhibit a robust CAGR in the period of assessment.

The market in North America is set to dominate the global embedded display market in terms of value and this trend is projected to sustain itself throughout the assessment period. North America embedded display market is the most attractive market, growing at a robust CAGR over the forecast period.

According to the projections of Persistence Market Research, the LED display type segment is expected to reach a value of about US$ 4,750 Mn in the year 2022. This signifies a robust CAGR during the forecast period of 2017-2022. The LED display type segment is estimated to account for more than one-fourth of the revenue share of the display type segment by the end of the year 2017 and is expected to lose in market share by 2022 over 2017.

According to the assessment of Persistence Market Research, the wearable devices segment is poised to touch a figure of about US$ 1,350 Mn in the year 2022. This signifies a CAGR of nearly 16% during the assessment period from 2017 till the year 2022. The wearable devices segment is estimated to account for nearly one-tenth of the revenue share of the application segment by the end of the year 2017 and is projected to gain market share by 2022 over 2017.

The report also profiles companies that are expected to remain active in the expansion of global embedded display market through 2022, which include Avnet, Inc., Microsoft Corp., Intel Corp., Green Hills Software Inc., Anders Electronics Plc, Planar Systems Inc., Enea AB., Esterel Technologies SA, Altia Inc. and Data Modul AG.

The global smartwatch display panel market size was valued at $1.21 billion in 2020, and is projected to reach $4.06 billion by 2030, registering a CAGR of 14.1% from 2021 to 2030. Smartwatch is a next-generation wearable computer in the form of a watch. It offers some of the prominent features such as text messaging, emails, appointments, app alerts, and voice calls. Hence, to have seamless experience of smartwatch, smartwatch display panel is the most important and key component of the watch.

The smartwatch display panel is generally less than 2 inches, which increases the need for high resolution in pixels per inch to provide sharp and easy-to-read fine text and graphics. In addition, it needs to produce fairly bright images, as watches are often viewed in high ambient light. A larger color gamut is required to counteract color washout from ambient light. Moreover, vibrant saturated colors are helpful while reading text and graphics information. Thus, smartwatch display panel market plays a crucial role in sales of smartwatches globally.

Emergence of large number of players in the smartwatch industry is the prime reason that drives the growth of the smartwatch display panel industry. Furthermore, high demand for flexible display technology accelerates the growth of the smartwatch display panel market. Moreover, increase in health awareness among consumers is opportunistic for the market growth. Considering these factors, the smartwatch display panel market is anticipated to witness substantial growth in the future.

Increase in pixel density is expected to offer lucrative growth opportunities for the market during the forecast period. However, smartwatch display panels consume significant energy, which is expected to hamper the market growth during the forecast period. On the contrary, some of the other factors driving the market growth are rise in demand for connected devices and increase in disposable income.

COVID-19 notably impacted both consumers and the economy. Electronics manufacturing hubs have been temporarily working at low efficiency to curb the spread of COVID-19. This has majorly affected the supply chain of semiconductor market by creating shortages of materials, components, and finished goods. Lack of business continuity has negatively impacted the revenue and shareholder returns, which are expected to create financial disruptions in the smartwatch display panel industry. However, the smartwatch display panel market is estimated to recover by the mid of 2021 with rapid technological advancements. Moreover, market players are deploying various strategies such as product launch, partnership, and agreement to boost the smartwatch display panel market growth during the forecast period.

The global smartwatch display panel market is segmented into panel type, display technology, display type, application, and region. On the basis of panel type, the market is bifurcated into rigid display and flexible display. The rigid display segment is further classified into round and square. The rigid display segment dominated the market, in terms of revenue in 2020, and is expected to follow the same trend during the forecast period. Depending on display technology, the market is segregated into LED-backlit LED and OLED. The LED-backlit LCD segment was the major revenue contributor in 2020, and is anticipated to witness significant market share during the forecast period. By display type, the market is fragmented into monochrome and colored. The market share for the colored segment was highest in 2020, and is expected to grow at a high CAGR from 2021 to 2030.

As per application, the market is differentiated into personal assistance, medical & health, fitness, and personal safety. The market share for the personal assistance segment was highest in 2020, however, the medical & health segment is expected to grow at a high CAGR from 2021 to 2030.

Significant factors that impact the growth of the smartwatch display panel market include emergence of large number of players in the smartwatch industry, high demand for flexible display technology, and increase in health awareness among the consumers. However, high energy consumption of smartwatch display panels hampers the market growth. On the contrary, increase in pixel density is expected to offer lucrative opportunities for the smartwatch display panel market during the forecast period.

Competitive analysis and profiles of the major smartwatch display panel market players such as AU Optronics, BOE Technology Group Co., Ltd., Everdisplay Optronics (Shanghai) Co., Ltd., Futaba Corporation, Japan Display, LG Electronics, Samsung Electronics Co., Ltd., Sharp Electronics, Truly Opto-electronics Ltd., and Visionox are provided in this report. These key players have adopted strategies, such as product portfolio expansion, mergers & acquisitions, agreements, regional expansion, and collaboration, to enhance their market penetration.

Key Benefits for StakeholdersThis study comprises analytical depiction of the smartwatch display panel market trends along with the current trends and future estimations to depict the imminent investment pockets.

Key Market Players AU Optronics Corp, BOE Technology Group Co., Ltd., Everdisplay Optronics (Shanghai) Co.,Ltd. (EDO), Futaba Corporation, JAPAN DISPLAY, LG Electronics Inc, Samsung Electronics, Sharp Corporation, Truly International Holdings Limited, Visionox Technology Inc.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey