lcd panel supply chain quotation

Liquid crystal display (LCD) is a flat panel display that uses the light modulating properties of liquid crystals. Liquid crystals do not produce light directly, instead using a backlight or reflector to produce images in colour or monochrome.

According to TrendForce"s latest panel price report, TV panel pricing is expected to arrest its fall in October after five consecutive quarters of decline and the prices of certain panel sizes may even be poised to move up. The price decline of IT panels, whether notebook panels or LCD monitor panels, has also begun showing signs of easing and overall pricing of large-size panels is developing towards bottoming out.

TrendForce indicates, with panel makers actively implementing production reduction plans, TV inventories have also experienced a period of adjustment, with pressure gradually being alleviated. At the same time, the arrival of peak sales season at year’s end has also boosted demand marginally. In particular, Chinese brands are still holding out hope for Double Eleven (Singles’ Day) Shopping Festival promotions and have begun to increase their stocking momentum in turn. Under the influence of strictly controlled utilization rate and marginally stronger demand, TV panel pricing, which are approaching the limit of material costs, is expected to halt its decline in October. Prices of panels below 75 inches (inclusive) are expected to cease their declines. The strength of demand for 32-inch products is the most obvious and prices are expected to increase by US$1. As for other sizes, it is currently understood that PO (Purchase Order) quotations given by panel manufacturers in October have are all increased by US$3~5. Currently China"s Golden Week holiday is ongoing but, after the holiday, panel manufacturers and brands are expected to wrestle with pricing. Based on prices stabilizing, whether pricing can actually be increased still depends on the intensity of demand generated by branded manufacturers for different sized products.

TrendForce observes that current demand for monitor panels is weak, and brands are poorly motivated to stock goods. At the same time, the implementation of production cuts by panel manufacturers has played a role and room for price negotiation has gradually narrowed. At present, the decline in panel pricing has slowed. Prices of small-size TN panels below 21.5 inches (inclusive) are expected to cease declining in October due to reduced supply and flat demand. As for mainstream sizes such as 23.8 and 27-inch, price declines are expected to be within US$1.5. The current demand for notebook panels is also weak and customers must still face high inventory issues and are relatively unwilling to buy panels. Panel makers are also trying to slow the decline in panel prices through their implementation of production reduction plans. Declining panel prices are currently expected to continue abating in October. Pricing for 14-inch and 15.6-inch HD TN panels are expected to drop by US$0.2~0.3, falling from a 1.8% drop in September to 0.7%, while pricing for 14-inch and 15.6-inch FHD IPS panels are expected to fall by US$1~1.2, falling from a 3.4% drop in September to 2.4%.

Compared with past instances when TV panels drove a supply/demand reversal through a sharp increase in demand and spiking prices, this current period of lagging TV panel pricing has been halted and reversed through active control of utilization rates by panel manufacturers and a slight increase in demand momentum. The basis for this break in decline and subsequent price increase is relatively weak. Therefore, in order to maintain the strength of this price backstop and eventual escalation and move towards a healthier supply/demand situation, panel manufacturers must continue to strictly and prudently control the utilization rate of TV production lines, in addition to observing whether sales performance from the forthcoming Chinese festivals beat expectations, allowing stocking momentum to continue, and laying a solid foundation for TV panels to completely escape sluggish market conditions.

The price of IT panels has also adhered to the effect of production reduction and the magnitude of its price drops has gradually eased. TrendForce believes, since the capacity for supplying IT panels is still expanding into the future, it is difficult to see declines in mainstream panel prices halt completely when demand remains weak. Even if new production capacity from Chinese panel factories is gradually completed starting from 2023, price competition in the IT panel market will intensify once products are verified by branded clients, so potential downward pressure in pricing still exists.

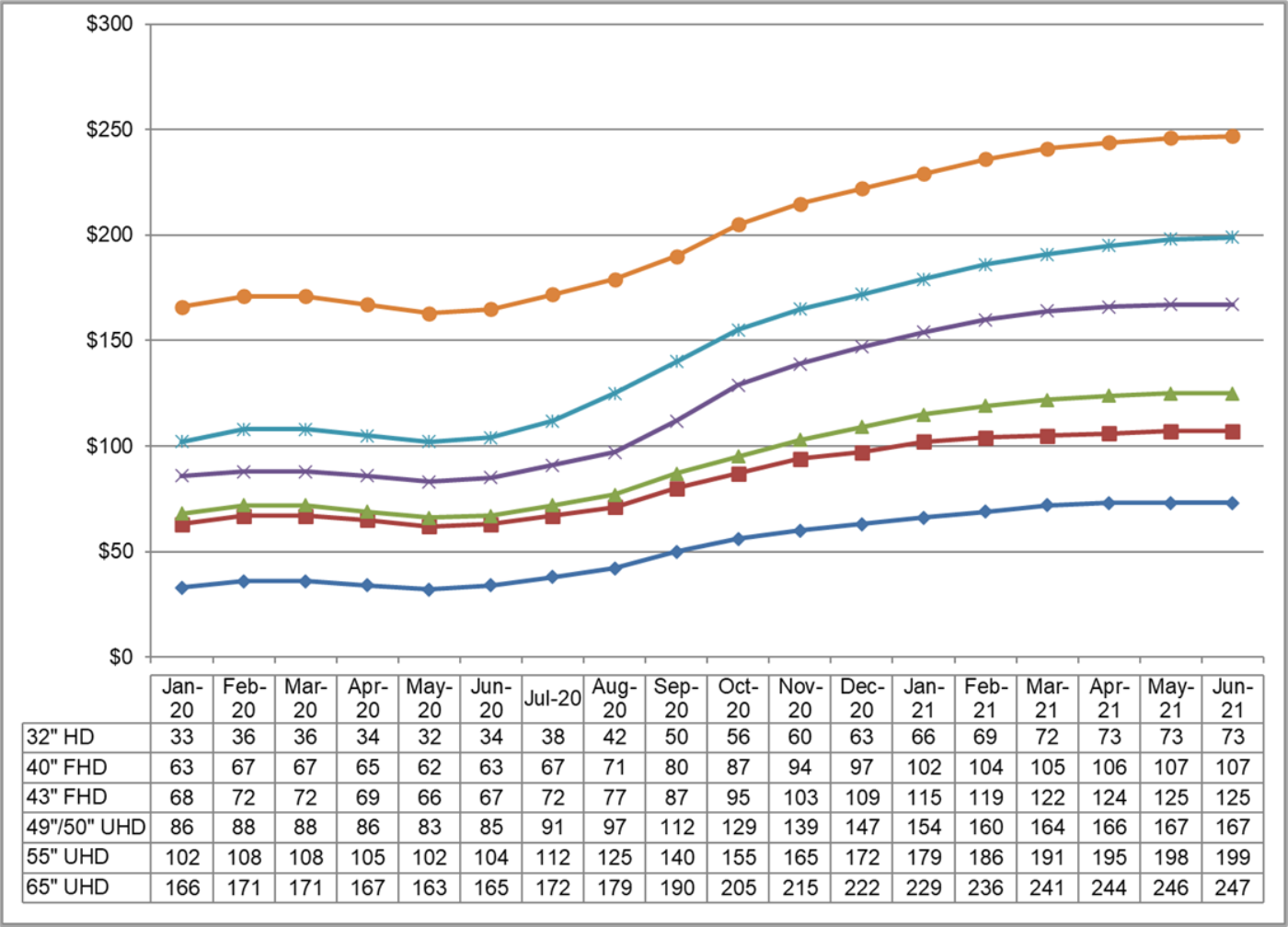

Display Logic has developed global sources of supply far beyond those of our competitors. Among those are selected manufacturers with which we have partnered with preferential pricing agreements.

(17 January, 2017) – Demand for liquid crystal display (LCD) panels from South Korean and Chinese TV makers was strong in the fourth quarter of 2017, but implementation of their panel purchasing strategies for the first quarter of 2018 may result in a correction as demand expectations change. While some TV brands are expected to maintain their panel purchasing plans, others are forecast to reduce demand in the first quarter as it is a traditionally slow season and some demand was pulled into the last quarter, according to

report by IHS Markit, South Korean TV makers are expected to reduce LCD panel purchasing volumes by 3 percent in the first quarter of 2018 compared to the previous quarter, or to increase by 1 percent compared to the same period last year.

“There is risk of a correction in demand as their panel purchasing plans get underway given that a sufficient supply chain buffer is already factored in for the first quarter. These manufacturers will likely continue to use their plans as a negotiating tactic for more competitive prices,” said

China’s top six TV makers -- ChangHong, Haier, Hisense, Konka, Skyworth and TCL -- are forecast to cut their LCD panel purchasing volumes by 30 percent in the first quarter of 2018 over quarter, and 5 percent over year.

“It is estimated that the Chinese brands carried relatively higher level of inventories as of the end of December 2017 as they have been preparing for the upcoming promotional seasons in early January and the Chinese New Year holidays in February. Given this, they are in no rush to secure more panel supplies in the first quarter, and may want to negotiate for lower prices,” Yang said.

“Due to a coming slow season, the bargaining power seems to be with TV makers. However, uncertainties about a stable supply of feature-rich premium and larger panels will have the top-tier TV brands concerned,” Yang said. Chinese panel makers, she said, have yet to prove that they will actually start mass-producing 65-inch LCD panels from the world’s first Gen 10.5 fabs in the first quarter.

“The top-tier TV brands will want to make sure they can secure sufficient panel supplies of 65-inch and larger panels,” Yang said. “At the same time, they also seek to attain better bargains on large and ultra-large panels in 2018 and beyond.”

Panel makers, however, have not agreed to offer more price concessions. Some panel makers are scheduled to remodel fabs in the first quarter and this will eventually cause an unstable supply of LCD TV panels, particularly for larger sizes. “All this points to the likelihood that the TV panel market will see chaotic swings in demand in the first quarter of 2018,” Yang said.

COVID-19 has had a dramatic effect on the electronics industry. The worldwide drive for people to work and educate from home and the increase in demand for medical products have taken the supply of electronics components from overcapacity to shortage and extended lead times. This was multiplied by the shutdown of manufacturing and the attempt to catch up with previous demand. The industrial market has also gotten hit by the loss of small gen fab capacity due to the shutting down of older, less competitive fabs.

Before COVID-19, the display market had been in an oversupply with the slowdown in cell phone demand. With the increased demand for laptops, monitors, and even TVs has backfilled this capacity and driven us into a shortage situation. This shortage of electronic components is not only in the display market but extends to basic components like resistors and capacitors.

Linda Lin covers large-sized TFT LCD panels and is in charge of survey reports involving the manufacturers and vendors of the notebook panel supply chain.

Linda worked previously at LCD market research firm WitsView, leading the research on panels as well as on downstream products that included monitors and TVs. At the Market Intelligence & Consulting Institute, Taiwan Chief Information and Communications Technology (ICT) market research group, she oversaw regional research for South and East Asia. It was during this time that she decided to make large-sized displays her main focus. Linda has a master’s degree in business administration from National Yunlin University of Science and Technology in Taiwan.

Kimi is a senior analyst for display (TFT LCD and OLED) touch and user interface at Omdia. He covers display price, supply chain, fingerprint, cover lens, shipment forecasts, and emerging technologies.

Prior to joining Omdia (formerly IHS Markit), Kimi was a research analyst at Tianma Group, where he spent over two years in LCD and AMOLED market research. He also oversaw the China FPD industry market at the Topology Research Institute for over five years. Kimi has a bachelor"s degree in telecommunications engineering and a master’s degree in microelectronics from Shanghai University, China.

Stacy is an experienced analyst in Omdia’s display research team, covering small and medium displays. She focuses on automotive displays, smartphone displays, and wearable displays. As a Principal Analyst, she covers small and medium display shipments, supply chain, pricing, and business strategy analysis. She is the lead analyst of the automotive display intelligent service.

As part of Omdia’s small/medium displays practice, Joy covers displays under 9 inches in size utilized in smartphones, tablets, wearables, and automotive displays. Her research touches areas such as the AMOLED ecosystem, new trends in smartphone panel displays, and the supply chain in China for smartphone displays.

Joy brings 17 years of experience to the subjects she covers. She worked previously at BOE, the giant Chinese display manufacturer, as a product manager for medical and industrial displays. She started her career at Tianma Group as an LCD module design engineer, then became manager of product design and development. She transferred to the marketing department as an analyst for mobile phone displays and then for automotive displays. Joy has a bachelor’s degree in automation from Beihang University, a major public research institution in China. She also holds a master’s degree in business management from Renmin University of China.

Mr. Hidetoshi Himuro is a Director at Omdia. He previously worked at DisplaySearch, a leader in primary research and forecasting on the global display market. At DisplaySearch, he served as director of IT & FPD market research. He was responsible for market research and analysis of large-area LCD applications, including monitor, notebook PCs and public display/digital signage. He also forecasted monthly large-area LCD panel pricing. With his background in engineering, he covered the LCD panel technology roadmap.

Prior to DisplaySearch, Mr. Himuro held a number of positions at NEC in both Japan and the US. At NEC, his diverse responsibilities included strategic planning, project management, LCD panel and monitor set procurement, design verification, vendor relationships and hardware development for notebook PCs and LCD monitors and their LCD panels. He has a bachelor"s degree in Electrical Engineering from Tokyo University of Science, Japan.

Peter Su conducts research on large-sized displays, tracking supply-and-demand dynamics, market trends, and product roadmaps on panels sized more than 9 inches measured diagonally and used in tablets, notebooks, monitors, and televisions.

Previously, Peter was at DisplaySearch, where he worked with large displays as well. At AU Optronics, he was in panel sales and strategic product marketing in the notebook PC and tablet business units. There, he was also involved in PC capacity planning, technology investment projects, and both upstream and downstream channels for panels and mobile PCs. Peter has a bachelor"s degree in economics from the University of Victoria in Canada, and a master’s degree in business administration from Concordia University Wisconsin in Mequon, Wisconsin.

Vicki Chen focuses on display materials and components, including new form factors, weight efficiencies, and technological advances in displays. She brings more than 10 years of experience in the flat-panel-display industry.

Vicki worked previously at Chinese firm Sigmaintell Consulting, where she was responsible for research on the mobile phone panel market and value chain. She also worked in new-project development at Taiwan Display, a part of Japan Display. She had her first taste of the flat-panel display industry and its workings as a product planning engineer in charge of the request-for-quote (RFQ) development for mobile phone products for China Brands at Innolux, a TFT LCD panel manufacturer in Taiwan.

Mr. Hiroshi Hayase is a Senior Director at Omdia. He previously worked at DisplaySearch and Solarbuzz, leading providers of display and solar market intelligence. With nearly 30 years of experience in the LCD industry, he brings an unparalleled focus to sales, marketing management, production, product engineering and market research and analysis.

At DisplaySearch, Mr. Hayase served as vice president of small and medium displays. Before that, he was responsible for sales and market research at a Taiwanese LCD panel/module manufacturer, Wintek Japan Corporation. Earlier, he served as sales manager with Applied Komatsu Technology (AKT), where he was responsible for sales of CVD systems to major Japanese panel producers. He also has 13 years of experience in sales management and production engineering across the full range of LCD production processes with Seiko Epson. Mr. Hayase holds a bachelor"s degree in Mechanical Engineering from Shizuoka University, Japan.

He previously worked at DisplaySearch and Solarbuzz, leading providers of display and solar market intelligence. Mr. Annis is a leading expert in flat panel display research and served in a dual role as vice president of manufacturing research at DisplaySearch as well as at its sister company of Solarbuzz. At DisplaySearch, he was responsible for analyzing emerging technologies, tracking and forecasting flat panel display investments, and researching equipment, materials and process trends. At Solarbuzz, he developed the company"s proprietary polysilicon, wafer and cell manufacturing databases and authored related reports.

Mr. Robin Wu is a Principal Analyst at Omdia. Previously he worked at DisplaySearch, a leader in primary research and forecasting on the global display market. At DisplaySearch, he served as a PC and TFT analyst, specializing in trend analysis of China"s PC, monitor, and panel markets. He also acted as vice chair of the VESA monitor task group in 2010 and has focused on monitor/panel standardization since early 2009.

Prior to DisplaySearch, Mr. Wu spent nearly seven years at the leading IT brand IBM/Lenovo. There, he focused on monitor/TFT business, delivering industry-leading green ThinkVision products and managing panel sourcing and qualifications. In addition to providing support to the desktop/AIO business, he acted as a liaison in the industry, building strong relationships with leading PC monitor OEMs in China. Mr. Wu has a bachelor"s degree in Mechanics & Electronics and a master"s degree in Micro-Electro-Mechanical Systems from Huazhong University of Science and Technology, China.

Jeff Lin is a longtime analyst and researcher in the field of displays, having previously worked at DisplaySearch, a leader in primary research and forecasting on the global display market. At DisplaySearch, he worked as an analyst covering Taiwan"s display market and was responsible for market research and analysis of the PC monitor value chain and large-area panel roadmap.

Before DisplaySearch, Jeff gained valuable experience handling panel sourcing and desktop monitor market analysis at BenQ Corporation. Prior to that, he served as a key monitor account sales manager at Samsung Electronics Taiwan, where he formed key relationships with leading PC monitor company and OEMs in the country. Before Samsung, he was an engineer at Chunghwa Picture Tubes (CPT), where he led TV panel development projects and planned TV panel roadmaps.

Jimmy joined the company in 2014 following the acquisition of DisplaySearch, where he served as a senior analyst covering display materials and LED analysis. Jimmy also worked at Samsung—first at Samsung LED, and then at Samsung Electronics. There, he led several R&D projects on new light sources for LCD backlighting and new BLU structures.

Jerry Kang is responsible for the OLED display market analysis at IHS. His main focus is the AMOLED panel and the next generation display market including flexible and transparent display with AMOLED.

Prior to joining IHS in 2011, Jerry worked as an OLED development engineer at Samsung SDI and Samsung Mobile Display, in charge of operational circuit designing for OLED and LCD.

David Hsieh is a noted expert in research and analysis of the TFT LCD, and LCD TV value chain for Mainland China and Taiwan. As head of the Displays team, he oversees the division’s end-to-end research on displays, covering the supply chain, materials and components, supply-and-demand dynamics, pricing and cost modeling, revenue and shipment forecasts, and emerging technologies.

In an earlier stint at DisplaySearch, he led the company’s primary research and forecasting on the global display market while concurrently serving as vice president of the greater China market. David also worked at HannStar Display, a leading manufacturer of TFT LCD panels, as a key account manager, production planner, and production engineer for the HannStar TFT LCD module line.

In his previous roles at the company, Jusy led the research team on TV technology and ecosystems, which included the panel display market for TVs and large-sized LCDs. He has also worked on the global monitor and public information markets.

SEOUL, April 27 (Reuters) - LG Display Co Ltd (034220.KS) saw first-quarter profit plummet far below forecasts and warned of a further drop in panel prices as pandemic-driven demand for TVs, smartphones and laptops fades and competition heats up.

The South Korean Apple Inc (AAPL.O) supplier said it would shift its focus to higher-end products and gradually lower production of more commoditised LCD TV panels where it lacked a competitive advantage over cheaper Chinese rivals.

The LCD TV market shrank by more than 10% in the first quarter and Chinese competitors are pricing their products lower than LG Display"s expectations, Lee Tai-jong, head of the company"s large display marketing division, said on a call with analysts.

"Margins have been squeezed chiefly due to panel price declines and weaker demand, as consumers have already bought many screens during COVID-19 in the past two years," said Kim Yang-jae, an analyst at DAOL Investment & Securities.

Chinese rival BOE Technology Group Co Ltd (000725.SZ) has been tapped to also supply Apple with display screens, said a source with knowledge of the matter.

In the first quarter, prices of 55-inch liquid crystal display (LCD) panels for TV sets fell 16% from the previous quarter while prices of LCD panels for notebooks and monitors dropped by around 7% to 11%, according to data from TrendForce"s WitsView.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey