lcd panel price drop made in china

Nikkei Asia reported on the 21st that the price of LCD panels for Smart TVs kept falling. Among the prices in June, that has been determined by panel manufacturers in China, Taiwan, South Korea, and TV manufacturer, the 55-inch Opencell price has decreased. The wholesale price of semi-finished products without backlight fell around 6 percent from May to around $90. The price has been declining for 11 consecutive months, continuing to rewrite the record low since the survey began in 2006. The price of 32-inch products for small-size TVs also dropped by 15 percent, setting a new record low.

The report points out that the price of TV LCD panels will continue to fall. Apparently, one of the strong reasons is continuous inflation. The continuous inflation has been deeply engulfing the world. The continuous health concerns, and the war, are leading to a major slowdown in the economy. There are rising doubts about the demand for TVs as the customer’s needs are changing. For instance, people are now considering essential goodies rather than spending on electronics when they already have one. For example, one user with a good Smart TV will think twice before upgrading to a new model just because yes. If the old model is serving well, then there is no real reason to upgrade due to technological upgrades.

However, there is still hope for small TVs. According to reports, panel factories in mainland China are reportedly expanding the production of 32-inch LCD panels. In the past, 55-inch products were the main priority due to their higher profit margin. However, the 55-inch panels now sit in unsatisfactory market conditions. Therefore, the factories will expand the supply of small products. After all, these smart TVs are commercialized at lower prices. Furthermore, some users are willing to save money no matter the display’s size.

Samsung, which always has been a strong maker in the LCD business, is shutting down the division.The company will focus on OLED and upcoming technologies. However, we don’t know if the costlier OLED TVs are in a better situation.

The price of LCD display panels for TVs is still falling in November and is on the verge of falling back to the level at which it initially rose two years ago (in June 2020). Liu Yushi, a senior analyst at CINNO Research, told China State Grid reporters that the wave of “falling tide” may last until June this year. For related panel companies, after the performance surge in the past year, they will face pressure in 2022.

LCD display panel prices for TVs will remain at a high level throughout 2021 due to the high base of 13 consecutive months of increase, although the price of LCD display panels peaked in June last year and began to decline rapidly. Thanks to this, under the tight demand related to panel enterprises last year achieved substantial profit growth.

According to China State Grid, the annual revenue growth of major LCD display panel manufacturers in China (Shentianma A, TCL Technology, Peking Oriental A, Caihong Shares, Longteng Optoelectronics, AU, Inolux Optoelectronics, Hanyu Color Crystal) in 2021 is basically above double digits, and the net profit growth is also very obvious. Some small and medium-sized enterprises directly turn losses into profits. Leading enterprises such as BOE and TCL Technology more than doubled their net profit.

Take BOE as an example. According to the 2021 financial report released by BOE A, BOE achieved annual revenue of 219.31 billion yuan, with a year-on-year growth of 61.79%; Net profit attributable to shareholders of listed companies reached 25.831 billion yuan, up 412.96% year on year. “The growth is mainly due to the overall high economic performance of the panel industry throughout the year, and the acquisition of the CLP Panda Nanjing and Chengdu lines,” said Xu Tao, chief electronics analyst at Citic Securities.

In his opinion, as BOE dynamically optimizes its product structure, and its flexible OLED continues to enter the supply chain of major customers, BOE‘s market share as the panel leader is expected to increase further and extend to the Internet of Things, which is optimistic about the company’s development in the medium and long term.

TCL explained that the major reasons for the significant year-on-year growth in revenue and profit were the significant year-on-year growth of the company’s semiconductor display business shipment area, the average price of major products and product profitability, and the optimization of the business mix and customer structure further enhanced the contribution of product revenue.

“There are two main reasons for the ideal performance of domestic display panel enterprises.” A color TV industry analyst believes that, on the one hand, under the effect of the epidemic, the demand for color TV and other electronic products surges, and the upstream raw materials are in shortage, which leads to the short supply of the panel industry, the price rises, and the corporate profits increase accordingly. In addition, as Samsung and LG, the two-panel giants, gradually withdrew from the LCD panel field, they put most of their energy and funds into the OLED(organic light-emitting diode) display panel industry, resulting in a serious shortage of LCD display panels, which objectively benefited China’s local LCD display panel manufacturers such as BOE and TCL China Star Optoelectronics.

Liu Yushi analyzed to reporters that relevant TV panel enterprises made outstanding achievements in 2021, and panel price rise is a very important contributing factor. In addition, three enterprises, such as BOE(BOE), CSOT(TCL China Star Optoelectronics) and HKC(Huike), accounted for 55% of the total shipments of LCD TV panels in 2021. It will be further raised to 60% in the first quarter of 2022. In other words, “simultaneous release of production capacity, expand market share, rising volume and price” is also one of the main reasons for the growth of these enterprises. However, entering the low demand in 2022, LCD TV panel prices continue to fall, and there is some uncertainty about whether the relevant panel companies can continue to grow.

According to Media data, in February this year, the monthly revenue of global large LCD panels has been a double decline of 6.80% month-on-month and 6.18% year-on-year, reaching $6.089 billion. Among them, TCL China Star and AU large-size LCD panel revenue maintained year-on-year growth, while BOE, Innolux, and LG large-size LCD panel monthly revenue decreased by 16.83%, 14.10%, and 5.51% respectively.

Throughout Q1, according to WitsView data, the average LCD TV panel price has been close to or below the average cost, and cash cost level, among which 32-inch LCD TV panel prices are 4.03% and 5.06% below cash cost, respectively; The prices of 43 and 65 inch LCD TV panels are only 0.46% and 3.42% higher than the cash cost, respectively.

The market decline trend is continuing, the reporter queried Omdia, WitsView, Sigmaintel(group intelligence consulting), Oviriwo, CINNO Research, and other institutions regarding the latest forecast data, the analysis results show that the price of the TV LCD panels is expected to continue to decline in April. According to CINNO Research, for example, prices for 32 -, 43 – and 55-inch LCD TV panels in April are expected to fall $1- $3 per screen from March to $37, $65, and $100, respectively. Prices of 65 – and 75-inch LCD TV panels will drop by $8 per screen to $152 and $242, respectively.

“In the face of weak overall demand, major end brands requested panel factories to reduce purchase volumes in March due to high inventory pressure, which led to the continued decline in panel prices in April.” Beijing Di Xian Information Consulting Co., LTD. Vice general manager Yi Xianjing so analysis said.

“Since 2021, international logistics capacity continues to be tight, international customers have a long delivery cycle, some orders in the second half of the year were transferred to the first half of the year, pushing up the panel price in the first half of the year but also overdraft the demand in the second half of the year, resulting in the panel price began to decline from June last year,” Liu Yush told reporters, and the situation between Russia and Ukraine has suddenly escalated this year. It also further affected the recovery of demand in Europe, thus prolonging the downward trend in prices. Based on the current situation, Liu predicted that the bottom of TV panel prices will come in June 2022, but the inflection point will be delayed if further factors affect global demand and lead to additional cuts by brands.

With the price of TV panels falling to the cash cost line, in Liu’s opinion, some overseas production capacity with old equipment and poor profitability will gradually cut production. The corresponding profits of mainland panel manufacturers will inevitably be affected. However, due to the advantages in scale and cost, there is no urgent need for mainland panel manufacturers to reduce the dynamic rate. It is estimated that Q2’s dynamic level is only 3%-4% lower than Q1’s. “We don’t have much room to switch production because the prices of IT panels are dropping rapidly.”

Ovirivo analysts also pointed out that the current TV panel factory shipment pressure and inventory pressure may increase. “In the first quarter, the production line activity rate is at a high level, and the panel factory has entered the stage of loss. If the capacity is not adjusted, the panel factory will face the pressure of further decline in panel prices and increased losses.”

In the first quarter of this year, the retail volume of China’s color TV market was 9.03 million units, down 8.8% year on year. Retail sales totaled 28 billion yuan, down 10.1 percent year on year. Under the situation of volume drop, the industry expects this year color TV manufacturers will also set off a new round of LCD display panel prices war.

The price of LCD TV panels continues to fall, and that could be welcome news for anyone who’s in the market to buy a new living room portal in time for the World Cup and the Christmas holidays.

A report this week from the analyst firm Sigmaintell Consulting revealed that LCD panel prices fell again last month, with the cost of 32-inch displays slipping by $2 per panel, and 55-inch units falling by $4 each. Meanwhile, 65-inch panels now cost $8 less, while 65-inch ones are $10 cheaper than they were a month ago.

The price of LCD TV panels has been sliding for months now, since the end of last year. That’s great for consumers of course, with the price of upper-end TVs that use LCD panels falling quite noticeably, including some of the newest models out this year.

Typically, LCD panels that are shipped out from the factory go straight into production once they reach their customer, and then end up in stores as finished TVs within just a few of months. As such, analysts believe the latest price drops will result in some steep discounts on LCD TV prices just before Christmas and Black Friday come around.

LCD display prices are falling because the market is becoming increasingly clogged with panels made by Chinese manufacturers, who’re able to make them more cheaply. Indeed, their competitiveness is so extreme that they have forced traditional South Korean display making giants such as Samsung Display and LG Display to withdraw from the market. Last month it was reported that Samsung will exit completely by the end of this month, while LG has drastically reduced its own production and is likely to quit altogether in the coming months.

There were fears that recent COVID-19 related lockdowns in China might push LCD prices back up again, however that didn"t happen, and with cities like Beijing and Shanghai now reopening, it’s expected that the downward price pressure will continue unabated, Sigmaintell Consulting said.

For anyone who’s struggling with the increased living costs that have resulted from higher inflation this year, the TV price drop will come as a welcome surprise. Many households have no doubt tried to avoid making big purchases such as a new TV, but if you need one then it becomes an almost essential buy. With any luck, people in that situation will soon be able to get their hands on a decent new box without breaking the bank.

(Yicai Global) March 11 -- Leading Chinese panel makers TCL Technology Group and BOE Technology Group saw revenue jump last year, but both firms are turning to higher-value products amid a drop in prices for standard liquid crystal displays.

But LCD panel prices have corrected since the third quarter of last year, and according to a report by industry researcher Sigmaintell, prices are still falling. In the 43 to 75 inch segment, the cost per panel fell by USD2 to USD6 this month from February. Affected by the Russia-Ukraine conflict, the drop in global demand for televisions is expected to deepen, putting further pressure on prices.

As it is increasingly difficult to make a profit from traditional LCD panels, TCL and BOE are expanding into higher value-added areas such as Mini LED and organic light-emitting diode screens. TCL released a new Mini LED TV on March 9, in sizes of 65, 75, 85 and 98 inches, all priced at more than CNY10,000 (USD1,579) each.

BOE is reportedly in talks with Honor to make a special OLED panel for smartphones that will be launched later this year. The technology could potentially reduce smartphone power consumption by about 30 percent.

(Yicai Global) June 13 -- BOE Technology Group, TCL China Star Optoelectronics Technology and other big Chinese liquid crystal display manufacturers are reducing output starting from this month to try and stop a freefall in prices caused by a global glut.

Panel makers are cutting production by 16 percent on average from this month, Rong Chaoping, senior researcher at market research firm AVC Revo, told Yicai Global. Television panel makers are expected to ship 3.6 million less panels than last month.

Panel makers will reduce capacity by between 15 and 20 percent this month, said Wu Rongbing, chief analyst at Chinese semiconductor intelligence service Omdia.

LCD TV display shipments from China’s five largest panel manufacturers accounted for 68.5 percent of the global market in April, a new high, and they were expected to exceed 70 percent this year, according to Omdia.

But there is much less demand for notebook computers, monitors and TVs now that fewer people are working from home as the Covid-19 pandemic wanes and amid pressure from global inflation. This is driving prices down, said Li Yaqin, general manager of market research firm Sigmaintell.

The global panel industry is expected to slash production by about 20 percent this year, according to Beijing-based Sigmaintell. It is the first time since 2013 that the worldwide sector has implemented such a large-scale and wide-ranging cut in manufacturing. But it should help to slow the fall in prices, Li said.

“Tumbling prices are squeezing profits,” Li said. “The price of a TV panel is now below cost price and that of some data panels is also below the manufacturing cost.”

The price of small and medium-sized TV displays has more than halved since the highest point last year, and that of large-sized screens have fallen by more than 40 percent, according to AVC Revo.

“Panel makers are facing rising liquidity pressure and bigger losses as prices are now below cost price, so the display industry is likely to undergo another big reshuffle,” Rong said.

Excess supply will ease in the third quarter once output is cut, and prices will start to pick up and then flatten out, Li said. Demand for consumer electronic products is shrinking by far more than expected so it is too early to tell whether prices will rebound in the second half, she added.

Panel prices are likely to stop dropping this month or next as output falls, Wu said. Whether prices will start to pick up soon depends on when demand improves.

Recently, it was announced that the 32-inch and 43-inch panels fell by approximately USD 5 ~ USD 6 in early June, 55-inch panels fell by approximately USD 7, and 65-inch and 75-inch panels are also facing overcapacity pressure, down from USD 12 to USD 14. In order to alleviate pressure caused by price decline and inventory, panel makers are successively planning to initiate more significant production control in 3Q22. According to TrendForce’s latest research, overall LCD TV panel production capacity in 3Q22 will be reduced by 12% compared with the original planning.

As Chinese panel makers account for nearly 66% of TV panel shipments, BOE, CSOT, and HKC are industry leaders. When there is an imbalance in supply and demand, a focus on strategic direction is prioritised. According to TrendForce, TV panel production capacity of the three aforementioned companies in 3Q22 is expected to decrease by 15.8% compared with their original planning, and 2% compared with 2Q22. Taiwanese manufacturers account for nearly 20% of TV panel shipments so, under pressure from falling prices, allocation of production capacity is subject to dynamic adjustment. On the other hand, Korean factories have gradually shifted their focus to high-end products such as OLED, QDOLED, and QLED, and are backed by their own brands. However, in the face of continuing price drops, they too must maintain operations amenable to flexible production capacity adjustments.

TrendForce indicates, that in order to reflect real demand, Chinese panel makers have successively reduced production capacity. However, facing a situation in which terminal demand has not improved, it may be difficult to reverse the decline of panel pricing in June. However, as TV sizes below 55 inches (inclusive) have fallen below their cash cost in May (which is seen as the last line of defense for panel makers) and are even flirting with the cost of materials, coupled with production capacity reduction from panel makers, the price of TV panels has a chance to bottom out at the end of June and be flat in July. However, demand for large sizes above 65 inches (inclusive) originates primarily from Korean brands. Due to weak terminal demand, TV brands revising their shipment targets for this year downward, and purchase volume in 3Q22 being significantly cut down, it is difficult to see a bottom for large-size panel pricing. TrendForce expects that, optimistically, this price decline may begin to dissipate month by month starting in June but supply has yet to reach equilibrium, so the price of large sizes above 65 inches (inclusive) will continue to decline in 3Q22.

TrendForce states, as panel makers plan to reduce production significantly, the price of TV panels below 55 inches (inclusive) is expected to remain flat in 3Q22. However, panel manufacturers cutting production in the traditional peak season also means that a disappointing 2H22 peak season is a foregone conclusion and it will not be easy for panel prices to reverse. However, it cannot be ruled out, as operating pressure grows, the number and scale of manufacturers participating in production reduction will expand further and its timeframe extended, enacting more effective suppression on the supply side, so as to accumulate greater momentum for a rebound in TV panel quotations.

The Korean display industry drove Korea’s exports, making Korea a display powerhouse in the world one exporter just 10 years ago. But it has been put into a position to completely lose its power as Korea’s national strategic industry due to a price war initiated by Chinese display makers and a complex global crisis.

LG Display and Samsung Display are struggling to find their ways out of the deterioration of their performance even after withdrawing from production of liquid crystal display (LCD) panels. The high-priced organic light emitting diode (OLED) panel sector regarded as a future growth engine is not growing fast due to the economic downturn. Even in the OLED panel sector, Chinese display makers are within striking distance of Korean display makers, experts say.

On Aug. 30, Display Supply Chain Consultants (DSCC), a market research company, predicted that LCD TV panel prices hit an all-time low in August and that an L-shaped recession will continue in the fourth quarter. According to DSCC, the average price of a 65-inch ultra-high-definition (UHD) panel in August was only US$109, a 62 percent drop from the highest price of US$288 recorded in July in 2021. The average price of a 75-inch UHD panel was only US$218, which was only about half of the highest price of US$410 in July last year. DSCC predicted that the average panel price in the third quarter will fall by 15.7 percent. As Chinese companies’ price war and the effect of stagnation in consumption overlapped, the more LCD panels display makers produce, the more loss they suffer.

As panel prices fell, manufacturers responded by lowering facility utilization rates. DSCC said that the LCD factory utilization rate descended from 87 percent in April to 83 percent in May, 73 percent in June, and 70 percent in July.

Now that the LCD panel business has become no longer lucrative, Korean display makers have shut down their LCD business or shrunk their sizes. In the LCD sector, China has outpaced Korea since 2018. China’s LCD market share reached 50.9 percent in 2021, while that of Korea dropped to 14.4 percent, lower than Taiwan’s 31.6 percent.

Samsung Display already announced its withdrawal from the LCD business in June. Only 10 years have passed since the company was spun off from Samsung Electronics in 2012. LG Display has decided to halt domestic LCD TV panel production until 2023 and reorganize its business structure centering on OLED panels. Its Chinese LCD production line will be gradually converted to produce LCD panels for IT or commercial products. TrendForce predicted that LG Display will stop operating its P7 Plant in the first quarter of next year.

Korean display makers’ waning LCD business led to a situation in which Korea even lost first place in the display industry. Korea with a display market share of 33.2 percent was already overtaken by China with 41.5 percent) in 2021 according to market researcher Omdia and the Korea Display Industry Association. Korea’s market share has never rebounded in for five years since 2017 amid the Korean government’s neglect. Seventeen years have passed since 2004 when Korea overtook Japan to rise to the top of the world in the LCD industry. Korea’s LCD exports amounted to more than US$30 billion in 2014, but fell to US$21.4 billion last year.

A bigger problem is that Korean display makers may lose its leadership in the OLED panel sector although it is still standing at the top spot. While Korea’s OLED market share fell from 98.1 percent in 2016 to 82.8 percent last year, that of China rose from 1.1 percent to 16.6 percent. Considering that the high-end TV market is highly likely to shrink for the time being due to a full-fledged global consumption contraction, some analysts say that the technology gap between Korea and China can be sharply narrowed through this looming TV market slump. According to industry sources, the Chinese government is now focusing on giving subsidies to the development of OLED panel technology rather LCD technology. On the other hand, in Korea, displays were also wiped out from national strategic technology industry items under the Restriction of Special Taxation Act which can receive tax benefits for R&D activities on displays.

TrendForce’s latest research finds that TV brands’ promotional activities related to China’s Singles’ Day were helped by the steep decline in display panel prices. With panel prices reaching a very low level, TV brands were able to cut their prices further so as to raise shipments of whole TV sets during the promotional period. On the other hand, the major international brands have come into the second half of this year with a high level of inventory as their sales performances were weaker than expected during the first half. In order to effectively consume the existing inventory, TV brands have significantly corrected down the panel procurement quantity for 2H22. As a result, TrendForce now estimates that global TV shipments in 2H22 will reach 109 million units, reflecting a YoY decline of 2.7%. Global TV shipments during the whole 2022 are currently projected to total 202 million units, showing YoY decline of 3.9%. This annual shipment figure represents a decade low.

This year, the TV market has seen a continuous decline in shipments. Fortunately, there has also been a sharp drop in prices of large-sized panels. Furthermore, freight transportation costs have fallen by more than 50%. Thus, TV brands have been able to vigorously promote large-sized products, and the average size of TVs has also risen by 1.4 inches to 56 inches.

TrendForce further points out that moving into 2023, supply will remain fairly plentiful for TV panels. With the chance of a substantial rally in panel prices being extremely low, brands should feel an easing of cost pressure and have more flexibility when it comes to large-scale promotional activities. However, the IMF has downgraded its global economic growth forecast for 2023 to 2.7%. Moreover, the US, the Eurozone, and China as the world’s three largest regional economies will continue to experience stagnation. Regarding the ongoing inflation, it has recently started to ease a bit in Europe and the US, but the major regional consumer markets on the whole will continue be under its pressure. Because of these factors, TrendForce believes the growth momentum of TV shipments will be severely constrained next year. Global TV shipments are currently forecasted to again register a YoY decline for 2023, falling by 1.4% to 199 million units.

TV sales in China during this year have been noticeably affected by government measures for controlling local COVID-19 outbreaks. During this second half of the year, TV panel prices have fallen to a new record low, and brands have also been aggressively cutting prices so as to meet their annual shipments targets. However, despite all these, TV sales in China for the Singles’ Day period still fell nearly 10% YoY. Turning to the North America, TV sales there shrank by 16.5% YoY for 1H22 as the rapidly mounting inflationary pressure squeezed consumers’ budgets. Around that same time, TV brands also reached their limit in terms of inventory accumulation. To reduce the glut, brands conducted inventory check across all sections of their supply chains and made significant revisions to their procurement plans. Now, in 2H22, brands have been aggressively spurring demand. Full-scale promotional activities commenced on Amazon’s Prime Day, and TV sales were then ramped up to a peak on Black Friday. Among brands, TCL made the largest price concession for this year, cutting the price of its 55-inch Mini LED backlit model by 70% to US$199. Other brands also energetically promoted their particular product models in the holiday sales competition. On account of brands’ efforts, TV sales in North America for the Black Friday period rose by 13% YoY. While China and North America have exhibited very contrasting performances for the busy season, it is also clear that TV brands on the whole have gradually lowered their inventories to a relatively optimal level after months of promotional activities across channels and corrections to panel procurements.

Another notable development that TrendForce has observed in the TV market is the tepid performance of high-end products. Due to the lack of supporting broadcasting content and high retail prices, most TV brands have not been particularly keen on pushing 8K models. And after years of advocacy, Samsung remains the single dominant brand for 8K TVs with a market share almost 70%. Additionally, high inflation has eaten into consumers’ budgets this year. TrendForce therefore projects that 8K TV shipments will register a YoY decline for the first time in 2022, dropping by 7.4% to just about 400,000 units. It is also worth noting that Europe as one of the main sales regions for 8K TVs could be affected by the updated EU energy consumption labelling scheme (i.e., Energy Efficiency Index). Specifically, energy consumption rules have been further tightened so that some older 8K models could be banned from the region starting in March 2023. However, Samsung is planning to launch new 8K models that meet the updated energy consumption standards. Moreover, display panel suppliers continue to promote 8K products so as to widen adoption among TV brands. TrendForce currently forecasts that shipments of 8K TVs will surpass the 500,000 unit mark for 2023, registering a YoY growth of 20%.

TrendForce’s latest research on panel prices finds that LCD panel prices have plummeted. In fact, the price of a 55-inch UHD LCD was 4.8 times lower than the price of a WOLED (white OLED) O/C panel at the end of 3Q22. With the price difference between the two panels returning to where it was at the start of 2020, selling WOLED TVs have been quite challenging for brands that do offer this kind of product. Therefore, TrendForce estimates that shipments of WOLED TVs will shrink by 6.2% YoY to 6.29 million units for 2022. Assuming that LG Display does not want to sacrifice profitability, it will maintain a conservative pricing strategy when quoting WOLED panels next year. Given this situation, TrendForce forecasts that WOLED TV shipments will dip again by 2.7% YoY for 2023.

SEOUL, April 27 (Reuters) - LG Display Co Ltd (034220.KS) saw first-quarter profit plummet far below forecasts and warned of a further drop in panel prices as pandemic-driven demand for TVs, smartphones and laptops fades and competition heats up.

The South Korean Apple Inc (AAPL.O) supplier said it would shift its focus to higher-end products and gradually lower production of more commoditised LCD TV panels where it lacked a competitive advantage over cheaper Chinese rivals.

The LCD TV market shrank by more than 10% in the first quarter and Chinese competitors are pricing their products lower than LG Display"s expectations, Lee Tai-jong, head of the company"s large display marketing division, said on a call with analysts.

"Margins have been squeezed chiefly due to panel price declines and weaker demand, as consumers have already bought many screens during COVID-19 in the past two years," said Kim Yang-jae, an analyst at DAOL Investment & Securities.

In the first quarter, prices of 55-inch liquid crystal display (LCD) panels for TV sets fell 16% from the previous quarter while prices of LCD panels for notebooks and monitors dropped by around 7% to 11%, according to data from TrendForce"s WitsView.

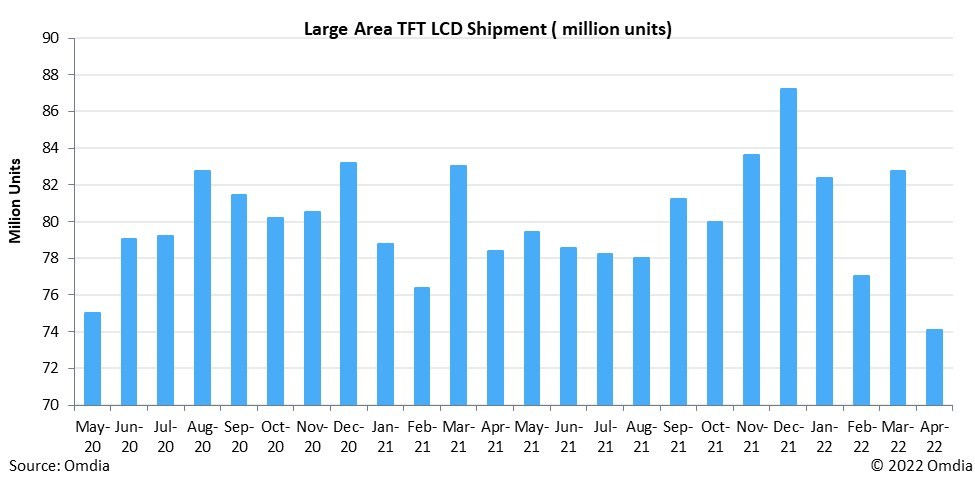

Large-area TFT LCD panel shipments decreased by 10% Month on Month (MoM) and 5% Year on Year (YoY) in April, to 74.1million units, representing historically low shipment performance since May 2020. Omdia defines large-area TFT LCD displays as larger than 9 inches.

"With continued ramifications from the pandemic, demand for IT panels for monitors and notebook PCs remained strong in 4Q21. But as the market became saturated starting in 2022, IT panel shipments started slowing in 1Q22 and early 2Q22," said Robin Wu, Principal Analyst for Large Area Display & Production, Omdia.

Wu said that notebook panel shipments decreased 21% MoM in April, to 18.2 million units, or a 33% decrease from a peak of 27.3 million units in November 2021.

While TV panel prices have decreased noticeably since 3Q21, TV LCD panel shipments increased to a peak of 23.4 million in December 2021, driven by low prices. But rising inflation, the Ukraine crisis and continued lockdowns in China have slowed demand. As a result, TV panel shipments posted a 9% MoM decline in April, to 21.7million units.

Many TV panel prices have fallen below manufacturing cost, and panel makers began to lose money in their TV panel business starting in 4Q21. But Chinese panel makers, the biggest capacity owners, still haven"t reduced their fab utilization. With no sign of demand recovery in 2Q22 or even 3Q22, the supply/demand situation is unlikely to see improvement, Wu said.

"IT LCD panels could still deliver positive cash flow for panel makers. But with prices dropping dramatically, panel makers will soon start to lose money in their IT panel business," Wu said. "Maybe only then will panel makers reduce their glass input and the overall supply/demand situation will return to balance."

LCD panel prices have risen for 4 months in a row because of your home gaming? Since this year, the whole LCD panel market smoke. Whether after the outbreak of the epidemic, LCD panel market prices rose for four months, or the panel giants in Japan and South Korea successively sold production lines, or the Chinese mainland listed companies frequently integrated acquisition, investment, and plant construction, all make the industry full of interesting.

LCD panel pricesare already a fact. Since May this year, LCD panel prices have risen for four months in a row, making the whole industry chain dynamic. Why are LCD panels going up in price in a volatile 2020? The key factor lies in the imbalance between supply and demand.

For larger sizes, overseas stocks remained strong, with prices for 65 inches and 75 inches rising $10 on average to $200 and $305 respectively in September.

The price of LCDS for large-size TVs of 70 inches or more hasn"t budged much. In addition, LTPS screens and AMOLED screens used in high-end phones have seen little or no increase in price.

As for October, LCD panel price increases are expected to moderate. The data shows that in October 32 inches or 2 dollars; Gains of 39.5 to 43 inches will shrink to $3;55 inches will fall back below $10; The 65-inch gain will narrow to $5.

During the epidemic, people stayed at home and had no way to go out for entertainment. They relied on TV sets, PCS, and game consoles for entertainment. After the resumption of economic work and production, the market of traditional home appliances picked up rapidly, and LCD production capacity was quickly digested.

However, due to the shutdown of most factories lasting 1-2 months during the epidemic period, LCD panel production capacity was limited, leading to insufficient production capacity in the face of the market outbreak, which eventually led to the market shortage and price increase for 4 consecutive months.

In fact, the last round of price rise of LCD panel was from 2016 to 2017, and its overall market price has continued to fall since 2018. Even in 2019, individual types have fallen below the material cost, and the whole industry has experienced a general operating loss. As a result, LCD makers have been looking for ways to improve margins since last year.

A return to a reasonable price range is the most talked about topic among panel makers in 2019, according to one practitioner. Some manufacturers for the serious loss of the product made the decision to reduce production or even stop production; Some manufacturers planned to raise the price, but due to the epidemic in 2020, the downstream demand was temporarily suppressed and the price increase was postponed. After the outbreak was contained in April, LCD prices began to rise in mid-to-late May.

This kind of price correction is in line with the law of industrial development. Only with reasonable profit space can the whole industry be stimulated to move forward.

In fact, the market price of LCD panels continued to decline in 2018-2019 because of the accelerated rise of China"s LCD industry and the influx of a large number of local manufacturers, which doubled the global LCD panel production capacity within a few years, but there was no suitable application market to absorb it. The result of excess capacity is oversupply, ultimately making LCD panel prices remain depressed.

Against this background, combined with the impact of the epidemic in 2020, the operating burden of LCD companies in Japan and South Korea has been further aggravated, and it is difficult to make profits in the production of LCD panels, so they have to announce the withdrawal of LCD business.

business in June 2022. In August, Sharp bought JDI Baishan, a plant in Ishikawa prefecture that makes liquid crystal display panels for smartphones. In early September, Samsung Display sold a majority stake in its SUZHOU LCD production plant to Starlight Electronics Technology, a unit of TCL Technology Group. LGD has not only pulled out of some of its production capacity but has announced that it will close its local production line in 2020. According to DSCC, a consultancy, the share of LCD production capacity in South Korea alone will fall from 19% to 7% between 2020 and 2021.

It is worth mentioning that in industry analysis, in view of the fact that Korean companies are good at using "dig through old bonus - selling high price - the development of new technology" the cycle of development mode, another 2020 out of the LCD production capacity, the main reason may be: taking the advantage of China"s expanding aggressively LCD manufacturers, Korean companies will own LCD panel production line hot sell, eliminating capacity liquid to extract its final value, and turning to the more profitable advantage of a new generation of display technologies, such as thinner, color display better OLED, etc. Samsung, for example, has captured more than 80% of the OLED market with its first-mover advantage.

From the perspective of production capacity, the launch of LCD tracks by major manufacturers in Japan and South Korea must reduce some production capacity in the short term, which to some extent induces market price fluctuations. In the long run, some of the Japanese and Korean LCD production capacity has been bought by Chinese manufacturers, coupled with frequent investment in recent years, the overall capacity is sure to recover as before, or even more than before. But now it will take time to expand the production layout, more or less will cause supply imbalance, the industry needs to be cautious.

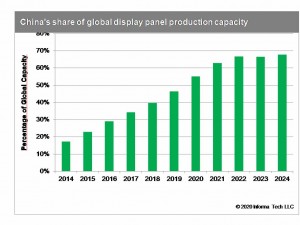

The LCD panel industry started in the United States and then gradually moved to Japan, South Korea, China, and Taiwan. At present, the proportion of production capacity in The Chinese mainland has reached 52% in 2020, and there are leading LCD panel products in China represented by BOE, Huxing Optoelectronics. Meanwhile, the production capacity layout of BOE, Huike, Huxing Optoelectronics, and other manufacturers has been basically completed, making industrial integration a necessity.

On the one hand, South Korean enterprises out of the LCD track, the domestic factory horse enclosure, plant expansion action. While LCDs may not sell as well as "upstart" flexible screens, respondents believe they are still strong enough in the traditional home appliance market to warrant continued investment. Zhao Bin, general manager of TCL Huaxing Development Center, has said publicly that the next-generation display technology will be mature in four to five years, but the commercialization of products may not take place until a decade later. "LCD will still be the mainstream in this decade," he said.

On the other hand, there is no risk of neck jam in China"s LCD panel industry, which is generally controllable. In mainland China, there will be 21 production lines capable of producing 32-inch or larger LCD panels by 2021, accounting for about two-thirds of the global total. In terms of the proportion of production capacity, the Chinese mainland accounted for 42% of the global LCD panel in 2019, 51% this year, and will continue to climb to 63% next year.

Of course, building factories and expanding production cannot be accomplished overnight. In the process of production capacity recovery, it is predicted that there will be several price fluctuations, and the cost may be passed on to the downstream LCD panel manufacturers or consumers when the price rises greatly, which requires continuous attention.

SEOUL, May 27 (Yonhap) -- China"s sweeping COVID-19 lockdowns are sending a shockwave in the display panel industry by exacerbating supply chain woes and parts procurement problems.

In April, global shipments of liquid crystal display (LCD) panels fell 15 percent from a year earlier amid the prolonged lockdowns in China, according to industry tracker Omdia.

The drop in shipments is largely blamed on production suspension at major parts suppliers, device makers and assemblers in China, following the implementation of stringent lockdown measures to keep the highly transmissible omicron variant at bay under its zero-tolerance coronavirus policy.

China"s lockdowns have dealt a serious blow to the production of set products, which in turn is sending a ripple effect throughout the supply chain of parts, including display panels.

The company reported dismal first-quarter earnings last month, with its net income dropping nearly 80 percent from a year ago, on lower demand for IT products, falling TV panel prices and parts procurement difficulties.

Demand for LCD panels has been waning, as most countries have lifted pandemic restrictions and people spend less time at home and on personal IT devices. Enterprise demand has also been slower than expected, the company said, due to the hostile macro environment.

LG Display could "swing to loss in the second quarter for the first time in eight quarters, as LCD panel prices have continued to fall and sales of IT panels, the company"s core product line, fell more than 10 percent due to China"s COVID-19 situation," analyst Kwon Sung-ryul from DB Financial Investment wrote in his latest report.

This photo, provided by LG Display Co., shows Turkish-American artist Refik Anadol"s NFT collection, "An Important Memory for Humanity," on the panel maker"s transparent organic light-emitting diode. (PHOTO NOT FOR SALE) (Yonhap)

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey