lcd panel price drop quotation

Recently, it was announced that the 32-inch and 43-inch panels fell by approximately USD 5 ~ USD 6 in early June, 55-inch panels fell by approximately USD 7, and 65-inch and 75-inch panels are also facing overcapacity pressure, down from USD 12 to USD 14. In order to alleviate pressure caused by price decline and inventory, panel makers are successively planning to initiate more significant production control in 3Q22. According to TrendForce’s latest research, overall LCD TV panel production capacity in 3Q22 will be reduced by 12% compared with the original planning.

As Chinese panel makers account for nearly 66% of TV panel shipments, BOE, CSOT, and HKC are industry leaders. When there is an imbalance in supply and demand, a focus on strategic direction is prioritised. According to TrendForce, TV panel production capacity of the three aforementioned companies in 3Q22 is expected to decrease by 15.8% compared with their original planning, and 2% compared with 2Q22. Taiwanese manufacturers account for nearly 20% of TV panel shipments so, under pressure from falling prices, allocation of production capacity is subject to dynamic adjustment. On the other hand, Korean factories have gradually shifted their focus to high-end products such as OLED, QDOLED, and QLED, and are backed by their own brands. However, in the face of continuing price drops, they too must maintain operations amenable to flexible production capacity adjustments.

TrendForce indicates, that in order to reflect real demand, Chinese panel makers have successively reduced production capacity. However, facing a situation in which terminal demand has not improved, it may be difficult to reverse the decline of panel pricing in June. However, as TV sizes below 55 inches (inclusive) have fallen below their cash cost in May (which is seen as the last line of defense for panel makers) and are even flirting with the cost of materials, coupled with production capacity reduction from panel makers, the price of TV panels has a chance to bottom out at the end of June and be flat in July. However, demand for large sizes above 65 inches (inclusive) originates primarily from Korean brands. Due to weak terminal demand, TV brands revising their shipment targets for this year downward, and purchase volume in 3Q22 being significantly cut down, it is difficult to see a bottom for large-size panel pricing. TrendForce expects that, optimistically, this price decline may begin to dissipate month by month starting in June but supply has yet to reach equilibrium, so the price of large sizes above 65 inches (inclusive) will continue to decline in 3Q22.

TrendForce states, as panel makers plan to reduce production significantly, the price of TV panels below 55 inches (inclusive) is expected to remain flat in 3Q22. However, panel manufacturers cutting production in the traditional peak season also means that a disappointing 2H22 peak season is a foregone conclusion and it will not be easy for panel prices to reverse. However, it cannot be ruled out, as operating pressure grows, the number and scale of manufacturers participating in production reduction will expand further and its timeframe extended, enacting more effective suppression on the supply side, so as to accumulate greater momentum for a rebound in TV panel quotations.

According to TrendForce"s latest panel price report, TV panel pricing is expected to arrest its fall in October after five consecutive quarters of decline and the prices of certain panel sizes may even be poised to move up. The price decline of IT panels, whether notebook panels or LCD monitor panels, has also begun showing signs of easing and overall pricing of large-size panels is developing towards bottoming out.

TrendForce indicates, with panel makers actively implementing production reduction plans, TV inventories have also experienced a period of adjustment, with pressure gradually being alleviated. At the same time, the arrival of peak sales season at year’s end has also boosted demand marginally. In particular, Chinese brands are still holding out hope for Double Eleven (Singles’ Day) Shopping Festival promotions and have begun to increase their stocking momentum in turn. Under the influence of strictly controlled utilization rate and marginally stronger demand, TV panel pricing, which are approaching the limit of material costs, is expected to halt its decline in October. Prices of panels below 75 inches (inclusive) are expected to cease their declines. The strength of demand for 32-inch products is the most obvious and prices are expected to increase by US$1. As for other sizes, it is currently understood that PO (Purchase Order) quotations given by panel manufacturers in October have are all increased by US$3~5. Currently China"s Golden Week holiday is ongoing but, after the holiday, panel manufacturers and brands are expected to wrestle with pricing. Based on prices stabilizing, whether pricing can actually be increased still depends on the intensity of demand generated by branded manufacturers for different sized products.

TrendForce observes that current demand for monitor panels is weak, and brands are poorly motivated to stock goods. At the same time, the implementation of production cuts by panel manufacturers has played a role and room for price negotiation has gradually narrowed. At present, the decline in panel pricing has slowed. Prices of small-size TN panels below 21.5 inches (inclusive) are expected to cease declining in October due to reduced supply and flat demand. As for mainstream sizes such as 23.8 and 27-inch, price declines are expected to be within US$1.5. The current demand for notebook panels is also weak and customers must still face high inventory issues and are relatively unwilling to buy panels. Panel makers are also trying to slow the decline in panel prices through their implementation of production reduction plans. Declining panel prices are currently expected to continue abating in October. Pricing for 14-inch and 15.6-inch HD TN panels are expected to drop by US$0.2~0.3, falling from a 1.8% drop in September to 0.7%, while pricing for 14-inch and 15.6-inch FHD IPS panels are expected to fall by US$1~1.2, falling from a 3.4% drop in September to 2.4%.

Compared with past instances when TV panels drove a supply/demand reversal through a sharp increase in demand and spiking prices, this current period of lagging TV panel pricing has been halted and reversed through active control of utilization rates by panel manufacturers and a slight increase in demand momentum. The basis for this break in decline and subsequent price increase is relatively weak. Therefore, in order to maintain the strength of this price backstop and eventual escalation and move towards a healthier supply/demand situation, panel manufacturers must continue to strictly and prudently control the utilization rate of TV production lines, in addition to observing whether sales performance from the forthcoming Chinese festivals beat expectations, allowing stocking momentum to continue, and laying a solid foundation for TV panels to completely escape sluggish market conditions.

The price of IT panels has also adhered to the effect of production reduction and the magnitude of its price drops has gradually eased. TrendForce believes, since the capacity for supplying IT panels is still expanding into the future, it is difficult to see declines in mainstream panel prices halt completely when demand remains weak. Even if new production capacity from Chinese panel factories is gradually completed starting from 2023, price competition in the IT panel market will intensify once products are verified by branded clients, so potential downward pressure in pricing still exists.

TrendForce’s latest research finds that TV brands’ promotional activities related to China’s Singles’ Day were helped by the steep decline in display panel prices. With panel prices reaching a very low level, TV brands were able to cut their prices further so as to raise shipments of whole TV sets during the promotional period. On the other hand, the major international brands have come into the second half of this year with a high level of inventory as their sales performances were weaker than expected during the first half. In order to effectively consume the existing inventory, TV brands have significantly corrected down the panel procurement quantity for 2H22. As a result, TrendForce now estimates that global TV shipments in 2H22 will reach 109 million units, reflecting a YoY decline of 2.7%. Global TV shipments during the whole 2022 are currently projected to total 202 million units, showing YoY decline of 3.9%. This annual shipment figure represents a decade low.

This year, the TV market has seen a continuous decline in shipments. Fortunately, there has also been a sharp drop in prices of large-sized panels. Furthermore, freight transportation costs have fallen by more than 50%. Thus, TV brands have been able to vigorously promote large-sized products, and the average size of TVs has also risen by 1.4 inches to 56 inches.

TrendForce further points out that moving into 2023, supply will remain fairly plentiful for TV panels. With the chance of a substantial rally in panel prices being extremely low, brands should feel an easing of cost pressure and have more flexibility when it comes to large-scale promotional activities. However, the IMF has downgraded its global economic growth forecast for 2023 to 2.7%. Moreover, the US, the Eurozone, and China as the world’s three largest regional economies will continue to experience stagnation. Regarding the ongoing inflation, it has recently started to ease a bit in Europe and the US, but the major regional consumer markets on the whole will continue be under its pressure. Because of these factors, TrendForce believes the growth momentum of TV shipments will be severely constrained next year. Global TV shipments are currently forecasted to again register a YoY decline for 2023, falling by 1.4% to 199 million units.

TV sales in China during this year have been noticeably affected by government measures for controlling local COVID-19 outbreaks. During this second half of the year, TV panel prices have fallen to a new record low, and brands have also been aggressively cutting prices so as to meet their annual shipments targets. However, despite all these, TV sales in China for the Singles’ Day period still fell nearly 10% YoY. Turning to the North America, TV sales there shrank by 16.5% YoY for 1H22 as the rapidly mounting inflationary pressure squeezed consumers’ budgets. Around that same time, TV brands also reached their limit in terms of inventory accumulation. To reduce the glut, brands conducted inventory check across all sections of their supply chains and made significant revisions to their procurement plans. Now, in 2H22, brands have been aggressively spurring demand. Full-scale promotional activities commenced on Amazon’s Prime Day, and TV sales were then ramped up to a peak on Black Friday. Among brands, TCL made the largest price concession for this year, cutting the price of its 55-inch Mini LED backlit model by 70% to US$199. Other brands also energetically promoted their particular product models in the holiday sales competition. On account of brands’ efforts, TV sales in North America for the Black Friday period rose by 13% YoY. While China and North America have exhibited very contrasting performances for the busy season, it is also clear that TV brands on the whole have gradually lowered their inventories to a relatively optimal level after months of promotional activities across channels and corrections to panel procurements.

Another notable development that TrendForce has observed in the TV market is the tepid performance of high-end products. Due to the lack of supporting broadcasting content and high retail prices, most TV brands have not been particularly keen on pushing 8K models. And after years of advocacy, Samsung remains the single dominant brand for 8K TVs with a market share almost 70%. Additionally, high inflation has eaten into consumers’ budgets this year. TrendForce therefore projects that 8K TV shipments will register a YoY decline for the first time in 2022, dropping by 7.4% to just about 400,000 units. It is also worth noting that Europe as one of the main sales regions for 8K TVs could be affected by the updated EU energy consumption labelling scheme (i.e., Energy Efficiency Index). Specifically, energy consumption rules have been further tightened so that some older 8K models could be banned from the region starting in March 2023. However, Samsung is planning to launch new 8K models that meet the updated energy consumption standards. Moreover, display panel suppliers continue to promote 8K products so as to widen adoption among TV brands. TrendForce currently forecasts that shipments of 8K TVs will surpass the 500,000 unit mark for 2023, registering a YoY growth of 20%.

TrendForce’s latest research on panel prices finds that LCD panel prices have plummeted. In fact, the price of a 55-inch UHD LCD was 4.8 times lower than the price of a WOLED (white OLED) O/C panel at the end of 3Q22. With the price difference between the two panels returning to where it was at the start of 2020, selling WOLED TVs have been quite challenging for brands that do offer this kind of product. Therefore, TrendForce estimates that shipments of WOLED TVs will shrink by 6.2% YoY to 6.29 million units for 2022. Assuming that LG Display does not want to sacrifice profitability, it will maintain a conservative pricing strategy when quoting WOLED panels next year. Given this situation, TrendForce forecasts that WOLED TV shipments will dip again by 2.7% YoY for 2023.

In another ominous sign for global TV industry supply, both demand and prices for TV-sized LCD panels continue to fall at the same time, recent reports from two display market analysts revealed.

Display industry market analysts TrendForce and Omdia each issued potentially troubling LCD TV display panel business updates this week as the global economic outlook continues to impact discretionary spending for non-essential items like TV sets.

According to TrendForce, the outlook for purchases by TV makers of LCD TV display panels — the major component part for LCD-based TVs that represent the vast majority of the TV sets — continues to decline even as prices for most panel sizes have fallen to record lows.

Recently, it was announced that the 32-inch and 43-inch panels fell by approximately $5-$6 in early June, 55-inch panels fell approximately $7, and prices for 65-inch and 75-inch panels, which face mounting overcapacity pressure, were down $12 to $14, TrendForce said.

“In order to alleviate pressure caused by price decline and inventory, panel makers are successively planning to initiate more significant production control in [the third quarter of 2022],” TrendForce said. “..Overall LCD TV panel production capacity in [the third quarter] will be reduced by 12% compared with original planning.”

According Omdia prices for TV-sized LCD display panels have been falling for the first year since Covid-19 appeared, while the increase in display demand area is expected to be up just 3%, half of the previous year.

Similarly, Omdia’s forecast released Thursday showed global display sales this year would decrease by 15% from last year to $133.18 billion. That compares to the global display sales increases of 14% in 2020 and 26% in 2021 due to the surge in demand for LCD panels and TVs generated by lockdowns forced by the pandemic.

LCD TV panel sales this year are expected to drop by 32% from last year ($38.3 billion) to $25.8 billion, according to Omdia’s predictions. The LCD TV panel demand area is expected to increase by 2% this year from last year, but the panel price decline is large.

“When there is an imbalance in supply and demand, a focus on strategic direction is prioritized,” TrendForce said. “TV panel production capacity of the three aforementioned companies in [Q3 2022] is expected to decrease by 15.8% compared with their original planning, and 2% compared with [the second quarter.]

TrendForce said Taiwanese manufacturers account for nearly 20% of TV panel shipments, and allocation of production capacity among those factories is now subject to “dynamic adjustment.”

The firm said TV sizes 55 inches and below have “fallen below their cash cost in May (which is seen as the last line of defense for panel makers) and is even flirting with the cost of materials, coupled with production capacity reduction from panel makers, the price of TV panels has a chance to bottom out at the end of June and be flat in July.”

However, the firm said, optimistically, “this price decline may begin to dissipate month by month starting in June but supply has yet to reach equilibrium, so the price of large sizes [65 inches and above] will continue to decline in [the third quarter].”

TrendForce said that as panel makers continue to significant reduce production, the price of TV panels 55 inches and under is expected to remain flat in through the third quarter.

“Panel manufacturers cutting production in the traditional peak season also means that a disappointing [second half 2022] peak season is a foregone conclusion and it will not be easy for panel prices to reverse,” according to TrendForce.

It is possible that if the supply/pricing pressures continue, the number, scale and duration of manufacturers cutting panel production output will grow in an effort to generate momentum for a rebound in TV panel quotations, TrendForce said.

As reported by S. Korean technology trade news site The Elec, Omdia said the LCD TV panel shipment targets for BOE were lowered to 60 million units this year from the original 65.5 million units. HKC decreased its targets from 49.5 million to 42 million, CSOT from 45 to 44.8 million, and LG Display from 23.5 million to 18 million. Innolux’s shipment target increased slightly from 34.5 million units to 34.6 million units.

On the other hand, organic light emitting diode (OLED) TV panel sales this year are expected to reach $5.4 billion, up 12% from last year ($4.8 billion), according to Omdia.

OLED TV panels are being mass-produced by LG Display and Samsung Display, as both manufacturers reduce their exposure in LCDs. Samsung Display will end LCD TV panel production entirly this summer. However, LG Display’s OLED panel production forecast is 10 times that of Samsung Display.

Meanwhile, Samsung Display hiked yield rates for its new large-size QD-OLED panels from 30% of capacity initially, 50% in 2021, 75% in April-May 2022 to 80% now, according to South Korea-based publication The Bell.

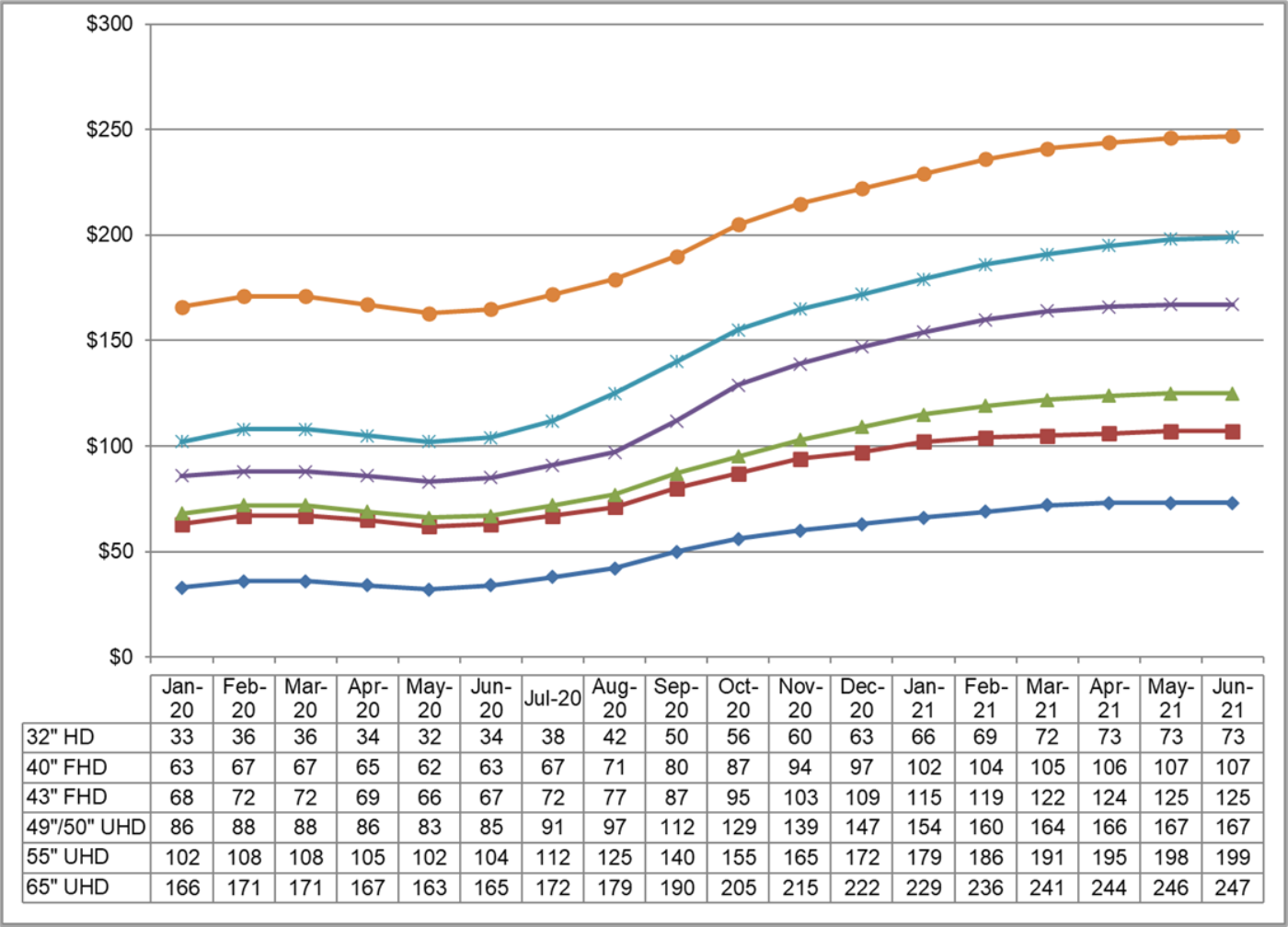

Prices for all TV panel sizes fluctuated and are forecast to fluctuate between 2020 and 2022. The period from March 2020 to July 2021 saw the biggest price increases, when a 65" UHD panel cost between 171 and 288 U.S. dollars. In the fourth quarter of 2021, such prices fell and are expected to drop to an even lower amount by March 2022.Read moreLCD TV panel prices worldwide from January 2020 to March 2022, by size(in U.S. dollars)Characteristic32" HD43" FHD49"/50" UHD55" UHD65" UHD------

DSCC. (January 10, 2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) [Graph]. In Statista. Retrieved February 22, 2023, from https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars)." Chart. January 10, 2022. Statista. Accessed February 22, 2023. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. (2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars). Statista. Statista Inc.. Accessed: February 22, 2023. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "Lcd Tv Panel Prices Worldwide from January 2020 to March 2022, by Size (in U.S. Dollars)." Statista, Statista Inc., 10 Jan 2022, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC, LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) Statista, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/ (last visited February 22, 2023)

LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) [Graph], DSCC, January 10, 2022. [Online]. Available: https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

That’s according to data from the market watcher WitsView, which said this week that LCD TV panel prices rose by just 0.3% from mid-June to July. That follows an earlier decrease in the rate of LCD TV panel price growth from mid-May to June, South Korean tech news website The Elec said.

LCD TV panel prices had endured years of decline up until early 2020, as the market became swamped by Chinese manufacturers that looked to compete with South Korea display makers on volume and cost. However, with the emergence of the COVID-19 pandemic last year and the disruption it caused to supply chains, the price of LCD TV panels jumped as they suddenly became more scarce. And prices have continued rising ever since.

Samsung Display and LG Display had both originally planned to quit making LCD TV display panels altogether, however the sharp rise in prices, coupled with a need to secure their own supply of them, caused them to postpone those plans. For instance Samsung Display, which was scheduled to stop making LCD TV panels in March 2021, announced in January that it would continue making them until at least the end of this year, and perhaps even longer. Just days later, LG Display announced that it too would keep its LCD TV panel production line up and running following a request from its parent firm LG Electronics, which was concerned about low supplies.

Despite the decelerating price growth seen last month, WitsView said the LCD TV display market remains very profitable as supplies are still tight. The price of a 75-inch LCD TV panel in at the beginning of July reached $407, up 0.2% from the month before. And 65-inch panel prices rose 0.3% to $297 in the same time frame.

Elsewhere, 55-inch panels hit an average price of $237, 50-inch panels were $198, 43-inch panels cost $148 and 32-inch panels sold for $88, WitsView said. The prices quoted are for 100 and 120Hz panels.

WitsView analysts said LCD panel prices are still much higher than one year ago. In July 2020, the average 75-inch display cost just $318, while 65-inch displays fetched $174 each. So prices are up about 30% on average, the data shows.

Another analyst firm, Display Supply Chain Consultants, has previously forecast that LCD panel prices will begin to decline in the second half of this year due to an expected reduction in demand in North American markets and greater supplies as factories in China return to normalcy. Even so, LCD TV panel makers are expected to continue to pump out as many panels as they can while the going is good, DSCC said.

Once the price of LCD TV panels returns to early 2020 levels, it’s expected that LG Display and Samsung Display will both go ahead with their plans to shutter production in favour of newer, more advanced display technologies such as OLED, QD-OLED, MicroLED and maybe even QNED.

SEOUL, April 27 (Reuters) - LG Display Co Ltd (034220.KS) saw first-quarter profit plummet far below forecasts and warned of a further drop in panel prices as pandemic-driven demand for TVs, smartphones and laptops fades and competition heats up.

The South Korean Apple Inc (AAPL.O) supplier said it would shift its focus to higher-end products and gradually lower production of more commoditised LCD TV panels where it lacked a competitive advantage over cheaper Chinese rivals.

The LCD TV market shrank by more than 10% in the first quarter and Chinese competitors are pricing their products lower than LG Display"s expectations, Lee Tai-jong, head of the company"s large display marketing division, said on a call with analysts.

"Margins have been squeezed chiefly due to panel price declines and weaker demand, as consumers have already bought many screens during COVID-19 in the past two years," said Kim Yang-jae, an analyst at DAOL Investment & Securities.

In the first quarter, prices of 55-inch liquid crystal display (LCD) panels for TV sets fell 16% from the previous quarter while prices of LCD panels for notebooks and monitors dropped by around 7% to 11%, according to data from TrendForce"s WitsView.

SEOUL, Jan 26 (Reuters) - South Korea"s LG Display Co Ltd (034220.KS) on Wednesday reported a 30% drop in quarterly operating profit as a one-off cost related to profit-sharing plan and lower TV panel prices offset solid shipments of smaller screens for computers, laptops and smartphones.

During the quarter, prices of 55-inch liquid crystal display (LCD) panels for TV sets fell 37% from the previous quarter, market data from TrendForce"s WitsView showed.

Solid shipments of high-end LCD panels for notebooks and monitors, whose prices declined by less than LCD TV panel prices in 2021, as well as higher-margin OLED panels for smartphones and TVs, should support LG"s results this year, analysts said.

LG Display said its shipments of advanced organic light-emitting diode (OLED) panels jumped more than 70% in 2021 and the display maker reached break-even in its OLED business.

Accidental Damage is any damage due to an unintentional act that is not the direct result of a manufacturing defect or failure. Accidental damage is not covered under the standard warranty of the product. Such damage is often the result of a drop or an impact on the LCD screen or any other part of the product which may render the device non-functional. Such types of damage are only covered under an Accidental Damage service offering which is an optional add-on to the basic warranty of the product. Accidental Damage must not be confused with an occasional dead or stuck pixel on the LCD panel. For more information about dead or stuck pixels, see the Dell Display Pixel Guidelines.

The LCD glass on the display is manufactured to rigorous specifications and standards and will not typically crack or break on its own under normal use. In general, cracked, or broken glass is considered accidental damage and is not covered under the standard warranty.

Internal cracks typically occur due to excessive force on the screen. This can be the result of some object hitting the screen, a drop, attempting to close the lid while an object is on the keypad area, or even holding the laptop by its screen.

Spots typically occur due to an external force hitting the screen causing damage to the LCD panel"s backlight assembly. While the top layer did not crack or break, the underlying area was compressed and damaged causing this effect.

If your Dell laptop LCD panel has any accidental damage but the laptop is not covered by the Accidental Damage service offering, contact Dell Technical Support for repair options.

How much does it cost to replace a MacBook Air screen? The cost to replace a MacBook Air screen is $299 for most models. The A1466 model is $179, while the A1932 and A1279 models are $299. The A2337 model is $299 for the LCD or $429 for the entire display.

This was the longest-running design for the screen on the MacBook Air. All the different models within these years are compatible with the same LCD panels. The cost seems to be coming down on the screen repairs for these A1369 and A1466 models. The cost to repair the screen on a 2010-2017 MacBook Air is $179. This will cover the LCD panel itself, the labor to install it, and the shipping to get the computer back to you.

Apple finally did a complete rebuild on the MacBook Air in 2018 and created a new model number A1932. The newer model has a redesigned display assembly that utilizes a different LCD panel and overall build than the prior 7 years of MacBook Air models. The cost to repair the screen of a 2018-2019 MacBook Air is $299.

The 2020-2021 MacBook Air looks basically identical to the 2018-2019 model, but the new model requires a different LCD panel than the older version of the laptop. There are actually 2 variations on this LCD panel. One is used for the intel-based models, and the other is used for the M1 models. I expect these LCD panels will be one of the harder-to-get models as it was only used for a single model of production.

The cost to replace a cracked LCD panel on an M1 2020 model A2337 MacBook Air is $299. If you would like to have the entire display assembly replaced with a genuine Apple display assembly, the .

Apple once again created an entirely new model with a completely redesigned screen in 2022 with their M2 MacBook Air. This new model hasn’t been out long enough for us to see what the price will end up being once the LCD panel is available on its own. For now, the cost to replace the full display assembly on the 2022 MacBook Air is $450-$750.

The LCD panel is the part of the screen that displays the image, it is the part of the screen that you can touch when the computer is open. This is the most commonly broken part on a MacBook Air screen. If you have a cracked screen, there is a very big chance that what you need is an LCD replacement.

The display assembly is the entire top half of the computer. It includes the LCD panel, the back housing where the Apple logo is, the clutch cover along the bottom of the screen where it says “MacBook Air”, the iSight camera, and the hinges. If there are any bends or dents on the corners of your display, you will likely need to replace the entire display assembly.

The clutch cover runs along the bottom of the MacBook screen. It is the part that says “MacBook Air” on it. Sometimes I see clutch covers that are cracked or broken while the LCD panel itself is working fine! This means the computer works perfectly and the entire screen is visible and working, but there is a crack along the bottom of the screen in the part that says “MacBook Air” on it. If this is the issue you have, you just need a clutch cover replacement rather than an LCD replacement.

The MacBook Air camera almost never has an issue. If the camera does stop responding, the issue is almost always with the logic board inside your computer rather than the camera itself. Sometimes though, the cameras will fail and require replacement. Unfortunately with the way these MacBook Airs are assembled, you usually have to replace the LCD panel when you replace the camera.

The back housing is sometimes referred to as the “lid”. It is the part that has the Apple logo on it. Usually, the housing does not need to be replaced, but if there is a dent on the corner of the housing, a dent on the housing itself, or if liquid damage is present in the housing, then you will need the housing replaced as well as the LCD. Again, because of the way these are assembled you normally can’t replace just the housing by itself.

Rossmanngroup – I have known the owner (Louise) since we were both newbies in the repair space. His shop provides great work at an affordable price. They are based in New York.

If you have a MacBook Air that is not covered under AppleCare+, you will spend between $450 and $650 repairing your screen through Apple. There are a couple of different ways that the display repair is billed, so the price you are quoted will vary, but these are the standard quotes. Note that each damage tier is added to by a labor charge, which is usually $100. So a Tier 1 repair is usually about $280 for the MacBook Air + a $100 labor charge.

UBreakiFix is not an Apple Authorized Service Provider. I do not know if they offer a genuine Apple screen (they could be utilizing Apple’s new self-repair program as I do for certain repairs), but I do know that their price for the 2020 M1 MacBook Air “starts at 479.99”. In order to get an exact quote, you have to bring your computer in for their free diagnosis.

The MacBook Air LCD replacement process is one that I don’t recommend for a beginner to an intermediate-level technician to attempt. It is best to start practicing with bad screens before moving on to these repairs. They are delicate and you can cause all kinds of problems during the repair by scratching backlight sheets or ripping cables under the LCD panel.

I will say I have seen a lot of damaged screens when people attempt to repair the LCD panel on a MacBook Air themselves. Normally the damage is not fixable and you have to then replace the entire display assembly. I have a troubleshooting page for the A1466 MacBook Air if you have attempted a repair and ran into problems.

If you are experienced enough to complete the repair, you can find the panels on public sites like iFixit, eBay, Amazon, etc. As a shop, you will probably want to work with your vendor to get panels that have a guarantee so you can hold them in stock. The price for panels usually ranges from around $100 to about $400 for the newest model. Generally, the panels decrease in price with time, but sometimes if an LCD panel is not used frequently by apple, they will become rare and cost more over time for new ones.

I have put together a few guides on how to replace the LCD yourself. I currently have a 2010-2017 display and LCD replacement guide available. I also have started working on an A2337 display replacement guide that is still a work in progress. I am also working on making video guides for screen repair and hope to have those posted by the March of 2023.

The cost to replace a MacBook Air screen is $299 for most models. The A1466 model is $179, while the A1932 and A1279 models are $299. The A2337 model is $299 for the LCD or $429 for the entire display.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey