lcd module technology comparison made in china

When it comes to cheap Labour, it is much cheaper in south-east Asia than in China. But why is China so popular? This involves the quality of the product. The reason why the labor force in many countries in southeast Asia is cheap is mainly that the economic level of these countries is not high, so no matter the production technology or technological level is inferior to China. To ensure the quality of their products, foreign companies naturally prefer to choose China.

In terms of product production efficiency, China is hard to compare with many other countries. According to relevant data, domestic product manufacturing efficiency is the highest in the world. On the one hand, this is because China’s factories have more comprehensive equipment and a high level of science and technology, which can shorten the production cycle of products. On the other hand, it is because of the high quality of Chinese workers, strong learning ability, and developed transportation, which also speeds up the operation of all aspects of product production.

It is believed that with the continuous development of Chinese manufacturing and science and technology, made-in-china manufactures will become more popular in the future.

Currently, the downstream segment of the PV industry – or at least a portion of the western world – is somewhat in panic mode over having to audit the supply channels of solar module producers, most of whom have been central to their global build-out plans over the past few years.

This article clarifies just how dominant the Chinese manufacturing sector is today within the PV industry, looking specifically at polysilicon, wafer, cell and module production stages. Also, the latest findings from our in-house PV ModuleTech Bankability Ratings analysis are shown, and discussed in relation to the ongoing made in China issue.

As government subsidies and incentives were reduced (or eliminated altogether) and solar started to compete with other forms of renewables in competitive auctions, it almost became an expectation that module prices would decline indefinitely at the ~ 10% annual rate. Until the end of 2020, this indeed was observed.

With the exception of First Solar (notably not made in China, and not silicon-based), the above summary largely explains why almost all of the module supply (for large-scale projects) is coming from Chinese-run companies. Without duties, or in the absence of any other manufacturing-related carve-out benefit for domestic manufacturing, nobody outside China can realistically come anywhere close to competing with these reported costs.

Today, PV manufacturing – as a global sector – has been decimated. A few module assembly fabs outside China (or their owned assets in Southeast Asia) are in operation, and every now and again an attempt is made to set up cell production. But the industry is dominated by Chinese manufacturing, and a lust for profits by global investors/developers.

The reaction of many global investors and developers today, following media coverage of the Xinjiang issue, is really quite painful to observe. With so many of the investor vehicles being public-listed – and acutely aware of public-perception and brand equity – it is fair to ask why so many largely ignored the fact that components (inverters, modules, steel) were all coming from China as a whole, or had parts made by Chinese companies producing in Southeast Asia. However, the reality is – did they actually have a choice?

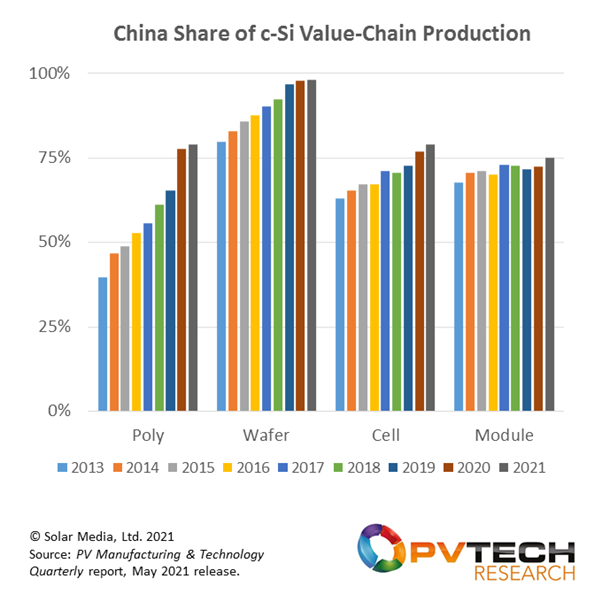

Removing thin-film module supply (all First Solar for simplicity), all other PV modules are largely similar. Polysilicon is pulled into ingots, these are then sliced into wafers; the wafers are processed into solar cells, and the cells are finally assembled into PV modules. Each step uses various raw materials (glass, silver, etc.); most, if not all, of these raw materials are also produced in China today.

However, the key steps to review now are polysilicon, wafer, cell and module. The figure below shows the percentage of production through the value chain for silicon-based modules, covering the period from 2013 to 2021.

Cell and module production have been seeing a somewhat static share from China, driven largely from Chinese companies having to produce cells and modules in Southeast Asia for US shipments. Again, as pointed out above, remove the 2012 CVD/AD and cell/module and production share levels in China would be above 90%.

From the graphic above, it is also clear that the China dominance is not new. Therefore, most solar farms built in the past decade will have various (if not all) module parts made in China, or at least, wafers (and probably polysilicon).

The PV ModuleTech Bankability Ratings analysis has now become the industry’s benchmark, in terms of understanding the financial and manufacturing health of leading module suppliers. It is used routinely by banks, investors, developers and (for benchmarking) module companies.

The latest (Q2 2021) hierarchy pyramid is shown below, with seven suppliers in the A grades. Compared to two years ago, when we launched the methodology, there are far fewer suppliers in the overall AAA-to-CC rating bands; this is coming from the increased shipment volumes from the leading players, and the relative share of the market from companies that have not kept up with market growth. However, there are still about 50 module suppliers to understand today, in order to perform benchmarking properly.

In reference to this article, it can be seen that First Solar and Hanwha Q CELLS are the leading non-Chinese entries. Aside from LONGi (by virtue of its wafering business), most of the leading module suppliers have similar models. JA Solar remains the leader in terms of in-house value chain production: others retain a more informal stance in terms of using third-party producers of components.

The other option is for some of the leading Chinese players to set up wafer and cell production outside China: without having to be forced into it! What a proactive move this would be, and would almost certainly see investors prioritising this in terms of future contractual module supply volumes. While the tendency can sometimes be to pick on the biggest player (or superpower) and try to impose sanctions to curb global dominance, making the market leaders part of the solution might not be a bad idea.

If you need detailed visibility across the PV manufacturing sector, our PV Manufacturing & Technology Report is an invaluable resource allowing you to track, benchmark and forecast the shifts in the PV market.

We are often asked to explain the difference between an LCD Module and an LCD Cell. These terminologies are sometimes misused, misinterpreted and often go unexplained leaving clients confused.Simply stated, an LCD Cell is a component within an LCD moduleIt happens to be the most important component that defines image quality and performance!

You wouldn"t typically purchase just an LCD Cell for your application. Cells are built into modules which are sold as "standard" products by LCD module makers, Cells are also used in semi-custom LCD module designs by display solution providers.

Aside from clarifying the terminologies, understanding the purpose of an LCD cell also helps support the value of working with a partner with a "build from cell" model....especially in volatile material market conditions as they are today.

It"s typical to find common mechanical and optical features across multiple LCD cells in any given size. For example, designing around a base 4.3" 800x480 resolution LCD cell with an IPS wide viewing cone and building an LCD module from there can yield:A de-risked supply chain with multiple qualified LCD cells

Take this approach into mid-large size display platforms and we start to see the possibility of "industrializing" consumer based LCD platforms. Typically OEM"s steer clear of such LCD Modules due to their short availability and often undesirable optical specifications but we are all lured in by amazing low pricing!Building a 15.6" 1920x1080 semi-custom module from a common cell platform using these strategies can result in a low cost, well supported optically robust LCD module solution

DCL Technologies has successfully designed LCD modules using this strategy from 2.x" to 15.6". If you"re looking for product differentiation and cost advantages while still getting great support and supply chain longevity and services, it"s worth a call!

One of today’s modern technological wonders is the flat-panel liquid crystal display (LCD) screen, which is the key component we find inside televisions, computer monitors, smartphones, and an ever-proliferating range of gadgets that display information electronically.What most people don’t realize is how complex and sophisticated the manufacturing process is. The entire world’s supply is made within two time zones in East Asia. Unless, of course, the factory proposed by Foxconn for Wisconsin actually gets built.

Last week I had the opportunity to tour BOE Technology Group’s Gen 10.5 factory in Hefei, the capital of China’s Anhui Province.This was the third factory, or “fab” that Beijing-based BOE built in Hefei alone, and in terms of capability, it is now the most advanced in the world.BOE has a total of 12 fabs in Beijing, Chongqing, and several other major cities across China; this particular factory was named Fab 9.

Liquid crystal display (LCD) screens are manufactured by assembling a sandwich of two thin sheets of glass.On one of the sheets are transistor “cells” formed by first depositing a layer of indium tin oxide (ITO), an unusual metal alloy that you can actually see through.That’s how you can get electrical signals to the middle of a screen.Then you deposit a layer of silicon, followed by a process that builds millions of precisely shaped transistor parts.This patterning step is repeated to build up tiny little cells, one for each dot (known as a pixel) on the screen.Each step has to be precisely aligned to the previous one within a few microns.Remember, the average human hair is 40 microns in diameter.

For the sake of efficiency, you would like to make as many panels on a sheet as possible, within the practical limitations of how big a sheet you can handle at a time.The first modern LCD Fabs built in the early 1990s made sheets the size of a single notebook computer screen, and the size grew over time. A Gen 5 sheet, from around 2003, is 1100 x 1300 mm, while a Gen 10.5 sheet is 2940 x 3370 mm (9.6 x 11 ft).The sheets of glass are only 0.5 - 0.7 mm thick or sometimes even thinner, so as you can imagine they are extremely fragile and can really only be handled by robots.The Hefei Gen 10.5 fab is designed to produce the panels for either eight 65 inch or six 75 inch TVs on a single mother glass.If you wanted to make 110 inch TVs, you could make two of them at a time.

The fab is enormous, 1.3 km from one end to the other, divided into three large buildings connected by bridges.LCD fabs are multi-story affairs.The main equipment floor is sandwiched between a ground floor that is filled with chemical pipelines, power distribution, and air handling equipment, and a third floor that also has a lot of air handling and other mechanical equipment.The main equipment floor has to provide a very stable environment with no vibrations, so an LCD fab typically uses far more structural steel in its construction than a typical skyscraper.I visited a Gen 5 fab in Taiwan in 2003, and the plant manager there told me they used three times as much structural steel as Taipei 101, which was the world’s tallest building from 2004- 2010.Since the equipment floor is usually one or two stories up, there are large loading docks on the outside of the building.When they bring the manufacturing equipment in, they load it onto a platform and hoist it with a crane on the outside of the building.That’s one way to recognize an LCD fab from the outside – loading docks on high floors that just open to the outdoors.

LCD fabs have to maintain strict standards of cleanliness inside.Any dust particles in the air could cause defects in the finished displays – tiny dark spots or uneven intensities on your screen.That means the air is passed through elaborate filtration systems and pushed downwards from the ceiling constantly.Workers have to wear special clean room protective clothing and scrub before entering to minimize dust particles or other contamination.People are the largest source of particles, from shedding dead skin cells, dust from cosmetic powders, or smoke particles exhaled from the lungs of workers who smoke.Clean rooms are rated by the number of particles per cubic meter of air.A class 100 cleanroom has less than 100 particles less than 0.3 microns in diameter per cubic meter of air, Class 10 has less than 10 particles, and so on. Fab 9 has hundeds of thousands of square meters of Class 100 cleanroom, and many critical areas like photolithography are Class 10.In comparison, the air in Harvard Square in Cambridge, MA is roughly Class 8,000,000, and probably gets substantially worse when an MBTA bus passes through.

The Hefei Gen 10.5 is one of the most sophisticated manufacturing plants in the world.On opening day for the fab, BOE shipped panels to Sony, Samsung Electronics, LG Electronics, Vizio, and Haier.So if you have a new 65 or 75-inch TV, there is some chance the LCD panel came from here.

TFT LCD is a mature technology. OLED is a relatively new display technology, being used in more and more applications. As for Micro LED, it is a new generation technology with very promising future. Followings are the pros and cons of each display technology.

TFT Liquid Crystal Display is widely used these days. Since LCD itself doesn"t emit light. TFT LCD relies on white LED backlight to show content. This is an explanation of how TFT LCD works.

Relatively lower contrast:Light needs to pass through LCD glasses, liquid crystal layer, polarizers and color filters. Over 90% is lost. Also, LCD can not display pure black.

Organic Light-Emitting Diode is built from an electro-luminescent layer that contains organic compounds, which emit light in response to an electric current. There are two types of OLED, Passive Matrix OLED (PMOLED) and Active Matrix OLED (AMOLED). These driving methods are similar to LCD"s. PMOLED is controlled sequentially using a matrix addressing scheme, m + n control signals are required to address a m x n display. AMOLED uses a TFT backplane that can switch individual pixels on and off.

Stroboscopic effect: most OLED screen uses PWM dimming technology. Some people who are easy perceive stroboscopic frequency may have sore eyes and tears.

Resistive Touch is the most widely used touch technology these days. Because it is cheaper to make and easier to use in different environments. A resistive touch screen is composed of two very thin layers of material, separated by a thin gap. The top layer is typically some type of clear polycarbonate material, while as the bottom layer is made from rigid material. LCD manufacturers normally use PET film and glass for these layers. The upper and bottom layers are lined with conducting material like indium tin oxide (ITO), facing each other, separated by a narrow gap. When a user touches the screen, two metallic layers make contact, it creates a change in resistance.

Capacitive touch panel technology relies on the capacitance of the human body, and not on mechanical pressure like resistive technology. There are two types of capacitive touch panels – surface capacitive and projected one.

Surface Capacitive Touch are the second most popular type of touch screens on the market. In a surface capacitive touch panel a thin glass surface covers capacitive touch screen. Under this glass surface, lies a thin layer of transparent electrodes on top of LCD glass panel.

FILE - A worker conducts quality-check of a solar module product at a factory of a monocrystalline silicon solar equipment manufacturer, in Xian, Shaanxi province, China, Dec. 10, 2019.

By comparison, China produces a little over 5% while the U.S. produces approximately 10%, according to market analysts. South Korea, Japan, and the Netherlands are the other sources of the product, which is at the heart of many electronic devices and machinery.

Semiconductor Manufacturing International Corp. (SMIC) in China, which has 5% of the global fabrication market, produces 14-nanometer chips. There is also evidence that SMIC has 7-nm technology, according to a TechInsights blog. These are considered less advanced than the 3-nm chips produced by TSMC.

Taiwan’s TSMC website states it is building a fabrication plant in the U.S. state of Arizona with the aim of starting production in 2024. It will produce semiconductor wafers using 5-nm technology. During her recent controversial visit to Taiwan, Pelosi met TSMC"s Liu. TSMC is expected to be one of the beneficiaries of the $52 billion CHIPS and Science Act.

The restriction would affect the shipment of machinery to produce 14 nm chips in China. This is an extension of the earlier ban, which prevented the supply of machinery for making advanced technology nodes of 10 nanometers. The idea is to cover a wider range of semiconductor equipment going to China.

From polysilicon production to soldering finished solar cells and modules onto panels, China has the largest share in every stage of solar panel manufacturing.

After China, the next leading nation in solar panel manufacturing is India, which makes up almost 3% of solar module manufacturing and 1% of cell manufacturing. To help meet the country’s goal of 280 gigawatts (GW) of installed solar power capacity by 2030 (currently 57.9 GW), in 2022 the Indian government allocated an additional $2.6 billion to its production-linked incentive scheme that supports domestic solar PV panel manufacturing.

Alongside China and India, the Asia-Pacific region also makes up significant amounts of solar panel manufacturing, especially modules and cells at 15.4% and 12.4% respectively.

In recent years, China and other countries have invested heavily in the research and manufacturing capacity of display technology. Meanwhile, different display technology scenarios, ranging from traditional LCD (liquid crystal display) to rapidly expanding OLED (organic light-emitting diode) and emerging QLED (quantum-dot light-emitting diode), are competing for market dominance. Amidst the trivium strife, OLED, backed by technology leader Apple"s decision to use OLED for its iPhone X, seems to have a better position, yet QLED, despite still having technological obstacles to overcome, has displayed potential advantage in color quality, lower production costs and longer life.

Which technology will win the heated competition? How have Chinese manufacturers and research institutes been prepared for display technology development? What policies should be enacted to encourage China"s innovation and promote its international competitiveness? At an online forum organized by National Science Review, its associate editor-in-chief, Dongyuan Zhao, asked four leading experts and scientists in China.

Zhao: We all know display technologies are very important. Currently, there are OLED, QLED and traditional LCD technologies competing with each other. What are their differences and specific advantages? Shall we start from OLED?

Huang: OLED has developed very quickly in recent years. It is better to compare it with traditional LCD if we want to have a clear understanding of its characteristics. In terms of structure, LCD largely consists of three parts: backlight, TFT backplane and cell, or liquid section for display. Different from LCD, OLED lights directly with electricity. Thus, it does not need backlight, but it still needs the TFT backplane to control where to light. Because it is free from backlight, OLED has a thinner body, higher response time, higher color contrast and lower power consumption. Potentially, it may even have a cost advantage over LCD. The biggest breakthrough is its flexible display, which seems very hard to achieve for LCD.

Liao: Actually, there were/are many different types of display technologies, such as CRT (cathode ray tube), PDP (plasma display panel), LCD, LCOS (liquid crystals on silicon), laser display, LED (light-emitting diodes), SED (surface-conduction electron-emitter display), FED (filed emission display), OLED, QLED and Micro LED. From display technology lifespan point of view, Micro LED and QLED may be considered as in the introduction phase, OLED is in the growth phase, LCD for both computer and TV is in the maturity phase, but LCD for cellphone is in the decline phase, PDP and CRT are in the elimination phase. Now, LCD products are still dominating the display market while OLED is penetrating the market. As just mentioned by Dr Huang, OLED indeed has some advantages over LCD.

Huang: Despite the apparent technological advantages of OLED over LCD, it is not straightforward for OLED to replace LCD. For example, although both OLED and LCD use the TFT backplane, the OLED’s TFT is much more difficult to be made than that of the voltage-driven LCD because OLED is current-driven. Generally speaking, problems for mass production of display technology can be divided into three categories, namely scientific problems, engineering problems and production problems. The ways and cycles to solve these three kinds of problems are different.

At present, LCD has been relatively mature, while OLED is still in the early stage of industrial explosion. For OLED, there are still many urgent problems to be solved, especially production problems that need to be solved step by step in the process of mass production line. In addition, the capital threshold for both LCD and OLED are very high. Compared with the early development of LCD many years ago, the advancing pace of OLED has been quicker.While in the short term, OLED can hardly compete with LCD in large size screen, how about that people may change their use habit to give up large screen?

Liao: I want to supplement some data. According to the consulting firm HIS Markit, in 2018, the global market value for OLED products will be US$38.5 billion. But in 2020, it will reach US$67 billion, with an average compound annual growth rate of 46%. Another prediction estimates that OLED accounts for 33% of the display market sales, with the remaining 67% by LCD in 2018. But OLED’s market share could reach to 54% in 2020.

Huang: While different sources may have different prediction, the advantage of OLED over LCD in small and medium-sized display screen is clear. In small-sized screen, such as smart watch and smart phone, the penetration rate of OLED is roughly 20% to 30%, which represents certain competitiveness. For large size screen, such as TV, the advancement of OLED [against LCD] may need more time.

Xu: LCD was first proposed in 1968. During its development process, the technology has gradually overcome its own shortcomings and defeated other technologies. What are its remaining flaws? It is widely recognized that LCD is very hard to be made flexible. In addition, LCD does not emit light, so a back light is needed. The trend for display technologies is of course towards lighter and thinner (screen).

But currently, LCD is very mature and economic. It far surpasses OLED, and its picture quality and display contrast do not lag behind. Currently, LCD technology"s main target is head-mounted display (HMD), which means we must work on display resolution. In addition, OLED currently is only appropriate for medium and small-sized screens, but large screen has to rely on LCD. This is why the industry remains investing in the 10.5th generation production line (of LCD).

Xu: While deeply impacted by OLED’s super thin and flexible display, we also need to analyse the insufficiency of OLED. With lighting material being organic, its display life might be shorter. LCD can easily be used for 100 000 hours. The other defense effort by LCD is to develop flexible screen to counterattack the flexible display of OLED. But it is true that big worries exist in LCD industry.

LCD industry can also try other (counterattacking) strategies. We are advantageous in large-sized screen, but how about six or seven years later? While in the short term, OLED can hardly compete with LCD in large size screen, how about that people may change their use habit to give up large screen? People may not watch TV and only takes portable screens.

Some experts working at a market survey institute CCID (China Center for Information Industry Development) predicted that in five to six years, OLED will be very influential in small and medium-sized screen. Similarly, a top executive of BOE Technology said that after five to six years, OLED will counterweigh or even surpass LCD in smaller sizes, but to catch up with LCD, it may need 10 to 15 years.

Xu: Besides LCD, Micro LED (Micro Light-Emitting Diode Display) has evolved for many years, though people"s real attention to the display option was not aroused until May 2014 when Apple acquired US-based Micro LED developer LuxVue Technology. It is expected that Micro LED will be used on wearable digital devices to improve battery"s life and screen brightness.

Micro LED, also called mLED or μLED, is a new display technology. Using a so-called mass transfer technology, Micro LED displays consist of arrays of microscopic LEDs forming the individual pixel elements. It can offer better contrast, response times, very high resolution and energy efficiency. Compared with OLED, it has higher lightening efficiency and longer life span, but its flexible display is inferior to OLED. Compared with LCD, Micro LED has better contrast, response times and energy efficiency. It is widely considered appropriate for wearables, AR/VR, auto display and mini-projector.

However, Micro LED still has some technological bottlenecks in epitaxy, mass transfer, driving circuit, full colorization, and monitoring and repairing. It also has a very high manufacturing cost. In short term, it cannot compete traditional LCD. But as a new generation of display technology after LCD and OLED, Micro LED has received wide attentions and it should enjoy fast commercialization in the coming three to five years.

Interestingly, quantum dots as light-emitting materials are related to both OLED and LCD. The so-called QLED TVs on market are actually quantum-dot enhanced LCD TVs, which use quantum dots to replace the green and red phosphors in LCD’s backlight unit. By doing so, LCD displays greatly improve their color purity, picture quality and potentially energy consumption. The working mechanisms of quantum dots in these enhanced LCD displays is their photoluminescence.

For its relationship with OLED, quantum-dot light-emitting diode (QLED) can in certain sense be considered as electroluminescence devices by replacing the organic light-emitting materials in OLED. Though QLED and OLED have nearly identical structure, they also have noticeable differences. Similar to LCD with quantum-dot backlighting unit, color gamut of QLED is much wider than that of OLED and it is more stable than OLED.

Another big difference between OLED and QLED is their production technology. OLED relies on a high-precision technique called vacuum evaporation with high-resolution mask. QLED cannot be produced in this way because quantum dots as inorganic nanocrystals are very difficult to be vaporized. If QLED is commercially produced, it has to be printed and processed with solution-based technology. You can consider this as a weakness, since the printing electronics at present is far less precision than the vacuum-based technology. However, solution-based processing can also be considered as an advantage, because if the production problem is overcome, it costs much less than the vacuum-based technology applied for OLED. Without considering TFT, investment into an OLED production line often costs tens of billions of yuan but investment for QLED could be just 90–95% less.

Given the relatively low resolution of printing technology, QLED shall be difficult to reach a resolution greater than 300 PPI (pixels per inch) within a few years. Thus, QLED might not be applied for small-sized displays at present and its potential will be medium to large-sized displays.

Peng: Good questions. Ligand chemistry of quantum dots has developed quickly in the past two to three years. Colloidal stability of inorganic nanocrystals should be said of being solved. We reported in 2016 that one gram of quantum dots can be stably dispersed in one milliliter of organic solution, which is certainly sufficient for printing technology. For the second question, several companies have been able to mass produce quantum dots. At present, all these production volume is built for fabrication of the backlighting units for LCD. It is believed that all high-end TVs from Samsung in 2017 are all LCD TVs with quantum-dot backlighting units. In addition, Nanosys in the United States is also producing quantum dots for LCD TVs. NajingTech at Hangzhou, China demonstrate production capacity to support the Chinese TV makers. To my knowledge, NajingTech is establishing a production line for 10 million sets of color TVs with quantum-dot backlighting units annually.China"s current demands cannot be fully satisfied from the foreign companies. It is also necessary to fulfill the demands of domestic market. That is why China must develop its OLED production capability.

So, originally, OLED was only one of Samsung"s several alternative technology pathways. But step by step, it achieved an advantageous status in the market and so tended to maintain it by expanding its production capacity.

Huang: The importance of China"s LCD manufacturing is now globally high. Compared with the early stage of LCD development, China"s status in OLED has been dramatically improved. When developing LCD, China has adopted the pattern of introduction-absorption-renovation. Now for OLED, we have a much higher percentage of independent innovation.

Although we cannot say that our advantages triumph over ROK, where Samsung and LG have been dominating the field for many years, we have achieved many significant progresses in developing the material and parts of OLED. We also have high level of innovation in process technology and designs. We already have several major manufacturers, such as Visionox, BOE, EDO and Tianma, which have owned significant technological reserves.

units for LCD and electroluminescence in QLED. For the photoluminescence applications, the key is quantum-dot materials. China has noticeable advantages in quantum-dot materials.

After I returned to China, NajingTech (co-founded by Peng) purchased all key patents invented by me in the United States under the permission of US government. These patents cover the basic synthesis and processing technologies of quantum dots. NajingTech has already established capability for large-scale production of quantum dots. Comparatively, Korea—represented by Samsung—is the current leading company in all aspects of display industry, which offers great advantages in commercialization of quantum-dot displays. In late 2016, Samsung acquired QD Vision (a leading quantum-dot technology developer based in the United States). In addition, Samsung has invested heavily in purchasing quantum-dot-related patents and in developing the technology.

China is internationally leading in electroluminescence at present. In fact, it was the 2014 Nature publication by a group of scientists from Zhejiang University that proved QLED can reach the stringent requirements for display applications. However, who will become the final winner of the international competition on electroluminescence remains unclear. China"s investment in quantum-dot technology lags far behind US and ROK. Basically, the quantum-dot research has been centered in US for most of its history, and South Korean players have invested heavily along this direction as well.

For electroluminescence, it is very likely to co-exist with OLED for a long period of time. This is so because, in small screen, QLED’s resolution is limited by printing technology.

Huang: When OLED was compared with LCD in the past, lots of advantages of OLED were highlighted, such as high color gamut, high contrast and high response speed and so on. But above advantages would be difficult to be the overwhelming superiority to make the consumers to choose replacement.

It seems to be possible that the flexible display will eventually lead a killer advantage. I think QLED will also face similar situation. What is its real advantage if it is compared with OLED or LCD? For QLED, it seems to have been difficult to find the advantage in small screen. Dr. Peng has suggested its advantage lies in medium-sized screen, but what is its uniqueness?

Peng: The two types of key advantages of QLED are discussed above. One, QLED is based on solution-based printing technology, which is low cost and high yield. Two, quantum-dot emitters vender QLED with a large color gamut, high picture quality and superior device lifetime. Medium-sized screen is easiest for the coming QLED technologies but QLED for large screen is probably a reasonable extension afterwards.

Huang: But customers may not accept only better wider color range if they need to pay more money for this. I would suggest QLED consider the changes in color standards, such as the newly released BT2020 (defining high-definition 4 K TV), and new unique applications which cannot be satisfied by other technologies. The future of QLED seems also relying on the maturity of printing technology.

Peng: New standard (BT2020) certainly helps QLED, given BT2020 meaning a broad color gamut. Among the technologies discussed today, quantum-dot displays in either form are the only ones that can satisfy BT2020 without any optical compensation. In addition, studies found that the picture quality of display is highly associated with color gamut. It is correct that the maturity of printing technology plays an important role in the development of QLED. The current printing technology is ready for medium-sized screen and should be able to be extended to large-sized screen without much trouble.

Xu: For QLED to become a dominant technology, it is still difficult. In its development process, OLED precedes it and there are other rivaling technologies following. While we know owning the foundational patents and core technologies of QLED can make you a good position, holding core technologies alone cannot ensure you to become a mainstream technology. The government"s investment in such key technologies after all is small as compared with industry and cannot decide QLED to become mainstream technology.

Liao: Due to their lack of kernel technologies, Chinese OLED panel manufacturers heavily rely on investments to improve their market competitiveness. But this may cause the overheated investment in the OLED industry. In recent years, China has already imported quite a few new OLED production lines with the total cost of about 450 billion yuan (US$71.5 billion).Lots of advantages of OLED over LCD were highlighted, such as high color gamut, high contrast and high response speed and so on …. It seems to be possible that the flexible display will eventually lead a killer advantage.

The year 2021 is a year of milestone significance in the history of the Communist Party of China and the People’s Republic of China. Under the strong leadership of the Central Committee of the Communist Party of China (CPC) with Comrade Xi Jinping as the core, all regions and departments took Xi Jinping Thought on Socialism with Chinese Characteristics for a New Era as the guideline, fully implemented the spirits of the 19th CPC National Congress and the Plenary Sessions of the 19th Central Committee of the CPC and fostered the great founding spirit of the CPC. All regions and departments followed the decisions and arrangements made by the CPC Central Committee and the State Council, committed to the general working guideline of making progress while maintaining stability, fully and faithfully implemented the new development philosophy on all fronts, accelerated fostering a new development pattern, comprehensively deepened the reform and opening up, insisted on innovation-driven development, and promoted the high-quality development. We celebrated the centenary of the founding of the CPC, fulfilled the First Centenary Goal, and embarked on the new journey to achieve the Second Centenary Goal. While responding with composure to changes and the pandemic both unseen in a century, we have made new advances in fostering a new development pattern and pursuing high-quality development, and got off to a good start in implementing the 14th Five-Year Plan. China has maintained the leading position in the economic growth and the epidemic prevention and control in the world. National strategic capacity in science and technology accelerated its growth, industrial chain resilience was improved, reform and opening-up was advanced in depth, people’s livelihood was strongly and effectively safeguarded, and ecological conservation was carried forward. These are the results of the strong leadership of the Central Committee of the CPC with Comrade Xi Jinping as the core and the results of concerted efforts and hard work by the Party and the Chinese people of all ethnic groups.

New industries, new forms and models of business gathered speed to grow. Among the industries above the designated size, the value added of the high technology manufacturing industry [14] increased by 18.2 percent over the previous year, accounting for 15.1 percent of that of all industrial enterprises above the designated size. The value added for the manufacture of equipment [15] was up by 12.9 percent, accounting for 32.4 percent of that of all industrial enterprises above the designated size. Among the service enterprises above the designated size [16], the business revenue of the strategic emerging service industries [17] went up by 16.0 percent compared with the previous year. In 2021, the investment in high technology industries [18] increased by 17.1 percent over the previous year. In 2021, the output of new energy vehicles reached 3.677 million, up by 152.5 percent compared with the previous year; and that of integrated circuits was 359.43 billion, up by 37.5 percent. In 2021, the online retail sales [19] reached 13,088.4 billion yuan, up by 14.1 percent over the previous year on comparable basis. In 2021, the number of newly registered market entities was 28.87 million with 25 thousand market entities newly registered per day on average. By the end of 2021, the market entities totaled 0.15 billion.

In 2021, the value added of the wholesale and retail trades was 11,049.3 billion yuan, up by 11.3 percent over the previous year; that of transport, storage and post was 4,706.1 billion yuan, up by 12.1 percent; that of hotels and catering services was 1,785.3 billion yuan, up by 14.5 percent; that of financial intermediation was 9,120.6 billion yuan, up by 4.8 percent; that of real estate was 7,756.1 billion yuan, up by 5.2 percent; that of information transmission, software and information technology services was 4,395.6 billion yuan, up by 17.2 percent; and that of leasing and business services was 3,535.0 billion yuan, up by 6.2 percent. In 2021, the business revenue of service enterprises above the designated size grew by 18.7 percent over the previous year, and the operating profits increased by 13.4 percent.

The turnover of post services [30] totaled 1,369.8 billion yuan, up by 25.1 percent over the previous year. In 2021, the number of mail delivery was 1.09 billion; that of parcel delivery was 20 million; and that of express delivery was 108.30 billion with a revenue reaching 1,033.2 billion yuan. The turnover of telecommunication services [31] totaled 1,696.0 billion yuan, up by 27.8 percent over the previous year. By the end of 2021, there were 9.96 million mobile phone base stations [32], among which the number of 4G base stations reached 5.90 million and that of 5G base stations 1.43 million. In 2021, there were 1,823.53 million phone subscribers in China, of whom 1,642.83 million were mobile phone subscribers. The mobile phone coverage was 116.3 sets per 100 persons. The number of fixed broadband internet users [33] reached 535.79 million, an increase of 52.24 million over the end of the previous year. Of this total, fixed fiber-optic broadband internet users [34] amounted to 505.51 million, an increase of 51.36 million. Users of cellular internet of things terminals [35] totaled 1.399 billion, an increase of 0.264 billion.The number of internet user was 1.032 billion, 1.029 billion of which were mobile internet surfers [36]. The coverage of internet was 73.0 percent, and 57.6 percent in rural areas. The mobile internet traffic in 2021 was 221.6 billion gigabytes, up by 33.9 percent over the previous year. Software revenue of software and information technology services industry [37] in 2021 was 9,499.4 billion yuan, up by 17.7 percent over 2020 on a comparable basis.

The year 2021 witnessed the establishment of 47,643 enterprises with foreign direct investment (excluding banking, securities and insurance), up by 23.5 percent over that of the previous year, and the foreign direct investment actually utilized totaled 1,149.4 billion yuan, up by 14.9 percent, or 173.5 billion US dollars, up by 20.2 percent. Specifically, there were 5,336 newly established enterprises receiving direct investment from countries along the Belt and Road (including the investment in China via some free ports), up by 24.3 percent; and foreign capital directly invested in China reached 74.3 billion yuan, up by 29.4 percent, or 11.2 billion US dollars, up by 36.0 percent. In 2021, the foreign investment actually utilized by high technology industry reached 346.9 billion yuan, up by 17.1 percent, or 52.2 billion US dollars, up by 22.1 percent.

Funds raised through A-shares issued on Shanghai and Shenzhen Stock Exchanges [48] amounted to 1,674.3 billion yuan in 2021, an increase of 132.6 billion yuan from the previous year. 481 A-shares were newly issued on Shanghai and Shenzhen Stock Exchanges, raising 535.1 billion yuan worth of capital altogether, up by 60.9 billion yuan over that of the previous year. Of the total, 162 shares were from the science and technology innovation board, raising 202.9 billion yuan; refinancing of A-shares on Shanghai and Shenzhen Stock Exchanges (including public newly issued, targeted placement, right issued, preferred stock and exchanged convertible bonds) raised 1,139.1 billion yuan, an increase of 71.7 billion yuan over that of the previous year. 11 shares were publicly issued on Beijing Stock Exchanges, raising [49] 2.1 billion yuan. Various types of market entities financed 8,655.3 billion yuan through issuing bonds (including corporate bonds, convertible bonds, exchangeable bonds, financial bonds issued by policy banks, local government bonds and asset-backed securities) on Shanghai and Shenzhen Stock Exchanges, up by 177.6 billion yuan over that of the previous year. There were 6,932 companies listed on National Equities Exchange and Quotations [50] and funds raised by listed companies reached 26.0 billion yuan in 2021.

Expenditures on research and experimental development activities (R&D) were worth 2,786.4 billion yuan in 2021, up by 14.2 percent over that of 2020, accounting for 2.44 percent of GDP. Of this total, 169.6 billion yuan was used for basic research programs. A total of 48,700 projects were financed by the National Natural Science Foundation. By the end of 2021, there were altogether 533 state key laboratories in operation, 191 national engineering research centers under the new sequence management, 1,636 state-level enterprise technology centers and 212 demonstration centers for business startups and innovation. The National Fund for Technology Transfer and Commercialization established 36 sub-funds, with the total funds reaching 62.4 billion yuan. There were 1,287 state-level technology business incubators [60], and 2,551 national mass makerspaces [61]. A total of 4,601 thousand patents were authorized, up by 26.4 percent over that of the previous year. The number of PCT patent applications accepted [62] was 73 thousand. By the end of 2021, the number of valid patents was 15,421 thousand, of which 2,704 thousand were domestic valid invention patents. The number of high-value invention patents per 10,000 people [63] was 7.5. Trademark registration totaled 7,739 thousand, up by 34.3 percent over that of the previous year. A total of 670 thousand technology transfer contracts were signed, representing 3,729.4 billion yuan in value, up by 32.0 percent over that of the previous year.

The year 2021 saw a total of 52 successful space launches. Tianwen-1 probe successfully landed on Mars and Zhurong Mars rover reached the Mars surface. Chinese entered their own space station for the first time by the successful launch of the core module Tianhe and the accomplishment of missions including launches of Shenzhou-12 and Shenzhou-13. The solar observation satellite Xihe was successfully launched. With the successful development of Zuchongzhi 2.1 and Jiuzhang 2.0, China has achieved a quantum computational advantage in two mainstream technical routes of superconducting quantum and photonics quantum. The deep-sea unmanned submersible Haidou-1 broke a number of world records. Hualong-1 nuclear reactor using domestically-designed third-generation nuclear power technology was put into commercial operation.

14. High technology manufacturing industry includes manufacture of medicine, manufacture of aerospace vehicle and equipment, manufacture of electronic and communication equipment, manufacture of computers and office equipment, manufacture of medical equipment, manufacture of measuring instrument and equipment and manufacture of optical and photographic equipment.

16. Service enterprises above the designated size refer to legal entities of transport, storage and post, information transmission, software and information technology services, water conservancy, environment and public facilities management, and health with annual business revenue of 20 million yuan and above; legal entities of real estate (excluding real estate development and operation), leasing and business services, scientific research and technology services and education with annual business revenue of 10 million yuan and above; and legal entities of services to households, repair and other services and culture, sports and entertainment, and social services with annual business revenue of 5 million and above.

17. Strategic emerging service industries refer to the related service sectors of information technology of new generation, manufacture of high-end equipment, new materials, biotech, new energy vehicles, new energy, energy-saving and environmental protection and digital creative industries, and service industries related to new technology, innovation and entrepreneurship. The growth rate of the business revenue of the strategic emerging service industries in 2021 was calculated on a comparable basis.

18. Investment in high technology industries refers to investment in six high technology manufacturing industries, including the manufacture of medicine and manufacture of aerospace vehicle and equipment, and nine high technology service industries, including information service and e-commerce service.

37. Software and information technology services industry includes software development, integrated circuit design, information system integration and internet of things technology services, operation maintenance services, information processing and storage support services, IT consulting services, digital content services and other IT services industry.

60. The state-level technology business incubators are technology-based business startup service providers consistent with the Administrative Measures for Technology Business Incubators that provide physical space, shared facilities and professional services with the mission of advancing transformation of technological achievements, cultivating technological enterprises and fostering the entrepreneurial spirit. They should be approved and accredited by the Ministry of Science and Technology.

61. The national mass makerspaces are new service platform for entrepreneurship and innovation that are in conformity with the Guidelines on Developing Mass Makerspaces and are reviewed and registered by the Ministry of Science and Technology in accordance with the Provisional Registration Regulations on National Mass Makerspaces.

63. The number of high-value invention patents per 10,000 people refers to the number of valid invention patents owned per 10,000 national residents which are authorized by the China National Intellectual Property Administration and satisfy any of the following conditions: invention patents for strategic emerging industries; invention patents having corresponding foreign patents; invention patents maintained more than 10 years; invention patents with a relatively high pledge financing amount; and invention patents that won the National Science and Technology Award and the China Patent Award.

In this Communiqué, data of newly increased employed people in urban areas, registered unemployment rate in urban areas, social security, unemployment insurance, work injury insurance and skilled workers schools are from the Ministry of Human Resources and Social Security; data of foreign exchange reserves and exchange rates are from the State Administration of Foreign Exchange; data of market entities, quality inspection, the formulation and revision of national standards and qualification rate of manufactured products are from the State Administration for Market Regulation; data of environment monitoring are from the Ministry of Ecology and Environment; data of output of aquatic products and area of farmland newly equipped with effective water-saving irrigation systems are from the Ministry of Agriculture and Rural Affairs; data of production of timber, area of afforestation, area of grass planting and improvement, national natural reserves and national parks are from the National Forestry and Grassland Administration; data of area of farmland newly equipped with irrigation system, water resources, water consumption and land newly saved from soil erosion are from the Ministry of Water Resources; data of installed power generation capacity, new power transformer equipment with a capacity of 220 kilovolts and above and electricity consumption are from the China Electricity Council; data of volume of freight handled by ports, container shipping of ports, highway transportation, waterway transportation, new and rebuilt highways and new throughput capacity of berths for over 10,000-tonnage ships are from the Ministry of Transport; data of railway transportation, new railways put into operation, new double-track railways put into operation and electrified railways put into operation are from China Railway; data of civil aviation and new civil transportation airports are from the Civil Aviation Administration of China; data of pipeline transportation are from China National Petroleum Cooperation, China Petrochemical Cooperation, China National Offshore Oil Cooperation and China Oil & Gas Piping Network Cooperation; data of motor vehicles for civilian use and traffic accidents are from the Ministry of Public Security; data of postal service are from the State Post Bureau; data of telecommunication, software revenue, and new lines of optical-fiber cables are from the Ministry of Industry and Information Technology; data of internet users and internet coverage are from China Internet Network Information Center; data of housing units rebuilt or renovated in rundown urban areas and government-subsidized rental housing are from the Ministry of Housing and Urban-Rural Development; data of imports and exports of goods are from the General Administration of Customs; data of imports and exports of services, foreign direct investment, outbound direct investment, overseas contracted projects and overseas labor contracts are from the Ministry of Commerce; data of finance are from the Ministry of Finance; data of newly added tax and fee cuts are from the State Taxation Administration; data of monetary finance and corporate credit bonds are from the People’s Bank of China; data of funds raised through domestic exchange markets are from China Securities Regulatory Commission; data of the insurance sector are from China Banking and Insurance Regulatory Commission; data of medical insurance and maternity insurance are from the National Healthcare and Security Administration; data of urban and rural minimum living allowances, relief and assistance granted to rural residents living in extreme poverty, temporary assistance and social welfare are from the Ministry of Civil Affairs; data of entitled people are from the Ministry of Veterans Affairs; data of natural science foundation projects are from the National Natural Science Foundation; data of state key laboratories, National Fund for Technology Transfer and Commercialization, state-level technology business incubators, national mass makerspaces and technology transfer contracts are from the Ministry of Science and Technology; data of national engineering research centers, enterprise technical centers and demonstration centers for business startups and innovation are from the National Development and Reform Commission; data of patents and trademarks are from the National Intellectual Property Administration; data of satellite launches are from the State Administration of Science, Technology and Industry for National Defense; data of education are from the Ministry of Education; data of art-performing groups, museums, public libraries, cultural centers and tourism are from the Ministry of Culture and Tourism; data of television and radio programs are from the National Radio and Television Administration; data of movies are from the China Film Administration; data of newspapers, magazines and books are from the National Press and Publication Administration; data of files are from the State Archives Administration; data of medical care and health are from the National Health Commission; data of sports are from the General Administration of Sport; data of physically-challenged athletes are from the China Disabled Persons’ Federation; data of supply of state-owned land for construction use and direct economic loss caused by oceanic disasters are from the Ministry of Natural Resources; data of average temperature and typhoons are from the China Meteorological Administration; data of areas of crops hit by natural disasters, direct economic loss caused by flood, waterlogging and geological disasters, direct economic loss caused by droughts, direct economic loss caused by low temperature, frost and snow, the number of earthquakes, direct economic loss caused by earthquakes, forest fires, areas of forests damaged and workplace accidents are from the Ministry of Emergency Management; all the other data are from the National Bureau of Statistics.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey