lcd panel price trend factory

The price of LCD display panels for TVs is still falling in November and is on the verge of falling back to the level at which it initially rose two years ago (in June 2020). Liu Yushi, a senior analyst at CINNO Research, told China State Grid reporters that the wave of “falling tide” may last until June this year. For related panel companies, after the performance surge in the past year, they will face pressure in 2022.

LCD display panel prices for TVs will remain at a high level throughout 2021 due to the high base of 13 consecutive months of increase, although the price of LCD display panels peaked in June last year and began to decline rapidly. Thanks to this, under the tight demand related to panel enterprises last year achieved substantial profit growth.

According to China State Grid, the annual revenue growth of major LCD display panel manufacturers in China (Shentianma A, TCL Technology, Peking Oriental A, Caihong Shares, Longteng Optoelectronics, AU, Inolux Optoelectronics, Hanyu Color Crystal) in 2021 is basically above double digits, and the net profit growth is also very obvious. Some small and medium-sized enterprises directly turn losses into profits. Leading enterprises such as BOE and TCL Technology more than doubled their net profit.

Take BOE as an example. According to the 2021 financial report released by BOE A, BOE achieved annual revenue of 219.31 billion yuan, with a year-on-year growth of 61.79%; Net profit attributable to shareholders of listed companies reached 25.831 billion yuan, up 412.96% year on year. “The growth is mainly due to the overall high economic performance of the panel industry throughout the year, and the acquisition of the CLP Panda Nanjing and Chengdu lines,” said Xu Tao, chief electronics analyst at Citic Securities.

In his opinion, as BOE dynamically optimizes its product structure, and its flexible OLED continues to enter the supply chain of major customers, BOE‘s market share as the panel leader is expected to increase further and extend to the Internet of Things, which is optimistic about the company’s development in the medium and long term.

TCL explained that the major reasons for the significant year-on-year growth in revenue and profit were the significant year-on-year growth of the company’s semiconductor display business shipment area, the average price of major products and product profitability, and the optimization of the business mix and customer structure further enhanced the contribution of product revenue.

“There are two main reasons for the ideal performance of domestic display panel enterprises.” A color TV industry analyst believes that, on the one hand, under the effect of the epidemic, the demand for color TV and other electronic products surges, and the upstream raw materials are in shortage, which leads to the short supply of the panel industry, the price rises, and the corporate profits increase accordingly. In addition, as Samsung and LG, the two-panel giants, gradually withdrew from the LCD panel field, they put most of their energy and funds into the OLED(organic light-emitting diode) display panel industry, resulting in a serious shortage of LCD display panels, which objectively benefited China’s local LCD display panel manufacturers such as BOE and TCL China Star Optoelectronics.

Liu Yushi analyzed to reporters that relevant TV panel enterprises made outstanding achievements in 2021, and panel price rise is a very important contributing factor. In addition, three enterprises, such as BOE(BOE), CSOT(TCL China Star Optoelectronics) and HKC(Huike), accounted for 55% of the total shipments of LCD TV panels in 2021. It will be further raised to 60% in the first quarter of 2022. In other words, “simultaneous release of production capacity, expand market share, rising volume and price” is also one of the main reasons for the growth of these enterprises. However, entering the low demand in 2022, LCD TV panel prices continue to fall, and there is some uncertainty about whether the relevant panel companies can continue to grow.

According to Media data, in February this year, the monthly revenue of global large LCD panels has been a double decline of 6.80% month-on-month and 6.18% year-on-year, reaching $6.089 billion. Among them, TCL China Star and AU large-size LCD panel revenue maintained year-on-year growth, while BOE, Innolux, and LG large-size LCD panel monthly revenue decreased by 16.83%, 14.10%, and 5.51% respectively.

Throughout Q1, according to WitsView data, the average LCD TV panel price has been close to or below the average cost, and cash cost level, among which 32-inch LCD TV panel prices are 4.03% and 5.06% below cash cost, respectively; The prices of 43 and 65 inch LCD TV panels are only 0.46% and 3.42% higher than the cash cost, respectively.

The market decline trend is continuing, the reporter queried Omdia, WitsView, Sigmaintel(group intelligence consulting), Oviriwo, CINNO Research, and other institutions regarding the latest forecast data, the analysis results show that the price of the TV LCD panels is expected to continue to decline in April. According to CINNO Research, for example, prices for 32 -, 43 – and 55-inch LCD TV panels in April are expected to fall $1- $3 per screen from March to $37, $65, and $100, respectively. Prices of 65 – and 75-inch LCD TV panels will drop by $8 per screen to $152 and $242, respectively.

“In the face of weak overall demand, major end brands requested panel factories to reduce purchase volumes in March due to high inventory pressure, which led to the continued decline in panel prices in April.” Beijing Di Xian Information Consulting Co., LTD. Vice general manager Yi Xianjing so analysis said.

“Since 2021, international logistics capacity continues to be tight, international customers have a long delivery cycle, some orders in the second half of the year were transferred to the first half of the year, pushing up the panel price in the first half of the year but also overdraft the demand in the second half of the year, resulting in the panel price began to decline from June last year,” Liu Yush told reporters, and the situation between Russia and Ukraine has suddenly escalated this year. It also further affected the recovery of demand in Europe, thus prolonging the downward trend in prices. Based on the current situation, Liu predicted that the bottom of TV panel prices will come in June 2022, but the inflection point will be delayed if further factors affect global demand and lead to additional cuts by brands.

With the price of TV panels falling to the cash cost line, in Liu’s opinion, some overseas production capacity with old equipment and poor profitability will gradually cut production. The corresponding profits of mainland panel manufacturers will inevitably be affected. However, due to the advantages in scale and cost, there is no urgent need for mainland panel manufacturers to reduce the dynamic rate. It is estimated that Q2’s dynamic level is only 3%-4% lower than Q1’s. “We don’t have much room to switch production because the prices of IT panels are dropping rapidly.”

Ovirivo analysts also pointed out that the current TV panel factory shipment pressure and inventory pressure may increase. “In the first quarter, the production line activity rate is at a high level, and the panel factory has entered the stage of loss. If the capacity is not adjusted, the panel factory will face the pressure of further decline in panel prices and increased losses.”

In the first quarter of this year, the retail volume of China’s color TV market was 9.03 million units, down 8.8% year on year. Retail sales totaled 28 billion yuan, down 10.1 percent year on year. Under the situation of volume drop, the industry expects this year color TV manufacturers will also set off a new round of LCD display panel prices war.

The current oversupply of liquid crystal display (LCD) panels is expected to continue through 2023, analyst firm TrendForce said in its latest forecast.

LCD panel prices had increased from June 2020 through the first half of 2021, the firm said, spurned by high demand for consumer electronics from Covid-19.

In supply, while LG Display could halt production at its P7 factory in Paju during the first quarter of next year, CSOT’s start of operation of its Gen 8.6 T9 factory could increase panel supply further than the current state, TrendForce said.

The analyst firm also said that LCD factories that use Gen 5 substrate or above could see their operation rate drop to 60% during the fourth quarter, which will be the lowest in ten years.

According to IMARC Group’s latest report, titled “TFT LCD Panel Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2022-2027”, the global TFT LCD panel market size reached US$ 157 Billion in 2021. Looking forward, IMARC Group expects the market to reach US$ 207.6 Billion by 2027, exhibiting a growth rate (CAGR) of 4.7% during 2022-2027.

A thin-film-transistor liquid-crystal display (TFT LCD) panel is a liquid crystal display that is generally attached to a thin film transistor. It is an energy-efficient product variant that offers a superior quality viewing experience without straining the eye. Additionally, it is lightweight, less prone to reflection and provides a wider viewing angle and sharp images. Consequently, it is generally utilized in the manufacturing of numerous electronic and handheld devices. Some of the commonly available TFT LCD panels in the market include twisted nematic, in-plane switching, advanced fringe field switching, patterned vertical alignment and an advanced super view.

The global market is primarily driven by continual technological advancements in the display technology. This is supported by the introduction of plasma enhanced chemical vapor deposition (PECVD) technology to manufacture TFT panels that offers uniform thickness and cracking resistance to the product. Along with this, the widespread adoption of the TFT LCD panels in the production of automobiles dashboards that provide high resolution and reliability to the driver is gaining prominence across the globe. Furthermore, the increasing demand for compact-sized display panels and 4K television variants are contributing to the market growth. Moreover, the rising penetration of electronic devices, such as smartphones, tablets and laptops among the masses, is creating a positive outlook for the market. Other factors, including inflating disposable incomes of the masses, changing lifestyle patterns, and increasing investments in research and development (R&D) activities, are further projected to drive the market growth.

The competitive landscape of the TFT LCD panel market has been studied in the report with the detailed profiles of the key players operating in the market.

THANK YOU FOR VISITING ENERGYTREND (HEREINAFTER REFERRED TO AS "THE WEBSITE"). THE WEBSITE, OWNED AND OPERATED BY TRENDFORCE CORP. (HEREINAFTER REFERRED TO AS "TRENDFORCE"), WILL COLLECT, HANDLE, AND USE PRIVATE USER DATA IN ACCORDANCE WITH THE PERSONAL INFORMATION PROTECTION LAW (HEREINAFTER "PERSONAL INFORMATION LAW") AND THE WEBSITE"S PRIVACY POLICY. THE WEBSITE AIMS TO RESPECT AND PROTECT ALL USERS" ONLINE PRIVACY RIGHTS. IN ORDER TO UNDERSTAND AS WELL AS PROTECT YOUR RIGHTS, PLEASE READ THE FOLLOWING TERMS CAREFULLY:

1.1. THE POLICY COVERS THE HANDLING OF THE PRIVATE INFORMATION EACH USER SHARES WITH TRENDFORCE WHILE VISITING OUR WEBSITES. IF A DIFFERENT PRIVATE POLICY HAS BEEN REFERED TO FOR SPECIFIC TRENDFORCE WEBSITES AND SERVICES, THAT POLICY WILL REPLACE OR SUPPLEMENT THE PRIVACY POLICY MENTIONED IN THIS DOCUMENT. THIS POLICY ALSO COVERS INDIVIDUALS LEGALLY RESIDING IN OR ORGANIZATIONS LEGALLY BASED IN MEMBER COUNTRIES OF THE EUROPEAN UNION (EU) AND ARE SUBJECTED TO EU GENERAL DATA PROTECTION REGULATION (GDPR) WITH REGARD TO PROVISION OF SERVICES AND PERSONAL DATA PROTECTION.

1.2. THIS POLICY IS NOT APPLICABLE TO EITHER COMPANIES OTHER THAN TRENDFORCE AND ITS SUBSIDIARIES OR PERSONNEL NOT EMPLOYED OR AUTHORIZED BY TRENDFORCE AND ITS SUBSIDIARIES.

2.4. THE WEBSITE COLLECTS TRANSACTION DATA BETWEEN YOU AND TRENDFORCE AND FROM RELEVANT BUSINESS PARTNERS. THESE INCLUDE SPECIFIC PRODUCTS AND SERVICES THAT ARE DIRECTLY OBTAINED FROM THE WEBSITE.

b. THIS WEBSITE WILL NOTIFY YOU ON MATTERS RELATED TO YOUR PERSONAL DATA BY EMAIL, OR TRENDFORCE CORP. WILL NOTIFY YOU BY OTHER MEANS (SUCH AS VIA TELEPHONE). CLIENTS ARE FULLY RESPONSIBLE FOR PROVIDING AN UPDATED, VALID, AND DELIVERABLE EMAIL ADDRESS THAT CAN RECEIVE NOTIFICATION EMAILS FROM TRENDFORCE CORP.

EXCEPT AS OTHERWISE EXPRESSEDLY PROVIDED BY GDPR OR ORDERED BY THE LAWS OF A COMPETENT JURISDICTION, CLIENTS CAN USE CUSTOMER EMAILServiceGDPR@energytrend.comTO CONTACT THIS WEBSITE TO EXERCISE THEIR RIGHTS PERTAINING TO THEIR ACCOUNT USER NAMES, ACCOUNT USER DATA, SESSION COOKIES, AND OTHER FORMS OF ACCOUNT DATA RECORDS. THESE RIGHTS INCLUDE RIGHT TO ACCESS, RIGHT TO RECTIFICATION, RIGHT TO BE FORGOTTEN/DATA ERASURE, RIGHT TO RESTRICTION OF PROCESSING, RIGHT OF DATA PORTABILITY, RIGHT TO OBJECT, AND ETC. TO EXERCISE THESE RIGHTS, A CLIENT MUST INCLUDE LEGALLY VALID AND VERIFICABLE PROOFS OF PERSONAL IDENITIFICATION ALONG WITH HIS/HER REQUEST. FURTHEMORE, THE CLIENT ISSUING THE REQUEST TO EXERCISE THESE RIGHTS MUST HAVE FUFILLED VARIOUS LEGAL OBLIGATIONS ON HIS/HER PART BEFOREHAND. AFTERWARDS, TRENDFORCE WILL FULFILL THE CLIENTS’ REQUEST/PROVIDE RESOLUTIONS WITHIN REASONABLE TIME AND EFFORT.

Recently, it was announced that the 32-inch and 43-inch panels fell by approximately USD 5 ~ USD 6 in early June, 55-inch panels fell by approximately USD 7, and 65-inch and 75-inch panels are also facing overcapacity pressure, down from USD 12 to USD 14. In order to alleviate pressure caused by price decline and inventory, panel makers are successively planning to initiate more significant production control in 3Q22. According to TrendForce’s latest research, overall LCD TV panel production capacity in 3Q22 will be reduced by 12% compared with the original planning.

As Chinese panel makers account for nearly 66% of TV panel shipments, BOE, CSOT, and HKC are industry leaders. When there is an imbalance in supply and demand, a focus on strategic direction is prioritised. According to TrendForce, TV panel production capacity of the three aforementioned companies in 3Q22 is expected to decrease by 15.8% compared with their original planning, and 2% compared with 2Q22. Taiwanese manufacturers account for nearly 20% of TV panel shipments so, under pressure from falling prices, allocation of production capacity is subject to dynamic adjustment. On the other hand, Korean factories have gradually shifted their focus to high-end products such as OLED, QDOLED, and QLED, and are backed by their own brands. However, in the face of continuing price drops, they too must maintain operations amenable to flexible production capacity adjustments.

TrendForce indicates, that in order to reflect real demand, Chinese panel makers have successively reduced production capacity. However, facing a situation in which terminal demand has not improved, it may be difficult to reverse the decline of panel pricing in June. However, as TV sizes below 55 inches (inclusive) have fallen below their cash cost in May (which is seen as the last line of defense for panel makers) and are even flirting with the cost of materials, coupled with production capacity reduction from panel makers, the price of TV panels has a chance to bottom out at the end of June and be flat in July. However, demand for large sizes above 65 inches (inclusive) originates primarily from Korean brands. Due to weak terminal demand, TV brands revising their shipment targets for this year downward, and purchase volume in 3Q22 being significantly cut down, it is difficult to see a bottom for large-size panel pricing. TrendForce expects that, optimistically, this price decline may begin to dissipate month by month starting in June but supply has yet to reach equilibrium, so the price of large sizes above 65 inches (inclusive) will continue to decline in 3Q22.

TrendForce states, as panel makers plan to reduce production significantly, the price of TV panels below 55 inches (inclusive) is expected to remain flat in 3Q22. However, panel manufacturers cutting production in the traditional peak season also means that a disappointing 2H22 peak season is a foregone conclusion and it will not be easy for panel prices to reverse. However, it cannot be ruled out, as operating pressure grows, the number and scale of manufacturers participating in production reduction will expand further and its timeframe extended, enacting more effective suppression on the supply side, so as to accumulate greater momentum for a rebound in TV panel quotations.

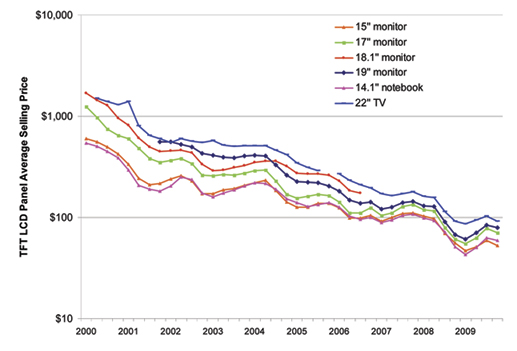

Factors that may influence the price of a certain type of LCD include: screen size, viewing angle, maximum brightness, color display,resolution and frame rate.

Screen size: larger size display more, and larger size cost more, these’re common sense. For example, in last year’s iPhone 8P which used a 5.5-inch LCD screen, the display (including touchscreen) cost 52.5 dollars, while a 43-inch LCD TV cost 128 dollars.

Viewing angle: it’s the maximum angle at which a display can be viewed with acceptable visual performance. It’s measured from one direction to the opposite, giving a maximum of 180° for a flat, one-sided screen. Early LCDs had strikingly narrow viewing angles, for now most of the manufacturers have improved them to more than 160°.

Color display: in early or simple LCDs, only two or very few colors can be displayed. As the technology advances, TFT LCD can display up to 65536 colors.

As the diagram shows above, LCD module covers the most part of the cost of a LCD TV. Within LCD module, there’re still many components. In the following diagram we’ll show you the price breakdown of these components.

The third quarter in the year is usually the demand season of LCD module, as a result the price will be the highest. However, situation varies in different market.

Due to the massive investment and low cost of Chinese mainland manufacturer, the capacity of LCD module for TVs increases significantly, so the price of these modules stay pretty low for the past year.

In another aspect, technology innovations keep push the price of high-end LCD to a higher level. For many users that are planning to replace their old TVs, these high-end LCDs are tempting choices.

Actually, though LCD screen has many advantages, its average price is keep decreasing in the past years. New technology brings lower cost is one reason, a strong competitor called OLED is another.

Main difference between OLED and LCD is OLED can give out light itself, that is to say OLED screen can run at a lower load compared to LCD screen, at least it doesn’t need a backlight system.

The global TFT-LCD display panel market attained a value of USD 148.3 billion in 2022. It is expected to grow further in the forecast period of 2023-2028 with a CAGR of 4.9% and is projected to reach a value of USD 197.6 billion by 2028.

The current global TFT-LCD display panel market is driven by the increasing demand for flat panel TVs, good quality smartphones, tablets, and vehicle monitoring systems along with the growing gaming industry. The global display market is dominated by the flat panel display with TFT-LCD display panel being the most popular flat panel type and is being driven by strong demand from emerging economies, especially those in Asia Pacific like India, China, Korea, and Taiwan, among others. The rising demand for consumer electronics like LCD TVs, PCs, laptops, SLR cameras, navigation equipment and others have been aiding the growth of the industry.

TFT-LCD display panel is a type of liquid crystal display where each pixel is attached to a thin film transistor. Since the early 2000s, all LCD computer screens are TFT as they have a better response time and improved colour quality. With favourable properties like being light weight, slim, high in resolution and low in power consumption, they are in high demand in almost all sectors where displays are needed. Even with their larger dimensions, TFT-LCD display panel are more feasible as they can be viewed from a wider angle, are not susceptible to reflection and are lighter weight than traditional CRT TVs.

The global TFT-LCD display panel market is being driven by the growing household demand for average and large-sized flat panel TVs as well as a growing demand for slim, high-resolution smart phones with large screens. The rising demand for portable and small-sized tablets in the educational and commercial sectors has also been aiding the TFT-LCD display panel market growth. Increasing demand for automotive displays, a growing gaming industry and the emerging popularity of 3D cinema, are all major drivers for the market. Despite the concerns about an over-supply in the market, the shipments of large TFT-LCD display panel again rose in 2020.

North America is the largest market for TFT-LCD display panel, with over one-third of the global share. It is followed closely by the Asia-Pacific region, where countries like India, China, Korea, and Taiwan are significant emerging market for TFT-LCD display panels. China and India are among the fastest growing markets in the region. The growth of the demand in these regions have been assisted by the growth in their economy, a rise in disposable incomes and an increasing demand for consumer electronics.

The report gives a detailed analysis of the following key players in the global TFT-LCD display panel Market, covering their competitive landscape, capacity, and latest developments like mergers, acquisitions, and investments, expansions of capacity, and plant turnarounds:

It may seem odd in the face of stalled economies and stalled AV projects, but the costs of LCD display products are on the rise, according to a report from Digital Supply Chain Consulting, or DSCC.

Demand for LCD products remains strong , says DSCC, at the same time as shortages are deepening for glass substrates and driver integrated circuits. Announcements by the Korean panel makers that they will maintain production of LCDs and delay their planned shutdown of LCD lines has not prevented prices from continuing to rise.

I assume, but absolutely don’t know for sure, that panel pricing that affects the much larger consumer market must have a similar impact on commercial displays, or what researchers seem to term public information displays.

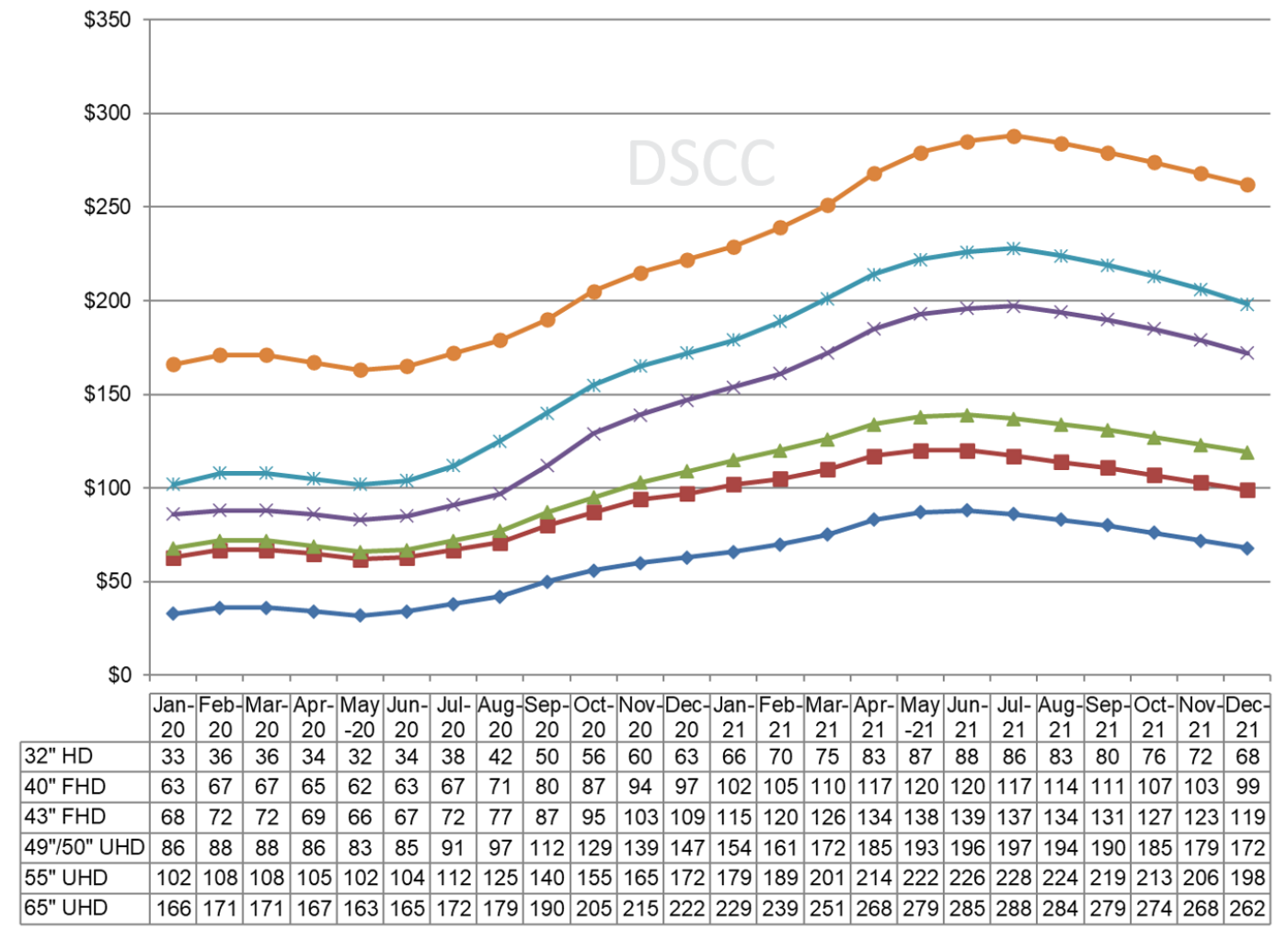

Panel prices increased more than 20% for selected TV sizes in Q3 2020 compared to Q2, and by 27% in Q4 2020 compared to Q3, we now expect that average LCD TV panel prices in Q1 2021 will increase by another 12%.

The first chart shows our latest TV panel price update, with prices increasing across the board from a low in May 2020 to an expected peak in May/June of this year. Last month’s update predicted a peak in February/March. However, our forecast for the peak has been increased and pushed out after AGC reported a major accident at a glass plant in Korea and amid continuing problems with driver IC shortages.

The inflection point for this cycle, the month of the most significant M/M price increases, was passed in September 2020, and the price increases have been slowing down each month since then, but the January increase averaged 4.1%. Prices in February 2021 have reached levels last seen exactly three years ago in February 2018.

Prices increased in Q4 for all sizes of TV panels, with massive percentage increases in sizes from 32” to 55” ranging from 28% to 38%. Prices for 65” and 75” increased at a slower rate, by 19% and 8% respectively, as capacity has continued to increase on those sizes with Gen 10.5 expansions.

Prices for every size of TV panel will increase in Q1 at a slower rate, ranging from 5% for 75” to 16% for 43”, and we now expect that prices will continue to increase in Q2, with the increases ranging from 3% to 6% on a Q/Q basis. We now expect that prices will peak in Q2 and will start to decline in Q3, but the situation remains fluid.

All that said, LCD panels are way less costly, way lighter and slimmer, and generally look way better than the ones being used 10 years ago, so prices is a relative problem.

Large LCD panel prices have been continuously increasing for last 10 months due to an increase in demand and tight supply. This has helped the LCD industry to recover from drastic panel price reductions, revenue and profit loss in 2019. It has also contributed to the growth of QD and miniLED LCD TV. Strong LCD TV panel demand is expected to continue in 2021, but component shortages, supply constraints, and very high panel price increase can still create uncertainties.

It was earlier anticipated that price increases would decelerate in 2Q, but now the price increase is accelerating compared to 1Q, according to a research by DSCC. Panel prices increased by 27 percent in 4Q20 compared to 3Q and slowed down to 14.5 percent in 1Q21 compared to 4Q, but the current estimate is that average LCD TV panel prices in 2Q21 will increase by another 17 percent. The prices are expected to peak sometime in 3Q21.

There has been a surge in prices across the board from a low in May 2020 to a high point in June 2021 which does not represent the peak. There have been multiple inflection points for this cycle: the first inflection point, the month of the biggest MoM price increases, was passed in September 2020, and the price increase slowed down, then started to accelerate again in January 2021, and there is another slowdown starting in May 2021. Prices in May 2021 have reached levels last seen in July 2017.

Prices increased in 1Q21 for all sizes of TV panels, with double-digit percentage increases in sizes from 32- to 65-inch ranging from 12-18 percent. Prices for 75-inch increased by 8 percent as capacity has continued to increase on Gen 10.5 lines, where 75-inch is an efficient six-cut. Prices for every size of TV panel will continue to increase in 2Q at an even faster rate, ranging from 12 percent for 75-inch to 24 percent for 32-inch. The prices are expected to continue to increase in 3Q.

The current upturn in the crystal cycle has seen the biggest trough-to-peak price increases for LCD TV panels, and the recent acceleration of prices has further extended this record. Comparing the forecast for June 2021 panel prices with the prices in May 2020, there is a trough-to-peak increases from 34 percent for 75-inch to 181 percent for 32-inch, with an average of 111 percent. In comparison, the average trough-to-peak increase of the 2016 to 2017 cycle was 48 percent, and prior cycles saw smaller increases.

Before the current upswing, the largest panels sold with an area premium, but the current cycle has flipped that upside down. Whereas in May 2020, 75-inch panels sold at an area premium of USD 77 per square meter higher than the 32-inch panel price, as of May 2021, they are selling at a USD 65 discount on an area basis. This means that those Gen 10.5 fabs could earn higher revenues from making 32-inch panels than from 75-inch panels. The pattern for 65-inch is even more severe, and 65-inch is now selling at a USD 69 per square meter discount (alternately, a 22% area discount) compared to 32-inch.

The improved pricing for LCD TV panels has already improved the profitability of panel makers. It will continue to drive their profits even higher, especially the two prominent Taiwanese players, who have Gen 7.5 and Gen 8.5 fabs but no Gen 10.5 fabs. Chinese panel makers HKC and CHOT have a similar industrial profile and stand to benefit greatly as well. The leading companies with Gen 10.5 fabs (BOE, CSOT and Foxconn/Sharp) stand to benefit less because the price increases on the largest sizes are more modest, but every LCD panel maker is doing well.

TV price index has increased from its all-time low of 42 in May 2020 to 87 in May 2021, and it is expected to reach 89 in June and over 90 in 3Q21 before declining in 4Q. The YoY increase has surpassed 100 percent in May 2021. It will remain at elevated levels throughout the second half of 2021.

In addition to being an exceptionally large upcycle, the current upswing matches some of the longest stretches of increasing prices ever seen, more than a full year from trough to peak. The length of the upswing can be attributed to several factors: glass and driver IC shortages, the pandemic-driven demand or the potential for Korean fab downsizing.

TV makers continued to make strong profits in 1Q21 despite increasing panel prices. The TV market typically slows down in 1Q and 2Q. TV maker revenues declined seasonally in 1Q but less than usual, and the operating margins for both Samsung and LGE increased sequentially. Samsung’s CE division operating profits exceeded USD 1 billion for the quarter for only the second time ever. With demand remaining strong, TV makers have weathered the increase in panel prices and remained very profitable.

There is a surge in LCD equipment spending to respond to dramatically improved market conditions in the LCD market. DSCC sees LCD revenues rising 32 percent in 2021 to USD 112 billion on strong unit and area growth with prices and profitability rebounding to or even exceeding the 2017 levels. With LCD suppliers able to sell everything they can make at attractive margins; it should be no surprise that most LCD manufacturers are looking to expand capacity.

However, unlike previous upturns when many new fabs were built, in this upturn panel suppliers are looking to stretch their capacity through smaller investments, simplifying their processes and debottlenecking. Having said that, there will be two new Gen 8.6 mega fabs being built. The result versus last quarter is a 10 percent or a USD 2.2 billion increase in 2020-2024 LCD spending from USD 21.8 billion to USD 24 billion. The 2021 LCD equipment spending forecast is up 15 percent versus last quarter’s forecast to USD 10 billion, with 2021 LCD equipment spending up 125 percent versus 2021. In addition, 2022 was upgraded by 28 percent to USD 3.5 billion.

Although there is a healthy upgrade in LCD equipment spending in 2021 and 2022, the outlook for 2022-2024 spending is still significantly lower than in previous years, resulting in tighter capacity and slower price reductions in the next downturn. In addition, with Korean LCD suppliers expected to reduce their LCD capacity and convert to potentially higher margin OLEDs, the outlook for LCD pricing and profitability looks quite healthy, which may result in even more equipment spending, especially as miniLEDs gain acceptance.

An unfortunate and untimely string of accidents has created a historic tight glass market and caused a very unusual industry average price increase of several percent. In last few months top glass suppliers Corning, NEG, and AGC have all experienced production problems. A tank failure at Corning, a power outage at NEG, and an accident at an AGC glass plant all resulted in glass supply constraints when demand and production has been increasing.

In March 2021 Corning announced its plan to increase glass prices in 2Q21. Corning has also increased supply by starting glass tank in Korea to supply China’s Gen 10.5 fabs that are ramping up. Most of the growth in capacity is coming from Gen 8.6 and Gen 10.5 fabs in China.

Besides glass there have been other component shortages including driver ICs and polarizers. The lack of investment in polarizers and base films in 2019 caught the industry off guard when demand turned around in 2020. Multiple other materials are also in tight supply and are affecting different makers in different ways, supporting inflationary price trends.

Widespread component supply shortages could impact availability on LCD TV panels from CSOT and Innolux. The display panel manufacturers have warned that supplies of panels are expected to be tight throughout the year.

According to Li Dongsheng, chairman, TCL, panel shortages will continue in 1H21, following conditions already hampered last year during the start of the COVID-19 pandemic. The situation for 2H21 remains to be seen but for 2021 overall panel supply will be tight.

James Yang, president, Innolux, has warned of a shortage in LCD panels caused by strong demand for LCD coming out of the global crisis and the conditions are expected to continue through 2021. Innolux has seen shortages in LCD components including power semiconductors, driver ICs and glass substrates that have kept production below capacity. Shortages of ICs and semiconductors could continue right up to the 1H22.

Ironically, prior to the run-on LCD panel supplies, manufacturers were faced with the dilemma of overproduction causing a glut in inventory, which was driving prices artificially lower. This was the result of giant new LCD fabs coming online in China and other areas of Asia.

Panel makers, being cognizant of that threat, are expected to produce panels at a more tempered pace to keep margins healthy. LCD panel prices continued to rise in March after moving up in February.

Almost all Chinese panel makers are doing everything they can to incrementally increase their current factories’ capacities through productivity enhancements and new equipment purchases for debottlenecking or capacity expansions. For the same reasons, South Korean panel makers continue to delay shutting down their domestic LCD TV factories.

TV manufacturers have been moving aggressively to replenish inventories of LCD panels to meet strong sales of TVs and other devices to meeting escalating demand, particularly in the United States and Europe.

An increase in demand for larger size TVs in 2H20 combined with component shortages has pushed the market to supply constraint and caused continuous panel price increases from June 2020 to March 2021. The panel price increase resulting in higher costs for TV brands. It has also made it difficult for lower priced brands to acquire enough panels to offer lower priced TVs. Further, panel suppliers are giving priority to top brands with larger orders during supply constraint.

For 3 years, from 2017 to 2020, LCD panel makers suffered through a continuous pattern of price declines interrupted only with brief respites. With the COVID-19 demand surge assisted by shortages in glass and DDICs, panel prices are spiking. Korean, Taiwanese, and Chinese panel makers are reporting robust margins in 1Q 2021 and the good news is anticipated for panel makers to get even better in 2Q.

Although multiple caveats remain about how both supply and demand will trend over the coming months, the modeled glut level is a leading indicator that the next cycle is now on its way, which implies falling prices, utilization, and profitability. Industry players should consider the implications when planning business strategies for the next 2 years.

The global TFT LCD panel market size reached US$ 165.0 Billion in 2022. Looking forward, IMARC Group expects the market to reach US$ 217.2 Billion by 2028, exhibiting a growth rate (CAGR) of 4.66% during 2023-2028.

TFT (Thin Film Transistor) is an active-matrix LCD along with an improved image quality where one transistor for every pixel controls the illumination of the display enabling an easy view even in bright environments. This technology currently represents the most popular LCD display technology and accounts for the majority of the global display market. Being light in weight, slim in construction, high in resolution with low power consumption, TFT’s are gaining prominence in almost all the industries wherever displays are required. They find applications in various electronic goods such as cell phones, portable video game devices, televisions, laptops, desktops, etc. They are also used in automotive industry, navigation and medical equipment, laser pointer astronomy, SLR cameras and digital photo frames.

IMARC Group provides an analysis of the key trends in each sub-segment of the global TFT LCD panel market report, along with forecasts at the global and regional level from 2023-2028. Our report has categorized the market based on size, technology and application.

This report provides a deep insight into the global TFT LCD panel industry covering all its essential aspects. This ranges from macro overview of the market to micro details of the industry performance, recent trends, key market drivers and challenges, SWOT analysis, Porter’s five forces analysis, value chain analysis, etc. The report also provides a comprehensive analysis for setting up a TFT LCD manufacturing plant. The study analyses the manufacturing requirements, project cost, project funding, project economics, expected returns on investment, profit margins, etc. This report is a must-read for entrepreneurs, investors, researchers, consultants, business strategists, and all those who have any kind of stake or are planning to foray into the TFT LCD panel industry in any manner.

According to Taiwan media Central News Agency, IDC’s latest global large-size LCD panel price research report shows that in November, notebook computers and LCD panels were still affected by sluggish demand, and prices continued to fall. The reduction in production is effective, and the price decline is expected to continue to converge.

Analysts pointed out that the panel factory has not yet seen an increase in the production of laptops, LCD panels, which will help November, and December production of laptops, LCD panels to slow down the price drop, and even have the opportunity to drive the first quarter of 2023 panel price trend to the direction of a slight decline.

Survey shows that 11.6-inch HD wide viewing angle notebook panel output significantly reduced, but demand has not yet warmed up, the average price per piece in November fell 0.1 U.S. dollars; 14-inch, 15.6-inch HD wide viewing angle panel, although the panel factory to reduce production so that inventory gradually reduced, but also due to low-price competition in November fell 0.1 U.S. dollars; 14-inch full HD high-end wide viewing angle panel in the major panel factory inventory is still at a high water level, the fourth quarter continued to decline.

Glass substrate with ITO electrodes. The shapes of these electrodes will determine the shapes that will appear when the LCD is switched ON. Vertical ridges etched on the surface are smooth.

A liquid-crystal display (LCD) is a flat-panel display or other electronically modulated optical device that uses the light-modulating properties of liquid crystals combined with polarizers. Liquid crystals do not emit light directlybacklight or reflector to produce images in color or monochrome.seven-segment displays, as in a digital clock, are all good examples of devices with these displays. They use the same basic technology, except that arbitrary images are made from a matrix of small pixels, while other displays have larger elements. LCDs can either be normally on (positive) or off (negative), depending on the polarizer arrangement. For example, a character positive LCD with a backlight will have black lettering on a background that is the color of the backlight, and a character negative LCD will have a black background with the letters being of the same color as the backlight. Optical filters are added to white on blue LCDs to give them their characteristic appearance.

LCDs are used in a wide range of applications, including LCD televisions, computer monitors, instrument panels, aircraft cockpit displays, and indoor and outdoor signage. Small LCD screens are common in LCD projectors and portable consumer devices such as digital cameras, watches, calculators, and mobile telephones, including smartphones. LCD screens have replaced heavy, bulky and less energy-efficient cathode-ray tube (CRT) displays in nearly all applications. The phosphors used in CRTs make them vulnerable to image burn-in when a static image is displayed on a screen for a long time, e.g., the table frame for an airline flight schedule on an indoor sign. LCDs do not have this weakness, but are still susceptible to image persistence.

Each pixel of an LCD typically consists of a layer of molecules aligned between two transparent electrodes, often made of Indium-Tin oxide (ITO) and two polarizing filters (parallel and perpendicular polarizers), the axes of transmission of which are (in most of the cases) perpendicular to each other. Without the liquid crystal between the polarizing filters, light passing through the first filter would be blocked by the second (crossed) polarizer. Before an electric field is applied, the orientation of the liquid-crystal molecules is determined by the alignment at the surfaces of electrodes. In a twisted nematic (TN) device, the surface alignment directions at the two electrodes are perpendicular to each other, and so the molecules arrange themselves in a helical structure, or twist. This induces the rotation of the polarization of the incident light, and the device appears gray. If the applied voltage is large enough, the liquid crystal molecules in the center of the layer are almost completely untwisted and the polarization of the incident light is not rotated as it passes through the liquid crystal layer. This light will then be mainly polarized perpendicular to the second filter, and thus be blocked and the pixel will appear black. By controlling the voltage applied across the liquid crystal layer in each pixel, light can be allowed to pass through in varying amounts thus constituting different levels of gray.

The chemical formula of the liquid crystals used in LCDs may vary. Formulas may be patented.Sharp Corporation. The patent that covered that specific mixture expired.

Most color LCD systems use the same technique, with color filters used to generate red, green, and blue subpixels. The LCD color filters are made with a photolithography process on large glass sheets that are later glued with other glass sheets containing a TFT array, spacers and liquid crystal, creating several color LCDs that are then cut from one another and laminated with polarizer sheets. Red, green, blue and black photoresists (resists) are used. All resists contain a finely ground powdered pigment, with particles being just 40 nanometers across. The black resist is the first to be applied; this will create a black grid (known in the industry as a black matrix) that will separate red, green and blue subpixels from one another, increasing contrast ratios and preventing light from leaking from one subpixel onto other surrounding subpixels.Super-twisted nematic LCD, where the variable twist between tighter-spaced plates causes a varying double refraction birefringence, thus changing the hue.

LCD in a Texas Instruments calculator with top polarizer removed from device and placed on top, such that the top and bottom polarizers are perpendicular. As a result, the colors are inverted.

The optical effect of a TN device in the voltage-on state is far less dependent on variations in the device thickness than that in the voltage-off state. Because of this, TN displays with low information content and no backlighting are usually operated between crossed polarizers such that they appear bright with no voltage (the eye is much more sensitive to variations in the dark state than the bright state). As most of 2010-era LCDs are used in television sets, monitors and smartphones, they have high-resolution matrix arrays of pixels to display arbitrary images using backlighting with a dark background. When no image is displayed, different arrangements are used. For this purpose, TN LCDs are operated between parallel polarizers, whereas IPS LCDs feature crossed polarizers. In many applications IPS LCDs have replaced TN LCDs, particularly in smartphones. Both the liquid crystal material and the alignment layer material contain ionic compounds. If an electric field of one particular polarity is applied for a long period of time, this ionic material is attracted to the surfaces and degrades the device performance. This is avoided either by applying an alternating current or by reversing the polarity of the electric field as the device is addressed (the response of the liquid crystal layer is identical, regardless of the polarity of the applied field).

Displays for a small number of individual digits or fixed symbols (as in digital watches and pocket calculators) can be implemented with independent electrodes for each segment.alphanumeric or variable graphics displays are usually implemented with pixels arranged as a matrix consisting of electrically connected rows on one side of the LC layer and columns on the other side, which makes it possible to address each pixel at the intersections. The general method of matrix addressing consists of sequentially addressing one side of the matrix, for example by selecting the rows one-by-one and applying the picture information on the other side at the columns row-by-row. For details on the various matrix addressing schemes see passive-matrix and active-matrix addressed LCDs.

LCDs are manufactured in cleanrooms borrowing techniques from semiconductor manufacturing and using large sheets of glass whose size has increased over time. Several displays are manufactured at the same time, and then cut from the sheet of glass, also known as the mother glass or LCD glass substrate. The increase in size allows more displays or larger displays to be made, just like with increasing wafer sizes in semiconductor manufacturing. The glass sizes are as follows:

Until Gen 8, manufacturers would not agree on a single mother glass size and as a result, different manufacturers would use slightly different glass sizes for the same generation. Some manufacturers have adopted Gen 8.6 mother glass sheets which are only slightly larger than Gen 8.5, allowing for more 50 and 58 inch LCDs to be made per mother glass, specially 58 inch LCDs, in which case 6 can be produced on a Gen 8.6 mother glass vs only 3 on a Gen 8.5 mother glass, significantly reducing waste.AGC Inc., Corning Inc., and Nippon Electric Glass.

In 1922, Georges Friedel described the structure and properties of liquid crystals and classified them in three types (nematics, smectics and cholesterics). In 1927, Vsevolod Frederiks devised the electrically switched light valve, called the Fréedericksz transition, the essential effect of all LCD technology. In 1936, the Marconi Wireless Telegraph company patented the first practical application of the technology, "The Liquid Crystal Light Valve". In 1962, the first major English language publication Molecular Structure and Properties of Liquid Crystals was published by Dr. George W. Gray.RCA found that liquid crystals had some interesting electro-optic characteristics and he realized an electro-optical effect by generating stripe-patterns in a thin layer of liquid crystal material by the application of a voltage. This effect is based on an electro-hydrodynamic instability forming what are now called "Williams domains" inside the liquid crystal.

In the late 1960s, pioneering work on liquid crystals was undertaken by the UK"s Royal Radar Establishment at Malvern, England. The team at RRE supported ongoing work by George William Gray and his team at the University of Hull who ultimately discovered the cyanobiphenyl liquid crystals, which had correct stability and temperature properties for application in LCDs.

The idea of a TFT-based liquid-crystal display (LCD) was conceived by Bernard Lechner of RCA Laboratories in 1968.dynamic scattering mode (DSM) LCD that used standard discrete MOSFETs.

On December 4, 1970, the twisted nematic field effect (TN) in liquid crystals was filed for patent by Hoffmann-LaRoche in Switzerland, (Swiss patent No. 532 261) with Wolfgang Helfrich and Martin Schadt (then working for the Central Research Laboratories) listed as inventors.Brown, Boveri & Cie, its joint venture partner at that time, which produced TN displays for wristwatches and other applications during the 1970s for the international markets including the Japanese electronics industry, which soon produced the first digital quartz wristwatches with TN-LCDs and numerous other products. James Fergason, while working with Sardari Arora and Alfred Saupe at Kent State University Liquid Crystal Institute, filed an identical patent in the United States on April 22, 1971.ILIXCO (now LXD Incorporated), produced LCDs based on the TN-effect, which soon superseded the poor-quality DSM types due to improvements of lower operating voltages and lower power consumption. Tetsuro Hama and Izuhiko Nishimura of Seiko received a US patent dated February 1971, for an electronic wristwatch incorporating a TN-LCD.

In 1972, the concept of the active-matrix thin-film transistor (TFT) liquid-crystal display panel was prototyped in the United States by T. Peter Brody"s team at Westinghouse, in Pittsburgh, Pennsylvania.Westinghouse Research Laboratories demonstrated the first thin-film-transistor liquid-crystal display (TFT LCD).high-resolution and high-quality electronic visual display devices use TFT-based active matrix displays.active-matrix liquid-crystal display (AM LCD) in 1974, and then Brody coined the term "active matrix" in 1975.

In 1972 North American Rockwell Microelectronics Corp introduced the use of DSM LCDs for calculators for marketing by Lloyds Electronics Inc, though these required an internal light source for illumination.Sharp Corporation followed with DSM LCDs for pocket-sized calculators in 1973Seiko and its first 6-digit TN-LCD quartz wristwatch, and Casio"s "Casiotron". Color LCDs based on Guest-Host interaction were invented by a team at RCA in 1968.TFT LCDs similar to the prototypes developed by a Westinghouse team in 1972 were patented in 1976 by a team at Sharp consisting of Fumiaki Funada, Masataka Matsuura, and Tomio Wada,

In 1983, researchers at Brown, Boveri & Cie (BBC) Research Center, Switzerland, invented the passive matrix-addressed LCDs. H. Amstutz et al. were listed as inventors in the corresponding patent applications filed in Switzerland on July 7, 1983, and October 28, 1983. Patents were granted in Switzerland CH 665491, Europe EP 0131216,

The first color LCD televisions were developed as handheld televisions in Japan. In 1980, Hattori Seiko"s R&D group began development on color LCD pocket televisions.Seiko Epson released the first LCD television, the Epson TV Watch, a wristwatch equipped with a small active-matrix LCD television.dot matrix TN-LCD in 1983.Citizen Watch,TFT LCD.computer monitors and LCD televisions.3LCD projection technology in the 1980s, and licensed it for use in projectors in 1988.compact, full-color LCD projector.

In 1990, under different titles, inventors conceived electro optical effects as alternatives to twisted nematic field effect LCDs (TN- and STN- LCDs). One approach was to use interdigital electrodes on one glass substrate only to produce an electric field essentially parallel to the glass substrates.Germany by Guenter Baur et al. and patented in various countries.Hitachi work out various practical details of the IPS technology to interconnect the thin-film transistor array as a matrix and to avoid undesirable stray fields in between pixels.

Hitachi also improved the viewing angle dependence further by optimizing the shape of the electrodes (Super IPS). NEC and Hitachi become early manufacturers of active-matrix addressed LCDs based on the IPS technology. This is a milestone for implementing large-screen LCDs having acceptable visual performance for flat-panel computer monitors and television screens. In 1996, Samsung developed the optical patterning technique that enables multi-domain LCD. Multi-domain and In Plane Switching subsequently remain the dominant LCD designs through 2006.South Korea and Taiwan,

In 2007 the image quality of LCD televisions surpassed the image quality of cathode-ray-tube-based (CRT) TVs.LCD TVs were projected to account 50% of the 200 million TVs to be shipped globally in 2006, according to Displaybank.Toshiba announced 2560 × 1600 pixels on a 6.1-inch (155 mm) LCD panel, suitable for use in a tablet computer,

In 2016, Panasonic developed IPS LCDs with a contrast ratio of 1,000,000:1, rivaling OLEDs. This technology was later put into mass production as dual layer, dual panel or LMCL (Light Modulating Cell Layer) LCDs. The technology uses 2 liquid crystal layers instead of one, and may be used along with a mini-LED backlight and quantum dot sheets.

Since LCDs produce no light of their own, they require external light to produce a visible image.backlight. Active-matrix LCDs are almost always backlit.Transflective LCDs combine the features of a backlit transmissive display and a reflective display.

CCFL: The LCD panel is lit either by two cold cathode fluorescent lamps placed at opposite edges of the display or an array of parallel CCFLs behind larger displays. A diffuser (made of PMMA acrylic plastic, also known as a wave or light guide/guiding plateinverter to convert whatever DC voltage the device uses (usually 5 or 12 V) to ≈1000 V needed to light a CCFL.

EL-WLED: The LCD panel is lit by a row of white LEDs placed at one or more edges of the screen. A light diffuser (light guide plate, LGP) is then used to spread the light evenly across the whole display, similarly to edge-lit CCFL LCD backlights. The diffuser is made out of either PMMA plastic or special glass, PMMA is used in most cases because it is rugged, while special glass is used when the thickness of the LCD is of primary concern, because it doesn"t expand as much when heated or exposed to moisture, which allows LCDs to be just 5mm thick. Quantum dots may be placed on top of the diffuser as a quantum dot enhancement film (QDEF, in which case they need a layer to be protected from heat and humidity) or on the color filter of the LCD, replacing the resists that are normally used.

WLED array: The LCD panel is lit by a full array of white LEDs placed behind a diffuser behind the panel. LCDs that use this implementation will usually have the ability to dim or completely turn off the LEDs in the dark areas of the image being displayed, effectively increasing the contrast ratio of the display. The precision with which this can be done will depend on the number of dimming zones of the display. The more dimming zones, the more precise the dimming, with less obvious blooming artifacts which are visible as dark grey patches surrounded by the unlit areas of the LCD. As of 2012, this design gets most of its use from upscale, larger-screen LCD televisions.

RGB-LED array: Similar to the WLED array, except the panel is lit by a full array of RGB LEDs. While displays lit with white LEDs usually have a poorer color gamut than CCFL lit displays, panels lit with RGB LEDs have very wide color gamuts. This implementation is most popular on professional graphics editing LCDs. As of 2012, LCDs in this category usually cost more than $1000. As of 2016 the cost of this category has drastically reduced and such LCD televisions obtained same price levels as the former 28" (71 cm) CRT based categories.

Monochrome LEDs: such as red, green, yellow or blue LEDs are used in the small passive monochrome LCDs typically used in clocks, watches and small appliances.

Today, most LCD screens are being designed with an LED backlight instead of the traditional CCFL backlight, while that backlight is dynamically controlled with the video information (dynamic backlight control). The combination with the dynamic backlight control, invented by Philips researchers Douglas Stanton, Martinus Stroomer and Adrianus de Vaan, simultaneously increases the dynamic range of the display system (also marketed as HDR, high dynamic range television or FLAD, full-area local area dimming).

The LCD backlight systems are made highly efficient by applying optical films such as prismatic structure (prism sheet) to gain the light into the desired viewer directions and reflective polarizing films that recycle the polarized light that was formerly absorbed by the first polarizer of the LCD (invented by Philips researchers Adrianus de Vaan and Paulus Schaareman),

A pink elastomeric connector mating an LCD panel to circuit board traces, shown next to a centimeter-scale ruler. The conductive and insulating layers in the black stripe are very small.

A standard television receiver screen, a modern LCD panel, has over six million pixels, and they are all individually powered by a wire network embedded in the screen. The fine wires, or pathways, form a grid with vertical wires across the whole screen on one side of the screen and horizontal wires across the whole screen on the other side of the screen. To this grid each pixel has a positive connection on one side and a negative connection on the other side. So the total amount of wires needed for a 1080p display is 3 x 1920 going vertically and 1080 going horizontally for a total of 6840 wires horizontally and vertically. That"s three for red, green and blue and 1920 columns of pixels for each color for a total of 5760 wires going vertically and 1080 rows of wires going horizontally. For a panel that is 28.8 inches (73 centimeters) wide, that means a wire density of 200 wires per inch along the horizontal edge.

The LCD panel is powered by LCD drivers that are carefully matched up with the edge of the LCD panel at the factory level. The drivers may be installed using several methods, the most common of which are COG (Chip-On-Glass) and TAB (Tape-automated bonding) These same principles apply also for smartphone screens that are much smaller than TV screens.anisotropic conductive film or, for lower densities, elastomeric connectors.

Monochrome and later color passive-matrix LCDs were standard in most early laptops (although a few used plasma displaysGame Boyactive-matrix became standard on all laptops. The commercially unsuccessful Macintosh Portable (released in 1989) was one of the first to use an active-matrix display (though still monochrome). Passive-matrix LCDs are still used in the 2010s for applications less demanding than laptop computers and TVs, such as inexpensive calculators. In particular, these are used on portable devices where less information content needs to be displayed, lowest power consumption (no backlight) and low cost are desired or readability in direct sunlight is needed.

STN LCDs have to be continuously refreshed by alternating pulsed voltages of one polarity during one frame and pulses of opposite polarity during the next frame. Individual pixels are addressed by the corresponding row and column circuits. This type of display is called response times and poor contrast are typical of passive-matrix addressed LCDs with too many pixels and driven according to the "Alt & Pleshko" drive scheme. Welzen and de Vaan also invented a non RMS drive scheme enabling to drive STN displays with video rates and enabling to show smooth moving video images on an STN display.

Bistable LCDs do not require continuous refreshing. Rewriting is only required for picture information changes. In 1984 HA van Sprang and AJSM de Vaan invented an STN type display that could be operated in a bistable mode, enabling extremely high resolution images up to 4000 lines or more using only low voltages.

High-resolution color displays, such as modern LCD computer monitors and televisions, use an active-matrix structure. A matrix of thin-film transistors (TFTs) is added to the electrodes in contact with the LC layer. Each pixel has its own dedicated transistor, allowing each column line to access one pixel. When a row line is selected, all of the column lines are connected to a row of pixels and voltages corresponding to the picture information are driven onto all of the column lines. The row line is then deactivated and the next row line is selected. All of the row lines are selected in sequence during a refresh operation. Active-matrix addressed displays look brighter and sharper than passive-matrix addressed displays of the same size, and generally have quicker response times, producing much better images. Sharp produces bistable reflective LCDs with a 1-bit SRAM cell per pixel that only requires small amounts of power to maintain an image.

Segment LCDs can also have color by using Field Sequential Color (FSC LCD). This kind of displays have a high speed passive segment LCD panel with an RGB backlight. The backlight quickly changes color, making it appear white to the naked eye. The LCD panel is synchronized with the backlight. For example, to make a segment appear red, the segment is only turned ON when the backlight is red, and to make a segment appear magenta, the segment is turned ON when the backlight is blue, and it continues to be ON while the backlight becomes red, and it turns OFF when the backlight becomes green. To make a segment appear black, the segment is always turned ON. An FSC LCD divides a color image into 3 images (one Red, one Green and one Blue) and it displays them in order. Due to persistence of vision, the 3 monochromatic images appear as one color image. An FSC LCD needs an LCD panel with a refresh rate of 180 Hz, and the response time is reduced to just 5 milliseconds when compared with normal STN LCD panels which have a response time of 16 milliseconds.

Samsung introduced UFB (Ultra Fine & Bright) displays back in 2002, utilized the super-birefringent effect. It has the luminance, color gamut, and most of the contrast of a TFT-LCD, but only consumes as much power as an STN display, according to Samsung. It was being used in a variety of Samsung cellular-telephone models produced until late 2006, when Samsung stopped producing UFB displays. UFB displays were also used in certain models of LG mobile phones.

In-plane switching is an LCD technology that aligns the liquid crystals in a plane parallel to the glass substrates. In this method, the electrical field is applied through opposite el

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey