lcd panel price trend free sample

The global TFT-LCD display panel market attained a value of USD 148.3 billion in 2022. It is expected to grow further in the forecast period of 2023-2028 with a CAGR of 4.9% and is projected to reach a value of USD 197.6 billion by 2028.

The current global TFT-LCD display panel market is driven by the increasing demand for flat panel TVs, good quality smartphones, tablets, and vehicle monitoring systems along with the growing gaming industry. The global display market is dominated by the flat panel display with TFT-LCD display panel being the most popular flat panel type and is being driven by strong demand from emerging economies, especially those in Asia Pacific like India, China, Korea, and Taiwan, among others. The rising demand for consumer electronics like LCD TVs, PCs, laptops, SLR cameras, navigation equipment and others have been aiding the growth of the industry.

TFT-LCD display panel is a type of liquid crystal display where each pixel is attached to a thin film transistor. Since the early 2000s, all LCD computer screens are TFT as they have a better response time and improved colour quality. With favourable properties like being light weight, slim, high in resolution and low in power consumption, they are in high demand in almost all sectors where displays are needed. Even with their larger dimensions, TFT-LCD display panel are more feasible as they can be viewed from a wider angle, are not susceptible to reflection and are lighter weight than traditional CRT TVs.

The global TFT-LCD display panel market is being driven by the growing household demand for average and large-sized flat panel TVs as well as a growing demand for slim, high-resolution smart phones with large screens. The rising demand for portable and small-sized tablets in the educational and commercial sectors has also been aiding the TFT-LCD display panel market growth. Increasing demand for automotive displays, a growing gaming industry and the emerging popularity of 3D cinema, are all major drivers for the market. Despite the concerns about an over-supply in the market, the shipments of large TFT-LCD display panel again rose in 2020.

North America is the largest market for TFT-LCD display panel, with over one-third of the global share. It is followed closely by the Asia-Pacific region, where countries like India, China, Korea, and Taiwan are significant emerging market for TFT-LCD display panels. China and India are among the fastest growing markets in the region. The growth of the demand in these regions have been assisted by the growth in their economy, a rise in disposable incomes and an increasing demand for consumer electronics.

The report gives a detailed analysis of the following key players in the global TFT-LCD display panel Market, covering their competitive landscape, capacity, and latest developments like mergers, acquisitions, and investments, expansions of capacity, and plant turnarounds:

According to IMARC Group’s latest report, titled “TFT LCD Panel Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2022-2027”, the global TFT LCD panel market size reached US$ 157 Billion in 2021. Looking forward, IMARC Group expects the market to reach US$ 207.6 Billion by 2027, exhibiting a growth rate (CAGR) of 4.7% during 2022-2027.

A thin-film-transistor liquid-crystal display (TFT LCD) panel is a liquid crystal display that is generally attached to a thin film transistor. It is an energy-efficient product variant that offers a superior quality viewing experience without straining the eye. Additionally, it is lightweight, less prone to reflection and provides a wider viewing angle and sharp images. Consequently, it is generally utilized in the manufacturing of numerous electronic and handheld devices. Some of the commonly available TFT LCD panels in the market include twisted nematic, in-plane switching, advanced fringe field switching, patterned vertical alignment and an advanced super view.

The global market is primarily driven by continual technological advancements in the display technology. This is supported by the introduction of plasma enhanced chemical vapor deposition (PECVD) technology to manufacture TFT panels that offers uniform thickness and cracking resistance to the product. Along with this, the widespread adoption of the TFT LCD panels in the production of automobiles dashboards that provide high resolution and reliability to the driver is gaining prominence across the globe. Furthermore, the increasing demand for compact-sized display panels and 4K television variants are contributing to the market growth. Moreover, the rising penetration of electronic devices, such as smartphones, tablets and laptops among the masses, is creating a positive outlook for the market. Other factors, including inflating disposable incomes of the masses, changing lifestyle patterns, and increasing investments in research and development (R&D) activities, are further projected to drive the market growth.

The competitive landscape of the TFT LCD panel market has been studied in the report with the detailed profiles of the key players operating in the market.

Display includes screen, computer output surface, and a projection surface that displays content, mainly test, graphics, pictures, and videos utilizing cathode ray tube (CRT), light-emitting diode (LED), liquid crystal display (LCD), and other technologies. These displays are majorly incorporated in devices such as televisions, smartphones, tablets, laptops, vehicles, and others. Emergence of advanced technologies offer enhanced visualizations in several industry verticals, which include consumer electronics, retail, sports & entertainment, and transportation. 3D displays are in trend in consumer electronics and entertainment sector.

By display type, the display market outlook is divided into flat panel display, flexible panel display, and transparent panel display. Flat panel display segment was the highest revenue contributor to the market, in 2021. The flexible panel display segment dominated the display market growth, in terms of revenue, in 2021, and is expected to follow the same trend during the forecast period.

Region wise, the display market trends are analyzed across North America (the U.S., Canada, and Mexico), Europe (UK, Germany, France, and rest of Europe), Asia-Pacific China, Japan, India, South Korea, and rest of Asia-Pacific), and LAMEA (Latin America, the Middle East, and Africa). Asia-Pacific, specifically the China, remains a significant participant in the global display industry. Major organizations and government institutions in the country are intensely putting resources into these displays.

Top impacting factors of the market include high demand for flexible display technology in consumer electronic devices, increase in adoption of electronic components in the automotive sector, and rise in trend of touch-based devices. Surge in adoption of displays in touch screen devices, rise in need for AR/VR devices, and commercialization of autonomous vehicles are expected to create lucrative in the future. Moreover, stagnant growth of desktop PCs, notebooks, and tablets hampers growth of the display market. However, each of these factors is expected to have a definite impact on growth of the display industry in the coming years.

KEY BENEFITSFOR STAKEHOLDERSThis study comprises analytical depiction of the display market forecast along with the current trends and future estimations to depict the imminent investment pockets.

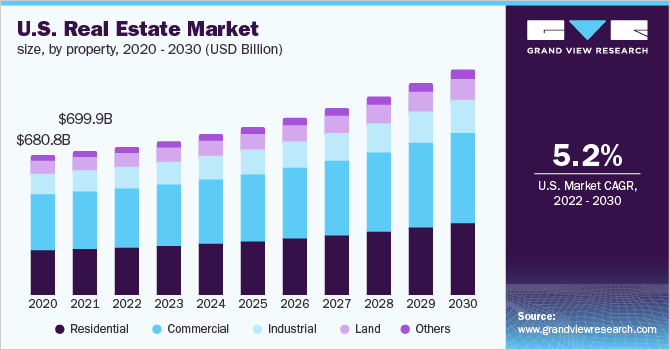

The U.S. large screen display market size was valued at $2.91 billion in 2020, and is projected to reach $8.45 billion by 2030, registering a CAGR of 11.0% from 2021 to 2030. Large screen displays are a class of large display screen formats, which improve the visual experience with its professional-grade image quality and are mostly used for endorsing and advertising. These displays have replaced the traditional small and micro-display screens with large wall-sized LED and LCD displays, used across various industries. They are designed for applications that require the vendors to engage their customers/audiences with its wider viewing angle and to extract maximum effectiveness from the marketing messages. In addition, these displays ensure higher durability and enhanced performance as against traditional display screens. Large screen displays are mostly suited for retail store, lobby, control room, or other professional application.

In addition, these displays provide high wavelength uniformity for fine pixel pitch displays. Further, they consume less power and deliver increased brightness, ultrahigh definition picture quality, improved color saturation, and faster response rate as compared to small OLEDs and LCDs, and thus, are suited for both indoor and outdoor displays.

Rise in demand for bright and power-efficient display panels and rapid digitalization and decline in demand for traditional billboards are the factors that drive the growth of theU.S. large screen display market.However, deployment of widescreen alternatives such as projectors and screenless displays, hampers the market growth to a certain extent. Furthermore, emerging display technology such as MicroLED and quantum dots and increase in preference of electronic giants toward large-screen displays offer lucrative opportunities for the U.S. large screen display market.

The U.S. large screen display market is segmented on the basis of screen size, application, product, location, end user, and region. By screen size, the market is classified into 80 Inch to 99 Inch, 100 inch to 149-inch, 150 inch to 199-inch, 200 inch to 300 inch, and above 300-inch segments. In 2020, the 80 Inch to 99 Inch segment secured highest revenue share and is expected to follow same trend during forecast period. Based on application, the market is divided into B to B and B to C applications, among which B to B segment is expected to dominate the U.S. large screen display market share.

The notable factors positively affecting the U.S. Large Screen Display Market include rise in demand for bright and power-efficient display panels, rapid digitalization, and decline in demand for traditional billboards. However, deployment of widescreen alternatives such as projectors and screenless displays, is expected to hinder the market growth. Moreover, emerging display technologies such as MicroLED & quantum dots and increase in preference of electronic giants toward large screen displays are expected to offer huge market opportunities in the coming years. Each of these factors is anticipated to have a definite impact on the U.S. large screen display market during the forecast period.

The key players profiled in the U.S. large screen display market report include iSEMC, Koninklijke Philips N.V., LG Electronics Inc., NEC Corporation, Panasonic Corporation, Planar Systems, Samsung Electronics Co. Ltd., Sony Corporation, ViewSonic Corporation, and Volanti Displays. These key players have adopted strategies, such as product portfolio expansion, mergers & acquisitions, agreements, geographical expansion, and collaborations to enhance their position in the U.S. large screen display industry. In 2019, Planer Systems launched 100-inch 4K LCD display with Ultra HD resolution (3840 x 2160), which offers high brightness of 700 nits and wide color gamut for stunning image quality and deep, rich color reproduction.

Key Benefits For StakeholdersThis study comprises analytical depiction of the U.S. large screen display market opportunities along with the current trends and future estimations to depict the imminent investment pockets.

Typical LCDs are edge-lit by a strip of white LEDs. The 2D backlighting system in Pro Display XDR is unlike any other. It uses a superbright array of 576 blue LEDs that allows for unmatched light control compared with white LEDs. Twelve controllers rapidly modulate each LED so that areas of the screen can be incredibly bright while other areas are incredibly dark. All of this produces an extraordinary contrast that’s the foundation for XDR.

With a massive amount of processing power, the timing controller (TCON) chip utilizes an algorithm specifically created to analyze and reproduce images. It controls LEDs at over 10 times the refresh rate of the LCD itself, reducing latency and blooming. It’s capable of multiple refresh rates for amazingly smooth playback. Managing both the LED array and LCD pixels, the TCON precisely directs light and color to bring your work to life with stunning accuracy.

The liquid crystal research of the 1960s was characterized by the discovery of and experiments on the properties of the liquid crystals. George H. Heilmeier of the RCA based his research on that of Williams, diving into the electro-optical nature of the crystals. After many attempts to use the liquid crystals to display different colors, he created the first working LCD using something called a dynamic scattering mode (DSM) that, when voltage is applied, turns the clear liquid crystal layer into a more translucent state. Heilmeier was thus deemed the inventor of the LCD.

In the late 1960s, the United Kingdom Royal Radar Establishment (RRE) discovered the cyanobiphenyl liquid crystal, a type that was fitting for LCD usage in terms of stability and temperature. In 1968, Bernard Lechner of RCA created the idea of a TFT-based LCD, and in that same year, he and several others brought that idea into reality using Heilmeier’s DSM LCD.

After the LCD’s entrance into the field of display technology, the 1970s were full of expansive research into improving the LCD and making it appropriate for a greater variety of applications. In 1970, the twisted nematic field effect was patented in Switzerland with credited inventors being Wolfgang Helfrich and Martin Schadt. This twisted nematic (TN) effect soon conjoined with products that entered the international markets like Japan’s electronic industry. In the US, the same patent was filed by James Fergason in 1971. His company, ILIXCO, known today as LXD Incorporated, manufactured TN-effect LCDs which grew to overshadow the DSM models. TN LCDs offered better features like lower operating voltages and power consumption.

From this, the first digital clock, or more specifically an electronic quartz wristwatch, using a TN-LCD and consisting of four digits was patented in the US and released to consumers in 1972. Japan’s Sharp Corporation, in 1975, began mass production of digital watch and pocket calculator TN LCDs, and eventually, other Japanese corporations began to rise in the market for wristwatch displays. Seiko, as an example, developed the first six-digit TN-based LCD quartz watch, an upgrade from the original four-digit watch.

Nevertheless, the DSM LCD was not rendered completely useless. A 1972 development by the North American Rockwell Microelectronics Corp integrated the DSM LCD into calculators marketed by Lloyds Electronics. These required a form of internal light to show the display, and so backlightswere also incorporated into these calculators. Shortly after, in 1973, Sharp Corporation brought DSM LCD pocket-sized calculators into the picture. A polymer called polyimide was used as the orientation layer of liquid crystal molecules.

In the 1980s, there was rapid progress made in creating usable products with this new LCD research. Color LCD television screens were first developed in Japan during this decade. Because of the limit in response times due to large display size (correlated with a large number of pixels), the first TVs were handheld/pocket TVs. Seiko Epson, or Epson, created the first LCD TV, releasing it to the public in 1982, which was soon followed by their first fully colored display pocket LCD TV in 1984. Also in 1984 was the first commercial TFT LCD display: Citizen Watch’s 2.7 inch color LCD TV. Shortly after, in 1988, Sharp Corporation created a 14 inch full-color TFT LCD that used an active matrix and had full-motion properties. Large-size LCDs now made LCD integration into large flat-panel displays like LCD screens and LCD monitors possible. LCD projection technology, first created by Epson, became readily available to consumers in compact and fully colored modes in 1989.

The LCD growth in the 1990s focused more on the optical properties of these new displays in attempts to advance their quality and abilities. Hitachi engineers were integral to the analysis of the LCD industry, previously centered in Japan, began expanding and moving towards South Korea, Taiwan, and later China as well.

As we entered the new century, the prominence of LCDs boomed. They surpassed the previously popular cathode-ray tube (CRT) displays in both image quality and sales across the world in 2007. Other developments continued to be made, such as the manufacturing of even larger displays, adoption of transparent and flexible materials for LCD hardware, and creation of more methods to

As of today, as LCD displays have developed quite a bit, but have remained consistent in structure. Illuminated by a backlight, the display consists of, from outermost to innermost two polarizers, two substrates (typically glass), electrodes, and the liquid crystal layer. Closer to the surface is sometimes a color filter as well, using an RGB scheme. As light passes through the polarizer closest to the backlight, it enters the liquid crystal layer. Now, depending on whether an electric field directed by the electrodes is present, the liquid crystal will behave differently. Whether using a TN, IPS, or MVS LCD, the electrode electric field will alter the orientation of the liquid crystal molecules to then affect the polarization of the passing light. If the light is polarized properly, it will pass completely through the color filter and surface polarizer, displaying a certain color. If partially polarized correctly, it will display a medium level of light, or a less bright color. If not polarized properly, the light will not pass the surface, and no color will be displayed.

1927: Vsevolod Frederiks in Russian devised the electrically switched light valve, called the Fréedericksz transition, the essential effect of all LCD technology.

1967: Bernard Lechner, Frank Marlowe, Edward Nester and Juri Tults built the first LCD to operate at television rates using discrete MOS transistors wired to the device.

1968: A research group at RCA laboratories in the US, headed by George Heilmeier, developed the first LCDs based on DSM (dynamic scattering mode) and the first bistable LCD using a mixture of cholesteric and nematic liquid crystals. The result sparked a worldwide effort to further develop LCDs. George H. Heilmeier was inducted in the National Inventors Hall of Fame and credited with the invention of LCDs. Heilmeier’s work is an IEEE Milestone.

1979, Peter Le Comber and Walter Spear at University of Dundee discovered that hydrogenated amorphous silicon (Alpha-Si:H) thin film transistors were suitable to drive LCDs. This is the major breakthrough that led to LCD television and computer displays.

1972: Tadashi Sasaki and Tomio Wada at Sharp Corporation built a prototype desktop calculator with a dynamic scattering LCD and started a program to build the first truly portable handheld calculator.

Fact.MR has announced the addition of the "LCD Panel Market Forecast, Trend Analysis & Competition Tracking - Global Review 2018 to 2028"report to their offering.

IMARC"s latest study "TFT LCD Panel Manufacturing Plant Project Report: Industry Trends, Manufacturing Process, Machinery, Raw Materials, Cost and Revenue" provides a techno-commercial roadmap for setting up a TFT LCD panel manufacturing plant.

Sharp has LCD panel factories in Kameyama and Sakai in Japan and produces small- and medium-sized panels for smartphones as well as large panels for TVs.

Sharp said yesterday it has agreed to pay Dell and two other companies US$198.5 million to settle a lawsuit for fixing LCD panel prices in Europe and North America.

Samsung Electronics Co Ltd (Korea:005930) (OTCOTHER: SSNLF) announced today that it is expanding the transparent display market with the production of a 46-inch transparent LCD panel, beginning this month.

The LCD panel business alliance still continues in a form, in order to "respond to such challenging conditions and to strengthen their respective market competitiveness," according to the statement released by Samsung.

As LCD panel prices continue to slide due to a supply glut, Sony is increasingly relying on other manufacturers for the key TV component as part of its cost-cutting efforts, the daily said.

With all the advantages and disadvantages, lcdds are essentially a good choice for those who see the TV starting from 4k smartphone. Nowadays, in addition to the wholesale models, lcdds are essentially a good option for those that don ’ t have the capacity of a device.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey