lcd display market free sample

The expansion of production LCD displays and their increased importance in automotive products drive the growth of the global automotive LCD display market.

The expansion of production LCD displays and their increased importance in automotive products drive the growth of the global automotive LCD display market. However, restricted view angle of LCD displays restricts the market growth. Moreover, increase in use of AR and VR devices in displays present new opportunities for the market in the coming years.

COVID-19 Scenario:The outbreak of the COVID-19 pandemic had a negative impact on the global automotive LCD display market, owing to temporary closure of manufacturing firms and disruptions in the supply chain during the prolonged lockdown.

European countries under lockdowns suffered major loss of businesses and revenues due to shutdown of manufacturing units in the region. Operations of production and manufacturing industries were heavily impacted by the outbreak of COVID-19, which led to the slowdown in the market growth.

Partnership/collaboration agreements with key stakeholders acted as a key strategy to sustain in the market. In the recent past, many leading players opted for product launch or partnership strategies to strengthen their foothold in the market.

Based on display size, the upto 7 inch segment held the highest market share in 2021, accounting for more than half of the global automotive LCD display market, and is estimated to maintain its leadership status throughout the forecast period. Moreover, the same segment is projected to manifest the

Based on vehicle type, the passenger car segment held the highest market share in 2021, accounting for nearly two-thirds of the global automotive LCD display market, and is estimated to maintain its leadership status throughout the forecast period. This is attributed to the huge demand for passenger cars throughout the world. However, the light commercial vehicle segment is projected to manifest the highest CAGR of 7.2% from 2022 to 2031, due to the adoption of advanced technologies.

Based on region, Asia-Pacific held the highest market share in terms of revenue in 2021, accounting for more than one-third of the global automotive LCD display market, and is likely to dominate the market during the forecast period. Moreover, the same region is expected to witness the fastest CAGR of 6.2% from 2022 to 2031. Surge in demand for interactive display, video walls, and touchscreen technology in this region, is expected to boost the market growth. The report also discusses other regions including the North America, Europe, and LAMEA.

Key Benefits For Stakeholders:This study comprises an analytical depiction of the market size along with the current trends and future estimations to depict the imminent investment pockets.

By Application (Smartphone & Tablet, Smart Wearable, Television & Digital Signage, PC & Laptop, Vehicle Display, and Others), Technology (OLED, Quantum Dot, LED, LCD, E-PAPER, and Others), Industry Vertical (Healthcare, Consumer Electronics, BFSI, Retail, Military & Defense, Automotive, and Others), Display Type (Flat Panel Display, Flexible Panel Display, and Transparent Panel Display): Global Opportunity Analysis and Industry Forecast, 2021-2031

By Type (Volumetric Display, Stereoscopic, and HMD), Technology (DLP RPTV, PDP, OLED, and LED), Access Method (Screen Based Display and Micro Display), and Application (TV, Smartphones, Monitor, Mobile Computing Devices, Projectors, HMD, and Others): Global Opportunity Analysis and Industry Forecast, 2021-2030

By Type (Visual Image, Retinal Display, and Synaptic Interface), Application (Holographic Projection, Head-mounted Display, Head-up Display, and Others), Industry Vertical (Aerospace & Defense, Automotive, Healthcare, Consumer Electronics, Commercial): Global Opportunity Analysis and Industry Forecast, 2020-2030

By Product (Auxiliary Display, Electronic Shelf Labels, E-Readers, and Others), Application (Consumer and Wearable Electronics, Institutional, Media and Entertainment, Retail, and Others): Global Opportunity Analysis and Industry Forecast, 2020-2030

Allied Market Research (AMR) is a full-service market research and business-consulting wing of Allied Analytics LLP based in Portland, Oregon. Allied Market Research provides global enterprises as well as medium and small businesses with unmatched quality of "

We are in professional corporate relations with various companies and this helps us in digging out market data that helps us generate accurate research data tables and confirms utmost accuracy in our market forecasting. Allied Market Research CEO Pawan Kumar is instrumental in inspiring and encouraging everyone associated with the company to maintain high quality of data and help clients in every way possible to achieve success. Each and every data presented in the reports published by us is extracted through primary interviews with top officials from leading companies of domain concerned. Our secondary data procurement methodology includes deep online and offline research and discussion with knowledgeable professionals and analysts in the industry.

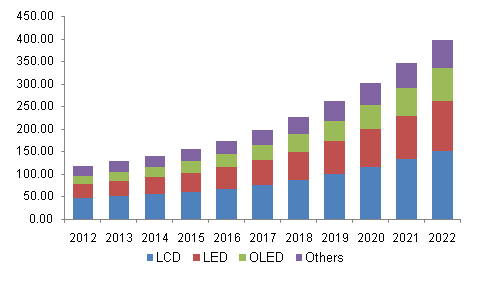

The global TFT-LCD display panel market attained a value of USD 148.3 billion in 2022. It is expected to grow further in the forecast period of 2023-2028 with a CAGR of 4.9% and is projected to reach a value of USD 197.6 billion by 2028.

The current global TFT-LCD display panel market is driven by the increasing demand for flat panel TVs, good quality smartphones, tablets, and vehicle monitoring systems along with the growing gaming industry. The global display market is dominated by the flat panel display with TFT-LCD display panel being the most popular flat panel type and is being driven by strong demand from emerging economies, especially those in Asia Pacific like India, China, Korea, and Taiwan, among others. The rising demand for consumer electronics like LCD TVs, PCs, laptops, SLR cameras, navigation equipment and others have been aiding the growth of the industry.

TFT-LCD display panel is a type of liquid crystal display where each pixel is attached to a thin film transistor. Since the early 2000s, all LCD computer screens are TFT as they have a better response time and improved colour quality. With favourable properties like being light weight, slim, high in resolution and low in power consumption, they are in high demand in almost all sectors where displays are needed. Even with their larger dimensions, TFT-LCD display panel are more feasible as they can be viewed from a wider angle, are not susceptible to reflection and are lighter weight than traditional CRT TVs.

The global TFT-LCD display panel market is being driven by the growing household demand for average and large-sized flat panel TVs as well as a growing demand for slim, high-resolution smart phones with large screens. The rising demand for portable and small-sized tablets in the educational and commercial sectors has also been aiding the TFT-LCD display panel market growth. Increasing demand for automotive displays, a growing gaming industry and the emerging popularity of 3D cinema, are all major drivers for the market. Despite the concerns about an over-supply in the market, the shipments of large TFT-LCD display panel again rose in 2020.

North America is the largest market for TFT-LCD display panel, with over one-third of the global share. It is followed closely by the Asia-Pacific region, where countries like India, China, Korea, and Taiwan are significant emerging market for TFT-LCD display panels. China and India are among the fastest growing markets in the region. The growth of the demand in these regions have been assisted by the growth in their economy, a rise in disposable incomes and an increasing demand for consumer electronics.

The report gives a detailed analysis of the following key players in the global TFT-LCD display panel Market, covering their competitive landscape, capacity, and latest developments like mergers, acquisitions, and investments, expansions of capacity, and plant turnarounds:

*At Expert Market Research, we strive to always give you current and accurate information. The numbers depicted in the description are indicative and may differ from the actual numbers in the final EMR report.

GlobalLiquid Crystal Display (LCD) Market, By Product (LCD Character Drivers, LCD Graphic Drivers, LCC Segment Drivers), Application (Automotive, Industrial, Medical, Small Appliance, Others) – Industry Trends and Forecast to 2029

Liquid crystal display (LCD) are widely being used in various sectors such as entertainment, corporate, transport, retail, hospitality, education, and healthcare, among others. These allow organizations in engaging with a broader audience. They also help in creating a centralized network for digital communications.

Global Liquid Crystal Display (LCD) Market was valued at USD 148.60 billion in 2021 and is expected to reach USD 1422.83 billion by 2029, registering a CAGR of 32.63% during the forecast period of 2022-2029. Small Appliance is expected to witness high growth owing to the rise in demand for devices such as smartphones. The market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis.

Liquid-crystal display is defined as aflat-panel display or other electronically modulated optical device which uses the light-modulating properties of liquid crystals combined with polarizers. Liquid crystals do not emit light directly, instead using a backlight or reflector to produce images in colour or monochrome.

This section deals with understanding the market drivers, advantages, opportunities, restraints and challenges. All of this is discussed in detail as below:

The increase in demand for the digitized promotion of products and services for attracting attention of the target audience acts as one of the major factors driving the growth of liquid crystal display (LCD) digital market.

The rise in demand for 4K digitized sign displays with the embedded software and media player accelerate the market growth. These signs deliver customers an affordable Ultra HD digital signage solution has a positive impact on the market.

The emergence of innovative products, such as leak detector systems, home monitoring systems and complicated monetary products further influence the market.

Additionally, rapid urbanization, change in lifestyle, surge in investments and increased consumer spending positively impact the liquid crystal display (LCD)digital market.

Furthermore, adoption of AMOLED displays, especially due to introduction of 5G and adoption of foldable and flexible displays extend profitable opportunities to the market players in the forecast period of 2022 to 2029. Also, rise in demand for Micro-LED and mini-LED technologies will further expand the market.

On the other hand, decline in demand for displays from retail sector due to drastic shift towards online advertisement, and high costs associated with new display technology-based products are expected to obstruct market growth. Also, deployment of widescreen alternatives, such as projectors and screenless displays is projected to challenge the liquid crystal display (LCD) digital market in the forecast period of 2022-2029.

This liquid crystal display(LCD) digital market report provides details of new recent developments, trade regulations, import-export analysis, production analysis, value chain optimization, market share, impact of domestic and localized market players, analyses opportunities in terms of emerging revenue pockets, changes in market regulations, strategic market growth analysis, market size, category market growths, application niches and dominance, product approvals, product launches, geographic expansions, technological innovations in the market. To gain more info on liquid crystal display (LCD) digital market contact Data Bridge Market Research for an Analyst Brief, our team will help you take an informed market decision to achieve market growth.

The COVID-19 has impacted liquid crystal display (LCD) digital market. The limited investment costs and lack of employees hampered sales and production of liquid crystal display (LCD) technology. However, government and market key players adopted new safety measures for developing the practices. The advancements in the technology escalated the sales rate of the li liquid crystal display (LCD) digital as it targeted the right audience. The increase in sales of devices across the globe is expected to further drive the market growth in the post-pandemic scenario.

Sharp launched the new massive 8K Ultra-HD professional LCD in November’2020. This display packs in 33 million pixels and employs a wide color gamut color filter coupled with optimized LED backlight phosphors.

The liquid crystal display (LCD) digital market is segmented on the basis of product and application. The growth amongst these segments will help you analyze meager growth segments in the industries and provide the users with a valuable market overview and market insights to help them make strategic decisions for identifying core market applications.

The liquid crystal display (LCD) digital market is analysed and market size insights and trends are provided by country, type, component, location, content category, end-user, size, display technology, brightness, and application as referenced above.

The countries covered in the liquid crystal display (LCD) digital market report are U.S., Canada, Mexico, Brazil, Argentina, Rest of South America, Germany, Italy, U.K., France, Spain, Netherlands, Belgium, Switzerland, Turkey, Russia, Rest of Europe, Japan, China, India, South Korea, Australia, Singapore, Malaysia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific, Saudi Arabia, U.A.E, South Africa, Egypt, Israel, Rest of Middle East and Africa (MEA).

North America dominates the liquid crystal display (LCD) digital market because of the presence of dedicated suppliers of the product and rise in demand for these displays in the retail industry within the region.

Asia-Pacific is expected to witness significant growth during the forecast period of 2022 to 2029 because of the rise in awareness regarding the benefits of LCD in the region.

The country section of the report also provides individual market impacting factors and changes in regulation in the market domestically that impacts the current and future trends of the market. Data points like down-stream and upstream value chain analysis, technical trends and porter"s five forces analysis, case studies are some of the pointers used to forecast the market scenario for individual countries. Also, the presence and availability of global brands and their challenges faced due to large or scarce competition from local and domestic brands, impact of domestic tariffs and trade routes are considered while providing forecast analysis of the country data.

The liquid crystal display (LCD) digital market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies" focus related to liquid crystal display (LCD) digital market.

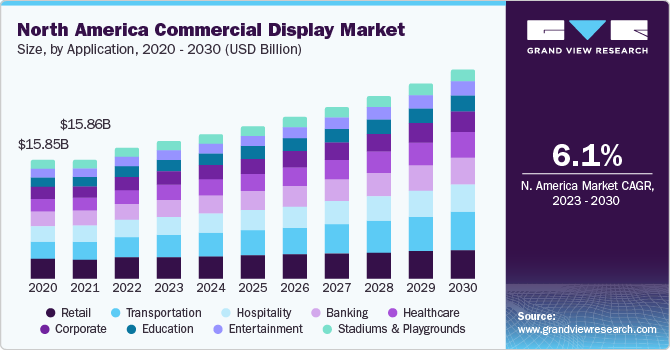

The global commercial display market size was valued at USD 51.17 billion in 2021. It is projected to reach USD 88.90 billion by 2030, growing at a CAGR of 7.2% during the forecast period (2022–2030). The commercial display is a subset of electronic displays that can manage centrally and individually to display text, animation, or video messages to an international audience. Commercial displays use technologies such as organic light-emitting diode (OLED), liquid crystal display (LCD), light-emitting diode (LED), quantum light-emitting diode (QLED), and projection for showing media and digital material, web pages, weather data, and text in a professional setting. Commercial displays are utilized extensively in the retail and hotel industries due to their extended warranties and ability to operate between 16 and 24 hours daily. In addition, this technology optimizes brightness in high-ambient-light circumstances and is integrated with a specific technology that contributes to superior onboard cooling, picture preservation, and resolution concerns.

In the commercial display industry, technological breakthroughs such as holographic displays, tactile touchscreens, and outdoor 3D screens raise product quality requirements and outweigh financial benefits. The commercial display market share is anticipated to increase steadily due to technological advancements and the widespread adoption of new technologies such as OLED and QLED.

The increasing need for digital signage in the healthcare and transportation industries is anticipated to propel the worldwide commercial display market"s expansion. Rapid industrialization, rising government spending on infrastructure development, and changing consumer lifestyles all contribute to the global expansion of the commercial display industry. Moreover, the increasing adoption of digital technologies by market participants for advertising products and services to make a strong impression on customers" minds is a major factor boosting the demand for commercial displays. In addition, the increasing integration of technologies such as AI and machine learning into commercial displays is driving the global market growth. The introduction of 4K and 8K displays accelerates the manufacturing of ultra-HD advertising content, contributing significantly to market expansion.

Increased urbanization and population growth, rising government spending on infrastructure building, and shifting consumer lifestyles are driving the rise of the commercial display market. Display technology developments and rising demand for energy-efficient panels are driving the expansion of the global commercial display industry. In addition, the increasing incorporation of technologies such as artificial intelligence and deep learning into commercial displays contributes to the market"s global growth.

The significant financial and energy costs associated with maintaining displays could impede the market growth. In addition, COVID-19 and its negative impact are a significant barrier to market expansion. As a result of these factors, display manufacturing has been halted all over the world. It is anticipated that an increase in commercial displays in industries such as hospitality, entertainment, banking, healthcare, education, and transportation will fuel the expansion of the market. Due to technological advancements and significant investments in research and development made by important companies to produce distinctive displays with sophisticated features, there is a sizable potential for market expansion.

In addition, the most recent low-cost display solutions are projected to penetrate a variety of commercial units such as restaurants, bars, and cafes at a faster rate. This is anticipated to give lucrative opportunities for the market. The growing popularity of contemporary technologies such as QLED, OLED, mini-LED, and micro-LED will give the sector multiple opportunities for growth in the years to come.

The digital signage segment dominates the market during the forecast period. The market category is divided into video walls, displays, transit LED screens, digital posters, and kiosks. In addition, the increasing preference for digital display solutions in business settings is also fueling the segment"s growth. The segment of display televisions is anticipated to grow at a CAGR of 4.23% during the forecast period. Manufacturers like SAMSUNG and LG Display Co., Ltd. are incorporating cutting-edge technology such as mini-LED and micro-LED into their most recent commercial-grade televisions. In addition, competitors are introducing many forms of TV panels, including rollable and flexible panels. These products are utilized extensively in hospitals, clinics, and multi-specialty healthcare institutions.

LCD is the most dominant segment during the forecast period. Several industry sectors, including corporate offices and banks, currently utilize LCD-based devices. One of the principal factors driving the widespread use of LCD technology is the decline in LCD production costs. However, the LED technology category is anticipated to account for a sizable market revenue share by 2030. LED technology improvements have led to the development of numerous LED displays, including OLED and QLED. Manufacturers widely employ these energy-efficient solutions in their commercial displays.

The hardware category retained the most significant market share during the forecast period. The segment"s expansion can be attributable to the greater demand for hardware than software. Displays, extenders and cables, accessories, and installation equipment are examples of hardware components. With the introduction of new and advanced software for digital signage, the software category had a significant market share. The software segment is expected to grow at an impressive CAGR of 6.26% during the forecast period. Due to the higher maintenance and repair requirements of commercial televisions and monitors, the services category experienced a substantially greater demand in 2021 than the software segment.

The flat panel display sector dominates the market during the forecast period. Numerous end-use sectors extensively employ flat-panel displays such as video walls, digital posters, monitors, and televisions. Entertainment, gaming, design, automotive, and manufacturing applications utilize curved panels extensively. These panels are widely utilized in TVs, monitors, smartphones, and wearable devices to satisfy various consumer demands.

Based on application, the market has been categorized into retail, hotel, entertainment, stadiums and playgrounds, corporate, banking, healthcare, education, and transportation.

The retail sector held the most significant market share during the forecast period. The central area requires digital advertisements for product and service marketing and promotion. Retailers are implementing a contemporary advertising strategy which is causing an increase in demand for commercial-grade televisions and digital signage. Due to the increasing number of hotels, motels, restaurants, QSRs, cafes, and bars, the hospitality industry is another significant contributor to the market expansion.

The sub-32-inch and 32-to-52-inch categories are expected to dominate the market during the forecast period. Customers prefer huge displays because of enhanced display clarity, energy-efficient technologies like OLED and micro-LED, and superior content quality. However, the sector of displays more significant than 75 inches is anticipated to have the highest CAGR due to the increasing demand for large-format displays. Retail, transportation, and healthcare industries use huge displays for signage purposes. In the past few years, leading players like SAMSUNG and LG Display Co., Ltd. have developed a plethora of commercial-grade televisions with displays more significant than 75 inches due to their growing popularity.

The global market for commercial displays has been classified by geography into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa.

North America accounted for more than 32.45% of the market share and is anticipated to dominate during the forecast period. Companies such as SAMSUNG, TCL North America, and others have developed a substantial consumer base in the area. In addition, the widespread usage of advanced display solutions across various industries is anticipated to stimulate regional market growth further. Asia-Pacific will experience the highest CAGR of 7.23% during the forecast period. Rapid urbanization and the increasing use of commercial displays in the healthcare, hotel, transportation, and retail sectors have contributed to the region"s expansion. In addition, the region is distinguished by the presence of manufacturers, original equipment manufacturers, and an extensive client base.

The global automotive LCD display market was valued at $7.2 billion in 2021, and is projected to reach $12.2 billion by 2031, growing at a CAGR of 5.6% from 2022 to 2031.

According to Vaishnavi Mate Lead Analyst, Semiconductor and Electronics, at Allied Market Research, the automotive LCD display Market is expected to showcase remarkable growth during the forecast period of 2022-2031. The report contains a thorough examination of the market size, automotive LCD display market trends, key market players, sales analysis, major driving factors, and key investment pockets. The report on the global automotive LCD display market provides an overview of the market as well as market definition and scope.

Automotive LCD displays are used to display vehicle information to driver and passengers. This display is also used for multimedia visualization. The emergence of advanced functions, including navigation, multimedia systems, driver assistance, and connected car features, and the improving driver-to-vehicle communication are anticipated to boost the use of the LCD display in the automotive sector. 3D displays are in trend in automotive sector. Also, LCD display technologies witness popularity at a high pace. In addition, the LCD display technology has gained increased importance in automotive products. Moreover, automotive manufacturers plan to incorporate LCD displays to attract the consumers. These automotive displays are highly customizable according to customer requirements. This display increases brand value of the vehicle. Hence, the expansion of production LCD displays is expected to drive the growth of the automotive LCD display market in this country.

Companies can operate their business in highly competitive market by launching new products or updated versions of existing products. Partnership/collaboration agreement with key stakeholders is expected to be a key strategy to sustain in the market. In the recent past, many leading players opted for product launch or partnership strategies to strengthen their foothold in the market.

The automotive lcd display market is segmented into Display Size and Vehicle Type.Factors such as growth in cloud computing, surge in edge computing, and rise in government regulations regarding localization of data centers fuel the growth of the automotive LCD display market size. However, restricted view angle of LCD displays may hamper the growth of the market. Furthermore, increase in AR and VR devices in displays is expected to offer lucrative opportunity for automotive LCD display market outlook.

On the basis of display size, the market is classified into upto 7 inch and more than7 inch. The upto 7 inch segment was the highest revenue contributor to the market and is expected to follow the same trend during the forecast period.

On the basis of vehicle type, it is categorized into passenger car, light commercial vehicle, and heavy commercial vehicle. Passenger car segment dominated the market in 2021.

On the basis of region, it is analyzed across North America, Europe, Asia-Pacific, and LAMEA along with their prominent countries. Asia-Pacific accounted for the largest market share in 2021. Major organizations and government institutions in the country are intensely putting resources into the technology to develop and deploy advanced technology solutions in the automotive.

Competitive analysis and profiles of the major globalautomotive LCD displayplayers that have been provided in the reportContinental AG, LG Display Corporation, Denso Corporation, Socionext, Yazaki, Japan Display Inc., Visteon Corporation, Samsung, Panasonic Corporation, Robert Bosch, and Sharp Corporation. These key players adopt several strategies such as new product launch and development, acquisition, partnership and collaboration and business expansion to increase the automotive LCD display market share during the forecast period.

Country-wise, the China acquired a prime share in the automotive LCD display industry in the Asia Pacific region and is expected to grow at a significant CAGR during the forecast period of 2019-2031.China holds major market share in terms of revenue generation from the sale of LCD display module because of the higher presence of presence of the automotive manufacturers.

In Europe, the UK, dominated the automotive LCD display market, in terms of revenue, in 2021 and is expected to follow the same trend during the forecast period. However, Germany is expected to emerge as the fastest-growing country in Europe"s automotive LCD display with a notable CAGR, due to advancement in the automotive industry which drives the usage of microelectronics in the country and thus creates lucrative growth automotive LCD display market opportunity in Germany.

In North America, U.S. is expected to emerge as a significant market for the automotive LCD display industry, owing to new developments in touch screen technologies has led to shift from single touch screen to sensitive multitouch screens. Continuous advancements in display technology help improve the quality of touch screen. Innovation in touch screen displays is the key driver expected to boost the market growth during the forecast period.

By LAMEA region, the Latin America country garner significant market share in 2021 due to the adoption of new technologies, digital transformation and connectivity are reshaping the future of automotive and the consumer electronics industry in Latin America. Moreover, the Middle East region is expected to grow at a significant CAGR from 2022 to 2031, owing to shifts in artificial intelligence, industry 4.0, and smart technological changes in recent years, which is expected to reshape the automotive LCD display market growth in the Middle East.

The significant factors impacting the automotive LCD display market include upsurge in adoption of Automotive LCD Monitor and LCD modules for automotive in touch screen devices. Rise in need for AR/VR devices and commercialization of autonomous vehicles is expected to create lucrative growth opportunities for the automotive LCD display market in the near future. However, restricted view angle of LCD displays restricts the market growth up to a certain level.

The globalautomotive LCD displaymarket is highly competitive, owing to the strong presence of existing vendors. Vendors of theautomotive LCD displaymarket with extensive technical and financial resources are expected to gain a competitive advantage over their competitors because they can cater to market demands. The competitive environment in this market is expected to increase as technological innovations, product extensions, and different strategies adopted by key vendors increase.

Continental AG, LG Display Corporation, Japan Display Inc., Visteon Corporation, Samsung, Panasonic Corporation, and Sharp Corporation are the top 5 companies holding a prime share in theautomotive LCD displaymarket. Top market players have adopted various strategies, such as product launches, contracts, and others to expand their foothold in the automotive LCD display market analysis.In August 2022, LG Display Co Ltd extended their liquid crystal display (LCD) production, as panel prices continue to rise on robust demand.

In May 2021, Japan Display Inc. (JDI) developed a 21.3-inch 5mega-pixel monochrome LCD (2048 × 2560ppi) with High-brightness and High-contrast ratio TFT display made by Dual-cell technology.

This study comprises an analytical depiction of the market size along with the current trends and future estimations to depict the imminent investment pockets.

Key Market Players LG Display Co Ltd, Denso Corporation, Socionext us, Yazaki Corp, JAPAN DISPLAY INC, Visteon Corporation, Samsung Electronics Co Ltd, Panasonic Corporation, Robert Bosch, Sharp Corporation, Continental AG

Glass substrate with ITO electrodes. The shapes of these electrodes will determine the shapes that will appear when the LCD is switched ON. Vertical ridges etched on the surface are smooth.

A liquid-crystal display (LCD) is a flat-panel display or other electronically modulated optical device that uses the light-modulating properties of liquid crystals combined with polarizers. Liquid crystals do not emit light directlybacklight or reflector to produce images in color or monochrome.seven-segment displays, as in a digital clock, are all good examples of devices with these displays. They use the same basic technology, except that arbitrary images are made from a matrix of small pixels, while other displays have larger elements. LCDs can either be normally on (positive) or off (negative), depending on the polarizer arrangement. For example, a character positive LCD with a backlight will have black lettering on a background that is the color of the backlight, and a character negative LCD will have a black background with the letters being of the same color as the backlight. Optical filters are added to white on blue LCDs to give them their characteristic appearance.

LCDs are used in a wide range of applications, including LCD televisions, computer monitors, instrument panels, aircraft cockpit displays, and indoor and outdoor signage. Small LCD screens are common in LCD projectors and portable consumer devices such as digital cameras, watches, digital clocks, calculators, and mobile telephones, including smartphones. LCD screens are also used on consumer electronics products such as DVD players, video game devices and clocks. LCD screens have replaced heavy, bulky cathode-ray tube (CRT) displays in nearly all applications. LCD screens are available in a wider range of screen sizes than CRT and plasma displays, with LCD screens available in sizes ranging from tiny digital watches to very large television receivers. LCDs are slowly being replaced by OLEDs, which can be easily made into different shapes, and have a lower response time, wider color gamut, virtually infinite color contrast and viewing angles, lower weight for a given display size and a slimmer profile (because OLEDs use a single glass or plastic panel whereas LCDs use two glass panels; the thickness of the panels increases with size but the increase is more noticeable on LCDs) and potentially lower power consumption (as the display is only "on" where needed and there is no backlight). OLEDs, however, are more expensive for a given display size due to the very expensive electroluminescent materials or phosphors that they use. Also due to the use of phosphors, OLEDs suffer from screen burn-in and there is currently no way to recycle OLED displays, whereas LCD panels can be recycled, although the technology required to recycle LCDs is not yet widespread. Attempts to maintain the competitiveness of LCDs are quantum dot displays, marketed as SUHD, QLED or Triluminos, which are displays with blue LED backlighting and a Quantum-dot enhancement film (QDEF) that converts part of the blue light into red and green, offering similar performance to an OLED display at a lower price, but the quantum dot layer that gives these displays their characteristics can not yet be recycled.

Since LCD screens do not use phosphors, they rarely suffer image burn-in when a static image is displayed on a screen for a long time, e.g., the table frame for an airline flight schedule on an indoor sign. LCDs are, however, susceptible to image persistence.battery-powered electronic equipment more efficiently than a CRT can be. By 2008, annual sales of televisions with LCD screens exceeded sales of CRT units worldwide, and the CRT became obsolete for most purposes.

Each pixel of an LCD typically consists of a layer of molecules aligned between two transparent electrodes, often made of Indium-Tin oxide (ITO) and two polarizing filters (parallel and perpendicular polarizers), the axes of transmission of which are (in most of the cases) perpendicular to each other. Without the liquid crystal between the polarizing filters, light passing through the first filter would be blocked by the second (crossed) polarizer. Before an electric field is applied, the orientation of the liquid-crystal molecules is determined by the alignment at the surfaces of electrodes. In a twisted nematic (TN) device, the surface alignment directions at the two electrodes are perpendicular to each other, and so the molecules arrange themselves in a helical structure, or twist. This induces the rotation of the polarization of the incident light, and the device appears gray. If the applied voltage is large enough, the liquid crystal molecules in the center of the layer are almost completely untwisted and the polarization of the incident light is not rotated as it passes through the liquid crystal layer. This light will then be mainly polarized perpendicular to the second filter, and thus be blocked and the pixel will appear black. By controlling the voltage applied across the liquid crystal layer in each pixel, light can be allowed to pass through in varying amounts thus constituting different levels of gray.

The chemical formula of the liquid crystals used in LCDs may vary. Formulas may be patented.Sharp Corporation. The patent that covered that specific mixture expired.

Most color LCD systems use the same technique, with color filters used to generate red, green, and blue subpixels. The LCD color filters are made with a photolithography process on large glass sheets that are later glued with other glass sheets containing a TFT array, spacers and liquid crystal, creating several color LCDs that are then cut from one another and laminated with polarizer sheets. Red, green, blue and black photoresists (resists) are used. All resists contain a finely ground powdered pigment, with particles being just 40 nanometers across. The black resist is the first to be applied; this will create a black grid (known in the industry as a black matrix) that will separate red, green and blue subpixels from one another, increasing contrast ratios and preventing light from leaking from one subpixel onto other surrounding subpixels.Super-twisted nematic LCD, where the variable twist between tighter-spaced plates causes a varying double refraction birefringence, thus changing the hue.

LCD in a Texas Instruments calculator with top polarizer removed from device and placed on top, such that the top and bottom polarizers are perpendicular. As a result, the colors are inverted.

The optical effect of a TN device in the voltage-on state is far less dependent on variations in the device thickness than that in the voltage-off state. Because of this, TN displays with low information content and no backlighting are usually operated between crossed polarizers such that they appear bright with no voltage (the eye is much more sensitive to variations in the dark state than the bright state). As most of 2010-era LCDs are used in television sets, monitors and smartphones, they have high-resolution matrix arrays of pixels to display arbitrary images using backlighting with a dark background. When no image is displayed, different arrangements are used. For this purpose, TN LCDs are operated between parallel polarizers, whereas IPS LCDs feature crossed polarizers. In many applications IPS LCDs have replaced TN LCDs, particularly in smartphones. Both the liquid crystal material and the alignment layer material contain ionic compounds. If an electric field of one particular polarity is applied for a long period of time, this ionic material is attracted to the surfaces and degrades the device performance. This is avoided either by applying an alternating current or by reversing the polarity of the electric field as the device is addressed (the response of the liquid crystal layer is identical, regardless of the polarity of the applied field).

Displays for a small number of individual digits or fixed symbols (as in digital watches and pocket calculators) can be implemented with independent electrodes for each segment.alphanumeric or variable graphics displays are usually implemented with pixels arranged as a matrix consisting of electrically connected rows on one side of the LC layer and columns on the other side, which makes it possible to address each pixel at the intersections. The general method of matrix addressing consists of sequentially addressing one side of the matrix, for example by selecting the rows one-by-one and applying the picture information on the other side at the columns row-by-row. For details on the various matrix addressing schemes see passive-matrix and active-matrix addressed LCDs.

LCDs, along with OLED displays, are manufactured in cleanrooms borrowing techniques from semiconductor manufacturing and using large sheets of glass whose size has increased over time. Several displays are manufactured at the same time, and then cut from the sheet of glass, also known as the mother glass or LCD glass substrate. The increase in size allows more displays or larger displays to be made, just like with increasing wafer sizes in semiconductor manufacturing. The glass sizes are as follows:

Until Gen 8, manufacturers would not agree on a single mother glass size and as a result, different manufacturers would use slightly different glass sizes for the same generation. Some manufacturers have adopted Gen 8.6 mother glass sheets which are only slightly larger than Gen 8.5, allowing for more 50 and 58 inch LCDs to be made per mother glass, specially 58 inch LCDs, in which case 6 can be produced on a Gen 8.6 mother glass vs only 3 on a Gen 8.5 mother glass, significantly reducing waste.AGC Inc., Corning Inc., and Nippon Electric Glass.

The origins and the complex history of liquid-crystal displays from the perspective of an insider during the early days were described by Joseph A. Castellano in Liquid Gold: The Story of Liquid Crystal Displays and the Creation of an Industry.IEEE History Center.Peter J. Wild, can be found at the Engineering and Technology History Wiki.

In 1922, Georges Friedel described the structure and properties of liquid crystals and classified them in three types (nematics, smectics and cholesterics). In 1927, Vsevolod Frederiks devised the electrically switched light valve, called the Fréedericksz transition, the essential effect of all LCD technology. In 1936, the Marconi Wireless Telegraph company patented the first practical application of the technology, "The Liquid Crystal Light Valve". In 1962, the first major English language publication Molecular Structure and Properties of Liquid Crystals was published by Dr. George W. Gray.RCA found that liquid crystals had some interesting electro-optic characteristics and he realized an electro-optical effect by generating stripe-patterns in a thin layer of liquid crystal material by the application of a voltage. This effect is based on an electro-hydrodynamic instability forming what are now called "Williams domains" inside the liquid crystal.

In 1964, George H. Heilmeier, then working at the RCA laboratories on the effect discovered by Williams achieved the switching of colors by field-induced realignment of dichroic dyes in a homeotropically oriented liquid crystal. Practical problems with this new electro-optical effect made Heilmeier continue to work on scattering effects in liquid crystals and finally the achievement of the first operational liquid-crystal display based on what he called the George H. Heilmeier was inducted in the National Inventors Hall of FameIEEE Milestone.

In the late 1960s, pioneering work on liquid crystals was undertaken by the UK"s Royal Radar Establishment at Malvern, England. The team at RRE supported ongoing work by George William Gray and his team at the University of Hull who ultimately discovered the cyanobiphenyl liquid crystals, which had correct stability and temperature properties for application in LCDs.

The idea of a TFT-based liquid-crystal display (LCD) was conceived by Bernard Lechner of RCA Laboratories in 1968.dynamic scattering mode (DSM) LCD that used standard discrete MOSFETs.

On December 4, 1970, the twisted nematic field effect (TN) in liquid crystals was filed for patent by Hoffmann-LaRoche in Switzerland, (Swiss patent No. 532 261) with Wolfgang Helfrich and Martin Schadt (then working for the Central Research Laboratories) listed as inventors.Brown, Boveri & Cie, its joint venture partner at that time, which produced TN displays for wristwatches and other applications during the 1970s for the international markets including the Japanese electronics industry, which soon produced the first digital quartz wristwatches with TN-LCDs and numerous other products. James Fergason, while working with Sardari Arora and Alfred Saupe at Kent State University Liquid Crystal Institute, filed an identical patent in the United States on April 22, 1971.ILIXCO (now LXD Incorporated), produced LCDs based on the TN-effect, which soon superseded the poor-quality DSM types due to improvements of lower operating voltages and lower power consumption. Tetsuro Hama and Izuhiko Nishimura of Seiko received a US patent dated February 1971, for an electronic wristwatch incorporating a TN-LCD.

In 1972, the concept of the active-matrix thin-film transistor (TFT) liquid-crystal display panel was prototyped in the United States by T. Peter Brody"s team at Westinghouse, in Pittsburgh, Pennsylvania.Westinghouse Research Laboratories demonstrated the first thin-film-transistor liquid-crystal display (TFT LCD).high-resolution and high-quality electronic visual display devices use TFT-based active matrix displays.active-matrix liquid-crystal display (AM LCD) in 1974, and then Brody coined the term "active matrix" in 1975.

In 1972 North American Rockwell Microelectronics Corp introduced the use of DSM LCDs for calculators for marketing by Lloyds Electronics Inc, though these required an internal light source for illumination.Sharp Corporation followed with DSM LCDs for pocket-sized calculators in 1973Seiko and its first 6-digit TN-LCD quartz wristwatch, and Casio"s "Casiotron". Color LCDs based on Guest-Host interaction were invented by a team at RCA in 1968.TFT LCDs similar to the prototypes developed by a Westinghouse team in 1972 were patented in 1976 by a team at Sharp consisting of Fumiaki Funada, Masataka Matsuura, and Tomio Wada,

In 1983, researchers at Brown, Boveri & Cie (BBC) Research Center, Switzerland, invented the passive matrix-addressed LCDs. H. Amstutz et al. were listed as inventors in the corresponding patent applications filed in Switzerland on July 7, 1983, and October 28, 1983. Patents were granted in Switzerland CH 665491, Europe EP 0131216,

The first color LCD televisions were developed as handheld televisions in Japan. In 1980, Hattori Seiko"s R&D group began development on color LCD pocket televisions.Seiko Epson released the first LCD television, the Epson TV Watch, a wristwatch equipped with a small active-matrix LCD television.dot matrix TN-LCD in 1983.Citizen Watch,TFT LCD.computer monitors and LCD televisions.3LCD projection technology in the 1980s, and licensed it for use in projectors in 1988.compact, full-color LCD projector.

In 1990, under different titles, inventors conceived electro optical effects as alternatives to twisted nematic field effect LCDs (TN- and STN- LCDs). One approach was to use interdigital electrodes on one glass substrate only to produce an electric field essentially parallel to the glass substrates.Germany by Guenter Baur et al. and patented in various countries.Hitachi work out various practical details of the IPS technology to interconnect the thin-film transistor array as a matrix and to avoid undesirable stray fields in between pixels.

Hitachi also improved the viewing angle dependence further by optimizing the shape of the electrodes (Super IPS). NEC and Hitachi become early manufacturers of active-matrix addressed LCDs based on the IPS technology. This is a milestone for implementing large-screen LCDs having acceptable visual performance for flat-panel computer monitors and television screens. In 1996, Samsung developed the optical patterning technique that enables multi-domain LCD. Multi-domain and In Plane Switching subsequently remain the dominant LCD designs through 2006.South Korea and Taiwan,

In 2007 the image quality of LCD televisions surpassed the image quality of cathode-ray-tube-based (CRT) TVs.LCD TVs were projected to account 50% of the 200 million TVs to be shipped globally in 2006, according to Displaybank.Toshiba announced 2560 × 1600 pixels on a 6.1-inch (155 mm) LCD panel, suitable for use in a tablet computer,transparent and flexible, but they cannot emit light without a backlight like OLED and microLED, which are other technologies that can also be made flexible and transparent.

In 2016, Panasonic developed IPS LCDs with a contrast ratio of 1,000,000:1, rivaling OLEDs. This technology was later put into mass production as dual layer, dual panel or LMCL (Light Modulating Cell Layer) LCDs. The technology uses 2 liquid crystal layers instead of one, and may be used along with a mini-LED backlight and quantum dot sheets.

Since LCDs produce no light of their own, they require external light to produce a visible image.backlight. Active-matrix LCDs are almost always backlit.Transflective LCDs combine the features of a backlit transmissive display and a reflective display.

CCFL: The LCD panel is lit either by two cold cathode fluorescent lamps placed at opposite edges of the display or an array of parallel CCFLs behind larger displays. A diffuser (made of PMMA acrylic plastic, also known as a wave or light guide/guiding plateinverter to convert whatever DC voltage the device uses (usually 5 or 12 V) to ≈1000 V needed to light a CCFL.

EL-WLED: The LCD panel is lit by a row of white LEDs placed at one or more edges of the screen. A light diffuser (light guide plate, LGP) is then used to spread the light evenly across the whole display, similarly to edge-lit CCFL LCD backlights. The diffuser is made out of either PMMA plastic or special glass, PMMA is used in most cases because it is rugged, while special glass is used when the thickness of the LCD is of primary concern, because it doesn"t expand as much when heated or exposed to moisture, which allows LCDs to be just 5mm thick. Quantum dots may be placed on top of the diffuser as a quantum dot enhancement film (QDEF, in which case they need a layer to be protected from heat and humidity) or on the color filter of the LCD, replacing the resists that are normally used.

WLED array: The LCD panel is lit by a full array of white LEDs placed behind a diffuser behind the panel. LCDs that use this implementation will usually have the ability to dim or completely turn off the LEDs in the dark areas of the image being displayed, effectively increasing the contrast ratio of the display. The precision with which this can be done will depend on the number of dimming zones of the display. The more dimming zones, the more precise the dimming, with less obvious blooming artifacts which are visible as dark grey patches surrounded by the unlit areas of the LCD. As of 2012, this design gets most of its use from upscale, larger-screen LCD televisions.

RGB-LED array: Similar to the WLED array, except the panel is lit by a full array of RGB LEDs. While displays lit with white LEDs usually have a poorer color gamut than CCFL lit displays, panels lit with RGB LEDs have very wide color gamuts. This implementation is most popular on professional graphics editing LCDs. As of 2012, LCDs in this category usually cost more than $1000. As of 2016 the cost of this category has drastically reduced and such LCD televisions obtained same price levels as the former 28" (71 cm) CRT based categories.

Monochrome LEDs: such as red, green, yellow or blue LEDs are used in the small passive monochrome LCDs typically used in clocks, watches and small appliances.

Today, most LCD screens are being designed with an LED backlight instead of the traditional CCFL backlight, while that backlight is dynamically controlled with the video information (dynamic backlight control). The combination with the dynamic backlight control, invented by Philips researchers Douglas Stanton, Martinus Stroomer and Adrianus de Vaan, simultaneously increases the dynamic range of the display system (also marketed as HDR, high dynamic range television or FLAD, full-area local area dimming).

The LCD backlight systems are made highly efficient by applying optical films such as prismatic structure (prism sheet) to gain the light into the desired viewer directions and reflective polarizing films that recycle the polarized light that was formerly absorbed by the first polarizer of the LCD (invented by Philips researchers Adrianus de Vaan and Paulus Schaareman),

Due to the LCD layer that generates the desired high resolution images at flashing video speeds using very low power electronics in combination with LED based backlight technologies, LCD technology has become the dominant display technology for products such as televisions, desktop monitors, notebooks, tablets, smartphones and mobile phones. Although competing OLED technology is pushed to the market, such OLED displays do not feature the HDR capabilities like LCDs in combination with 2D LED backlight technologies have, reason why the annual market of such LCD-based products is still growing faster (in volume) than OLED-based products while the efficiency of LCDs (and products like portable computers, mobile phones and televisions) may even be further improved by preventing the light to be absorbed in the colour filters of the LCD.

A pink elastomeric connector mating an LCD panel to circuit board traces, shown next to a centimeter-scale ruler. The conductive and insulating layers in the black stripe are very small.

A standard television receiver screen, a modern LCD panel, has over six million pixels, and they are all individually powered by a wire network embedded in the screen. The fine wires, or pathways, form a grid with vertical wires across the whole screen on one side of the screen and horizontal wires across the whole screen on the other side of the screen. To this grid each pixel has a positive connection on one side and a negative connection on the other side. So the total amount of wires needed for a 1080p display is 3 x 1920 going vertically and 1080 going horizontally for a total of 6840 wires horizontally and vertically. That"s three for red, green and blue and 1920 columns of pixels for each color for a total of 5760 wires going vertically and 1080 rows of wires going horizontally. For a panel that is 28.8 inches (73 centimeters) wide, that means a wire density of 200 wires per inch along the horizontal edge.

The LCD panel is powered by LCD drivers that are carefully matched up with the edge of the LCD panel at the factory level. The drivers may be installed using several methods, the most common of which are COG (Chip-On-Glass) and TAB (Tape-automated bonding) These same principles apply also for smartphone screens that are much smaller than TV screens.anisotropic conductive film or, for lower densities, elastomeric connectors.

Monochrome and later color passive-matrix LCDs were standard in most early laptops (although a few used plasma displaysGame Boyactive-matrix became standard on all laptops. The commercially unsuccessful Macintosh Portable (released in 1989) was one of the first to use an active-matrix display (though still monochrome). Passive-matrix LCDs are still used in the 2010s for applications less demanding than laptop computers and TVs, such as inexpensive calculators. In particular, these are used on portable devices where less information content needs to be displayed, lowest power consumption (no backlight) and low cost are desired or readability in direct sunlight is needed.

A comparison between a blank passive-matrix display (top) and a blank active-matrix display (bottom). A passive-matrix display can be identified when the blank background is more grey in appearance than the crisper active-matrix display, fog appears on all edges of the screen, and while pictures appear to be fading on the screen.

Displays having a passive-matrix structure are employing Crosstalk between activated and non-activated pixels has to be handled properly by keeping the RMS voltage of non-activated pixels below the threshold voltage as discovered by Peter J. Wild in 1972,

STN LCDs have to be continuously refreshed by alternating pulsed voltages of one polarity during one frame and pulses of opposite polarity during the next frame. Individual pixels are addressed by the corresponding row and column circuits. This type of display is called response times and poor contrast are typical of passive-matrix addressed LCDs with too many pixels and driven according to the "Alt & Pleshko" drive scheme. Welzen and de Vaan also invented a non RMS drive scheme enabling to drive STN displays with video rates and enabling to show smooth moving video images on an STN display.

Bistable LCDs do not require continuous refreshing. Rewriting is only required for picture information changes. In 1984 HA van Sprang and AJSM de Vaan invented an STN type display that could be operated in a bistable mode, enabling extremely high resolution images up to 4000 lines or more using only low voltages.

High-resolution color displays, such as modern LCD computer monitors and televisions, use an active-matrix structure. A matrix of thin-film transistors (TFTs) is added to the electrodes in contact with the LC layer. Each pixel has its own dedicated transistor, allowing each column line to access one pixel. When a row line is selected, all of the column lines are connected to a row of pixels and voltages corresponding to the picture information are driven onto all of the column lines. The row line is then deactivated and the next row line is selected. All of the row lines are selected in sequence during a refresh operation. Active-matrix addressed displays look brighter and sharper than passive-matrix addressed displays of the same size, and generally have quicker response times, producing much better images. Sharp produces bistable reflective LCDs with a 1-bit SRAM cell per pixel that only requires small amounts of power to maintain an image.

Segment LCDs can also have color by using Field Sequential Color (FSC LCD). This kind of displays have a high speed passive segment LCD panel with an RGB backlight. The backlight quickly changes color, making it appear white to the naked eye. The LCD panel is synchronized with the backlight. For example, to make a segment appear red, the segment is only turned ON when the backlight is red, and to make a segment appear magenta, the segment is turned ON when the backlight is blue, and it continues to be ON while the backlight becomes red, and it turns OFF when the backlight becomes green. To make a segment appear black, the segment is always turned ON. An FSC LCD divides a color image into 3 images (one Red, one Green and one Blue) and it displays them in order. Due to persistence of vision, the 3 monochromatic images appear as one color image. An FSC LCD needs an LCD panel with a refresh rate of 180 Hz, and the response time is reduced to just 5 milliseconds when compared with normal STN LCD panels which have a response time of 16 milliseconds.

Samsung introduced UFB (Ultra Fine & Bright) displays back in 2002, utilized the super-birefringent effect. It has the luminance, color gamut, and most of the contrast of a TFT-LCD, but only consumes as much power as an STN display, according to Samsung. It was being used in a variety of Samsung cellular-telephone models produced until late 2006, when Samsung stopped producing UFB displays. UFB displays were also used in certain models of LG mobile phones.

Twisted nematic displays contain liquid crystals that twist and untwist at varying degrees to allow light to pass through. When no voltage is applied to a TN liquid crystal cell, polarized light passes through the 90-degrees twisted LC layer. In proportion to the voltage applied, the liquid crystals untwist changing the polarization and blocking the light"s path. By properly adjusting the level of the voltage almost any gray level or transmission can be achieved.

In-plane switching is an LCD technology that aligns the liquid crystals in a plane parallel to the glass substrates. In this method, the electrical field is applied through opposite electrodes on the same glass substrate, so that the liquid crystals can be reoriented (switched) essentially in the same plane, although fringe fields inhibit a homogeneous reorientation. This requires two transistors for each pixel instead of the single transistor needed for a standard thin-film transistor (TFT) display. The IPS technology is used in everything from televisions, computer monitors, and even wearable devices, especially almost all LCD smartphone panels are IPS/FFS mode. IPS displays belong to the LCD panel family screen types. The other two types are VA and TN. Before LG Enhanced IPS was introduced in 2001 by Hitachi as 17" monitor in Market, the additional transistors resulted in blocking more transmission area, thus requiring a brighter backlight and consuming more power, making this type of display less desirable for notebook computers. Panasonic Himeji G8.5 was using an enhanced version of IPS, also LGD in Korea, then currently the world biggest LCD panel manufacture BOE in China is also IPS/FFS mode TV panel.

In 2015 LG Display announced the implementation of a new technology called M+ which is the addition of white subpixel along with the regular RGB dots in their IPS panel technology.

Most of the new M+ technology was employed on 4K TV sets which led to a controversy after tests showed that the addition of a white sub pixel replacing the traditional RGB structure would reduce the resolution by around 25%. This means that a 4K TV cannot display the full UHD TV standard. The media and internet users later called this "RGBW" TVs because of the white sub pixel. Although LG Display has developed this technology for use in notebook display, outdoor and smartphones, it became more popular in the TV market because the announced 4K UHD resolution but still being incapable of achieving true UHD resolution defined by the CTA as 3840x2160 active pixels with 8-bit color. This negatively impacts the rendering of text, making it a bit fuzzier, which is especially noticeable when a TV is used as a PC monitor.

In 2011, LG claimed the smartphone LG Optimus Black (IPS LCD (LCD NOVA)) has the brightness up to 700 nits, while the competitor has only IPS LCD with 518 nits and double an active-matrix OLED (AMOLED) display with 305 nits. LG also claimed the NOVA display to be 50 percent more efficient than regular LCDs and to consume only 50 percent of the power of AMOLED displays when producing white on screen.

This pixel-layout is found in S-IPS LCDs. A chevron shape is used to widen the viewing cone (range of viewing directions with good contrast and low color shift).

Vertical-alignment displays are a form of LCDs in which the liquid crystals naturally align

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey