lcd panel demand manufacturer

LCD displays utilize two sheets of polarizing material with a liquid crystal solution between them. An electric current passed through the liquid causes the crystals to align so that light cannot pass through them. Each crystal, therefore, is like a shutter, either allowing light to pass through or blocking the light. LCD panel is the key components of LCD display. And the price trends of LCD panel directly affect the price of liquid crystal displays. LCD panel consists of several components: Glass substrate, drive electronics, polarizers, color filters etc. Only LCD panel applied for TV will be counted in this report

Samsung Display, LG Display, Innolux Crop and AUO captured the top four revenue share spots in the LCD TV Panel market in 2015. Samsung Display dominated with 22.11 percent revenue share, followed by LG Display with 19.72 percent revenue share and Innolux Crop Display with 19.30 percent revenue share.

The global LCD TV Panel market is valued at 51130 million USD in 2020 is expected to reach 59640 million USD by the end of 2026, growing at a CAGR of 2.2% during 2021-2026.

Which are the prominent LCD TV Panel Market players across the Globe? ● Along with this survey you also get their Product Information Types (32"" and Below, 37"", 39"", 40""/42""/43"", 46""/47""48"", 50"", 55""/58"", 60"", 65"", 65""+), Applications (Residential, Commercial), and Specification. Detailed profiles of the Top major players in the industry:Samsung Display, LG Display, Innolux Crop., AUO, CSOT, BOE, Sharp, Panasonic, CEC-Panda

● LCD TV Panel Market research contains an in-depth analysis of report complete data on factors influencing demand, growth, opportunities, challenges, and restraints, and Analysis of Pre and Post COVID-19 Market.

What Overview LCD TV Panel Market Says? ● This Overview Includes Diligent Analysis of Scope, Types, Application, Sales by region, types and applications.

LCD TV Panel Market Manufacturing Cost Analysis ● This Analysis is done by considering prime elements like Key RAW Materials, Price Trends, Market Concentration Rate of Raw Materials, Proportion of Raw Materials and Labour Cost in Manufacturing Cost Structure.

The Global LCD TV Panel market is expected to rise at a considerable rate during the forecast period, between 2022 and LCD TV Panel. In 2021, the market is rising at a steady rate and with the expanding adoption of strategies by key players, the market is expected to rise over the projected horizon.

LCD TV Panel Market Report identifies various key players in the market and sheds light on their strategies and collaborations to combat competition. The comprehensive report provides a two-dimensional picture of the market. By knowing the global revenue of manufacturers, the global price of manufacturers, and the production by manufacturers during the forecast period of 2022 to LCD TV Panel, the reader can identify the footprints of manufacturers in the LCD TV Panel industry.

As well as providing an overview of successful marketing strategies, market contributions, and recent developments of leading companies, the report also offers a dashboard overview of leading companies" past and present performance. Several methodologies and analyses are used in the research report to provide in-depth and accurate information about the LCD TV Panel Market.

The current market dossier provides market growth potential, opportunities, drivers, industry-specific challenges and risks market share along with the growth rate of the global LCD TV Panel market. The report also covers monetary and exchange fluctuations, import-export trade, and global market

status in a smooth-tongued pattern. The SWOT analysis, compiled by industry experts, Industry Concentration Ratio and the latest developments for the global LCD TV Panel market share are covered in a statistical way in the form of tables and figures including graphs and charts for easy understanding.

LCD TV Panel Market Growth rate or CAGR exhibited by a market certain forecast period is calculate on the basic types, application, company profile and their impact on the market. Secondary Research Information is collected from a number of publicly available as well as paid databases. Public sources involve publications by different associations and governments, annual reports and statements of companies, white papers and research publications by recognized industry experts and renowned academia, etc. Paid data sources include third-party authentic industry databases.

Geographically, this report is segmented into several key regions, with sales, revenue, market share and growth Rate of LCD TV Panel in these regions, from 2015 to 2026, covering ● North America (United States, Canada and Mexico)

This LCD TV Panel Market Research/Analysis Report give Answers to following Questions: ● How Porter"s Five Forces model helps you to study LCD TV Panel Market?

● Which Manufacturing Technology is used for LCD TV Panel? What Developments Are Going On in That Technology? Which Trends Are Causing These Developments?

With tables and figures helping analyse worldwide Global LCD TV Panel market trends, this research provides key statistics on the state of the industry and is a valuable source of guidance and direction for companies and individuals interested in the market.

LCD TV Panel Market is 2022 Research Report on Global professional and comprehensive report on the LCD TV Panel Market. The report monitors the key trends and market drivers in the current scenario and offers on the ground insights. Top Key Players are – Samsung Display, LG Display, Innolux Crop., AUO, CSOT, BOE, Sharp, Panasonic, CEC-Panda.

Global “LCD TV Panel Market” (2022-2028) the report additionally centers around worldwide significant makers of the LCD TV Panel market with important data, such as, company profiles, segmentation information, challenges and limitations, driving factors, value, cost, income and contact data. Upstream primitive materials and hardware, coupled with downstream request examination is likewise completed. The Global LCD TV Panel market improvement patterns and marketing channels are breaking down. In conclusion, the attainability of new speculation ventures is surveyed and in general, the research ends advertised.

Global LCD TV Panel Market Report 2022 is spread across 117 pages and provides exclusive vital statistics, data, information, trends and competitive landscape details in this niche sector.

LCD displays utilize two sheets of polarizing material with a liquid crystal solution between them. An electric current passed through the liquid causes the crystals to align so that light cannot pass through them. Each crystal, therefore, is like a shutter, either allowing light to pass through or blocking the light. LCD panel is the key components of LCD display. And the price trends of LCD panel directly affect the price of liquid crystal displays. LCD panel consists of several components: Glass substrate, drive electronics, polarizers, color filters etc. Only LCD panel applied for TV will be counted in this report.

Due to the COVID-19 pandemic, the global LCD TV Panel market size is estimated to be worth USD 53490 million in 2021 and is forecast to a readjusted size of USD 53490 million by 2028 with a CAGR of 2.2% during the review period. Fully considering the economic change by this health crisis, by Size accounting for (%) of the LCD TV Panel global market in 2021, is projected to value USD million by 2028, growing at a revised (%) CAGR in the post-COVID-19 period. While by Size segment is altered to an (%) CAGR throughout this forecast period.

Global LCD TV Panel key players include Samsung Display, LG Display, Innolux Crop, AUO, CSOT, etc. Global top five manufacturers hold a share over 80%.

The global LCD TV Panel market is segmented by company, region (country), by Size and by Application. Players, stakeholders, and other participants in the global LCD TV Panel market will be able to gain the upper hand as they use the report as a powerful resource. The segmental analysis focuses on sales, revenue and forecast by region (country), by Size and by Application for the period 2017-2028.

Global LCD TV Panel market analysis and market size information is provided by regions (countries). Segment by Application, the LCD TV Panel market is segmented into United States, Europe, China, Japan, Southeast Asia, India and Rest of World. The report includes region-wise LCD TV Panel market forecast period from history 2017-2028. It also includes market size and forecast by players, by Type, and by Application segment in terms of sales and revenue for the period 2017-2028.

The report introduced the LCD TV Panel basics: definitions, classifications, applications and market overview; product specifications; manufacturing processes; cost structures, raw materials and so on. Then it analyzed the world’s main region market conditions, including the product price, profit, capacity, production, supply, demand and market growth rate and forecast etc. In the end, the report introduced new project SWOT analysis, investment feasibility analysis, and investment return analysis.

LCD TV Panel market size competitive landscape provides details and data information by players. The report offers comprehensive analysis and accurate statistics on revenue by the player for the period 2017-2021. It also offers detailed analysis supported by reliable statistics on revenue (global and regional level) by players for the period 2017-2021. Details included are company description, major business, company total revenue and the sales, revenue generated in LCD TV Panel business, the date to enter into the LCD TV Panel market, LCD TV Panel product introduction, recent developments, etc.

The report offers detailed coverage of LCD TV Panel industry and main market trends with impact of coronavirus. The market research includes historical and forecast market data, demand, application details, price trends, and company shares of the leading LCD TV Panel by geography. The report splits the market size, by volume and value, on the basis of application type and geography. Report covers the present status and the future prospects of the global LCD TV Panel market for 2017-2028.

Global LCD TV Panel Market report forecast to 2028 is a professional and comprehensive research report on the world’s major regional market conditions, focusing on the main regions (North America, Europe and Asia-Pacific) and the main countries (United States, Germany, United Kingdom, Japan, South Korea and China).

To Know How COVID-19 Pandemic Will Impact LCD TV Panel Market/Industry- Request a sample copy of the report-https://www.researchreportsworld.com/enquiry/request-covid19/21019731

The report offers exhaustive assessment of different region-wise and country-wise LCD TV Panel market such as U.S., Canada, Germany, France, U.K., Italy, Russia, China, Japan, South Korea, India, Australia, Taiwan, Indonesia, Thailand, Malaysia, Philippines, Vietnam, Mexico, Brazil, Turkey, Saudi Arabia, U.A.E, etc. Key regions covered in the report are North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

For the period 2017-2028, the report provides country-wise revenue and volume sales analysis and region-wise revenue and volume analysis of the global LCD TV Panel market. For the period 2017-2021, it provides sales (consumption) analysis and forecast of different regional markets by Application as well as by Type in terms of volume.

What are the market opportunities and threats faced by the vendors in the global LCD TV Panel market? What industrial trends, drivers, and challenges are manipulating its growth?

With tables and figures helping analyze worldwide Global LCD TV Panel market trends, this research provides key statistics on the state of the industry and is a valuable source of guidance and direction for companies and individuals interested in the market.

We have thousands of standard products that are in stock and available from our Seattle, WA and Hong Kong warehouses to support fast product development and preproduction without MOQ. The stock covers TN, STN LCD display panels, COB, COG character LCD display, graphic LCD display, PMOLED, AMOLED display, TFT display, IPS display, high brightness and transflective, blanview sunlight readable display, super high contrast ratio display, lightning fast response displays, efficient low power consumption display, extreme temperature range display, HMI display, HDMI display, Raspberry Pi Display, Arduino display, embedded display, capacitive touch screen, LED backlight etc. Customers can easily purchase samples directly from our website to avoid time delays with setting up accounts and credit terms and shipping within 24 hours.

Many of our customers require customized OEM display solutions. With over two decades of experience, we apply our understanding of available display solutions to meet our customer’s requirements and assist from project concept to mass production. Using your ideas and requirements as a foundation, we work side by side with you to develop ideas/concepts into drawings, build prototypes and to final production seamlessly. In order to meet the fast changing world, we can provide the fastest turnaround in the industry, it takes only 3-4 weeks to produce LCD panels samples and 4-6 weeks for LCD display module, TFT LCD, IPS LCD display, and touch screen samples. The production time is only 4-5 weeks for LCD panels and 5-8 weeks for LCD display module, TFT LCD, IPS LCD display, and touch screen.

Among the world famous brands, the screen of South Korea"s samsung and LG is known to be produced and sold by themselves.Display screens of other niche brands, and those brands capable of self-production and self-marketing, also have an unassailable position in their own segments, facing various brands.For buyers, how to find suitable suppliers from these LCD panel manufacturers?

The world-renowned LCD panel production line is mainly controlled by several enterprises: au optronics in Taiwan;Chi mei electronics in Taiwan, China;Sharp, Japan;South Korea samsung, South Korea LG;Philips;Boe, etc.These companies supply the world"s main demand for liquid crystal displays.

LG Display is currently the world"s first LCD panel manufacturer. It is affiliated to LG group and headquartered in Seoul, South Korea.Its subsidiaries are: LG electronics, LG display, GS caltex, LG chemistry, LG life and health, etc., covering the fields of chemical energy, electronics and appliances, communication and service.LG Display"s customers include Apple, HP, DELL, SONY, Toshiba, PHILIPS, Lenovo, Acer and other world-class consumer electronics manufacturers.LG"s manufacturing base in China is in nanjing, shenyang.

Samsung electronics is South Korea"s largest electronics company and the largest subsidiary of the samsung group.Its product development strategy emphasizes not only the matching principle of "leading technology, using the most advanced technology to develop new products in the leading-in stage to meet the high-end market demand", but also the matching principle of "leading technology, using the most advanced technology to develop new products, creating new demand and new high-end market".Samsung"s customers are mainly targeting samsung itself.Samsung"s manufacturing base in China is in suzhou, nanjing.

Innolux is a tft-lcd panel manufacturing company founded by foxconn technology group in 2003.The factory is located in longhua foxconn technology park in shenzhen.Innolux has a strong display technology research and development team, coupled with foxconn"s strong manufacturing capacity, to effectively play the vertical integration benefits, to improve the level of the world plane display industry will have a pointer contribution.In March 2010, it merged with chi mei electronics and tong bao optoelectronics.

Au optronics, formerly known as acer technology, was founded in August 1996. It was renamed au optronics after the merger of au optronics and united optronics in 2001.Au optronics is the world"s first tft-lcd design, manufacturing and development company to be publicly listed on the New York stock exchange (NYSE).

Boe, founded in April 1993, is the largest display panel manufacturer in China and a provider of Internet of things technology, products and services.At present, boe has reached the world"s first place in the field of notebook LCD, flat LCD and mobile LCD. With its success in joining the apple supply chain, boe will become the world"s top three LCD panel manufacturers in the near future.

Sharp is known as "the father of LCD panel".Since its founding in 1912, sharp corporation has been developing the world"s first calculator and liquid crystal display, represented by the live pencil, which is the name of the company. At the same time, sharp corporation has been actively expanding new fields, contributing to the improvement of human living standards and social progress.Sharp is already owned by foxconn.

The company has set up tft-lcd key materials and technology national engineering laboratory, national enterprise technology center, post-doctoral mobile workstation, and undertakes national development and reform commission, ministry of science and technology, ministry of industry and information technology and other major national special projects.The company"s strong technology and scientific research capabilities become the cornerstone of the company"s sustainable development.

With the explosive growth of new energy vehicles and vehicle intelligence in 2021, in-vehicle display technology has also undergone a period of rapid development. First, end-users and OEMs have begun to pursue multi-screen, high-resolution, and large-size displays. And, secondly, major panel manufacturers have actively adopted diversification strategies based on their own particular strengths and adjusted their own layouts accordingly.

These changes are clearly visible in the numbers. According to statistics from Sigmaintell, for instance, the global demand for front-mountedvehicle display panels in 2021 was about 160 million pieces, a year-on-year increase of about 21.2%. And, on top of this, shipments of LTPD LCD panels also rapidly increased, with the penetration rate topping out at 12.0% in 2021. This increase is made even more remarkable when one considers that the automotive market was heavily affected by chip shortages in the second half of 2021.

Heading into 2022, the ongoing Russian-Ukrainian war casts a new shadow on the already tight supply situation and thus threatens to slow down the pace of vehicle display growth. However, due to the accelerated penetration of automobile intelligence (especially in new energy vehicles, which tend to be the most significant carriers of automobile intelligence) and vehicle-mounted displays as an important hardware facility for human-computer interaction, the trend towards the adoption of large-screen and multi-screen displays is likely to continue at pace. Sigmaintell clearly believe this is the case, as they estimate that global shipments of automotive display panels (only front-mounted) in 2022 will likely exceed 180 million units – a year-on-year increase of about 11.5%.

Prior to the Covid-19 pandemic outbreak in early 2020, the flat-panel display (FPD) market was gloomy. Oversupply, falling prices and losses were the common themes in the market.

It’s been a different story during the outbreak. In 2020, the FPD market rebounded. In the stay-at-home economy, consumers went on a buying spree for monitors, PCs, tablets and TVs. As a result, demand for displays exploded. And shortages soon surfaced for display driver ICs and other components.

Cars, industrial equipment, PCs, smartphones and other products all incorporate flat-panel displays in one form or another. The majority of TV screens are based on liquid-crystal displays (LCDs). TVs use other display types, such as organic light-emitting diodes (OLEDs) and quantum dots.

Smartphone displays are based on LCDs and OLEDs. Other display technologies, such as microLEDs and miniLEDs, are in the works. Flat-panel displays are made in giant fabs. Suppliers from China, Korea and Taiwan dominate the display market.

It’s been a roller coaster ride in the arena. “Before Covid, the FPD market in the second half of 2019 was not very pretty,” said Ross Young, CEO of Display Supply Chain Consultants (DSCC), in a presentation at Display Week 2021. “We had declining revenues, declining prices, declining margins, companies announcing their exit in the LCD market, CapEx was falling, and there was little interest from investors.”

Basically, demand for computers, TVs and other products were sluggish. Plus, there was too much display manufacturing capacity. So product prices fell and many suppliers were swimming in red ink. Driven by higher-margin OLEDs, the smartphone display market was slightly better.

The result? “From a demand standpoint, Covid-19 led to strong demand from the IT market. The education market saw very robust demand. Students and teachers needed more home computers, and schools accelerated their IT investments. Workers made home PCs a priority. There are also millions of workers that went from jobs not requiring a PC to jobs requiring a home PC,” he said.

Demand for PCs, TVs and other products fueled renewed growth for displays. In total, the flat-panel display market reached $118 billion in 2020, up 6% over 2019, according to DSCC. That’s above the previous 2% growth forecast.

The numbers include LCDs, OLEDs and other displays. Of those figures, the LCD market reached $84 billion, while OLEDs were $33 billion in 2020, according to DSCC.

Then, the market is projected to hit a record $152 billion in 2021, up 29% over 2020, according to the firm. Of those figures, the LCD market is expected to reach $113 billion, while OLEDs are $39 billion, they said.

Average selling prices are up, but the market is still beset with component shortages. “Panel prices have risen significantly, particularly since August of last year. They’ve more than doubled in some cases,” Young said. “Adding to the pricing pressure have been components shortages in driver ICs, touch controllers, glass substrates compensation film, polarizers and other materials. We do expect prices to peak in Q3 (of 2021) as a result of shortages easing and the impact of double booking, leaving some potential air pockets in demand. We expect panel pricing to fall in the fourth quarter, but we’re not expecting sharp downturns, as in the past, due to slower supply growth.”

Going forward, the market may come back down to earth. “After 29% growth in 2021, the FPD market is expected to fall by 5% in 2022, as shortage concerns ease, supply growth outpaces demand growth, and prices fall. We expect the IT markets to decline. TV revenues will fall significantly on lower prices, but still slower price declines than in previous downturns,” he said.

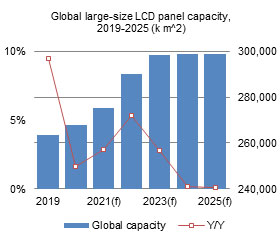

Large-area TFT LCD panel shipments decreased by 10% Month on Month (MoM) and 5% Year on Year (YoY) in April, to 74.1million units, representing historically low shipment performance since May 2020. Omdia defines large-area TFT LCD displays as larger than 9 inches.

"With continued ramifications from the pandemic, demand for IT panels for monitors and notebook PCs remained strong in 4Q21. But as the market became saturated starting in 2022, IT panel shipments started slowing in 1Q22 and early 2Q22," said Robin Wu, Principal Analyst for Large Area Display & Production, Omdia.

Wu said that notebook panel shipments decreased 21% MoM in April, to 18.2 million units, or a 33% decrease from a peak of 27.3 million units in November 2021.

While TV panel prices have decreased noticeably since 3Q21, TV LCD panel shipments increased to a peak of 23.4 million in December 2021, driven by low prices. But rising inflation, the Ukraine crisis and continued lockdowns in China have slowed demand. As a result, TV panel shipments posted a 9% MoM decline in April, to 21.7million units.

Many TV panel prices have fallen below manufacturing cost, and panel makers began to lose money in their TV panel business starting in 4Q21. But Chinese panel makers, the biggest capacity owners, still haven"t reduced their fab utilization. With no sign of demand recovery in 2Q22 or even 3Q22, the supply/demand situation is unlikely to see improvement, Wu said.

"IT LCD panels could still deliver positive cash flow for panel makers. But with prices dropping dramatically, panel makers will soon start to lose money in their IT panel business," Wu said. "Maybe only then will panel makers reduce their glass input and the overall supply/demand situation will return to balance."

As display panels get bigger, thinner and more expensive, manufacturers look to the semiconductor industry for guidance on how to get particle contamination under control

In the electronics industry where the never-ending goal is usually to shrink the size of products and technology, display manufacturing is an anomaly. It is one of the few sectors struggling to meet the demand for bigger technology, bigger tools, and bigger production facilities. In a world where smaller equals better, display manufacturers are often pushing the envelope in the opposite direction.

As consumer demand for giant screen TVs, advanced gaming devices, and huge computer monitors grows, the display industry rushes to advance its technology and fabs to accommodate the need. New glass technology and world-class processes are constantly moving forward to address the continual development of larger, thinner, lighter, sharper and more cost-efficient displays.

In the beginning, consumers were happy with boxy 30-inch TVs and would tolerate a few blank spots on an otherwise working screen, but today expectations are much higher. Liquid crystal displays (LCDs), which offer several advantages over traditional cathode-ray tube (CRT) displays, are becoming the norm for today’s TV and computer screens. Since 2000, glass substrate size has approximately doubled every 1.5 years. It took ten years for the display industry to migrate from Generation One glass sizes to Generation Four, but it took only four years to get from Generation Four to Generation Seven glass sizes. Generation Five and larger size substrates are expected to account for nearly 80 percent of all glass substrates produced by 2007.

This fast migration to larger-generation glass is driven both by product applications, such as bigger, flatter TVs and desktop monitors, and by economies of scale. Large generation glass offers dramatic manufacturing efficiencies, allowing display makers to produce more panels at lower costs with less waste. While a typical Generation Four sheet yields four 17-inch panels, a Generation Five sheet increases that yield threefold, to twelve 17-inch panels. A Generation Six substrate can produce eight larger panels of 32 inches, and a Generation Seven substrate can produce twelve 32-inch panels.

The industrywide migration by LCD manufacturers to large-generation substrates is expected to reduce prices to consumers, further driving the adoption of LCD technology in the desktop monitor and television market segments. LCD desktop monitors accounted for more than 50 percent of all monitors sold in 2004 and are projected to account for nearly 80 percent in 2007, which is twice the penetration rate of 2003. In 2004, LCD TVs represented only 5 percent of the color television market, but new screen sizes, falling prices and expanding availability are expected to drive market penetration to approximately 20 percent by 2007.

Contamination control, for example, is becoming more critical, and the need for standards to manage the production process is increasing, just as it did for the semi industry several years ago. As a result, display manufacturers often look to the semi industry for guidance, says Mark Merrill, vice president of Photon Dynamics, a San Jose, California-based yield management company that offers test, repair and inspection tools throughout array, cell and module fabs for the display-panel manufacturing industry (see Fig. 1). “The display manufacturing process is a lot like the semiconductor manufacturing process, it’s just simpler and bigger.”

Figure 1. Photon Dynamics offers a full suite of yield management solutions for the FPD industry, including test, repair and inspection of LCDs. Photo courtesy of Photon Dynamics, Inc.Click here to enlarge image

As in the semi industry, where one particulate can destroy an entire chip, in large-display manufacturing one unfortunately placed particle can ruin an entire large, flat screen, which is a much more costly yield loss than the smaller panels of previous generations.

If the manufacturer is making smaller displays, a single panel of glass might be cut into 16 individual panels, whereas if it’s making larger displays, it may only be cut into four panels. “Imagine 100 particles falling on that piece of glass, and five of them cause pixel damage,” Merrill says. “That might kill five of the 16 smaller panels, but it could kill all of the four larger panels. That has a huge impact on yield.”

Managing yields through process control is an essential component of optimizing costs and time-to-market throughout the electronics industry. In the flat-panel display sector, the industry’s migration toward high-volume production of larger display panels is driving the need to maximize manufacturing yields. “They are bigger panels, but they have the same defect density,” Merrill points out, which means the environment can support fewer particles just to achieve the same yields.

A 90 percent yield may sound impressive for some industries, but in display manufacturing, where one panel costs close to $1000, a yield loss of 2 percent can cost a company several million dollars. Because of the high cost of materials used in the manufacture of LCDs, defective LCDs, especially larger displays, can be quite costly and ultimately drive up both panel and end-product costs. “That’s the reason why, in this industry, you test 100 percent of the product,” Merrill says. “We don’t just sample. We need to know that every single panel is going to work.”

Figure 2. Pictured here is the latest-generation ArraySaver system from Photon Dynamics, Inc. used in the manufacture of LCDs. Photo courtesy of Photon Dynamics, Inc.Click here to enlarge image

Manufacturing high performance LCDs for TV applications further increases process complexities, especially when dealing with color filters on array, viewing angle technologies, and photo spacers on color filters that are applied to the glass during processing.

Adding to the challenge of controlling particulate contamination is the fact that the fabs, the tools and the glass keep getting bigger. Every new generation of fab increases in size to accommodate the equipment needed to manage the product. Fabs today span several football fields in size, and the glass panels may be two to three meters across. Because of its size and weight, the glass is transported on ever bigger conveyers, which require larger open air spaces and broader chamber doors to move the glass in and out of the work space. The fab itself continues to expand, requiring more floor and air space, making environmental control processes more complex.

Once a fab is up and running, the display manufacturing process begins with the production of the glass, explains Peter Bocko, division vice president of commercial technology for Corning Display Technologies, maker of pristine flat glass used in LCDs for computer and electronics companies. These glass substrates are the foundation for active matrix LCDs.

When the molten glass achieves the right viscosity and temperature, it is fed into an arrowhead-shaped trough called an Isopipe. The glass flows evenly over both sides of the trough, meeting at the pointed bottom where it forms into a continuous sheet of viscous glass that is 0.7 to 0.5 millimeter in thickness. These thinner glass panels dramatically reduce the overall weight of the end product, but create a more delicate surface with which to work.

Because the glass sheet is formed in air, its surface is pristine and flat; no subsequent grinding or polishing, which could damage the glass, is required. The fusion process also maintains tight control over the thickness of the glass, leading to a consistent product. This is critical in the production of panels for LCD televisions, where viewing angle technology sensitizes the image to thickness differences in the glass.

How much degradation occurs depends on how the glass is handled and how clean the environment is in which it is processed. Every step in the process creates potential contaminants. When the glass is etched, broken and polished, particulate material is generated; the tools used to process the glass create dust and metal particles; cleaning chemicals and water used during beveling can leave residues; and transportation exposes the glass to potential damage from contaminants and movement. “There are two things that are especially bad for an LCD surface-water and particulates,” Bocko says.

“We monitor particulates to one micron,” Bocko says. “And if any particulate larger than three to five microns remains on the glass after it is washed, the glass can be rejected.” The size limit of three to five microns is critical because this is the thickness of the LCD layer that’s sandwiched between the layers of glass.

LCD displays utilize two sheets of polarizing material with a liquid crystal solution between them. An electric current passed through the liquid causes the crystals to align so that light cannot pass through them. Each crystal, therefore, is like a shutter, either allowing light to pass through or blocking the light. They are flat, and use only a fraction of the power required by CRTs. Thus, a particle thicker than the liquid center will create a cell gap in the final product, knocking out pixels and leaving dark spots on the screen.

If a panel is approved, the finished glass is then packed for delivery to the customer (see Fig. 5). Packaging and transporting large-generation substrates present another set of challenges.

Figure 5. If a panel is approved, the finished glass is then packed for delivery to the customer, presenting another set of challenges. Photo courtesy of Corning Display Technologies.Click here to enlarge image

In the conventional system, glass panels are packed in slotted crates to prevent them from touching as a result of vibration during transport. The air gap needed between each substrate in a slotted crate limits the number of substrates per case to twenty.

Corning recently switched to a new technique that protects the glass and allows for greater numbers of panels to be shipped in a smaller amount of space. Called the “DensePak” system, it allows for the safe transport, storage and staging of up to 500 sheets per case, in the same footprint as a 20-substrate case.

In the DensePak, another layer of polymer film is adhered to each panel, so they can be packed side-by-side in a vertical glass brick. “The polymer surface is enough to protect the glass, and it’s more efficient because it doesn’t require huge shipping boxes full of air,” Bocko says.

The glass is then reinspected and prepped for LCD applications. At this stage in the process, the two layers of glass are sandwiched together with a thin layer of LCD material between them.

Particulates continue to be an increasing risk as the display-manufacturing industry strives to master thinner LCD layers in an effort to create clearer, sharper pictures. “With thinner technology, even smaller particulates will cause problems,” Merrill says. “A half-micron particle in the right spot could take out a whole panel.”

Because the challenges of managing particulates in such a large environment are so great, and the impact on yield so significant, reliable, repeatable methods of analyzing production-line data and repairing process-related defects are essential for the production of larger, higher-quality LCDs at affordable price points. This means testing the glass at key steps in the manufacturing process to ensure that particulates have been removed before panels are permanently affixed with LCD material.

When the pixels are in place on a display prior to its completion, they can be powered up using an LCD sensor that determines whether they will turn on. If the test reveals a dark pixel due to a microscopic particle, it can often be vaporized or knocked out with a laser to fix the problem, Merrill says.

If particulate is inside, however, once the LCD material is sandwiched between the glass, it can’t be repaired. “At that point, the best you can do is try to determine the source of the contamination so you can fix it before it does more damage,” he says.

Fortunately, there are only four or five steps in the display-manufacturing process, making it easier to find the contamination culprit. The industry doesn’t always analyze the make-up of any given particulate, instead manufacturers look back over the life of the panel to identify the problem. It may be caused by failure in a process tool, human error, or a cleaning problem. “Finding the source requires a lot of excursion control,” Merrill says.

He’s found that the best way to monitor actual particles in the fab is to use a witness panel, which is a glass substrate with a metalized layer, left at workbench level in a working fab for up to 10 days. Hegde moves the witness panel around the fab, scanning the particles accumulated in each area. “Even with HEPA filters there are going to be a lot of particles in the environment,” he admits. “But if they get outrageous, we analyze them and try to eliminate the problem.”

The display industry is still easily a decade behind semconductor in its ability to control contaminants, and it continues to be an issue. As the display industry moves toward the future, fabs will get bigger and processors will struggle to bring yields under control. Consumers will continue to demand bigger and higher-quality screens, and their tolerance for any faults is already minimal, notes Bob Pinnel, chief technology officer for the U.S. Display Consortium in San Jose, Calif. “In the first laptops, six faulty pixels were considered acceptable,” he says. “Now it’s zero in almost all high-quality display products.”

While the equipment manufacturers would like to see standards developed for manufacturing technology, display manufacturers are typically so large and self-contained that this has, thus far, been a tough sell. “For larger groups, it’s cost effective to create their own in-house handling systems,” Merrill says. Even though standards would ultimately bring the costs of equipment down, the companies would have to change the way they do things internally to meet the standards, which is unlikely to happen unless external forces in the industry demand it. “It’s a Catch 22, but eventually standards will come.”

LCD prices are on a relentless downward trend. Lower prices are key to stimulating more demand and further growing the total market in terms of units as well as shifting demand to larger panel sizes. In order to maintain margins as prices fall, LCD producers constantly strive to lower costs. This trend is being exacerbated by the current weak economic environment and significant oversupply, causing prices to fall near cost levels, ever intensifying the focus on cost reduction.

Accounting for 15%-25% of total module costs, backlight unit and inverters are the single most expensive components of an LCD. For this reason, it is not surprising that the backlight assembly is an important focal point of cost reduction. In the backlit unit (BLU), CCFL lamps are the most expensive components, accounting for 30%-40% of the bill of materials — and in the case of LED-based BLUs, the lamps are substantially more expensive.

Increasing LCD panel transmissivity has now become an industrywide goal — not for the purpose of increasing on screen brightness, but rather to maintain brightness and reduce backlight lamps, inverters, and optical films in order to lower panel costs. Another benefit of improved transmissivity is power reduction. Not only is lower power consumption “green,” but in conventional LCDs the large majority of illumination generated by the backlight lamps is lost from polarizer absorption, shading by the TFT array aperture ratio, color filter, etc. so that only about 5% of the light emitted makes it to the front of the screen.

Even small improvements in transmissivity can lead to large gains in BLU lamp reduction. For example, a typical 400-nit panel with 5% transmissivity has 8000-nits luminance at the backlight. If transmissivity is increased from 5% to 10%, the same amount of front of panel luminance can be achieved with a 4000-nit backlight. In other words, the number of backlight lamps and inverters can be reduced by 50%.

There are a variety of technologies in production or in development by different panel manufacturers that target transmissivity improvements. Some of the most important include:

Adoption of low resistance gate and data lines provides multiple benefits that include reduced RC delay that improves performance and can potentially eliminate requirements for dual scan driving. In addition, due to lower resistivity, the width of the bus line can be reduced, which increases aperture ratio without sacrificing performance. Since copper has a very low resistance, it is the material of choice. Already LG Display is mass-producing the majority of its larger panels using Cu, and over the next five years Cu and Cu-alloy application is expected to grow substantially.

In PSA, a polymer alignment layer is formed over a conventionally coated polyimide by mixing a UV curable monomer into the LC. The monomer is then activated by UV radiation while applying an AC voltage. The monomer reacts with the polymer layer to form a surface that fixes the pre-tilt angle of the LC. Because it eliminates a protrusion from the color filter side of the display, aperture ratio is increased and panel brightness can be improved by more than 20%; contrast ratio and LC switching speed are also improved. At the same time, costs are reduced because the protrusion mask step can be eliminated from the color filter process.

PSA technology was originally developed by Fujitsu, and now AUO is bringing it to mass production, showing stunning examples of its technology (called “AMVA-III”) at this year’s FPD International. PSA offers multiple benefits, with minimum trade-offs. Several panel makers are expected to start mass production of PSA for both small/medium and large size LCDs over the next year.

In the color filter process, panel manufacturers are reducing the width of the black matrix (BM). Similar to reducing the width of gate and data lines, a thinner BM translates to a wider aperture ratio.

COA is another CF related manufacturing technology that moves RGB pixels from the common electrode glass to the array glass. There are multiple variations of this technology, but all increase transmissivity by widening the aperture ratio as well as improve contrast. However, moving color pixels to the array creates multiple process challenges, specifically yield loss. For this reason, COA is not yet widely adopted. TMDisplay and Samsung are currently the two main producers of COA based LCDs.

Lowering LCD costs are essential to maintain margins, and in the current environment, just to stay in business. Panel makers are applying a holistic strategy to cost reduction, which includes implementing new manufacturing technologies. Of these, improving panel transmission in order to lower backlight costs has emerged as a key trend. What technologies will be adopted will vary by panel maker, but those that both reduce cost and at the same time improve performance with minimal trade-offs will see the highest adoption rates. Particularly, LCDs adopting low-resistance bus lines, thinner BM, and PSA are already available in stores, and expect more in the near future.

LCDs find application in a wide range of devices such as smartphones, notebooks, televisions, curved TVs, tablets, digital signage and offer various other benefits with regard to performance and lightweight properties. These displays have higher resolution and more portable than traditional televisions and monitors ; they can produce high-quality digital images.

Prior to the Covid-19 pandemic outbreak in early 2020, the flat-panel display (FPD) market was gloomy. Oversupply, falling prices and losses were the common themes in the market.

It’s been a different story during the outbreak. In 2020, the FPD market rebounded. In the stay-at-home economy, consumers went on a buying spree for monitors, PCs, tablets and TVs. As a result, demand for displays exploded. And shortages soon surfaced for display driver ICs and other components.

2021 is expected to be another boom year, but the party may be over in 2022. The global flat panel display market is expected to jump 28% in 2021 to reach a record high of $ 151 billion. A performance drawn more by old LCD screens (liquid crystal display) than Oled screens.

In 2019 State-backed Chinese manufacturer BOE Technology Group has outstripped South Korea’s LG Display as the top maker of flat-panel displays this year, marking China’s growing dominance in the field. In 2021, another Chinese, CSOT, will climb to second place according to DSCC, and in 2024, a third Chinese, HKC, will climb to the third step of the podium.

Increasing use of flat panel display in healthcare industry is creating opportunities for manufacturers as the demand for high-pixel density display for diagnostic in healthcare is increasing. The demand is increasing for new surgical platforms that consists of ultra-high level of brightness to avoid glare and reflection in high light environment so there are opportunities for manufacturers to develop these platforms.

– Screen coating to protect the screen against scratches, touch, reflection, … this coating is applied to the substrate in liquid form and then cured in large oven. One problem with preferred coating compositions is that the temperature can not be tolerated by the glass substrate of the screen panel. For example one protective coating composition cures at about 800°C and the maximum temperature the glass substrate can withstand is about 550°C before it brings thermal damage. To compensate, the protective coating is “cured” in an oven set at a temperature lower than specified but for an extremely long period of time.

With the evolutionary changes in consumer electronics from past few years, the demand for the electronic parts is increasing rapidly. LCD display modules are electronically modulated optical device or flat-panel display and use the light-modulating properties of liquid crystals.

LCD display modules display arbitrary image or fixed images and low content information. The information can be displayed or kept hidden including digits, preset words, and seven-segment displays, as in a digital clock.

Increasing production of electronic devices such as aircraft cockpit displays, computer monitors, LCD televisions, indoor and outdoor signage and instrument panels is responsible for the increasing demand for the LCD display module. Manufacturers of the LCD display modules are focusing on developing innovative products to attract more customers to increase the revenue generation by sales of displays.

Manufacturers of the LCD display modules are coming up with the product innovations such as background display colors, character sizes, number of rows, and others and these features are fueling the increasing integration of the LCD display modules.

Constant advancements in the LCD display modules and improvement in the functionality of displays is the primary factor driving the growth of the LCD display module market.

The manufacturers are also focusing on the delivering a LCD display modules are per the end user requirements as these displays are primarily used for the consumer electronic devices which are produced in bulk quantity.

The increasing production of small electronic devices such as cameras, watches, calculators, clocks, mobile telephones, DVD players, clocks, and other devices is creating a huge demand from manufacturers of these products for the LCD display modules as per their product requirements.

On the other hand, availability of LCD display modules at low prices due to the entry of new players from developing countries, shortage of electronic components is a significant challenge for the established players in this market.

The global vendors for LCD Display Module include RAYSTAR OPTRONICS, INC., WINSTAR Display Co., Ltd., Newhaven Display International, Inc., Sharp Microelectronics, 4D Systems, ELECTRONIC ASSEMBLY GmbH, Kyocera International, Inc., Displaytech, and others. LCD display manufacturers are coming up with the new features and more advanced functionalities of the displays for sustaining in the global competition.

In February 2018, Displaytech, LCD display module manufacturer released DT070CTFT, a 7 inch 800 x 480 TFT display. The company is offering LCD displays with a resistive touch as well as a capacitive touch panel.

The global market for LCD Display Module is divided on the basis of regions into North America, Latin America, Western Europe, Eastern Europe, the Asia Pacific Excluding Japan, Japan, China, and Middle East & Africa. Among these regions, the countries such as Taiwan, South Korea, and China holds major market share in terms of revenue generation from the sale of LCD display module because of the higher presence of manufacturers for these displays as well as the dense presence of the consumer electronics manufacturers.

North America, Western Europe is the second largest market for the LCD display module due to increasing demand from consumer electronics manufacturers. MEA region is expected to grow at moderate CAGR.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey