lcd panel demand factory

Prior to the Covid-19 pandemic outbreak in early 2020, the flat-panel display (FPD) market was gloomy. Oversupply, falling prices and losses were the common themes in the market.

It’s been a different story during the outbreak. In 2020, the FPD market rebounded. In the stay-at-home economy, consumers went on a buying spree for monitors, PCs, tablets and TVs. As a result, demand for displays exploded. And shortages soon surfaced for display driver ICs and other components.

Cars, industrial equipment, PCs, smartphones and other products all incorporate flat-panel displays in one form or another. The majority of TV screens are based on liquid-crystal displays (LCDs). TVs use other display types, such as organic light-emitting diodes (OLEDs) and quantum dots.

Smartphone displays are based on LCDs and OLEDs. Other display technologies, such as microLEDs and miniLEDs, are in the works. Flat-panel displays are made in giant fabs. Suppliers from China, Korea and Taiwan dominate the display market.

It’s been a roller coaster ride in the arena. “Before Covid, the FPD market in the second half of 2019 was not very pretty,” said Ross Young, CEO of Display Supply Chain Consultants (DSCC), in a presentation at Display Week 2021. “We had declining revenues, declining prices, declining margins, companies announcing their exit in the LCD market, CapEx was falling, and there was little interest from investors.”

Basically, demand for computers, TVs and other products were sluggish. Plus, there was too much display manufacturing capacity. So product prices fell and many suppliers were swimming in red ink. Driven by higher-margin OLEDs, the smartphone display market was slightly better.

The result? “From a demand standpoint, Covid-19 led to strong demand from the IT market. The education market saw very robust demand. Students and teachers needed more home computers, and schools accelerated their IT investments. Workers made home PCs a priority. There are also millions of workers that went from jobs not requiring a PC to jobs requiring a home PC,” he said.

Demand for PCs, TVs and other products fueled renewed growth for displays. In total, the flat-panel display market reached $118 billion in 2020, up 6% over 2019, according to DSCC. That’s above the previous 2% growth forecast.

The numbers include LCDs, OLEDs and other displays. Of those figures, the LCD market reached $84 billion, while OLEDs were $33 billion in 2020, according to DSCC.

Then, the market is projected to hit a record $152 billion in 2021, up 29% over 2020, according to the firm. Of those figures, the LCD market is expected to reach $113 billion, while OLEDs are $39 billion, they said.

Average selling prices are up, but the market is still beset with component shortages. “Panel prices have risen significantly, particularly since August of last year. They’ve more than doubled in some cases,” Young said. “Adding to the pricing pressure have been components shortages in driver ICs, touch controllers, glass substrates compensation film, polarizers and other materials. We do expect prices to peak in Q3 (of 2021) as a result of shortages easing and the impact of double booking, leaving some potential air pockets in demand. We expect panel pricing to fall in the fourth quarter, but we’re not expecting sharp downturns, as in the past, due to slower supply growth.”

Going forward, the market may come back down to earth. “After 29% growth in 2021, the FPD market is expected to fall by 5% in 2022, as shortage concerns ease, supply growth outpaces demand growth, and prices fall. We expect the IT markets to decline. TV revenues will fall significantly on lower prices, but still slower price declines than in previous downturns,” he said.

[Introduction]: This paper analyzes the competitive pattern of the panel display industry from both supply and demand sides. On the supply side, the optimization of the industry competition pattern by accelerating the withdrawal of Samsung’s production capacity is deeply discussed. Demand-side focuses on tracking global sales data and industry inventory changes.

Since April 2020, the display device sector rose 4.81%, ranking 11th in the electronic subsectors, 3.39 percentage points behind the SW electronic sector, 0.65 percentage points ahead of the Shanghai and Shenzhen 300 Index. Of the top two domestic panel display companies, TCL Technology is up 11.35 percent in April and BOE is up 4.85 percent.

Specific to the panel display plate, we still do the analysis from both ends of supply and demand: supply-side: February operating rate is insufficient, especially panel display module segment grain rate is not good, limited capacity to boost the panel display price. Since March, effective progress has been made in the prevention and control of the epidemic in China. Except for some production lines in Wuhan that have been delayed, other domestic panels show that the production lines have returned to normal. In South Korea, Samsung announced recently that it would accelerate its withdrawal from all LCD production lines. This round of output withdrawal exceeded market expectations both in terms of pace and amplitude. We will make a detailed analysis of it in Chapter 2.

Demand-side: We believe that people spend more time at home under the epidemic situation, and TV, as an important facility for family entertainment, has strong demand resilience. In our preliminary report, we have interpreted the pick-up trend of domestic TV market demand in February, which also showed a good performance in March. At present, the online market in China maintains a year-on-year growth of about 30% every week, while the offline market is still weak, but its proportion has been greatly reduced. At present, people are more concerned about the impact of the epidemic overseas. According to the research of Cinda Electronics Industry Chain, in the first week, after Italy was closed down, local TV sales dropped by about 45% from the previous week. In addition, Media Markt, Europe’s largest offline consumer electronics chain, also closed in mid-March, which will affect terminal sales to some extent, and panel display prices will continue to be under pressure in April and May. However, we believe that as the epidemic is brought under control, overseas market demand is expected to return to the pace of China’s recovery.

From a price perspective, the panel shows that prices have risen every month through March since the bottom of December 19 reversed. However, according to AVC’s price bulletin of TV panel display in early April, the price of TV panel display in April will decrease slightly, and the price of 32 “, 39.5 “, 43 “, 50 “and 55” panels will all decrease by 1 USD.65 “panel shows price down $2; The 75 “panel shows the price down by $3.The specific reasons have been described above, along with the domestic panel display production line stalling rate recovery, supply-side capacity release; The epidemic spread rapidly in Europe and the United States, sports events were postponed, local blockades were gradually rolled out, and the demand side declined to a certain extent.

Looking ahead to Q2, we think prices will remain under pressure in May, but prices are expected to pick up in June as Samsung’s capacity is being taken out and the outbreak is under control overseas. At the same time, from the perspective of channel inventory, the current all-channel inventory, including the inventory of all panel display factories, has fallen to a historical low. The industry as a whole has more flexibility to cope with market uncertainties. At the same time, low inventory is also the next epidemic warming panel show price foreshadowing.

In terms of valuation level, due to the low concentration and fierce competition in the panel display industry in the past ten years, the performance of sector companies is cyclical to a certain extent. Therefore, PE, PB, and other methods should be comprehensively adopted for valuation. On the other hand, the domestic panel shows that the leading companies in the past years have sustained large-scale capital investment, high depreciation, and a long period of poor profitability, leading to the inflated TTM PE in the first half of 2014 to 2017. Therefore, we will display the valuation level of the sector mainly through the PB-band analysis panel in this paper.

In 2017, due to the combined impact of panel display price rise and OLED production, the valuation of the plate continued to expand, with the highest PB reaching 2.8 times. Then, with the price falling, the panel shows that PB bottomed out at the end of January 2019 at only 1.11 times. From the end of 2019 to February, the panel shows that rising prices have driven PB all the way up, the peak PB reached 2.23 times. Since entering March, affected by the epidemic, in the short term panel prices under pressure, the valuation of the plate once again fell back to 1.62 times. In April, the epidemic situation in the epidemic country was gradually under control, and the valuation of the sector rebounded to 1.68 times.

We believe the sector is still at the bottom of the stage as Samsung accelerates its exit from LCD capacity and industry inventories remain low. Therefore, once the overseas epidemic is under control and the domestic demand picks up, the panel shows that prices will rise sharply. In addition, the plate will also benefit from Ultra HD drive in the long term. Panel display plate medium – and long-term growth logic is still clear. Coupled with the optimization of the competitive pattern, industry volatility will be greatly weakened. The current plate PB compared to the historical high has sufficient space, optimistic about the plate leading company’s investment value.

Revenue at Innolux and AU Optronics has been sluggish for several months and improved in March. Since the third quarter of 2017, Innolux’s monthly revenue growth has been negative, while AU Optronics has only experienced revenue growth in a very few months.AU Optronics recorded a record low revenue in January and increased in February and March. Innolux’s revenue returned to growth in March after falling to its lowest in recent years in February. However, because the panel display manufacturers in Taiwan have not put in new production capacity for many years, the production process of the existing production line is relatively backward, and the competitiveness is not strong.

On March 31, Samsung Display China officially sent a notice to customers, deciding to terminate the supply of all LCD products by the end of 2020.LGD had earlier announced that it would close its local LCDTV panel display production by the end of this year. In the following, we will analyze the impact of the accelerated introduction of the Korean factory on the supply pattern of the panel display industry from the perspective of the supply side.

The early market on the panel display plate is controversial, mainly worried about the exit of Korean manufacturers, such as LCD display panel price rise, or will slow down the pace of capacity exit as in 17 years. And we believe that this round of LCD panel prices and 2017 prices are essentially different, the LCD production capacity of South Korean manufacturers exit is an established strategy, will not be transferred because of price warming. Investigating the reasons, we believe that there are mainly the following three factors driving:

(1) Under the localization, scale effect, and aggregation effect, the Chinese panel leader has lower cost and stronger profitability than the Japanese and Korean manufacturers. In terms of cost structure, according to IHS data, material cost accounts for 70% of the cost displayed by the LCD panel, while depreciation accounts for 17%, so the material cost has a significant impact on it. At present, the upstream LCD, polarizer, PCB, mold, and key target material line of the mainland panel display manufacturers are fully imported into the domestic, effectively reducing the material cost. In addition, at the beginning of the factory, manufacturers not only consider the upstream glass and polarizer factory but also consider the synergy between the downstream complete machine factory, so as to reduce the labor cost, transportation cost, etc., forming a certain industrial clustering effect. The growing volume of shipments also makes the economies of scale increasingly obvious. In the long run, the profit gap between the South Korean plant and the mainland plant will become even wider.

(2) The 7 and 8 generation production lines of the Korean plant cannot adapt to the increasing demand for TV in average size. Traditionally, the 8 generation line can only cut the 32 “, 46 “, and 60” panel displays. In order to cut the other size panel displays economically and effectively, the panel display factory has made small adjustments to the 8 generation line size, so there are the 8.5, 8.6, 8.6+, and 8.7 generation lines. But from the cutting scheme, 55 inches and above the size of the panel display only part of the generation can support, and the production efficiency is low, hindering the development of large size TV. Driven by the strong demand for large-size TV, the panel display generation line is also constantly breaking through. In 2018, BOE put into operation the world’s first 10.5 generation line, the Hefei B9 plant, with a designed capacity of 120K/ month. The birth of the 10.5 generation line is epoch-making. It solves the cutting problem of large-size panel displays and lays the foundation for the outbreak of large-size TV. From the cutting method, one 10.5 generation line panel display can effectively cut 18 43 inches, 8 65 inches, 6 75 inches panel display, and can be more efficient in hybrid mode cutting, with half of the panel display 65 inches, the other half of the panel display 75 inches, the yield is also guaranteed. Currently, there are a total of five 10.5 generation lines in the world, including two for domestic panel display companies BOE and Huaxing Optoelectronics. Sharp has a 10.5 generation line in Guangzhou, which is mainly used to produce its own TV. Korean manufacturers do not have the 10.5 generation line. In the context of the increasing size of the TV, Korean manufacturers are obviously at a disadvantage in competitiveness.

(3) As the large-size OLED panel display technology has become increasingly mature, Samsung and LGD hope to transfer production to large-size OLED with better profit prospects as soon as possible. Apart from the price factor, the reason why South Korean manufacturers are exiting LCD production is more because the large-size OLED panel display technology is becoming mature, and Samsung and LGD hope to switch to large-size OLED production as soon as possible, which has better profit prospects. At present, there are three major large-scale OLED solutions including WOLED, QD OLED, and printed OLED, while there is only WOLED with a mass production line at present.

According to statistics, shipments of OLED TVs totaled 2.8 million in 2018 and increased to 3.5 million in 2019, up 25 percent year on year. But it accounted for only 1.58% of global shipments. The capacity gap has greatly limited the volume of OLED TV.LG alone consumes about 47% of the world’s OLED TV panel display capacity, thanks to its own capacity. Other manufacturers can only purchase at a high price. According to the industry chain survey, the current price of a 65-inch OLED panel is around $800-900, while the price of the same size LCD panel is currently only $171.There is a significant price difference between the two.

Samsung and LGD began to shut down LCD production lines in Q3 last year, leading to the recovery of the panel display sector. Entering 2020, the two major South Korean plants have announced further capacity withdrawal planning. In the following section, we will focus on its capacity exit plan and compare it with the original plan. It can be seen that the pace and magnitude of Samsung’s exit this round is much higher than the market expectation:

(1) LGD: LGD currently has three large LCD production lines of P7, P8, and P9 in China, with a designed capacity of 230K, 240K, and 90K respectively. At the CES exhibition at the beginning of this year, the company announced that IT would shut down all TV panel display production capacity in South Korea in 2020, mainly P7 and P8 lines, while P9 is not included in the exit plan because IT supplies IT panel display for Apple.

(2) Samsung: At present, Samsung has L8-1, L8-2, and L7-2 large-size LCD production lines in South Korea, with designed production capacities of 200K, 150K, and 160K respectively. At the same time in Suzhou has a 70K capacity of 8 generation line.

Global shipments of TV panel displays totaled 281 million in 2019, down 1.06 percent year on year, according to Insight. In fact, TV panel display shipments have been stable since 2015 at between 250 and 300 million units. At the same time, from the perspective of the structure of sales volume, the period from 2005 to 2010 was the period when the size of China’s TV market grew substantially. Third-world sales also leveled off in 2014. We believe that the sales volume of the TV market has stabilized and there is no big fluctuation. The impact of the epidemic on the overall demand may be more optimistic than the market expectation.

In contrast to the change in volume, we believe that the core driver of the growth in TV panel display demand is actually the increase in TV size. According to the data statistics of Group Intelligence Consulting, the average size of TV panel display in 2014 was 0.47 square meters, equivalent to the size of 41 inches screen. In 2019, the average TV panel size is 0.58 square meters, which is about the size of a 46-inch screen. From 2014 to 2019, the average CAGR of TV panel display size is 4.18%. Meanwhile, the shipment of TV in 2019 also increased compared with that in 2014. Therefore, from 2014 to 2019, the compound growth rate of the total area demand for TV panel displays is 6.37%.

It is assumed that 4K screen and 8K screen will accelerate the penetration and gradually become mainstream products in the next 2-3 years. The pace of screen size increase will accelerate. We have learned through industry chain research that the average size growth rate of TV will increase to 6-8% in 2020. Driven by the growth of the average size, the demand area of global TV panel displays is expected to grow even if TV sales decline, and the upward trend of industry demand remains unchanged.

Meanwhile, the global LCDTV panel display demand will increase significantly in 2021, driven by the recovery of terminal demand and the continued growth of the average TV size. In 2021, the whole year panel display will be in a short supply situation, the mainland panel shows that both males will enjoy the price elasticity.

This paper analyzes the competition pattern of the panel display industry from both supply and demand sides. On the supply side, the optimization of the industry competition pattern by accelerating the withdrawal of Samsung’s production capacity is deeply discussed. Demand-side focuses on tracking global sales data and industry inventory changes. Overall, we believe that the current epidemic has a certain impact on demand, and the panel shows that prices may be under short-term pressure in April or May. But as Samsung’s exit from LCD capacity accelerates, industry inventories remain low. So once the overseas epidemic is contained and domestic demand picks up, the panel suggests prices will surge. We are firmly optimistic about the A-share panel display plate investment value, maintain the industry “optimistic” rating. Suggested attention: BOE A, TCL Technology.

The key factors that drive the market of a display factory are mother glass size, product size, panels per sheet, process yield, and operating efficiency. For example, to manufacture 820 million smartphone displays per year of 6-in diagonal size in Gen 6 fabs, approximately 380,000 (or 380K) MG sheets per month will be required to be processed at 85% yield and 85% operating efficiency. As an additional example, to manufacture 35 million TV displays per year of 55-in diagonal size in Gen 8.5 fabs, approximately 640,000 (640K) MG sheets per month will be required to be processed at 90% yield and 85% operating efficiency

Also, surging demand for smart consumer electronics, the emerging number of manufacturing facilities, and the low cost of labor in counties such as India, Pakistan, Bangladesh, etc., are some of the factors that are supporting the market growth of the display panel in the countries. Moreover, due to the low cost of manufacturing in the countries, numerous companies announced the establishment of their new OLED and LCD panel manufacturing plants.

Furthermore, the rising adoption of display devices in various industries, especially in countries such as China, India, and South Korea, is a key factor supporting the market growth. Moreover, due to the COVID-19 pandemic, the demand for smartphones and laptops has increased because of work-from-home norms. Also, financial and education institutions are adopting digital teaching methods. These factors are contributing to the increased demand for small- and large-scale displays for commercial and business purposes.

are AU Optronics Corporation, BOE Japan Co. Ltd, Innolux Corporation, LG Display Co. Ltd, Samsung Electronics Co. Ltd, Panasonic Corporation, Sharp Corporation, Hisense Co. Ltd, Toshiba Corporation, Sony Corporation, etc., are some of the prominent players operating in the display panel market. Several M&As along with partnerships have been undertaken by these players to facilitate customers with innovative products.

Based on the type of display, the market is fragmented into LCD, OLED, and Others (AMOLED, MicroLED, etc) The OLED segment grabbed major market share in 2020 and dominated the market. The advantage of OLED displays such as s being light in weight and their flexibility, have enabled them to gain a competitive advantage over other segments. The OLED technology is recognized as a lighter and thinner alternative than conventional LED and LCD systems. In addition, OLED panels do not require any type of backlighting compared to LCD. Stable performance in sunlight is an additional advantage of OLEDs.

Based on the resolution, the market is fragmented into 8K, 4K, HD, and Others. The 8K segment grabbed the major market share and dominated the market. 8k TVs have 4 times as many pixels as their 4k counterparts and a shocking 16 times as many pixels as a 1080p TV. These extra pixels should make a significant difference in picture quality. Moreover, the player is launching products with 8K resolution, n August 2019, Sharp Corporation launched the Sharp 8M-B80AX1U 80″ Class 8K Ultra HD LCD. This display offers ultimate high definition, conforming to the 8K Ultra HD standards and pixel resolution 16 times greater than Full HD and four times greater than 4K.

For a better understanding of the market adoption of the display panel market, the market is analyzed based on its worldwide presence in the countries such as North America (the United States and Canada), Europe (Germany, France, Italy, Spain, United Kingdom, and Rest of Europe), Asia-Pacific (China, Japan, India, Australia, and Rest of APAC), and Rest of World. Asia Pacific region grabbed XX% market for the display panel Market industry and generated revenue of USD XX Million in 2020. However, the North America region would witness the highest CAGR during the forthcoming years

The display panel market can further be customized as per the requirement or any other market segment. Besides this, UMI understands that you may have your own business needs, hence feel free to connect with us to get a report that completely suits your requirements.

According to the latest report by IMARC Group, titled "TFT LCD Panel Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2021-2026,"the global TFT LCD panel marketreached a value of US$ 150.2 Billion in 2020. Looking forward, IMARC Group expects the market to reach a value of US$ 196.7 Billion by 2026. A thin-film-transistor liquid-crystal display (TFT LCD) panel is a liquid crystal display that is generally attached to a thin film transistor. It is an energy-efficient product variant that offers a superior quality viewing experience without straining the eye. Additionally, it is lightweight, less prone to reflection and provides a wider viewing angle and sharp images. Consequently, it is generally utilized in the manufacturing of numerous electronic and handheld devices. Some of the commonly available TFT LCD panels in the market include twisted nematic, in-plane switching, advanced fringe field switching, patterned vertical alignment and an advanced super view.

The global market is primarily driven by continual technological advancements in the display technology. This is supported by the introduction of plasma enhanced chemical vapor deposition (PECVD) technology to manufacture TFT panels that offers uniform thickness and cracking resistance to the product. Along with this, the widespread adoption of the TFT LCD panels in the production of automobiles dashboards that provide high resolution and reliability to the driver is gaining prominence across the globe. Furthermore, the increasing demand for compact-sized display panels and 4K television variants are contributing to the market growth. Moreover, the rising penetration of electronic devices, such as smartphones, tablets and laptops among the masses, is creating a positive outlook for the market. Other factors, including inflating disposable incomes of the masses, changing lifestyle patterns, and increasing investments in research and development (R&D) activities, are further projected to drive the market growth.

Key Market Segmentation:On the basis of the size, the market has been bifurcated into large size TFT-LCD display panel and medium and small size TFT-LCD display panel. The large size TFT-LCD display panel presently represents the leading market segment.

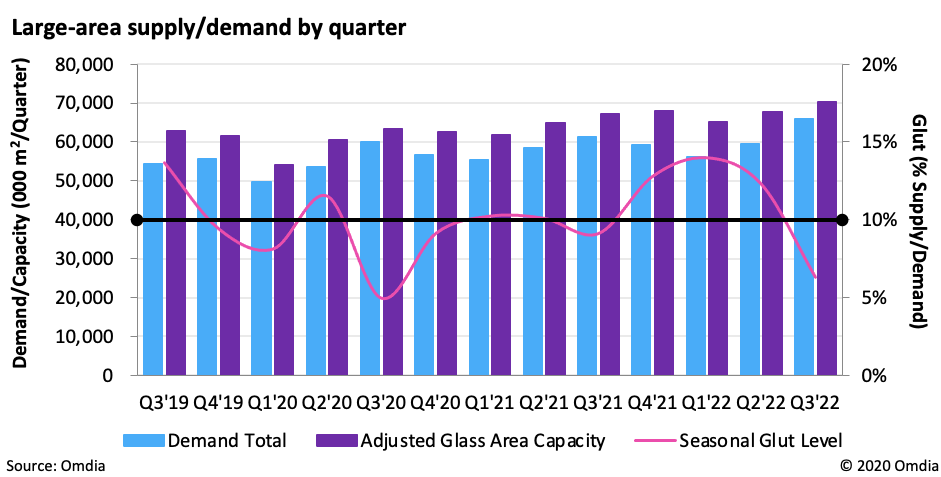

Large-area TFT LCD panel shipments decreased by 10% Month on Month (MoM) and 5% Year on Year (YoY) in April, to 74.1million units, representing historically low shipment performance since May 2020. Omdia defines large-area TFT LCD displays as larger than 9 inches.

"With continued ramifications from the pandemic, demand for IT panels for monitors and notebook PCs remained strong in 4Q21. But as the market became saturated starting in 2022, IT panel shipments started slowing in 1Q22 and early 2Q22," said Robin Wu, Principal Analyst for Large Area Display & Production, Omdia.

Wu said that notebook panel shipments decreased 21% MoM in April, to 18.2 million units, or a 33% decrease from a peak of 27.3 million units in November 2021.

While TV panel prices have decreased noticeably since 3Q21, TV LCD panel shipments increased to a peak of 23.4 million in December 2021, driven by low prices. But rising inflation, the Ukraine crisis and continued lockdowns in China have slowed demand. As a result, TV panel shipments posted a 9% MoM decline in April, to 21.7million units.

Many TV panel prices have fallen below manufacturing cost, and panel makers began to lose money in their TV panel business starting in 4Q21. But Chinese panel makers, the biggest capacity owners, still haven"t reduced their fab utilization. With no sign of demand recovery in 2Q22 or even 3Q22, the supply/demand situation is unlikely to see improvement, Wu said.

"IT LCD panels could still deliver positive cash flow for panel makers. But with prices dropping dramatically, panel makers will soon start to lose money in their IT panel business," Wu said. "Maybe only then will panel makers reduce their glass input and the overall supply/demand situation will return to balance."

A string of new LCD factories being built, combined with slow demand for notebook and desktop PC screens, caused LCD prices to fall during the first three months of the year, and the downward trend is expected to continue, vendors and analysts said.

Falling prices for LCD (liquid crystal display) screens should help ensure that users find bargains for new monitors, laptops and LCD TVs this year, since the screen is among the most-expensive components in those products. The price declines are also causing vendors to improve picture quality to catch users" eyes and draw them away from competitors.

Makers such as LG.Philips and Samsung Electronics, the world"s two largest LCD producers, are ramping up production at state-of-the-art factories, while rivals continue to add lines at existing plants. Other big players, such as AU Optronics in Taiwan, expect to add plants later this year, which should help keep LCD prices tame.

"The biggest impact from the new plants will be in the first part of this year, but there will be some impact throughout the year," said Frank Lee, an LCD industry analyst for Deutsche Securities Asia in Taipei.

The new LCD plants were built largely to keep pace with demand for LCD TVs, which have been among the hottest-selling items this year. Cutthroat competition among LCD makers also has been a boon to users, ensuring steadily falling prices for the past few years, as screen sizes increase.

For example, prices for 42-inch LCD screens that will be delivered to TV makers in the second half of April fell by $35 each since the end of March, to an average of $890, according to WitsView Technology Co., an industry researcher. Prices for 19-inch panels for PC monitors fell $5 to an average $160.

Average selling prices for LCD panels at AU Optronics fell nearly 12% quarter-on-quarter by the end of March, and the company forecast continued declines into the second quarter, according to executives at its first quarter earnings conference Thursday.

The company expects the price of screens used in desktops and laptops to drop by about 10% quarter-on-quarter during the April to June period, while LCD-TV screen prices will decline by a smaller percentage, in the mid single digits, it said.

LG.Philips said its sales declined in the first quarter compared to the fourth, because of a decline in the average selling prices in LCDs destined for laptops and desktop monitors, with an overall price decline of around 10% for all LCD screen products.

The company is increasing production at a state-of-the-art LCD factory in Korea, as is rival Samsung. AU is building a similar plant in Taiwan that it expects to be in production by the third quarter of this year. LG said it would produce mainly 42-inch and 47-inch screens at the plant, aimed at the LCD-TV market.

Other LCD industry competitors are also increasing production to keep up with demand for LCD-TVS. On Wednesday, S-LCD Corp., the LCD-panel manufacturing joint venture of Sony and Samsung, said it plans to invest $238 million to expand production at its factory in Tangjeong, South Korea.

LCDs find application in a wide range of devices such as smartphones, notebooks, televisions, curved TVs, tablets, digital signage and offer various other benefits with regard to performance and lightweight properties. These displays have higher resolution and more portable than traditional televisions and monitors ; they can produce high-quality digital images.

Prior to the Covid-19 pandemic outbreak in early 2020, the flat-panel display (FPD) market was gloomy. Oversupply, falling prices and losses were the common themes in the market.

It’s been a different story during the outbreak. In 2020, the FPD market rebounded. In the stay-at-home economy, consumers went on a buying spree for monitors, PCs, tablets and TVs. As a result, demand for displays exploded. And shortages soon surfaced for display driver ICs and other components.

2021 is expected to be another boom year, but the party may be over in 2022. The global flat panel display market is expected to jump 28% in 2021 to reach a record high of $ 151 billion. A performance drawn more by old LCD screens (liquid crystal display) than Oled screens.

In 2019 State-backed Chinese manufacturer BOE Technology Group has outstripped South Korea’s LG Display as the top maker of flat-panel displays this year, marking China’s growing dominance in the field. In 2021, another Chinese, CSOT, will climb to second place according to DSCC, and in 2024, a third Chinese, HKC, will climb to the third step of the podium.

Increasing use of flat panel display in healthcare industry is creating opportunities for manufacturers as the demand for high-pixel density display for diagnostic in healthcare is increasing. The demand is increasing for new surgical platforms that consists of ultra-high level of brightness to avoid glare and reflection in high light environment so there are opportunities for manufacturers to develop these platforms.

– Screen coating to protect the screen against scratches, touch, reflection, … this coating is applied to the substrate in liquid form and then cured in large oven. One problem with preferred coating compositions is that the temperature can not be tolerated by the glass substrate of the screen panel. For example one protective coating composition cures at about 800°C and the maximum temperature the glass substrate can withstand is about 550°C before it brings thermal damage. To compensate, the protective coating is “cured” in an oven set at a temperature lower than specified but for an extremely long period of time.

The global display panel market size is expected to reach USD 163.88 Billion in 2030 and register a revenue CAGR of 10.3% over the forecast period, according to latest report by Reports and Data. A growing consumer base for smart appliances and rise in consumer demand for quality display panels are driving revenue growth of the display panel market.

The global display panel market is being driven by a number of factors, such as consumer demand for large LCD televisions, increase in smartphone screen size, and development of vehicle display. Moreover, introduction of ultra-thin LCD televisions, high-resolution & slim smartphone designs, and improved user interface & touch screens for car display are driving demand for display panels.

The new trend of foldable display panels has become popular in tablets, smartphones, and notebooks, and they are made from flexible substrates, such as plastic, metal, or flexible glass, which allow them to bend. Plastic and metal panels are light, thin, and sturdy, and are nearly shatterproof. Flexible display technology, which is based on OLED panels, is used to make foldable phones, and there is mass production of flexible OLED display panels for smartphones, televisions, and smartwatches by companies, such as Samsung and LG, to meet customer demand.

Display panels are witnessing surge in demand due to rising trend of downsizing the parts required to produce an LED screen. LED screens have not only become ultra-thin but have also grown in size due to miniaturization of internal parts, which allow them to be placed on any surface, inside or out. Applications of LED have grown in recent years due to technological developments, such as improved resolution, increased brightness, product diversity, and introduction of small and hardened surface LEDs. LED displays have also found applications in digital signage, such as advertising and digital billboards, which help businesses to stand out.

In July 2021, The TCL Group announced a finalized plan to set up their handset and television display panel manufacturing unit in Andhra Pradesh, India. It would be the second-largest unit of handset display assembly in India after Samsung, with a workforce of roughly 1000 people. TCL’s 280,000-square-meter factory in Tirupati is the company’s largest out-of-home market investment to date.

LCD segment accounted for largest revenue share in 2021. New developments in the LCD technology are allowing to make displays three to four times sharper and better. Higher resolution LCDs are being used in Virtual Reality (VR), and LCD-based devices are currently used in a variety of areas, including retail, corporate offices, and banks. High competition from newer technologies, disruption in the supply-demand ratio, and drop in average selling prices of LCD display panels are expected to drive growth of the segment.

Asia-Pacific market is expected to register a rapid revenue growth rate during the forecast period. Factors driving market growth in Asia-Pacific include increasing number of display panel manufacturing plants in the region and rapid adoption of OLED displays. Display panel manufacturing costs are lower in the region due to low labor costs, which is encouraging several companies to establish their new OLED and LCD panel manufacturing facilities in Asia-Pacific. Consumer electronics, retail, BFSI, healthcare, transportation, and sports & entertainment sectors are all expected to play a significant role in display panel market growth in APAC.

For this report, Reports and Data has segmented the global display panel market based on application, panel resolution, panel size, display type, end-use, and region:

The current oversupply of liquid crystal display (LCD) panels is expected to continue through 2023, analyst firm TrendForce said in its latest forecast.

LCD panel prices had increased from June 2020 through the first half of 2021, the firm said, spurned by high demand for consumer electronics from Covid-19.

In supply, while LG Display could halt production at its P7 factory in Paju during the first quarter of next year, CSOT’s start of operation of its Gen 8.6 T9 factory could increase panel supply further than the current state, TrendForce said.

The analyst firm also said that LCD factories that use Gen 5 substrate or above could see their operation rate drop to 60% during the fourth quarter, which will be the lowest in ten years.

Flat panel displays use different backplane technologies. Small and medium OLEDs for mobile phones use a low temperature polysilicon (LTPS) backplane which is created by laser annealing amorphous silicon (a-Si). OLED TVs use a metal oxide backplane. Both backplanes use deposited thin films which must be highly uniform and contamination free to maximize electrical performance. The OLEDs are evaporated or deposited and encapsulated to reduce degradation caused by water vapor and oxygen exposure. Encapsulation uses either strengthened glass or thin films, depending on whether the OLED is rigid or flexible. Dissimilarity of materials within the rigid and flexible stacks make cutting and singulation of individual display devices a challenge. The highly complex nature of this process can induce defects, decreasing throughput and yield.

Samsung’s display-making subsidiary, Samsung Display initially decided to shut down its LCD business by the end of 2020. The company was reportedly forced to reconsider after the demand for LCD panels increased in the post-pandemic (Covid-19) period. In 2021, more reports suggested that the company again decided to stop producing LCD panels, but Samsung didn’t stop making them. However, according to a report by Sammobile, Samsung Display is now finally ready to shut down its LCD production. The report also suggests that Samsung is now buying LCD panels from China.

As per the report, Samsung might be planning to shut down LCD panel production in June as it doesn’t align with Samsung Display’s long-term vision for the business. The company plans to substitute LCD panels with Quantum Dot (QD-OLED) displays as Samsung recently repurposed an obsolete LCD plant to produce OLED panels.

The company is not willing to compete in a market that’s dominated by affordable panels from Chinese and Taiwanese counterparts. The falling prices of LCD are also preventing Samsung from continuing production, the report claims.

Samsung Display’s largest buyer was the consumer electronics arm of the conglomerate, Samsung Electronics. However, the company itself is opting for affordable LCD panels from Chinese and Taiwanese suppliers. Samsung Display is expected to primarily focus on the manufacturing of Quantum Dot and OLED displays after its LCD business shuts down. The employees appointed for the LCD production are also likely to be transferred to the QD division.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey